5G Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 133.73 Billion |

| Market Size (2031) | USD 320.48 Billion |

| Growth Rate (2026 - 2031) | 19.10% CAGR |

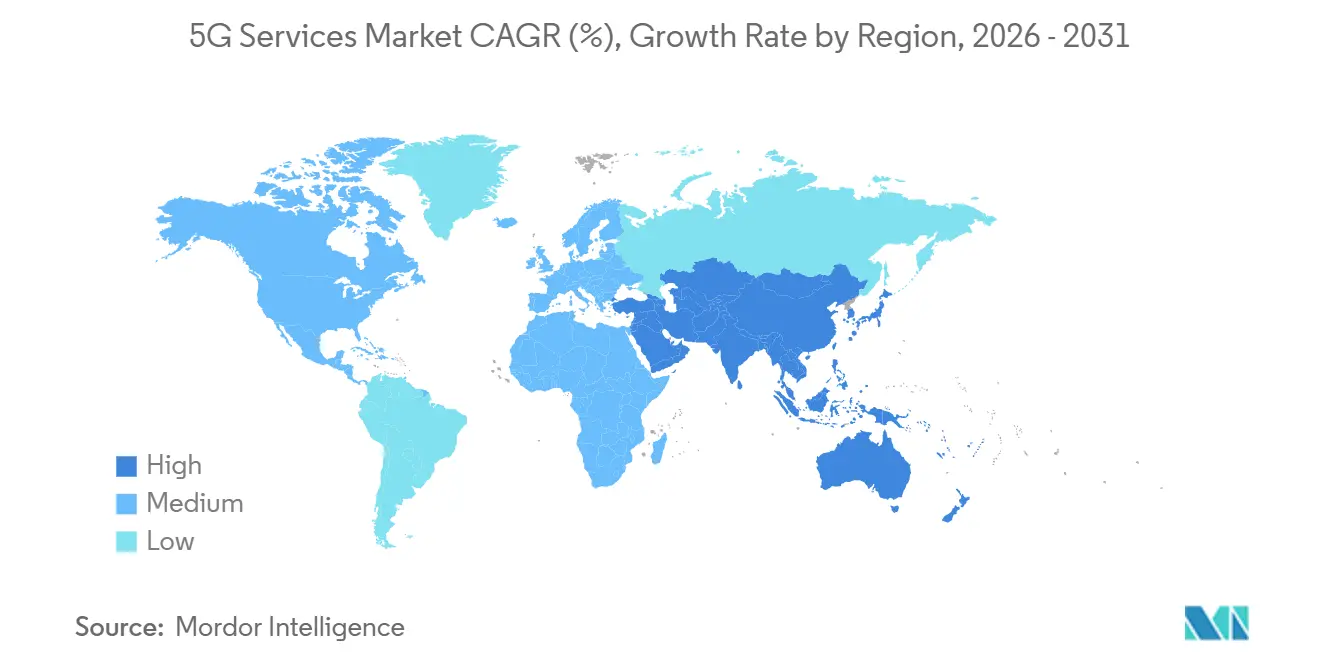

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G Services Market Analysis by Mordor Intelligence

The 5G services market size is expected to increase from USD 130.46 billion in 2025 to USD 133.73 billion in 2026 and reach USD 320.48 billion by 2031, growing at a CAGR of 19.1% over 2026-2031. Robust network-slicing monetization, expanding private-network adoption, and the scale-out of fixed-wireless access are widening revenue pools beyond traditional consumer plans. Operators are prioritizing mid-band densification to balance coverage and capacity, while hyperscale cloud alliances are compressing connectivity margins and accelerating vertical-specific solution launches. Policy momentum around spectrum, together with Release 18 upgrades, is pulling forward enterprise demand for ultra-reliable low-latency connectivity.

Key Report Takeaways

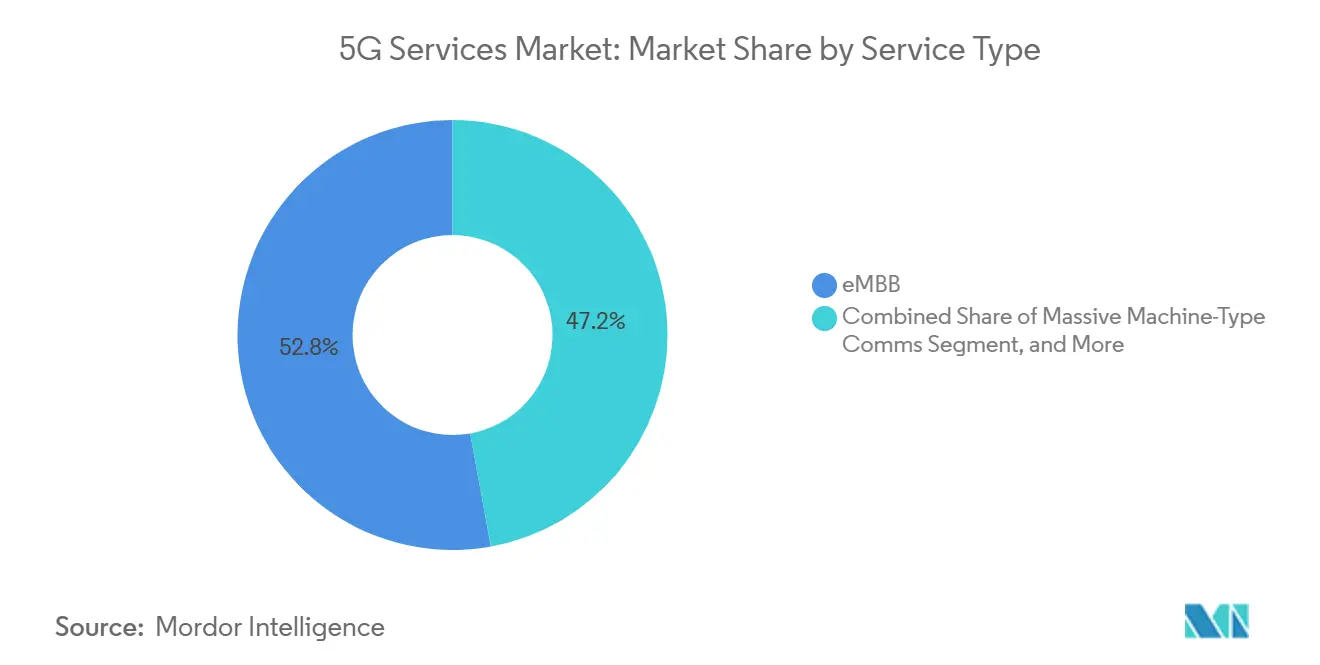

- By service type, Enhanced Mobile Broadband led with 52.84% of the 5G services market share in 2025, while Massive Machine-Type Communications is forecast to expand at a 19.21% CAGR to 2031.

- By network architecture, Non-Standalone deployments captured 63.72% share of the 5G services market size in 2025, whereas Standalone cores are advancing at a 19.53% CAGR through 2031.

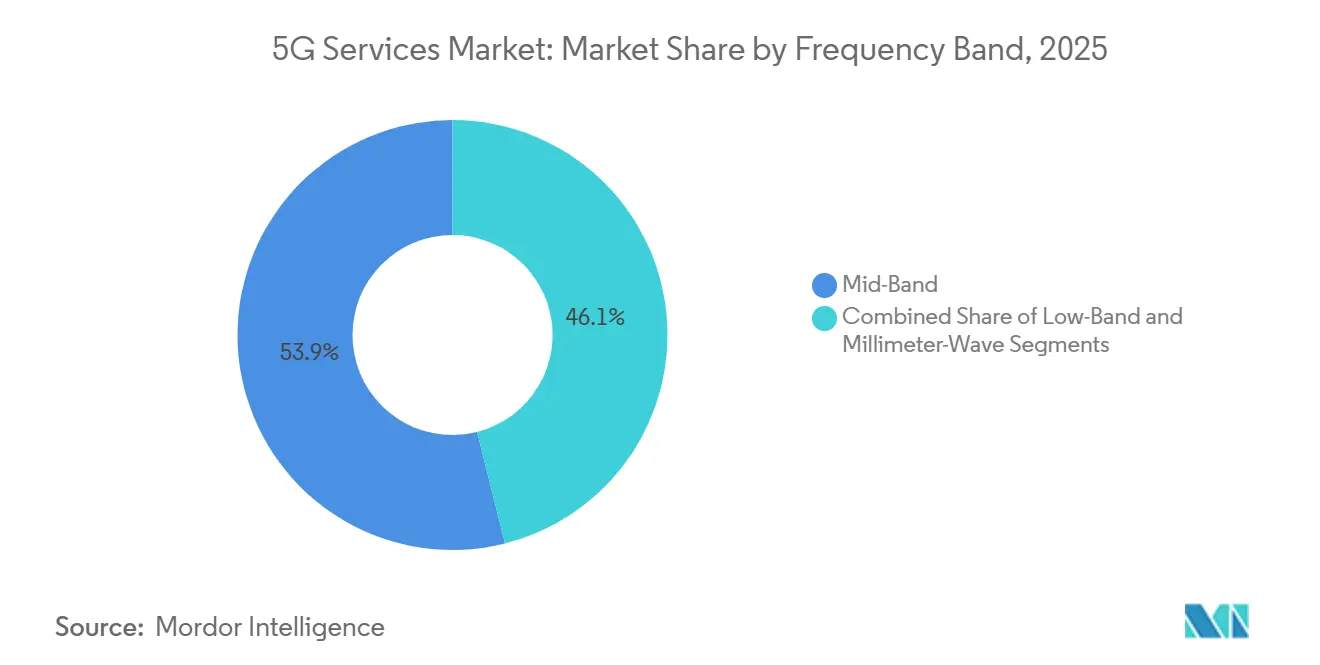

- By frequency band, mid-band assets commanded 53.92% of the 5G services market size in 2025 and are projected to grow at a 19.14% pace up to 2031.

- By end-user industry, the IT and telecom segment held 29.63% revenue share in 2025; manufacturing is the fastest riser, climbing at a 20.07% CAGR to 2031.

- By geography, Asia Pacific accounted for 40.92% of 2025 revenue; the Middle East is the fastest-growing region, with a 20.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 5G Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding mobile data traffic | +8.5% | Global, with highest impact in Asia Pacific and North America | Medium term (2-4 years) |

| High consumer demand for eMBB services | +6.2% | Global, led by developed markets in North America and Europe | Short term (≤ 2 years) |

| Enterprise digital-transformation use-cases | +12.8% | Global, with early adoption in manufacturing hubs across Asia Pacific and Europe | Long term (≥ 4 years) |

| Government spectrum-release initiatives | +7.1% | Regional, concentrated in North America, Europe, and select Asia Pacific markets | Medium term (2-4 years) |

| Private-5G uptake in CBRS and local-licence bands | +5.4% | North America and Europe, with emerging adoption in Asia Pacific | Long term (≥ 4 years) |

| Monetisation via network slicing and SLA tiers | +9.8% | Global, with advanced implementations in Asia Pacific and select European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding Mobile Data Traffic

Monthly traffic rose from 141 exabytes in 2025 to an estimated 400 exabytes by 2031, straining suburban macro layers and triggering extra mid-band cell splits. Fixed-wireless lines doubled year-on-year in North America, diverting capacity from mobility channels and validating the economics of millimeter-wave small cells. Ultra-HD video now represents 72% of downlink volumes, while cloud gaming introduces bursty uplink peaks that require dynamic spectrum sharing. Always-connected wearables and automotive telematics diversify session profiles, pushing carriers toward AI-driven traffic steering that sustains quality of experience during congestion events.

High Consumer Demand for eMBB Services

Unlimited gigabit plans account for 52.84% of total 5G revenue, and U.S. operators report average revenue per user uplifts of USD 4.20 from plan migration. South Korean carriers bundled cloud storage and streaming perks, boosting premium-tier adoption to more than 38% within 6 months. Smartphone-based 8K capture creates symmetrical traffic bursts, forcing investment in uplink carrier aggregation and supplemental spectrum blocks. Operators monetize handset upgrades through zero-interest financing that shortens replacement cycles and locks subscribers into higher-margin tiers.

Enterprise Digital-Transformation Use Cases

Private networks in factories, logistics hubs, and hospitals demand sub-10 millisecond latency and 99.999% reliability. A German electronics plant cut downtime 18% by shifting to a standalone slice that supports predictive maintenance.[1]Siemens, “Siemens Activates Private 5G Network at Amberg Electronics Plant,” SIEMENS.COM U.S. automotive lines using CBRS private 5G shaved cycle times 12% as 240 autonomous vehicles coordinated in real time. Healthcare pilots achieved remote robotic surgery with sub-8 millisecond haptic delay, satisfying investigational thresholds. These proofs lift board-level confidence and propel pipeline growth for turnkey 5G campus networks.

Government Spectrum-Release Initiatives

Regulators accelerated mid-band auctions, raising billions to fund connectivity programs while binding winners to rapid build-out clauses. The U.S. 3.45 GHz sale collected USD 7.2 billion and mandates 60% deployment by 2027.[2]Federal Communications Commission, “FCC Concludes Upper 3.45 GHz Spectrum Auction,” FCC.GOV Europe harmonized the 6 GHz band, supporting cross-border logistics slices. Saudi Arabia auctioned 2.6 GHz and 3.5 GHz channels, commanding USD 1.01 billion and stipulating 70% coverage within three years, favoring vendors with turnkey radios. Streamlined releases anchor investment certainty that accelerates carrier capex cycles.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | |

|---|---|---|---|

| High Deployment Cost and Long ROI Horizons | -2.8% | Global, acute in emerging markets and rural North America | Long term (≥ 4 years) |

| Fragmented and Delayed Spectrum Policy | -1.9% | South America, Africa, parts of Southeast Asia | Medium term (2-4 years) |

| Limited 5G Device Readiness in Emerging Markets | -1.6% | Sub-Saharan Africa, South Asia, parts of Latin America | Short term (≤ 2 years) |

| Geopolitical Vendor Restrictions and Trade Bans | -2.1% | Europe, North America, Australia, select Asia Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Deployment Cost and Long ROI Horizons

Standalone cores, dense mid-band grids, and upgraded backhaul exceed USD 150 billion in global outlays over 2024-2027, stretching payback to 7-9 years.[3]GSMA Intelligence, “Global Mobile Infrastructure Investment Outlook 2024-2027,” GSMAINTELLIGENCE.COM A U.S. carrier revealed USD 18 billion incremental capex for C-band densification, while rural sites without fiber need USD 250,000 each, widening digital divides. Energy bills rise 30-40% versus 4G, pushing operators to sign renewable power agreements to satisfy carbon pledges and control opex. Capital pressure delays stand-alone migration in cost-sensitive regions.

Fragmented and Delayed Spectrum Policy

Disjointed band plans frustrate equipment scale economies. Brazil postponed its 26 GHz auction to 2026, slowing fixed-wireless deployments in major metros and letting fiber incumbents entrench. Only 18 of 54 African nations assigned 5G bands by end-2025; high reserve prices left many blocks unsold. ASEAN states still lack 3.5 GHz harmonization, forcing multinationals to source country-specific radios and deterring cross-border roaming for tourism. Regulatory lag depresses investor confidence and defers rural coverage upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Shift From Throughput to Connection Density

Enhanced Mobile Broadband accounted for 52.84% of 2025 revenue, reflecting demand for gigabit-rate consumer packages and suburban fixed-wireless links. Massive Machine-Type Communications, however, is expanding at 19.21% through 2031, signaling a pivot toward battery-efficient sensors that flood manufacturing, utilities, and smart-city grids. The 5G services market size for narrowband IoT endpoints is rising as operators refarm guard bands and legacy 2G spectrum for low-power overlays, enabling support for 50,000 devices per cell at module prices below 5 USD.

URLLC remains niche, limited to vehicle-to-everything pilots and remote control robotics awaiting mature liability frameworks. Still, by 2028, Release 18 scheduling and edge-compute convergence will blur the lines between service types. Operators bundling mMTC slices with analytics platforms generate sticky enterprise revenue, bolstering long-term growth of the 5G services market.

By Network Architecture: Standalone Unlocks Monetization

Non-Standalone deployments held 63.72% share in 2025 because LTE cores enabled quick time-to-market. Yet Standalone networks, growing at 19.53%, are a prerequisite for slicing, deterministic latency, and voice-over-new-radio services. A U.S. carrier trimmed call set-up times 35% after national SA activation. The 5G services market share shift accelerates as enterprise clients demand dedicated SLAs that NSA cannot guarantee.

Capex hurdles remain, but operators retiring legacy packet cores realize opex savings from data-center consolidation and cloud-native automation. Emerging markets may retain NSA longer, yet greenfield entrants without LTE baggage leapfrog straight to cloud-native SA, expanding the 5G services market footprint in underserved geographies.

By Frequency Band: Mid-Band Remains the Workhorse

Mid-band spectrum captured 53.92% of 2025 revenue, driven by 3.5 GHz and C-band deployments that blend area reach with 400-500 Mbps median speeds. The 5G services market size tied to mid-band is projected to grow 19.14% as operators aggregate carriers and leverage Massive MIMO. Millimeter-wave adoption stays localized to stadiums and downtown cores, yet Release 18 carrier aggregation promises multi-gigabit boosts for premium consumer tiers. Low-band layers sustain rural reach but offer limited upsell potential, serving primarily as mobility coverage backstop.

China’s early 2.6 GHz rollouts gave it a head start, while North American carriers densify C-band to square off against cable broadband. European regulators’ calibrated 6 GHz rules will unlock a fresh tranche of harmonized mid-band, reinforcing the spectrum mix that underpins the global 5G services market.

By End-User Industry: Manufacturing Surges

IT and telecom generated 29.63% of 2025 revenue as operators and cloud players internalized 5G for network control and edge hosting. Manufacturing, however, is climbing at a 20.07% CAGR, powered by private-network rollouts that orchestrate autonomous robots and machine-vision inspection. The 5G services market for shop-floor connectivity is growing as assembly plants demand deterministic latency for real-time control loops.

Automotive and mobility trials in Michigan affirmed cooperative collision avoidance, while energy utilities deployed private 5G for sub-second grid-fault isolation. Healthcare pilots remain exploratory, though regulators’ evolving reimbursement rules could unlock sizable upside post-2027. Media producers exploit portable 5G uplinks for 8K broadcasts, underscoring the breadth of vertical opportunities that now extend well beyond consumer mobility.

Geography Analysis

Asia Pacific supplied 40.92% of 2025 revenue, anchored by China’s four-million-site mid-band footprint and India’s rapid urban coverage by two national carriers. China Mobile launched 5G-Advanced in 300 cities late in 2025, bundling 10 Gbps premium tiers and gaming passes. Japan’s Open RAN buildouts cut rural site costs 28%, while South Korea boasts 72% 5G penetration, the world’s highest.

The Middle East is the fastest-growing territory at a 20.01% CAGR. United Arab Emirates operators achieved 95% population reach by mid-2025, underpinning smart-city pilots with autonomous shuttles and AI traffic controls. Saudi carriers launched standalone cores across major metros to serve oil, logistics, and healthcare verticals in line with Vision 2030 ambitions, while Turkey switched on 5G in its three largest cities, targeting fixed-wireless competition

North America and Europe exhibit slower subscriber-driven growth but pivot to enterprise and fixed-wireless scaling. A U.S. carrier’s C-band network covered 230 million people by December 2025, monetizing 4 million fixed-wireless lines. Deutsche Telekom’s cross-border slices boosted enterprise revenue 14% year-on-year. South America and Africa trail because of auction delays, device affordability gaps, and backhaul shortfalls, although selective rollouts in Brazil and South Africa defend mobile incumbents against fiber overtures.

Regulatory Landscape

The regulatory environment for 5G services continues to be shaped by spectrum policy, wholesale access rules, and standards alignment. In April 2026, the UK Government published its final Statement of Strategic Priorities for telecommunications, directing Ofcom to align spectrum and broader telecom regulation with economic growth and investment in high-quality networks. This reinforced a pro-investment posture that supports mid-band densification and enterprise-grade 5G rollouts.

Across major markets, regulators are also tightening the link between market structure and network economics. In May 2026, the Canadian Radio-television and Telecommunications Commission (CRTC) directed major ILECs including Bell Canada and TELUS to issue revised tariff pages for aggregated wholesale high-speed access services, shaping backhaul and broadband competition dynamics that interact with 5G fixed wireless access. At the regional level, the European Commission advanced work on a proposed Digital Networks Act in 2026 to reduce fragmented national frameworks and simplify authorization and spectrum processes for high-capacity networks. Standards bodies such as ETSI (TS 129 500 V17.16.0, February 2026) also continued to publish 5G core architecture specifications that underpin interoperable service delivery and slicing implementations.

Value Chain Analysis

The 5G services value chain starts with spectrum and licensing regimes, then flows through network equipment and software (RAN, transport, and cloud-native cores), integration and deployment, and finally service monetization across consumer eMBB, fixed wireless access, private networks, and managed slices. Infrastructure supply remains concentrated among a small set of large RAN vendors (Ericsson, Nokia, Huawei), with Samsung and ZTE present in select regions. Hyperscale cloud alliances and telecom system integrators increasingly influence how operators package edge-enabled connectivity offers for industry verticals.

Upstream component dependencies remain a key constraint, particularly for silicon, memory, and RF front-end parts that affect radio unit cost and availability. Vendor supply chains are bifurcated, with Ericsson and Nokia relying heavily on Western semiconductor and tooling ecosystems while Huawei leans more on domestic Chinese suppliers, creating different risk profiles under geopolitical restrictions and export controls. Competition for advanced semiconductor capacity from AI data centers also feeds into telecom equipment costs and lead times, and long qualification cycles for base-station components limit rapid substitution when shortages emerge. Policy actions, including the FCC equipment authorization framework in the United States and diversification initiatives in the UK focused on Open RAN testing and interoperability (for example, via SONIC Labs and UKTL), continue to shape vendor selection, procurement strategies, and multi-vendor deployment readiness.

Competitive Landscape

Global service revenue is moderately concentrated: the top ten operators control about 58%, yet most markets remain national oligopolies fenced by license barriers. Western vendor share shifted to Ericsson, Nokia, and Samsung amid geopolitical restrictions on Huawei gear, while Huawei and ZTE still dominate much of Asia Pacific and the Middle East. Hyperscale clouds cut joint go-to-market deals with telcos, bundling edge compute and threatening pure-connectivity margins.

Operators thin vertical stacks by buying system-integration boutiques and edge-platform startups, in pursuit of turnkey Industry 4.0 deals. Open RAN trials broaden the vendor pool, letting software specialists nibble at incumbents’ base-band share. A Japanese greenfield carrier showcased 40% capex savings with a cloud-native network, prompting emerging-market entrants to weigh similar economics.

Device ecosystems accelerated after a leading chipset supplier unveiled a Release 18 modem supporting ambient IoT and XR enhancements. Sub-USD 300 standalone-capable handsets appeared in late 2025, shrinking affordability barriers and expanding the addressable base for 5G services. The race now tilts toward service differentiation, with slice marketplaces, private-network orchestration, and fixed-wireless gigabit offers providing levers for share defense.

5G Services Industry Leaders

Huawei Technologies Co Ltd

Verizon Communications Inc

China Mobile Ltd.

AT&T Inc.,

Telefonaktiebolaget LM Ericsson

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise and vertical-specific 5G monetization continues to open whitespace where operators can sell outcomes, such as latency, availability, and device density, rather than generic connectivity. Network slicing and private networks are key commercial mechanisms, and standardization milestones provide a roadmap for feature-driven service differentiation. In June 2026, 3GPP approved the Release 21 timeline and formally initiated foundational 6G study work (including the first 6G RAN study), while operators and vendors use 5G-Advanced upgrades to improve efficiency and enable new SLA-backed offers that depend on standalone cores, cloud RAN optimization, and edge compute integration.

Spectrum and infrastructure programs are also expanding the addressable footprint for high-capacity 5G services across sub-6 GHz and mmWave. In May 2026, Innovation, Science and Economic Development Canada outlined steps toward a 2027 mmWave auction (26 GHz and 38 GHz) and signaled a non-competitive licensing approach for portions of 26 GHz, supporting dense capacity use cases such as fixed wireless access and venue-grade services. Several operator and country-level initiatives point to continued network build activity that supports new service bundles and enterprise solutions, including Egypts Spectrum Strategy 2026 to 2030 with 410 MHz of new spectrum allocated to four mobile operators (valued at USD 3.5 billion) and India TRAIs February 2026 recommendation to reduce spectrum costs by up to 10% in exchange for deploying new unique sites in uncovered areas. These policies and capital programs connect to opportunities for managed private 5G, industry campuses, and performance-tier consumer plans that depend on mid-band densification and standalone feature activation.

Recent Industry Developments

- July 2026: Verizon began providing 5G Standalone and 4G LTE connectivity for newly manufactured BMW Group vehicles for the US market using KDDIs Global Communications Platform. The move extends 5G monetization into embedded automotive connectivity and reinforces the role of platform partnerships in scaling cross-border device onboarding and lifecycle connectivity management.

- June 2026: Ericsson announced that Ericsson Private 5G became available for Verizon Business private networks internationally. This broadened Verizons addressable enterprise footprint beyond the domestic market and strengthened the packaged private-network offer model for manufacturing, logistics, and campus deployments.

- December 2025: China Mobile launched 5G-Advanced in 300 cities, combining mid-band and millimeter-wave assets to support peak-rate tiers and performance-sensitive applications such as UHD streaming and cloud gaming. The rollout helped normalize premium, feature-led pricing constructs that depend on advanced radio capabilities and tighter integration with service bundles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue earned from delivering 5G connectivity services over public and private 5G networks, including consumer and enterprise usage, and wholesale or managed service contracts that monetize 5G capacity.

The scope excludes device sales, customer premises equipment, and one-time hardware-only network build revenue from the market value.

Segmentation Overview

- By Service Type

- Enhanced Mobile Broadband (eMBB)

- Ultra-Reliable Low-Latency Comms (URLLC)

- Massive Machine-Type Comms (mMTC)

- By Network Architecture

- Non-Standalone (NSA) 5G

- Standalone (SA) 5G

- By Frequency Band

- Low-Band (Less than 1 GHz)

- Mid-Band (1- 6 GHz)

- Millimetre-Wave (Greater than 24 GHz)

- By End-User Industry

- IT and Telecom

- Media and Entertainment

- Automotive and Mobility

- Energy and Utilities

- Aerospace and Defense

- Manufacturing

- Healthcare

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by anchoring the market to public rollout and adoption signals, and then mapping them to service revenue pools. We reviewed sources such as the ITU for telecom indicators, the GSMA for subscription and coverage context, the OECD for comparable broadband metrics, and the FCC plus the European Commission for licensing and policy direction.

To keep assumptions grounded, we also checked operator annual reports, earnings transcripts, and investor decks for pricing, ARPU direction, and 5G monetization statements. Where needed, a paid subscription for company financials and intelligence and a patent database were used to cross-check technology focus and timing for new service models. These desk sources are not exhaustive, and we relied on additional public references for data collection, validation, and study clarifications.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with telecom operators, network and managed service providers, enterprise connectivity decision-makers, and ecosystem specialists who track 5G adoption. For a global view, conversations were balanced across APAC, EMEA, and the Americas to confirm pricing paths, uptake by service type, and the pace of standalone core and slicing commercialization.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 39% |

| Mid tier: 43% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 18% | Managers: 56% | Americas: 26% |

Market-Sizing & Forecasting

The core build uses a top-down approach where adoption and usage indicators are converted into service revenue by applying pricing and monetization logic that matches how 5G is sold. In practice, subscriber and enterprise connection growth, coverage and population reach, standalone versus non-standalone migration, and data traffic intensity are tracked, and then translated into service revenue using ARPU and service attach assumptions.

To keep totals grounded, selective bottom-up checks are used, such as sampling operator 5G revenue disclosures, validating enterprise contract ranges for private 5G and managed slices, and stress-testing implied revenue per user against country-level affordability and competitive intensity. When direct disclosure is missing, gaps are handled using peer benchmarking within similar tariff structures and rollout maturity, followed by adjustment after primary feedback. Forecasts are developed using scenario analysis supported by expert expectations on price compression, capacity additions, and enterprise adoption timing, and then the scenarios are reconciled into a single base case.

Data Validation & Update Cycle

Validation is done by triangulating the modeled market value against independent signals such as 5G subscription counts, network coverage milestones, and operator service revenue direction, which helps confirm that growth is not overstated in any one region. Outliers are reviewed at the country and operator-cluster level, and assumptions are rechecked when implied ARPU or enterprise contract values drift away from what interviews indicate.

Before sign-off, the model goes through multi-step analyst reviews where key inputs, conversions, and currency treatment are checked again, followed by a final consistency pass across years. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major spectrum auctions, sharp pricing shifts, or a step-change in standalone core adoption. Right before delivery, a fresh data pass is run so the view reflects the latest public releases.

Mordor Intelligence's 5g Services Market Size Compared Against Other Published Estimates

Published market values for 5G services can look far apart, even when the topic label is the same, because the boundary around what counts as service revenue is not always consistent. Differences also come from how quickly models are refreshed, how currency conversion timing is handled, and how service pricing is allowed to move as markets mature.

In a refresh-led read of the numbers, the spread usually widens when a study locks earlier FX rates, assumes aggressive ARPU uplift without checking tariff resets, or counts adjacent items like hardware-heavy build spend inside services. The approach used by Mordor Intelligence relies on frequent cross-checks to recent operator disclosures and a consistent currency timing rule, then adjusts ASP and ARPU paths using primary validation so short-term volatility does not distort the base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 130.46 B (2025) | |

| Global Consultancy A | USD 196.42 B (2025) | Uses an earlier base year build and applies rapid pricing uplift assumptions, which can inflate the 2025 bridge when later tariff compression is not reflected evenly across regions. |

| Industry Publisher B | USD 208.86 B (2025) | Applies a fast-growth curve with broad service inclusion and less visible currency timing choices, which can raise the base year when conversion points and validation checks are not aligned to the same reporting windows. |

The table indicates the gap is mainly explained by pricing-path treatment and the timing of FX and base year refresh, rather than a disagreement that 5G adoption is growing. When the scope is kept to service revenue and assumptions are rechecked against recent disclosures and interview feedback, the resulting market size stays easier to trace and update year after year.

Key Questions Answered in the Report

How fast is revenue expected to grow for 5G service providers between 2026 and 2031?

Global revenue is projected to expand at a 19.1% CAGR from USD 133.73 billion in 2026 to USD 320.48 billion by 2031.

Which region will be the quickest to scale enterprise 5G adoption?

The Middle East is forecast to post a 20.01% CAGR to 2031, supported by greenfield standalone rollouts and sovereign digital programs.

Why are operators moving from Non-Standalone to Standalone cores?

Standalone networks enable guaranteed-latency network slices, voice-over-NR, and edge-compute monetization, benefits not possible over LTE-anchored Non-Standalone architectures.

What is driving manufacturing demand for private 5G networks?

Factories use deterministic latency to coordinate autonomous robots, real-time quality control, and predictive maintenance, yielding double-digit productivity gains.

How are spectrum policies affecting deployment timelines?

Harmonized mid-band auctions accelerate build-outs, while delays or high reserve prices in parts of Africa and South America postpone investment and coverage expansion.

Page last updated on: