3D Animation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 31.49 Billion |

| Market Size (2031) | USD 54.36 Billion |

| Growth Rate (2025 - 2031) | 11.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Animation Market Analysis by Mordor Intelligence

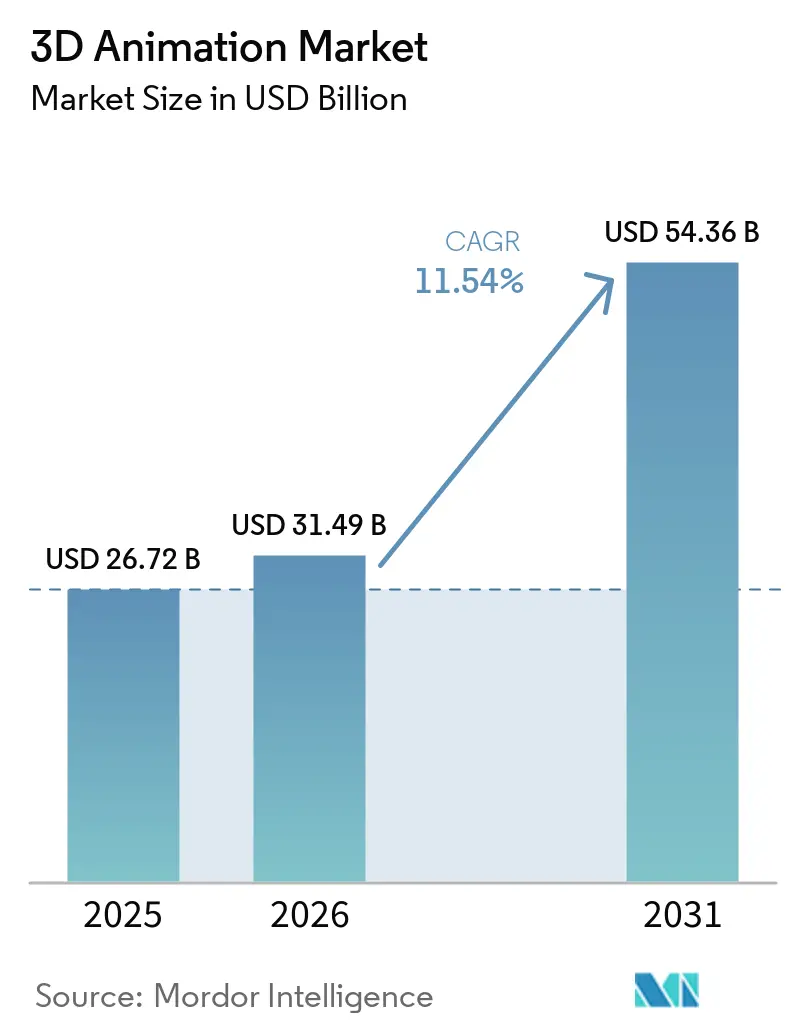

The 3D animation market size is expected to grow from USD 26.72 billion in 2025 to USD 31.49 billion in 2026 and is forecast to reach USD 54.36 billion by 2031 at 11.54% CAGR over 2026-2031. Demand from streaming platforms and film studios continued to keep high-quality animation and visual effects work active across major production hubs. AI-assisted rigging, real-time production workflows, and broader use of shared asset standards shortened delivery cycles and changed how studios planned labor, software, and infrastructure. The use of 3D visualization also widened beyond entertainment, with healthcare, architecture, engineering, construction, and enterprise training creating new demand for precision rendering and simulation-based content. Competition tightened as established software vendors added AI-native features to defend installed user bases, while cloud and managed service providers tried to win larger creative workloads through rendering, integration, and pipeline support. Growth remained exposed to rising compute and licensing costs, a limited pool of production-ready technical talent, and unresolved legal questions around AI-assisted content ownership and indemnification.

Key Report Takeaways

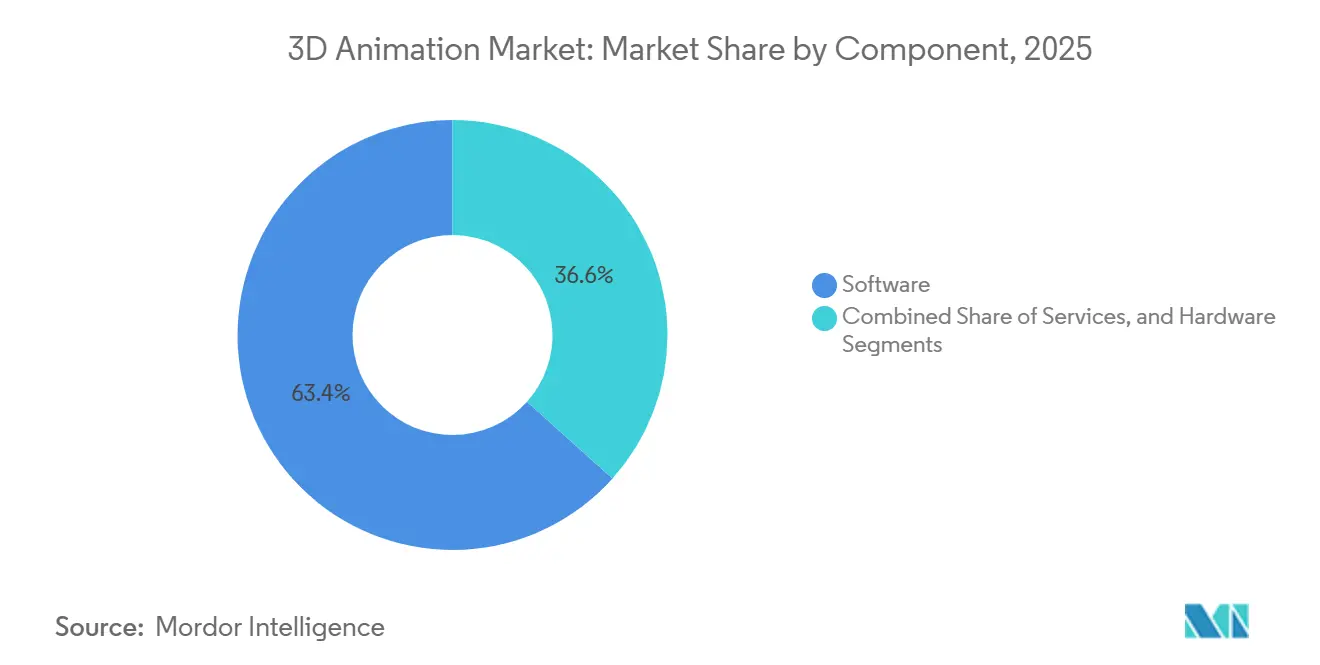

- By component, software held the largest share of 63.37% of the 3D animation market in 2025, while services are projected to expand at a 12.14% CAGR through 2031.

- By deployment mode, on-premise held 59.91% of the 3D animation market share in 2025, while cloud is expected to record the fastest growth at 11.92% CAGR through 2031.

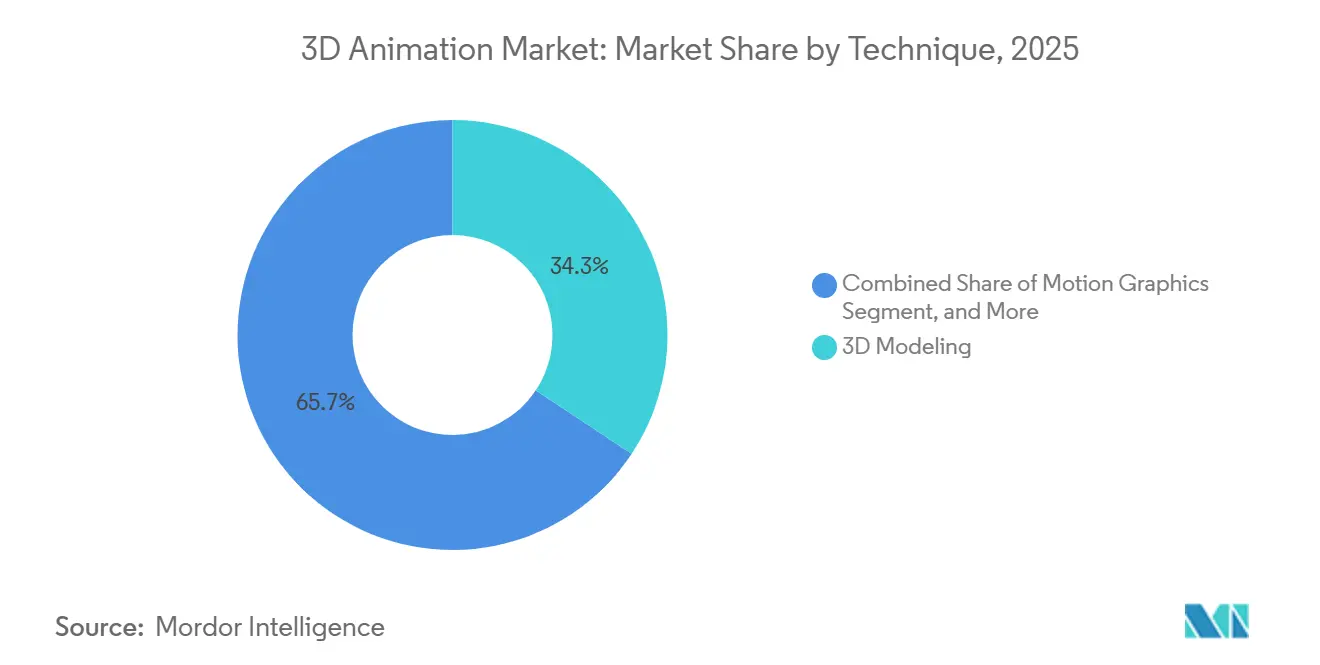

- By technique, 3D modeling accounted for 34.31% of the 3D animation market in 2025 and remained the fastest-growing technique category through 2031 with 12.31% CAGR.

- By end use, media and entertainment led with a 37.83% revenue share in 2025, while gaming is projected to expand at a 13.09% CAGR through 2031.

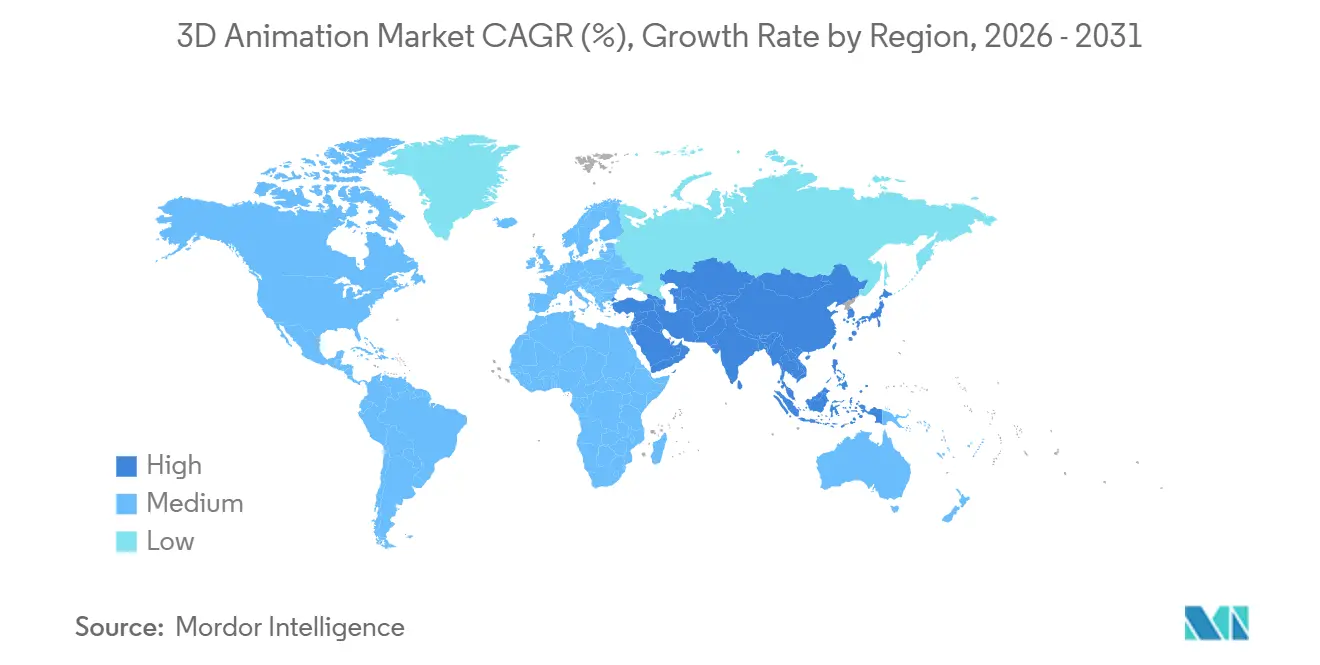

- By geography, North America led with 39.84% of global revenue in 2025, while Asia-Pacific remained the fastest-growing regional cluster, with a 12.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 3D Animation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising VFX Demand Across Streaming and Film | +3.2% | Global | Short term (≤ 2 years) |

| Expanding Game and Esports Content Pipelines | +2.5% | North America and Asia-Pacific | Medium term (2-4 years) |

| Wider Use of 3D Animation in Healthcare, Architecture, and Training | +1.8% | North America and Europe | Medium term (2-4 years) |

| AI Rigging and AI-Assisted Character Pipeline Compression | +1.5% | Global | Short term (≤ 2 years) |

| Cloud-Based Tool Access for Small and Mid-Sized Studios | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| OpenUSD-Based Asset Interoperability Across Creation Pipelines | +0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising VFX Demand Across Streaming and Film

Premium streaming platforms continued to prioritize visual quality as a core driver of subscriber retention, keeping demand for animation and effects work elevated across the 3D animation market. Disney committed USD 24 billion in content investment for fiscal year 2026, showing that large content owners still supported aggressive production pipelines even as cost discipline became more visible. Netflix launched INKubator in May 2026 as an artist-led, GenAI-native animation studio, demonstrating that major platforms were investing directly in internal production systems rather than relying solely on external vendors. Netflix also opened Eyeline Studios in Hyderabad in March 2026, expanding high-end visual effects capacity into a production market that previously sat outside the first tier of global facility networks. Amazon, MGM Studios, and AWS launched Project Nara in April 2026, cutting pilot timelines from 3-6 months to 5 weeks and signaling that infrastructure-backed speed had become part of the creative value proposition in the 3D animation market. As a result, content demand in this market was no longer driven only by volume, because it was increasingly tied to how quickly studios could move from concept to production-ready output.

Expanding Game and Esports Content Pipelines

The esports economy created a steady stream of short-cycle content work, pushing the 3D animation market beyond traditional film and game launch schedules. Broadcast packages, branded sequences, cinematic intros, and real-time effects all required high-quality 3D assets with tighter revision windows than most film productions. The Valorant Champions 2026 activation for Red Bull used bespoke 3D integration assets and real-time visual effects, reflecting the level of polish now expected at large esports events. This pattern favored cloud rendering, modular assets, and AI-assisted content generation because teams needed to iterate quickly across events, sponsors, and formats. The 3D animation market also benefited from the expansion of esports infrastructure in the United States, South Korea, and Saudi Arabia, broadening the regional demand base for professional production services.

Wider Use of 3D Animation in Healthcare, Architecture, and Training

The 3D animation market expanded further into healthcare, architecture, and training, where accuracy and repeatability mattered as much as visual quality. A PLOS ONE study published in April 2025 documented an open-source workflow for anatomically accurate digital organ models used in surgical simulation and training, with future augmented reality integration identified as a logical next step. That work showed that medical use cases were moving beyond simple visualization and into structured training environments with reproducible model requirements.[1]Ikeuchi et al., “Development of Anatomically Accurate Digital Organ Models for Surgical Simulation and Training,” PLOS ONE, journals.plos.org In architecture, Maxon formally entered the AEC market in March 2026, with Redshift for Vectorworks available, an Autodesk Revit beta launched, and a Graphisoft Archicad integration planned for later in 2026. These moves mattered because AEC and healthcare buyers often operate on longer procurement cycles and require stronger workflow reliability than entertainment clients. Once embedded, these customers tend to raise switching costs for vendors in the 3D animation market through compliance, validation, and integration needs.

AI Rigging and AI-Assisted Character Pipeline Compression

AI-assisted rigging changed the economics of the 3D animation market by compressing one of the most labor-intensive stages in character production. Autodesk introduced MotionMaker in Maya 2026.1 in June 2025, demonstrating that a 10-second locomotion task that once required 2 weeks of manual work could be generated in 1 minute. That level of compression reduced repetitive work and pushed studios to reconsider how much manual rigging labor they needed on each show. The UniRig paper presented at SIGGRAPH 2025 introduced a unified autoregressive framework for automatic skeleton prediction and skinning weight assignment across diverse asset types, with better benchmark performance in skeletal accuracy and skinning quality. Autodesk then extended MotionMaker to horse archetypes in Maya 2027 and added OTIO-based workflow improvements in Maya 2027.1, demonstrating that AI coverage was expanding rapidly across production needs. The result was a 3D animation market where smaller studios could narrow delivery-speed gaps with larger incumbents, while large studios faced more pressure to justify labor-heavy legacy workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Compute, Licensing, and Talent Costs | -1.8% | Global | Medium term (2-4 years) |

| Shortage of Production-Ready Technical Artists and Animators | -1.2% | North America and Europe | Long term (≥ 4 years) |

| Copyright Ambiguity Around AI-Assisted Outputs | -0.8% | Global | Short term (≤ 2 years) |

| Software Piracy and Compliance Leakage | -0.5% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Compute, Licensing, and Talent Costs

The 3D animation market remained expensive to operate at a high quality level, especially for mid-sized studios that could not spread fixed costs across large project slates. Cloud GPU demand rose sharply, and AWS capacity tied to Project Nara alone was projected to account for 15% of total AWS GPU allocation by year-end 2026, pointing to tighter infrastructure availability and margin pressure. Licensing costs added to that pressure, because a professional Cinema 4D subscription costs USD 109 per month or USD 839 per year before studios added rendering, compositing, motion capture, or collaboration tools. Those software costs were only part of the picture, because experienced technical artists and pipeline specialists still commanded premium compensation in major production centers. Many firms in the 3D animation market, therefore, delayed upgrades, mixed paid and open-source tools, or moved selected workloads to external partners to avoid locking in high fixed costs. That response helped control spending, but it also increased compatibility risk and made workflow standardization harder across projects.

Shortage of Production-Ready Technical Artists and Animators

The 3D animation market still faced a talent bottleneck, especially for technical artists who could manage both creative output and pipeline logic. The core issue was not only the number of graduates entering the field, but also that many academic programs still lagged behind commercial workflows built around OpenUSD, AI tools, and real-time engines. This created a gap between entry-level skill sets and the production-ready capabilities studios needed for live projects. Amazon’s projection that Project Nara could automate 40% of routine animation tasks did not remove the need for skilled workers, because it shifted demand toward supervision, prompt design, review, and pipeline control. In the 3D animation market, that meant studios still had to spend on retraining and workflow redesign, even when automation reduced repetitive manual work.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Managed Services Are Becoming Essential to Pipeline Planning

Software held the largest share of 63.37% in the 3D animation market in 2025, reflecting studios' long-standing reliance on core authoring, rigging, simulation, rendering, and compositing tools. Autodesk’s Maya and Arnold stack remained central to character and production workflows, while Maxon’s Maxon One bundle brought Cinema 4D, ZBrush, Redshift, and Red Giant into a single subscription model that reinforced recurring software spend.[2]Evan Atherton, “Meet MotionMaker: Maya’s New AI Animation Tool,” Autodesk Media and Entertainment Blog, blogs.autodesk.com Hardware occupied a smaller share, but it stayed relevant because GPU upgrades, motion capture devices, and review systems still shaped production performance and real-time capability. Services were the fastest-growing component in the 3D animation market and were projected to expand at a 12.14% CAGR from 2026 to 2031. That growth reflected the need for flexible rendering capacity, pipeline integration, and outsourced content production without large capital commitments.

Studios across the 3D animation industry increasingly treated rendering and pipeline management as variable operating costs rather than fixed infrastructure decisions. Project Nara illustrated this direction by combining production tooling, AI support, and managed compute into a single workflow environment. OpenUSD adoption also supported services demand, because more studios needed integration, migration, and consulting support after the OpenUSD Core Specification 1.0 was ratified in 2025. Training and support services remained smaller, but they stayed relevant where teams had to adapt quickly to new AI features and cross-application workflows. This kept the component mix in the 3D animation market tilted toward software leadership, while services captured a larger share of incremental growth.

By Deployment Mode: On-Premise Still Leads While Cloud Keeps Advancing

On-premises deployment retained a 59.91% share of the 3D animation market in 2025, indicating that major studios still preferred control over their core production environments. Large facilities continued to value predictable frame throughput, stronger security over proprietary assets, and the ability to customize pipelines without depending on shared cloud capacity. That preference was especially strong in feature film and episodic work, where delivery delays could disrupt entire production schedules. Hardware improvements also helped keep internal rendering viable for studios with enough frame volume to justify dedicated infrastructure. In practice, this meant the 3D animation market still relied heavily on on-premises compute for its most intensive workloads.

Cloud was the fastest-growing deployment mode in the 3D animation market, with a CAGR of 11.92%, as smaller studios, ad agencies, and cross-disciplinary teams needed elastic access to compute and collaborative tools. Blackmagic Design’s public beta release of Fusion Studio 20.x in December 2025 included architectural improvements that enabled broader cloud compatibility. Rokoko also launched Rokoko Create in April 2026 as a browser-based text-to-animation tool, which showed how vendors were designing lighter access points that did not require heavy local setups. As interoperability improves through OpenUSD and similar standards, cloud adoption in the 3D animation market is likely to face less integration friction than it did in older pipeline models. Independent studios in emerging markets stand to benefit first because cloud access reduces the capital barrier that once limited entry into high-end production.

By Technique: 3D Modeling Remains the Core Layer of Production

3D Modeling accounted for 34.31% of the 3D animation market in 2025 and remained the fastest-growing technique with a CAGR of 12.31% throughout the forecast period. Its lead reflected the simple fact that nearly every downstream workflow, from effects to motion graphics, still started with model creation and asset preparation. That structural position made modeling less exposed to fluctuations in any one end-use vertical. The UniRig research presented at SIGGRAPH 2025 showed that even foundational asset preparation was entering a new phase of automation, with stronger results in skeletal prediction and skinning across different 3D categories. This supported the view that the 3D animation market was accelerating at the base layer of the pipeline rather than only at specialized downstream stages.

Visual effects held the second-largest share of techniques, driven by streaming and film demand that continued to favor complex shots and higher asset density. Motion graphics expanded quickly in branded content and esports, where shorter campaign cycles favored iterative production and faster turnarounds. 3D rendering also became more distinct as a commercial workload, because rendering-as-a-service and GPU-based delivery models separated compute from content authoring. Maxon’s expansion of Redshift into Vectorworks and Revit workflows showed how rendering tools were being positioned for clients outside core entertainment. The 3D animation market, therefore, showed a mix of techniques in which modeling remained central, while rendering and visual effects continued to gain new demand in adjacent verticals.

By End-User Industry: Gaming Sets the Growth Pace While Enterprise Verticals Broaden Demand

Media and entertainment accounted for 37.83% of the 3D animation market in 2025, making it the largest end-use segment. Streaming platforms continue to influence this market by supporting large content pipelines and increasingly building internal animation capacity. Netflix’s launch of INKubator and the expansion of Eyeline Studios reflected a move toward more direct ownership of production systems and creative infrastructure. Gaming was the fastest-growing end-use area, with the 3D animation market size for gaming projected to expand at a 13.09% CAGR from 2026 to 2031. The growth pattern showed that game publishers now operated more like continuous content studios, with live-service updates, cinematic assets, and esports production all adding to content volume.

The 3D animation industry also found room to grow in healthcare and AEC, where demand was less tied to entertainment cycles and more to workflow accuracy and long-term integration needs. The PLOS ONE study on anatomical digital organ models supported the growing role of simulation-led medical content and structured training environments. Maxon’s formal entry into AEC in March 2026 showed that major vendors were now allocating product resources to architecture visualization and related procurement channels. Advertising and marketing remained stable, but shorter campaign cycles pushed more work toward templated motion graphics and reusable assets. Education and training, manufacturing and industrial, and government and defense remained smaller in revenue, yet they offered higher-value contracts where fidelity and simulation requirements were critical.

Geography Analysis

North America held 39.84% of the 3D animation market share in 2025, which made it the leading regional cluster by revenue. The United States drove much of that position through the concentration of major studios, streaming platforms, AAA game publishers, and software vendors that anchored procurement and R&D. Disney’s fiscal 2026 content spending plans and Netflix’s broader studio build-out showed that high-end production demand remained concentrated in this region even as some capacity expanded abroad. Canada continued to benefit from tax credits and a mature animation cluster, and Rodeo FX’s acquisition of Mikros Animation in March 2025 strengthened its integrated VFX and animation footprint. Mexico remained an emerging outsourcing location in the 3D animation market, but its pipeline maturity still trailed hubs such as Vancouver and Los Angeles.

Asia-Pacific was the fastest-growing region, with a 12.48% CAGR in the 3D animation market, and India and China were the clearest growth engines. Netflix opened Eyeline Studios in Hyderabad in March 2026, spanning 32,000 sq. ft., formally bringing India into Netflix’s top-tier VFX network alongside Los Angeles, Vancouver, Seoul, and London. China’s animated film box office reached CNY 25 billion (USD 3.47 billion) in 2025, accounting for close to 50% of the country’s total theatrical box office, indicating that domestic animation demand had entered a structurally larger phase. South Korea continued to serve as an outsourcing destination for animation and VFX work, while Japan pushed further into integrated production and distribution with U-NEXT Holdings’ acquisition of GoHands in May 2026. The 3D animation market in Asia-Pacific also had an industrial layer that was becoming more important, because OpenUSD adoption in manufacturing and digital twin environments suggested another route to future demand.[3]Alliance for OpenUSD, “AOUSD Year in Review: A Landmark Year for OpenUSD Standardization and Growth in 2025,” AOUSD, aousd.org

Strong independent production ecosystems in the United Kingdom, Germany, and France supported Europe’s 3D animation market. The United Kingdom benefited from tax incentives for high-end television production, which supported demand for compositing and effects tools. Germany stood out for enterprise use cases, where OpenUSD-based digital twin workflows opened new procurement paths tied to manufacturing and engineering applications. South America, the Middle East, and Africa remained smaller, but the 3D animation market gained support from event-led content demand in Saudi Arabia, creative technology incentives in the UAE, and co-production links between South Africa and European broadcasters.

Competitive Landscape

The 3D animation market remained moderately fragmented, with Autodesk and Maxon anchoring the commercial software layer, while the Blender Foundation competed on the open-source side. No single vendor controlled a majority position, because the market was split across authoring tools, rendering specialists, compositing software, motion capture providers, and workflow standards. Autodesk strengthened its position by rolling out MotionMaker across successive Maya releases from June 2025 to May 2026, demonstrating a steady strategy to expand AI capabilities within an established product family. Maxon pursued a different path in the 3D animation market by widening its product reach across AEC, mobile workflows, and subscription bundling.[4]Maxon Computer GmbH, “Maxon Announces Free Tools and Mobile Expansion of ZBrush and Cinema 4D,” Maxon, maxon.net Blender continued to pressure mid-tier paid tools because its open-source model lowered entry barriers for independent creators and some professional pipelines.

Standards also became a competitive tool in the 3D animation market, not just a technical one. The ratification of the OpenUSD Core Specification 1.0 in 2025, alongside AOUSD membership growth to 50 general and 88 contributor organizations, pushed interoperability higher on studio procurement agendas. Vendors with deeper USD workflow alignment gained an advantage because clients increasingly wanted asset portability across applications and teams. This weakened some of the negotiating leverage that once came from proprietary lock-in.

The next layer of competition in the 3D animation market centered on AI-native workflow access, real-time production, and hardware-software convergence. Rokoko’s browser-based Rokoko Create lowered the barrier to text-to-animation workflows and challenged demand for entry-level motion capture and basic animation services. Blackmagic Design’s URSA Cine Immersive 100G launch in April 2026 showed that spatial and immersive production was becoming a more visible strategic target for vendors that combined cameras, software, and live production tools. At the same time, anticipated AI content-labeling scrutiny in late 2026 suggested that larger vendors with legal and compliance depth could be better positioned than small entrants if rules around disclosure and indemnification tightened. That dynamic kept the 3D animation market open to innovation, but it also elevated the value of scale, alignment with standards, and compliance readiness.

3D Animation Industry Leaders

Maxon Computer GmbH

Side Effects Software Inc.

The Foundry Visionmongers Limited

Chaos Software EOOD

Reallusion Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Netflix confirmed the launch of INKubator, described as an artist-led, GenAI-native animation studio, structured to develop animated shorts and specials using AI-driven pipelines, with stated ambitions to scale toward feature-quality content and longer-form productions based on Netflix's existing IP catalog.

- May 2026: Autodesk released Maya 2027.1, adding OpenTimelineIO (OTIO) support to the Sequencer for multi-DCC shot data interchange, Arnold 5.6.1.1 with custom AOVs for volume shaders, additional MotionMaker workflow improvements, and Smart Bevel system enhancements.

- May 2026: U-NEXT Holdings, Japan's largest streaming platform, announced the acquisition of GoHands, an anime studio, as a wholly owned subsidiary, effective June 1, 2026, targeting cost reductions and productivity improvements through digital technology integration across its streaming-to-production value chain.

- April 2026: Amazon, MGM Studios, and AWS launched the GenAI Creators' Fund and Project Nara, an in-house generative-AI production platform, 3 animated series were piloted in 5 weeks, compared to a traditional 3-to-6-month timeline, with Project Nara projected to automate 40% of routine animation tasks and consume 15% of AWS's total GPU capacity by year-end 2026.

Global 3D Animation Market Report Scope

The 3D Animation Market encompasses software, hardware, cloud platforms, and professional services used to create, manipulate, render, and deploy three-dimensional digital content for visual communication, entertainment, simulation, and interactive applications. 3D animation involves developing digital models, characters, environments, visual effects, and motion sequences using computer-generated imagery (CGI), enabling realistic, immersive visual experiences across multiple industries.

The 3D Animation Market Report is Segmented by Component (Software, Hardware, and Services), Deployment Mode (On-Premise, and Cloud), Technique (3D Modeling, Motion Graphics, 3D Rendering, and Visual Effects), End-User Industry (Media and Entertainment, Gaming, Advertising and Marketing, Architecture, Engineering, and Construction, Healthcare and Life Sciences, Education and Training, Manufacturing and Industrial, and Government and Defense), Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Hardware |

| Services |

| On-premise |

| Cloud |

| 3D Modeling |

| Motion Graphics |

| 3D Rendering |

| Visual Effects |

| Media and Entertainment |

| Gaming |

| Advertising and Marketing |

| Architecture, Engineering, and Construction |

| Healthcare and Life Sciences |

| Education and Training |

| Manufacturing and Industrial |

| Government and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Hardware | ||

| Services | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| By Technique | 3D Modeling | |

| Motion Graphics | ||

| 3D Rendering | ||

| Visual Effects | ||

| By End-User Industry | Media and Entertainment | |

| Gaming | ||

| Advertising and Marketing | ||

| Architecture, Engineering, and Construction | ||

| Healthcare and Life Sciences | ||

| Education and Training | ||

| Manufacturing and Industrial | ||

| Government and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the 3D animation market in 2026 and how fast is it expected to grow?

The 3D animation market stood at USD 31.49 billion in 2026 and is forecast to reach USD 54.36 billion by 2031, growing at an 11.54% CAGR over 2026-2031.

Which region leads global revenue for 3D animation?

North America led global revenue with a 39.84% share in 2025, supported by the concentration of major studios, streaming platforms, and software vendors.

Which deployment model is currently dominant in 3D animation workflows?

On-premise remained the largest deployment mode in 2025 with a 59.91% share, mainly because large studios still prioritize security, throughput control, and pipeline customization.

Which end-use area is growing the fastest?

Gaming is the fastest-growing end-use segment, with a projected 13.09% CAGR through 2031 as publishers expand cinematic content, live-service assets, and esports production.

Why are managed services gaining traction in 3D production?

Studios are using managed rendering, pipeline integration, and outsourced content support to reduce fixed-cost exposure and scale capacity more flexibly, which is why services are the fastest-growing component segment at 12.14% CAGR.

What are the main risks affecting growth through 2031?

The main risks are rising compute and licensing costs, shortages of production-ready technical talent, and legal uncertainty around AI-assisted output and content ownership.

Page last updated on: