Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

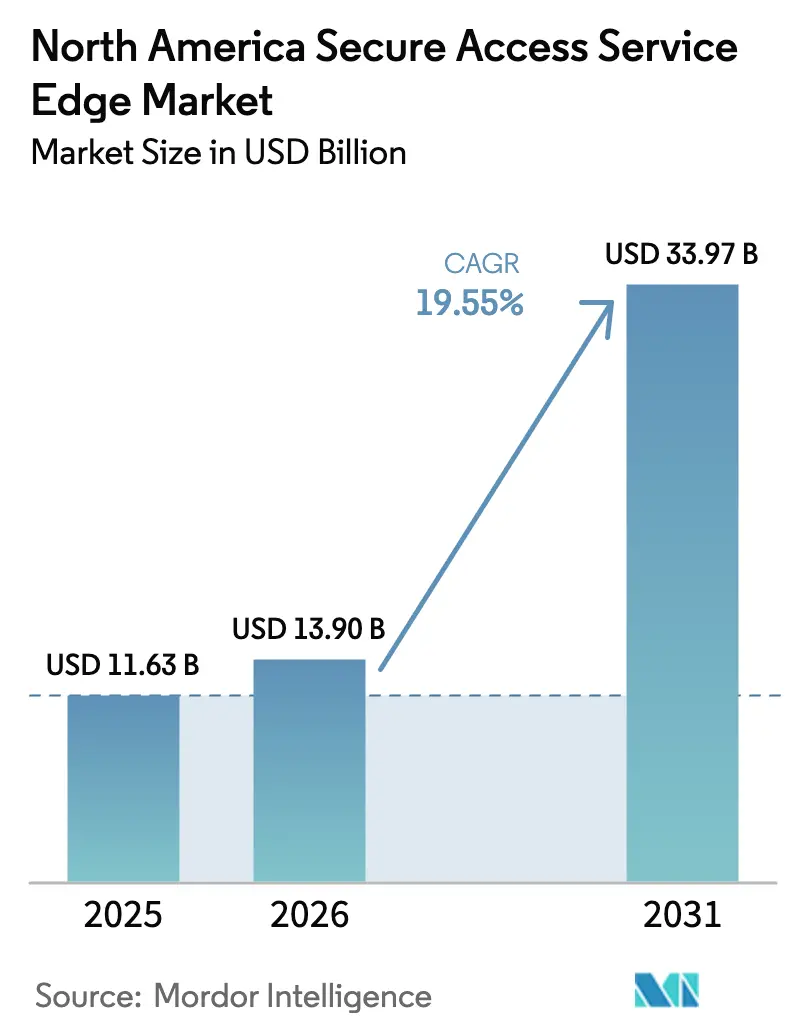

| Base Year Market Size (2025) | USD 11.63 Billion |

| Market Size (2026) | USD 13.9 Billion |

| Market Size (2031) | USD 33.97 Billion |

| Growth Rate (2026 - 2031) | 19.55% CAGR |

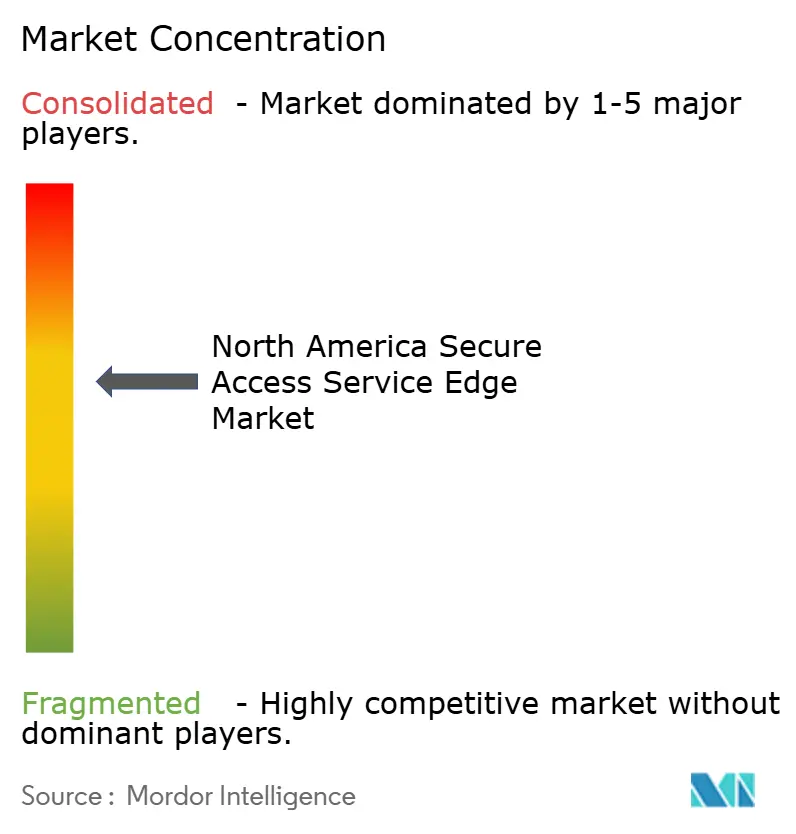

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Secure Access Service Edge Market Analysis by Mordor Intelligence

The secure access service edge market size in 2026 is estimated at USD 13.9 billion, growing from 2025 value of USD 11.63 billion with 2031 projections showing USD 33.97 billion, growing at 19.55% CAGR over 2026-2031. Rapid convergence of networking and security in a single cloud-native stack satisfies hybrid-work connectivity, suppresses recurrent cyber threats, and eliminates costly on-premise hardware. Cloud delivery removes geographic constraints, helping large enterprises standardize policy enforcement and allowing small and medium companies to acquire enterprise-grade protection without capital outlays. Persistent regulatory pressure around data privacy accelerates platform upgrades, while 5G-enabled edge connectivity fuels managed-service uptake among distributed branches. Leading vendors compete on AI-assisted orchestration that provisions dynamic policies, safeguards multi-cloud traffic, and trims operating expenses through automated troubleshooting.

Key Report Takeaways

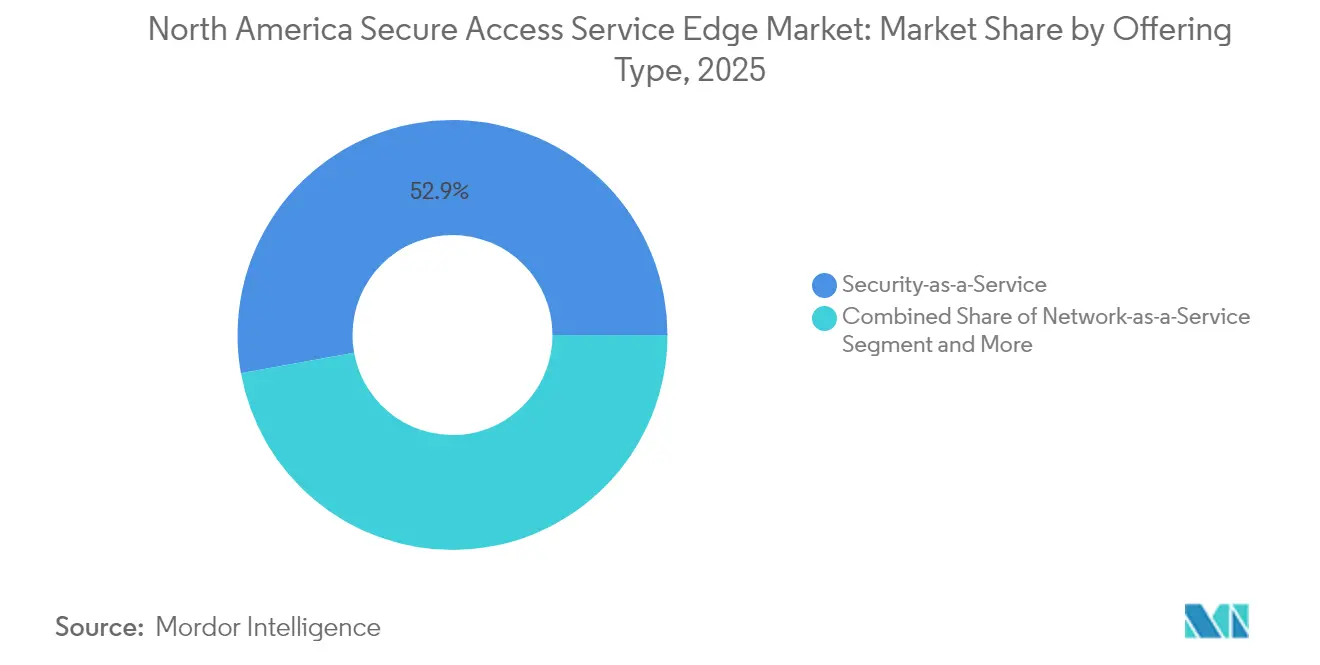

- By offering type, Security-as-a-Service captured 52.85% of secure access service edge market share in 2025, while Managed SASE Services is forecast to grow at 20.1% CAGR to 2031.

- By component, SD-WAN held 41.25% contribution to secure access service edge market size in 2025; Zero-Trust Network Access is poised to advance at 20.9% CAGR through 2031.

- By deployment mode, cloud deployments accounted for 64.92% of secure access service edge market size in 2025 and are expected to register 22.15% CAGR during the period.

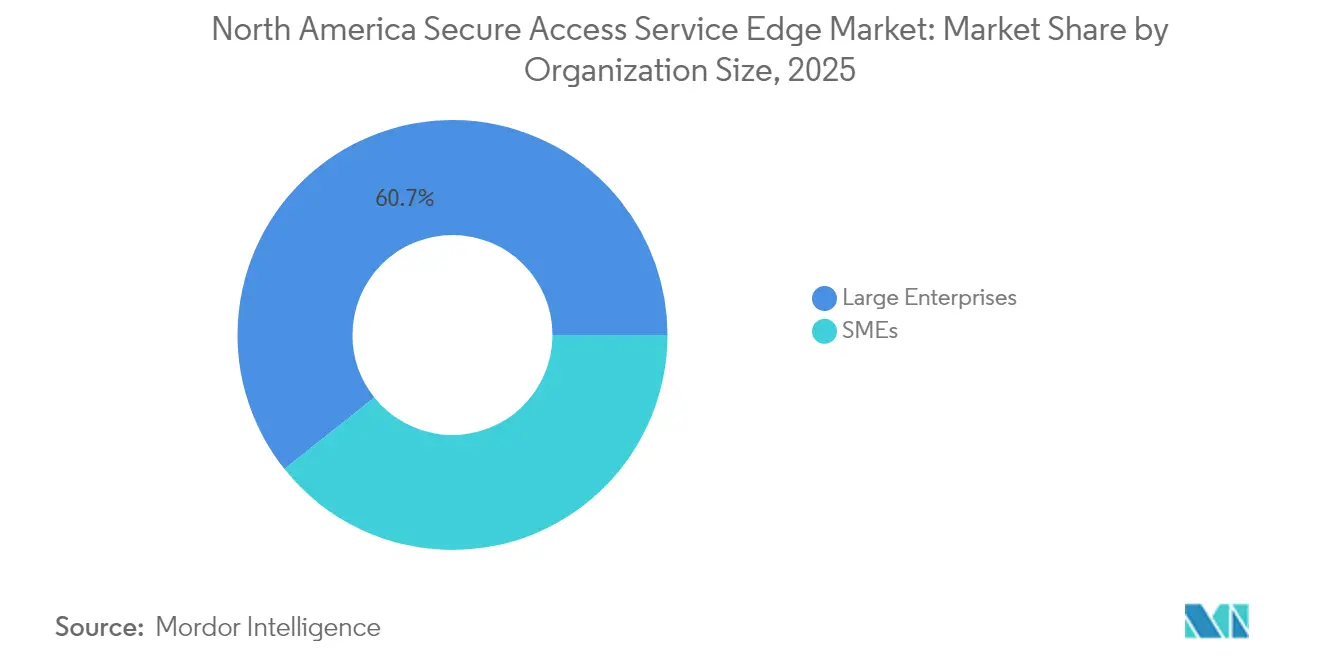

- By organization size, large enterprises controlled 60.72% of secure access service edge market size in 2025, whereas SMEs are expanding at 21.05% CAGR through 2031.

- By end-user vertical, BFSI commanded 27.05% revenue in 2025; healthcare is projected to grow at 19.95% CAGR through 2031.

- By country, the United States maintained 79.25% share of secure access service edge market size in 2025, while Mexico is anticipated to post 20.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Secure Access Service Edge Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hybrid-work connectivity demands | +4.2% | Global, with highest concentration in US and Canada | Short term (≤ 2 years) |

| Exploding multi-cloud and SaaS traffic volumes | +3.8% | North America core, spill-over to Mexico | Medium term (2-4 years) |

| Tightening data-privacy mandates (CCPA, Quebec Bill-64) | +2.9% | US California, Canada Quebec, expanding regionally | Long term (≥ 4 years) |

| AI-driven policy automation lowering OPEX | +3.1% | US enterprise hubs, Canada financial centers | Medium term (2-4 years) |

| 5G carriers bundling managed SASE at the edge | 2.7% | US major metros, Canada urban centers | Long term (≥ 4 years) |

| Sustainability push to consolidate branch hardware | 2.5% | North America, with early gains in tech corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Hybrid-Work Connectivity Demands

More than 80% of North American organizations plan Zero Trust adoption by 2026, reflecting a decisive shift away from legacy VPNs that reported an 82.5% increase in critical vulnerabilities between 2020 and 2025.[1]Mary Pratt, “Why 81% of Organizations Plan to Adopt Zero Trust by 2026,” CIO, cio.com SASE platforms enforce identity-centric access, micro-segmentation, and continuous verification, thereby stabilizing remote productivity. A case study from Salesforce recorded a fivefold bandwidth gain after swapping MPLS links for an SD-WAN-powered SASE backbone without inflating connectivity cost.

Exploding Multi-Cloud and SaaS Traffic Volumes

Direct cloud break-out via SD-WAN reduces round-trip latency up to five times compared with data-center backhaul, ensuring reliable SaaS performance.[2]Zeus Kerravala, “Achieving WAN Transformation with Security-Driven Networking,” Network World, networkworld.com SASE delivers uniform policy across Amazon Web Services, Microsoft Azure, and Google Cloud workloads. Cisco’s Cloud OnRamp cuts public-cloud onboarding from days to hours and optimizes routing for biopharma R&D platforms handling genome datasets.

Tightening Data-Privacy Mandates (CCPA, Quebec Bill-64)

California and Quebec privacy laws impose real-time breach notification and hefty penalties for data mismanagement. Native Data Loss Prevention inside SASE inspects traffic streams to block regulated content exfiltration. Healthcare illustrates urgency: 181 ransomware incidents exposed 25.6 million patient records in 2024, driving average ransom demands to USD 5.7 million.

AI-Driven Policy Automation Lowering OPEX

Cato Networks applies predictive analytics to recommend granular access rules that self-adjust as usage patterns shift, reducing manual ticket volumes. Palo Alto Networks adds natural-language prompts to its AI-Powered SASE so administrators can describe intent in everyday English rather than syntax-heavy commands.[3]Palo Alto Networks, “Salesforce Supercharges Its Bandwidth with Prisma SD-WAN,” paloaltonetworks.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy MPLS migration complexity | -2.8% | US enterprise corridors, Canada financial districts | Medium term (2-4 years) |

| Cyber-security talent scarcity | -2.1% | North America, acute in rural and mid-tier cities | Long term (≥ 4 years) |

| Single-vendor lock-in concerns | -1.7% | US large enterprises, Canada government sectors | Short term (≤ 2 years) |

| Rural-broadband latency constraints | -1.4% | Rural US, remote Canada, northern Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy MPLS Migration Complexity

MPLS bandwidth now grows only 6.7% through 2028, contrasted with cloud traffic that climbs 29% annually, leaving a widening performance gap. Rip-and-replace strategies risk downtime and mis-configured access controls, so many enterprises stage migration by overlaying SD-WAN tunnels on existing circuits. Temporary exposure of unused firewall rules can create lateral-movement opportunities that adversaries exploit during cut-over windows.

Cyber-Security Talent Scarcity

ISC² research reports that North America faces a shortfall of 500,000 qualified practitioners, with rural municipalities experiencing the steepest hiring challenges. Mexican executives mention talent deficits among the top three obstacles to 5G security adoption. SASE mitigates the gap by consolidating control planes and surfacing AI-generated recommendations that level workloads across lean IT teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering Type: Managed Services Accelerate Cloud Security Adoption

The secure access service edge market records Security-as-a-Service at 52.85% contribution in 2025 owing to preference for subscription models that eliminate capex. Managed SASE Services, though smaller today, shows a 20.1% CAGR and benefits from bundled connectivity that collapses firewall, VPN, and SD-WAN into a per-site fee. Telecom carriers deepen addressable reach by embedding clientless authentication in SIM cards, reducing provisioning friction for field workers. Professional Services remain critical during transition, guiding assessments, design validation, and post-migration optimization for highly regulated sectors such as banking. Network-as-a-Service reinforces subscription momentum through bandwidth-on-demand that scales during seasonal traffic peaks. Strategic alliances between integrators and hyperscalers further streamline adoption cycles as pre-tested reference architectures shorten proof-of-concept phases.

Service evolution also reflects vendor appetite to bolster recurring revenue. Verizon’s Advanced SASE, ATandT’s edge computing partnership, and T-Mobile’s 5G slices illustrate diversified roadmaps that broaden addressable verticals. Enterprises that once purchased security appliances every five years now renew cloud licenses annually, improving forecast accuracy for providers. As price competition intensifies, AI-enhanced self-service dashboards emerge as differentiation levers, empowering customers to tweak policies without professional-service engagements.

By Component: Zero Trust Reconfigures Network Foundations

SD-WAN furnished 41.25% revenue in 2025 and remains the baseline for traffic steering and dynamic path selection. Yet growth moderates as the technology becomes table-stakes. Zero-Trust Network Access rises on a 20.9% CAGR trajectory as remote access modernizes beyond VPN. Incorporation of device posture checks and user behavioral analytics reduces attack surface inside high-value workloads. Secure Web Gateway and Cloud Access Security Broker still attract compliance-driven spending among financial and healthcare entities that must log every SaaS transaction. Firewall-as-a-Service migrates distributed policy engines to cloud points of presence, cutting update latency. Data Loss Prevention gains from privacy mandates, while Digital Experience Monitoring helps operations teams diagnose latency spikes with real-time hop-by-hop visibility.

Component convergence favors single-vendor catalogs: Gartner forecasts that unified platforms will control 65% of SD-WAN procurement by 2027, up from 20% in 2024. Netskope’s purchase of Infiot produced a Borderless WAN delivering Zero Trust, quality-of-experience analytics, and application acceleration inside one portal. Fortinet integrates threat intelligence across next-generation firewall, SD-WAN, and secure edge, minimizing policy drift and expediting incident response.

By Deployment Mode: Cloud-First Outpaces On-Premise Holdings

Cloud accounts for 64.92% adoption and advances at 22.15% CAGR as enterprises dislodge data-center security stacks in favor of distributed inspection nodes closer to users. Scalability appeals to seasonal businesses that ramp capacity for promotional events then dial down to baseline. On-premise retains a foothold for low-latency trading desks and classified government workloads bound by sovereign mandates. Hybrid blueprints combine colocation gateways with SASE points of presence to maintain predictable performance while managing compliance. VMware’s portfolio exemplifies deployment flexibility by allowing customers to toggle between cloud gateways and locally hosted orchestrators without altering policy objects.

Edge computing reshapes the landscape further. 5G adoption climbs and pushes inspection to base-station proximity, cutting round-trip delay for augmented-reality maintenance in manufacturing plants. Carrier-controlled slices reserve predictable throughput and embed inline DNS filtering, closing gaps that previously existed between cellular and fixed branches. Energy-efficient hardware designed for remote office shelves supports the sustainability imperative to shrink rack density and power draw at subordinate sites.

By Organization Size: SMEs Narrow the Protection Gap

Large enterprises command 60.72% of revenue due to entrenched budget allocations and multicloud complexity that demands ultra-granular segmentation. Still, SMEs clock a 21.05% CAGR, capitalizing on pay-as-you-grow licensing that removes upfront hardware procurement. One cloud dashboard replaces a patchwork of disparate firewalls, content filters, and VPN concentrators, lowering training overhead. Technology partners target SMEs with pre-configured blueprints that auto-discover endpoints and push least-privileged rules in seconds.

For large organizations, consolidation motives dominate. Internal audits reveal overlapping firewall renewals, redundant web gateways, and scattered SSL decryption services that bloat opex. A pivot to a single platform achieves lower renewal complexity and simplifies vendor management. Governance gains as audit trails centralize under one management plane, satisfying board-level scrutiny on cyber-risk posture.

By End-User Vertical: Healthcare Surges as Threats Multiply

BFSI keeps 27.05% share due to strict regulatory frameworks such as PCI-DSS and FFIEC guidelines that direct continuous monitoring and data-in-motion encryption. Healthcare is the fastest riser at 19.95% CAGR as ransomware crews shift to double-extortion tactics, threatening to leak protected health information if payment stalls. Zero Trust Hospital architecture introduces micro-segmentation at every medical device, blocking lateral movement that often cripples radiology or infusion pumps during an attack. Retail benefits from omnichannel ordering, requiring branch connectivity that scales with seasonal peaks. Government agencies adopt the architecture to satisfy the U.S. Executive Order on Improving the Nation’s Cybersecurity, which stipulates a Zero Trust shift for federal networks. Manufacturing embraces SASE to guard operational technology that now stream telemetry directly to cloud analytics platforms.

Digital transformation aligns with pandemic-driven telehealth expansion. SASE integrates with HIPAA-compliant video solutions and EHR systems, performing in-line policy checks that ensure patient data remain confined to approved domains. Endpoint isolation restricts contractor access to specific hospital departments, preventing credentials hijacked from remote staff from pivoting into electronic records.

Geography Analysis

The secure access service edge market exhibits material regional divergence across North America. The United States contributes 79.25% revenue in 2025 thanks to dense enterprise clusters in Silicon Valley, New York, and Washington D.C. that require high-grade perimeterless security. Cloud migration across federal agencies and Fortune 500 banks sustains multiyear upgrades, reinforcing first-mover status. Tier-1 carriers partner with platform vendors to embed Zero Trust in 5G fixed-wireless offerings that backhaul traffic to nationwide SASE points of presence.

Canada follows with steady momentum anchored by Quebec Bill-64, which elevates data-sovereignty obligations and compels cross-border businesses to adopt uniform inspection across states and provinces. Financial centers in Toronto and Vancouver install cloud gateways that log flows in Canadian soil to satisfy local residency mandates. Healthcare networks adopt SASE to mitigate ransomware, leveraging AI analytics to flag anomalous East-West traffic within patient portals.

Competitive Landscape

North American competition remains moderately consolidated. The top five vendors, led by Palo Alto Networks, Cisco, Zscaler, Fortinet, and Cato Networks, together oversee a sizable slice of recurring subscription revenue. Consolidation persists: Palo Alto Networks completed its USD 28 billion Splunk takeover in 2024, folding observability into security analytics to provide richer threat context. Cisco acquired IBM’s QRadar assets to infuse SIEM telemetry into Secure Connect, strengthening lateral-movement detection. Netskope added Infiot and now markets Borderless WAN that merges connectivity and security into one license.

Vendors differentiate on AI. Zscaler processes over 500 billion daily transactions through machine-learning models that correlate user, device, and destination risk scores. Cato’s Autonomous Policies predict optimal segmentation tags and auto-tune them to traffic shifts, easing administration for resource-constrained teams. Fortinet leverages custom ASICs inside its Security Fabric to push deep-packet inspection at wire rates that match high-speed fiber links, preserving user experience during cloud breakout.

North America Secure Access Service Edge Industry Leaders

Akamai Technologies Inc.

Aruba Networks (an HPE Company)

AT&T Inc.

Barracuda Networks Inc.

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Zscaler announced the acquisition of Red Canary to fold managed detection and response into its Zero Trust Exchange platform.

- May 2025: T-Mobile and Palo Alto Networks introduced a managed SASE service that embeds Prisma SASE into 5G network slices for rapid device onboarding.

- April 2025: Netskope closed its acquisition of Infiot, delivering a single-vendor SASE complete with Borderless WAN optimization.

- September 2024: Palo Alto Networks finalized the purchase of IBM’s QRadar SaaS assets to enhance Cortex XSIAM analytics.

North America Secure Access Service Edge Market Report Scope

For security and connectivity, the secure access service edge architecture is recommended. SASE combines wide area network (WAN) technology for robust onramp to cloud and network security services into one cloud-delivered connectivity and security software stack. This enables enterprises to connect geographically diverse workforces securely while reducing network latency and performance issues.

The North American secure access service edge market is segmented into offering type (network-as-a-service and security-as-a-service), organization size (large enterprises and small and medium enterprises), end-user vertical (BFSI, IT and telecom, retail, healthcare, government, manufacturing, and other end-user verticals), and country (United States and Canda). The report offers market forecasts and size in value (USD) for all the above segments.

By Offering Type

| Network-as-a-Service |

| Security-as-a-Service |

| Managed SASE Services |

| Professional Services (Assessment, Integration) |

By Component

| Software-defined WAN (SD-WAN) |

| Secure Web Gateway (SWG) |

| Cloud Access Security Broker (CASB) |

| Zero-Trust Network Access (ZTNA) |

| Firewall-as-a-Service (FWaaS) |

| Data-Loss Prevention (DLP) |

| Digital Experience Monitoring |

By Deployment Mode

| Cloud |

| On-premise |

By Organization Size

| Large Enterprises |

| SMEs |

By End-user Vertical

| Banking, Financial Services and Insurance (BFSI) |

| IT and Telecommunications |

| Retail and eCommerce |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Manufacturing and Industrial |

| Education |

| Other Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Offering Type | Network-as-a-Service |

| Security-as-a-Service | |

| Managed SASE Services | |

| Professional Services (Assessment, Integration) | |

| By Component | Software-defined WAN (SD-WAN) |

| Secure Web Gateway (SWG) | |

| Cloud Access Security Broker (CASB) | |

| Zero-Trust Network Access (ZTNA) | |

| Firewall-as-a-Service (FWaaS) | |

| Data-Loss Prevention (DLP) | |

| Digital Experience Monitoring | |

| By Deployment Mode | Cloud |

| On-premise | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By End-user Vertical | Banking, Financial Services and Insurance (BFSI) |

| IT and Telecommunications | |

| Retail and eCommerce | |

| Healthcare and Life Sciences | |

| Government and Public Sector | |

| Manufacturing and Industrial | |

| Education | |

| Other Industries | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current value of the North American secure access service edge market?

The secure access service edge market size stands at USD 13.9 billion in 2026.

How fast is the market expected to grow?

The market is projected to post a 19.55% CAGR and reach USD 33.97 billion by 2031.

Which deployment model leads adoption?

Cloud deployment holds 64.92% share and is growing at 22.15% CAGR, reflecting strong preference for cloud-first security.

What vertical will grow the fastest?

Healthcare is projected to expand at 19.95% CAGR as hospitals combat ransomware and comply with privacy regulations.

Page last updated on: