Conditional Access System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

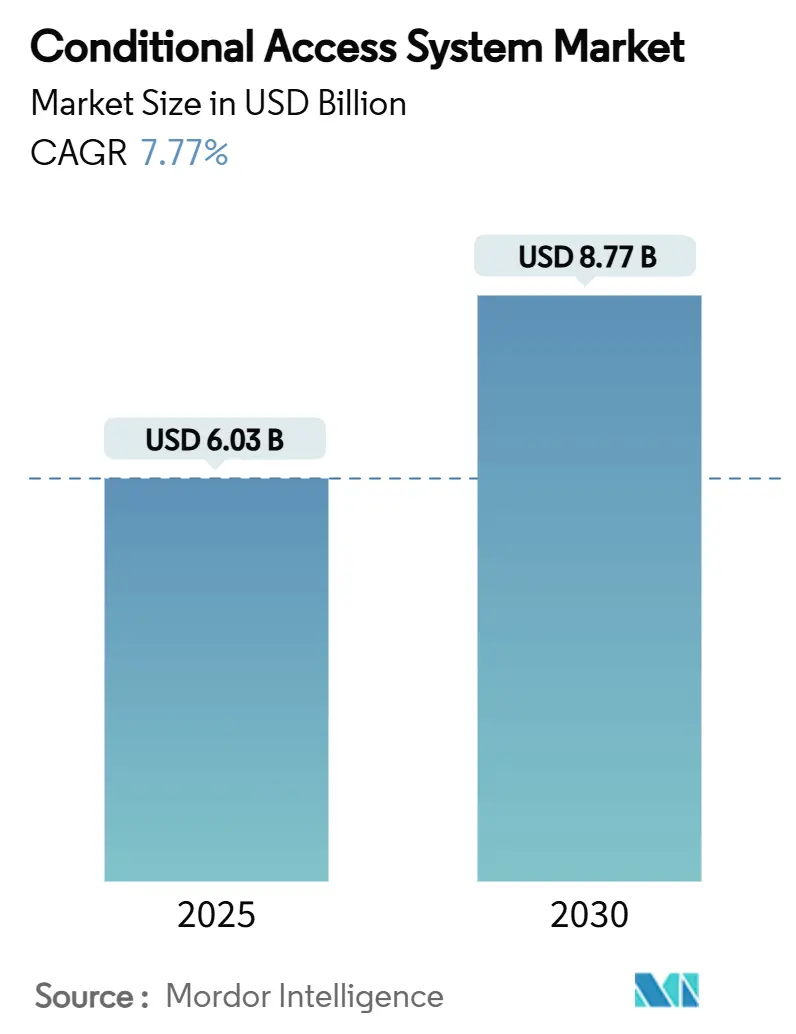

| Market Size (2025) | USD 6.03 Billion |

| Market Size (2030) | USD 8.77 Billion |

| Growth Rate (2025 - 2030) | 7.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Conditional Access System Market Analysis by Mordor Intelligence

The conditional access system market size stands at USD 6.03 billion in 2025 and is forecast to reach USD 8.77 billion by 2030, expanding at a 7.77% CAGR during the period 2025-2030. Intensifying digital-TV switchover programmes, rising piracy threats, and operator migration from legacy smart-card infrastructure to cloud-hosted security platforms sustain steady capital spending despite cord-cutting pressures in mature economies. Cardless architectures, multi-DRM convergence, and SaaS delivery models underpin cost optimisation strategies, while satellite networks, 5G-broadcast pilots, and the proliferation of free ad-supported streaming television (FAST) diversify distribution pathways. Competitive positioning centres on AI-driven threat analytics and forensic watermarking, with vendors bundling anti-piracy services to defend high-value sports and premium Asian drama franchises. Meanwhile, regional bifurcation persists: APAC’s subscriber expansion offsets North American and Western European contraction, prompting vendors to localise price-sensitive solutions for Africa and South Asia.

Key Report Takeaways

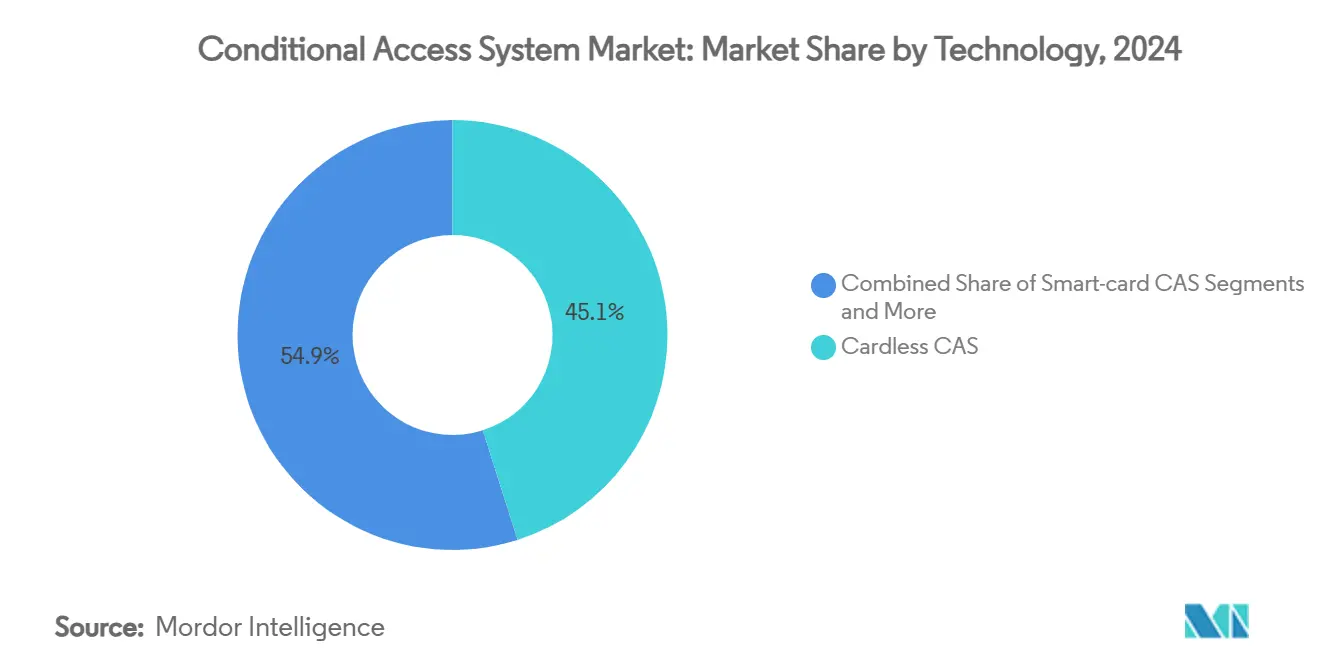

- By technology, cardless platforms captured 45.1% of the conditional access system market share in 2024; CAS-as-a-Service is projected to expand at an 8.5% CAGR to 2030, the fastest within the segment.

- By network type, satellite TV held 38.2% of the conditional access system market size in 2024; whereas OTT/streaming networks are advancing at a 7.9% CAGR through 2030.

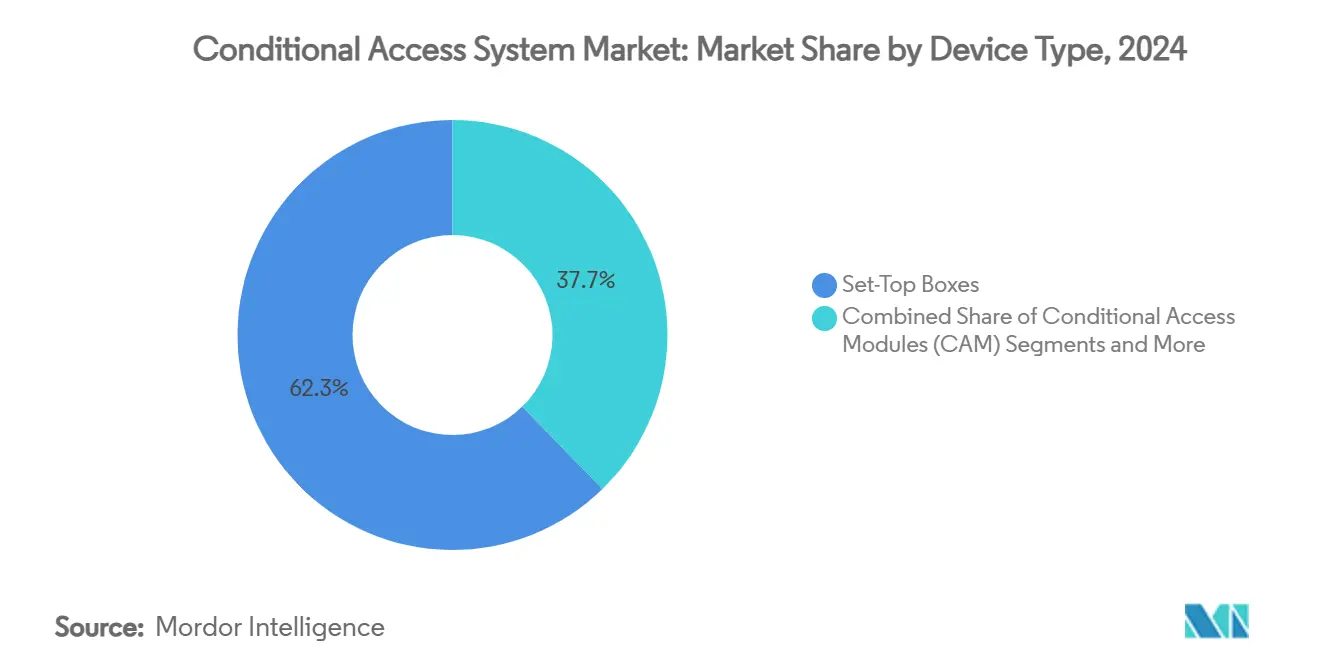

- By device, set-top boxes accounted for 62.3% of the conditional access system market share in 2024; while, streaming dongles are forecast to grow at an 8.2% CAGR through 2030.

- By end user, pay-TV operators commanded 54.5% of the conditional access system market size in 2024; whereas content aggregators/OTT platforms record the highest projected CAGR at 8.8% to 2030.

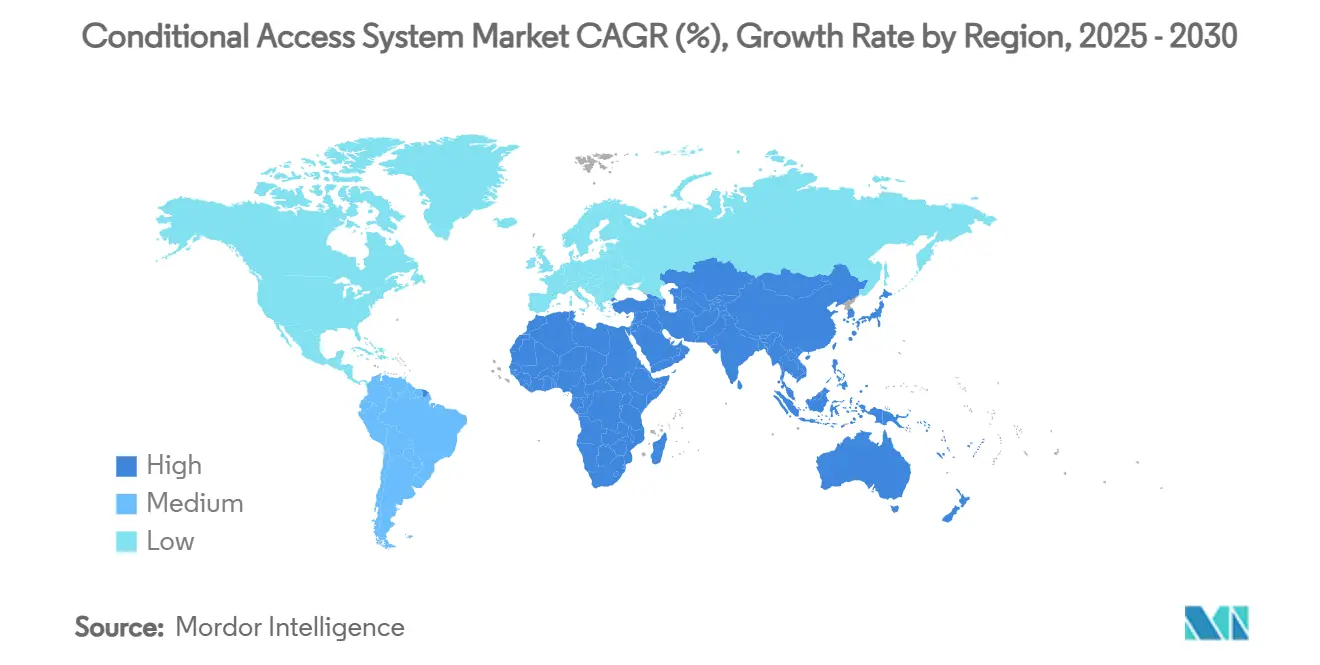

- By geography, Asia Pacific led with 42.5% conditional access system market share in 2024; while Asia Pacific is forecast to post an 8.4% CAGR through 2030.

Global Conditional Access System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated digital-TV switchover deadlines | +1.2% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Rising piracy and need for content protection | +1.8% | Global, with emphasis on APAC and emerging markets | Long term (≥ 4 years) |

| Migration to cardless and SaaS CAS lowers OpEx | +1.5% | Global, early adoption in North America & EU | Short term (≤ 2 years) |

| Expanding pay-TV base in Africa and South Asia | +1.0% | Africa, South Asia, with spillover to ASEAN | Medium term (2-4 years) |

| FAST channels need lightweight CAS | +0.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| 5G-broadcast mobile TV roll-outs | +0.4% | EU pilot markets, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandated Digital-TV Switchover Deadlines Drive Infrastructure Modernisation

Government-imposed analogue switch-off schedules in India, China, and selected African states compel broadcasters and multichannel operators to retrofit or replace head-end encryption and subscriber management systems on strict calendars. India’s digitisation programme alone covers more than 130 million TV households, generating urgent vendor demand for scalable, cardless conditional access deployments capable of meeting compressed roll-out windows. Vendors that can bundle network design, systems integration, and managed security services secure premium margins as smaller operators lack in-house expertise. Secondary cities and rural districts favour hybrid cloud solutions that offset limited logistics capacity for physical smart-card distribution. Africa’s forecast addition of 12 million satellite pay-TV subscribers by 2029 further illustrates the structural linkage between policy mandates and market expansion.

Rising Piracy Escalates Content-Protection Investment

Content piracy erodes USD 30 billion in annual revenue across the Asian video supply chain, prompting platform owners to converge conditional access with multi-DRM and forensic watermarking layers that identify source leaks in real time. Indonesia’s 54% piracy incidence catalysed formal industry-regulator taskforces, validating the effectiveness of cross-sector coalitions. AI-based traffic analysis flags abnormal streaming patterns, while watermark payloads trace illegal feeds to household level within minutes. Rapid threat visibility elevates security spending among rights holders of premium Korean drama and UEFA football fixtures, and creates recurring monitoring revenue for vendors. French public broadcaster France Télévisions shifted to a unified DRM-CAS stack for live sports in 2024 to balance scale with heightened risk exposure.

Migration to Cardless and SaaS CAS Lowers Operational Complexity

Operators transitioning from smart-card to software-based conditional access shave logistics, warehousing, and truck-roll expenses, while enabling weekly security patching and feature upgrades over IP backchannels. Charter Communications documented 40% higher lifecycle costs for dual CableCARD/STB installations, underscoring the economic case for cardless architectures. SaaS delivery further converts capital outlays into predictable opex: 86% of surveyed enterprises place SaaS security at the top of their budgets, with 76% projecting larger allocations in 2025. Cloud-native CAS extends enterprise-grade protection to micro-operators in Africa and Eastern Europe, accelerating competitive parity. Vendor investment in edge nodes mitigates latency for UHD sports streams, ensuring QoE targets remain intact.

Expanding Pay-TV Base in Africa and South Asia Creates Volume Opportunities

Sub-Saharan Africa is set to climb to 55 million pay-TV accounts by 2029, equating to 28% growth against 2024 baselines; Nigeria has already overtaken South Africa at 10 million subscribers. Satellite concentration demands low-cost, high-capacity conditional access solutions, while South Asian markets leverage India’s emerging Digital Public Infrastructure rails to support real-time entitlement messaging. [1]ERIA, “India-ASEAN Digital Public Infrastructure,” eria.org Vendors engineer tiered security profiles to accommodate price-sensitive subscribers without compromising encryption integrity. Fixed-wireless broadband in Southeast Asia, forecast to exceed 7.8 million lines by 2028, multiplies last-mile options and accelerates CAS node proliferation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pay-TV saturation in US and W. Europe | -1.5% | North America & Western Europe | Medium term (2-4 years) |

| High upgrade costs for legacy STBs | -0.9% | Global, concentrated in mature markets | Short term (≤ 2 years) |

| Encryption standards facing post-quantum scrutiny | -0.6% | Global, early impact in government/defense | Long term (≥ 4 years) |

| Rise of open-source / freemium anti-piracy tools | -0.4% | Global, particularly emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pay-TV Saturation in US and Western Europe Constrains Growth

North America’s pay-TV base will slide from 111 million in 2015 to roughly 60 million in 2029, slashing penetration to 43%. Western Europe faces a parallel, though milder, 8% contraction over the same horizon. With only 5% of US connected homes retaining pay-TV alone, conditional access vendors pivot toward upselling advanced watermark and anti-piracy modules to safeguard dwindling but high-value premium bundles. British broadcast plans to sunset terrestrial networks by 2034 illustrate how cost avoidance, rather than subscriber expansion, shapes capital allocations. Commercial success hinges on cross-border diversification and deeper penetration of hospitality, healthcare, and enterprise micro-segments.

High Upgrade Costs for Legacy Set-Top Boxes

Roughly 20 million PowerKEY-encrypted boxes risk service outage due to expired certificates, compelling US cable operators to budget USD 40 million per million devices for replacement when software patches prove unviable. Emerging-market operators also grapple with sunk investments in early-generation MPEG-2 zapper STBs introduced during the first digital wave. Adara Technologies’ “time-wrap” workaround for Dominican cable firm Aster shows the commercial appeal of firmware fixes that defer truck-rolls and landfill costs. Nonetheless, lingering fleets delay adoption of next-gen security protocols and diminish overall conditional access system market agility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Cardless Dominance Anchors Transition

Cardless systems represented 45.1% of conditional access system market share in 2024 and remain the de-facto standard for new roll-outs thanks to remote provisioning, inventory-free logistics, and stronger patch cadence. Operators in India and Indonesia adopted cardless simulcrypt to maintain encrypted broadcast services while layering DRM for catch-up content, reducing dual-vendor complexity. Smart-card platforms persist in military, casino, and maritime deployments where removable tokens assure physical custody. Unified CAS-plus-DRM suites widen appeal among OTT aggregators seeking one entitlement gateway across STB, mobile, and smart-TV footprints. CAS-as-a-Service, growing at an 8.5% CAGR, lowers entry barriers for micro-ISPs in Africa and Eastern Europe by pooling SOC functionality in regional cloud hubs.

The cloud trajectory also reshapes vendor economics: licence revenue converts to monthly subscription, while analytics extras such as concurrent-stream detection generate incremental fees. Yet regulatory stipulations in France and Saudi Arabia still compel on-premise key servers for Tier-1 sports, tempering immediate SaaS ubiquity. Post-quantum readiness emerges as the next differentiator, with early prototypes adding lattice-based key exchange inside cardless clients, though real-world adoption lags at just 0.029% of OpenSSH connections. [2]arXiv, “Measuring PQC Adoption Rates,” arxiv.org Collectively, these factors reinforce steady expansion of the conditional access system market toward hybrid, cloud-first architectures.

By Network Type: Satellite Retains Leadership Amid OTT Surge

Satellite held 38.2% of the conditional access system market size in 2024, underpinned by Africa’s vast rural geography and India’s direct-to-home subscriber inertia. Ku-band capacity deals remain cheaper than fibre backhaul in low-density regions, keeping dish-based TV relevant. Cable declines in the United States drove plant upgrades to IP video, yet Latin American MSOs still deploy DOCSIS-enabled hybrid networks to maximise sunk coaxial assets. IPTV’s share rises across South Korea and Vietnam where gigabit fibre penetration exceeds 80%; operators capitalise on in-home Wi-Fi 6 gateways that support multicast encryption with minimal delay.

OTT and FAST, advancing at a 7.9% CAGR, capture cord-cutters but amplify multi-DRM complexity as services span smartphones, consoles, and connected cars. 5G-broadcast pilots in Bavarian and Austrian alpine zones validated lower spectrum cost per bit relative to unicast, motivating regulators to re-evaluate UHF allocations for hybrid DVB-I plus 5G broadcast services. Conditional access vendors that embed both Broadcast-AES and Widevine L1 within a single entitlement stack gain procurement advantage as multi-network operators pursue capex efficiencies.

By Device Type: Set-Top Boxes Persist Against Streaming Dongles

Set-top boxes contributed 62.3% of conditional access system market share in 2024, retaining dominance as operators prefer turnkey control over UI, storage, and encryption upgrades. HDMI dongles nonetheless enjoy 8.2% CAGR owing to lower bill-of-material costs and self-install simplicity for transient subscribers in college dorms and rental flats. Conditional Access Modules (CAM) flourish in Germany and Scandinavia where integrated TVs ship with CI Plus 1.4 slots, eliminating external hardware while satisfying pay-TV compliance.

Smart-TV vendors pre-load embedded CAS, slashing operator subsidy expense, yet firmware fragmentation heightens QA overhead for security patches. Legacy PowerKEY fleets complicate North American upgrade blueprints; in response, Adara’s time-wrap deferral buys operators breathing room while they negotiate mass-market Android-TV STBs with SoC-level root-of-trust. Across all form factors, the conditional access system market gravitates toward secure video pipelines anchored by Trusted Execution Environments and dynamic fingerprinting.

By End User: Pay-TV Operators Hold Volume Leadership, OTT Drives Growth

Pay-TV operators owned 54.5% of conditional access system market size in 2024 but confront steady attrition in North America and Western Europe. Survival strategies include packaging broadband, voice, and FAST aggregations under one invoice, reinforcing customer lock-in. Telco TV units in Thailand and the Philippines pioneer prepaid wallet pricing, leveraging cloud CAS to activate or deactivate channels in seconds without new card issuance.

Content aggregators––principally SVOD, AVOD, and hybrid FAST providers––drive an 8.8% CAGR through 2030, spurred by data-centric monetisation and global addressable advertising inventory. Multi-regional-rights holders adopt unified entitlement fabric that honours studio contracts while delivering geo-specific ad pods. Enterprise TV emerges as a niche, with Fortune 500 firms streaming CEO town-halls and training modules behind CAS authentication. In hospitality, premium sports packages integrate NFC guest authentication to curb in-room piracy and upsell UHD events. These diversified use cases enlarge the conditional access system market beyond traditional broadcasting.

Geography Analysis

Asia Pacific leads the conditional access system market with a 42.5% share in 2024 and is projected to grow at 8.4% CAGR to 2030. India’s digitisation mandate alone accounts for more than 130 million households requiring encrypted cable and DTH feeds, while China’s policy support fuels regional vendor ecosystems that deliver low-cost cardless security chips. ASEAN’s fixed-wireless boom, projected at 7.87 million subscriptions by 2028, broadens IP-compatible security deployments. [3]Asia Video Industry Association, "The Asia Video Industry Report 2024," avia.org Local content such as Korean drama and Japanese anime continues to command premium CPMs, reinforcing investment in forensic watermarking.

North America’s subscriber erosion constricts domestic revenue pools, yet operators invest in AI-powered anti-piracy suites to protect high-value NFL and NBA rights, preserving average revenue per user even as household counts fall from 111 million to 60 million by 2029. Europe follows similar patterns: the UK eyes terrestrial shutdown by 2034, and German cable groups negotiate wholesale fibre migration, shifting security budgets toward cloud CAS with elastic concurrency controls. 5G-broadcast trials in Italy and Spain seek to revitalise free-to-air reach during public emergencies.

Middle East and Africa promise above-trend volume expansion, adding an estimated 12 million pay-TV homes by 2029, mostly via satellite. Nigerian DTH providers order low-bitrate HEVC encoders paired with entry-level cardless CAS to balance affordability with copy-protection. Latin America’s digital-terrestrial spectrum refarming accelerates hybrid broadcast-mobile models, yet fragmented regulatory regimes delay cross-border equipment harmonisation. Overall, geographic divergence compels conditional access vendors to engineer modular portfolios that scale both downwards for prepaid packages and upwards for 8K HDR live events.

Competitive Landscape

The conditional access system market maintains moderate concentration, with leading trio Nagra, Irdeto, and Synamedia integrating AI-assisted threat analytics and watermarking into core CAS licences to retain customers. Nagra’s OpenTV deployment at German cable group Tele Columbus extended service reach to smartphones and tablets, illustrating multi-screen convergence around a unified entitlement stack. Irdeto’s partnership with Media Distillery embeds content discovery AI within CAS workflows, boosting engagement for mid-tier European operators. Synamedia enhances forensic watermarking speeds to sub-second latency for live sports, meeting studio compliance mandates.

Emerging challengers leverage cloud-native architectures: Verimatrix Streamkeeper offers pay-as-you-stream pricing, while China-based AVFront builds open-source conditional access modules to compete on cost. Patent filings in post-quantum key derivation and zero-trust service mesh indicate next-wave differentiation, though commercial roll-outs remain limited. Consolidation intensifies in adjacent physical access sectors, exemplified by ASSA ABLOY’s USD 21 million twin acquisition to reinforce credential management synergies with digital video security.

Strategic alliances with hyperscale clouds reduce go-to-market friction: AWS Elemental integrates conditional access APIs that auto-scale during peak events, while Azure’s Confidential Computing enclaves host decryption keys. Smaller vendors lacking capital for SOC upgrades gravitate toward joint marketing bundles or white-label options under incumbent umbrellas. Collectively, AI toolchains, cloud elasticity, and forensic watermark breadth form the decisive axes of competition through 2030, shaping procurement criteria across the conditional access system industry.

Conditional Access System Industry Leaders

-

Nagra (Kudelski Group)

-

Irdeto

-

Synamedia

-

Verimatrix

-

Viaccess-Orca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tele Columbus added mobile apps to its PŸUR TV service using Nagravision’s OpenTV Platform and 3SS’s 3Ready, enhancing AI-driven content recommendations.

- February 2025: Acre Security acquired REKS to infuse generative-AI chat into access control interfaces, reinforcing natural-language diagnostics.

- January 2025: ASSA ABLOY agreed to acquire 3millID and Third Millennium for USD 21 million, broadening its North American and UK credential portfolios.

- November 2024: Adara Technologies delivered a PowerKEY “time-wrap” fix for Aster Tecnodisa, safeguarding 45,000 cable subscribers from device sunset.

Global Conditional Access System Market Report Scope

| Smart-card CAS |

| Cardless CAS |

| Hybrid Simulcrypt Solutions |

| CAS-as-a-Service (SaaS) |

| CAS + Multi-DRM Unified |

| Cable TV |

| Satellite TV |

| IPTV |

| Digital Terrestrial (DTT) |

| OTT / Streaming |

| 5G Broadcast / Mobile |

| Set-Top Boxes |

| Conditional Access Modules (CAM) |

| Smart TVs (embedded CAS) |

| Streaming Dongles / STB-less |

| Pay-TV Operators |

| Content Aggregators / OTT Platforms |

| Hospitality |

| Healthcare |

| Education and Campus TV |

| Enterprise and Corporate TV |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| ASEAN (Indonesia, Thailand, Vietnam, Philippines, Malaysia) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Egypt | ||

| Rest of Africa | ||

| By Technology | Smart-card CAS | ||

| Cardless CAS | |||

| Hybrid Simulcrypt Solutions | |||

| CAS-as-a-Service (SaaS) | |||

| CAS + Multi-DRM Unified | |||

| By Network Type | Cable TV | ||

| Satellite TV | |||

| IPTV | |||

| Digital Terrestrial (DTT) | |||

| OTT / Streaming | |||

| 5G Broadcast / Mobile | |||

| By Device Type | Set-Top Boxes | ||

| Conditional Access Modules (CAM) | |||

| Smart TVs (embedded CAS) | |||

| Streaming Dongles / STB-less | |||

| By End User | Pay-TV Operators | ||

| Content Aggregators / OTT Platforms | |||

| Hospitality | |||

| Healthcare | |||

| Education and Campus TV | |||

| Enterprise and Corporate TV | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| ASEAN (Indonesia, Thailand, Vietnam, Philippines, Malaysia) | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | Nigeria | ||

| South Africa | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the conditional access system market?

The conditional access system market size stands at USD 6.03 billion in 2025.

Which region leads the conditional access system market?

Asia Pacific holds the largest share at 42.5% in 2024 and is also the fastest-growing region.

Which technology segment is growing the fastest?

CAS-as-a-Service is expanding at an 8.5% CAGR through 2030 due to its opex-friendly pricing.

How are streaming platforms influencing conditional access demand?

The rise of OTT and FAST services, growing at 7.9% CAGR, pushes demand for unified multi-DRM and CAS solutions across devices.

What are the main restraints on market growth?

Subscriber saturation in North America and Western Europe and the costly upgrade of legacy set-top boxes weigh on near-term expansion.

Who are the key players in the conditional access system industry?

Nagravision, Irdeto, and Synamedia lead the market, each combining traditional CAS with AI-powered anti-piracy and watermarking services.

Page last updated on: