5G PCB Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

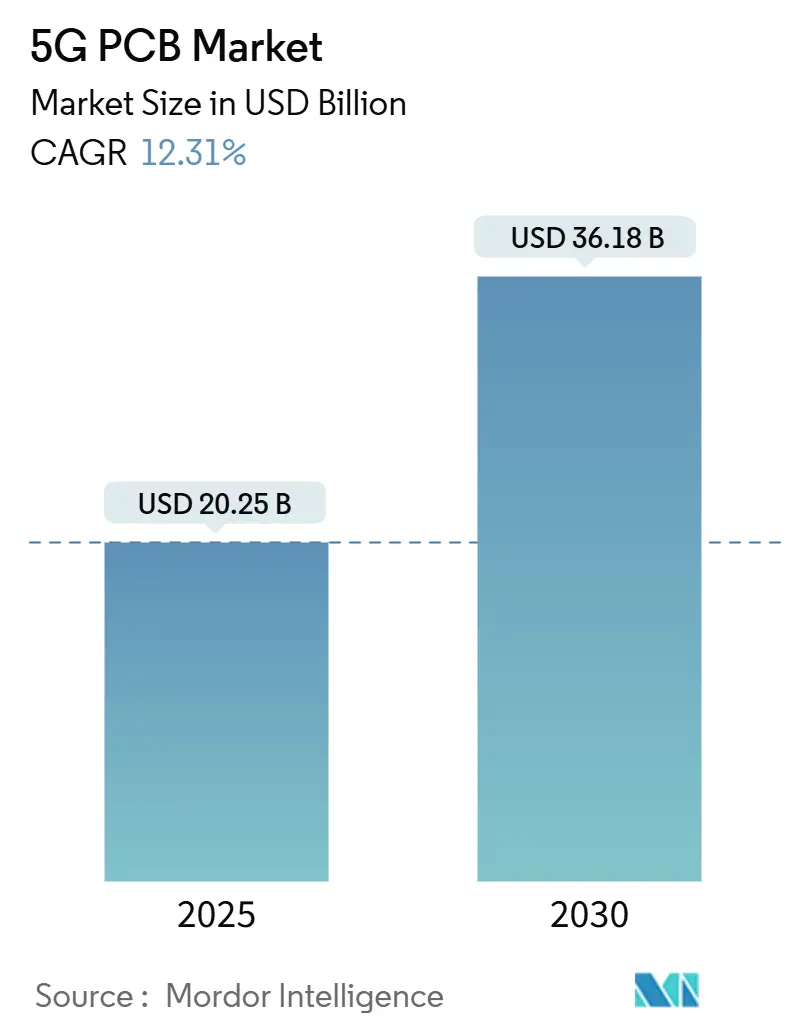

| Market Size (2025) | USD 20.25 Billion |

| Market Size (2030) | USD 36.18 Billion |

| Growth Rate (2025 - 2030) | 12.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G PCB Market Analysis by Mordor Intelligence

The 5G PCB market size stands at USD 20.25 billion in 2025 and is forecast to reach USD 36.18 billion by 2030, expanding at a 12.31% CAGR. Rigorous infrastructure densification, rapid adoption of high-frequency laminates, and the migration of private industrial networks underpin this trajectory. Asia-Pacific retains production primacy by leveraging scale advantages and vertical supply-chain integration, while North America and Europe carve out leadership niches in advanced R&D and high-reliability applications. Product evolution favors RF/Microwave and HDI designs that combine fine-line traces with low-loss substrates to sustain signal integrity above 24 GHz. End-user diversification into automotive V2X, data-center computing, and industrial automation amplifies demand visibility, cushioning the market from pure telecom-cycle volatility. Meanwhile, competitive dynamics shift toward substrate processing prowess and thermal engineering finesse rather than pure cost competition.

Key Report Takeaways

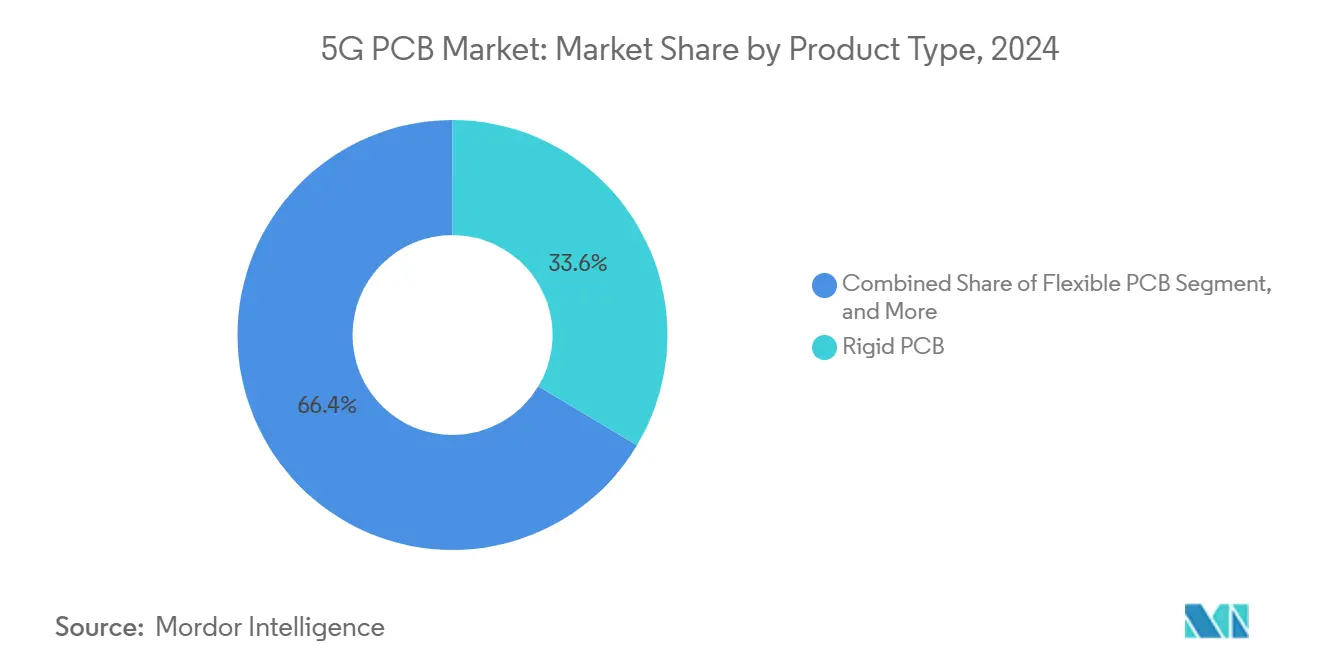

- By product type, rigid boards held 33.58% of the 5G PCB market share in 2024, while RF/Microwave boards are projected to record a 12.54% CAGR through 2030.

- By application, macro/micro base stations contributed 42.37% share of the 5G PCB market size in 2024; IoT and edge devices will expand fastest at a 12.67% CAGR to 2030.

- By frequency band, Sub-6 GHz represented 51.27% of 2024 revenue, yet the mmWave segment is advancing at a 13.96% CAGR through 2030.

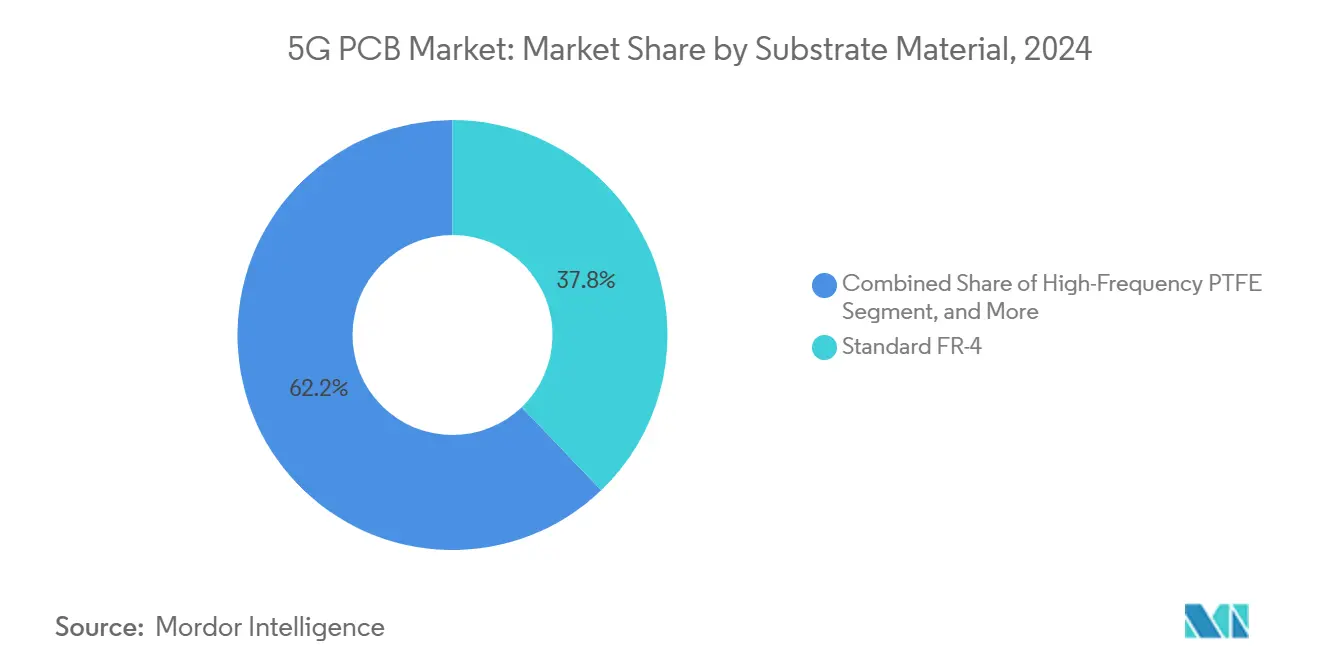

- By substrate material, standard FR-4 retained a 37.83% share in 2024, whereas liquid-crystal polymer (LCP) substrates are growing at a 12.89% CAGR.

- By end-user, telecom infrastructure vendors commanded 45.89% demand in 2024, while industrial manufacturers are set to grow at a 12.76% CAGR.

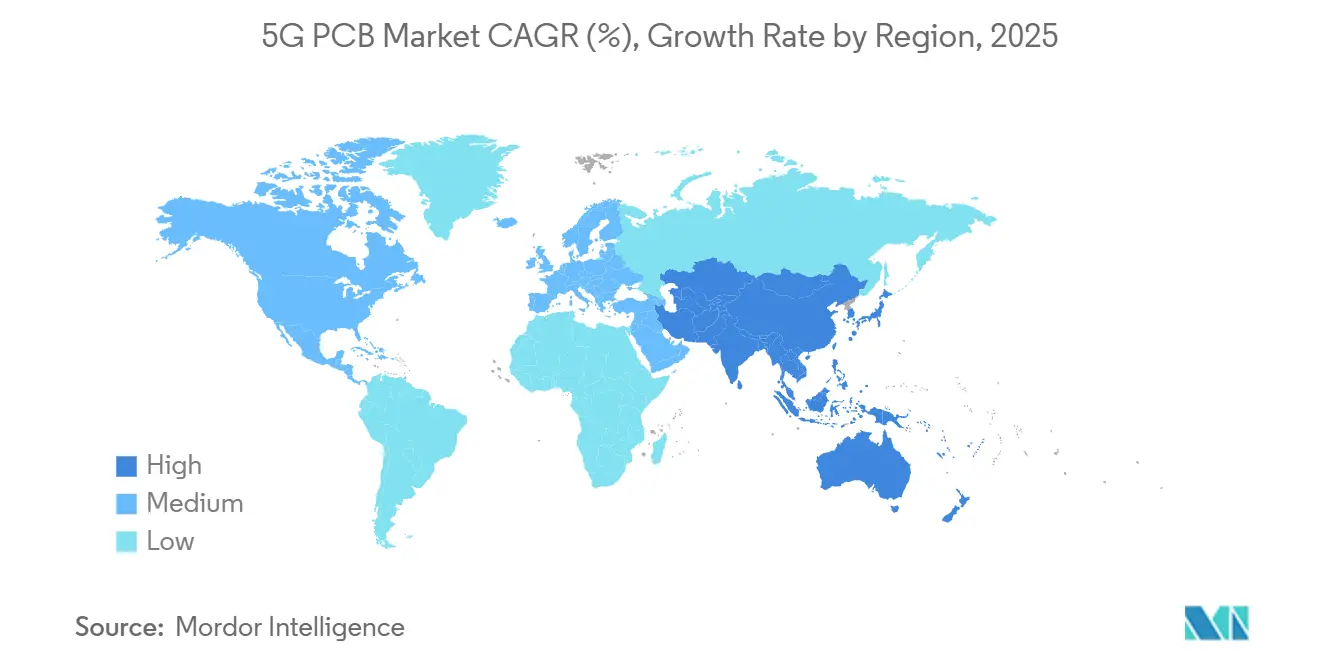

- By geography, Asia-Pacific contributed 63.84% to 2024 revenue and is forecast to expand at a 13.23% CAGR through 2030.

Global 5G PCB Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid densification of 5G mid-band and mmWave base-stations | +2.8% | Global, with Asia-Pacific and North America leading | Medium term (2-4 years) |

| Miniaturization and antenna-in-package design in 5G smartphones | +2.1% | Global, concentrated in consumer electronics hubs | Short term (≤ 2 years) |

| Adoption of high-frequency laminates for signal integrity | +1.9% | North America and EU for R&D, Asia-Pacific for manufacturing | Medium term (2-4 years) |

| Automotive V2X migration to 5G telematics | +1.6% | North America, Europe, China automotive corridors | Long term (≥ 4 years) |

| Private 5G networks for Industry 4.0 driving rugged PCB demand | +1.4% | Industrial regions globally, Germany, China, US | Medium term (2-4 years) |

| 5.5G / 6G R&D investment in advanced substrates | +0.8% | R&D centers in US, EU, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid densification of 5G mid-band and mmWave base stations

Operators continue to deploy compact radios and small cells to close coverage gaps, raising demand for PCBs that blend fine-line geometry with robust thermal paths. Component vendors targeting C-band networks specify insertion-loss budgets that only ceramic-PTFE hybrids can meet, steering procurement away from legacy FR-4. Manufacturers able to guarantee Class 3 reliability win preference because outdoor radios face accelerated thermal cycling. These stringent specifications elevate average selling prices and lock in high-frequency specialists. [1]“Antenna-in-Package Design for 5G Mobile Devices,” IEEE, ieee.org

Miniaturization and antenna-in-package design in 5G smartphones

Phone OEMs integrate antennas directly onto rigid-flex stacks to free space for larger batteries. This shift forces ultra-tight dielectric-constant control across hybrid stack-ups combining LCP and modified polyimide layers. Yield risk climbs because a micron-level lamination void can detune multiband arrays, so suppliers invest heavily in inline X-ray and optical metrology. The trend accelerates the adoption of SiP platforms where the board doubles as an RF module carrier.

Adoption of high-frequency laminates for signal integrity

At mmWave, dielectric loss scales rapidly with frequency, prompting OEMs to qualify PTFE and LCP substrates even for cost-sensitive devices. Rogers RO4000 series boards cost up to 5 × FR-4 yet remain indispensable for 28 GHz radios where each 0.1 dB insertion-loss cut equates to tangible range improvement. [2]Rogers Corporation, “Annual Report 2024,” rogerscorp.com Material supply remains geographically concentrated, creating both pricing leverage for laminate vendors and lead-time risk for PCB fabs.

Automotive V2X migration to 5G telematics

Automakers pursuing Level 3 autonomy favor 5G PCBs qualified to AEC-Q100 and IATF 16949, demanding vibration-resistant microvias and extended temperature survivability. European regulations catalyze early deployments, while Chinese OEMs embrace 5G-enabled over-the-air firmware updates. PCB suppliers with automotive pedigrees, therefore, secure high-margin, multi-year awards. [3]“Mercedes, BMW Advance 5G Telematics Integration,” Automotive News, autonews.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain volatility of copper-clad laminates | -1.8% | Global, particularly affecting Asia-Pacific manufacturing | Short term (≤ 2 years) |

| High cost and lower yields of ultra-high multilayer RF PCBs | -1.2% | Global, concentrated in high-frequency applications | Medium term (2-4 years) |

| Trade restrictions on advanced PCB exports (US-China) | -0.9% | US-China trade corridor, spillover to global supply chains | Medium term (2-4 years) |

| Thermal-management challenges at mmWave frequencies | -0.7% | Global, affecting mmWave-specific applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-chain volatility of copper-clad laminates

Capacity curbs and environmental audits in China pushed laminate prices up 18% in 2024, eroding gross margins across mid-tier fabs. Large players neutralize shocks via multi-sourcing contracts, yet smaller shops often carry under one-month raw-stock cover, exposing them to spot-price spikes. Volatility is most acute in high-frequency products because qualified substitutes remain scarce.

Thermal-management challenges at mmWave frequencies

As radio power amplifiers concentrate watts into thumb-sized footprints, junction temperatures soar. Designers migrate toward metal-core and AlN substrates that dissipate heat ten times faster than FR-4, but these materials raise fabrication complexity, depress yields, and inflate BOM costs. Suppliers capable of laser-drilled vias and embedded copper coins command premiums, while laggards risk design disqualification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RF boards accelerate premium mix.

Rigid boards delivered 33.58% of 2024 revenue, anchoring bread-and-butter macro-cell contracts. RF/Microwave boards, though smaller in volume, outpaced all peers with a 12.54% CAGR, a clear signal that high-frequency functionality commands disproportionate value in the 5G PCB market. The 5G PCB market share of RF/Microwave designs is set to widen as operators transition to mmWave radios requiring multilayer ceramic-PTFE hybrids. HDI technology complements this shift by enabling finer traces and stacked microvias that cut transmission loss.

Yield complexity escalates sharply above 20 layers, prompting fabs to automate optical-impedance monitoring to sustain profitability. Flexible and rigid-flex boards serve foldable phones and wearable healthcare devices, yet remain niche in revenue terms. Shennan Circuits reported RF board ASPs running nearly 4 × those of standard rigid units, illustrating the premium available to technology leaders.

By Application: Infrastructure still leads, but IoT surges

Macro and micro base stations supplied 42.37% of 2024 demand and bind the 5G PCB market size tightly to operator capex cycles. However, industrial IoT and edge nodes will clock a 12.67% CAGR through 2030, a trajectory fueled by smart-factory private networks that prize ultra-reliable low-latency connections. Small-cell deployments bridge both domains, pairing infrastructure-grade RF sections with consumer-priced enclosures.

Automotive telematics emerges as another bright spot as V2X mandates crystallize in China and Europe. Smartphone volume growth is plateauing, yet SKU complexity keeps PCB layer counts rising: flagship devices now integrate more than six antenna arrays within a single rigid-flex stack. Healthcare devices exploit miniaturized 5G transceivers for continuous patient monitoring, expanding the addressable base for designs prioritizing biocompatible laminates.

By Frequency Band: mmWave captures momentum.

Sub-6 GHz still anchors 51.27% of revenue, but its share erodes as mmWave boards advance at 13.96% CAGR. The 5G PCB market size for mmWave assemblies will therefore become the dominant value pool within the decade as dense urban scenarios require multi-band radios capable of 10 Gbps peak rates. Each incremental jump from 28 GHz to 39 GHz slices material options, favoring LCP and ceramics over PTFE. Designers adopt air-cavity structures and margin-free reference-plane spacing to tame insertion loss.

Mid-band (2–6 GHz) offers a balanced trade-off between coverage and capacity, sustaining demand for cost-optimized mixed-glass laminates. Yet even here, operators increasingly order multi-band radios sharing PLLs across sub-6 GHz and mmWave paths, nudging board specifications closer to high-frequency tolerance windows.

By Substrate Material: LCP gains traction

Standard FR-4 maintains a 37.83% share thanks to unbeatable cost metrics, but its dielectric loss beyond 10 GHz restricts deployment scope. LCP’s 12.89% CAGR places it center-stage for high-density antenna-in-package modules where its low DK and moisture absorption shine. PTFE remains essential in macro radios yet faces supply-chain risks due to limited producer count. Ceramic-filled epoxies and metal-core variants serve power-dense amplifiers, with embedded copper coins dissipating heat efficiently.

Environmental compliance reshapes supplier roadmaps; halogen-free formulations now earn preferred-supplier status among European OEMs. JLCPCB’s RoHS-compliant glass-reinforced LCP exemplifies how substrate innovation now intertwines with eco-regulation.

By End-User: The Industrial vertical rises fastest

Telecom OEMs still represent 45.89% of demand, yet industrial facilities piloting private 5G lines contribute the steepest growth at 12.76% CAGR. Automotive OEMs source rugged multilayers for ADAS and infotainment domains, valuing traceability and PPAP documentation on par with RF performance. Consumer-electronics brands keep the volume engine humming, though ASPs face pressure as mid-range handsets adopt mmWave only selectively.

Energy utilities experiment with 5G-enabled smart-grid relays, opening another long-tail vertical that prizes extended temperature ratings and lightning-strike resilience. Healthcare device makers prioritize miniaturization and biocompatibility, spurring demand for ultra-thin LCP flex circuits. This diversifying demand matrix insulates the 5G PCB market from single-vertical cyclicality.

Geography Analysis

Asia-Pacific controlled 63.84% of 2024 revenue and is expected to grow 13.23% CAGR to 2030. China anchors volume, South Korea and Japan contribute material science depth, and Taiwan meshes PCB and advanced packaging capacity. Governments co-sponsor 5G factory deployments, reinforcing domestic pull for high-frequency boards. Yet dependence on a narrow set of copper-clad laminate vendors exposes the region to raw-material shocks.

North America ranks second, propelled by the defense and aerospace appetite for mission-critical communications. TTM Technologies reported USD 3.2 billion 2024 revenue with aerospace and defense accounting for 47%-a proxy for the region’s premium-grade demand. Federal subsidies targeting on-shore substrate production aim to temper over-reliance on Asian supply.

Europe centers on automotive and industrial automation. Regional directives encouraging private-network licenses stimulate OEM–fabricator partnerships. Environmental regulations push fabs toward closed-loop copper recovery and VOC-free lamination, giving EU suppliers an edge in sustainability-weighted RFQs. Middle East and Africa and South America are early-stage, leaning on imported high-frequency boards but showing investment upticks as telecom operators accelerate 5G rollouts.

Competitive Landscape

The 5G PCB market displays moderate concentration. Chinese, Taiwanese, and South Korean manufacturers supply over 70% of global volume, yet North American and European firms command niche positions in ultra-reliable and defense applications. Shennan Circuits integrates substrate fabrication with module assembly, capturing economies across the stack. TTM Technologies focuses on high-mix, low-volume aerospace boards, reporting 22% of 2024 revenue from data-center customers requiring 5G-ready backplanes.

Strategic moves center on capacity scale-ups and M&A. Bain Capital’s 2025 acquisition of Somacis extended European reach in RF boards. DBG Technology’s purchase of All Circuits broadened RF qualification footprints for automotive clients. Collaboration across the value chain deepens: laminate producers co-develop next-gen LCP grades with fab houses, targeting sub-0.002 loss-tangent thresholds.

Emerging disruptors such as inkjet-printed flex startups address sustainability and rapid prototyping but lack the capex to contend in mmWave macro-cell volumes. Compliance with IPC-6018 and automotive PPAPs acts as a moat, as the certification timeline can exceed 18 months, deterring newcomers.

5G PCB Industry Leaders

Avary Holding (Shenzhen) Co., Ltd.

Zhen Ding Technology Holding Limited

Nippon Mektron, Ltd.

Unimicron Technology Corporation

TTM Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TTM Technologies posted USD 805 million Q1 revenue, up 8.2% YoY, citing demand spikes in data-center and defense segments.

- March 2025: Alchip Technologies logged USD 1.62 billion 2024 revenue, up 65.4%, underscoring packaging-substrate pull-through for 5G SoCs.

- February 2025: SMIC shipped 948,000 eight-inch-equivalent wafers in Q4 2024, sustaining demand for advanced substrate interposers.

- January 2025: Bain Capital finalized the Somacis takeover to scale European RF PCB capabilities.

Global 5G PCB Market Report Scope

| Rigid PCB |

| Flexible PCB |

| Rigid-Flex PCB |

| High-Density Interconnect (HDI) PCB |

| RF / Microwave PCB |

| 5G Macro/Micro Base Stations |

| 5G Small Cells and CPE |

| 5G Smartphones and Tablets |

| IoT and Edge Devices |

| Automotive and V2X Modules |

| Industrial and Enterprise Equipment |

| Sub-6 GHz |

| Mid-Band (2–6 GHz) |

| mmWave (>24 GHz) |

| Standard FR-4 |

| High-Frequency PTFE |

| Liquid-Crystal Polymer (LCP) |

| Ceramic and Hybrid |

| Metal-Core |

| Telecom Infrastructure Vendors |

| Consumer Electronics OEMs |

| Automotive OEMs |

| Industrial Manufacturers |

| Other End-User |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Rigid PCB | ||

| Flexible PCB | |||

| Rigid-Flex PCB | |||

| High-Density Interconnect (HDI) PCB | |||

| RF / Microwave PCB | |||

| By Application | 5G Macro/Micro Base Stations | ||

| 5G Small Cells and CPE | |||

| 5G Smartphones and Tablets | |||

| IoT and Edge Devices | |||

| Automotive and V2X Modules | |||

| Industrial and Enterprise Equipment | |||

| By Frequency Band | Sub-6 GHz | ||

| Mid-Band (2–6 GHz) | |||

| mmWave (>24 GHz) | |||

| By Substrate Material | Standard FR-4 | ||

| High-Frequency PTFE | |||

| Liquid-Crystal Polymer (LCP) | |||

| Ceramic and Hybrid | |||

| Metal-Core | |||

| By End-User | Telecom Infrastructure Vendors | ||

| Consumer Electronics OEMs | |||

| Automotive OEMs | |||

| Industrial Manufacturers | |||

| Other End-User | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the 5G PCB market by 2030?

The 5G PCB market is forecast to reach USD 36.18 billion by 2030, implying a 12.31% CAGR through the forecast period.

Which product category is expanding fastest?

RF/Microwave boards are advancing at a 12.54% CAGR thanks to rising mmWave deployments and antenna-in-package adoption.

Why is Asia-Pacific dominant in manufacturing?

The region offers integrated supply chains, large-scale laminate capacity, and proximity to telecom infrastructure rollouts, giving it 63.84% of 2024 revenue.

How are automotive applications influencing demand?

V2X migration toward 5G telematics is driving orders for rugged, AEC-Q100-qualified multilayer boards with extended thermal and vibration resilience.

What materials are replacing standard FR-4 in high-frequency designs?

Liquid-crystal polymer and PTFE substrates are gaining share because their low dielectric loss sustains signal integrity above 24 GHz.

Which end-user vertical shows the highest growth?

Industrial manufacturers deploying private 5G networks are projected to grow at 12.76% CAGR, outpacing telecom infrastructure spending.

Page last updated on: