Animation Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

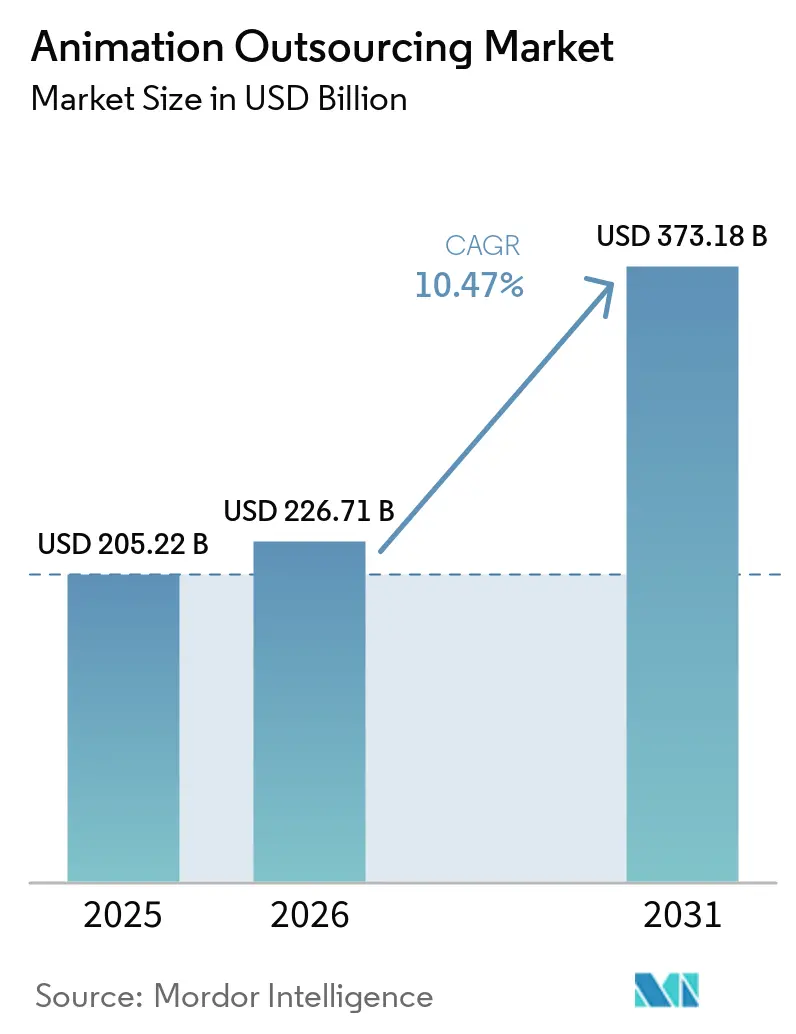

| Market Size (2026) | USD 226.71 Billion |

| Market Size (2031) | USD 373.18 Billion |

| Growth Rate (2026 - 2031) | 10.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animation Outsourcing Market Analysis by Mordor Intelligence

The Animation Outsourcing market size in 2026 is estimated at USD 226.71 billion, growing from 2025 value of USD 205.22 billion with 2031 projections showing USD 373.18 billion, growing at 10.47% CAGR over 2026-2031. The Animation Outsourcing market has moved from cost arbitrage toward strategic partnerships that supply specialized talent and cutting-edge pipelines demanded by streaming, gaming, and advertising clients. Robust demand for original IP across global platforms is pulling new work into Asia-Pacific hubs, while North American studios retain most creative pre-production activity. Tax-credit rivalries in Canada, the UK, and France continue to redirect production budgets, and real-time engines plus generative AI are reshaping schedules and lowering entry barriers for boutique vendors. Competitive intensity stays high because fragmented suppliers differentiate on technology and niche expertise rather than price alone.

Key Report Takeaways

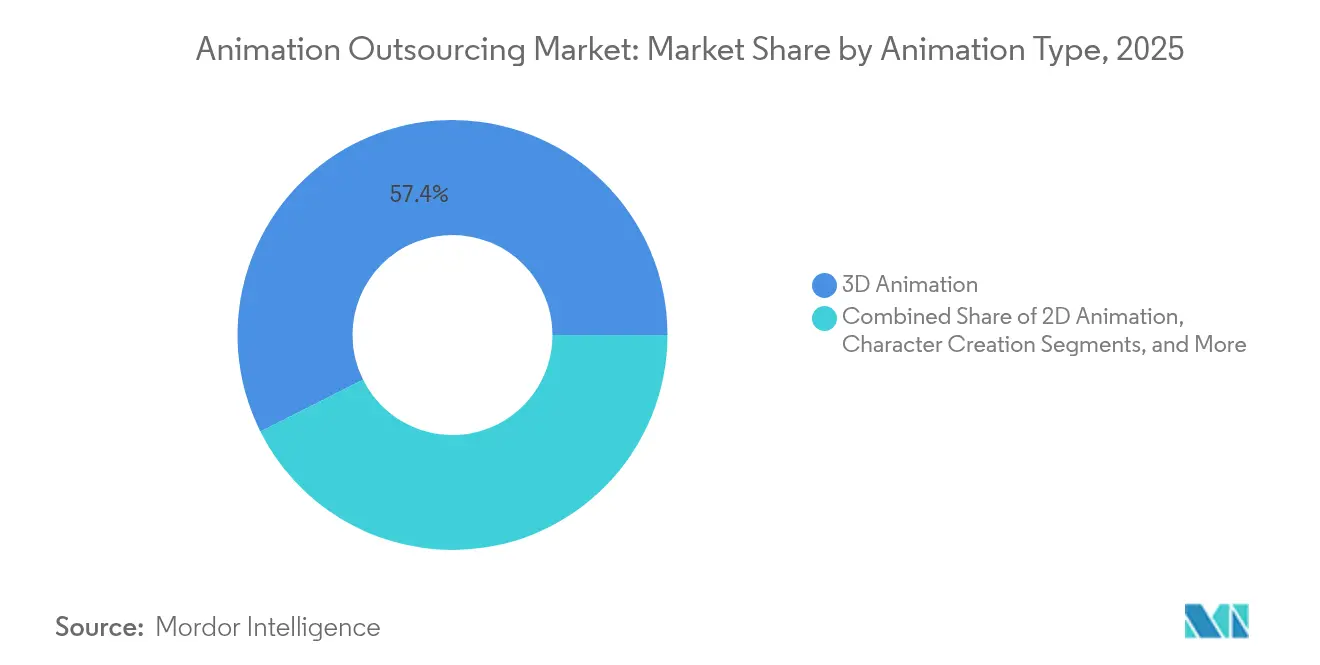

- By animation type, 3D captured 57.40% of Animation Outsourcing market share in 2025, while motion graphics is projected to grow at a 12.58% CAGR to 2031.

- By production stage, production services accounted for 51.30% of the Animation Outsourcing market size in 2025; post-production and VFX record the fastest CAGR at 12.92% through 2031.

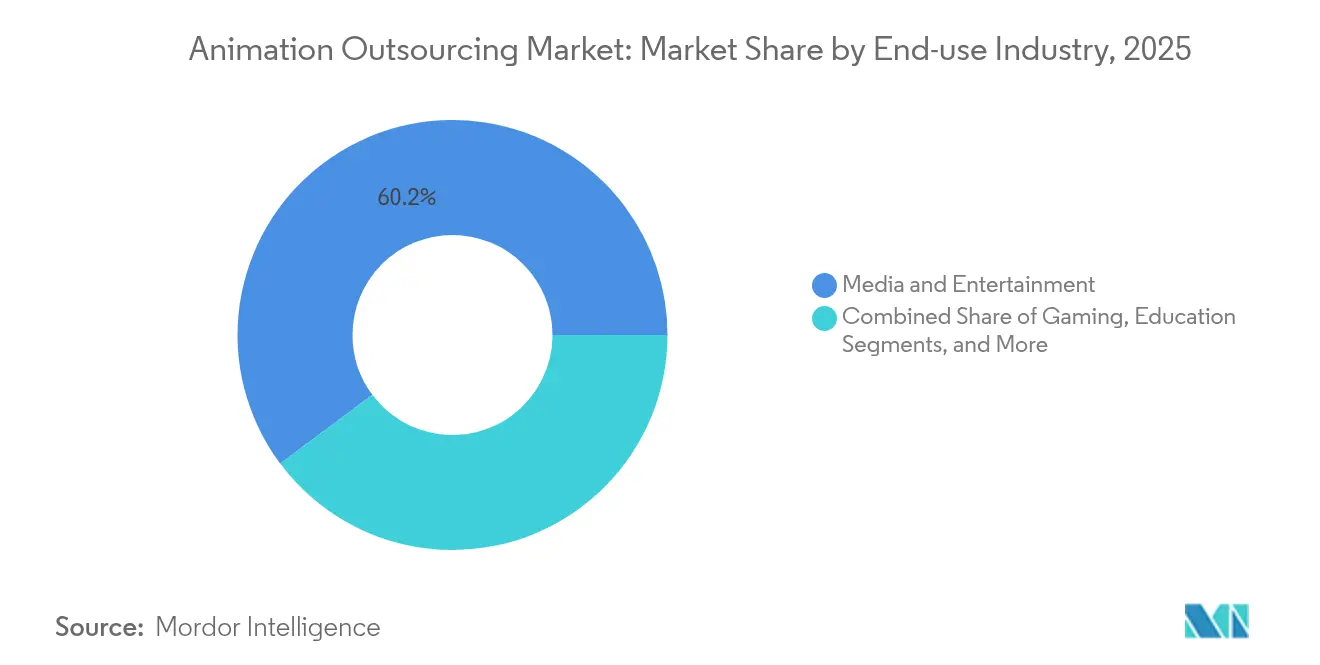

- By end-use industry, media and entertainment held 60.20% of Animation Outsourcing market share in 2025, whereas gaming shows a 14.24% CAGR over the forecast period.

- By platform, OTT/streaming originals are advancing at 14.93% CAGR, surpassing film and television growth rates.

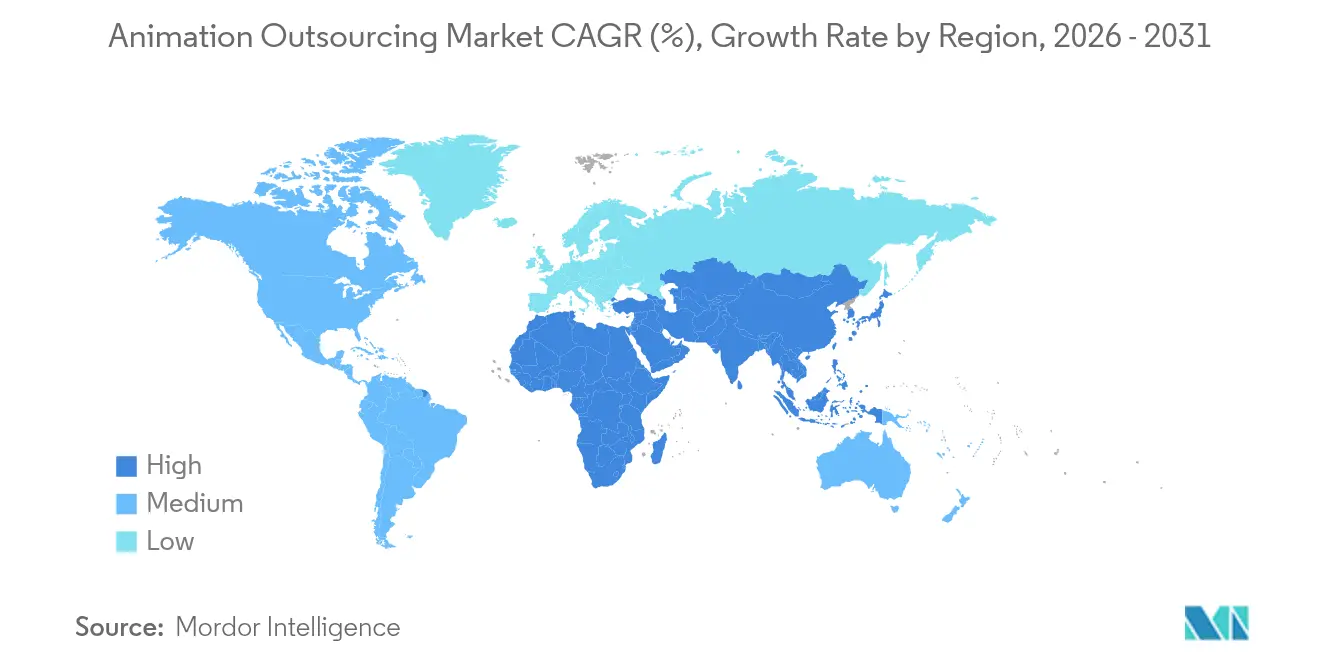

- By region, Asia-Pacific is the fastest-growing area at 11.82% CAGR, while North America retains 33.60% revenue share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Animation Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in original content spend by streaming giants fueling APAC 3D pipelines | +3.5% | Global; APAC hubs | Medium term (2-4 years) |

| Tight studio release windows driving near-shore hybrid production (US-Mexico) | +2.8% | North America; Latin America | Short term (≤ 2 years) |

| Tax-incentive race in Canada, UK & France boosting outsourced post-production | +2.1% | North America; Europe | Medium term (2-4 years) |

| Mobile gaming boom in China & India elevating demand for cost-efficient character rigging | +1.7% | Asia-Pacific | Medium term (2-4 years) |

| Real-time engines enabling virtual production outsourcing for advertisers | +1.4% | Global | Long term (≥ 4 years) |

| Generative-AI-powered rapid concept art increasing outsourcing volumes | +1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in original content spend by streaming giants fueling APAC 3D pipelines

Global platforms prioritized volume in 2025, commissioning entire seasons of animated series upfront to accelerate subscriber growth. Disney’s multiyear content budget and similar allocations from Netflix and Amazon overloaded domestic facilities, pushing 3D series work into Indian and South Korean studios where labor pools scaled rapidly.[1]“Content Spending by Streaming Giants 2024.” crystalcapitalpartners.com Regional vendors upgraded pipelines with USD 200 million in combined investments to meet HDR and Dolby Atmos standards demanded by clients. Government support amplified momentum, with South Korea funding R&D grants that subsidize up to 30% of real-time engine adoption costs.[2]“South Korea Invests USD 106 Million in Animation.” animemojo.com As deal flow rises, APAC suppliers secure longer retainer contracts that stabilize utilization rates. These factors collectively elevate the Animation Outsourcing market growth path through mid-decade.

Tight studio release windows driving near-shore hybrid production

Franchise sequels and streaming spin-offs now target 18-month turnarounds, compressing traditional schedules by nearly 25%. To bridge gaps, Hollywood showrunners increasingly lean on Guadalajara and Mexico City boutiques that synchronize daily reviews over shared daylight hours.[3]Animation Guild. “Outsourcing Trends Update 2024.” animationguild.org Bilingual teams reduce revision cycles, while cross-border co-production treaties simplify asset transfers under aligned IP law. Mexican facilities reported a 38% rise in Storyboard Pro license counts in 2024, signaling deeper integration into pre-visualization stages. This hybrid approach anchors critical path tasks near the U.S. creative core and delegates render-intensive shots southward, reinforcing agility in the Animation Outsourcing market pipeline.

Tax-incentive race in Canada, UK and France boosting outsourced post-production

Financial incentives intensified in 2025 as the UK Audio-Visual Expenditure Credit rose to an effective 23.4% cash benefit, matching aggressive schemes in British Columbia and Quebec. Producers now routinely split shows across multiple jurisdictions to stack rebates, with compositing and lighting finalized in Montreal while layout occurs in London hubs. The policy-driven arbitrage lowered average post-production budgets by 14% for mid-tier series in 2024. Talent clusters flourished around these credits, adding 6,800 new VFX artists in Canada alone. Such dynamics make fiscal optimization a core strategic lever inside the Animation Outsourcing market.

Mobile gaming boom in China and India elevating demand for cost-efficient character rigging

Mobile titles accounted for three-quarters of global game revenues in 2024, spurring nonstop content drops that strain internal art teams. Publishers outsourcing low-poly rigging to Indian studios cut asset costs by 35% while meeting weekly live-ops deadlines.[4]India Brand Equity Foundation. “AVGC Sector Landscape 2025.” ibef.org Chinese vendors specialize in spine animation optimized for Unity, completing 50-character packs in under four weeks. This cost-performance blend drives steady contract renewals and positions gaming as the fastest-expanding end-use within the Animation Outsourcing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wage inflation in traditional hubs eroding cost advantage | -1.8% | India; Philippines | Medium term (2-4 years) |

| IP leakage concerns limiting high-budget feature film work to tier-1 vendors | -1.5% | Global | Long term (≥ 4 years) |

| Scarcity of senior technical directors creating capacity bottlenecks | -1.3% | Global | Medium term (2-4 years) |

| Currency volatility in emerging centers raising contracting risk | -1.1% | Latin America; Middle East & Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Wage Inflation in Traditional Hubs Eroding Cost Advantage

Salary growth in Bangalore and Manila rose by 8-12% each year during 2024, pushing average senior-animator pay to USD 38,000 The higher payroll narrows the historic cost gap with Eastern Europe, making price the sole selling point less persuasive. Vendors answer by adding automation plug-ins that remove routine scene-assembly steps and save up to 20% of staff hours. Some firms are also opening satellite studios in Vietnam and inland China where wage pressure is lower. Clients respond by splitting projects across multiple hubs to balance budgets and talent depth. These shifts keep the Animation Outsourcing market focused on productivity gains rather than simple labor arbitrage.

IP leakage concerns limiting high-budget feature film work

Large studios maintain strict security audits that only a small group of ISO-27001-certified vendors can pass. This policy places most tent-pole films with about 25 suppliers worldwide, reducing opportunities for new entrants even when they offer lower bids. Emerging vendors invest in encrypted file-transfer systems and closed network rooms to win trust. Studios still restrict premium assets such as final character models to on-site teams, moving only lower-risk shots offshore. As a result, high-budget projects circulate within a tight circle, while other vendors focus on games, ads, or episodic work to build credentials. This tiered access structure shapes long-term competition across the Animation Outsourcing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animation Type: 3D remains dominant while motion graphics accelerates

3D held 57.40% of Animation Outsourcing market share in 2025, because its assets travel easily across film, streaming, and high-end games. Producers favor 3D pipelines that now combine real-time renders and AI-assisted clean-ups to trim delivery days without lowering polish. These gains keep the segment firmly ahead even as smaller studios join the field. Motion graphics follows as the fastest riser, helped by the low cost of a 60-second corporate clip that averaged USD 3,130 in 2025. Marketing teams want punchy explainer videos for social feeds, and that demand funnels steady briefs to boutique vendors.

The Animation Outsourcing market responds by pairing senior 3D leads with junior motion-graphics teams so each project balances creativity and budget. Character creation services stay relevant because mobile games need fresh avatars every season, while stop-motion keeps a loyal niche of storytellers. Greater software interoperability means crews can pivot from motion graphics to 3D within the same toolset, raising utilization. Together these shifts diversify revenue sources and lock in a broad skills mix across the global vendor base.

By Production Stage: Post-production & VFX lead growth

Production services commanded 51.30% of the Animation Outsourcing market size in 2025, reflecting long-established workflows that external teams can scale quickly. Studios share clear model sheets and shot lists, letting overseas partners animate large volumes while home offices focus on art direction. Post-production and VFX, however, post the strongest 12.92% CAGR through 2031 as hybrid live-action shows call for heavier compositing. The increasing adoption of Animation and VFX services across OTT platforms, gaming studios, and virtual production projects is further supporting outsourcing demand globally.

Vendors chase this margin by investing in secure render farms that clear studio security audits, a must for tent-pole titles. Pre-production tasks also grow because generative AI can spit out three storyboard options overnight, cutting early-phase costs. Clients then lock animatics faster and slide savings downstream. These changes shift bargaining power toward suppliers that cover every stage inside one pipeline, strengthening project continuity within the Animation Outsourcing market.

By End-use Industry: Gaming challenges media & entertainment dominance

Media and entertainment owned 60.20% of Animation Outsourcing market share in 2025, buoyed by streaming giants that order multi-season animation slates. The steady rhythm of episodic work fills vendor calendars year-round. Yet gaming shows a 14.24% CAGR that threatens to close the gap by 2031 as publishers seek film-quality trailers and richer cutscenes.

Studios in India aim to capture USD 40 billion of global AVGC work by 2025, a figure that would tilt more contracts toward Asia. Educational animation climbs too, thanks to healthcare simulations that command premium fees and improve patient training outcomes. As a result, suppliers diversify portfolios so sudden slowdowns in one vertical do not idle rigs or staff. This hedge makes the overall Animation Outsourcing market more resilient.

By Platform: OTT/streaming originals disrupt traditional channels

Film and television still contribute 45.40% of 2025 revenue, but OTT originals sprint ahead with a 14.93% CAGR as platforms race to retain subscribers. Binge-worthy animated series provide global reach while staying family-friendly, an advertiser sweet spot. Meanwhile, social-media shorts rely on motion graphics for quick viewer engagement.

Game cinematics and metaverse assets add steady incremental demand because publishers refresh live-service worlds monthly. AR/VR projects remain small yet strategic, letting vendors test real-time pipelines that may soon dominate. Each platform shift nudges studios to blend multiple content types per deal, ensuring full-pipeline utilization across the Animation Outsourcing market.

Geography Analysis

North America retained a 33.60% revenue share worth USD 68.95 billion in 2025, anchored by the major studios that commission premium projects. California’s headcount dipped after productions chased richer rebates in British Columbia, where animation jobs rose 72% since 2019. Local guilds lobby for stronger state incentives to stem the work drain.

Asia-Pacific posts the fastest 11.82% CAGR as governments back the sector with grants and training. South Korea pledged USD 106 million for AI-enabled pipelines, while India’s AVGC roadmap targets 5% of worldwide demand. Chinese studios excel at high-volume rigging for mobile games, driving continual asset flow. The region now supplies a growing share of 3D series for global platforms, lifting the Animation Outsourcing market outlook.

Europe leverages attractive tax credits, such as the UK’s Audio-Visual Expenditure Credit and Spain’s 60% rebate, to win complex compositing gigs. Brexit-led paperwork adds delays but has not reversed inbound work. Latin America, led by Mexico, benefits from timezone alignment with U.S. showrunners, while South African shops in the Middle East and Africa carve niches in multilingual e-learning. These cross-regional dynamics reduce concentration risk and broaden client choice.

Competitive Landscape

Global supply remains fragmented; the ten largest vendors hold under 40% of revenue, proving no single player dominates. Technicolor Creative Studios closed its U.S. sites in early 2025, and alumni launched Arc Creative to pursue high-end advertising. TransPerfect bought Technicolor Games and rehired Bangalore staff, signaling continued consolidation.

Market leaders invest heavily in proprietary real-time tools that shave render hours and attract clients seeking faster delivery. Framestore’s facial-rig breakthroughs on ‘IF’ boosted character nuance and set a new bar for hybrid films. Boutique studios specialize in AR/VR, educational visuals, or regional folklore, letting them command higher margins than generalist shops.

Security compliance now acts as a hard gate: ISO-27001 certification often decides bid winners on feature films. Vendors also diversify footprints, opening hubs in lower-cost regions to buffer wage inflation. These strategies keep competition lively and ensure the Animation Outsourcing market evolves through technology rather than simple price wars.

Animation Outsourcing Industry Leaders

Cinesite

Pixune Studios

Next Animation Studio Ltd.

Digitoonz

N-iX LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The UK government raised VFX tax relief via its Audio-Visual Expenditure Credit, lifting the effective cash benefit for animation and post-production Screen Daily.

- February 2025: Technicolor Creative Studios closed its U.S. operations; former artists from The Mill launched Arc Creative to pursue high-end advertising and game cinematics AWN.

- January 2025: South Korea’s Ministry of Culture, Sports and Tourism unveiled a USD 106 million 2025–2030 plan to fund AI-enabled production tools and global partnerships Animemojo.

- January 2025: TransPerfect acquired Technicolor Games, retaining the entire Bangalore workforce and expanding end-to-end art-services capacity Animation World Network.

Global Animation Outsourcing Market Report Scope

Animation outsourcing refers to the practice by which firms outsource the creation, development, and production of animation content to other studios, agencies, or freelancers that might be resident in different countries with low production costs. This involves using competence and resources from specialized providers of animation services to produce quality 2D and 3D animations, visual effects, motion graphics, and other related services.

The animation outsourcing market is segmented by animation type (2D animation, 3D animation, character creation, stop motion animation, motion graphics, others), by industry (media & entertainment, education, healthcare, others), by geography (North America [United States, Canada, Mexico, and Rest of North America], Europe [Germany, United Kingdom, France, Spain, and Rest of Europe], Asia-Pacific [India, China, Japan, New Zealand, Australia and Rest of Asia-Pacific], Latin America [Brazil, Argentina, and Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, and Rest of Middle East and Africa]).

The report offers market forecasts and size in value (USD) for all the above segments.

| 2D Animation |

| 3D Animation |

| Character Creation |

| Stop-Motion Animation |

| Motion Graphics |

| Others |

| Pre-production Services |

| Production Services |

| Post-production and VFX |

| Media and Entertainment |

| Gaming |

| Education (e-Learning, EdTech) |

| Healthcare and Scientific Visualisation |

| Advertising and Marketing |

| Others |

| Film and Television |

| Video Games (Console, PC, Mobile) |

| OTT/Streaming Originals |

| AR/VR and Metaverse Experiences |

| Web and Social Media Content |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Animation Type | 2D Animation | |

| 3D Animation | ||

| Character Creation | ||

| Stop-Motion Animation | ||

| Motion Graphics | ||

| Others | ||

| By Production Stage | Pre-production Services | |

| Production Services | ||

| Post-production and VFX | ||

| By End-use Industry | Media and Entertainment | |

| Gaming | ||

| Education (e-Learning, EdTech) | ||

| Healthcare and Scientific Visualisation | ||

| Advertising and Marketing | ||

| Others | ||

| By Platform | Film and Television | |

| Video Games (Console, PC, Mobile) | ||

| OTT/Streaming Originals | ||

| AR/VR and Metaverse Experiences | ||

| Web and Social Media Content | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the Animation Outsourcing market?

The market stands at USD 226.71 billion in 2026 and is on track to reach USD 373.18 billion by 2031 at a 10.47% CAGR.

Which animation segment is growing fastest?

Motion graphics posts the highest growth, with a 12.58% CAGR forecast as demand for short-form digital content surges.

Why is Asia-Pacific attracting more outsourced work?

Competitive labor costs, government incentives, and large talent pools have combined with rising regional streaming investment to deliver a 11.82% CAGR, the fastest globally.

How do real-time engines affect outsourcing strategies?

Unreal and Unity pipelines shorten render schedules by up to 30%, letting advertisers and studios entrust more shots to specialized vendors that master virtual production.

What risks limit premium outsourcing contracts?

IP-security concerns mean only ISO-certified tier-1 vendors receive blockbuster features, constraining newer studios seeking high-budget work.

How concentrated is vendor power in the Animation Outsourcing market?

The top 10 vendors hold under 40% share, indicating a fragmented landscape with many specialized firms.

Page last updated on: