5G New Radio Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

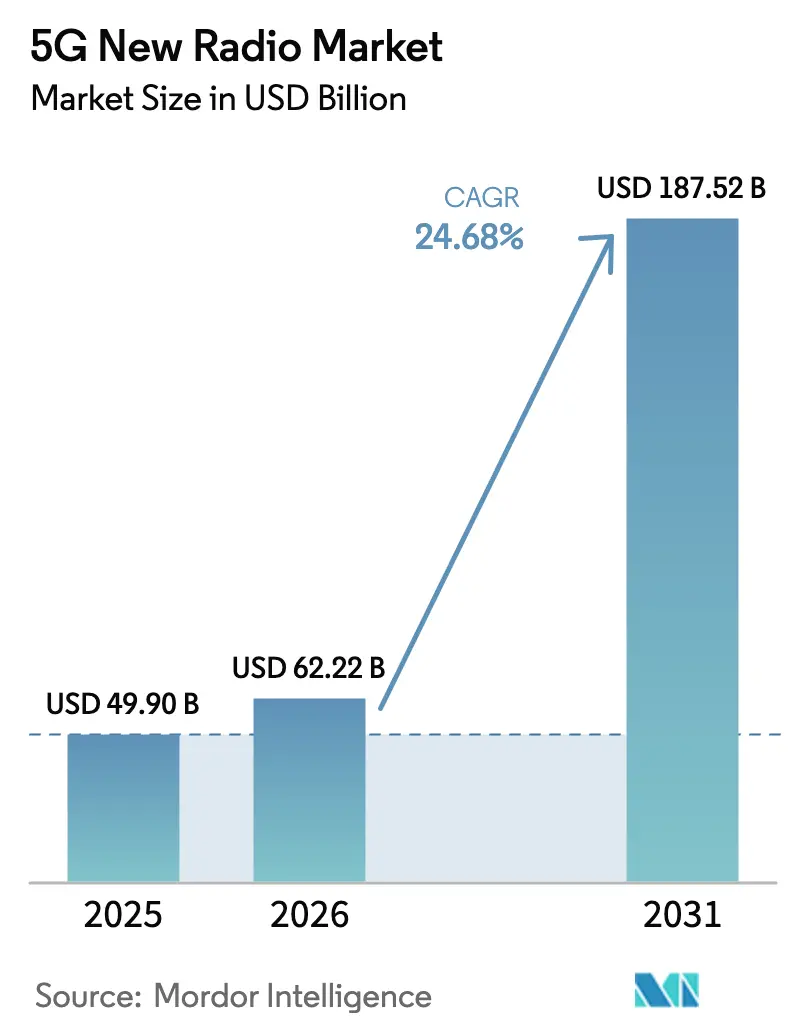

| Market Size (2026) | USD 62.22 Billion |

| Market Size (2031) | USD 187.52 Billion |

| Growth Rate (2026 - 2031) | 24.68% CAGR |

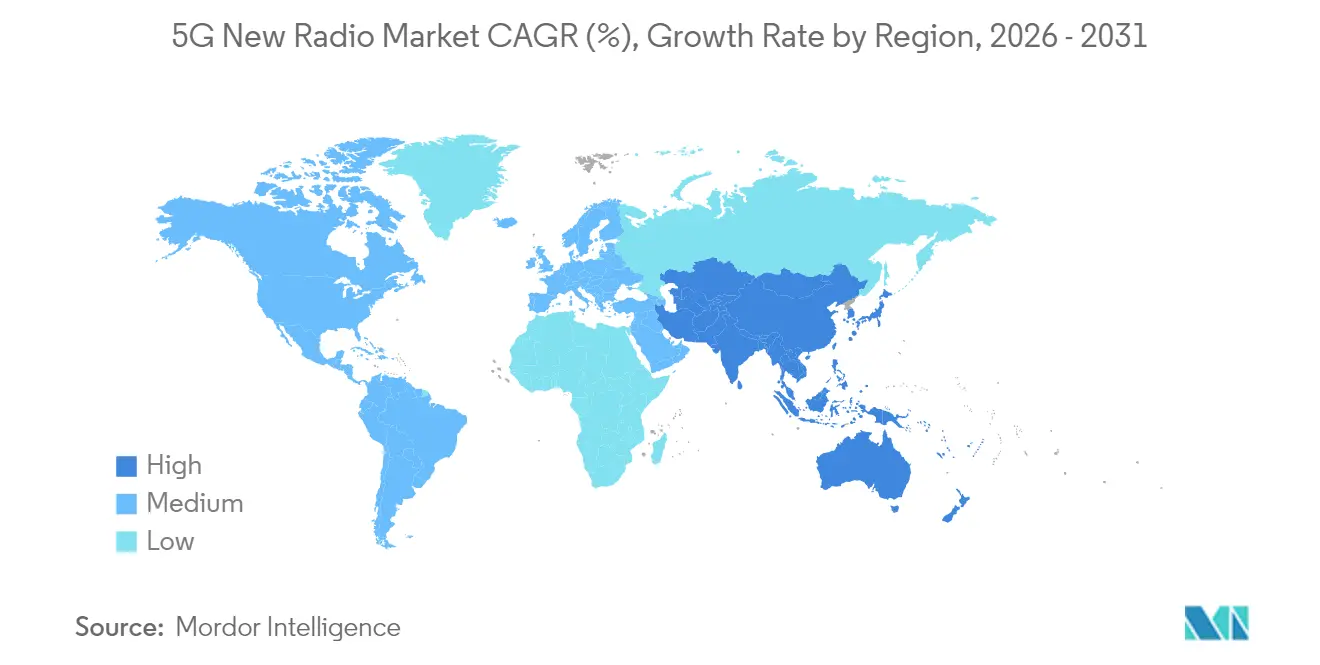

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

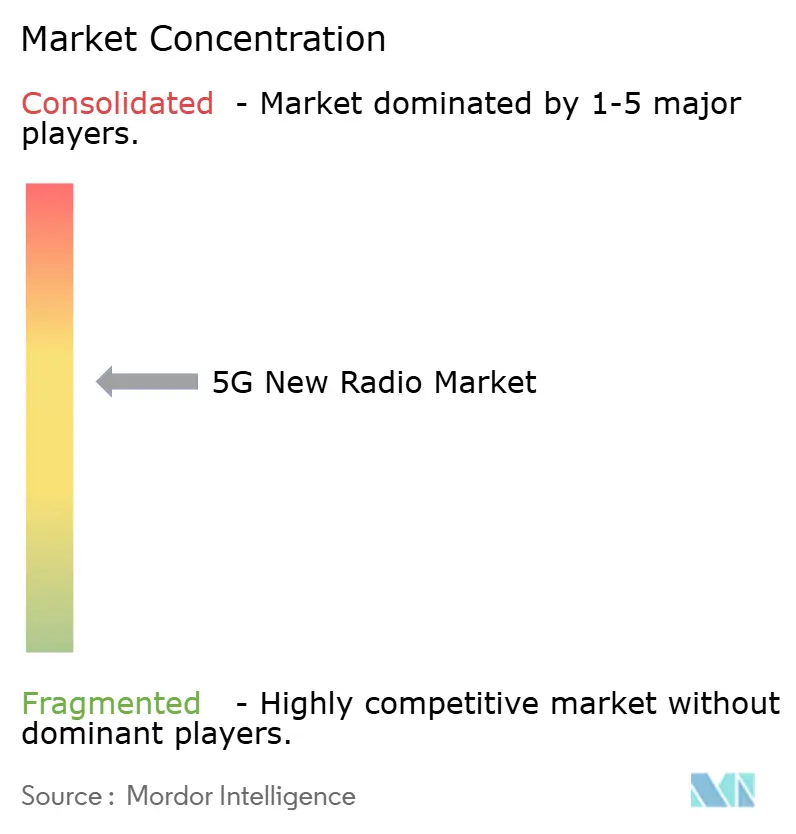

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G New Radio Market Analysis by Mordor Intelligence

The 5G New Radio Market size was valued at USD 49.9 billion in 2025 and estimated to grow from USD 62.22 billion in 2026 to reach USD 187.52 billion by 2031, at a CAGR of 24.68% during the forecast period (2026-2031). Growth rests on three structural forces: satellite-terrestrial convergence through non-terrestrial networks, expanding private-network activity in manufacturing plants, and wider spectrum access that brings extreme-band resources into commercial use. Mobile-video traffic that now exceeds 75% of all cellular data, intense enterprise digitalization mandates, and greenfield standalone rollouts reinforce the demand trajectory. As networks virtualize, software orchestration reduces operating costs and lowers time-to-market for value-added services. Meanwhile, persistent chipset shortages and heightened cybersecurity requirements in multi-vendor open-RAN environments create near-term execution challenges that operators must navigate.

Key Report Takeaways

- By frequency band, Sub-6 GHz commanded 64.12% of the 5G New Radio market share in 2025, whereas extreme-band (>40 GHz) spectrum is projected to expand at a 26.15% CAGR through 2031.

- By deployment mode, non-standalone maintained a 65.05% revenue share of the 5G New Radio market in 2025; standalone architecture is projected to record the highest CAGR at 25.6% through 2031.

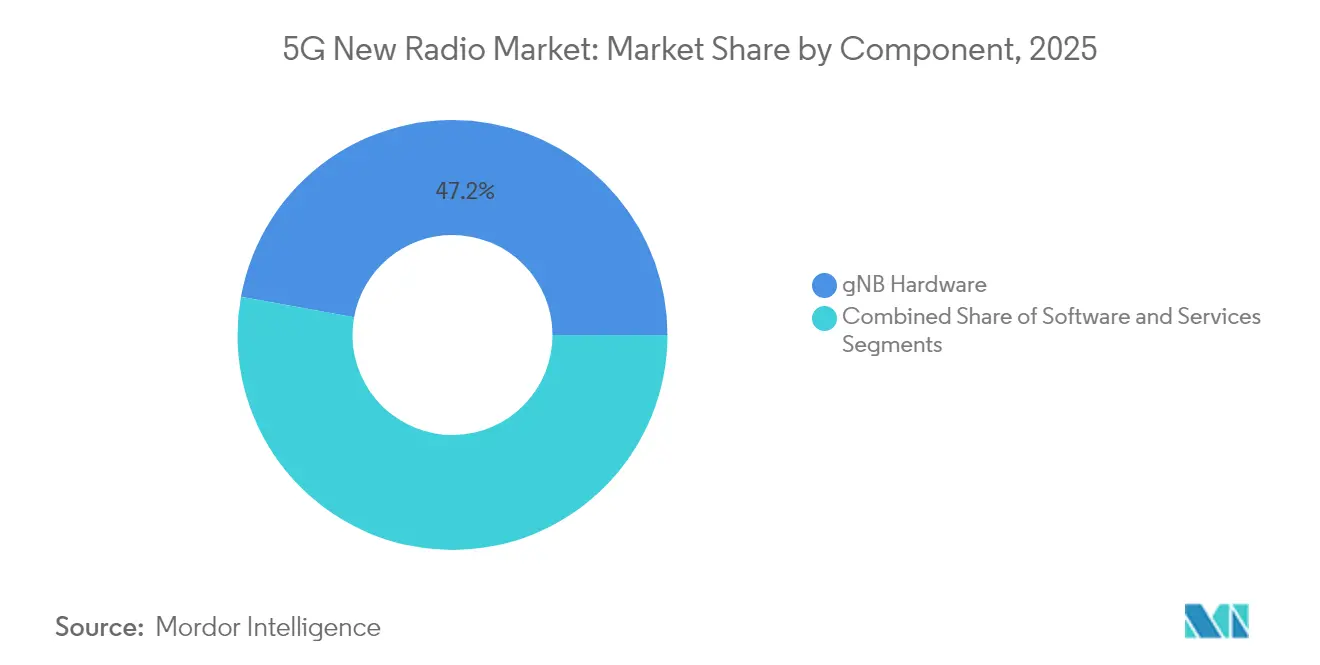

- By component, software captured 52.85% of the 5G New Radio market size in 2025 and is forecasted to grow at a 25.98% CAGR between 2026 and 2031.

- By end-user industry, the manufacturing sector is advancing at a 27.4% CAGR in the 5G New Radio market through 2031, and telecom operators captured a 57.85% share in 2025.

- By geography, North America led the 5G New Radio market with a 37.95% revenue share in 2025, while the Asia-Pacific region is expected to post the fastest growth at a 26.4% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 5G New Radio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging mobile-data traffic and video consumption | +4.2% | Global | Short term (≤ 2 years) |

| Spectrum liberalization in mid- and high-band ranges | +3.8% | Europe, North America | Medium term (2-4 years) |

| Network-virtualization-driven cost efficiencies | +3.5% | North America, Europe, and spill-over to Asia Pacific | Medium term (2-4 years) |

| Government-led industrial digitalization programs | +4.1% | Asia Pacific core, expanding to Europe and North America | Long term (≥ 4 years) |

| Private-5G demand from Industry 4.0 facilities | +3.9% | Global | Medium term (2-4 years) |

| Satellite-terrestrial 5G-NTN integration | +2.7% | Global, maritime and remote focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Mobile-Data Traffic and Video Consumption

Global 4K and 8K video streaming, augmented-reality apps, and cloud gaming platforms drove average monthly data usage per subscriber 40% higher in 2024, exhausting 4G capacity in dense urban corridors.[1]Eric Parsons, “Mobility Report November 2024,” Ericsson, ERICSSON.COM Network operators report peak-hour congestion that stresses the limits of spectral efficiency, hastening 5G migration schedules in North America, Europe, and key Asian cities. Sub-6 GHz cells enhance coverage and indoor penetration, while mmWave layers provide high-density capacity for stadiums, transport hubs, and metropolitan hotspots. Traffic forecasts that predict a threefold increase in data by 2028 underpin continued investment in carrier aggregation, massive MIMO radios, and small-cell densification. As immersive media gains mainstream adoption, operators position network slicing and edge compute resources to deliver guaranteed throughput and latency. These measures translate directly into accelerated orders for 5G New Radio market hardware and orchestration software, cementing demand visibility through the medium term.

Spectrum Liberalization in Mid-Band and High-Band Ranges

The World Radiocommunication Conference 2023 assigned the 6425-7125 MHz frequency range to International Mobile Telecommunications and affirmed contiguous 26 GHz blocks for regional regulators, unlocking new capacity for enhanced mobile broadband services.[2]ITU Radiocommunication Bureau, “WRC-23 Outcomes,” ITU.INT Harmonization reduces equipment variance, lowering radio-unit costs by up to 15% in Europe. In the United States, successive Federal Communications Commission auctions, coupled with National Telecommunications and Information Administration spectrum-sharing frameworks, have opened once-restricted military bands for commercial 5G operations. The combined policy arc supplies operators with wider channels that underpin extreme-band deployments and fixed-wireless-access rollouts. Spectrum certainty supports long-range procurement contracts, shielding vendors from boom-and-bust cycles, and sustains the 5G New Radio market through predictable, multi-year investment plans.

Network Virtualization-Driven Cost Efficiencies

Cloud-native network functions reduce operating expenditure by 30-40% compared to proprietary hardware stacks, according to trials among Tier-1 European carriers.[3]K. Maeda, “Cloud-Native RAN Economics,” Nokia, NOKIA.COM Open-RAN enables the disaggregation of radio, distributed-unit, and centralized-unit elements, allowing them to be mixed and matched across suppliers, which spurs component innovation and drives down unit prices. Automated orchestration reduces manual configuration and maintenance visits, resulting in a 25% reduction in field-service costs in 2024. Dynamic slicing permits differentiated quality-of-service tiers, unlocking fresh revenue streams ranging from enterprise SLA products to premium consumer gaming bundles. Virtualization thus creates a positive feedback loop: lower costs encourage broader coverage, which in turn enlarges the 5G New Radio market base.

Government-Led Industrial Digitalization Programs

The European Union earmarked EUR 7.5 billion (USD 8.4 billion) for 5G corridors and factory modernization under its Digital Decade initiative. Germany subsidizes up to 50% of qualified private-network expenditures to accelerate Industry 4.0 transformation, while India’s telecom policy aims to cover industrial clusters nationwide by 2026. South Korea, Japan, and China extend similar preferential financing and tax rebate schemes. Public-sector support lowers investment risk for manufacturers and accelerates proofs of concept. As pilots mature into scaled deployments, factory automation, AGVs, and real-time analytics requirements enlarge the 5G New Radio market, especially for standalone-core and edge-compute integration projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain chipset shortages beyond 2025 | -2.8% | Global, mmWave focus | Short term (≤ 2 years) |

| High total cost of ownership for greenfield standalone rollouts | -3.2% | Emerging markets, small operators | Medium term (2-4 years) |

| Regulatory delays in mmWave licensing | -1.9% | Jurisdiction-specific | Medium term (2-4 years) |

| Cyber-security concerns in open-RAN deployments | -2.1% | Global, critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Chipset Shortages Beyond 2025

Tight 7-nm and 5-nm fabrication capacity continues to constrain mmWave radio-front-end and beamform-IC supply, especially for discrete RF modules. Lead times stretched past 40 weeks in 2024, prompting operators to defer high-band deployments and prioritize mid-band rollouts. Vendor diversification reduces exposure; yet, few foundries can meet the power-efficiency profile required for extreme-band phased arrays. Component scarcity, therefore, caps peak throughput in early commercial 5G New Radio networks and tempers near-term revenue expansion in the 5G New Radio market.

High Total Cost of Ownership for Greenfield Standalone Rollouts

Full standalone coverage in low-density geographies can require USD 200-400 million in upfront capex, eclipsing projected revenue for many rural and emerging-market carriers. Fiber backhaul gaps, tower leasing fees, and core-network overhauls add further expense. Operators thus maintain non-standalone overlays that limit advanced 5G functionality and delay monetization of network slicing. Until financing vehicles or network-sharing frameworks mature, the 5G New Radio market must contend with phased implementation schedules outside Tier-1 operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Frequency Band: Extreme Spectrum Unlocks New-Use Cases

Sub-6 GHz commanded 64.12% of the 5G New Radio market in 2025 because its favorable propagation profile supports fast nationwide rollouts. The band maintains essential rural reach, indoor penetration, and cost-efficient macro-cell economics, anchoring broad coverage for consumer broadband and voice. Operators favor reallocating refarmed 1800 MHz and 2100 MHz holdings to 5G, complementing newly auctioned 3.5 GHz or C-band channels to raise capacity. The result is a balanced network design that maximizes the reuse of existing tower grids.

Extreme-band allocations above 40 GHz represent the fastest-growing slice, advancing at 26.15% CAGR as spectrum decisions mature. The 5G New Radio market size for this segment benefits from wider 800 MHz to 2 GHz channels, which deliver multi-gigabit peak speeds. Enhanced beamforming, subarray architectures, and RF-silicon process improvements enable a coverage radius of nearly 500 meters in dense urban layouts. Holographic communications, extended-reality streaming, and high-resolution sensor backhaul rely on these capacities. Regulatory harmonization across the European Union, South Korea, and parts of the United States assists vendor scale economies, trimming radio-unit costs and accelerating city-center densification projects.

By Deployment Mode: Standalone Functionality Scales

Non-standalone architecture retained 65.05% revenue share in 2025, reflecting its rapid time-to-market advantage. Leveraging 4G LTE cores, operators launched 5G radios with limited additional capex, satisfying consumer demand for higher downlink speeds. This pragmatic path yielded early service differentiation and accelerated device adoption. It also gave operators margin headroom as usage surged.

Standalone deployments are projected to log a 25.6% CAGR to 2031, supported by cloud-native cores and service-based interfaces that enable end-to-end slicing. The shift unlocks ultra-reliable, low-latency communications for manufacturing, logistics, and public safety ecosystems. Network exposure functions simplify the creation of API-based services, broadening revenue diversification. Greenfield digital-native operators in India and fixed-wireless specialists in the United States move directly to standalone networks, bypassing the complexities of transitional non-standalone networks. As device portfolios with release-17 firmware proliferate, the 5G New Radio market expands via premium enterprise offers that justify higher ARPU.

By Component: Software Surpasses Hardware Weight

gNB hardware still accounted for 47.15% of 2025 spending, reflecting the physical necessity of antennas, remote radio heads, and integrated baseband units for each cell site. Vendors deliver turnkey solutions optimized for energy efficiency, which is vital for operators facing rising electricity tariffs. Advanced M-MIMO arrays with up to 64 transmit and receive chains remain essential for maximizing spectral efficiency in mid-band deployments.

Software revenue, however, leads growth at 25.98% CAGR. Virtual RAN functions, orchestration platforms, AI-based network-optimization tools, and security analytics now represent the largest component group by value. Operators embrace pay-as-you-grow license models that align expense with traffic scale. The 5G New Radio market size for software accelerates further as integrated development kits enable third-party ISVs to launch domain-specific slices. Services complete the stack, covering systems integration, managed optimization, and lifecycle support essential for operators lacking in-house expertise.

By End-User Industry: Manufacturing Outpaces Telecom Capex

Telecom operators accounted for 57.85% of the total 5G New Radio market expenditure in 2025, unsurprising given their role in national coverage builds. Consumer broadband, mobile voice, and IoT connectivity underpin recurring revenue, keeping operator capex resilient. Yet manufacturing overtakes other verticals in growth, rising 27.4% annually through the forecast as factory automation takes precedence. Private licensed spectrum, deterministic latency, and on-premises data sovereignty persuade plant managers to migrate from wired fieldbus and Wi-Fi systems.

Public-safety agencies are accelerating upgrades to mission-critical broadband, utilizing isolated slices for push-to-talk, body-worn camera feeds, and unmanned drone control. Transport and logistics networks adopt standalone 5G to support autonomous yard trucks, smart-port cranes, and real-time fleet telemetry. Utilities implement wide-area sensor grids for dynamic load balancing and outage localization. Each vertical adds differentiated requirements such as time-sensitive networking, packet-delay budget compliance, or encryption wrappers that propel specialist software vendors into the 5G New Radio market.

Geography Analysis

North America led the 5G New Radio market, accounting for 37.95% of the revenue share in 2025, driven by favorable spectrum auctions and capital intensity among Tier-1 carriers. Verizon, AT&T, and T-Mobile collectively invested more than USD 30 billion in 2024 to accelerate standalone deployments, with a focus on enterprise edge services and fixed wireless access. The Federal Communications Commission’s mid-band auctions and NTIA’s spectrum-sharing roadmaps ensured contiguous, high-capacity holdings for operators. Cloud-native cores entered commercial service by mid-2024, enabling differentiated SLA-backed products and lifting average revenue per user.

Asia-Pacific stands out for velocity, logging a 26.4% CAGR. China is expected to have erected 3.5 million 5G sites by the end of 2024, extending coverage into rural areas under the “Broadband Countryside” plan. [4]Ministry of Industry and Information Technology, “5G Base-Station Count 2024,” MIIT.GOV.CN. Japan’s Smart Cities Consortium is incentivizing the deployment of millimeter-wave small cells across train stations and stadiums in preparation for the 2025 Osaka World Expo. India’s mandatory domestic-equipment preference bolsters local manufacturing, trimming radio-unit costs and shortening delivery cycles as governments pursue digitization to boost productivity, private-network tenders surge, deepening the 5G New Radio market opportunity among local integrators and hyperscalers.

Europe maintains moderate, policy-driven expansion. Pan-EU spectrum harmonization reduces the number of device variants and simplifies cross-border roaming for truck and rail operators. The Digital Decade fund underwrites fiber backhaul in less-dense regions, thereby catalyzing the development of neutral-host models. Meanwhile, European regulators are championing open-RAN to diversify supplier ecosystems, following security-based vendor restrictions. These initiatives sustain healthy though measured growth, balancing fiscal prudence with industrial competitiveness.

Competitive Landscape

Incumbent vendors Ericsson, Nokia, Huawei, and Samsung continue dominating aggregated global shipments, leveraging end-to-end portfolios that span radios, cores, transport, and professional services. Their integrated road-maps de-risk deployment for operators and secure long-term maintenance contracts. That said, software orientation reshapes the field. Mavenir, Parallel Wireless, and Rakuten Symphony capitalize on open-RAN momentum, supplying cloud-native stacks that displace proprietary baseband hardware. Intel’s FlexRAN reference architecture attracts server-OEM partners, extending the x86 ecosystem into radio processing.

Strategic differentiation now hinges on energy efficiency, AI-powered automation, and vertical-specific solution catalogs. Ericsson and Nokia embed machine-learning inference in transport nodes to slash operational power. Samsung prioritizes ASIC-based beamformers for mmWave units, which reduce thermal load. Acquisition pipelines illustrate convergence: Nokia bought Infinera to secure optical backhaul capacity, while cloud hyperscalers pursue telco-edge positions through joint ventures. Component specialists, such as Qualcomm and Analog Devices, anchor semiconductor innovation by partnering through reference designs.

Competitive pressure cascades to service models. Vendors evolve from hardware sales into revenue-sharing managed services, bundling lifecycle analytics and network-as-code toolkits. As software’s share of the 5G New Radio market rises, license renewals and feature subscriptions stabilize cash flows but heighten churn risk if innovation lags. Net outcome: the market exhibits moderate concentration with increasing fragmentation at the application layer.

5G New Radio Industry Leaders

Huawei Technologies Co., Ltd.

Telefonaktiebolaget LM Ericsson

Nokia Corporation

Samsung Electronics Co., Ltd.

ZTE Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Nokia and Microsoft entered a USD 8.2 billion partnership to bring cloud-native 5G to enterprises. The plan combines Azure edge computing with Nokia standalone cores and will start rolling out private 5G networks for factories and logistics hubs in North America and Europe by Q1 2026.

- September 2025: Samsung Electronics extended its Verizon contract to 2028 at USD 12.4 billion. The deal adds satellite-terrestrial links, extreme-band radios, Open-RAN gear, and AI-based optimization, further solidifying Samsung’s role in advanced 5G deployments.

- August 2025: Ericsson bought Cradlepoint for USD 1.1 billion to gain edge computing and SD-WAN capabilities. The acquisition strengthens Ericsson’s position in private 5G and supports Industry 4.0 projects across the manufacturing and transportation sectors.

- July 2025: Qualcomm introduced the Snapdragon X85 5G Advanced modem, which operates on early 6G research bands and offers enhanced support for satellite connectivity. The chip enables seamless handovers between terrestrial and non-terrestrial networks, expanding continuous coverage applications.

- June 2025: Intel committed USD 15 billion to expand 5G infrastructure chip production in Ireland and Germany. The investment will enable the manufacture of Open-RAN processors and edge hardware, easing supply-chain pressure and supporting Europe’s digital sovereignty objectives.

Global 5G New Radio Market Report Scope

| Sub-6 GHz |

| 24-40 GHz (mmWave) |

| Above 40 GHz (extreme-band) |

| Non-Standalone (NSA) |

| Standalone (SA) |

| gNB Hardware |

| Software |

| Services |

| Telecom Operators |

| Manufacturing |

| Public Safety |

| Transport and Logistics |

| Energy and Utilities |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Rest of Asia Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Frequency Band | Sub-6 GHz | |

| 24-40 GHz (mmWave) | ||

| Above 40 GHz (extreme-band) | ||

| By Deployment Mode | Non-Standalone (NSA) | |

| Standalone (SA) | ||

| By Component | gNB Hardware | |

| Software | ||

| Services | ||

| By End-User Industry | Telecom Operators | |

| Manufacturing | ||

| Public Safety | ||

| Transport and Logistics | ||

| Energy and Utilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What was the 2026 revenue figure for the 5G New Radio market?

The 5G New Radio market size reached USD 62.22 billion in 2026.

Which region leads current spending on 5G NR infrastructure?

North America held 37.95% revenue share in 2025, the highest globally.

Which deployment mode is growing fastest?

Standalone architecture is posting a 25.6% CAGR as operators move toward cloud-native cores.

Why are manufacturers adopting private 5G?

Manufacturing plants need deterministic latency and uptime for automation, driving a 27.4% CAGR in that vertical.

How does spectrum liberalization affect rollout economics?

Harmonized mid- and high-band allocations cut radio-unit costs and permit wider channels, accelerating extreme-band deployments.

Page last updated on: