5G Enterprise Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.73 Billion |

| Market Size (2031) | USD 32.08 Billion |

| Growth Rate (2026 - 2031) | 29.74% CAGR |

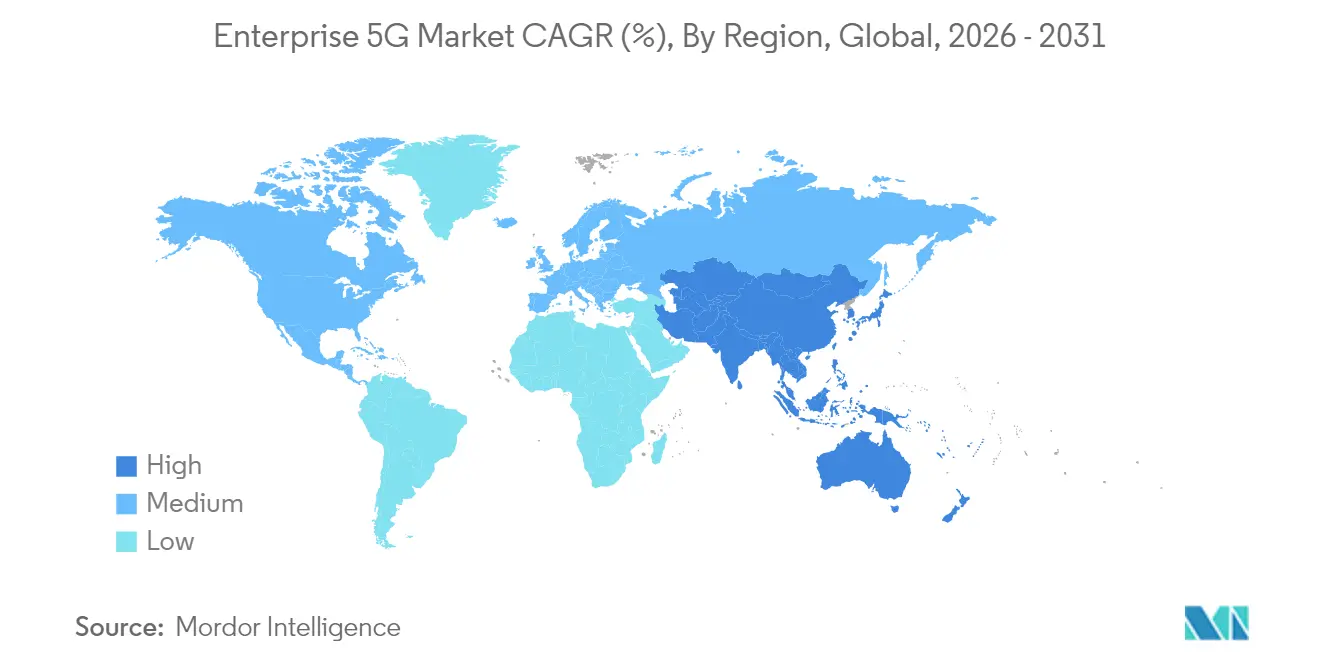

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

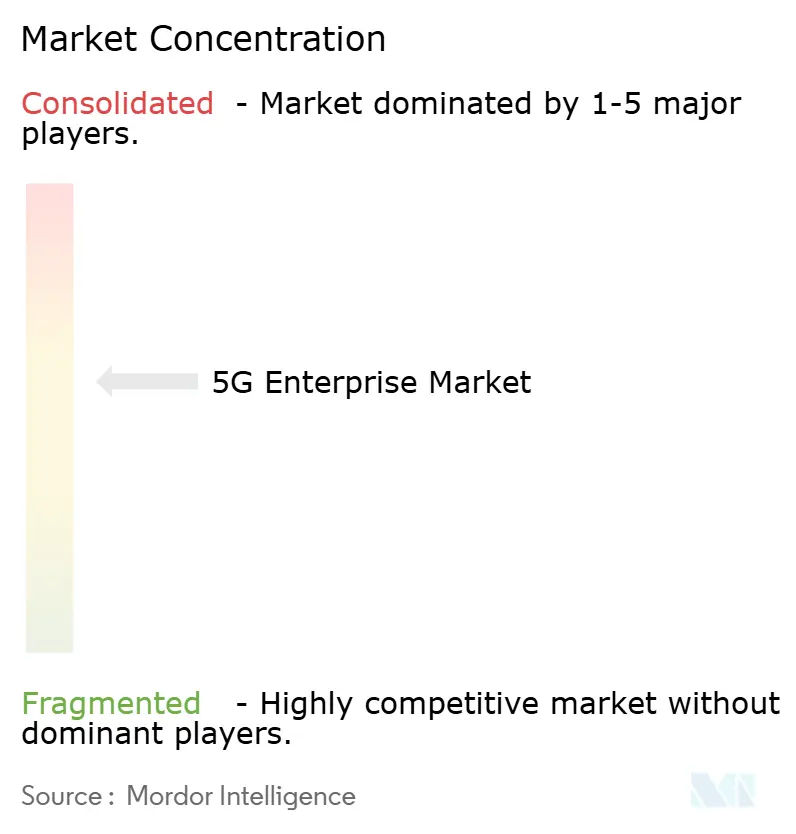

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G Enterprise Market Analysis by Mordor Intelligence

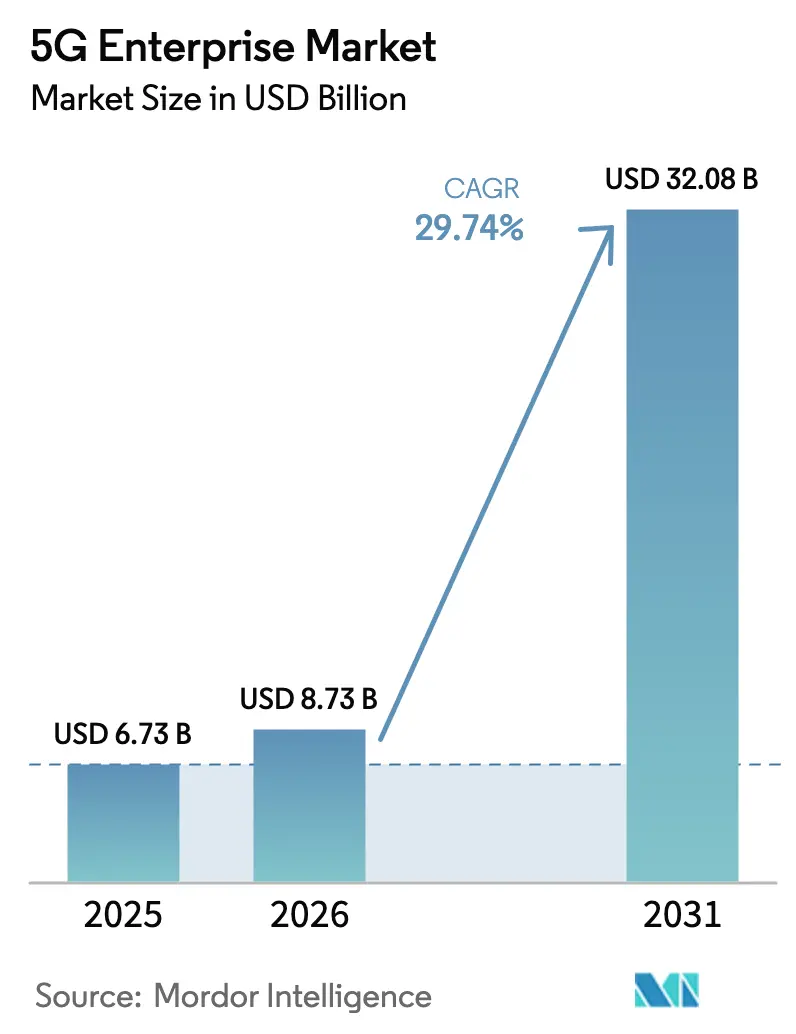

The 5G Enterprise Market size was valued at USD 6.73 billion in 2025 and estimated to grow from USD 8.73 billion in 2026 to reach USD 32.08 billion by 2031, at a CAGR of 29.74% during the forecast period (2026-2031).

This expansion springs from enterprises treating 5G as the digital backbone for automation, analytics, and immersive applications. Robust interest in standalone 5G, already offered by 47 mobile operators, is speeding up adoption of features such as network slicing and ultra-reliable low-latency communications[1]GSMA, “The Mobile Economy Europe 2025,” gsma.com. Private deployments and edge architectures are removing performance bottlenecks, while unlicensed and shared spectrum access is lowering entry barriers. Early industrial rollouts show measurable productivity gains, and satellite-5G partnerships now span 43 countries, broadening coverage footprints. Even so, high capital outlays, brown-field integration complexity, and a pronounced shortage of cross-disciplinary 5G/OT talent temper the near-term uptake.

Key Report Takeaways

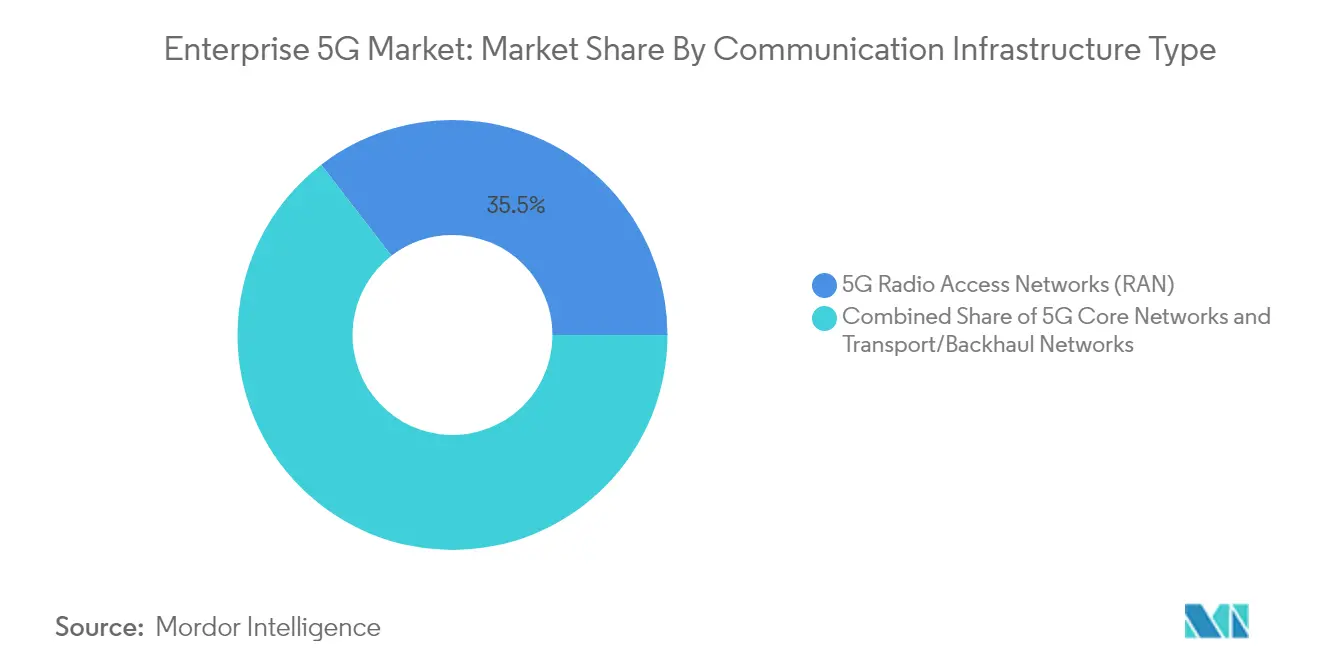

- By communication infrastructure type, Radio Access Networks led with a 35.45% revenue share in 2025, while 5G core networks are projected to advance at a 31.88% CAGR through 2031.

- By deployment model, private networks held 37.60% of 5G enterprise market share in 2025; the same segment is forecast to expand at a 35.48% CAGR to 2031.

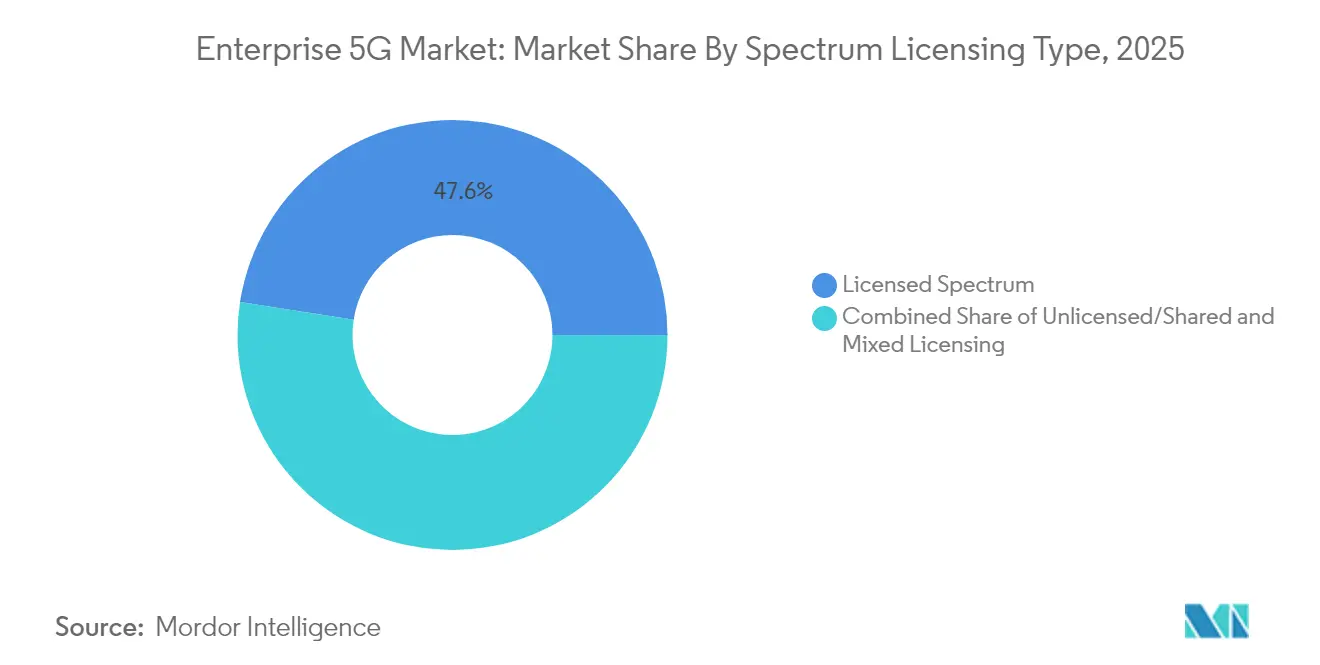

- By spectrum licensing, licensed bands captured 47.55% of the 5G enterprise market size in 2025; unlicensed/shared bands recorded the fastest growth at a 38.85% CAGR.

- By enterprise vertical, discrete manufacturing accounted for 28.85% of the 5G enterprise market size in 2025, whereas healthcare is moving ahead at a 31.5% CAGR.

- By geography, North America commanded 37.10% revenue share in 2025; Asia-Pacific is on track for a 32.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 5G Enterprise Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Release of unlicensed/shared spectrum | +8.50% | North America, Europe, select APAC countries | Medium term (2-4 years) |

| Edge computing and network slicing | +7.20% | Global, early in North America and East Asia | Medium term (2-4 years) |

| Industrial-IoT adoption in smart plants | +6.40% | North America, Europe, China, Japan, South Korea | Short term (≤ 2 years) |

| Net-zero mandates for energy-optimised 5G | +3.90% | Europe, North America, advanced APAC economies | Long term (≥ 4 years) |

| 5G-TSN convergence for deterministic control | +2.8% | Europe, North America, Japan | Medium term (2-4 years) |

| Non-terrestrial networks for remote coverage | +2.2% | Global, focus on remote regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Release of Unlicensed/Shared Spectrum Transforms Enterprise Access

Regulators opening mid-band frequencies have made private 5G viable for firms that once shied away from spectrum fees. In the United States, the Citizens Band Radio Service has already supported more than 250,000 industrial device activations, encouraging similar frameworks in Europe’s 3.8-4.2 GHz band. Siemens anticipates deployments moving from pilots to scale during 2025 as harmonization progresses. Greater flexibility allows factories, logistics hubs, and energy sites to customize coverage footprints, improving uptime and security. Shared spectrum also stimulates a growing ecosystem of network-in-a-box vendors that package radios, edge cores, and management tools as turnkey kits. The cumulative effect is a wider funnel of prospects entering the 5G enterprise market, accelerating time to revenue for suppliers.

Edge Computing and Network Slicing Redefine Enterprise Architectures

Enterprises are refactoring networks so that latency-sensitive workloads sit within meters of connected assets. Operators such as T-Mobile illustrate the concept through priority slices for first responders. Forty-seven operator groups are now standardizing APIs that expose slice configuration to developers, lowering orchestration effort. Combining dedicated slices with on-premises compute nodes helps manufacturers push decision loops below 1 ms, enabling synchronous robotics and vision inspection. A Wray Castle study indicates network slicing can boost overall spectrum utilisation by 40%. These gains feed directly into OpEx savings, reinforcing the value proposition of private-edge architecture inside the 5G enterprise market.

Industrial IoT Accelerates Manufacturing Transformation

Latency under 1 ms and support for one million devices per square kilometer have made massive sensor grids practical on factory floors. Transport and logistics already represented 26% of global 5G IoT links in 2024, with telematics and real-time navigation yielding quick ROI. Pilot plants such as ZTE’s AI-empowered facility report throughput improvements above 30% thanks to closed-loop control. The Manufacturing Institute found that 91% of producers see 5G as central to competitiveness, predicting average cost cuts of 38%. Although only 2% of enterprises had live private networks by late 2024, falling equipment prices and cloud-managed offerings suggest a tipping point is near.

Net-Zero Mandates Drive Energy-Optimized Deployments

Telecom stakeholders are aligning with global climate goals, embedding efficiency metrics into RFPs and design guides. Ten UK connectivity firms representing approximately GBP 50 billion in annual turnover have set joint standards for supplier emissions disclosure[2]Ericsson, “United Kingdom Telecoms Sign Supplier Emissions Commitment,” ericsson.com. Nokia targets net-zero operations by 2040, bundling renewable-powered radios and intelligent cooling as part of its enterprise portfolio. These commitments resonate with buyers facing their own ESG targets, shifting procurement toward low-carbon network gear. In turn, spectrum regulators in Europe and North America reward greener deployments through expedited licensing and policy support, adding momentum to the 5G enterprise market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and integration complexity | -5.80% | Global, greater impact in emerging markets | Short term (≤ 2 years) |

| Scarcity of 5G/OT engineering talent | -4.30% | Global, acute in fast-growing markets | Medium term (2-4 years) |

| Fragmented device-certification ecosystem | -3.1% | Global, varying with regulatory maturity | Medium term (2-4 years) |

| Local-spectrum rules hindering multinational roll-outs | -2.7% | Global, impact on multinational enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Integration Complexity Slow Adoption

Standalone 5G cores, multi-band radios, and industrial gateways can push a mid-sized brown-field deployment into multi-million-dollar territory. A 2024 Kyndryl survey showed many firms deferring projects until they blueprint migration paths for legacy SCADA and MES layers. Open RAN promises vendor diversity yet introduces fresh interoperability testing, as flagged by the Open RAN Integration Playbook. Network-as-a-Service models are emerging to smooth cash-flow peaks by shifting spend from capex to OpEx, but clarity around service-level commitments still varies. This financial and technical inertia trims early growth in segments with razor-thin margins.

Scarcity of 5G/OT Engineering Talent Creates Implementation Bottleneck

Enterprises need professionals who grasp both radio optimization and operational workflows, yet the talent pool remains shallow. India alone reports a gap of 2.4 million skilled telecom workers, with employability at 40% of graduates in relevant streams. Ericsson’s academic private 5G network at Tecnologico de Monterrey exemplifies partnerships designed to fill the pipeline. Until supply catches up, integrators are charging premium rates and projects risk delays, capping roll-out velocity for the 5G enterprise market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Infrastructure Type: Core Networks Poised for Accelerated Uptake

The 5G Radio Access Network segment generated the largest slice of revenue in 2025 at 35.45%, reflecting its indispensable role in linking endpoints. This foundational investment gave operators and integrators a head starts in monetizing coverage obligations. Rising enterprise need for deterministic performance now shifts attention to cloud-native 5G cores, which are on course for a 31.88% CAGR. The 5G enterprise market size for core solutions is projected to expand sharply as standalone deployments move beyond trials. Network function virtualization lets firms bolt on low-code policy engines, converged charging, and AI-driven assurance, driving higher ARPU per site.

Transport and backhaul, though smaller in absolute terms, are evolving rapidly. Partnerships such as Ericsson with Juniper and ECI Telecom confirm demand for high-capacity packet transport between cell sites and data centers. E-band and emerging W-band links unlock multi-gigabit throughput, complementing fibre in dense industrial parks. These innovations reduce bottlenecks that once throttled remote-vision analytics. As a result, core and transport segments are becoming tightly coupled, expanding their combined wallet share inside the 5G enterprise market.

By Deployment Model: Private Networks Solidify Strategic Relevance

Private deployments captured 37.60% of revenue in 2025, reinforcing the preference for on-premises control. With a 35.48% CAGR, the 5G enterprise market size for private deployments is set to multiply, led by factories, hospitals, and logistics yards that value deterministic Quality of Service. A 2024 Digitalization World survey forecasts global private-5G revenues at USD 6 billion by 2027. Contrast that with public 5G, which suits use cases where coverage breadth outweighs micro latency needs.

Hybrid models are also standing out. Enterprises employ public slices for non-sensitive traffic while reserving a campus-wide micro-core for robotics or AGVs. Neutral-host solutions enable venue owners to share infrastructure costs, facilitating rapid multi-tenant coverage. This approach helps operators penetrate new verticals without redeploying full stacks, broadening addressable revenue streams across the 5G enterprise market.

By Spectrum Licensing Type: Unlicensed Choices Catalyze Growth

Licensed bands commanded 47.55% revenue in 2025 as mobile network operators used existing allocations to serve enterprises. Guaranteed interference protection remains compelling for mission-critical mobility. Unlicensed and shared access, however, posts the fastest 38.85% CAGR. The 5G enterprise market share of unlicensed deployments rises as CBRS and similar models let firms self-provision radios. Entry cost falls and procurement cycles shorten, though enterprises must master interference management.

Hybrid spectrum plans are gaining ground. Organizations route control traffic through licensed mid-band and reserve best-effort data for 60 GHz unlicensed channels. The Wireless Infrastructure Association notes that a balanced allocation across bands improves reliability while containing spend. The net effect is a broader inclusion of small and medium enterprises in the 5G enterprise industry, deepening overall penetration.

By Enterprise Vertical: Healthcare Outpaces All Others

Discrete manufacturing held a 28.85% revenue share in 2025, benefiting from deterministic TSN integration and real-time machine monitoring. Early adopters report production cost drops near 38% alongside productivity hikes above 40%. Process sectors such as chemicals and food are now replicating these gains through sensor-dense environments.

Healthcare moves fastest with a 31.5% CAGR. Tele-ultrasound, remote surgery support, and always-connected ambulances require sustained uplink capacity and single-digit millisecond latency. Studies show 5G enables high-resolution imaging without perceptible delay, improving diagnostic accuracy. BFSI, energy, and utilities trail closely, each trialing blockchain-ready secure channels and grid modernization tools. Retail, e-commerce, and transport use 5G for inventory robotics and real-time fleet telemetry. Collectively, these deployments confirm vertical depth inside the 5G enterprise market.

Geography Analysis

North America commanded the largest regional footprint at 37.10% revenue share in 2025, anchored by early spectrum releases and active systems-integration ecosystems. The United States sees 76% of manufacturers planning private networks, though a recent policy shift caused an 11% dip in short-term enthusiasm. Public funding proposals worth USD 9 billion aim to extend 5G broadband into rural zones, which will widen the customer base. Canada follows with strong incentives for Industry 4.0 testbeds. Together, these initiatives reinforce leadership even as North American coverage ambitions mature.

Asia-Pacific is the fastest climber with a 32.88% CAGR through 2031. China’s 5G+ Smart Factory programs show quantifiable gains in throughput and defect reduction. Japan and South Korea exploit longstanding industrial automation cultures, layering 5G over existing lean-manufacturing cells. India’s telecom-sector skills gap tops 2.4 million workers, which policy makers address via reskilling campaigns lightreading. Despite talent constraints, lower equipment prices bolster adoption among mid-tier enterprises.

Europe retains a solid foothold despite coverage gaps. Germany’s auction of 3.8-4.2 GHz licenses directly to industry pioneers expanded campus network pilots. Pan-EU harmonization simplifies device certification, although total capital investment slid for the first time in seven years to EUR 57.9 billion. Open RAN and edge cloud projects attract new entrants, fueling competitive variety. GSMA expects 5G to contribute over EUR 160 billion to European GDP by 2030. These figures underscore steady, if uneven, progression.

The Middle East and Africa witness growing momentum led by Saudi Arabia’s fresh spectrum auctions, driving vendor revenue up 9% in Q4 2024 for Nokia. Latin America remains in the early adoption phase but benefits from satellite-backed 5G coverage for mining and agriculture. Collectively, global demand diversity positions the 5G enterprise market for broad-based expansion.

Competitive Landscape

The supplier base is moderately concentrated. Nokia, Ericsson, and Huawei provide full-stack portfolios covering radios, transport, and cloud-native cores, which anchor incumbency across several continents. New entrants focus on private-network simplicity: Celona rallies around a modest-footprint solution that edges into incumbent share, characterizing the contest as a “three-horse race”. Cisco pairs with NEC to supply turnkey private 5G bundles in EMEA, blending NEC’s systems integration experience with Cisco’s standalone core.

Vertical-specific capability marks the next battleground. T-Mobile partners with NVIDIA, Ericsson, and Nokia in an AI-RAN Innovation Center that uses GPU-accelerated analytics to balance cell-edge loads and cut latency. Such differentiation layers artificial intelligence on telecom fundamentals, raising performance ceilings. Suppliers also hedge geopolitical risk: Nokia and Ericsson have expanded U.S. production sites to offset potential tariff costs, a move their CEOs argue keeps total cost of ownership stable for domestic carriers. The 5G enterprise industry thus sees rival camps sharpening propositions around integration speed, AI-ready architectures, and compliance confidence.

White-space opportunities concentrate on healthcare and discrete manufacturing, where tailored SLAs, deterministic networking, and edge analytics remain underserved. Mergers such as Vodafone and Three in the United Kingdom, approved in June 2025, create aggregated spectrum pools and promise GBP 11 billion in new 5G spend, injecting fresh rivalry among enterprise service providers. Strategic outsourcing of AI infrastructure to partners like NVIDIA underscores a growing preference for collaborative ecosystems over solitary rollouts, reshaping partnership dynamics within the 5G enterprise market.

5G Enterprise Industry Leaders

Cisco System Inc.

Telefonaktiebolaget LM Ericsson

Huawei Technologies Co. Ltd.

NEC Corporation

Samsung Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vodafone and Three completed their merger, forming VodafoneThree and pledging GBP 11 billion for standalone 5G expansion focused on enterprise services.

- May 2025: NVIDIA partnered with mobile operators across five continents to deploy sovereign AI infrastructure that integrates tightly with 5G cores.

- September 2024: Ericsson rolled out a three-tier enterprise portfolio featuring Private 5G Compact and neutral-host solutions.

- September 2024: T-Mobile, NVIDIA, Ericsson, and Nokia established the AI-RAN Innovation Center in Washington State.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the 5G enterprise market as the revenue stream that equipment makers, software firms, and network operators earn from 5G-based connectivity, infrastructure, and managed services sold to business and public-sector users. The frame therefore embraces private and hybrid campus networks, licensed and shared spectrum operations, and all enabling core, RAN, transport, and edge platforms that supply ultra-reliable low-latency links for automation, analytics, and massive-IoT workloads.

Scope exclusion: consumer mobile broadband subscriptions and fixed-wireless access aimed at households are outside this analysis.

Segmentation Overview

- By Communication Infrastructure Type

- 5G Radio Access Networks (RAN)

- 5G Core Networks

- Transport/Backhaul Networks

- By Deployment Model

- Private 5G Networks

- Public 5G Networks

- Hybrid/Shared Networks

- By Spectrum Licensing Type

- Licensed Spectrum

- Unlicensed/Shared (e.g., CBRS, LAA)

- Mixed Licensing

- By Enterprise Vertical

- IT and Telecommunications

- BFSI

- Manufacturing - Discrete

- Manufacturing - Process

- Retail and E-commerce

- Healthcare

- Energy and Utilities

- Transportation and Logistics

- Other Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with mobile-network operators, industrial automation leads, and neutral-host integrators across North America, Europe, and Asia-Pacific. These discussions tested spectrum-licensing costs, private-network pricing tiers, and site-level demand forecasts, ensuring desk-derived ratios aligned with on-the-ground decisions.

Desk Research

We began with authoritative public datasets, ITU ICT indicators, GSMA Intelligence adoption trackers, 3GPP release notes, FCC and Ofcom spectrum-auction filings, and the European 5G Observatory to size baseline coverage, spectrum depth, and rollout pace across regions. Company 10-Ks, investor decks, and procurement disclosures then clarified capital intensity and average selling prices for 5G core, small-cell, and edge hardware.

To enrich financial and competitive signals, analysts tapped D&B Hoovers for vendor revenue splits, Dow Jones Factiva for deal flow, and patent analytics from Questel to benchmark technology maturity. The sources listed illustrate our desk research foundation; many additional open and paid references were consulted to validate figures and assumptions.

Market-Sizing & Forecasting

A top-down build starts with country-level licensed-spectrum blocks and enterprise penetration rates, which are then converted into addressable MHz-pop value pools. Selective bottom-up checks, supplier roll-ups of small-cell shipments and sampled ASP × volume for 5G cores, fine-tune totals. Key variables include spectrum price per MHz-pop, number of industrial facilities adopting 5G, edge-computing node counts, sub-6 GHz versus mmWave mix, and private-network ASP progression. Five-year forecasts employ multivariate regression that links enterprise 5G spend to industrial production indices, IoT device growth, and spectrum release calendars vetted by our primary-research panel. Where granular shipment data are scarce, gap-filling uses conservative ratios from analogous 4G deployments viewed through current ASP differentials.

Data Validation & Update Cycle

Outputs pass variance checks against third-party capex disclosures and government rollout targets; outliers trigger re-contact with sources before sign-off. Reports refresh yearly, with interim updates when material events, large spectrum auctions, major regulatory shifts, or step-change vendor price moves occur, and an analyst review ensures clients receive the latest view.

Why our 5G Enterprise Baseline commands confidence

Published estimates often diverge because providers select different service scopes, input variables, and refresh cadences. We openly anchor our base year to observable licensed-spectrum holdings, verifiable private-network contract values, and equipment ASPs that have been cross-checked with buyers and suppliers.

Key gap drivers are typically the inclusion of broader 5G infrastructure spend, omission of shared-spectrum deployments, or reliance on aggressive price-erosion curves. Mordor's scoped-in variables, annual refresh, and mixed top-down/bottom-up cross-checks curb such swings, yielding a balanced, repeatable baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.73 bn | Mordor Intelligence | - |

| USD 7.43 bn | Regional Consultancy A | Counts edge servers and on-prem MEC hardware inside the same pool |

| USD 6.52 bn | Trade Journal B | Excludes public-network slicing revenues purchased by enterprises |

| USD 10.2 bn | Global Consultancy C | Rolls private 5G plus small-cell hardware for indoor coverage into one figure |

In sum, differences stem mainly from scope breadth and price-erosion assumptions; Mordor's disciplined variable selection and annual update cadence provide decision-makers a transparent, dependable baseline.

Key Questions Answered in the Report

What is the current 5G enterprise market size and how fast is it growing?

The 5G enterprise market stands at USD 8.73 billion in 2026 and is projected to reach USD 32.08 billion by 2031, expanding at a 29.74% CAGR.

Which deployment model leads revenue today?

Private 5G networks are ahead with 37.60% revenue share in 2025 and are also the fastest-growing segment at a 35.48% CAGR.

Why are unlicensed and shared spectrum bands important for enterprises?

They remove spectrum-acquisition costs, simplify licensing, and let firms customise coverage, propelling unlicensed/shared deployments at a 38.85% CAGR.

Which vertical is poised for the highest growth through 2031?

Healthcare shows the quickest acceleration with a 31.5% CAGR, supported by telemedicine, remote surgery, and real-time patient monitoring use cases.

What are the main obstacles slowing wider 5G enterprise adoption?

High capital expenditure, integration with legacy systems, and a global shortage of 5G/OT engineering talent are the chief headwinds identified by enterprises and integrators.

How concentrated is the supplier landscape?

A moderate concentration exists: the top five vendors hold just above 60% combined share, giving a score of 6 on a 1–10 scale and leaving competitive space for innovative niche players.

Page last updated on: