Zero Trust Network Access Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

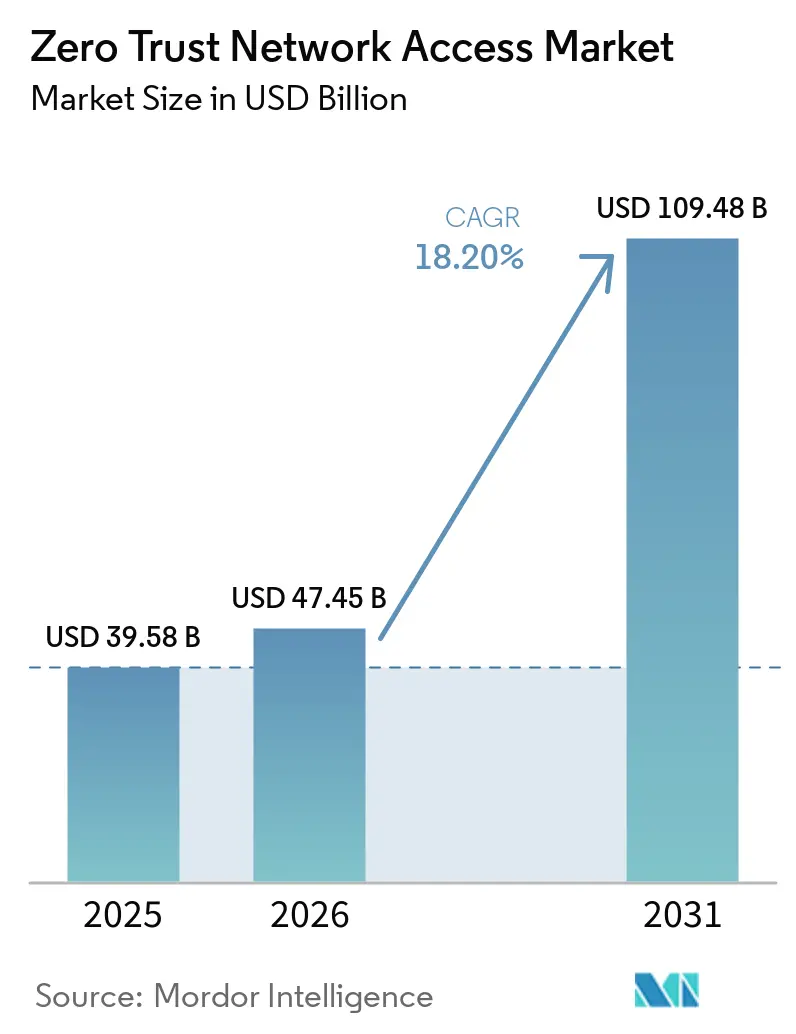

| Market Size (2026) | USD 47.45 Billion |

| Market Size (2031) | USD 109.48 Billion |

| Growth Rate (2026 - 2031) | 18.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zero Trust Network Access Market Analysis by Mordor Intelligence

The Zero Trust Network Access market size is projected to be USD 39.58 billion in 2025, USD 47.45 billion in 2026, and reach USD 109.48 billion by 2031, growing at an 18.20% CAGR from 2026 to 2031. The acceleration reflects a regulatory push that places cyber-risk squarely on executive balance sheets. Board-level accountability under United States and EU rules is turning zero-trust architecture into a fiduciary duty, while converged cloud-native security stacks shorten deployment cycles and lower total cost of ownership. Hyperscalers are bundling access control into wider cloud contracts, squeezing point-solution providers on price yet opening white-space opportunities in industrial networks that cannot host agents. A global shortage of skilled architects threatens rollout timelines, and proprietary policy engines raise migration costs, but open-standards efforts are gaining traction. Mergers and acquisitions centered on AI-enabled analytics underscore the shift from perimeter defense to identity-centric verification at every hop.

Key Report Takeaways

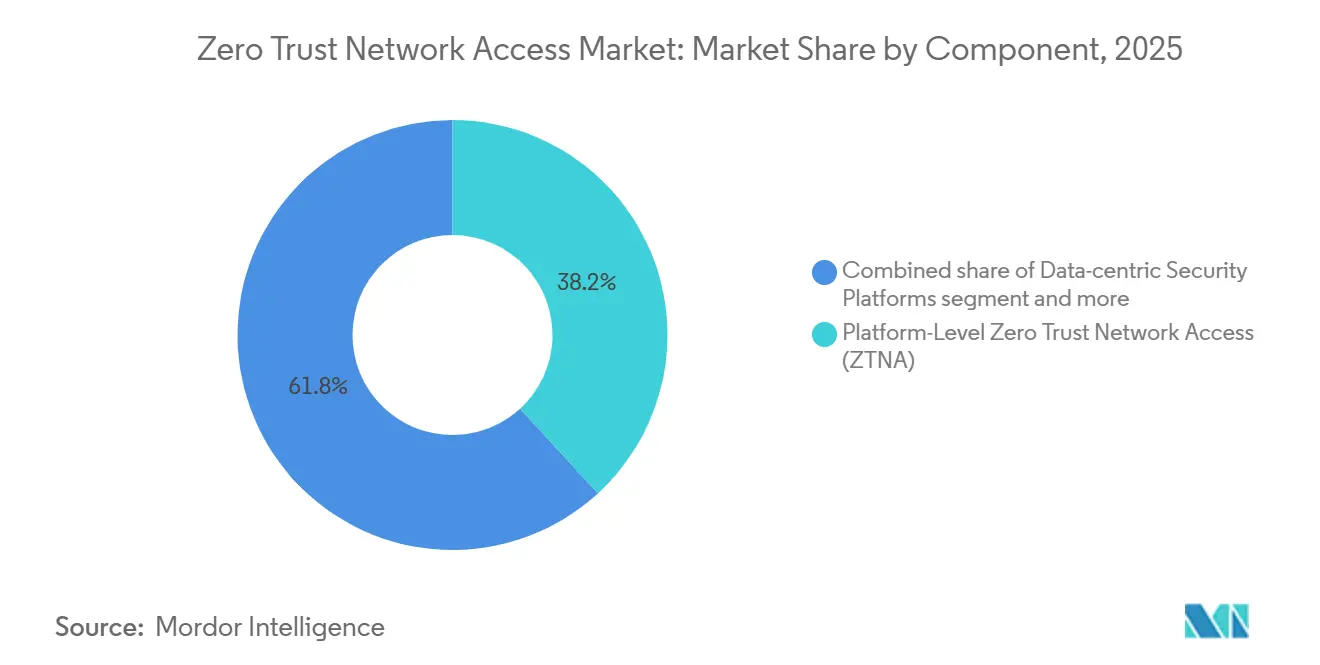

- By component, Platform-Level ZTNA led with 38.18% of the Zero Trust Network Access market share in 2025, while Security Service Edge is advancing at an 18.96% CAGR through 2031.

- By deployment mode, Cloud-Based delivery accounted for 63.71% of the Zero Trust Network Access market in 2025 and is expanding at a 18.57% CAGR through 2031.

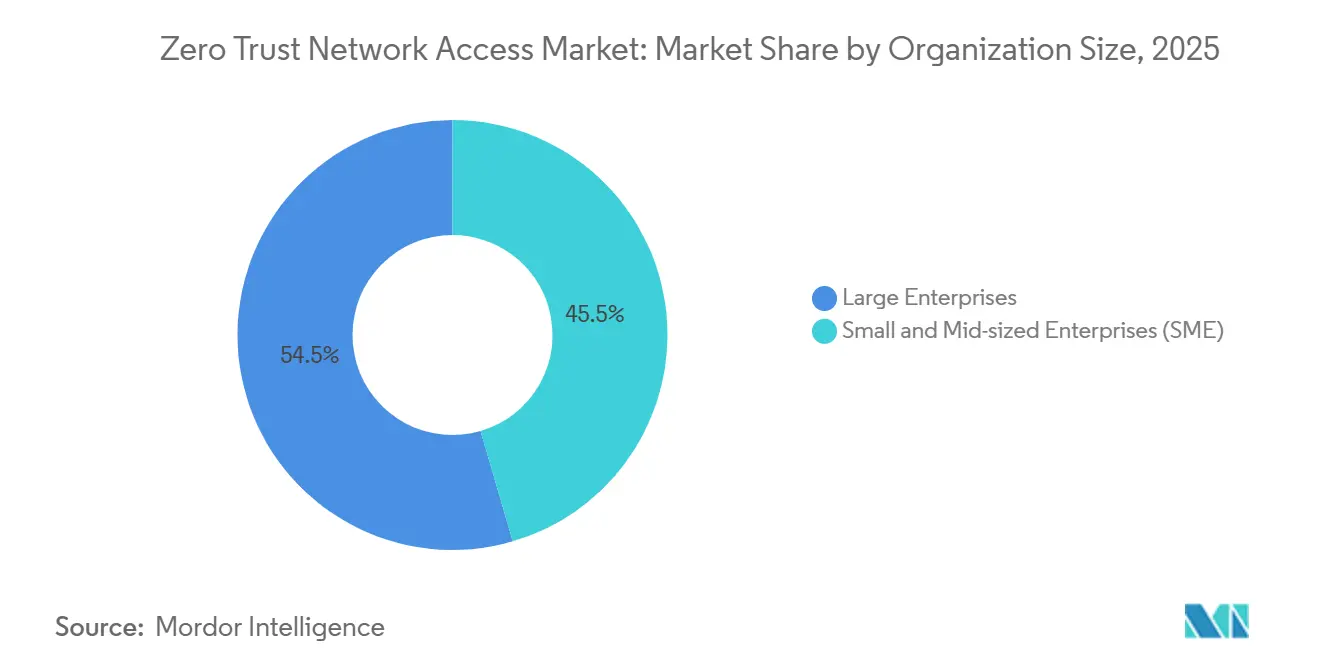

- By organization size, Large Enterprises captured 54.53% of the Zero Trust Network Access market share in 2025, whereas Small and Mid-Sized Enterprises are forecast to grow at an 18.71% CAGR between 2026 and 2031.

- By industry vertical, Banking, Financial Services, and Insurance held a 19.19% share of the Zero Trust Network Access market in 2025, while Healthcare and Life Sciences are poised to grow at an 18.78% CAGR through 2031.

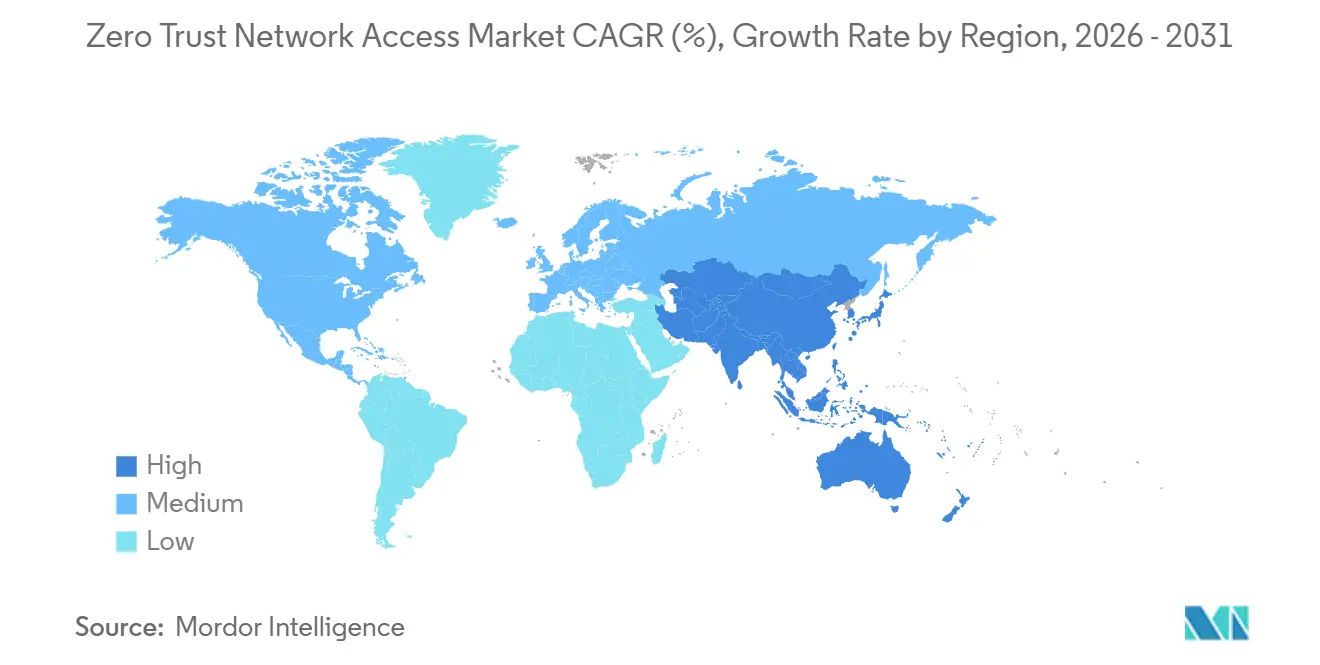

- By geography, North America dominated the Zero Trust Network Access market with 41.24% market share in 2025, yet Asia-Pacific is projected to record an 18.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Zero Trust Network Access Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Board-Level Cyber-Risk Accountability | +3.8% | North America and Europe, with spillover to Asia-Pacific hubs | Short term (≤ 2 years) |

| Mandates for Zero-Trust by Public Sectors | +3.5% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Cloud-Native Data Fabrics Requiring Micro-Segmentation | +3.2% | Global, with early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Generative-AI Threat Surface Expansion | +2.9% | Global | Short term (≤ 2 years) |

| Tokenization and Confidential-Computing Uptake | +2.1% | North America, Europe, and Asia-Pacific core markets | Long term (≥ 4 years) |

| Quantum-Resistant Encryption Pilots | +1.3% | North America and Europe, with pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Board-Level Cyber-Risk Accountability

The U.S. Securities and Exchange Commission rule that came into force in December 2023 forces listed companies to disclose material incidents within four business days, linking director liability to security controls. Boards now demand auditable zero-trust logs that prove least-privilege enforcement and shorten breach investigations.[1]U.S. Securities and Exchange Commission, “Cybersecurity Risk Management, Strategy, Governance, and Incident Disclosure,” sec.gov U.S. Department of Justice budget requests for fiscal 2027 earmark USD 110.3 million for zero-trust, signaling that public procurement will set the private-sector baseline.[2]U.S. Department of Justice, “FY 2027 Budget Summary,” justice.gov Legal counsel describes ZTNA as evidence of reasonable safeguards, a phrase that redefines cyber-risk as a governance metric. As a result, the Zero Trust Network Access market is moving from discretionary IT spending to compliance-driven obligations. Vendors able to map product features directly to disclosure requirements win faster board approval.

Mandates for Zero-Trust by U.S. and EU Public-Sector IT Spending

OMB memorandum M-22-09 sets a December 2026 deadline for U.S. civilian agencies to satisfy five zero-trust pillars, while CISA’s directive on phishing-resistant MFA disqualifies SMS tokens.[3]Cybersecurity and Infrastructure Security Agency, “Binding Operational Directive 23-01,” cisa.gov In parallel, the EU NIS2 Directive, transposed into national law by October 2024, expands obligations across 18 critical sectors and introduces personal liability for management.[4]European Union, “Directive (EU) 2022/2555 on Measures for a High Common Level of Cybersecurity,” eur-lex.europa.eu Vendors with FedRAMP High or EU certification gain preferred-bidder status, creating a procurement edge. These mandates establish a global compliance floor that private firms must match, driving sustained growth in the Zero Trust Network Access market. Spending accelerates first in North America and Europe, with Asia-Pacific governments quickly aligning to remain eligible for supply-chain contracts.

Cloud-Native Data Fabrics Needing Identity-Aware Micro-Segmentation

Enterprises federating workloads across AWS, Azure, and Google Cloud find that IP-based segmentation fails to control lateral movement at the container or serverless scope. Identity-aware micro-segmentation tags every API call with cryptographic identity, letting policies follow workloads rather than network locations. Kubernetes-centric platforms such as Calico Cloud enforce these rules inside service meshes, blocking east-west traffic even on the same subnet. Adoption rises further when confidential computing enclaves require attestation before keys are released, a flow that tokenization services embed. The driver lifts global demand because scalable data fabrics are a prerequisite for analytics, AI, and multicloud resilience.

Generative-AI Threat Surface Expansion

Prompt injection and autonomous AI agents introduce exfiltration paths that legacy VPNs cannot inspect. NIST has documented dozens of prompt-injection techniques bypassing model filters.[5]National Institute of Standards and Technology, “Adversarial Machine Learning: Taxonomy and Terminology,” nist.gov ZTNA mitigates the risk by verifying the user, device, and model deployment context before allowing an AI API call. Platforms inspect prompts for regulated identifiers, blocking them in real time. Shadow AI usage through browser extensions escapes perimeter defenses but is visible to device-posture checks inherent in zero-trust policies. As companies integrate large language models into processes, demand for ZTNA rises in lockstep.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy IAM Stacks | -2.4% | Global, acute in mature North American and European estates | Medium term (2-4 years) |

| High Transition CAPEX for Brown-Field OT | -1.9% | Global, centered on manufacturing hubs in Germany, Japan, and the U.S. Midwest | Long term (≥ 4 years) |

| Shortage of Zero-Trust Architects | -1.6% | Global | Medium term (2-4 years) |

| Vendor Lock-In Around Proprietary Engines | -1.2% | Global, pronounced in multicloud enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy IAM Stacks Slowing Policy Unification

Enterprises often juggle Active Directory, Okta, Ping Identity, and bespoke LDAP systems, each with different schemas and session lifetimes. CISA’s Known Exploited Vulnerabilities list registered 1,143 identity-related flaws by March 2025, illustrating how attackers chain gaps across these silos. Running parallel authentication during consolidation dilutes zero-trust coverage. The October 2023 Okta breach, where support-portal tokens were stolen, showed that a single weak link undermines federated trust. Until identity harmonization accelerates, ZTNA projects face longer timelines and higher costs.

High Transition CAPEX for Brown-Field OT Networks

Industrial control systems use protocols such as Modbus RTU and DNP3 that lack fields for user attributes. Retrofitting gateways that translate legacy traffic into identity-enriched sessions incurs capital outlays that few operators budget for. Dragos reported that 78% of the average OT security budget of USD 3.2 million in 2024 went to compliance rather than modernization. Latency-sensitive loops cannot tolerate the delays introduced by inline gateways, posing safety risks. As a result, adoption stalls in manufacturing and utilities despite regulatory pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Converged Security Service Edge Gains Momentum

Security Service Edge solutions are forecast to expand at an 18.96% CAGR, eclipsing traditional platform offerings that held a 38.18% share in 2025. The shift arises because converged stacks bundle secure web gateway, CASB, and ZTNA into a single cloud policy, cutting integration overhead. Dell’Oro projects combined SASE and SSE spending to approach USD 97 billion by 2030, reinforcing that convergence is now the mainstream buying pattern. Standalone platforms remain relevant for hybrid estates, but face price pressure as hyperscalers embed access control into larger deals. Data-centric security platforms address regulated data flows by wrapping tokenization around workloads in confidential-computing enclaves. IAM suites continue as the identity backbone, yet must synchronize attributes across multicloud deployments, a task that slows projects.

Platform-level ZTNA keeps strategic value where on-premises data centers persist. Cisco’s Armorblox buy added natural-language analytics to detect phishing in collaboration tools. Niche providers target OT segmentation, offering protocol-aware controls that SSE vendors do not. Over the forecast horizon, the Zero Trust Network Access market size for component categories will hinge on how quickly buyers collapse point tools into unified clouds.

By Deployment Mode: Cloud Delivery Dominates New Projects

Cloud-based deployments accounted for 63.71% of spending in 2025 and are projected to grow at a 18.57% CAGR. SaaS consumption models priced per user remove the capital hurdle of appliance refresh cycles. Zscaler’s cloud processes more than 500 billion daily transactions across 150 nodes, illustrating the scale advantage. Hybrid models appeal to sectors bound by data-residency laws because vendors can place policy nodes within national borders. On-premises deployments persist in air-gapped or classified networks but face staffing shortages; CISA counts a 500,000-person gap in zero-trust talent for secure enclaves.

Operational economics favor cloud because monthly fees of USD 5-15 per user are easier to approve than six-figure hardware buys. Hybrid solutions must constantly sync policies between cloud engines and local gateways, a complexity that vendors like Palo Alto Networks attempt to mask through automated replication. On industrial sites that require protocol translation, on-premises gateways remain relevant, though uptake is slower due to CAPEX constraints.

By Organization Size: SaaS Lowers Barriers for Smaller Firms

Large Enterprises controlled 54.53% of the Zero Trust Network Access market in 2025, but Small and Mid-Sized Enterprises will narrow the gap with an 18.71% CAGR. Cloudflare’s free tier for up to 50 users exemplifies democratization. SMEs struggle to hire security staff; the ISC² study shows many have no dedicated professional. Managed ZTNA services; therefore, gained currency by bundling policy templates and 24-hour monitoring. Large Enterprises focus on custom integrations for IoT and partner ecosystems and often spend USD 0.5-2 million on professional services engagements.

Vendor roadmaps prioritize ease of onboarding to accelerate SME adoption. Bookings data from Zscaler showed 40% growth among customers with fewer than 1,000 employees, highlighting a shift toward service consumption. Regulatory carve-outs occasionally reduce SME urgency, but supply-chain requirements from larger partners still pull them into compliance.

By Industry Vertical: Healthcare Becomes Fastest-Growing Adopter

Banking, Financial Services, and Insurance retained a 19.19% share in 2025, thanks to stringent regulations such as SWIFT CSP and DORA. Healthcare and Life Sciences will, however, post the highest CAGR at 18.78%. The 2024 Change Healthcare breach, which cost USD 872 million, pushed hospitals to replace legacy VPNs. The U.S. HHS penalty of USD 4.75 million for inadequate controls clarifies financial exposure. Government agencies adopt ZTNA under OMB mandates, while telecom operators embed identity controls into 5G core networks to protect slicing. Manufacturing firms face OT challenges, driving demand for protocol-aware gateways certified to IEC 62443.

Retailers comply with PCI DSS v4.0 segmentation rules, and critical infrastructure providers integrate ZTNA into their remote monitoring systems. Over the forecast, the Zero Trust Network Access market size allocation by vertical will reflect both regulatory intensity and infrastructure complexity.

Geography Analysis

North America continues to lead with 41.24% share, supported by U.S. federal mandates, SEC disclosure rules, and a mature ecosystem of integrators. The U.S. justice budget seeks USD 110.3 million for zero-trust in fiscal 2027, signaling sustained demand. Canada’s proposed Critical Cyber Systems Protection Act extends requirements to telecom and energy, boosting homegrown suppliers. Mexico lags on budgets, yet near-shoring of U.S. manufacturing drives cross-border ZTNA to secure data flows.

Asia-Pacific is forecast to have the fastest 18.91% CAGR as governments align cyber rules with digital-economy goals. Japan earmarked JPY 300 billion (USD 2 billion) of its USD 11.2 billion digital budget to cybersecurity in 2024. India’s CERT-In directive mandates breach reporting within 6 hours and 180-day log retention. Singapore’s Smart Nation program requires identity-aware access for citizen services, and South Korea mandates zero-trust for biometric data processors. China’s security reviews favor domestic vendors, fragmenting the global market into separate policy domains.

Europe grows despite uneven NIS2 adoption, with Germany passing its law in 2024, while Italy and Spain delayed into 2025. The UK’s NCSC principles recommend phased zero-trust rollouts starting with high-value assets. The Middle East invests in sovereign clouds: Saudi Arabia mandates in-country data storage, and the UAE published national standards aligned to UN e-government rankings. South America and Africa remain early-stage; compliance drivers exist under Brazil’s LGPD and South Africa’s POPIA, but budgets and skill shortages slow uptake.

Competitive Landscape

Competition in the market is moderate. The leading vendors, including Microsoft, Cisco, Palo Alto Networks, Zscaler, and Broadcom, hold a significant share, while numerous other players also compete actively. Hyperscalers utilize their established cloud infrastructure to integrate ZTNA into broader service offerings, often positioning them competitively against standalone solutions. Cisco’s Armorblox purchase added natural-language threat detection to its Duo platform, while Microsoft folded Entra Private Access into Microsoft 365 subscriptions to deepen lock-in. Point providers like Illumio focus on workload segmentation, and emerging players such as Tailscale court developers with open-source clients.

Technology roadmaps center on AI-powered analytics that reduce manual policy tuning. Zscaler’s AI-aware SASE scans prompts to block data-exfiltration attempts in large language models. Patent filings climbed 34% in 2024, with a focus on cryptographic attestation and policy-as-code. Compliance certifications from ISO 27001 to FedRAMP High are now table stakes, diverting up to 20% of revenue for smaller firms. Open-standards bodies work on policy portability to lower switching costs, but proprietary languages remain a lock-in barrier.

The Zero Trust Network Access market concentration score is 6 because the top five vendors control near 50% of spending, yet many specialized and regional players fragment the remainder.

Zero Trust Network Access Industry Leaders

Zscaler, Inc.

Cisco Systems, Inc.

Palo Alto Networks, Inc.

Cloudflare, Inc.

Okta, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Microsoft released Entra Private Access for Government Cloud with FedRAMP High authorization, meeting OMB deadlines.

- January 2026: Zscaler bought Airgap Networks for USD 120 million to extend agentless micro-segmentation to IoT and OT devices.

- December 2025: Cisco closed its USD 28 billion Splunk acquisition, merging SIEM telemetry with zero-trust enforcement.

- November 2025: Cloudflare partnered with NVIDIA to embed GPU-accelerated threat inspection into its Zero Trust platform.

Global Zero Trust Network Access Market Report Scope

The Zero Trust Network Access (ZTNA) Market refers to the ecosystem of solutions and services that provide secure, identity-based access to applications and resources without relying on a traditional network perimeter. The market includes technologies that hide internal applications from discovery, reduce lateral movement, and replace or reduce dependence on legacy VPN-based access. Demand is being driven by remote work, cloud adoption, regulatory pressure, and the need for stronger protection across distributed enterprise environments.

The Zero Trust Network Access Market Report is Segmented by Component (Platform-Level ZTNA, Data-Centric Security Platforms, IAM Suites, SSE Solutions), Deployment Mode (Cloud-Based, Hybrid, On-Premises), Organization Size (Large Enterprises, SME), Industry Vertical (BFSI, Healthcare, Government, IT and Telecom, Manufacturing, Retail), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Platform-Level Zero Trust Network Access (ZTNA) |

| Data-Centric Security Platforms |

| Identity And Access Management (IAM) Suites |

| Security Service Edge (SSE) Solutions |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small And Mid-Sized Enterprises (SME) |

| Banking, Financial Services And Insurance (BFSI) |

| Healthcare And Life Sciences |

| Government And Public Sector |

| IT And Telecom |

| Manufacturing And Critical Infrastructure |

| Retail And E-Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | Platform-Level Zero Trust Network Access (ZTNA) | |

| Data-Centric Security Platforms | ||

| Identity And Access Management (IAM) Suites | ||

| Security Service Edge (SSE) Solutions | ||

| By Deployment Mode | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small And Mid-Sized Enterprises (SME) | ||

| By Industry Vertical | Banking, Financial Services And Insurance (BFSI) | |

| Healthcare And Life Sciences | ||

| Government And Public Sector | ||

| IT And Telecom | ||

| Manufacturing And Critical Infrastructure | ||

| Retail And E-Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and outlook for the Zero Trust Network Access market?

The Zero Trust Network Access market was valued at USD 29.58 billion in 2025, reached USD 47.45 billion in 2026, and is projected to reach USD 109.48 billion by 2031 at a CAGR of 18.20%.

How fast is Asia-Pacific spending on zero-trust expected to grow?

Asia-Pacific spending on zero-trust is projected to expand at an 18.91% CAGR between 2026-2031, outpacing all other regions.

Why are Small and Mid-Sized Enterprises now viable customers for zero-trust solutions?

SaaS delivery priced per user removes the need for six-figure hardware purchases and offsets the shortage of in-house security talent, making adoption practical for smaller firms.

Which deployment mode holds the largest share today?

Cloud-based deployment leads with 63.71% of current spending because it offers rapid onboarding and eliminates appliance maintenance.

What challenges slow down zero-trust rollouts in industrial plants?

Legacy control systems use protocols that cannot carry identity attributes, and adding gateways introduces latency, raising both cost and safety concerns.

How concentrated is the vendor landscape?

The five largest providers account for roughly half of global revenue, indicating moderate concentration with room for specialized competitors.

Page last updated on: