5G Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Volume (2026) | 7.42 Billion units |

| Market Volume (2031) | 14.56 Billion units |

| Growth Rate (2026 - 2031) | 14.43% CAGR |

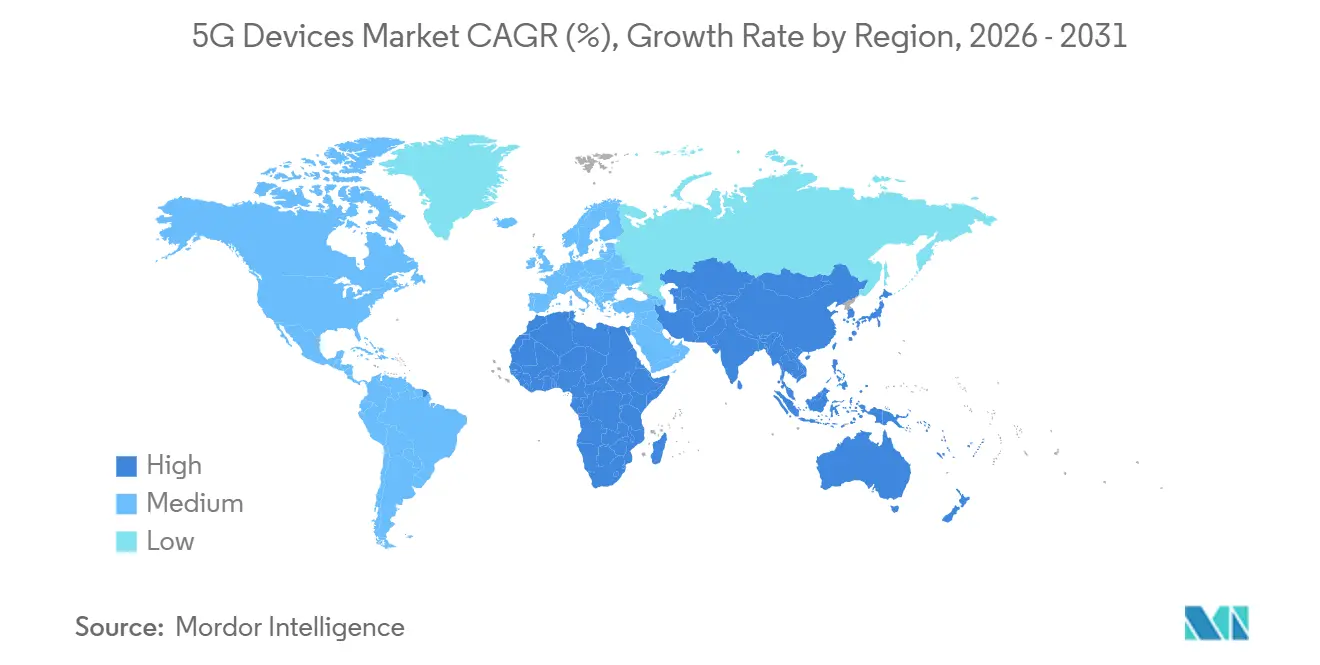

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

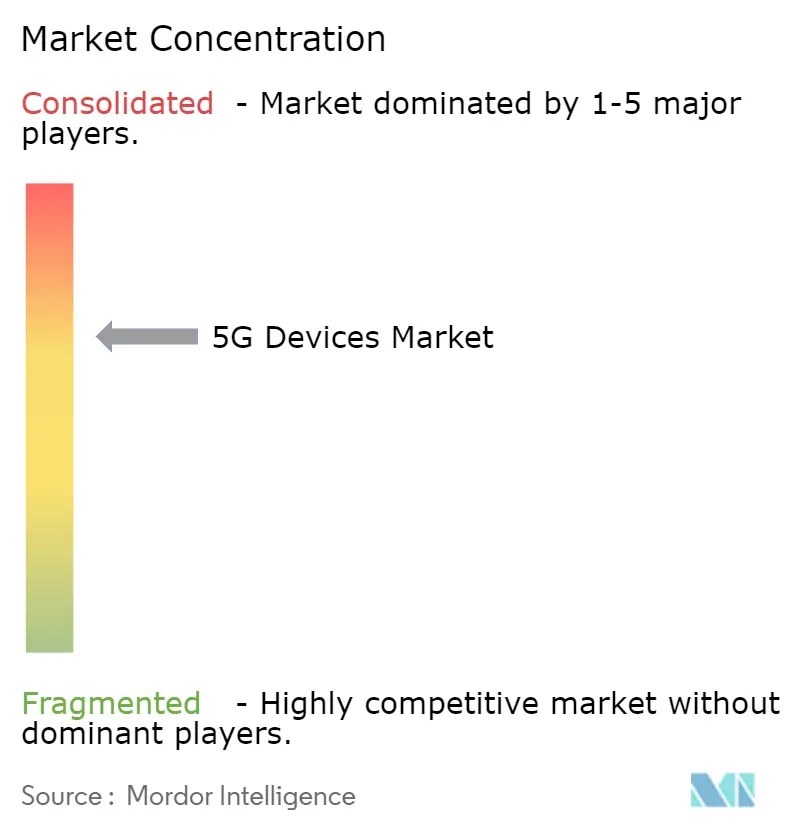

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G Devices Market Analysis by Mordor Intelligence

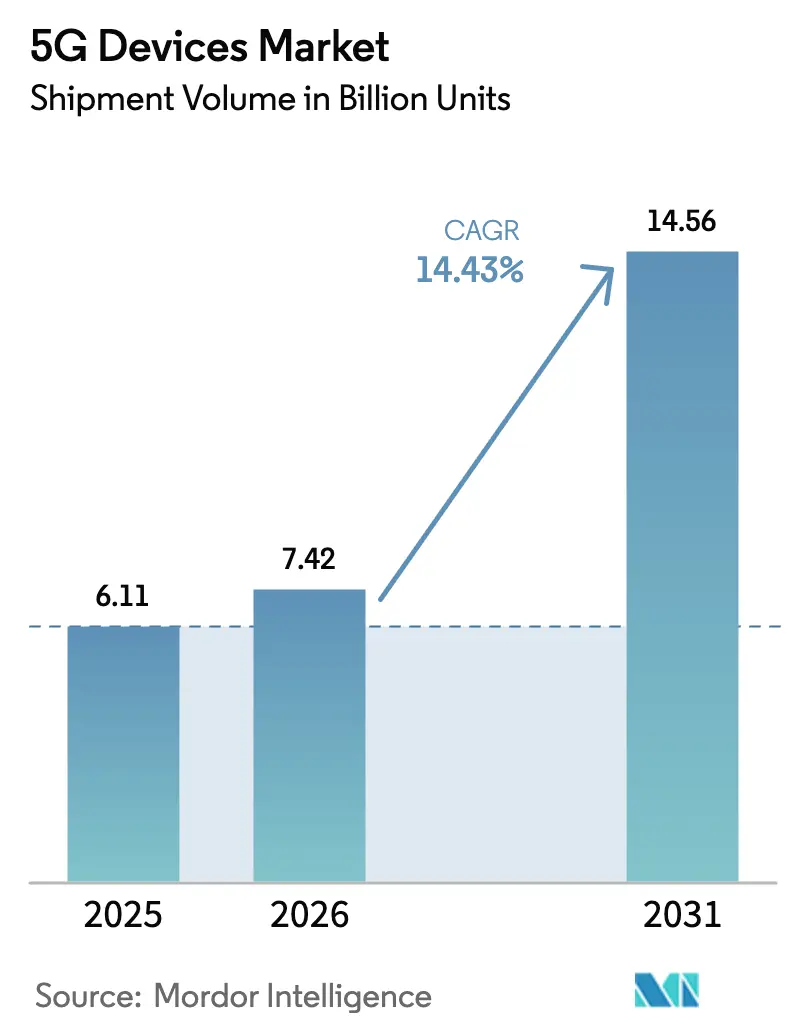

The 5G Devices market size in terms of shipment volume is expected to grow from 6.11 billion units in 2025 to 7.42 billion units in 2026 and is forecast to reach 14.56 billion units by 2031 at 14.43% CAGR over 2026-2031. Volume growth reflects falling chipset costs, wider carrier subsidies, and an accelerated rollout of enterprise private networks. Sub-6 gigahertz radios dominate mainstream demand because they balance coverage, cost, and power efficiency, while mmWave integration remains a premium feature reserved for fixed-wireless gateways and flagship smartphones. Wearables and extended-reality products are expanding faster than handsets as insurers, employers, and content platforms demand continuous connectivity. Geographically, Asia-Pacific accounts for more than half of shipments as Chinese and Indian manufacturing ecosystems compress bill-of-materials costs. Chipset competition keeps mid-tier prices low, yet the scarcity of gallium nitride and silicon germanium substrates periodically disrupts the premium mmWave supply.

Key Report Takeaways

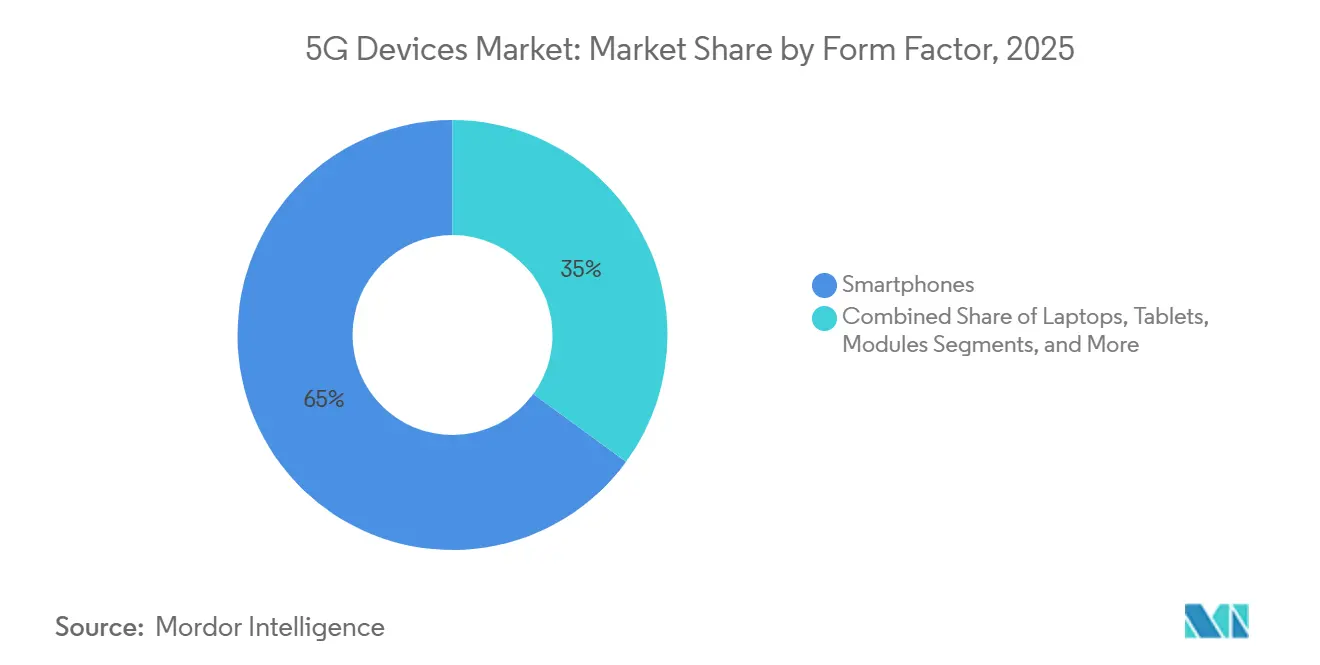

- By form factor, smartphones commanded 64.96% of the 5G devices market in 2025, whereas wearables and extended-reality hardware are forecast to rise at a 15.52% CAGR through 2031.

- By spectrum, sub-6 GHz products secured 58.22% of the 5G device market share in 2025, while mmWave hardware is set to grow at 14.86% annually as densification accelerates.

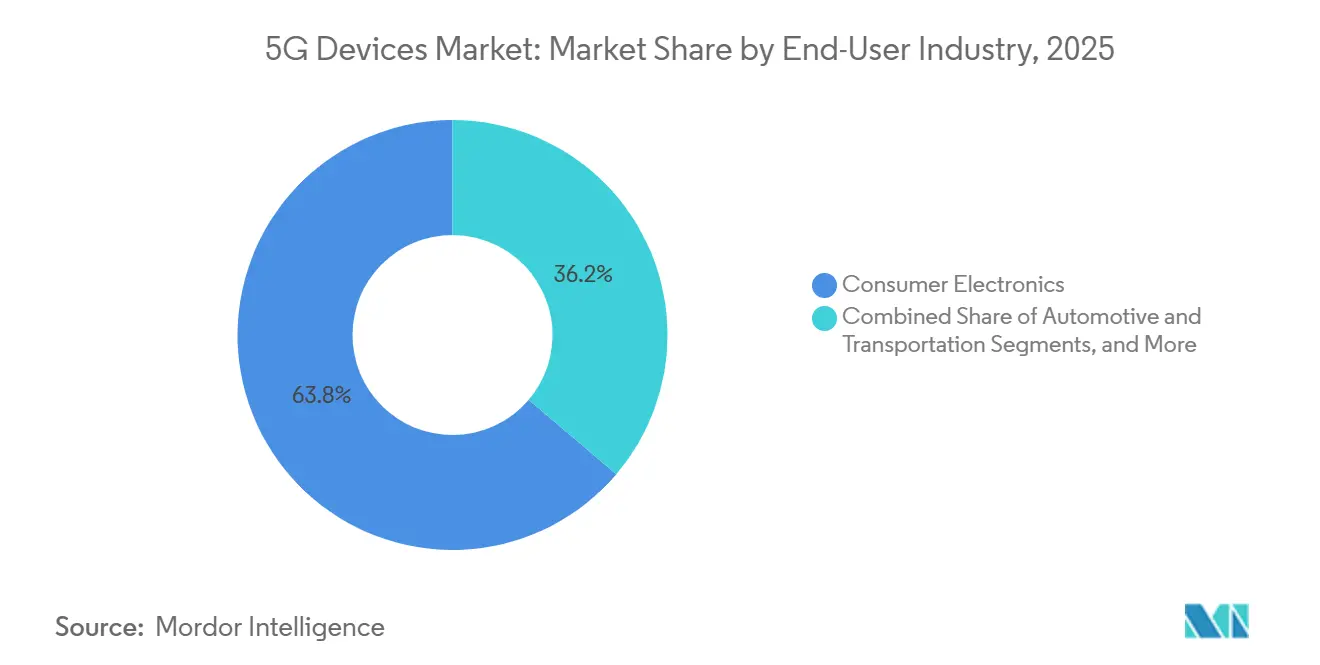

- By end-user industry, consumer electronics led with 63.78% share in 2025; automotive and transportation applications are poised for the fastest 15.11% CAGR through 2031.

- By application, enhanced mobile broadband held 55.06% share in 2025, whereas ultra-reliable low-latency communications devices will expand at 15.94% to 2031.

- By geography, Asia-Pacific captured 55.73% of shipments in 2025; the Middle East will be one of the quickest-growing region at a 16.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 5G Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Mobile-Data Demand in Emerging Economies | +3.2% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Declining ASP of 5G Chipsets and RF Front-Ends | +2.8% | Global, with acute effects in India, Southeast Asia, Latin America | Short term (≤ 2 years) |

| Aggressive Carrier Device-Subsidy Programs | +2.1% | North America, Europe, China | Short term (≤ 2 years) |

| Enterprise Private-Network Roll-Outs | +1.9% | Global, early gains in Germany, United States, Japan | Medium term (2-4 years) |

| Regulatory Spectrum-Sharing Models (CBRS, UK LSA) Catalysing Industrial Devices | +1.6% | North America and Europe, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Multi-Access Edge AI Chips Enabling Ultra-Low-Power 5G Wearables | +1.5% | Global, premium-segment concentration in North America, Europe, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Mobile-Data Demand in Emerging Economies

Monthly data consumption per user in India surpassed 20 gigabytes in 2025, driven by cloud gaming, augmented-reality filters, and real-time translation tools that require latency under 100 milliseconds. Although global 5G coverage reached 55%, penetration in low-income nations was only 4%, so affordability rather than infrastructure dictated adoption. Carriers responded with financing schemes that lowered upfront handset costs, prompting brands to release sub-USD 150 smartphones trimmed of high-end features. This dynamic expanded the 5G device market beyond early adopters, even as margins tightened. The result is a broadening unit base that underpins double-digit shipment growth.

Declining ASP of 5G Chipsets and RF Front-Ends

Qualcomm’s Snapdragon 4-series average selling price dropped 22% year over year in fiscal 2024, mainly because MediaTek discounted Dimensity 6000 processors. GaAs power amplifiers for sub-6 gigahertz bands fell below USD 2 per unit in 2025, down from USD 3.50 in 2022.[1]Semiconductor Industry Association, “2024 State of the U.S. Semiconductor Industry,” SIA, semiconductors.org As a result, the bill-of-materials premium for 5G over 4G fell below USD 15, dismantling the largest barrier to mass-market adoption. MmWave front-end modules still cost USD 12-18, confining that band to premium devices. Even so, falling core silicon prices widen the 5G devices market by making entry-level models affordable in emerging economies.

Aggressive Carrier Device-Subsidy Programs

Verizon spent USD 1.2 billion on handset subsidies and promotional credits in 2024, 17% more than in 2023, to push subscribers onto unlimited 5G plans.[2]Verizon Communications, “2024 Annual Report,” Verizon, verizon.com T-Mobile reported that 68% of 2024 activations involved trade-in or installment forgiveness that lowered consumer out-of-pocket costs by up to USD 500. In China, China Mobile co-funded 12 million rural smartphones with local brands. These programs compress carrier margins but accelerate refresh rates, helping the 5G devices market sustain mid-teens volume growth even in saturated regions.

Enterprise Private-Network Rollouts

More than 700 private 5G networks were operational worldwide by late 2024, with manufacturing sites accounting for 38%. Germany alone issued 174 local spectrum licenses to enterprises, enabling Bosch and Siemens to deploy on-premises ultra-reliable low-latency infrastructure. Industrial buyers prioritize uptime and deterministic performance over raw throughput, so they accept higher device prices for ruggedized routers and modules. As factories, logistics hubs, and energy assets digitize, these specialized deployments enlarge the 5G devices market beyond consumer endpoints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Volatility for RF Semiconductors | -1.8% | Global, acute in North America and Europe for mmWave deployments | Short term (≤ 2 years) |

| Patchy mmWave Coverage Outside Dense Urban Zones | -1.4% | Global, most severe in rural North America, Europe, and emerging markets | Medium term (2-4 years) |

| E-Waste Regulations Restricting Rapid Handset Refresh | -1.1% | Europe, North America, pilot programs in Japan and South Korea | Long term (≥ 4 years) |

| Cross-Border Security Certifications Delaying Industrial Routers | -0.9% | Global, friction points at North America-Europe and Asia-Pacific regulatory boundaries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility for RF Semiconductors

Gallium-nitride wafer shortages pushed RF front-end lead times to 30 weeks in 2024, compared with 14 weeks for baseband silicon.[3]IEEE Spectrum Editors, “The Semiconductor Supply Chain Crisis,” IEEE Spectrum, spectrum.ieee.org Only three fabs worldwide can mass-produce gallium-nitride-on-silicon-carbide substrates, so premium mmWave gear often reaches stores late. Original equipment manufacturers mitigate risk by shipping dual stock-keeping units: volume sub-6 gigahertz models and limited mmWave variants. The bifurcation blunts the overall 5G devices market CAGR until new fab capacity comes online.

Patchy mmWave Coverage Outside Dense Urban Zones

MmWave 5G covered less than 8% of the global land area in 2024, clustered in city centers, stadiums, and transit hubs. Consumers who pay USD 100 premiums for hybrid phones experience gigabit speeds only occasionally, which dampens their willingness to upgrade. Operators redirect capital toward sub-6 gigahertz “nationwide 5G,” which offers broader reach but fewer ultra-low-latency advantages. Until coverage widens, mmWave device growth remains confined to fixed-wireless gateways and enterprise hotspots, slowing the high-margin slice of the 5G devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form Factor: Smartphones Hold Volume, Wearables Lead Growth

Smartphones accounted for 64.96% of shipments in 2025, underscoring their central role as primary access devices for more than 4.5 billion users worldwide. Yet replacement intervals lengthened to 31 months in 2025, signaling maturation. Wearables and extended-reality hardware are on a 15.52% CAGR path to 2031, lifted by insurer wellness incentives and workplace safety mandates. Apple reported that cellular-enabled watches formed 38% of its wearable mix in 2024, up from 22% in 2022.[4]Apple Inc., “Form 10-K 2024,” Apple, apple.com Customer-premises equipment for fixed wireless has risen with rural broadband initiatives, while industrial routers priced at USD 500-1,200 thrive in harsh-environment deployments. Modules, critical for machine-to-machine automotive and metering links, scale in parallel with the Internet of Things.

Growth leadership shows why pocket-centric demand is plateauing while body-worn and ambient endpoints surge. Augmented-reality glasses lower maintenance errors in factories by overlaying instructions in workers’ fields of view. However, battery anxiety persists because users expect multi-day endurance on wrist and eyewear devices. Continuous silicon advances that push power draw below 300 milliwatts therefore remain decisive for form-factor migration. As these advances materialize, the 5G devices market will rely less on handsets for its next 7 billion-unit expansion.

By Spectrum Support: Sub-6 Gigahertz Dominance Continues

Sub-6 gigahertz radios captured 58.22% share in 2025 since they deliver 300-600 megabits per second across kilometer-scale cells at front-end costs below USD 6. MmWave shipments grow at 14.86% but start from a lower base because modules cost USD 12-18 and require network densification that is still underway. Hybrid devices that combine both bands represented 18% of 2025 smartphones, catering to early adopters keen on peak speeds. Carriers must install 10-15 times more mmWave small cells than sub-6 gigahertz sites to match signal reach, a heavy capital burden that delays ubiquitous coverage.

Momentum favors sub-6 gigahertz for nationwide availability, with mmWave reserved for stadiums, airports, and high-density downtown corridors. Consequently, sub-6 gigahertz hardware will stay the volume backbone of the 5G devices market while mmWave targets premium tiers. Once densities rise and front-end prices fall, the share of mmWave could approach 30% by 2031, but its upside hinges on solving both infrastructure and component supply bottlenecks.

By End-User Industry: Automotive Accelerates

Consumer electronics held 63.78% unit share in 2025, but automotive and transportation endpoints are projected to log a 15.11% CAGR through 2031. The European Union mandated cellular vehicle-to-everything capabilities for new passenger cars sold after July 2024, spawning a captive pipeline for 5G modules. Qualcomm disclosed design wins with 18 automakers for its Snapdragon Ride platform in 2024. Industrial sites invest in ruggedized routers that ensure uptime in vibration-prone environments, while healthcare adoption remains gradual due to lengthy medical approvals. Energy and utilities shift smart meters from 2G and 3G to 5G as legacy networks phase out.

As vehicles morph into software-first products, over-the-air updates and predictive maintenance hinge on reliable cellular networks. Tesla’s 2024 filing noted revenue from post-sale software features enabled via 5G connectivity. Automotive certification cycles stretch 18–24 months, slowing refresh but ensuring long-term module demand. As connectivity becomes standard across mass-market models, the 5G devices market will benefit from large yet predictable unit shipments over a decade-long vehicle life.

By Application: URLLC Gains Momentum

Enhanced mobile broadband owned 55.06% of demand in 2025 due to video and social media consumption. Ultra-reliable low-latency communications devices will rise at 15.94% annually through 2031 as factories automate and surgeons pilot remote procedures. Private network slicing enables enterprises to allocate deterministic bandwidth to mission-critical robots. Massive machine-type communications grows more slowly because LTE-M already covers many low-throughput IoT use cases. Fixed wireless accounted for 12% of new U.S. broadband lines in 2024, demonstrating that 5G can substitute for wireline in rural areas.

Network slicing reached commercial readiness only in 2024, so most URLLC devices connect to campus networks rather than public carriers. This two-track model separates consumer broadband gear from industrial equipment with separate certification, supply chains, and service contracts. As slicing matures, wider carrier services will expand the market for 5G devices to address latency-sensitive endpoints.

Geography Analysis

Asia-Pacific shipped 55.73% of global units in 2025, buoyed by China’s 420 million-device output and India’s production-linked incentive program that drew USD 15 billion in assembly investments. Japan and South Korea punch above their volume-based rank by owning 40% of the premium tier above USD 1,000. Southeast Asian markets expand rapidly on sub-USD 300 handsets, whereas Australia and New Zealand see 36-month cycles that temper growth. Localized component ecosystems give Asia-Pacific up to 30% cost advantages versus Europe and North America, locking in its leadership of the 5G devices market.

The Middle East is one of the fastest risers, with a 16.01% CAGR to 2031. Saudi Arabia allocated USD 20 billion to 5G smart-city projects under Vision 2030, and the United Arab Emirates achieved 95% population coverage in 2024. Device uptake lags network rollout because average selling prices remain high; continued chipset cost erosion will unlock the next leg of adoption.

North America and Europe face countervailing forces: mature 5G footprints coexist with regulatory pressures that slow handset churn. The European Union tightened e-waste rules in 2023, adding end-of-life fees of USD 2-5 per phone. U.S. right-to-repair debates encourage longer use, holding region-wide CAGR to low double digits. South America and Africa together account for 12% of shipments, though fixed wireless presents a mid-term leapfrog path in underserved rural areas.

Regulatory Landscape

5G devices operate under a layered regime in which global technical baselines set the reference frame, and national authorities translate them into spectrum licensing, equipment approvals, and security or environmental compliance requirements. In early 2026, the ITU advanced IMT-2020 specifications and convergence guidance through approvals including ITU-R M.2150-3 (February 2026) for terrestrial radio interfaces and ITU-T Recommendations Q.5016 and Q.5035 (January 2026) covering fixed, mobile, and satellite convergence signaling and IMS interconnection. These updates feed into chipset, modem, and device certification targets across regions.

At the national level, regulators are both expanding the addressable spectrum pipeline and tightening operating conditions for higher-capacity networks, which shapes device feature roadmaps. TRAI issued final recommendations in February 2026 covering auction of IMT-identified bands from 800 MHz up to 26 GHz and adding newly identified mid-band ranges (including 6425-6725 MHz and 7025-7125 MHz), supporting sub-6 and higher-band device development. In May 2026, Innovation, Science and Economic Development Canada outlined steps toward a 2027 mmWave auction in the 26 GHz and 38 GHz bands, along with an additional 850 MHz in 26 GHz via non-competitive licensing, a direct input for planning mmWave-capable CPE and premium handsets. In parallel, the US NTIA progressed federal-to-commercial repurposing in the 2.7 GHz band as part of a broader spectrum reallocation mandate.

Value Chain Analysis

The 5G devices value chain starts with IP and standards inputs (3GPP and ITU), moves through RF and baseband silicon, power management, memory, displays, cameras, and sensors, and then reaches device OEM design, manufacturing (EMS/ODM), certification, and multi-channel distribution via carriers, retailers, and enterprise integrators. Value capture tends to concentrate in application processors, modems, and RF front ends, where Qualcomm and MediaTek are central, while downstream differentiation increasingly shows up in device software stacks and enterprise management for routers, gateways, and modules. The ecosystem breadth continues to widen, with the global device ecosystem tracking thousands of 5G devices across dozens of form factors (as recorded by GSA by December 2025).

Supply reliability and regionalization are increasingly visible determinants of cost and availability, especially for RF materials and mature-node semiconductors used in power management and RF transceivers. On the upstream side, Apple announced a multiyear USD 30 billion commitment with Broadcom in July 2026 to produce large volumes of US-made components such as FBAR filters in Fort Collins, Colorado, backed by reported USD 1.5 billion in capital expenditure, highlighting efforts to secure critical RF content. In India, localization spans multiple chain nodes, from Ericsson commercial releases of made-in-India antennas from VVDN Technologies (June 2025) to operator-led moves such as Reliance Jio deploying locally manufactured 5G small cells via a Sanmina joint venture (May 2025), and packaging capacity additions such as CG Power inaugurating an OSAT facility in Sanand, Gujarat (July 2026) with partners including Renesas Electronics and Stars Microelectronics. Manufacturing test and compliance capabilities also remain enabling links, including LitePoint and Pegatron initiating volume manufacturing of 5G O-RAN radio units using test solutions aligned to 3GPP 38.141 (May 2025), reinforcing the role of validation, calibration, and conformance testing in scaling device shipments.

Competitive Landscape

Chipset makers and smartphone original equipment manufacturers dominate value capture, while module, router, and customer-premises equipment vendors operate on slimmer margins. Qualcomm and MediaTek together hold 65% of application processor units, but MediaTek’s cost advantage yielded a 51% share of India’s 2024 5G chipset market. Apple and Samsung, through vertical integration, command 45% of global smartphone gross profit on a 22% unit share. Chinese brands led by Xiaomi, OPPO, and Vivo win volume tiers by leveraging domestic supply chains that shave 8-10 percentage points off bill-of-materials cost versus global peers.

White-space segments, such as intrinsically safe handhelds for oil rigs and ISO 26262-certified automotive modules, remain fragmented. Fibocom secured functional-safety approval in 2024, opening telematics opportunities beyond infotainment. Patent filings at ETSI show that Ericsson and Nokia lead in ultra-reliable low-latency communications intellectual property and aim to monetize it via licensing rather than hardware. As chipset prices converge, differentiation migrates to software ecosystems, cloud integrations, and enterprise management platforms.

The competitive outlook therefore splits the 5G devices market into high-margin premium ecosystems controlled by vertically integrated giants and a commoditized volume base where scale and efficient supply chains decide winners.

5G Devices Industry Leaders

Apple Inc.

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

Xiaomi Corp

Guangdong OPPO Mobile Telecommunications Corp., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most direct near-term whitespace for incremental device shipments and mix improvement is linked to the shift from non-standalone 5G to 5G Standalone (SA) and the commercialization of slicing and 5G-Advanced capabilities, which drive new device certifications, modem feature adoption, and enterprise-grade endpoints. As of April 2026, GSA reported 95 operators had launched 5G SA services (up sharply since 1Q25), and 35 operators were investing in 5G-Advanced, while June 2026 reporting referenced dozens of live network slicing offerings globally. This transition expands the opportunity beyond smartphones into industrial routers and gateways for URLLC use cases, fixed wireless access CPE for capacity upgrades, and modules designed for deterministic connectivity profiles in private networks.

Operator investment and upgrade programs add a measurable demand pull for SA-capable devices and RF content, particularly where radio upgrades run alongside fiber and site densification. In the United Kingdom, Virgin Media O2 signed multiyear agreements with Ericsson and Nokia in March 2026 to upgrade the RAN across thousands of sites to support 5G Standalone (5G+), and later confirmed a 2026 network investment program that includes capacity upgrades and expanded SA coverage. In the United States, T-Mobile outlined a 2026 capital plan focused on 5G standalone core evolution, 5G-Advanced, and network slicing, aligning with device categories that monetize SA features, including premium smartphones, hotspots, and enterprise equipment. In India, Bharti Airtel announced a 2026 capex plan tied to adding 5G sites and expanding fiber-to-the-home capacity, which supports demand for cost-optimized sub-6 devices and fixed wireless gateways as coverage and backhaul improve.

Recent Industry Developments

- July 2026: Apple announced a multiyear USD 30 billion commitment with Broadcom to design and produce custom US-made components, including FBAR filters, backed by reported capital investment in Fort Collins, Colorado. Securing RF front-end supply at scale supports higher-volume 5G device builds and reduces exposure to component bottlenecks in premium radio configurations.

- September 2025: Apple introduced Apple Watch SE 3 and Apple Watch Series 11 with 5G cellular capabilities. The update broadens the addressable base for always-connected wearables and reinforces the shift of incremental 5G unit growth toward body-worn devices rather than handsets alone.

- July 2024: Huawei launched its first commercial 5.5G (5G Advanced) version, Apollo, based on 3GPP Release 18. This milestone accelerated vendor roadmaps around 5G-Advanced features that influence modem capability requirements and the upgrade cycle for CPE and other high-performance 5G endpoints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the 5G devices market is defined as shipments of end devices that connect over 5G networks, counted in units across consumer and enterprise use worldwide. We treat the market as device shipments in the year, and not as service revenue.

Scope exclusions: We exclude 5G network infrastructure equipment and carrier services, and we also do not count replacement parts sold after the initial device shipment.

Segmentation Overview

- By Form Factor

- Smartphones

- Customer-Premises Equipment (Indoor / Outdoor)

- Industrial Grade Routers / Gateways

- Modules

- Laptops/Tablets

- Hotspots

- Wearables and XR Devices

- By Spectrum Support

- Sub-6 GHz

- mmWave

- Hybrid (Sub-6 GHz + mmWave)

- By End-User Industry

- Consumer Electronics

- Industrial and Manufacturing

- Automotive and Transportation

- Healthcare

- Energy and Utilities

- Enterprise/Commercial

- By Application

- Enhanced Mobile Broadband (eMBB)

- Ultra-Reliable Low-Latency Comms (URLLC)

- Massive Machine-Type Comms (mMTC)

- Fixed Wireless Access

- Vehicle-to-Everything (V2X)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market and to anchor assumptions that are hard to learn only through interviews. We typically refer to public sources such as the ITU for spectrum and 5G policy context, GSMA for mobile ecosystem indicators, OECD for telecom and digital economy series, and the World Bank for macro variables that influence device affordability and upgrade cycles.

To cross-check adoption signals, we also review device ecosystem trackers and standards releases from 3GPP, along with company filings, investor presentations, and credible press coverage on launches, pricing moves, and channel availability. Where needed, paid subscription databases are used for company financials and news screening, and patent databases are referenced to understand where device feature roadmaps are moving. These examples are not exhaustive, and other public sources were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating shipment logic by device category and checking the pace of 5G capability expansion across price tiers. We spoke with a mix of device ecosystem participants and channel-facing roles, and we also used surveys to pressure-test assumptions on upgrade intent, availability of 5G models, and the split between sub-6 GHz and mmWave support across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 41% |

| Mid tier: 45% | Functional/Unit leaders: 26% | EMEA: 37% |

| Smaller Players: 19% | Managers: 59% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the total 5G device shipment pool by linking 5G subscriber additions, network coverage readiness, and device replacement cycles, and then translating those signals into units shipped. To keep the totals realistic, we corroborate results with selective bottom-up approximations such as sampled ASP x volume checks by major form factors, along with channel discussions that help adjust for timing gaps.

Key inputs used in the model include the pace of 5G network rollouts and mid-band availability, the mix shift from 4G to 5G in entry and mid-range devices, the split between sub-6 GHz and mmWave capable models, and form factor adoption patterns like CPE for fixed wireless access versus smartphones. When data is sparse for smaller categories, we apply conservative penetration curves and then validate directionally with interview feedback before locking the totals.

Forecasting is run using scenario analysis supported by trend smoothing, where device shipment growth is tied to a small set of drivers that can be tracked each year, and then refined with what experts expect for pricing and availability. The final forecast is adjusted only when multiple signals line up, so the model remains repeatable for future refreshes.

Data Validation & Update Cycle

Validation is done through a series of cross-checks where we compare model outputs with independent demand signals, and then investigate any sharp variances before sign-off. Outliers are reviewed at the geography and form factor level, and if the shipment curve looks misaligned with rollout timing or affordability, the assumptions are reworked and rechecked.

Each deliverable goes through multi-step internal review, and respondents are re-contacted when a key assumption shifts or when new launches change the near-term mix. Reports are refreshed annually, with interim updates triggered by material events such as major spectrum changes or sudden pricing disruptions. Before delivery, an analyst performs a fresh pass to incorporate the latest public indicators so clients receive an up-to-date view.

Mordor Intelligence's 5g Devices Market Size Compared With Other Published Estimates

Published market sizes for 5G devices can look far apart because some sources measure revenue, while others track shipments, and the year choices are not always aligned. Differences also come from what is counted as a 5G device, since some studies blend devices with network equipment or include services.

Key gap drivers usually include mixing unit and USD measures, using aggressive price curves for early years, and applying adoption rates that are not tested against rollout readiness. Another common issue is currency timing, where a single-year conversion rate is applied even though device ASPs and regional mix can swing within the year, and updates are not always made after major pricing moves.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.42 B (2026) | |

| Trade Publisher A | USD 136.79 B (2024) | This figure is presented as revenue, and it also uses an earlier base year, so it is not directly comparable to a shipment-based unit model that is anchored on rollout and replacement timing. |

| Industry Brief B | USD 13.25 B (2023) | The estimate appears to apply a narrower early-stage revenue pool and a steep growth path into later years, which can undercount mainstream smartphone shipments while overstating later uplift if ASP decline is not refreshed. |

The table shows that the biggest spread is driven by mixing revenue with unit shipment sizing and by using different year anchors. Counting shipments in units, and then validating the curve using rollout readiness and device mix checks, keeps the market total traceable to repeatable inputs, a choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current shipment volume for 5G devices?

Shipments reached 7.42 billion units in 2026 and are on track for 14.56 billion units by 2031.

Which region accounts for the largest share of global shipments?

Asia-Pacific held 55.73% of unit volume in 2025 due to Chinese and Indian manufacturing scale.

Which application segment is growing the fastest?

Ultra-reliable low-latency communications devices are projected to grow at a 15.94% CAGR through 2031.

How do declining chipset prices influence adoption?

A reduction in 5G bill-of-materials premiums from USD 40–50 in 2021 to under USD 15 in 2025 has opened the mass-market tier.

Why is automotive demand accelerating?

Regulatory mandates for cellular vehicle-to-everything and long vehicle lifecycles drive a 15.11% CAGR in automotive modules.

Page last updated on: