Yoga Mat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 16.24 Billion |

| Market Size (2031) | USD 20.45 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

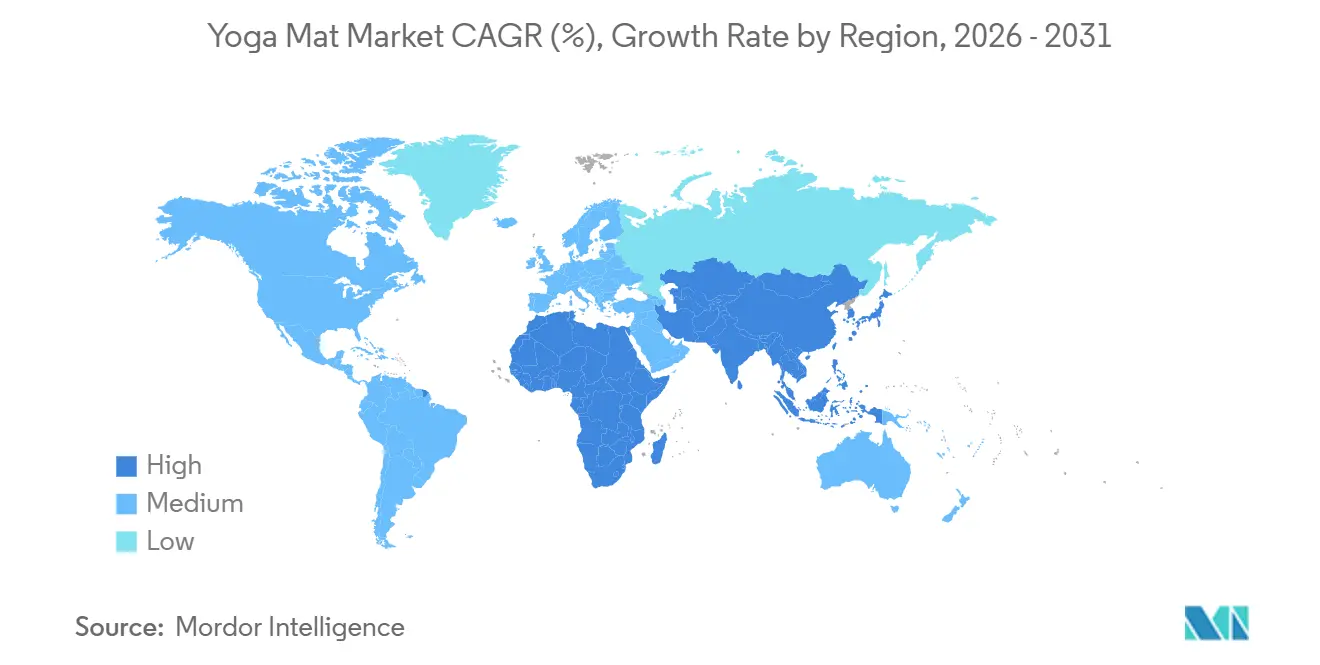

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Yoga Mat Market Analysis by Mordor Intelligence

The yoga mat market size was valued at USD 15.53 billion in 2025 and is estimated to grow from USD 16.24 billion in 2026 to reach USD 20.45 billion by 2031, at a CAGR of 4.72% during the forecast period 2026 to 2031. The yoga mat market continues to demonstrate stable growth, supported by sustained participation in yoga and increasing replacement cycles as consumers upgrade from entry-level products to higher-performance alternatives. Purchasing decisions are increasingly driven by product attributes such as grip, durability, material certifications, and supply chain transparency rather than price alone, contributing to stronger demand for premium and eco-friendly offerings. While conventional mats continue to account for the majority of volume sales, premium and organic segments are gaining market share and driving value growth. Regionally, North America is expected to maintain its position as the largest market in 2025, supported by established wellness spending patterns, while Asia-Pacific is projected to record the highest growth rate through 2031, driven by increasing urbanization, rising health awareness, and broader adoption of wellness practices. Together, these factors underscore the market's transition toward higher-value products and diversified demand channels.

Key Report Takeaways

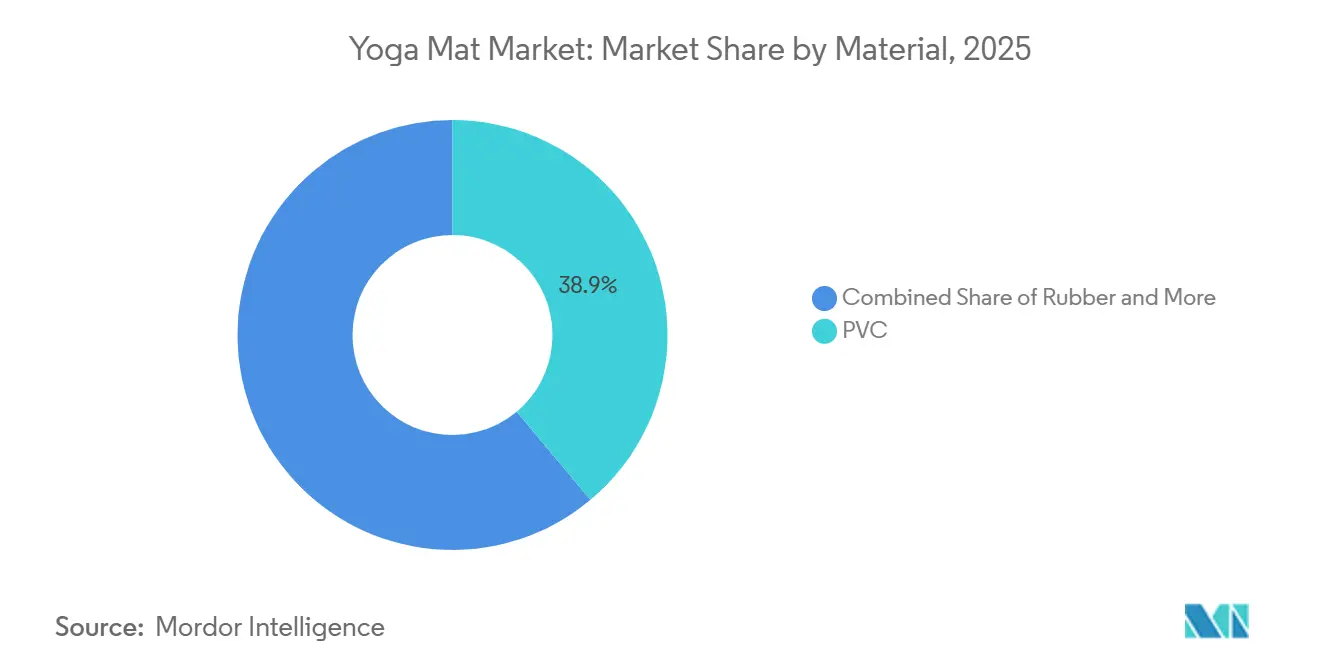

- By material type, PVC led with 38.9% revenue share in 2025, while rubber recorded the highest projected CAGR at 4.80% through 2031.

- By category, conventional mats held a 58.45% share in 2025, while organic or natural mats are forecast to expand at a 6.84% CAGR through 2031.

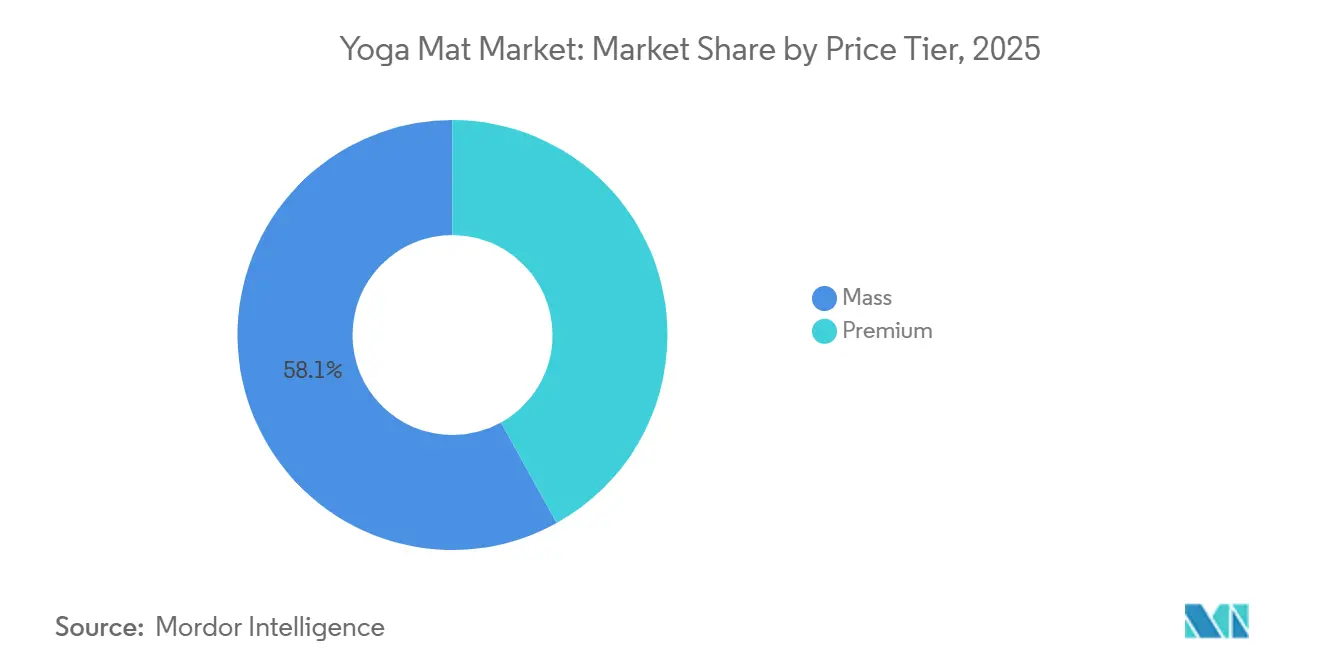

- By price tier, the mass segment accounted for a 58.02% share in 2025, while the premium tier is advancing at a 7.01% CAGR through 2031.

- By end use, individual buyers represented 68.14% of demand in 2025, while commercial buyers are projected to grow at a 6.50% CAGR through 2031.

- By geography, North America held a 34.90% share in 2025, while Asia-Pacific is expected to expand at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Yoga Mat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Yoga And Wellness Participation | +1.2% | Global, with concentration in North America, Western Europe, and India | Long term (≥ 4 years) |

| Expanding Home Fitness And Exercise Trends | +0.8% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Increasing Demand For Eco-Friendly Yoga Products | +0.7% | Western Europe, North America, Japan, Australia | Medium term (2-4 years) |

| Product Innovation In Materials And Performance | +0.6% | Global, led by APAC manufacturing and North America and Europe consumption | Long term (≥ 4 years) |

| Growing Corporate Wellness And Mindfulness Fitness | +0.4% | North America and Europe, with emerging adoption in APAC | Medium term (2-4 years) |

| Strong Influence Of Social Media Fitness | +0.3% | Global, strongest in India, Southeast Asia, and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Yoga And Wellness Participation

The continued expansion of yoga participation beyond traditionally mature markets is strengthening the long-term demand foundation of the yoga mat market. With more than 300 million yoga practitioners worldwide in 2025 and approximately 38.4 million practitioners in the United States, the market benefits from a substantial and growing installed user base that supports both new product adoption and recurring replacement demand [1]Source: Yoga Alliance, “Yoga in the World,” Yoga Alliance, yogaalliance.org. This expanding consumer pool contributes not only to first-time purchases but also to higher replacement rates as users upgrade from entry-level mats, replace worn products, and adopt specialized mats tailored to different practice styles and fitness routines. These dynamics create a balanced demand structure across multiple price segments and help sustain market resilience during periods of economic uncertainty. As yoga remains a relatively accessible and low-cost wellness activity, the requirement for a dedicated mat as a core piece of equipment continues to provide a stable and recurring source of demand for manufacturers and retailers.

Increasing Demand For Eco-Friendly Yoga Products

Sustainability has evolved from a niche consideration into a key purchasing criterion, significantly influencing product development, sourcing strategies, and brand positioning across the yoga mat market. Consumers are increasingly evaluating products based on material provenance, chemical safety standards, renewable content, and third-party certifications, particularly within premium segments where transparency and brand credibility play an important role in purchase decisions. The launch of innovative products such as the Mushroom Mat by JadeYoga in 2025 highlights how manufacturers are integrating sustainability directly into product differentiation strategies rather than treating it solely as a marketing claim. This trend is accelerating demand for eco-friendly materials including natural rubber, jute, cork, and other renewable alternatives, while simultaneously increasing scrutiny of conventional materials with respect to safety, environmental impact, and product longevity. As a result, sustainability is becoming a competitive factor across the value chain, influencing both consumer preference and brand positioning. The growing emphasis on environmentally responsible materials, cleaner manufacturing processes, and certification compliance is also supporting premiumization within the market, enabling higher average selling prices and strengthening value growth in eco-conscious product categories.

Product Innovation In Materials And Performance

Material innovation is expanding the addressable market for yoga mats by positioning them as multi-functional fitness accessories rather than products used exclusively for traditional yoga practice. Consumers increasingly demand enhanced cushioning, superior grip and stability, ease of maintenance, and long-term durability capable of supporting a wider range of physical activities, including strength training, functional fitness, and high-intensity workouts. This shift is reflected in Manduka’s April 2026 introduction of the P/ROX Hybrid Fitness Mat, which was designed for a broader range of fitness applications, including strength training and high-impact exercises, rather than being limited to conventional yoga use. Similarly, brands are increasingly integrating recycled and sustainable materials into high-performance product designs, indicating that environmental responsibility and functional performance are becoming complementary rather than competing objectives. This convergence of advanced materials, enhanced durability, and multi-purpose usability is supporting ongoing premiumization across the yoga mat market. By delivering greater versatility and longer product lifecycles, manufacturers are creating opportunities to capture higher-value demand from both individual consumers and institutional buyers.

Growing Corporate Wellness And Mindfulness Fitness

Corporate wellness programs are emerging as an increasingly important demand driver for the yoga mat market as organizations expand investments in employee health, wellness, and mindfulness initiatives. The growing integration of yoga sessions, stress-management programs, and workplace fitness activities into corporate wellness strategies is creating a steady source of institutional demand for yoga-related equipment. This channel is particularly significant because purchasing decisions are typically based on recurring procurement cycles, program scalability, and long-term supplier relationships rather than individual consumer spending patterns. As corporate wellness programs become more established, equipment purchases tend to be more predictable and repeatable, providing manufacturers with a stable revenue stream. Commercial buyers also evaluate products using criteria that differ from those of individual consumers, with greater emphasis on durability, ease of maintenance, hygiene standards, storage efficiency, and professional aesthetics. These requirements are encouraging manufacturers to develop products specifically designed for high-frequency, shared-use environments. As institutional adoption continues to expand, the yoga mat market is becoming increasingly diversified, reducing reliance on discretionary consumer spending and benefiting from structured wellness budgets across corporate organizations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Price Competition From Low-Cost Manufacturers | -0.6% | Global, most acute in APAC and Latin America | Short term (≤ 2 years) |

| Limited Product Differentiation Across Market Segments | -0.4% | Global, most acute in mass and mid-tier segments | Medium term (2-4 years) |

| Fluctuating Demand From Seasonal Fitness Trends | -0.3% | North America and Europe | Short term (≤ 2 years) |

| Availability Of Substitute Fitness Equipment | -0.4% | North America, Europe, and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense Price Competition From Low-Cost Manufacturers

The yoga mat market continues to face significant pricing pressure due to intense competition within the entry-level and mass-market segments, where products are often differentiated primarily by price and distribution reach. The abundance of low-cost alternatives creates a highly competitive environment that can limit pricing power across the category and intensify margin pressures for manufacturers. Chinese manufacturers benefit from integrated supply chains, efficient export infrastructure, and large-scale production capabilities, enabling cost-efficient manufacturing and strong price competitiveness in global markets [2]China National Development and Reform Commission / Government of China. "China Views Sports Industry as New Growth Driver in Next Five Years. This challenge is particularly pronounced for mid-tier brands, which often struggle to compete effectively against budget-focused suppliers while lacking the brand equity, performance differentiation, or sustainability credentials required to command premium pricing. As basic yoga mats are increasingly perceived as commoditized products, competitive dynamics shift toward price-based purchasing decisions, reducing profitability and limiting the resources available for product innovation, marketing, and brand development. In response, many manufacturers are expanding direct-to-consumer (DTC) sales channels to improve margin retention and strengthen customer relationships. However, while DTC strategies can enhance gross margins, they also increase exposure to customer acquisition costs, digital marketing expenses, and customer retention challenges. As a result, profitability becomes increasingly dependent on repeat purchases, brand loyalty, and lifetime customer value.

Availability of Substitute Fitness Equipment

The yoga mat market faces competitive pressure from a range of adjacent fitness and wellness products that serve similar functional purposes within home exercise environments. Products such as resistance bands, foam rollers, balance trainers, and multi-purpose exercise mats can address overlapping use cases, including stretching, bodyweight workouts, mobility training, and recovery activities. As a result, consumers often evaluate these alternatives within the same discretionary fitness spending budget. The risk of substitution is particularly evident among casual fitness participants, who tend to prioritize versatility and value when selecting exercise equipment. Within the mass-market segment, multi-purpose floor mats can attract demand by offering broader functionality across various workout formats, even if they do not provide the specialized performance characteristics required for dedicated yoga practice. However, substitution pressures are less pronounced in premium segments, where purchasing decisions are increasingly influenced by differentiated product attributes such as superior grip performance, advanced material quality, durability, comfort, and sustainability certifications. These features create a stronger value proposition that is more difficult for generic fitness products to replicate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Rubber Gains As Certification And Grip Matter More

PVC accounted for 38.9% of total segment revenue in 2025, maintaining its position as the leading material category due to its durability, cost efficiency, and widespread availability across mass retail and e-commerce channels. However, rubber-based mats are projected to record the fastest growth rate, with a CAGR of 4.8% through 2031, reflecting increasing consumer preference for premium products that offer superior grip, cushioning, durability, and environmental credentials.

The growing adoption of rubber materials underscores a broader premiumization trend across the yoga mat market, where purchasing decisions are increasingly influenced by performance characteristics and sustainability considerations rather than price alone. Meanwhile, thermoplastic elastomer (TPE) continues to occupy a strategic middle-market position by providing a lightweight, perceived eco-friendlier alternative to conventional PVC while remaining more cost-effective than natural rubber-based products. Material selection has become an increasingly important competitive differentiator, extending beyond product feel and weight to influence brand perception, certification eligibility, retailer acceptance, regulatory compliance, and end-user positioning.

By Category: Conventional Volume Meets Organic and Natural Upgrade Demand

Conventional yoga mats accounted for 58.5% of total market share in 2025, maintaining a dominant position due to their affordability, broad retail availability, and suitability for a wide range of end users, including first-time practitioners, fitness centers, and yoga studios. Their accessibility and cost-effectiveness continue to support strong demand across both consumer and commercial channels.

In contrast, the organic and natural yoga mat segment is projected to expand at a CAGR of 6.8% through 2031, making it one of the fastest-growing categories within the broader market. Growth in this segment is being driven by increasing consumer awareness of material safety, environmental sustainability, responsible sourcing practices, and overall product transparency. As wellness-oriented consumers become more selective about the products they use, demand is shifting toward mats that offer both functional performance and stronger sustainability credentials. The category is also benefiting from ongoing product innovation that enhances the appeal of natural materials without compromising performance standards. New product developments have demonstrated that sustainability-focused materials can deliver competitive levels of grip, durability, and comfort while supporting environmentally responsible brand positioning.

By Price Tier: Premium Growth Outruns Mass Volume

The pricing structure of the yoga mat market continues to be led by the mass-market segment, which accounted for 58% of total revenue in 2025. This segment maintains its dominant position due to its affordability, broad accessibility, and strong appeal among first-time users, occasional practitioners, and value-conscious consumers seeking essential functionality at a competitive price point. Mass-market products also benefit from extensive distribution across retail, e-commerce, fitness, and institutional channels, supporting high sales volumes.

However, the premium segment is projected to record a CAGR of 7.0% through 2031, outpacing the overall market and highlighting an ongoing shift toward higher-value product offerings. Growth in this segment is being driven by increasingly experienced practitioners who prioritize product performance, durability, comfort, and sustainability over initial purchase price. Key purchasing factors include enhanced grip, extended product lifespan, advanced cushioning, certified materials, and multifunctional designs that support a broader range of fitness and wellness activities.

By End Use: Commercial Demand Adds Repeat Purchase Visibility

End-user demand within the yoga mat market remains predominantly consumer-driven, with individual buyers accounting for 68.1% of total demand in 2025. This segment continues to form the foundation of market growth, supported by increasing participation in yoga, expanding home-based fitness activities, personal wellness routines, and ongoing adoption among new practitioners. Individual consumers represent the primary source of volume demand, with purchasing decisions influenced by factors such as comfort, performance, durability, price, and sustainability preferences.

The commercial segment is projected to expand at a CAGR of 6.5% through 2031, outpacing several traditional end-user categories and highlighting the growing role of institutional demand within the market. Growth is being driven by increasing investments in wellness infrastructure across yoga studios, fitness centers, hotels, resorts, healthcare facilities, and corporate wellness programs. The expansion of workplace wellness initiatives is further strengthening this trend, as organizations increasingly incorporate yoga, mindfulness, and fitness programs into broader employee health strategies. The demonstrated business value of corporate wellness partnerships is encouraging greater investment in structured wellness programming, which in turn supports recurring demand for yoga-related equipment and accessories.

Geography Analysis

North America accounted for 34.9% of global market revenue in 2025, maintaining its position as the largest regional market. The region benefits from high consumer spending on health and wellness, a well-established specialty retail ecosystem, strong e-commerce penetration, and a large base of active yoga practitioners. These factors support robust demand for both replacement purchases and premium product upgrades. The United States remains the primary growth engine within the region, driven by strong consumer preference for branded, performance-oriented, and certified products, while Canada and Mexico contribute additional demand across both consumer and institutional channels.

Europe represents one of the highest-value regional markets, characterized by strong consumer emphasis on product quality, material transparency, sustainability, and regulatory compliance. Markets such as Germany, the United Kingdom, France, the Netherlands, Italy, Spain, and the Nordic countries demonstrate heightened demand for products with verified environmental and safety credentials. This environment creates favorable conditions for materials such as natural rubber, TPE, cork, and other sustainable alternatives that align with increasingly stringent consumer and retailer expectations. As a result, Europe continues to support premium pricing strategies and offers stronger competitive positioning for brands that can demonstrate product differentiation through quality, certification, and responsible sourcing practices.

Asia-Pacific is projected to be the fastest-growing regional market, with a CAGR of 8.1% through 2031. Growth is being driven by increasing urbanization, rising health and wellness awareness, expanding middle-class populations, improving retail accessibility, and supportive initiatives promoting physical activity across several major economies. The region also benefits from a well-developed manufacturing ecosystem that supports both domestic consumption and global supply chains. China remains a critical market due to its combination of large-scale production capabilities and expanding wellness consumer base, while India serves as both a high-growth consumption market and an important source of natural rubber and fiber-based raw materials. Meanwhile, Japan and South Korea continue to drive demand for premium, performance-focused products, and Southeast Asian markets are gaining importance as both consumer markets and manufacturing hubs.

Although South America and the Middle East & Africa currently represent a smaller share of global demand, both regions offer attractive long-term growth opportunities. Countries including Brazil, Argentina, the United Arab Emirates, Saudi Arabia, and South Africa are experiencing increasing wellness adoption, expanding fitness infrastructure, and growing hospitality investments. These trends are supporting the development of niche premium segments and creating opportunities for market participants seeking expansion beyond established regional markets.

Competitive Landscape

The yoga mat market remains highly fragmented, with no single manufacturer holding sufficient market share to exert significant pricing influence across regions, product categories, or end-user segments. Competitive dynamics are shaped by a diverse mix of premium, mid-tier, and value-oriented brands that differentiate through product performance, material innovation, sustainability credentials, distribution reach, and brand positioning rather than scale alone.

Premium market participants compete primarily on quality, performance, sustainability, and community engagement. These brands focus on delivering differentiated value through advanced materials, enhanced durability, certified sourcing practices, and strong brand affinity among dedicated practitioners. In contrast, volume-oriented manufacturers target entry-level and mid-market consumers through broad retail distribution, accessible pricing strategies, and functional product offerings designed to maximize market reach. This competitive structure keeps the category highly dynamic while reinforcing the importance of brand differentiation, product innovation, and channel execution as key drivers of market success.

The commercial segment represents a particularly attractive growth opportunity, as many existing product portfolios continue to focus primarily on individual consumers rather than the specific requirements of shared-use environments such as fitness centers, yoga studios, hotels, healthcare facilities, and corporate wellness programs. Products optimized for durability, hygiene, maintenance efficiency, and institutional purchasing requirements are likely to gain increasing relevance as commercial demand expands.

Yoga Mat Industry Leaders

-

Lululemon Athletica Inc.

-

Manduka Europe

-

Gaiam

-

JadeYoga

-

Decathlon Sports

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: JadeYoga launched its licensed Peanuts collection featuring FSC-certified, OEKO-TEX certified natural rubber mats designed around Snoopy, Linus, and Charlie Brown characters. The collection targets casual and lifestyle-oriented practitioners, expanding JadeYoga's addressable demographic beyond serious practitioners.

- October 2025: JadeYoga introduced the Mushroom Mat™, combining natural rubber with repurposed mushroom material, manufactured entirely on renewable energy, and certified under OEKO-TEX 100. The product is JadeYoga's most technologically differentiated sustainability offering to date and continues the brand's "Buy a Mat, Plant a Tree" program

- November 2024: Manduka partnered with SuperCircle to launch the yoga industry's first end-of-life recycling program, allowing consumers to return yoga mats of any brand and condition for responsible recycling rather than landfill disposal. Participants receive a prepaid shipping label and a 20% discount on a future Manduka purchase, supporting the company's circular economy and sustainability strategy.

Global Yoga Mat Market Report Scope

A yoga mat is a cushioned, portable exercise surface designed to provide grip, stability, and comfort during yoga practice and related floor-based fitness activities. The Yoga Mat Market Report is segmented by material type, including rubber, cotton, PVC, TPE, EVA, and others. The market is segmented by category, including conventional and natural or organic mats. Based on end use, the market is divided into individual consumers and commercial consumers. The study examines the yoga mat in both emerging and established markets worldwide, encompassing North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market forecasts are provided in terms of value in USD.

| Rubber |

| Cotton |

| Polyvinyl Chloride (PVC) |

| Thermoplastic Elastomer (TPE) |

| Others (Ethylene Vinyl Acetate/ Cork/Jute) |

| Conventional |

| Organic/Natural |

| Mass |

| Premium |

| Individual |

| Commercial |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Norway | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Material Type | Rubber | |

| Cotton | ||

| Polyvinyl Chloride (PVC) | ||

| Thermoplastic Elastomer (TPE) | ||

| Others (Ethylene Vinyl Acetate/ Cork/Jute) | ||

| By Category | Conventional | |

| Organic/Natural | ||

| By Price Tier | Mass | |

| Premium | ||

| By End Use | Individual | |

| Commercial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Sweden | ||

| Norway | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected size of the yoga mat market by 2031?

The yoga mat market is forecast to reach USD 20.45 billion by 2031 from USD 16.24 billion in 2026, reflecting a 4.72% CAGR over the forecast period.

Which region leads global demand for yoga mats?

North America led with 34.9% share in 2025 because of strong wellness spending, mature retail access, and a large practitioner base.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow at 8.1% CAGR through 2031, supported by rising urban participation, manufacturing strength, and expanding wellness adoption.

Which product category is expanding the fastest?

The premium price tier is the fastest-growing segment at 7.01% CAGR, while organic and natural mats are also growing quickly at 6.84% CAGR as buyers seek performance and cleaner materials.

Page last updated on: