5G in Aviation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.23 Billion |

| Market Size (2031) | USD 17.05 Billion |

| Growth Rate (2026 - 2031) | 32.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G in Aviation Market Analysis by Mordor Intelligence

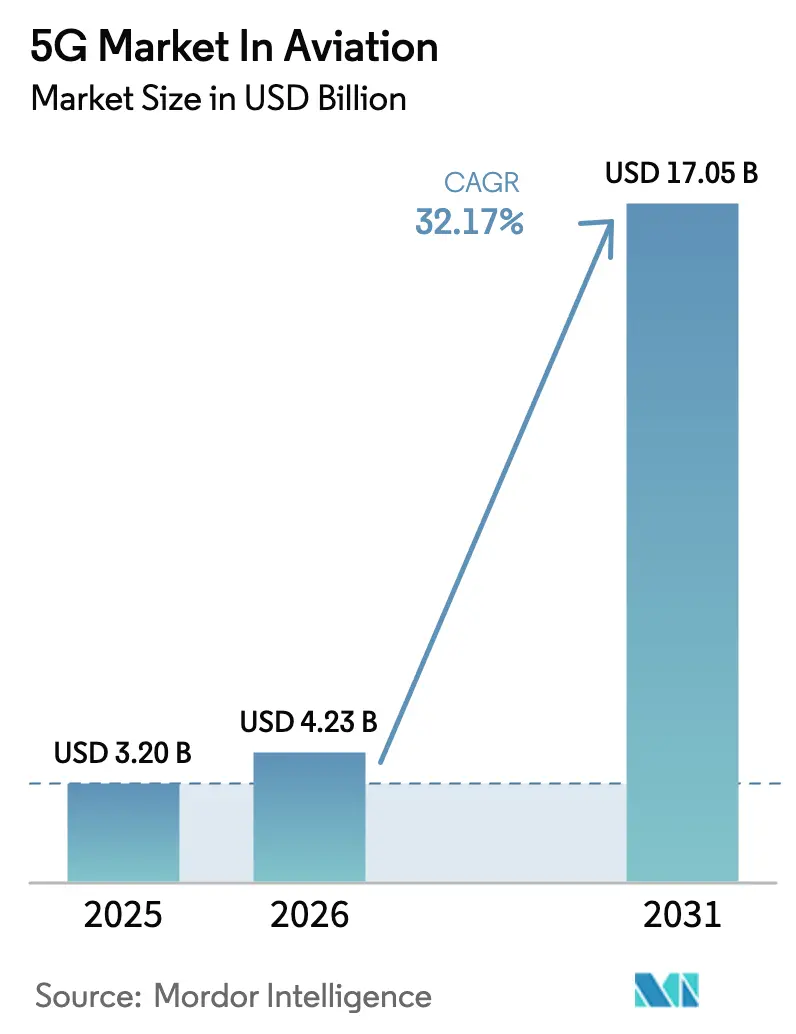

The 5G Market size In Aviation Industry is expected to grow from USD 3.20 billion in 2025 to USD 4.23 billion in 2026 and is forecast to reach USD 17.05 billion by 2031 at 32.17% CAGR over 2026-2031.

The 5G in Aviation Market industry size stood at USD 3.2 billion in 2025 and is forecast to reach USD 13.4 billion by 2030, reflecting a 33.17% CAGR. This rapid climb underscores how 5G is reshaping every layer of aviation, from passenger connectivity and predictive maintenance to data-driven air-traffic management. Rising travellers expectations for seamless inflight broadband, airport digitization programs, and the need for real-time analytics across aircraft and ground assets are converging to propel adoption. A growing backlog of connected-aircraft retrofits, expanding drone corridors, and the promise of latency cuts for safety-critical links add further momentum to the 5G in Aviation Market. North America currently anchors deployment on the strength of mature telecom rollouts and supportive regulation, yet Asia Pacific is quickly matching the overall growth pace through aggressive infrastructure investment and flagship private-network projects at megahubs.

Key Report Takeaways

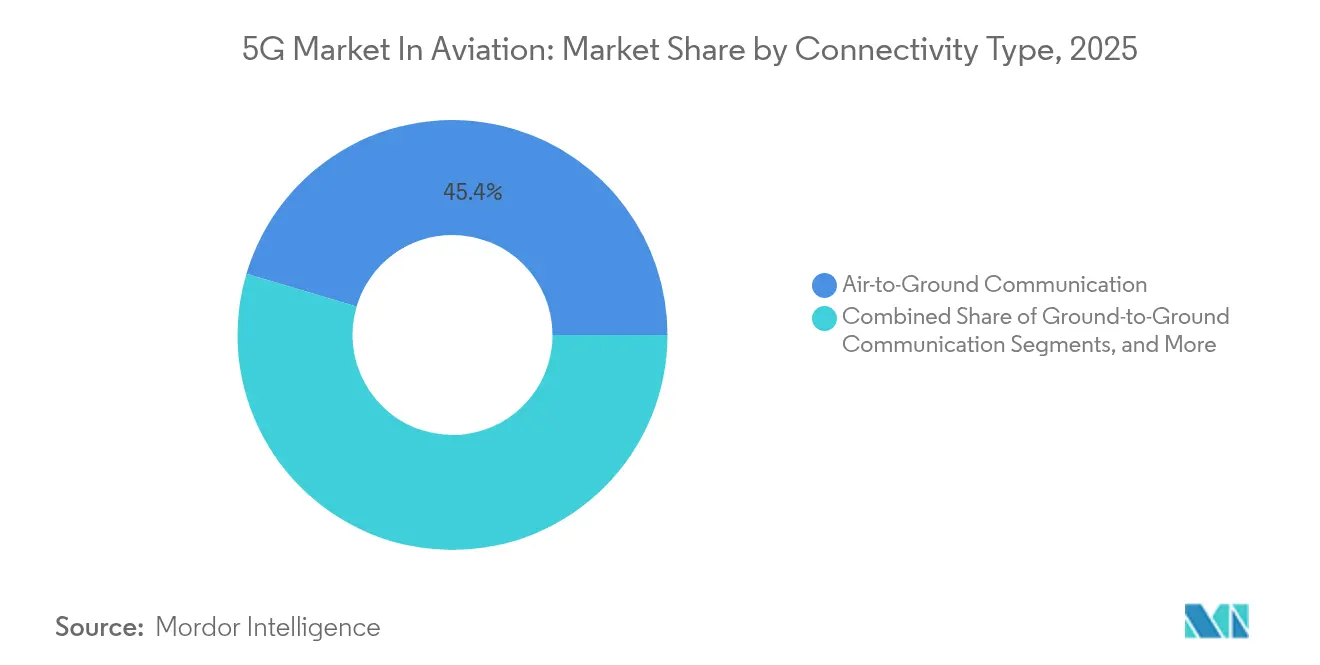

- By connectivity type, air-to-ground communication led with 45.40% of 5G in Aviation Market share in 2025; air-to-air communication is projected to advance at a 43.2% CAGR through 2031.

- By offering, services commanded 37.80% of the 5G in Aviation Market size in 2025, while software solutions are poised for the fastest 33.4% CAGR over the same horizon.

- By application, passenger-experience platforms held 51.20% revenue share in 2025; drone and urban air-mobility operations are forecast to expand at a 44.8% CAGR to 2031.

- By deployment model, private networks accounted for 43.30% of the 5G in Aviation Market size in 2025 and are set to compound at a 36.2% CAGR between 2026-2031.

- By stakeholder, airlines captured 48.20% of the 5G in Aviation Market share in 2025, whereas air-navigation service providers are on track for a 34.5% CAGR through 2031.

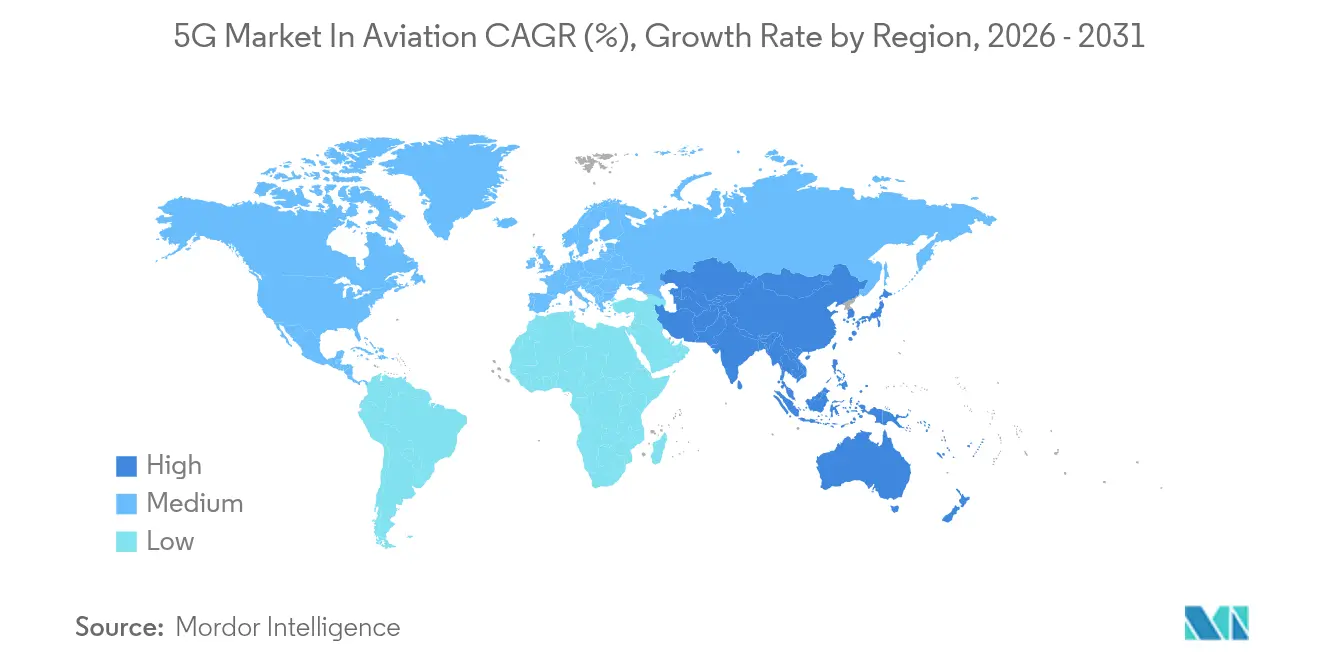

- Regionally, North America retained 36.40% market share in 2025; Asia Pacific mirrors the overall 32.17% growth pace through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 5G in Aviation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IFEC demand | +5.0% | Global; strongest in North America And Europe | Medium term (2–4 years) |

| Airport digital-transformation programs | +4.2% | Global; dense in Asia Pacific and Middle East | Medium term (2–4 years) |

| Rapid expansion of aviation IoT sensors and edge computing | +3.8% | North America, Europe, advanced Asia Pacific hubs | Short term (≤ 2 years) |

| National 5G spectrum auctions and aviation testbeds | +3.5% | Global; regulatory variation by region | Medium term (2–4 years) |

| 5G-enabled Advanced Air Mobility corridors | +3.1% | North America, Japan, South Korea, UAE | Medium term (2–4 years) |

| Real-time 8K cabin analytics for ancillary-revenue upselling | +2.7% | Global early adopters; strongest in premium airlines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of IFEC demand

Seventy-seven percent of passengers now rank onboard Wi-Fi as a deciding factor when booking flights, turning connectivity into a core service benchmark. Qatar Airways’ 2024 launch of Starlink inflight Wi-Fi delivered peak speeds of 500 Mbit/s, narrowing the technology gap between cabin and ground experiences. Gogo’s aviation-specific 5G network, due in 2025, promises consistent 25 Mbps average speeds for business jets, rising to 75-80 Mbps bursts, reshaping cabin entertainment and real-time collaboration.

Airport digital-transformation programs

Airports are shifting from fragmented legacy systems to unified 5G platforms that link thousands of sensors, cameras, and handheld terminals. Frankfurt Airport’s private network reduces blind spots caused by metal airframes and supports secure point-of-sale, automated baggage tracking, and real-time video analytics, cutting mishandled-bag incidents and communication latency.[2]NTT, “Frankfurt Airport Private 5G Case Study,” ntt.com

Rapid expansion of aviation IoT sensors and edge computing

A modern wide-body aircraft houses up to 5,000 sensors that generate 844 TB of data each flight. Coupled with thousands of airport-side devices, this data volume demands 5G’s throughput and ultra-low latency. Purdue University Airport’s living-lab ties Ericsson radios to Saab’s Aerobahn platform, enabling predictive maintenance that trims maintenance spend by 30% and boosts situational awareness for drone detection.[1]Ericsson, “Purdue Airport Living Lab Press Release,” ericsson.com

National 5G spectrum auctions and aviation testbeds

Regulators are creating innovation zones that let airlines and airports trial advanced 5G use cases with protected spectrum. The United Kingdom’s 5G Innovation Regions initiative supports transport pilots across the North East region, while Singapore’s Infocomm Media Development Authority has teamed with Airbus on drone-flight corridors backed by dedicated 5G slices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for private 5G network build-out | −4.5% | Global; sharper in developing economies | Medium term (2–4 years) |

| Aviation-grade cybersecurity And safety certification hurdles | −3.8% | Global; toughest in North America and EU | Short term (≤ 2 years) |

| Interference risks with radio-altimeters in mmWave bands | −2.9% | North America, Europe | Short term (≤ 2 years) |

| Limited 5G device refresh cycles in legacy aircraft fleets | −2.4% | Global airlines with older fleets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for private 5G network build-out

Airport-wide 5G installations often call for USD 3-10 million outlays, covering ruggedized radios, fiber backhaul, and spectrum-access fees. Alternative models are emerging: Brazil-based Atech offers “ATC-as-a-service,” letting navigation service providers tap advanced traffic-management tools without heavy upfront spend, achieving 40% cost savings over traditional projects.

Aviation-grade cybersecurity and safety certification hurdles

Radio-altimeter protection mandates illustrate the rigorous sign-off path. The FAA requires band-pass-filter retrofits on susceptible fleets by April 2025, adding 12-18 months and 15-25% to typical deployment budgets. Suppliers such as Mercury Systems fast-track compliance through SOSA-aligned mission computers that combine 20-fold processing gains with certifiable design.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity Type: Air-to-Air Communications Redefine Flight Operations

Air-to-ground links commanded 45.40% of the 5G in Aviation Market industry size in 2025, benefiting from established tower infrastructure and immediate passenger-service needs. Air-to-air connectivity, however, is accelerating at a 43.2% CAGR. Direct aircraft-to-aircraft data exchange eliminates ground relays, shaving latency by 65% for collision-avoidance messages and enabling fuel-optimized formation flying. EchoStar’s hybrid satellite-5G contracts with Turkish AJet and Delta Airlines show commercial appetite for continuous, route-agnostic coverage.

Moving toward mesh networks marks a profound design shift, replacing hub-and-spoke traffic flows with dynamic peer links. SESAR’s 5G-AirSky trials recorded sub-12-millisecond delays, validating readiness for safety-critical messaging

By Offering: Software Platforms Drive Innovation Velocity

Service contracts spanning radio-planning, rollout, and managed operations held 37.80% of the 5G in Aviation Market industry share in 2025. Yet, software revenues are set for a 33.4% CAGR through 2031 as airlines favor virtual upgrades over hardware swaps. Gogo’s 5G protocol-stack emulation lets engineers fine-tune algorithms before airborne installation, preserving capital and accelerating feature releases.

Edge computing and network-slicing tools allow bespoke lanes for air-traffic data, cargo tracking, or passenger streaming without physical network duplication. Eurocontrol’s 2024 CNS Evolution Plan projects 15-20% efficiency gains for early adopters that embrace cloud-delivered services and AI-assisted automation.

By Application: Urban Air Mobility Emerges as Growth Catalyst

Passenger-experience platforms represented 51.20% of the 5G in Aviation Market industry in 2025, reflecting widespread cabin Wi-Fi retrofits. Drone and urban-air-mobility operations, however, are expanding at 44.8% CAGR as regulators open low-altitude corridors. The commercial-drone sector is on track to rise at a signficant rate, relying on 5G for beyond-visual-line-of-sight command and real-time telemetry.

Vertiport construction needs deterministic links for unmanned-traffic-management platforms. Hong Kong International Airport’s private network underpins vehicle-to-everything pilots and IoT baggage robots, showing how a single 5G layer boosts customer satisfaction and cuts operational overhead.

By Deployment Model: Private Networks Secure Critical Infrastructure

Private systems accounted for 43.30% of the 5G in Aviation Market industry size in 2025 and are projected to grow at a 36.2% CAGR. Aviation’s strict uptime and security thresholds favor on-premises core networks under airport or ANSP control. Ericsson and Streamwide’s deployment at Charles de Gaulle airport unifies push-to-talk, video, and messaging for 120,000 users, replacing a patchwork of analog radios and public-cellular contracts.

Moving from siloed subsystems to platform architectures lets operators tie RFID baggage belts, point-of-sale terminals, and CCTV feeds into one orchestration layer. Purdue University Airport’s testbed validates these scenarios in a live environment, accelerating certification and de-risking commercial rollouts.

By Stakeholder: ANSPs Drive Next-Generation Airspace Management

Airlines held the largest revenue slice at 48.20% in 2025, monetizing passenger-connectivity upgrades and inflight retail. Air-navigation service providers, though smaller today, are set for a 34.5% CAGR as they pivot toward cloud-hosted, service-oriented architectures. Eurocontrol’s roadmap envisions layered ATM built on 5G and satellite links, enabling predictive flow management and unmanned integration across Europe’s busiest corridors.

SESAR’s 78 active projects, backed by EUR 650 million (USD 757.4 million), include CNS-as-a-Service pilots that carve dedicated slices for low-altitude drone traffic without overloading legacy VHF channels. Early simulations point to 15-20% capacity gains and sharper conformance monitoring for mixed aircraft populations.

Geography Analysis

North America led the 5G in Aviation Market industry with 36.40% share in 2025, equivalent to USD 1.16 billion. The FAA earmarked USD 43.4 million in 2025 for airport-technology research, reinforcing public-sector commitment to integrated 5G testbeds. Commercial momentum is equally strong: Gogo’s planned nationwide aviation-only 5G network will upgrade more than 250 towers and blend licensed and unlicensed spectrum for resilient in-flight coverage.

Asia Pacific is matching the broader 32.17% CAGR, buoyed by national-scale 5G deployments and rising data-center capacity. China’s build-out and Hong Kong International Airport’s private network showcase position the region as a laboratory for connected ground-service vehicles and dynamic resource allocation. GSMA forecasts 5G will inject USD 130 billion into the regional economy by 2030, with aviation capturing a meaningful share.

Europe positions itself as an innovation hub through coordinated R&D and regulatory alignment. The UK’s 5G Innovation Regions program seeds airport pilots, while EASA’s Research Agenda 2025 prioritizes performance metrics for ATM ground equipment and spectrum coexistence frameworks vital to 5G deployment.

Competitive Landscape

Innovation and Integration Drive Market Success

Competition is moderate yet intensifying, with telecom vendors, satcom specialists, and IFEC providers forming cross-disciplinary alliances. Ericsson pairs radio-access leadership with aviation domain know-how from Saab at Purdue University, yielding live-traffic dashboards and ADS-B sensor fusion that heighten ground-movement visibility. The same vendor’s pact with Streamwide at Charles de Gaulle airport removed legacy radio silos, boosting worker collaboration across 120,000 staff.

Consolidation is reshaping strategic positions. Satcom Direct’s 2024 acquisition of Gogo for USD 375 million fuses ground-based and satellite pipelines into a single connectivity stack, diversifying revenue across cabin, cockpit, and operations. SpaceX’s Starlink has entered the arena through airline Wi-Fi agreements, adding LEO capacity that challenges incumbent GEO satcom providers.

Certification experience is a differentiator. Mercury Systems’ ROCK3 mission computer aligns to SOSA profiles, shortening avionics approval cycles and reinforcing the supplier’s standing in safety-critical compute.

5G in Aviation Industry Leaders

Telefonaktiebolaget LM Ericsson

SK Telecom Co. Ltd

KT Corporation

Deutsche Telekom AG

Gogo LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mercury Systems launched the ROCK3 safety-certifiable mission computer supporting 5G-enabled avionics.

- May 2025: Skyguide and ADB SAFEGATE partnered to modernize Swiss tower operations with 5G-ready electronic flight strips.

- April 2025: Transport Canada issued a Safety Alert establishing 5G exclusion zones at 35 airports to mitigate radio-altimeter interference.

- March 2025: The FAA mandated new RF band-pass filters for certain MHI RJ aircraft to shield altimeters from 5G C-Band signals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

In our analysis, we define the 5G in aviation market as the global revenue earned from 5G radio-access equipment, core network software, and managed services that enable ground-to-ground, air-to-ground, and air-to-air links for commercial, general, and unmanned aviation stakeholders. We count spending by airlines, airports, MROs, air-navigation service providers, and system integrators across both public and private deployments.

We exclude satellite bandwidth sold outside a 5G backhaul chain and any legacy 4G or Ku/Ka-band connectivity fees.

Segmentation Overview

- By Connectivity Type

- Ground-to-Ground Communication

- Air-to-Ground Communication

- Air-to-Air Communication

- By Offering

- Hardware

- Software

- Services

- By Application

- Passenger Experience

- In-flight Wi-Fi

- AR/VR Entertainment

- Airport Operations

- Baggage and Cargo Tracking

- Smart Security and Border Control

- Flight Operations

- Real-time Flight Tracking

- Predictive Maintenance Telemetry

- Drone and Urban Air Mobility Operations

- Passenger Experience

- By Deployment Model

- Public 5G Networks

- Private 5G Networks

- Hybrid Networks

- By Stakeholder

- Airlines

- Airports

- MRO Providers

- ANSPs

- OEMs

- Passengers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview airport CIOs, airline connectivity leads, tower OEM engineers, and regional telecom regulators across North America, Europe, Asia-Pacific, and the Middle East; we confirm adoption timing, spectrum clearances, and average selling prices.

Desk Research

We start with FAA, EASA, ICAO, and FCC datasets for fleet size, airport counts, spectrum allocation, and safety advisories. Passenger-kilometer trends from IATA and base-station density benchmarks from GSMA complement those figures. Company filings, investor decks, and trusted press, accessed via D&B Hoovers and Dow Jones Factiva, reveal contract values and capital budgets. This list is illustrative; many additional documents inform every refresh.

During a second pass, we validate unit-cost curves through Questel patent analytics and price disclosures in national telecom consultations, grounding all assumptions in verifiable signals.

Market-Sizing & Forecasting

We build a top-down demand pool from passenger traffic, average connected flight hours, and 5G penetration, then cross-check it with selective bottom-up roll-ups of announced base-station orders and retrofit quotes. Key variables like unit hardware cost, equipped-aircraft share, private-network penetration, spectrum pricing, and data-usage uplift feed a multivariate regression that projects value through 2030. Where supplier roll-ups under-report emerging regions, import-shipment data provide adjustment factors.

Data Validation & Update Cycle

Our analysts compare model outputs with independent fleet trackers, capex surveys, and currency benchmarks, resolving anomalies before sign-off. Reports refresh annually, with interim updates when major contracts, rulings, or technology launches shift the outlook.

Why Mordor's 5G In Aviation Baseline Commands Confidence

Published estimates differ because scope, baseline year, and adoption curves vary.

By auditing variables yearly and aligning scope with real spend, we narrow those gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.20 B (2025) | Mordor Intelligence | |

| USD 2.68 B (2024) | Global Consultancy A | Focus on airborne Wi-Fi hardware; ignores airport private networks |

| USD 1.77 B (2024) | Trade Journal B | Omits private 5G deployments and assumes uptake only after 2028 |

We believe these contrasts show how Mordor's balanced mix of real traffic drivers, timely data, and transparent steps offers the most dependable baseline for decision-makers.

Key Questions Answered in the Report

What is the current value of the 5G in Aviation Market industry?

The 5G in Aviation Market industryDriver (~) % Impact on CAGR Forecast Geographic Relevance Impact Timeline Proliferation of IFEC demand +5.0% Global; strongest in North America & Europe Medium term (2–4 years) Airport digital-transformation programs +4.2% Global; dense in APAC and Middle East Medium term (2–4 years) Rapid expansion of aviation IoT sensors and edge computing +3.8% North America, Europe, advanced APAC hubs Short term (≤ 2 years) National 5G spectrum auctions and aviation testbeds +3.5% Global; regulatory variation by region Medium term (2–4 years) 5G-enabled Advanced Air Mobility corridors +3.1% North America, Japan, South Korea, UAE Medium term (2–4 years) Real-time 8K cabin analytics for ancillary-revenue upselling +2.7% Global early adopters; strongest in premium airlines Short term (≤ 2 years)size is USD 4.23 billion in 2026 and is projected to climb to USD 17.05 billion by 2031.

Which connectivity type is expanding the fastest?

Air-to-air communication tops the growth chart with a 43.2% CAGR between 2026-2031, enabled by direct aircraft-to-aircraft data exchange.

Why are private 5G networks preferred at airports?

They deliver deterministic coverage, resilient security, and tailored performance that public networks cannot guarantee for mission-critical airport processes.

How does 5G support urban-air-mobility operations?

Low-latency links allow drones and eVTOL aircraft to fly beyond visual line of sight, while network slicing allocates dedicated bandwidth for unmanned-traffic management.

What are the biggest hurdles to 5G adoption in aviation?

High upfront capital for private infrastructure and stringent cybersecurity–safety certification timelines can add 15-25% costs and 12-18 months to rollout periods.

Which region will grow the fastest through 2031?

Asia Pacific matches the global 32.17% CAGR as China, Singapore, and Hong Kong accelerate private-network deployments and supportive regulation.

Page last updated on: