5G Network Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

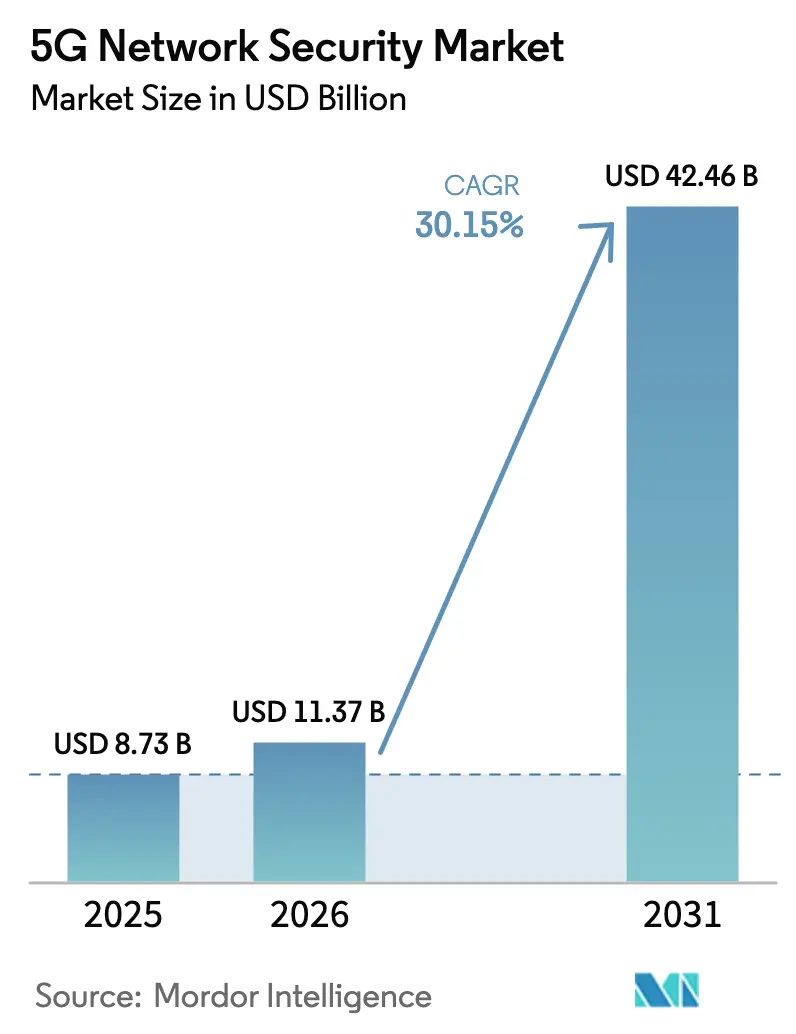

| Market Size (2026) | USD 11.37 Billion |

| Market Size (2031) | USD 42.46 Billion |

| Growth Rate (2026 - 2031) | 30.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G Network Security Market Analysis by Mordor Intelligence

The 5G network security market size is expected to grow from USD 8.73 billion in 2025 to USD 11.37 billion in 2026 and is forecast to reach USD 42.46 billion by 2031 at 30.15% CAGR over 2026-2031. Growth is powered by the shift to standalone 5G cores, rapid network-slicing adoption, and overlapping mandates from 3GPP, NIST, and ETSI that require deeper, API-level protection. Enterprises are moving quickly to private 5G, especially in manufacturing and healthcare, and they expect carrier-grade security controls that scale from core to edge. Managed security services are gaining favor because few firms can keep pace with the skill demands of zero-trust architectures. Meanwhile, the push for multi-access edge computing (MEC) drives demand for distributed threat detection that works within stringent latency budgets. Together, these conditions reinforce a robust expansion path for the 5G network security market.

Key Report Takeaways

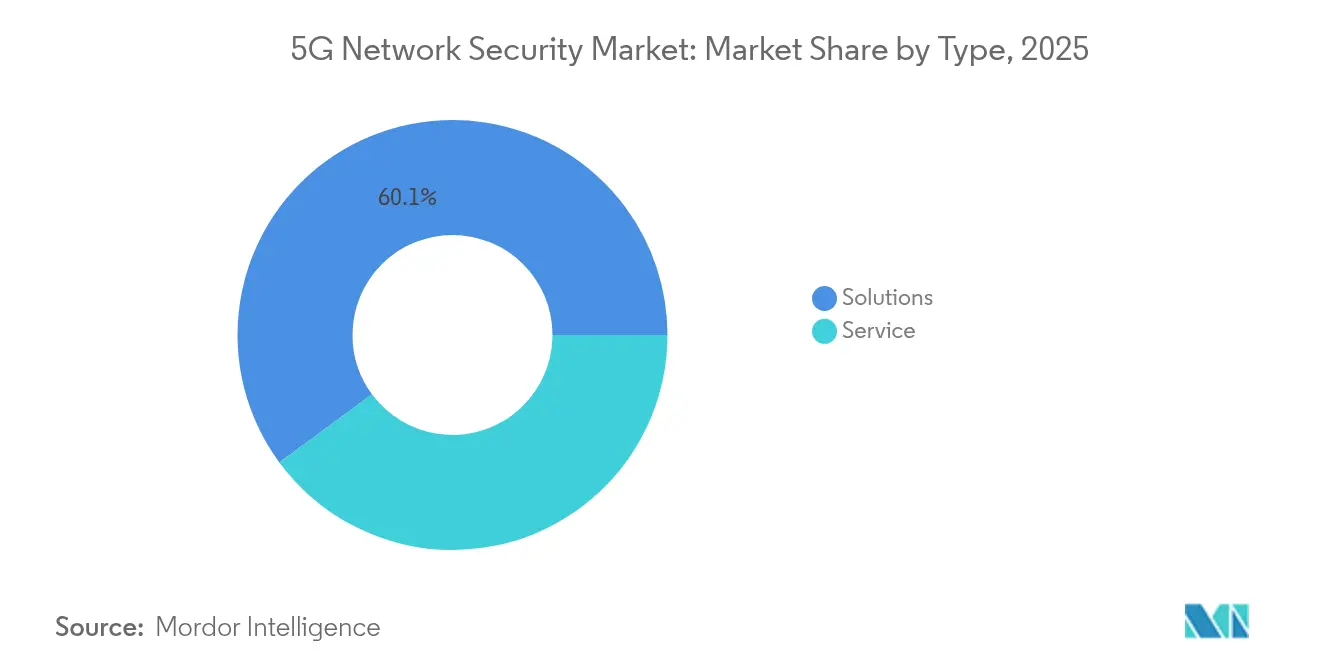

- By type, solutions held 60.10% of 5G network security market share in 2025, while services are on course for a 34.20% CAGR through 2031.

- By deployment, on-premises captured 52.30% of the 5G network security market size in 2025; cloud deployments are set to expand at 36.10% CAGR.

- By security layer, core security led with 38.95% revenue share in 2025; edge security is the fastest-growing layer at 37.85% CAGR.

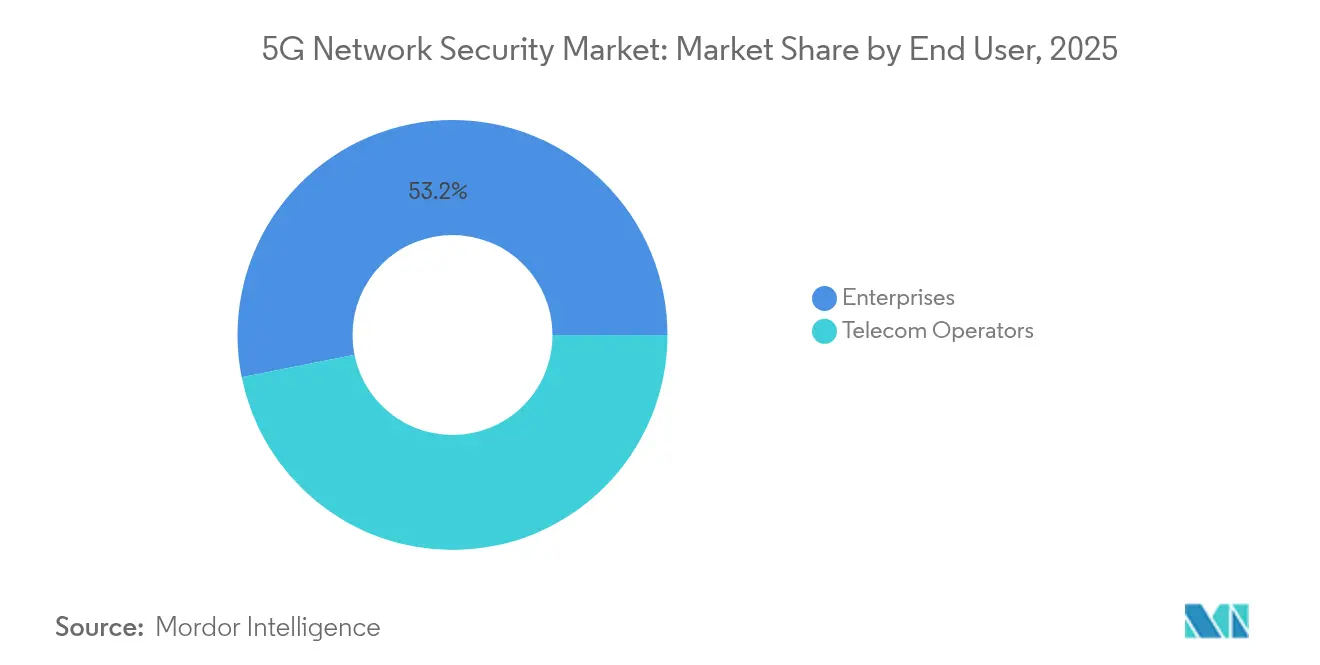

- By end user, telecom operators accounted for 46.85% of demand in 2025, but manufacturing is advancing at a leading 35.05% CAGR.

- By organization size, large enterprises commanded 68.20% share of the 5G network security market size in 2025, while SMEs grow at 34.60% CAGR.

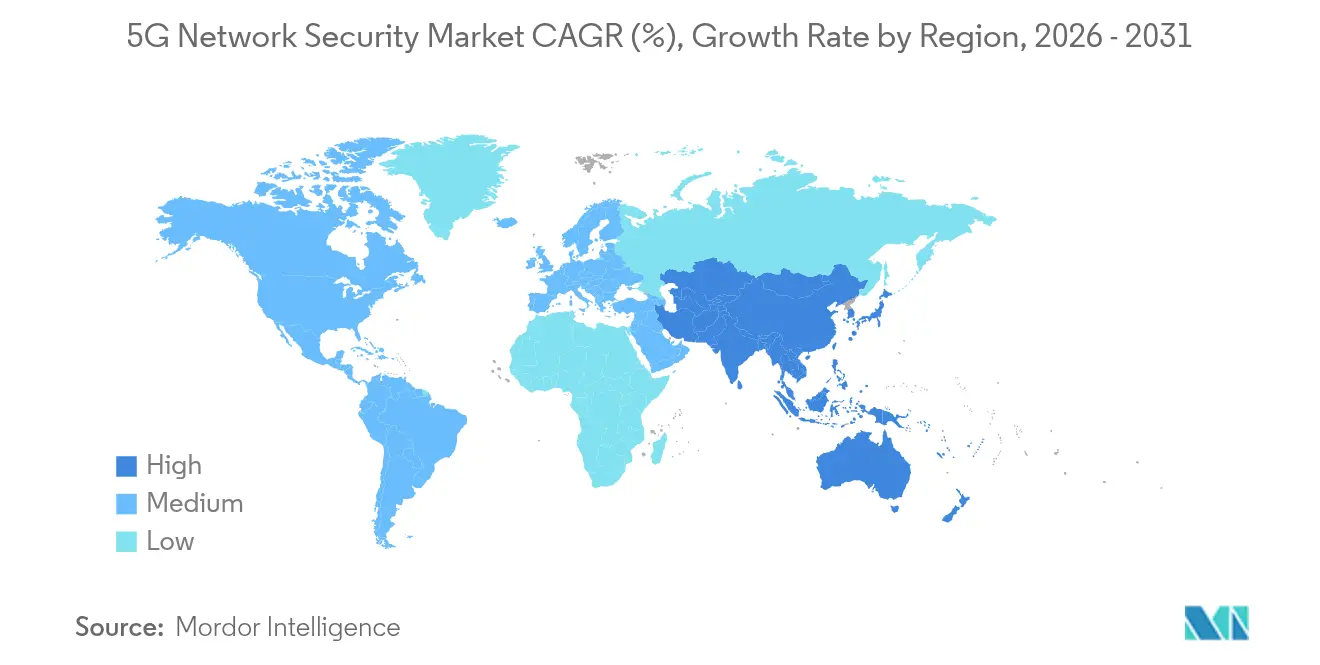

- By geography, North America led with 39.10% share in 2025; Asia-Pacific is forecast to rise at 36.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 5G Network Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G Stand-Alone (SA) Core Deployments | +8.2% | Global, early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Adoption of Network Slicing for Enterprise Use-Cases | +6.8% | North America and EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Regulatory Mandates on 5G Security | +5.4% | Global, strongest in North America and EU | Short term (≤ 2 years) |

| Growth of Edge Computing and MEC Infrastructure | +4.9% | Asia-Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| Rise in Private 5G Networks in Industrial Settings | +3.7% | Global, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Integration of AI/ML for Zero-Trust and Anomaly Detection | +2.6% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Stand-Alone (SA) Core Deployments

Standalone cores eliminate LTE anchors and rely on cloud-native network functions that communicate over exposed APIs. The 3GPP SA3 working group lists 127 discrete security requirements for SA, triple that of NSA, underscoring the complexity surge. Ericsson disclosed that 55% of its 2024 5G contracts specified SA-only architectures, signalling a rapid pivot to capabilities such as ultra-low latency and network slicing that heighten security stakes.[1]Ericsson, “Ericsson Mobility Report 2024,” ericsson.com Vulnerability research has highlighted Service Communication Proxy weaknesses that could allow unauthorized access, prompting urgent investment in signalling firewalls and API gateways.

Adoption of Network Slicing for Enterprise Use-Cases

Enterprises now request carrier-grade slices with bespoke policies, but isolated virtual networks create complex inter-slice trust challenges. Singtel’s national 5G+ rollout enforces 47 unique policies across live enterprise slices while stopping lateral movement between customers.[2]Singtel, “Singtel unleashes nationwide 5G + slicing for enterprises,” singtel.com T-Mobile’s security-slice service embeds Palo Alto Networks threat detection into slice orchestration to satisfy zero-trust requirements. These examples show why granular, slice-aware security orchestration is becoming table stakes for the 5G network security market.

Regulatory Mandates on 5G Security (3GPP, NIST, ETSI)

The EU’s NIS2 Directive compels operators to allot 9% of IT budgets to cybersecurity and to report 5G incidents within 24 hours, accelerating demand for compliant solutions.[3]European Union, “Directive (EU) 2022/2555 on measures for a high common level of cybersecurity,” eur-lex.europa.eu NIST’s 2024 framework adds 89 controls, including mandatory control-plane encryption and continuous slice monitoring. ETSI’s certification scheme forces third-party validation, further solidifying a compliance-driven runway for security vendors.

Growth of Edge Computing and MEC Infrastructure

MEC moves workloads closer to users, lowering latency while multiplying entry points for attackers. Lanner Electronics notes that edge deployments require 73% more controls than centralized equivalents, ranging from physical tamper protection to local AI-driven threat response. Industrial IoT use cases must also meet stringent uptime goals, demanding lightweight yet autonomous security agents that fit constrained power budgets. This need positions edge-aware platforms at the forefront of 5G network security market evolution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Security Standards Across Vendors | -4.3% | Global, strongest impact in multi-vendor environments | Medium term (2-4 years) |

| High Energy Consumption of 5G Security Functions | -2.8% | Global, notable in energy-constrained regions | Long term (≥ 4 years) |

| Shortage of 5G-Skilled Cyber-Security Workforce | -3.1% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Slow Monetization Outlook for 5G Security Investments | -2.4% | Global, strongest impact in developing markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Security Standards Across Vendors

Multi-vendor deployments represent 78% of enterprise rollouts, yet each supplier implements proprietary security controls and management interfaces. Integration projects reveal an average of 23 custom tie-ins to achieve unified policy enforcement, elevating cost and exposing integration-layer vulnerabilities. Enterprises therefore seek vendor-neutral orchestration, but standards convergence remains slow, restraining the 5G network security market.

High Energy Consumption of 5G Security Functions

Inline encryption, deep-packet inspection, and AI inference engines raise power draw significantly versus 4G counterparts. Operators in regions with high energy costs confront difficult trade-offs between performance and efficiency. While silicon advances promise incremental gains, the lack of immediate low-power options tempers adoption curves for some high-density scenarios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Accelerate Despite Solutions Dominance

The 5G network security market size for solutions stood at USD 5.25 billion in 2025, equal to a 60.10% share, anchored by mandatory gateways, signaling firewalls, and DDoS mitigation. Vendors bundle hardware acceleration with software orchestration to meet deterministic latency targets. Professional and managed services, though smaller today, are scaling at 34.20% CAGR as operators and enterprises outsource complex integration and 24/7 response. This surge reflects a recognition that few firms can recruit or retain the niche talent needed to secure distributed, slice-aware networks.

Rising cyber-insurance prerequisites and board-level scrutiny amplify interest in managed detection and response. Providers leverage economies of scale and global SOC footprints to deliver rapid remediation that an individual enterprise would struggle to replicate. As a result, services revenues are projected to close much of the gap with solutions by 2031, reinforcing a hybrid buying pattern across the 5G network security market.

By Deployment: Cloud Gains Momentum Against On-Premises Legacy

On-premises environments preserved 52.30% of the 5G network security market share in 2025 because telecom operators and highly regulated verticals prioritize data sovereignty. Local control allows fine-grained latency and determinism, which are critical for public-safety slices and mission-critical OT. Even so, cloud-native models are climbing at 36.10% CAGR as enterprises value elastic scaling, pay-as-you-grow pricing, and automatic updates. Cloud control planes increasingly deliver real-time threat intel that propagates policies across distributed cores and edges within seconds.

Hybrid topologies are emerging as the default operating model. Operators host subscriber databases and lawful intercept nodes on-premises while shifting analytics and AI-based anomaly detection to cloud regions compliant with residency rules. This arrangement balances regulatory obligations with the agility benefits that hyperscalers provide, ensuring the 5G network security market progresses toward software-defined security.

By Security Layer: Edge Security Emerges as Growth Leader

Core-layer defenses retained 38.95% of revenue in 2025 because standalone architectures require robust signaling protection across service-based interfaces. Inline API gateways, SEPP firewalls, and unified data-plane encryption remain foundational. However, MEC proliferation propels edge security at a 37.85% CAGR as enterprises spin up localized compute to meet sub-10 ms response targets.

At the edge, smaller form-factor appliances integrate zero-trust network access, trusted-platform modules, and AI-powered intrusion prevention. They also run in constrained power envelopes, satisfying green-IT goals. Vendors, therefore, treat edge as the strategic foothold for platform stickiness, bundling lifecycle management across thousands of micro-sites.

By End User: Manufacturing Drives Enterprise Adoption

Telecom operators commanded 46.85% of procurement in 2025, reflecting regulatory accountability for public networks. Their spending priorities range from SEPP compliance at interconnect borders to slice lifecycle management. Manufacturing plants, meanwhile, are scaling fastest at 35.05% CAGR. Tesla’s Berlin Gigafactory relies on encrypted 5G private networks to orchestrate autonomous material handling and to guard trade secrets.

Factory owners prioritize ultra-reliable, low-latency communication that supports machine vision and predictive maintenance. They demand deterministic security enforcement spanning OT protocols and IT estate. Healthcare, BFSI, retail, and government follow with tailored compliance drivers such as HIPAA or national security. Each vertical adds incremental demand diversity, widening the addressable scope of the 5G network security industry.

By Organization Size: SMEs Embrace Cloud-Native Security

Large enterprises controlled 68.20% of spending in 2025, typically operating multi-site private 5G and integrating with SIEM and SOAR stacks. Their procurement cycles favor multi-year contracts for end-to-end suites that cover core, edge, and slice orchestration. Yet SMEs represent the highest unit-growth cohort at 34.60% CAGR. Consumption-based SaaS lowers entry barriers, enabling mid-market firms to gain capabilities such as behavioral analytics that were once reserved for Fortune 500 budgets.

Marketplace-based delivery and automated configuration wizards reduce deployment timelines from months to days. As hyperscalers embed blueprint templates for manufacturing, retail, or smart-building use cases, SME traction will intensify, ensuring the 5G network security market continues to democratize advanced protection.

Geography Analysis

North America held 39.10% of 2025 revenue thanks to early standalone deployments and stringent FCC oversight that requires operators to document detection and response capabilities before spectrum allocation. Enterprises in manufacturing and finance favor private 5G secured by NIST guidelines, leveraging partnerships between carriers and cybersecurity vendors for unified SLA enforcement. Strong venture capital funding fuels continuous innovation, and federal grants encourage zero-trust adoption across critical infrastructure.

Asia-Pacific is expanding fastest at 36.25% CAGR. China’s USD 150 billion 5G build-out specifies security audits for every core node and insists on hardware root-of-trust. Japan and South Korea advance private campus networks in automotive and shipbuilding, embedding slice isolation from day one. Government-industry task forces disseminate best practices region-wide, accelerating maturity. As multi-access edge computing scales to serve gaming and logistics, localized threat detection strengthens demand for adaptive security fabrics.

Competitive Landscape

The 5G network security market shows moderate fragmentation. Ericsson, Nokia, and Huawei leverage deep RAN and core knowledge, embedding security into network functions. Palo Alto Networks, Fortinet, and Check Point focus on advanced threat analytics, offering vendor-agnostic firewalls that slot into multi-vendor cores. Collaboration outweighs acquisition: Ericsson pairs with Palo Alto Networks for integrated slice security, while Nokia integrates Fortinet’s threat intel to close visibility gaps across edge nodes.

AI-centric challengers such as Mavenir and AdaptiveMobile Security tackle signalling fraud and slice isolation with machine-learning models trained on 5G telemetry. They compete on time-to-detect metrics measured in milliseconds. Hyperscalers bundle security orchestration into network-as-a-service offerings, courting SMEs that want turnkey solutions. Differentiation increasingly rests on zero-touch policy provisioning and cross-layer correlation rather than hardware specs.

5G Network Security Industry Leaders

Ericsson

Huawei

Nokia

Cisco Systems

Palo Alto Networks

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Indian Railways (Bhopal Division) and Thales Group rolled out “Next-Gen NTES” across seven stations, deploying an AI-powered passenger information system aligned with Digital India objectives.

- January 2025: Cubic Transportation Systems delayed the Clipper 2.0 upgrade, pushing mobile and contactless fare integration to August 2025 and highlighting hurdles in real-time transit data delivery.

- October 2024: Wabtec and Siemens Mobility agreed to equip Munich S-Bahn trains with real-time information displays under a multi-million-euro deal.

- April 2024: Alstom SA and Tag i Bergslagen signed an MoU to develop enhanced passenger information technologies over two years at Alstom’s Stockholm Innovation Station.

Global 5G Network Security Market Report Scope

5G security is an area of wireless network security focused on fifth-generation (5G) wireless networks. 5G security technologies help protect 5G infrastructure and 5G-enabled devices against data loss, cyberattacks, hackers, malware, and other threats.

The 5G network security market is segmented by type (solutions, services), by deployment (cloud, on-premises), by security type (ran security, core security) by end-users (BFSI, IT and telecom, healthcare, retail and ecommerce, manufacturing, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions | Network Security Gateway | |

| Next-Gen Firewall and IPS | ||

| DDoS Protection | ||

| Signalling and Diameter Security | ||

| Others | ||

| Services | Professional Services | Integration and Deployment |

| Consulting | ||

| Support and Maintenance | ||

| Managed Security Services | ||

| On-Premises |

| Cloud |

| Hybrid |

| RAN Security |

| Transport Security |

| Core Security |

| Edge Security |

| Application Security |

| Telecom Operators | |

| Enterprises | BFSI |

| Healthcare | |

| Manufacturing | |

| Retail and E-commerce | |

| Government and Public Safety | |

| Media and Entertainment | |

| Others |

| Large Enterprises |

| Small and Mid-Sized Enterprises (SMEs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Type | Solutions | Network Security Gateway | |

| Next-Gen Firewall and IPS | |||

| DDoS Protection | |||

| Signalling and Diameter Security | |||

| Others | |||

| Services | Professional Services | Integration and Deployment | |

| Consulting | |||

| Support and Maintenance | |||

| Managed Security Services | |||

| By Deployment | On-Premises | ||

| Cloud | |||

| Hybrid | |||

| By Security Layer | RAN Security | ||

| Transport Security | |||

| Core Security | |||

| Edge Security | |||

| Application Security | |||

| By End User | Telecom Operators | ||

| Enterprises | BFSI | ||

| Healthcare | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Government and Public Safety | |||

| Media and Entertainment | |||

| Others | |||

| By Organization Size | Large Enterprises | ||

| Small and Mid-Sized Enterprises (SMEs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the 5G network security market?

The 5G network security market size is USD 11.37 billion in 2026.

How fast is the 5G network security market expected to grow?

It is forecast to expand at a 30.15% CAGR, reaching USD 42.46 billion by 2031.

Which segment is growing the quickest?

Edge-layer security is advancing the fastest at 37.85% CAGR as MEC deployments multiply.

Why are managed security services gaining traction?

Enterprises lack in-house 5G expertise, so they turn to managed providers that offer 24/7 monitoring and compliance reporting.

Page last updated on: