LTE And 5G Broadcast Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

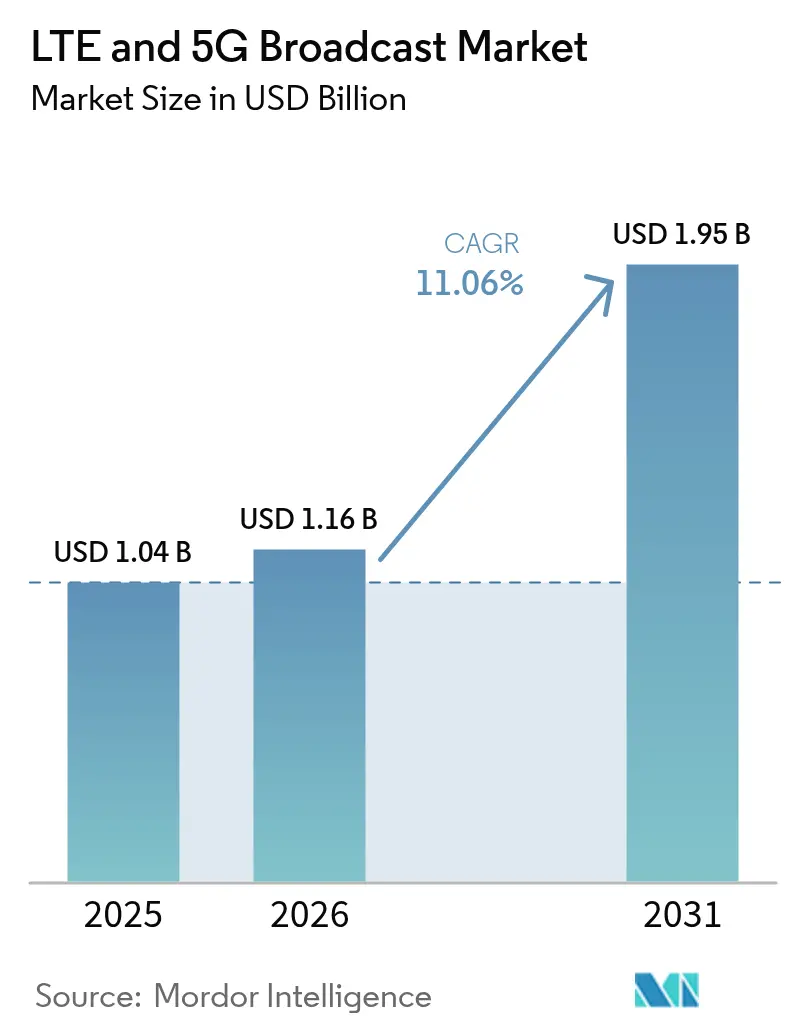

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.95 Billion |

| Growth Rate (2026 - 2031) | 11.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LTE And 5G Broadcast Market Analysis by Mordor Intelligence

LTE and 5G broadcast market size in 2026 is estimated at USD 1.16 billion, growing from 2025 value of USD 1.04 billion with 2031 projections showing USD 1.95 billion, growing at 11.06% CAGR over 2026-2031. Rising demand for spectrum-efficient video delivery, emergency-alert modernization, and rapid device proliferation are expanding commercial trials into nationwide rollouts. Operators are migrating from legacy LTE eMBMS toward 5G FeMBMS to gain multicast flexibility and AI-driven resource allocation, while broadcasters experiment with hybrid ATSC 3.0–5G workflows. Vendors that combine end-to-end cellular and broadcast know-how secure early contracts, and patent filings around Release 18 multicast enhancements hint at new licensing models that could further reshape competition.

Key Report Takeaways

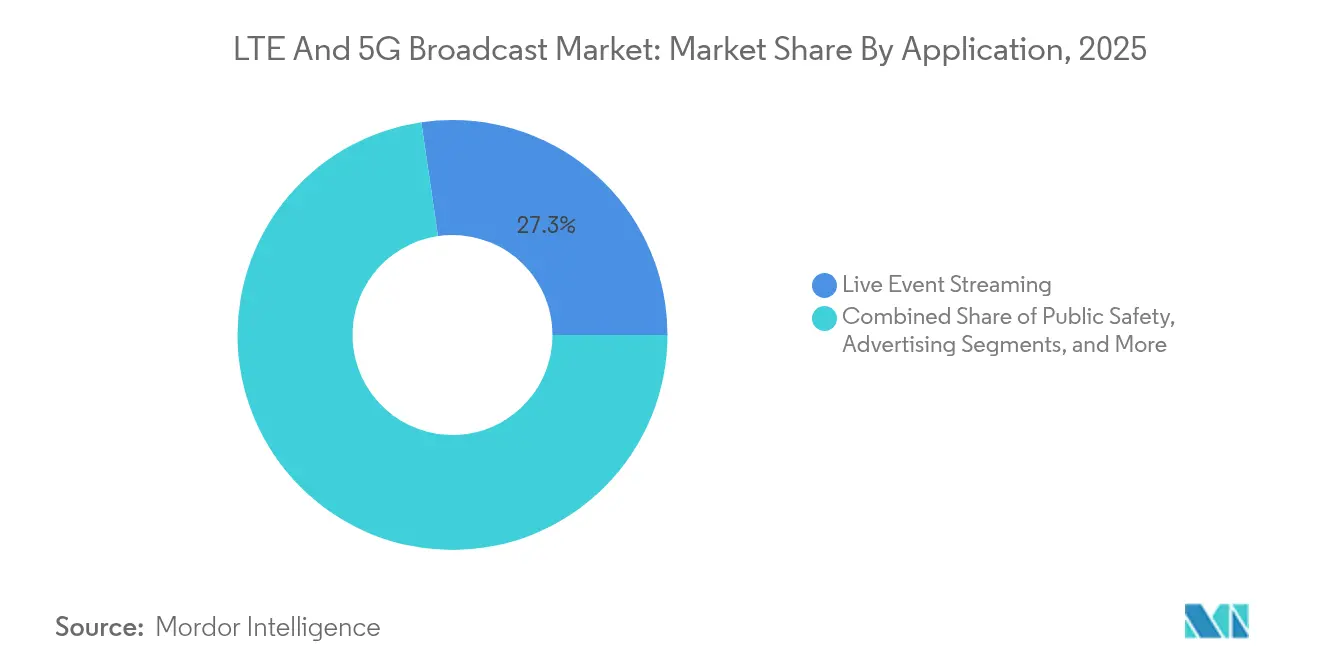

- By application, Live Event Streaming led with 27.32% revenue share in 2025; Connected Vehicles is projected to expand at a 11.93% CAGR to 2031.

- By broadcast technology, LTE eMBMS accounted for 60.25% of the LTE and 5G broadcast market share in 2025, while 5G FeMBMS records the highest projected CAGR at 13.94% through 2031.

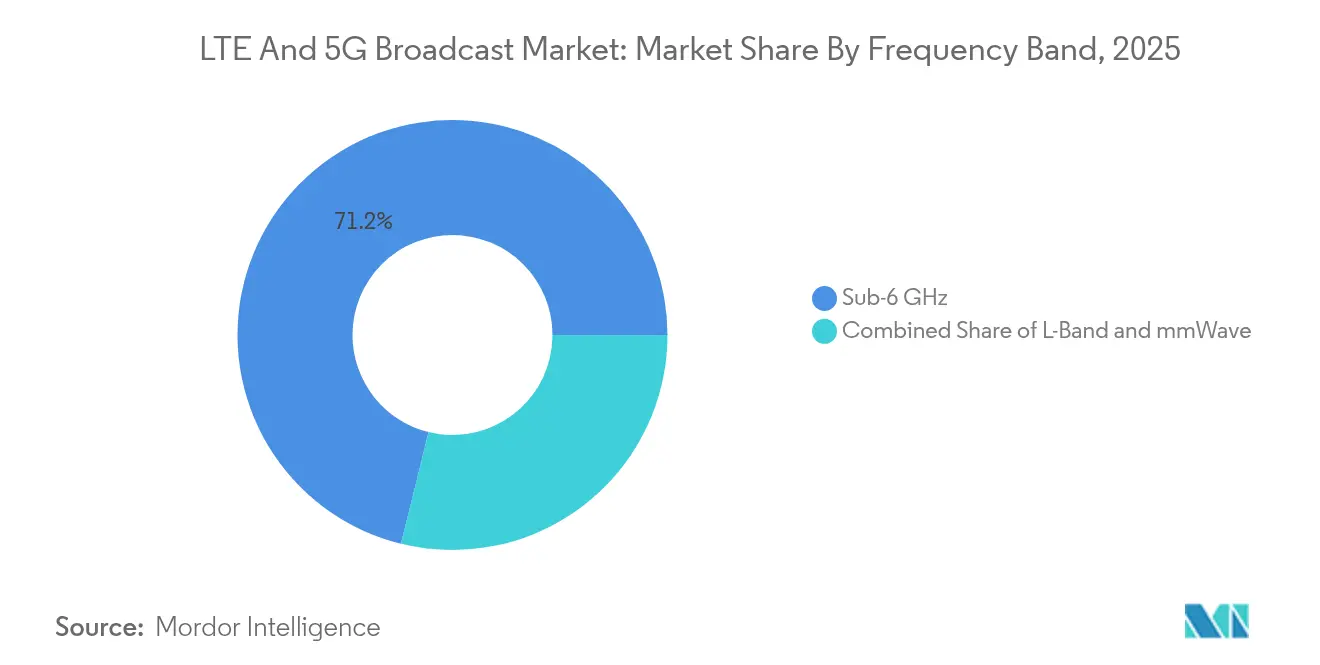

- By frequency band, Sub-6 GHz commanded 71.15% share of the LTE and 5G broadcast market size in 2025; mmWave deployment is advancing at a 13.62% CAGR through 2031.

- By end user, Mobile Network Operators held a 54.38% share in 2025, whereas Automotive OEMs posted the fastest CAGR of 12.31% to 2031.

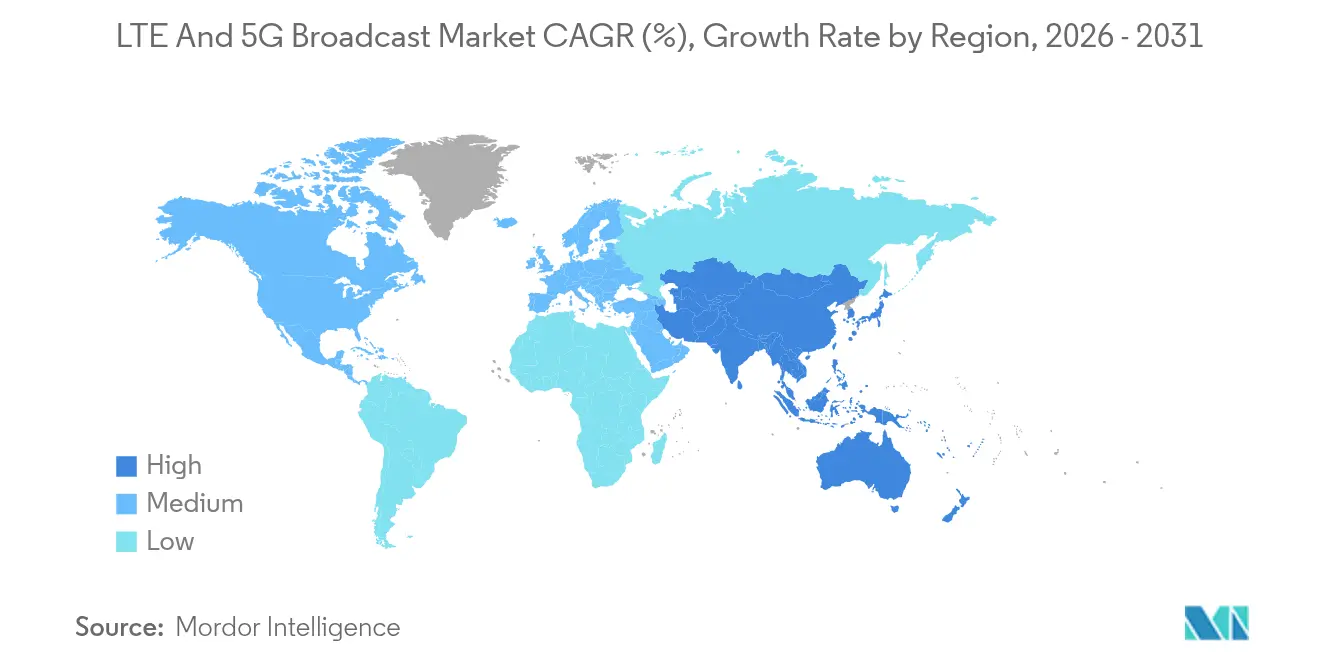

- Regional view: Asia Pacific captured 37.65% revenue in 2025 and is growing at a 14.12% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of LTE And 5G Broadcast Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for mobile video and live event streaming | +2.8% | Global, strongest in North America and Asia-Pacific | Medium term (2–4 years) |

| Surge in 5G-enabled device penetration | +2.1% | Asia-Pacific core, spill-over to Europe and North America | Short term (≤ 2 years) |

| Spectrum-efficiency gains via 5G FeMBMS multicast | +1.9% | Global, notably Europe and North America | Long term (≥ 4 years) |

| Emergency-alert modernization mandates | +1.6% | North America and EU, expanding to Asia-Pacific | Medium term (2–4 years) |

| Automotive OTA updates leveraging broadcast channels | +1.4% | Global, early adoption in Germany and China | Long term (≥ 4 years) |

| Hybrid satellite-to-mobile (NTN) convergence | +1.2% | Global, focused on rural and remote areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for mobile video and live event streaming

Operators pivot to multicast to curb unicast congestion as mobile viewers demand 4K, 360-degree, and augmented-reality feeds. Deutsche Telekom and Ericsson delivered sub-25 ms latency and 500 Mbps uplinks for Euro 2024 wireless cameras, proving viability for professional production.[1]Ericsson, “RTL Deutschland and Deutsche Telekom deliver live TV production via private 5G,” ericsson.com Malaysia streamed its National Day parade over a network-sliced 5G link, ensuring stable quality even at peak load.[2]Digital TV Europe, “Malaysia stages first 5G live broadcast,” digitaltveurope.com Broadcasters now request 50 Mbps sustained uplink per camera, a requirement met only when several viewers share the same multicast flow. Verizon has added AI-based audience-density recognition inside its private 5G broadcast suite to fine-tune bitrate in real time.[3]Verizon, “Verizon Business debuts private 5G and AI video solution at NAB 2025,” verizon.com

Surge in 5G-enabled device penetration

NTT Docomo demonstrated 6.6 Gbps downlink on 5G Stand-Alone, signaling handset readiness for high-bitrate broadcast reception. BMW equips all 2025 models with 5G antennas to stream broadcast content and push simultaneous firmware updates. China’s mandate that premium phones support 700 MHz expanded the installed base capable of FeMBMS reception, accelerating service availability. While broadcast-specific chipsets remain scarce, automotive infotainment suppliers are integrating them first, creating a beachhead for wider consumer adoption.

Spectrum-efficiency gains via 5G FeMBMS multicast

Release 18 introduces AI-controlled resource allocation that can lift spectral efficiency by 40% versus LTE eMBMS. China Unicom is inserting these capabilities across 300 cities by end-2025.[4]RCR Wireless News, “China Unicom accelerates 5G-Advanced deployment,” rcrwireless.com Nokia reported that a single 20 MHz TDD carrier can now transmit UHD video simultaneously to 1 million users, cutting per-viewer cost dramatically. Operators can switch between unicast and multicast on overlap thresholds as low as five users, ensuring resource gains even in mid-density cells.

Emergency-alert modernization mandates

FirstNet and AT&T are investing USD 6.3 billion to overlay 5G broadcast features such as real-time drone feeds and multimedia evacuation guidance. Japan attained 98.1% 5G coverage in 2024, enabling its cell-broadcast upgrade to include hazard-map video and sign-language overlays for residents with accessibility needs. These mandates create non-discretionary spending lines in operator budgets, insulating the LTE and 5G broadcast market from macroeconomic slowdowns.

Restraints Impact Analysis of LTE And 5G Broadcast Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CapEx for broadcast-capable upgrades | −2.4% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Fragmented spectrum and regulatory uncertainty | −1.8% | Global, allocation varies by region | Medium term (2–4 years) |

| Limited chipset/device support for FeMBMS | −1.6% | Global, affects consumer adoption | Medium term (2–4 years) |

| Edge-caching and Wi-Fi offload diluting ROI | −1.3% | Developed markets with dense infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CapEx for broadcast-capable upgrades

Adding multicast controllers, re-tuning antennas, and deploying dense mmWave small cells can raise per-site cost by 50% versus data-only 5G. Nokia noted weaker equipment orders in 2024 as operators deferred broadcast modules to preserve cash. mmWave broadcast, essential for stadiums, needs 1.5–2× more base stations than Sub-6 GHz, further stretching budgets. Some carriers adopt phased rollouts, enabling broadcast only on 10% of cells that carry 70% of peak video traffic, yet this tactic elongates nationwide coverage timelines.

Limited chipset/device support for FeMBMS

Semiconductor vendors rank broadcast support behind modem power efficiency and AI accelerators. Qorvo signalled slower Android 5G refresh cycles, constraining volumes needed to justify dedicated broadcast silicon. Automotive Tier-1 suppliers are custom-integrating FeMBMS receivers, but smartphone adoption hinges on unified global standards to avoid regional SKUs. The resulting chicken-and-egg dynamic delays mass-market consumer services and tempers immediate ROI expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

LTE And 5G Broadcast Market Segment Analysis

By Application:

Connected Vehicles Gain PaceLive Event Streaming retained 27.32% of 2025 revenue by exploiting marquee sports and cultural broadcasts that demand guaranteed quality levels. Still, Connected Vehicles will post a 11.93% CAGR through 2031 as automotive OEMs push over-the-air updates to millions of cars simultaneously, a task unicast networks struggle to scale. BMW’s fully 5G-equipped model line and Tesla’s factory private networks show broadcast’s dual role in production analytics and in-vehicle infotainment. The LTE and 5G broadcast market underpins remote diagnostics, V2X safety messages, and map data refresh without user intervention.

A second growth lane appears in public safety. FirstNet’s upgrade adds multicast drone imagery and real-time body-camera feeds that improve situational awareness for first responders. Mobile TV and video on demand rely on broadcast to reduce backhaul in flash-crowd situations like election nights, while advertising networks test location-based multicast spots that insert local offers into a national video stream. These varied use cases cement application-layer diversity and maintain resilience against single-segment downturns.

By Broadcast Technology:

5G FeMBMS AcceleratesLTE eMBMS still commands 60.25% of the LTE and 5G broadcast market share in 2025 on the strength of earlier deployments, yet 5G FeMBMS grows 13.94% annually as operators overlay Release 18 software onto existing 5G cores. China Mobile’s 100-city launch validated FeMBMS scalability, and plans to triple coverage by 2025 illustrate aggressive timelines. Operators appreciate FeMBMS’s seamless switch between unicast and multicast when audience thresholds are met, thereby optimizing every megahertz.

ATSC 3.0 hybrid broadcast gives terrestrial media companies an entry point to mobile distribution. Brazil’s roadmap to nationwide ATSC 3.0 by the 2026 World Cup and ongoing FCC trials in the United States demonstrate convergent cellular–terrestrial standards. Release 18’s AI schedulers cut cell-edge packet loss and boost mobility, benefits that accrue across both LTE and 5G implementations. As device ecosystems mature, the transition narrative will shift from coexistence to sunset planning for LTE eMBMS in the next decade.

By Frequency Band:

Sub-6 GHz Dominates, mmWave RisesSub-6 GHz supplied 71.15% of revenue in 2025, thanks to nationwide coverage needs and favorable propagation. Japan’s network, which increased 5G base stations by 20% in one year, predominantly uses mid-band to reach 98.1% coverage. The LTE and 5G broadcast market size for Sub-6 GHz deployments will still expand, albeit more slowly, as greenfield operators in developing economies prioritize cost-effective wide-area service.

mmWave posts a 13.62% CAGR because event venues, smart factories, and city centers demand multi-gigabit throughput and ultra-low latency. NTT Docomo’s 6.6 Gbps showcase underscores mmWave headroom for future XR and holographic services. Regulatory release of 700 MHz to broadcast in China shows that low-band is equally strategic, especially for emergency alerts where deep indoor coverage is essential. L-Band keeps a niche in satellite-to-mobile links, extending multicast to maritime and rural segments that lack terrestrial backhaul.

By End User:

Automotive OEMs OutperformMobile Network Operators held 54.38% revenue in 2025 as they monetized existing infrastructure and wholesale capacity. Yet, Automotive OEMs will outpace all groups at 12.31% CAGR, turning vehicles into rolling terminals for software, maps, and entertainment without SIM-based billing friction. Ford and AT&T’s 5G edge-compute pilot cut factory floor latency by 40%, enabling real-time quality control via broadcast video analytics.

Media and entertainment firms embrace private 5G to streamline on-site production. RTL Deutschland cut cabled camera runs at Euro 2024, saving installation days and labor costs. Public-safety agencies adopt broadcast for mission-critical push-to-X services. The net effect is a diversified LTE and 5G broadcast industry customer base that insulates vendors from sector-specific budget swings.

Geography Analysis

APAC LTE And 5G Broadcast Market

Asia Pacific commands 37.65% of 2025 revenue and grows at 14.12% CAGR. Government-backed 5G-Advanced rollouts in China, Japan, and South Korea embed multicast from day one. China Mobile’s coverage of 100 cities, expanding to 300 in 2025, serves UHD streaming, industrial IoT, and mass alerts on the same platform. Japanese operators added 20% more base stations in 2024, pairing mid-band with mmWave for broadcast in dense metros. South Korea complements consumer focus with private 5G grants for factories, accelerating broadcast adoption in manufacturing and logistics.

North America LTE And 5G Broadcast Market

North America ranks second, propelled by the FirstNet Authority’s USD 8 billion ten-year plan, including USD 6.3 billion earmarked for broadcast-centric 5G enhancements. Automotive majors—Ford, GM, Tesla—install private 5G to synchronize plant robots and push software to vehicles overnight. The device ecosystem is mature, yet CapEx discipline tempers rapid nationwide broadcast upgrades.

EMEA and South America LTE And 5G Broadcast Market

Europe advances on regulatory harmonization. The European Broadcasting Union’s hybrid 5G/satellite pilot reduces rural coverage gaps while complying with EU Green Deal energy targets. Germany leads automotive broadcast integration; BMW’s 5G connectivity plan covers both assembly lines and post-sale updates. Smaller regions—Middle East, Africa, South America—mirror overall 5G timelines; where spectrum auctions conclude early, broadcast trials begin within 18 months, albeit at modest scale.

Regulatory Landscape

Regulation for LTE eMBMS and 5G FeMBMS deployments is anchored in 3GPP specifications and their regional adoptions, with Release 18 acting as the key reference point for multicast and broadcast service evolution during 2025-2026. In markets where terrestrial TV spectrum is being evaluated for 5G broadcast use, coexistence requirements shape deployment design, including channel bandwidth support added in Release 17 (6/7/8 MHz) to align with regional allocations and broadcasting channel plans.

Spectrum governance and interference coordination remain central constraints when 5G broadcast is introduced near or within UHF bands used for digital terrestrial television, including coordination frameworks such as the GE06 Agreement in ITU Region 1. Separately, national compliance regimes can add device certification friction for multicast-capable products; Indonesia's KOMDIGI Decree No. 569/2025 took effect on 19 January 2026, tightening type-approval expectations tied to frequency band support and recertification, which can affect how quickly broadcast-capable devices and modules are cleared for commercial use.

Value Chain Analysis

The value chain starts with standards and profiles set by 3GPP and ETSI, which define the functional building blocks for LTE-based 5G terrestrial broadcast and multicast services. Upstream suppliers include RAN and core software vendors, broadcast-network equipment providers (for example Rohde & Schwarz), and chipset and device ecosystem participants that determine receiver availability and feature support. Middleware and service-layer software then connects broadcast and multicast delivery to applications such as live event streaming, emergency alerts, mobile TV, advertising insertion, and connected-vehicle data delivery.

Implementation typically runs through mobile network operators, broadcasters, consortiums, and private-network integrators that assemble end-to-end solutions and conduct field trials to prove coexistence, coverage, and device reception. Key downstream channels include public safety agencies and media production users that procure managed services, as well as automotive OEMs and device makers that drive embedded receiver volumes. Bottlenecks remain concentrated around spectrum access, multi-stakeholder coordination, and limited mass-market device support for FeMBMS, which keeps early deployments focused on controlled footprints and specialized receivers even as Release-aligned solutions mature.

Competitive Landscape

The LTE and 5G broadcast market shows moderate concentration. Huawei remained revenue leader at CNY 862.1 billion in 2024 on the back of 5G-Advanced wins that include multicast features. Ericsson and Nokia pursue licensing income to supplement hardware margins; Nokia signed a 5G RAN expansion with T-Mobile US in April 2025 that embeds broadcast cores in 2,400 sites. Qualcomm, Samsung, and Apple escalate patent filings around Release 18 AI multicast schedulers, raising cross-licensing stakes for device vendors.

Technical differentiation centers on AI at the edge. Verizon’s NAB 2025 demo paired NVIDIA GPUs with C-band, CBRS, and mmWave to manage 60 simultaneous 4K feeds while auto-prioritizing action shots for live mixing. Specialized software entrants craft network-slice orchestration that lets broadcasters lease capacity without owning spectrum. Incumbent TV transmitter suppliers such as Rohde & Schwarz retrofit gear with 5G plug-ins, creating joint bids with cellular vendors.

Regulatory compliance and multi-domain integration raise entry barriers. Vendors that manage spectrum, service layer, and device certification in one package win early RFPs. Automotive OEMs increasingly issue direct tenders for private networks, inviting smaller radio vendors that can customize to factory layouts, subtly diluting incumbent share yet broadening overall ecosystem depth

LTE And 5G Broadcast Industry Leaders

KT Corporation

Verizon Wireless

AT&T Inc.

Huawei Technologies Co. Ltd.

SK Telecom Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

LTE And 5G Broadcast Market Companies Covered in this Report

- Huawei Technologies Co. Ltd.

- ZTE Corporation

- Ericsson AB

- Nokia Corp.

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- KT Corporation

- Verizon Communications Inc.

- AT&T Inc.

- China Unicom (HK) Ltd.

- SK Telecom Co. Ltd.

- KDDI Corporation

- Telstra Corp. Ltd.

- Reliance Jio Infocomm Ltd.

- Rohde and Schwarz GmbH

- Enensys Technologies SA

- Harmonic Inc.

- Ateme SA

- MediaTek Inc.

- Rohde & Schwarz GmbH & Co KG

Market Opportunities and Future Outlook

Commercial whitespace is opening around hybrid terrestrial workflows that combine broadcast infrastructure with cellular-defined multicast, enabling broadcasters and network operators to reuse UHF assets while adding one-to-many delivery to mobile devices. A concrete proof point is the April 2026 hybrid 5G Broadcast and ATSC 3.0 pilot demonstrated at NAB in Las Vegas, which showed practical interworking paths for broadcasters that already invest in terrestrial transmission while pursuing mobile distribution and emergency alert modernization.

A further opportunity is the shift from trials to deployable footprints in the United States using Low Power TV station assets and receive-only device concepts, reducing reliance on SIM-based connectivity for broadcast consumption. Castanet's strategy to build coverage using LPTV stations, with 456 stations under MOU as of February 2026 and a stated 95% US population coverage objective, reflects an execution model that can speed up network reach once device availability and local permissions align. On the enabling-technology side, Release 19 work items and specifications that address interworking between non-3GPP terrestrial broadcast and 5G MBS, along with features such as CAS muting described in Release 19 technical reports, create a clearer engineering path for coexistence and integrated alerting, supporting procurement discussions with public safety and large-event stakeholders.

Recent Industry Developments in LTE And 5G Broadcast Market

- May 2026: Nakolos announced completion and implementation of an end-to-end 5G Broadcast solution aligned to the 3GPP Release 19 feature set, including capabilities such as CAS muting. The release-level completeness helps operators and broadcast-network builders move from feature-by-feature trialing to more standardized procurement and integration. It also tightens vendor differentiation around interoperability and deployment-readiness for mixed broadcast-broadband environments.

- April 2026: Neutral Wireless and Castanet completed a hybrid 5G Broadcast and ATSC 3.0 pilot at NAB in Las Vegas using Release 19-compliant technology and a 533 MHz transmitter. Demonstrating hybrid transmission in an event setting validates coexistence approaches for broadcasters that want to extend terrestrial investments into mobile-device delivery. The pilot also reinforces the strategic role of UHF spectrum and existing station assets in scaling mobile broadcast coverage.

- February 2026: XGN Global and X1 Mobile announced a 5G Broadcast-enabled rugged smartphone at Mobile World Congress, with a European model shipping in May 2026 and a US-specific model scheduled for Q3 2026. Device availability is a gating factor for FeMBMS and 5G Broadcast monetization, and a commercial handset form factor signals progress beyond lab receivers. It supports ecosystem pull-through for network trials and creates a tangible endpoint for enterprise and public-safety use cases that need resilient one-to-many reception.

LTE And 5G Broadcast Market Report Scope and Research Methodology

Market Definition and Coverage

This market is defined as the revenues generated from LTE Broadcast and 5G Broadcast capabilities that enable one-to-many content delivery over cellular networks, typically using 3GPP multicast and broadcast features. We count related equipment, software, and managed services that make these deployments work in live networks.

Scope exclusions: Excluded from the numbers are traditional over-the-air TV broadcast standards such as DVB-T/T2 and ATSC 3.0.

Segments Covered in This Report

- By Application

- Public Safety

- Connected Vehicles

- Live Event Streaming

- Mobile TV Streaming

- Advertising

- Content/Data Delivery

- Video on Demand

- By Broadcast Technology

- LTE eMBMS

- 5G FeMBMS

- ATSC 3.0 Hybrid Broadcast

- By Frequency Band

- Sub-6 GHz (<6 GHz)

- L-Band (1-2 GHz)

- mmWave (>24 GHz)

- By End User

- Mobile Network Operators

- Media and Entertainment Firms

- Automotive OEMs

- Public Safety Agencies

- Others

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the technical and commercial baseline so the model stays aligned with what is realistically deployed and monetized. We reviewed public standards and technical references, such as 3GPP specifications for eMBMS and FeMBMS, along with regulatory and spectrum publications from bodies such as the ITU and national telecom regulators.

To connect technology readiness with demand, we also referred to public datasets and disclosures such as mobile traffic indicators from organizations like the GSMA, emergency alerting frameworks published by government agencies, and peer-reviewed papers on multicast efficiency and network utilization. Company annual reports, investor decks, press releases, and product documentation were then used to map solution availability and typical buying patterns across operators and broadcast ecosystem partners. Paid subscriptions supporting company financials and intelligence, patent databases, and news and financials were used selectively to cross-check timelines, product positioning, and corporate activity. The sources listed here are illustrative, and other public references were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating which LTE and 5G broadcast features are being commercialized, how pricing is structured, and where rollouts remain in pilots. We spoke with a mix of network-side stakeholders, solution enablers, and users of broadcast delivery (for live events and public warning use cases), and coverage was balanced across APAC, EMEA, and the Americas to avoid region-specific bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 19% | APAC: 43% |

| Mid tier: 51% | Functional/Unit leaders: 23% | EMEA: 37% |

| Smaller Players: 20% | Managers: 58% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where operator and ecosystem spending is reconstructed into a broadcast-specific demand pool using adoption and utilization signals. The model then gets pressure-tested with selective bottom-up approximations, such as sampled deal values, solution stack pricing (software plus network upgrades), and rollout counts indicated through deployments and trials, which are then used to adjust totals when gaps show up.

Key inputs used in the model include the pace of 5G network expansion that can support broadcast features, the share of live event and public warning use cases that are configured for multicast, the prevalence of eMBMS and FeMBMS capable infrastructure, and typical pricing progressions for licenses, integration, and managed services. We also track indicators like spectrum and regulatory readiness for broadcast modes, plus regional differences in emergency alert mandates and mobile video consumption. For forecasting, scenario analysis is used so the numbers reflect different commercialization speeds, and scenario weightings are validated through expert views collected in interviews. When bottom-up details are not fully visible for smaller deployments, assumptions are kept conservative and tied back to observable rollout signals and public disclosures.

Data Validation & Update Cycle

Validation is done through multiple checks that look for mismatches between the model and independent signals, such as deployment announcements, standards milestones, and operator capex patterns tied to feature upgrades. If an outlier appears at a country or region level, we revisit the core drivers, recheck currency conversion timing, and recontact sources when the variance cannot be explained through public evidence.

Before sign-off, the analysis goes through an internal review where calculations, assumptions, and year-to-year movements are revalidated, and inconsistencies are corrected with clear notes. Reports are refreshed annually, and interim updates are made when there are material events such as major commercial launches, expansions of public safety programs, or meaningful standards and device ecosystem shifts. Right before delivery, a final analyst pass is completed so clients receive the most current view possible.

Mordor Intelligence's Lte and 5g Broadcast Market Size Versus Other Published Estimates

Published market values for LTE and 5G broadcast can look different because each publisher draws the line around what they count as broadcast, and they may also use different start years and conversion timings. We also see differences when forecasts assume fast mass adoption versus a slower path where deployments stay tied to specific venues and public warning programs.

Traditional over-the-air TV standards such as DVB-T/T2 and ATSC 3.0 sit outside Mordor Intelligence's scope, which narrows the total to cellular-based broadcast revenue linked to 3GPP multicast features. That single exclusion explains part of the spread you see in the table. Other gaps tend to come from whether revenues are limited to network equipment and software tied to eMBMS and FeMBMS, or whether adjacent streaming infrastructure and broader mobile TV service revenues get bundled in. Finally, update cadence matters because pilots can move quickly into scaled rollouts in one region, and stale assumptions can overstate or understate near-term revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.16 B (2026) | |

| Global Consultancy A | USD 0.89 B (2024) | Uses an earlier base year and appears to treat commercialization as broader across end uses, which can undercount later ramp-up years and may not fully align revenues to operator-side multicast feature enablement. |

| Industry Publisher B | USD 0.93 B (2025) | Includes a wider set of application discussions, but exclusions are not clearly stated, and the forecast window differs, which can shift what is counted as core broadcast versus adjacent mobile video delivery spending. |

Taken together, the spread is mainly explained by scope clarity, base year selection, and how quickly adoption is assumed to move beyond pilots into repeatable operator programs. Our approach stays traceable by tying totals to observable deployment readiness, use case activation, and realistic pricing building blocks, which helps keep the market view consistent year to year.

Key Questions Answered in the Report

What is the current value of the LTE and 5G broadcast market?

The LTE and 5G broadcast market size stands at USD 1.16 billion in 2026 and is forecast to reach USD 1.95 billion by 2031.

Which region leads the market and why?

Asia Pacific holds 37.65% of global revenue due to large-scale 5G-Advanced deployments in China, Japan, and South Korea that integrate multicast from the outset.

Why is 5G FeMBMS growing faster than LTE eMBMS?

5G FeMBMS delivers 40% better spectral efficiency and supports AI-based resource allocation, prompting operators to migrate despite LTE’s installed base dominance.

How are automotive companies using broadcast technology?

Automotive OEMs employ multicast to push over-the-air software updates and infotainment content simultaneously to millions of vehicles, avoiding unicast congestion.

What role does broadcast play in emergency communications?

Next-generation alert systems use 5G multicast to send real-time video, hazard maps, and evacuation guidance that remain reliable even during peak network loads.

What is the main barrier to faster adoption?

High capital expenditure for broadcast-capable upgrades and limited chipset support delay large-scale rollouts, especially in markets with tighter budgets.

Page last updated on: