G.Fast Chipset Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

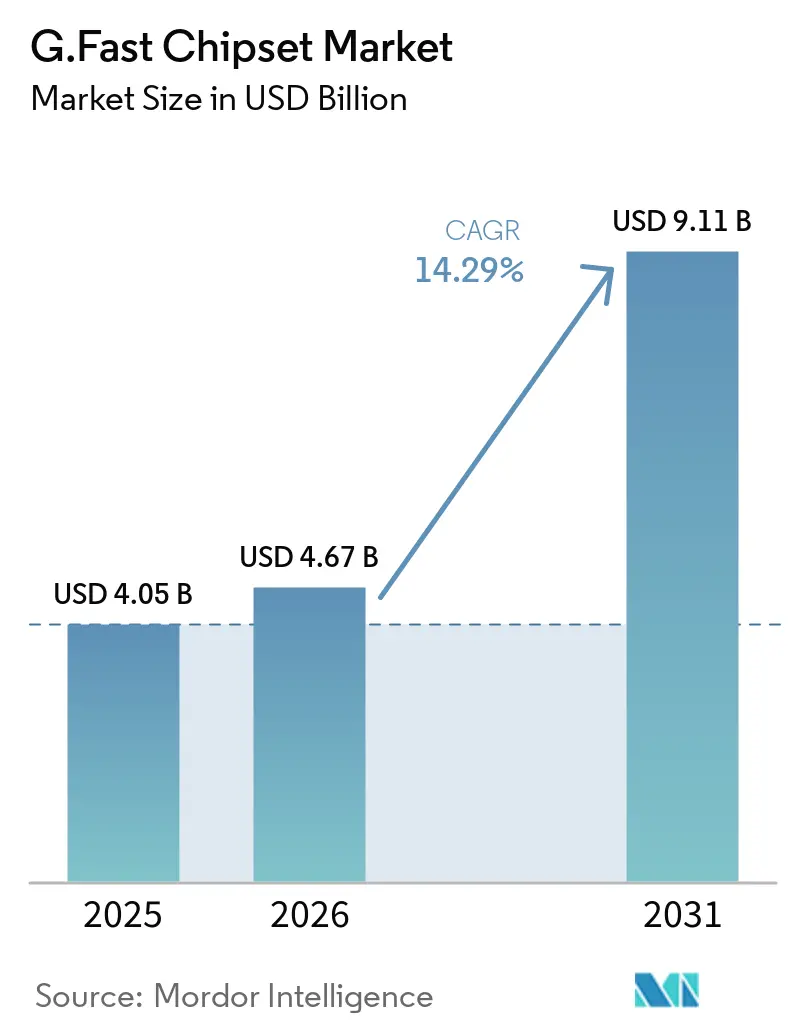

| Market Size (2026) | USD 4.67 Billion |

| Market Size (2031) | USD 9.11 Billion |

| Growth Rate (2026 - 2031) | 14.29% CAGR |

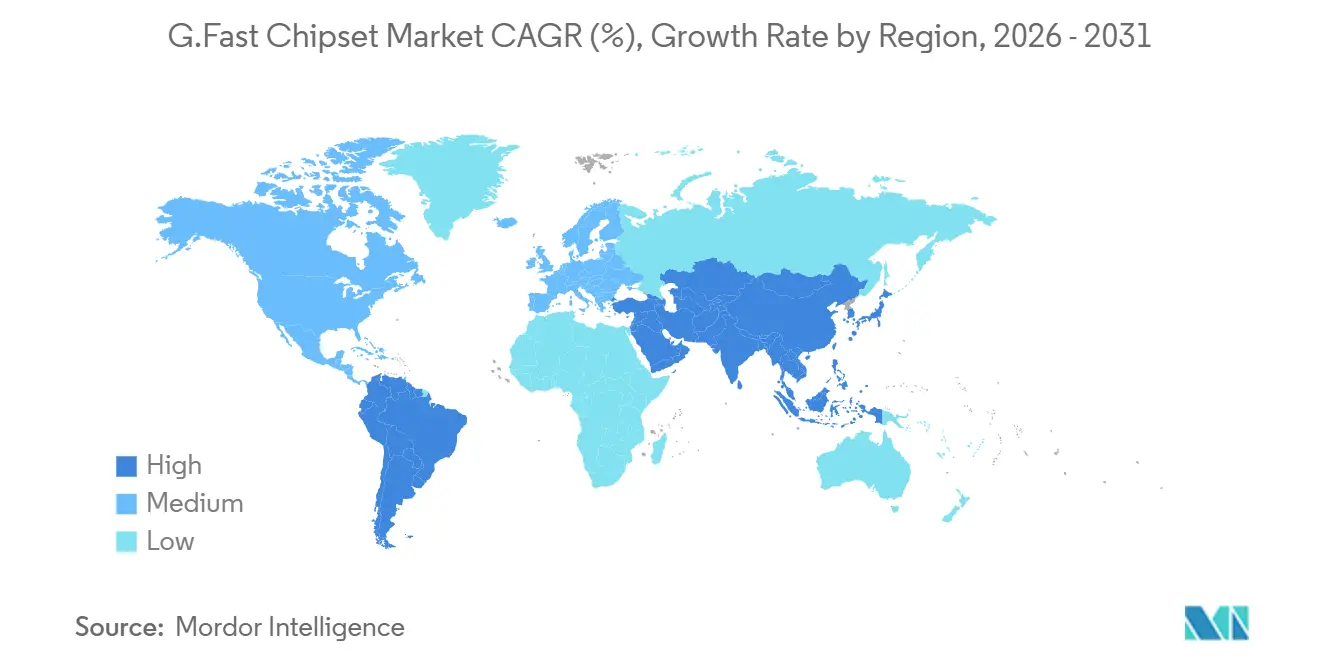

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

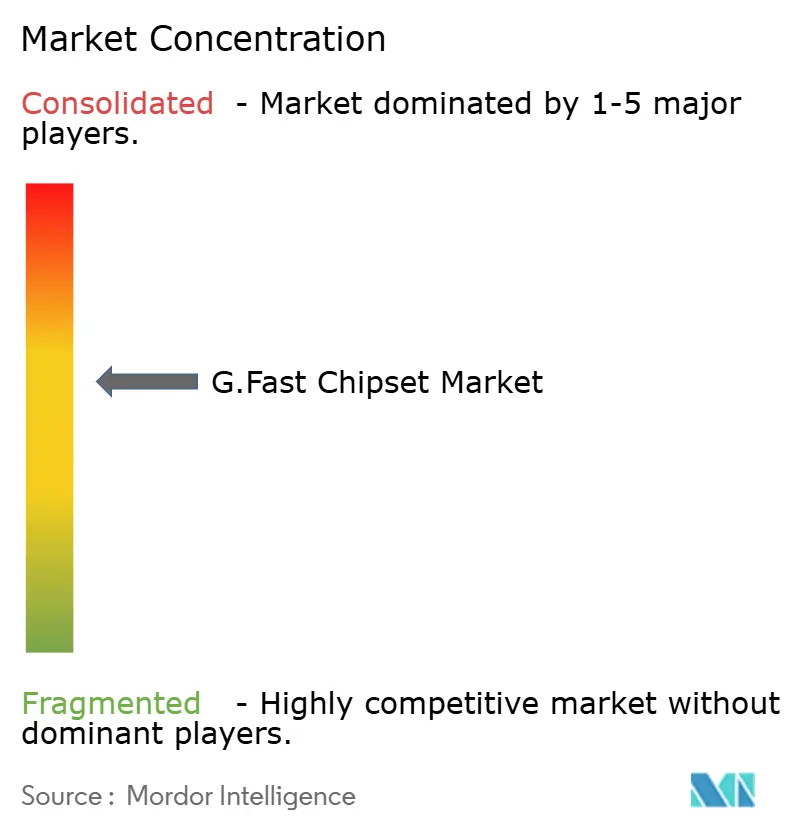

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

G.Fast Chipset Market Analysis by Mordor Intelligence

The G.fast chipset market size is expected to increase from USD 4.05 billion in 2025 to USD 4.67 billion in 2026 and reach USD 9.11 billion by 2031, growing at a CAGR of 14.29% over 2026-2031. Healthy operator appetite for hybrid fiber-copper architectures keeps demand robust, especially where legacy twisted-pair assets can still be monetized. Distribution point units dominate current rollouts because they let carriers avoid re-wiring subscriber premises, while silicon advances such as integrated vectoring engines and reverse-power-feed controllers lower total cost of ownership. The technology also benefits from public broadband subsidies that reward rapid service activation, and from the emergence of higher-frequency 424 MHz G.mgfast profiles that enable symmetrical gigabit performance over short loops. Competitive pressure from fiber-to-the-home and DOCSIS 4.0, however, forces vendors to migrate quickly to 14- to 10-nanometer process nodes to deliver lower-power, highly integrated chipsets with extended feature sets.

Key Report Takeaways

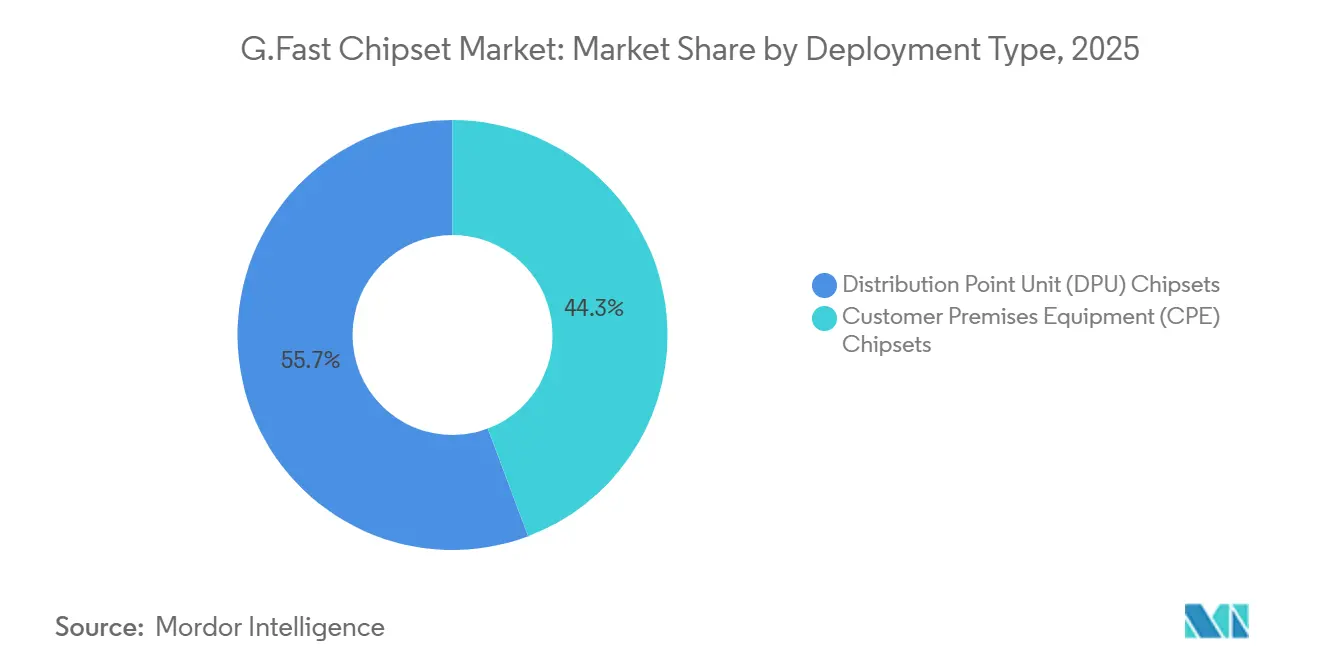

- By deployment type, distribution point unit chipsets led with 55.74% of G.fast chipset market share in 2025, while customer premises equipment chipsets are projected to expand at a 15.11% CAGR to 2031.

- By frequency profile, the 212 MHz variant accounted for 46.29% of 2025 revenue, whereas the 424 MHz G.mgfast profile is forecast to deliver the fastest growth at 14.67% CAGR through 2031.

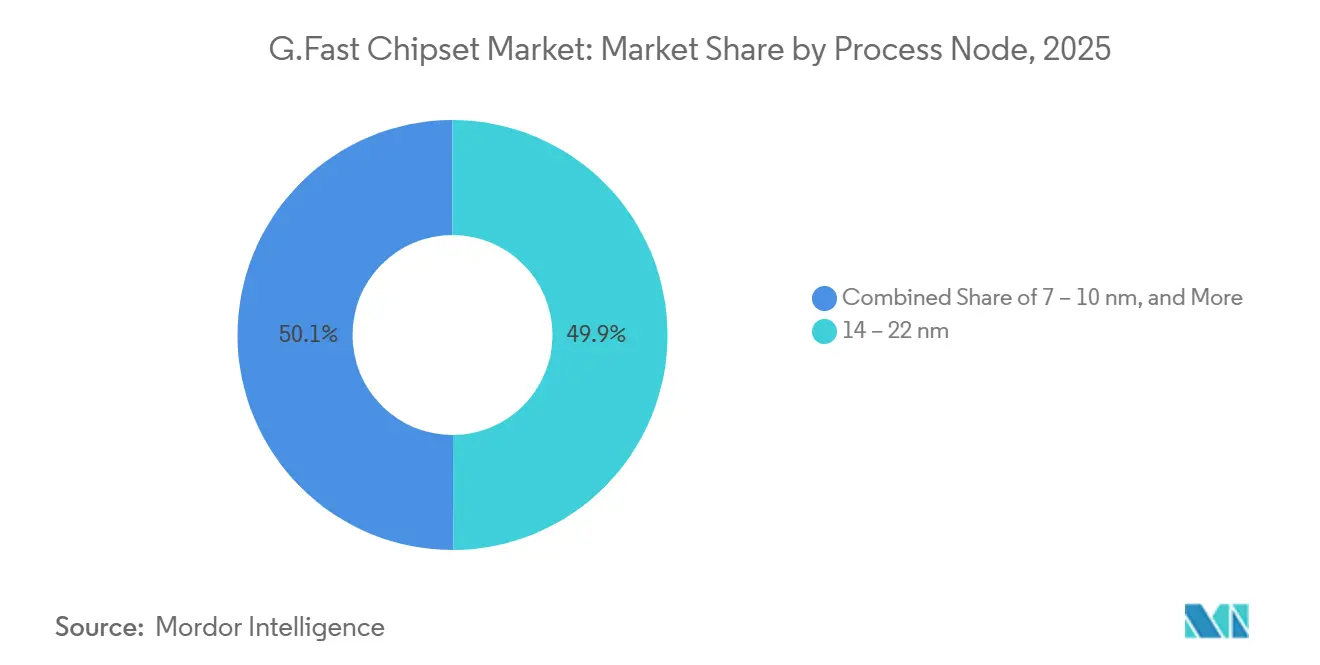

- By process node, 14- to 22-nanometer designs held 49.94% share of the G.fast chipset market size in 2025, and 7- to 10-nanometer devices are expected to post a 14.53% CAGR between 2026-2031.

- By end-use application, multi-dwelling unit broadband commanded 42.63% of 2025 revenue; small-cell and Wi-Fi offload backhaul is anticipated to register a 14.91% CAGR to 2031.

- By geography, Asia-Pacific captured 34.11% of global revenue in 2025, while the Middle East and Africa region is projected to record the fastest regional expansion at 14.78% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of G.Fast Chipset Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Fiber‑to‑the‑Distribution‑Point (FTTdp) Build‑Outs by Tier‑1 Operators | +3.2% | Europe; East Asia | Medium term (2‐4 years) |

| National Gigabit Broadband Subsidy Programs | +2.8% | Europe; East Asia | Medium term (2‐4 years) |

| Silicon‑Level Integration of Vectoring and Single‑Ended Line Testing (SELT) | +2.5% | Global | Long term (≥ 4 years) |

| Cost‑Effective Reverse‑Power‑Feed Designs Enabling Micro‑DPUs | +2.1% | Europe; Asia‑Pacific | Short term (≤ 2 years) |

| Growing Adoption of G.mgfast (424 MHz) Profiles | +2.0% | Asia‑Pacific; Middle East & Africa; Europe | Medium term (2‐4 years) |

| Transition of Former Intel/Lantiq Portfolios to Pure‑Play Access Silicon Suppliers | +1.7% | North America; Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Fiber-to-the-Distribution-Point Build-Outs by Tier-1 Operators

European and East Asian incumbents intensify fiber-to-the-distribution-point (FTTdp) rollouts to deliver gigabit services without entering subscriber homes. Germany budgeted EUR 1.8 billion (USD 1.98 billion) in January 2026 for 536 broadband projects that extend fiber only to street cabinets yet rely on G.fast for the last 100-300 meters.[1]Federal Ministry for Digital and Transport, “Gigabit Funding: New 1.8 Billion EUR Call,” bundesregierung.de The United Kingdom’s Project Gigabit includes voucher grants of up to GBP 4,500 (USD 5,625) per premises, incentivizing operators to deploy micro-distribution point units in rural areas. South Korea, with 89% fiber penetration, treats 100 Mbps as a universal service and channels KRW 625 billion (USD 0.47 billion) into 6G research, but still leverages G.fast in older multi-dwelling units where rewiring costs are prohibitive. Streamlined civil-works rules under the European Union’s Gigabit Infrastructure Act, fully applicable since November 2025, further compress deployment timelines. These policy signals shorten payback periods, making G.fast chipset investments attractive as an interim capacity solution.

National Gigabit Broadband Subsidies in Europe and East Asia

Public funding mechanisms accelerate hybrid fiber-copper projects when full fiber-to-the-home economics are challenging. The European Commission’s Connecting Europe Broadband Fund earmarked EUR 420 million for next-generation access, complementing national programs such as the United Kingdom’s vouchers and Germany’s cumulative EUR 21 billion (USD 23.1 billion) broadband spend since 2015. Japan’s Digital Garden City blueprint targets 99.9% fiber coverage by 2027; nevertheless, legacy copper in rural prefectures sustains demand for G.fast as a bridging technology. These subsidies value speed-to-market, prompting carriers to deploy distribution point units that can be installed in days rather than months.

Silicon Integration of Vectoring and Single-Ended Line Testing

Vendors now embed vectoring engines, echo-cancellation blocks, and single-ended line testing into monolithic system-on-chip designs fabricated on 14- to 10-nanometer nodes. Broadcom’s BCM65550 vector processor pairs with the BCM63158 customer premises equipment SoC to deliver symmetrical gigabit throughput while lowering power by roughly 25% versus previous-generation discrete solutions. Integrated diagnostics enable remote loop qualification, cutting truck rolls and supporting predictive maintenance, which in turn extends copper plant life, especially in Europe where much of the twisted-pair network was upgraded after 2000. These architectural advances reinforce the cost advantage of the G.fast chipset market in scenarios where existing loops exhibit low attenuation.

Cost-Effective Reverse-Power-Feed Designs Enabling Micro-DPUs

Reverse-power-feed allows distribution point units to draw energy from customer premises equipment, eliminating the need for grid connections at curbside cabinets. Third-generation silicon cuts total consumption below 10 watts, enabling installations on utility poles and in building basements that lack mains power. [2]International Telecommunication Union, “Reverse Power Feed Technical Report,” itu.int Faster activation times give operators a revenue edge, particularly in dense Asian cities where securing electrical permits can delay projects. Furthermore, reverse-power-feed supports modular field-swap designs, reducing mean-time-to-repair and improving quality-of-experience metrics tracked under service-level agreements.

Restraints Impact Analysis of G.Fast Chipset Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Overbuild of Fiber‑to‑the‑Home (FTTH) in Dense Metropolitan Areas | −2.5% | North America; Europe; tier‑1 Asia‑Pacific cities | Short term (≤ 2 years) |

| Low Customer‑Premises‑Equipment (CPE) Attach Rates | −1.8% | North America | Medium term (2‐4 years) |

| Shrinking Availability of Broadband‑Qualified Copper Pairs in New Housing Developments | −1.5% | Global | Long term (≥ 4 years) |

| Uncertain Technology Roadmap Beyond 424 MHz in the Context of 10‑Gigabit Passive Optical Networks (10G‑PON) | −1.3% | North America; Europe | Medium term (2‐4 years) |

| Source: Mordor Intelligence | |||

Rapid Over-Build of Fiber-to-the-Home in Dense Metros

North American and European operators are heavily investing in passive optical networks that bypass copper altogether. Verizon pledged USD 20 billion between 2024-2027 to pass an additional 3.4 million premises, and AT&T allocates USD 2 billion annually to reach 30 million fiber locations by end-2025. Similar momentum exists in the United Kingdom, where nationwide gigabit coverage hit 78% in mid-2025. [3]Ofcom, “Project Gigabit Vouchers,” ofcom.org.uk As operators amortize fiber capex across dense subscriber bases, G.fast becomes less competitive, confining chip demand to interim upgrades or specialized backhaul applications. Equipment vendors such as Nokia and Huawei are already shipping 10-gigabit passive optical network systems, raising performance expectations and eroding copper-based value propositions.

Low Customer Premises Equipment Attach Rates in North America

Consumers in the United States and Canada often prefer DOCSIS 3.1 or full-fiber packages bundled with video and mobile services. Cable majors Charter Spectrum and Comcast Xfinity each serve more than 32 million broadband customers, overshadowing G.fast-based offers. MaxLinear disclosed USD 58 million broadband revenue in Q3 2025 and noted that operators increasingly favor passive optical network and DOCSIS gateways over standalone G.fast modems. Without attractive subsidy models, carriers hesitate to underwrite customer premises equipment costs, which keeps attachment rates low and restrains chipset volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

G.Fast Chipset Market Segment Analysis

By Deployment Type:

Distribution Point Units Anchor Capital EfficiencyDistribution point unit silicon captured 55.74% of 2025 revenue, demonstrating the appeal of centralizing active electronics in street cabinets, basements, or poles. Operators favor this architecture because reverse-power-feed removes the need for local electricity, while integrated vectoring engines minimize crosstalk across multiple subscriber loops. As a result, field installation times fall and network operations remain streamlined. The customer premises equipment category is poised for 15.11% CAGR through 2031, lifted by upgrade cycles from legacy DSL modems to G.fast devices and by migrations from 212 MHz to 424 MHz profiles that require new hardware. Leading system-on-chip offerings, such as Broadcom’s BCM63158, integrate quad-core processing with multi-gigabit Ethernet ports, cutting bill-of-materials costs for original equipment manufacturers.

Operators view distribution point units as future-proof because software updates can unlock higher frequencies or new diagnostic features without changing curbside equipment. Conversely, lagging customer premises equipment adoption, particularly in North America, creates an inventory liability if end users decline service upgrades. European and Asian carriers mitigate this risk by bundling hardware with service contracts, which lifts attachment rates. Overall, the balance between centralized intelligence and premises-level refresh cycles shapes near-term revenue growth across both segments of the G.fast chipset market.

By Frequency Profile:

212 MHz Maturity Meets 424 MHz AmbitionAt 46.29% market share in 2025, the 212 MHz profile remains the workhorse for tier-1 incumbents that value its proven reach and established operational toolsets. The 424 MHz G.mgfast profile, however, is expected to record a 14.67% CAGR because it doubles usable spectrum and enables symmetrical gigabit tiers across short copper runs, making it attractive for multi-dwelling unit distribution and small-cell backhaul. Vendors like Sckipio position exclusively around 424 MHz silicon, targeting greenfield deployments where backward compatibility is less critical.

Operators still choose 212 MHz when loop lengths exceed 150-200 meters or where attenuation risks jeopardize quality-of-experience. Silicon roadmaps now include advanced echo-cancellation modules that extend 424 MHz reach, narrowing the performance gap and broadening addressable scenarios. Regulatory clarity following the Broadband Forum’s TR-507 specification ensures interoperability, further accelerating adoption of higher-frequency chipsets.

By Process Node:

Migration to Advanced Nodes AcceleratesChipsets produced on 14- to 22-nanometer nodes accounted for 49.94% of 2025 revenue, reflecting the sweet spot between performance and wafer cost. Foundries are shifting capacity toward 10- and 7-nanometer processes, and the G.fast chipset market size for these advanced nodes is projected to grow at 14.53% CAGR through 2031. Shrinking geometries let vendors integrate neural-processing engines, secure boot, and hardware telemetry within a single die, reducing board footprint and power consumption. Broadcom’s CES 2026 reveal of its BCM4918 accelerated processing unit underscores this integration shift, packing Armv8 cores, AI accelerators, and cryptographic engines onto one chip.

Legacy 28-nanometer designs persist in cost-sensitive regions but face supply constraints as fabs reallocate lines to higher-margin segments. Operators increasingly set power-per-bit thresholds in sourcing criteria, effectively forcing suppliers to adopt advanced nodes. The resulting performance uplift strengthens the competitive stance of G.fast relative to DOCSIS and passive optical network silicon that already leverage sub-10-nanometer processes.

By End-Use Application:

MDUs Dominate While 5G Small-Cell Backhaul Gains PaceMulti-dwelling unit deployments represented 42.63% of 2025 revenue, leveraging existing in-building wiring to avoid disruptive fiber-to-the-apartment construction. The approach resonates in high-rise-dense markets across Asia-Pacific, the Middle East and Africa, and parts of Europe, where building owners seek quick, low-cost broadband upgrades. Small-cell and Wi-Fi offload backhaul is forecast to accelerate at 14.91% CAGR, propelled by 5G densification that demands low-latency links between macro sites and distributed antennas. Where copper pairs already reach lamp posts or utility-room patch panels, G.fast offers gigabit performance at a fraction of fiber trenching costs.

Single-family curbside deployments remain relevant in rural or historic districts where civil-works limitations hinder fiber projects, but growth is slower as greenfield housing increasingly adopts fiber-ready standards. Industrial internet-of-things use cases endure, although many utilities favor private optical or wireless networks. Overall, rising urbanization and 5G densification reinforce the shift toward applications that monetize short copper loops with high-throughput silicon.

Geography Analysis

APAC G.Fast Chipset Market

Asia-Pacific led the market with 34.11% revenue share in 2025. South Korea’s 89% fiber penetration limits copper use primarily to older apartment blocks, yet operators still roll out G.fast in basements to avoid costly in-unit rewiring. China added more than 50 million fiber-to-the-home ports in 2025, but secondary cities with legacy cabling continue to require incremental capacity upgrades, sustaining unit demand. Japan aims for near-universal fiber by 2027, although rural prefectures retain sufficient copper plant quality for interim G.fast deployments. Local subsidy frameworks consistently reward rapid service activation, making the technology an attractive bridge until fiber reaches every doorstep.

Europe G.Fast Chipset Market

Europe remains a pivotal region, thanks to Germany’s EUR 1.8 billion (USD 1.98 billion) January 2026 broadband allocation and the United Kingdom’s GBP 5 billion (USD 6.25 billion) Project Gigabit fund. These programs foster extensive fiber-to-the-distribution-point installations in rural areas, where long civil-works lead times would otherwise impede gigabit targets,. However, aggressive fiber-to-the-home over-builds in major cities compress the urban addressable space. The European Union’s Gigabit Infrastructure Act expedites permitting, thereby accelerating both fiber and hybrid rollouts, and placing downward pressure on long-term G.fast volumes in metro cores.

The Americas and MEA G.Fast Chipset Market

The Middle East and Africa region is forecast to deliver the fastest growth at 14.78% CAGR from 2026-2031. Gulf Cooperation Council carriers exploit G.fast for rapid small-cell backhaul and mixed fiber-copper connectivity during large-scale data-center expansions, including the UAE’s 400-gigabit EMIX core upgrade in January 2026. Multi-tenant housing in rapidly urbanizing cities further stimulates demand for 424 MHz silicon. North America experiences the most pronounced headwinds: sizable fiber capex commitments at Verizon and AT&T, alongside DOCSIS 4.0 upgrades by cable incumbents, restrict G.fast uptake to niche applications such as temporary service activation and legacy multi-dwelling unit refurbishments. South America and Africa outside the Gulf states remain largely untapped due to limited qualified copper infrastructure and the popularity of fixed wireless access.

Competitive Landscape

Broadcom, MaxLinear, and Qualcomm collectively control the bulk of design wins, leveraging 14- to 10-nanometer system-on-chip platforms that merge DSL modems, vectoring engines, reverse-power-feed controllers, and application processors. MaxLinear’s 2020 acquisition of Intel’s Home Gateway Platform Division added more than 2,000 broadband patents, deepening relationships with European and North American incumbents, although the firm reported only USD 58 million in broadband revenue for Q3 2025 amid a shift toward passive optical networks. Broadcom’s BCM4918, unveiled at CES 2026, integrates Armv8 CPU cores, an AI inference engine, and cryptographic accelerators, positioning the company for edge-computing use cases that demand simultaneous wired and wireless traffic offload.

Sckipio focuses on 424 MHz G.mgfast silicon targeted at greenfield deployments in emerging markets, betting that operators will prioritize spectral efficiency over backward compatibility. MediaTek entered the arena at MWC 2026 with a customer premises equipment reference design that combines a 5G-A module and Wi-Fi 8 chip, signaling potential convergence between fixed wireless access and G.fast gateways. Competitive differentiation now hinges on deeper integration: vendors embed digital pre-distortion, hardware telemetry, and on-device AI to lower operating expenses and enhance predictive maintenance. Interoperability driven by Broadband Forum standards, particularly TR-507, reduces lock-in and heightens pressure on suppliers to innovate around power efficiency and feature richness.

Small-cell backhaul and in-building multi-tenant distribution present white-space opportunities where new entrants can capture share without displacing entrenched passive optical or cable platforms. As operators demand unified silicon that supports copper, fiber, Wi-Fi 8, and 5G termination on one board, chipset houses able to deliver heterogeneous compute on sub-10-nanometer nodes enjoy a strategic advantage. Overall, the market exhibits moderate concentration, but ongoing process-node migration and application diversification offer room for challenger gains.

G.Fast Chipset Industry Leaders

Broadcom Inc.

MaxLinear, Inc.

MediaTek Inc.

Sckipio Technologies Ltd.

Triductor Technology (Suzhou) Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

G.Fast Chipset Market Companies Covered in this Report

- Sckipio Technologies Ltd.

- MaxLinear, Inc.

- Broadcom Inc.

- Qualcomm Technologies, Inc.

- MediaTek Inc.

- Hisilicon Technologies Co., Ltd.

- Triductor Technology (Suzhou) Co., Ltd.

- Metanoia Communications Inc.

- Realtek Semiconductor Corporation

- Marvell Technology, Inc.

- Renesas Electronics Corporation

- Microchip Technology Inc.

- NXP Semiconductors N.V.

- DZS Inc.

- Calix, Inc.

- Zyxel Communications Corp.

- Adtran, Inc.

- Proscend Communications Inc.

- Versatek, LLC

Recent Industry Developments in G.Fast Chipset Market

- March 2026: MediaTek and Fibocom introduced a fixed wireless access platform that combines 5G-A and Wi-Fi 8 for high-density premises equipment.

- March 2026: MediaTek and Fibocom introduced a fixed wireless access platform that combines 5G-A and Wi-Fi 8 for high-density premises equipment.

- February 2026: The United Arab Emirates joined the USD 700 million WorldLink subsea cable project connecting the UAE, Iraq, and Turkey, enhancing regional data transfer resilience.

- January 2026: e& UAE upgraded its EMIX IP transit platform to 400 Gbps, incorporating AI-driven network automation for faster provisioning.

Global G.Fast Chipset Market Report Scope

The G.Fast Chipset Market pertains to the industry segment dedicated to semiconductor solutions that utilize G.Fast technology, an advanced DSL standard, to enable ultra-fast broadband access over existing copper telephone lines. These chipsets are specifically designed to deliver gigabit-level internet speeds by employing advanced modulation techniques and dynamic spectrum management. This makes them a cost-efficient alternative to fiber deployment for last-mile connectivity.

The G.Fast Chipset Market Report is Segmented by Deployment Type (Distribution Point Unit (DPU) Chipsets, and Customer Premises Equipment (CPE) Chipsets), Frequency Profile (106 MHz Profile, 212 MHz Profile, and 424 MHz Profile (G.mgfast)), Process Node (28 nm and Above, 14 -22 nm, and 7 -10 nm), End-Use Application (Multi-Dwelling Unit Broadband, Single-Family FTTC / FTTB, Small-Cell / Wi-Fi Offload Backhaul, and Industrial IoT / Smart-Grid Backhaul), and Geography (North America,Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

| Distribution Point Unit (DPU) Chipsets |

| Customer Premises Equipment (CPE) Chipsets |

| 106 MHz Profile |

| 212 MHz Profile |

| 424 MHz Profile (G.mgfast) |

| 28 nm and Above |

| 14 -22 nm |

| 7 -10 nm |

| Multi-Dwelling Unit Broadband |

| Single-Family FTTC / FTTB |

| Small-Cell / Wi-Fi Offload Backhaul |

| Industrial IoT / Smart-Grid Backhaul |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Deployment Type | Distribution Point Unit (DPU) Chipsets | |

| Customer Premises Equipment (CPE) Chipsets | ||

| By Frequency Profile | 106 MHz Profile | |

| 212 MHz Profile | ||

| 424 MHz Profile (G.mgfast) | ||

| By Process Node | 28 nm and Above | |

| 14 -22 nm | ||

| 7 -10 nm | ||

| By End-Use Application | Multi-Dwelling Unit Broadband | |

| Single-Family FTTC / FTTB | ||

| Small-Cell / Wi-Fi Offload Backhaul | ||

| Industrial IoT / Smart-Grid Backhaul | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the G.fast chipset market?

The G.fast chipset market is valued at USD 4.67 billion in 2026.

How fast is the market expected to grow through 2031?

Market revenue is forecast to reach USD 9.11 billion by 2031, representing a 14.29% CAGR during 2026-2031.

Which deployment segment leads revenue today?

Distribution Point Unit (DPU) chipsets account for 55.74% of 2025 revenue, driven by operator focus on street-cabinet and basement deployments.

Which region offers the highest growth potential?

The Middle East & Africa region is projected to grow the fastest, registering a 14.78% CAGR through 2031.

Why are 424-MHz G.mgfast chipsets gaining attention?

They double the available spectrum, enabling symmetrical gigabit speeds for multi-dwelling units (MDUs) and small-cell backhaul over short copper loops.

How is silicon integration influencing competitive dynamics?

Migration to 10-nm and 7-nm process nodes enables integration of AI engines, secure boot, and reverse-power-feed controllers, reducing power consumption and board costs while increasing feature density.

Page last updated on: