Virtual Private Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

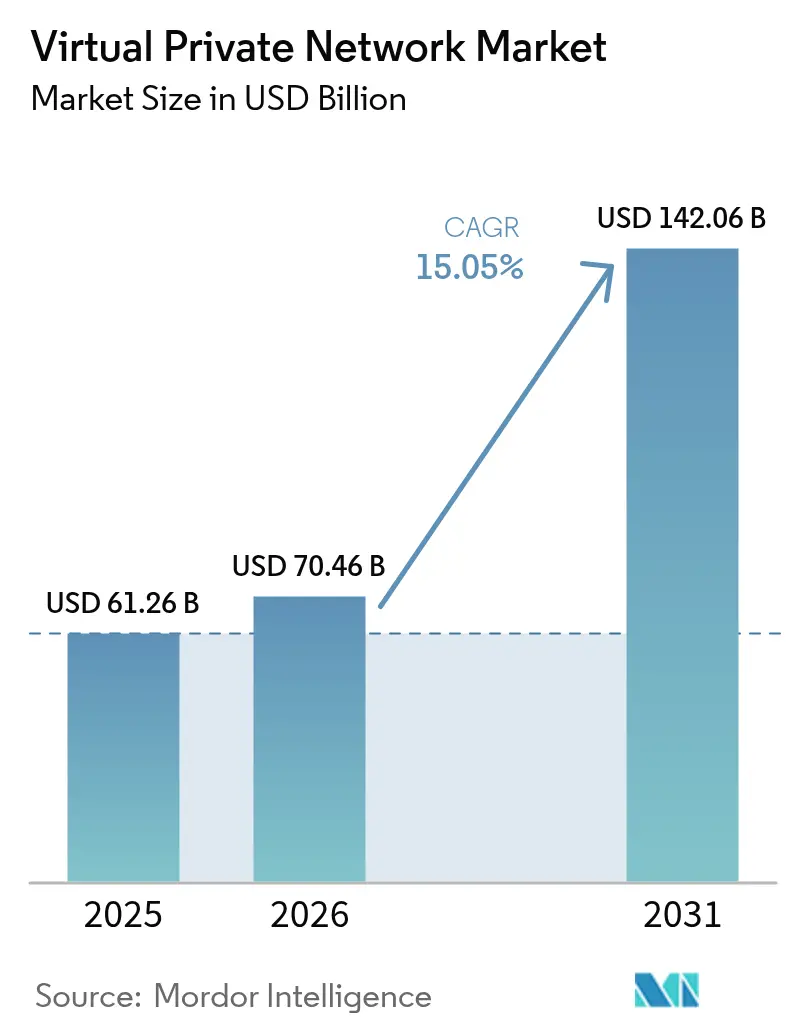

| Market Size (2026) | USD 70.46 Billion |

| Market Size (2031) | USD 142.06 Billion |

| Growth Rate (2026 - 2031) | 15.05% CAGR |

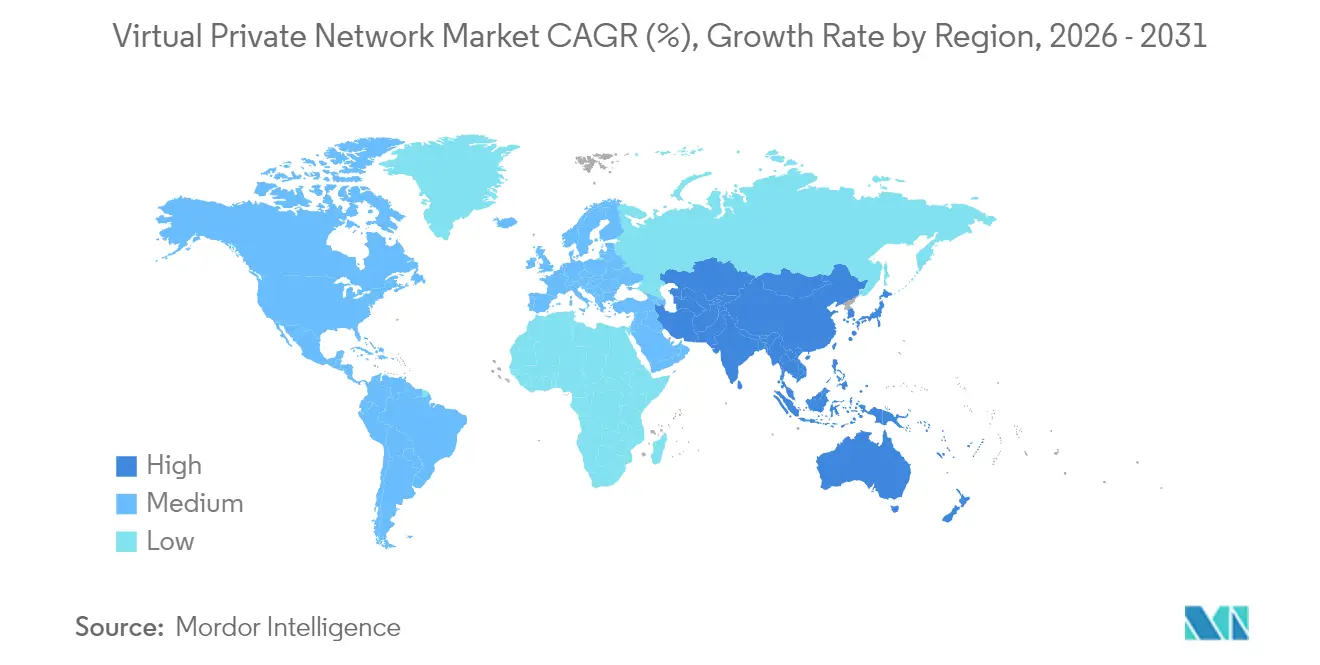

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Virtual Private Network Market Analysis by Mordor Intelligence

The virtual private network market size is expected to grow from USD 61.26 billion in 2025 to USD 70.46 billion in 2026 and is forecast to reach USD 142.06 billion by 2031 at 15.05% CAGR over 2026-2031. Expansion stems from hybrid-workforce security requirements, persistent ransomware pressure, and firm migration toward Secure Access Service Edge (SASE) platforms that merge networking and security functions. Hardware appliances still anchor many deployments, yet cloud-delivered services accelerate because they remove on-premises bottlenecks and simplify administration. Zero-trust network access (ZTNA) models are replacing legacy concentrators, trimming attack surfaces and enhancing user experience. Growing device footprints in Internet of Things (IoT) factories, 5G deployments, and satellite broadband roll-outs extend encrypted connectivity requirements into new sites and geographies. Competitive advantage is shifting to vendors that integrate AI-driven threat detection, post-quantum encryption, and unified policy management.

Key Report Takeaways

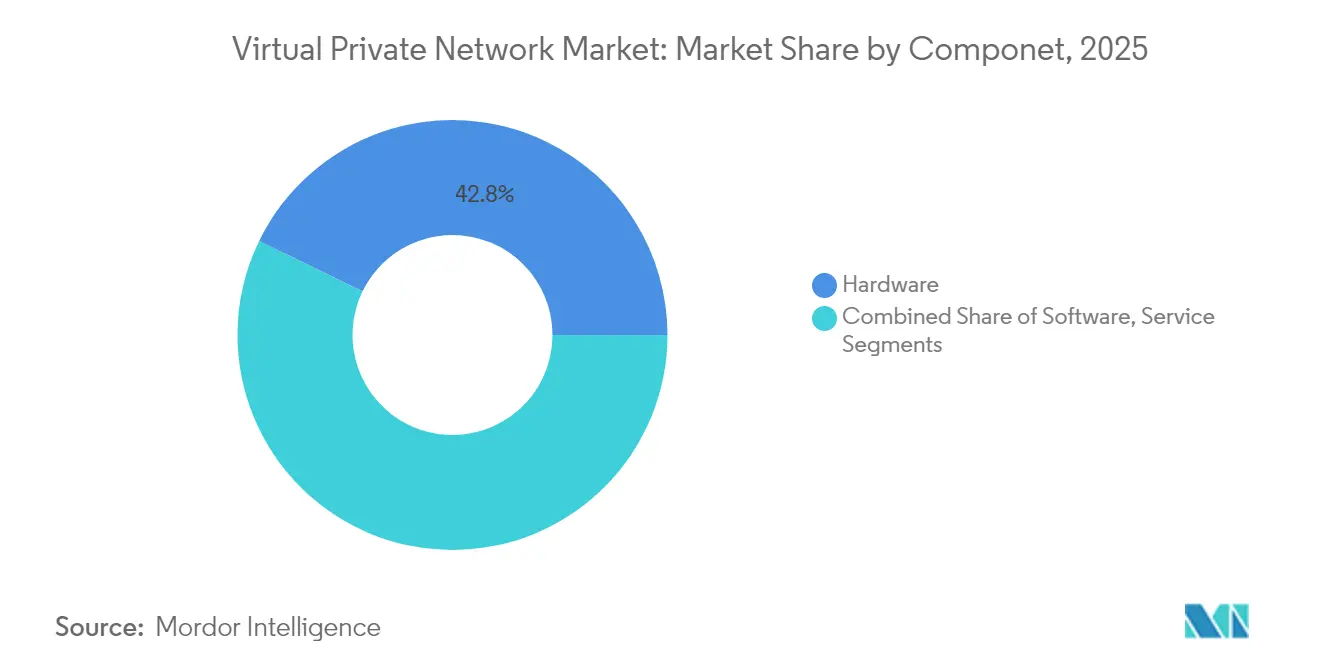

- By component, hardware captured 42.80% of virtual private network market share in 2025; software is projected to grow at a 15.72% CAGR through 2031.

- By type, the hosted and managed segment held 24.45% revenue share in 2025, while MPLS VPN is forecast to expand at a 16.52% CAGR to 2031.

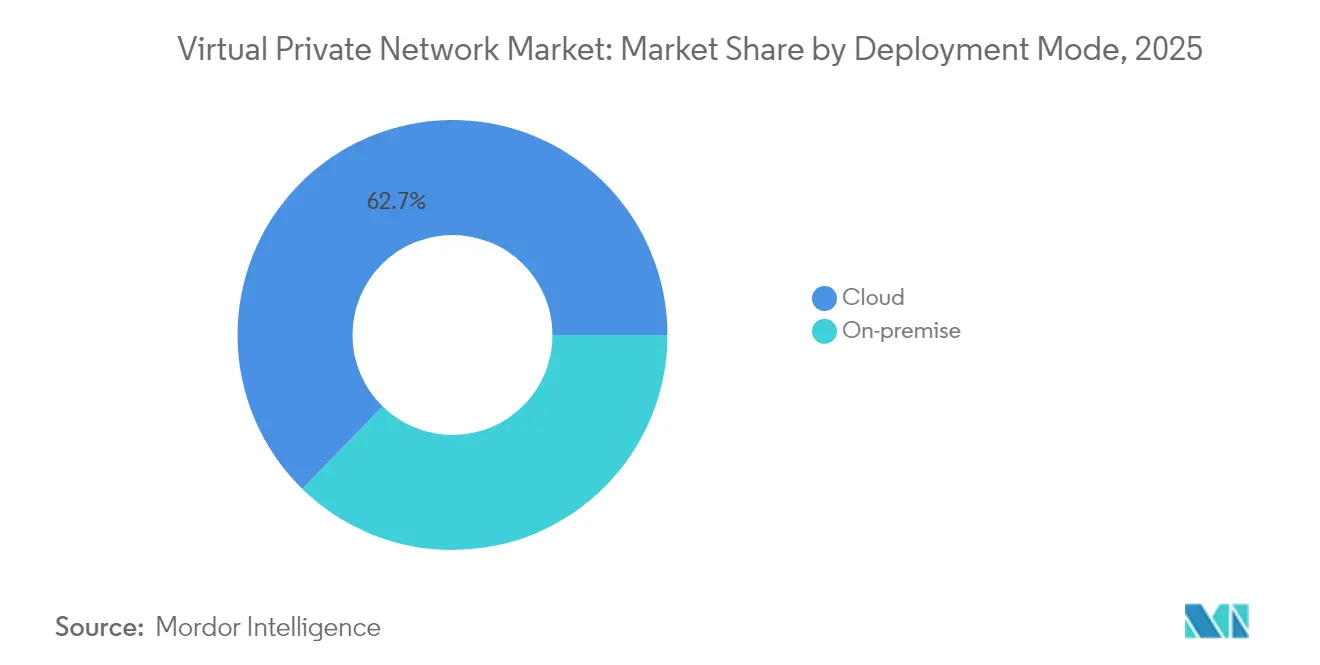

- By deployment mode, cloud solutions dominated with 62.70% of the virtual private network market size in 2025 and are advancing at a 16.83% CAGR through 2031.

- By end-user industry, BFSI led with 29.40% revenue share in 2025; healthcare and life sciences is expanding at a 15.41% CAGR to 2031.

- By region, North America accounted for 26.85% of the virtual private network market in 2025, whereas Asia-Pacific is growing fastest at 15.96% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Virtual Private Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hybrid-workforce dependence on secure remote access | +3.2% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Proliferation of IoT devices requiring encrypted connectivity | +2.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Escalating ransomware losses driving zero-trust network spending | +2.5% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Cloud-native application adoption boosting demand for Cloud VPN and SASE | +3.1% | Global | Medium term (2-4 years) |

| Emergence of privacy regulations spurring corporate VPN roll-outs | +1.9% | Europe, expanding to Asia-Pacific and Americas | Long term (≥ 4 years) |

| Satellite broadband expansion unlocking new VPN user bases | +1.8% | MEA, Latin America, Rural Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hybrid-Workforce Dependence on Secure Remote Access

Shifts in work patterns have elevated VPN connectivity to business-critical status. The New York City Department of Education migrated more than 1 million users and 2 million devices to a zero-trust framework and reported a 15% reduction in attacks alongside a 40% increase in blocked threats.[1]Zscaler, “State Government Saves USD 875 Million by Moving from VPN to Zero Trust,” zscaler.com Enterprises increasingly adopt cloud-native SASE platforms that route traffic directly to applications, eliminating the latency and patching burdens found in traditional concentrators.

Proliferation of IoT Devices Requiring Encrypted Connectivity

Industrial networks now demand granular, identity-based access. Cisco’s Secure Equipment Access replaces broad VPN tunnels with fine-grained, zero-trust controls for operational technology resources.[2]Cisco, “Cisco Secure Equipment Access Wins IoT Security Innovation of the Year,” blogs.cisco.com At Guangdong University, China Mobile’s 5G VPN delivered ten-fold downlink speed versus legacy solutions while supporting 20,000 concurrent users.

Escalating Ransomware Losses Driving Zero-Trust Network Spending

ThreatLabz observed an 82.5% rise in VPN Common Vulnerabilities and Exposures between 2020 and 2025; 60% carried high or critical scores. After a ransomware intrusion via legacy VPN, a government agency rebuilt remote access on Prisma Access ZTNA to close credential abuse pathways.[3]Palo Alto Networks, “Prisma Access Enables Zero Trust for Federal Agency,” paloaltonetworks.com

Cloud-Native Application Adoption Boosting Demand for Cloud VPN and SASE

Fortinet’s Unified SASE recurring revenue climbed 26% in Q1 2025 to USD 1.54 billion, underscoring enterprise appetite for single-vendor networking and security platforms. Integration of Software-Defined WAN with Security Service Edge is streamlining policy enforcement across dispersed sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage in VPN/SASE administration inflating total cost of ownership | -1.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Performance/latency penalties versus SDP and ZTNA alternatives | -2.1% | Global | Short term (≤ 2 years) |

| Heightened regulatory scrutiny on consumer VPN logging practices | -1.2% | Europe, expanding globally | Long term (≥ 4 years) |

| Commodity pricing wars among retail VPN brands squeezing margins | -1.5% | Global consumer market | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent Shortage in VPN/SASE Administration Inflating Total Cost of Ownership

Demand for skilled engineers exceeds supply, pushing organizations toward managed services. Providers report staffing outlays approaching 30% of total operating expense, steering customers to integrated SASE offerings that reduce manual upkeep.

Performance and Latency Penalties Versus SDP and ZTNA Alternatives

Research presented to the Brazilian Computer Society confirmed distance-related latency spikes in VPN tunnels to industrial sites. VersaBank’s deployment of a WireGuard-based mesh network erased these delays and improved remote employee productivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Foundation Supports Software Expansion

Hardware appliances accounted for 42.80% of the virtual private network market in 2025, underpinning many large-scale remote access roll-outs. Segment resilience is tied to long refresh cycles in sectors with on-premises compliance mandates. Yet software is growing at a 15.72% CAGR, fueled by containerized gateways and virtual firewalls that deploy in minutes on hyperscale clouds. Supply-chain tightness around semiconductors catalyzed adoption of cloud-hosted images such as pfSense Plus on AWS and Azure, accelerating proofs of concept. Services revenue, spanning managed operations and implementation projects, scales in tandem with SASE transitions and currently forms the third pillar of component spend. Organizations continue to blend hardware for on-site performance with software gateways to extend reach, signalling coexistence rather than replacement.

By Type: Hosted Services Lead, MPLS Rebounds

Hosted and managed offerings secured 24.45% of virtual private network market share in 2025 as enterprises shifted maintenance burdens to specialists. These services integrate continuous updates, threat intelligence feeds, and 24×7 monitoring within predictable subscription models. Meanwhile, MPLS VPN shows a renaissance, pacing at 16.52% CAGR as firms require deterministic latency for hybrid cloud and mission-critical collaboration. Cloud VPN and broader SASE suites converge IPsec, SD-WAN, and firewall-as-a-service under unified orchestration, trimming policy sprawl. IPsec VPN remains essential for defense and government entities adhering to established protocol accreditation, while emerging WireGuard solutions emphasize streamlined code bases and near-line-rate throughput.

By Deployment Mode: Cloud Dominance Accelerates

Cloud delivery owned 62.70% of the virtual private network market in 2025 and is growing at 16.83% CAGR as organizations prioritize agility over capital expenditure. Cloud gateways auto-scale to match bursts in remote connections and ship with global PoPs to reduce round-trip times. A case from The Guidance Center showed total cost halved by adopting FortiSASE, illustrating operating-expense efficiencies. On-premises deployments persist where data residency dictates local control, though many agencies now implement hybrid designs that route sensitive workloads internally and non-sensitive traffic through cloud nodes.

By End-User Industry: BFSI Holds Lead, Healthcare Surges

BFSI organizations commanded 29.40% of 2025 revenue, leveraging robust VPN fabrics to secure trading floors and branch connectivity. Capitec Bank blocked 745,000 threats annually after adopting zero-trust access, demonstrating compliance and risk reduction The segment’s defensive spending is expected to preserve absolute dollar leadership through 2030.

Healthcare and life sciences, however, is the fastest-growing vertical at 15.41% CAGR. Telehealth usage and strict patient-data rules drive hospital groups to encrypt traffic from remote clinicians and medical IoT devices. RWJBarnabas Health integrated Fortinet’s platform to connect satellite clinics securely, exemplifying the sector’s modernization push. Manufacturing, government, and education also register material growth as Industry 4.0, smart-city, and distance-learning initiatives extend attack surfaces.

Geography Analysis

North America remained the largest regional contributor with 26.85% of virtual private network market revenue in 2025. Spending momentum is sustained by early zero-trust pilots and stringent breach disclosure regulations. Federal and state programs accelerate upgrades from IPsec concentrators to identity-centric SASE nodes, while hyperscalers’ dense PoP distribution keeps latency low for dispersed users.

Asia-Pacific delivers the fastest expansion at 15.96% CAGR. Massive digitization programs, combined with rising cyber insurance uptake, push enterprises to secure cloud workloads and mobile workforces. Trials in Chinese universities demonstrate ten-fold performance gains for mobile VPN on 5G stand-alone networks. India’s financial regulators now require encrypted connectivity for outsourced processing centers, further catalyzing adoption.

Europe maintains steady progress under General Data Protection Regulation enforcement. Enterprises prefer providers with in-region data centers to ensure sovereignty, and many layer VPN with data-loss prevention for compliance. Government projects in Germany and France specify post-quantum readiness in new remote access procurement.

Meanwhile, Middle East and Africa benefit from Starlink roll-outs that extend broadband to rural districts; VPN services ride on top to protect emerging e-commerce and e-government traffic. Latin America gains traction as Brazilian banks and Mexican retailers embrace managed VPN to bypass local talent shortages.

Regulatory Landscape

Regulation shaping VPN deployments is shifting from privacy-focused compliance toward operational cybersecurity controls and provider accountability. In the European Union, implementation activity around NIS2 is pulling commercial VPN operators into stricter incident reporting and governance practices via national CSIRTs, while GDPR enforcement continues to influence provider choices on in-region processing and data handling.

In April 2026, ETSI advanced VPN-specific standardization with EN 304 620 (Virtual Private Networks) aligned to the EU Cyber Resilience Act, which signals more prescriptive security baselines for VPN software and services entering EU supply chains. Elsewhere, governments are reinforcing technical and assurance requirements through standards and security baselines, including China's GB/T 44887.10-2024 (VPN+ for network slicing) implemented from March 2025, and updates to GB/T 32922-2023 which replaced the 2016 version. In the United States, the Department of Defense continues to mandate VPN gateway hardening through STIG controls, while policy debate on VPN provider oversight continues in markets such as India, where July 2026 reporting highlighted work on a new framework after earlier 2022 rules failed to achieve intended outcomes.

Competitive Landscape

Competition sits at the intersection of networking and security. Large incumbents such as Cisco, Palo Alto Networks, Check Point, and Fortinet deepen portfolios through M&A and in-house development. Check Point’s 2025 purchase of Perimeter 81 expanded its secure access service into mid-market channels. Fortinet’s acquisition of Lacework reinforced cloud-workload protection, creating a unified SASE plus CNAPP proposition.

Pure-play SASE entrants leverage cloud-native roots to simplify roll-out and pricing. Zscaler’s multitenant architecture scales from tens to hundreds of thousands of users without customer-managed hardware, landing state-wide transformations such as Oklahoma’s 100-agency consolidation. WireGuard-focused innovators, including Tailscale and Mullvad, emphasize lightweight code and post-quantum upgrades; Mullvad enabled ML-KEM key exchanges across desktop apps in 2025.

Strategic differentiation centers on AI-driven anomaly detection, unified telemetry dashboards, and cryptographic agility. Vendors are racing to integrate NIST-selected algorithms before quantum threats materialize. Price pressure is muted in the enterprise tier, where buyers prioritize reliability and compliance support over lowest list price.

Virtual Private Network Industry Leaders

Cisco Systems Inc.

Microsoft Corp. (Azure)

Palo Alto Networks Inc.

Check Point Software Technologies Ltd.

IBM Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise modernization work is creating room for VPN capabilities that integrate with SASE and zero-trust controls, rather than operating as standalone remote-access gateways. Security-driven replacement cycles are also visible in vendor end-of-life milestones and vulnerability pressure around SSL VPN and remote-access gateways, which is pushing buyers toward hosted and managed delivery models that reduce patching and operational load.

Cloud delivery is continuing to expand, with cloud-delivery holding 62.70% share in 2025, and vendors have opportunities to package VPN functions inside unified policy stacks that route traffic into SSE and secure access services. Standards and compliance-by-design efforts are further opening differentiation lanes around cryptographic agility and audit-ready controls, with ETSI work on EN 304 620 (mature draft published April 2026) and China's GB/T standards for VPN+ and IPsec secure access supporting procurement processes that require conformance evidence. On the protocol side, MASQUE over QUIC and post-quantum cryptography for VPN and IPsec implementations create room for vendors to offer quantum-safe and next-generation tunneling options that fit modern application traffic patterns, particularly as organizations seek tighter visibility and control over encrypted flows moving between cloud workloads, mobile users, and IoT-connected sites.

Recent Industry Developments

- June 2026: Palo Alto Networks Unit 42 disclosed active exploitation of PAN-OS CVE-2026-0257 affecting GlobalProtect portal and gateway components. The advisory prompted organizations to accelerate patching and hardening of remote access VPN estates, and reinforced the value of architectures that reduce exposure of internet-facing VPN services.

- May 2026: Cisco announced general availability of Cisco SASE with Meraki, enabling Meraki Auto VPN traffic steering into Cisco Secure Access. The integration tightens alignment between SD-WAN and secure access services, supporting enterprises consolidating point VPN and perimeter tools into SASE managed policy and enforcement.

- May 2025: T-Mobile and Palo Alto Networks launched T-Mobile SASE with Palo Alto Networks, combining 5G Advanced connectivity with Prisma SASE 5G for cloud-delivered security without on-premises hardware. The offer strengthened carrier-led go-to-market routes for secure remote access and accelerated adoption of hosted and managed VPN and SASE bundles for distributed enterprises.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the virtual private network (VPN) market is defined as paid hardware, software, and services that create encrypted tunnels to enable secure remote access and private connectivity over public or shared networks, sold to consumers and organizations.

Scope exclusions: Excludes general-purpose networking gear and broader security platforms unless VPN functionality is directly priced and delivered as part of the VPN offering.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Type

- Hosted / Managed

- IPsec VPN

- MPLS VPN

- Cloud VPN / SASE

- Others

- By Deployment Mode

- Cloud

- On-premise

- By End-User Industry

- BFSI

- Healthcare and Life Sciences

- IT and Telecom

- Government and Public Sector

- Manufacturing and Industrial

- Retail and E-Commerce

- Education

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping demand signals and supply capacity, then cleaning overlaps between enterprise and consumer use. We use public sources like the International Telecommunication Union (internet usage and broadband indicators), NIST cybersecurity guidance, FCC broadband data (for the US), OECD digital economy statistics, and World Bank development indicators to anchor connectivity and adoption context.

We also review company filings and investor presentations for product mix cues, alongside association websites and reputable press for changes tied to remote work policies and major cyber incidents. Where needed, paid subscriptions are used for company financials and intelligence, patent databases, and news and financials so that product launches and pricing motions are not missed. These sources are illustrative only, and many other public references were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk sources cannot show clearly, like how many paid seats are active versus bundled, and how pricing moves between on-premise and cloud-delivered VPN. We spoke with a mix of enterprise IT buyers, managed service partners, and product and engineering leaders across major regions, and then we used follow-up checks where responses were inconsistent.

Inputs from these discussions were used to validate adoption rates by organization size, typical contract lengths, and the split between hardware refresh and subscription spend.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 39% |

| Mid tier: 45% | Functional/Unit leaders: 43% | EMEA: 37% |

| Smaller Players: 17% | Managers: 45% | Americas: 24% |

Market-Sizing & Forecasting

Our sizing starts with a top-down demand pool build that links secure remote access needs to connectivity, workforce patterns, and enterprise network footprints, then translates it into addressable VPN spending. Once the demand pool is shaped, it is cross-checked with selective bottom-up approximations such as sampled average selling prices times user counts, channel checks on managed VPN contracts, and spot supplier roll ups where disclosures are available.

Key model inputs include remote and hybrid workforce penetration, enterprise VPN concurrency and seat utilization, cloud adoption levels that shift spend toward subscription delivery, average price per user and per site, and the pace of hardware refresh cycles for gateway appliances. Where direct volume is not observable, gaps are handled using ranges agreed with interviewees, and the midpoint is adjusted only when multiple signals point in the same direction.

For forecasting, we use scenario analysis supported by regression-style relationships between the main demand drivers and VPN spend, so the outlook stays explainable and can be recalculated when a driver changes. Growth assumptions are tuned by region using broadband trends, regulatory pressure on data protection, and the practical substitution pressure from adjacent access solutions discussed in interviews.

Data Validation & Update Cycle

Validation is done in steps, starting with checks that totals reconcile with independent indicators like enterprise security spending direction, cloud network service growth, and reported customer additions for VPN offerings. When a variance looks too large, we revisit the input that drives it, re-check the math, and then re-contact sources if the gap is tied to adoption, pricing, or packaging changes.

Before sign-off, the model goes through a second-analyst review so that assumptions, currency handling, and year mapping are consistent across regions. Reports are refreshed annually, and interim updates are made when major events shift demand, such as large regulatory changes or broad enterprise policy moves toward new access architectures. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Virtual Private Network Market Size Measured Against Other Published Estimates

Published VPN market values often differ because each publisher draws the market line in a slightly different place, and because the same product can be sold as hardware, subscription software, or a managed service. Timing also matters, since price-per-user and the mix shift toward cloud delivery can change quickly from one year to the next.

Consumer VPN subscriptions bundled inside broader security suites sit outside Mordor Intelligence's scope, which tends to narrow the counted revenue to more directly priced VPN offerings and reduces double counting when buyers purchase overlapping security packages. Other estimates can also diverge when they back-cast from a long forecast without rechecking base-year pricing, or when they convert currency using different average-year rates instead of the same timing across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 61.26 B (2025) | |

| Industry Publisher A | USD 54.10 B (2025) | Uses a narrower counted revenue pool in practice, where enterprise-grade managed services and some hardware gateways appear to be partially underrepresented, and the slower CAGR suggests conservative ASP progression. |

| Industry Research Desk B | USD 48.50 B (2023) | Different base year and a shorter historical window can compress the starting value, and some versions of this scope treat connectivity and deployment splits differently, which shifts what is attributed to VPN versus adjacent network security spend. |

The spread is mainly explained by what gets counted as paid VPN revenue versus bundled security features, along with base-year selection and how price changes are carried forward. By keeping the inputs tied to visible demand signals and checking them with interview feedback, the estimate stays traceable to repeatable steps rather than being driven by a single headline growth rate.

Key Questions Answered in the Report

What is the projected size of the virtual private network market by 2031?

The market is expected to reach USD 142.06 billion by 2031, supported by a 15.05% CAGR.

Which deployment mode is expanding fastest in the virtual private network market?

Cloud deployment is growing at a 16.83% CAGR and held 62.70% of 2025 revenue.

Why is Asia-Pacific the fastest-growing region?

Rapid digitization, 5G expansion, and new cybersecurity mandates are driving a 15.96% CAGR in the region.

Which industry vertical shows the highest growth potential?

Healthcare and life sciences is advancing at a 15.41% CAGR due to telemedicine and strict data privacy regulations.

Page last updated on: