Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

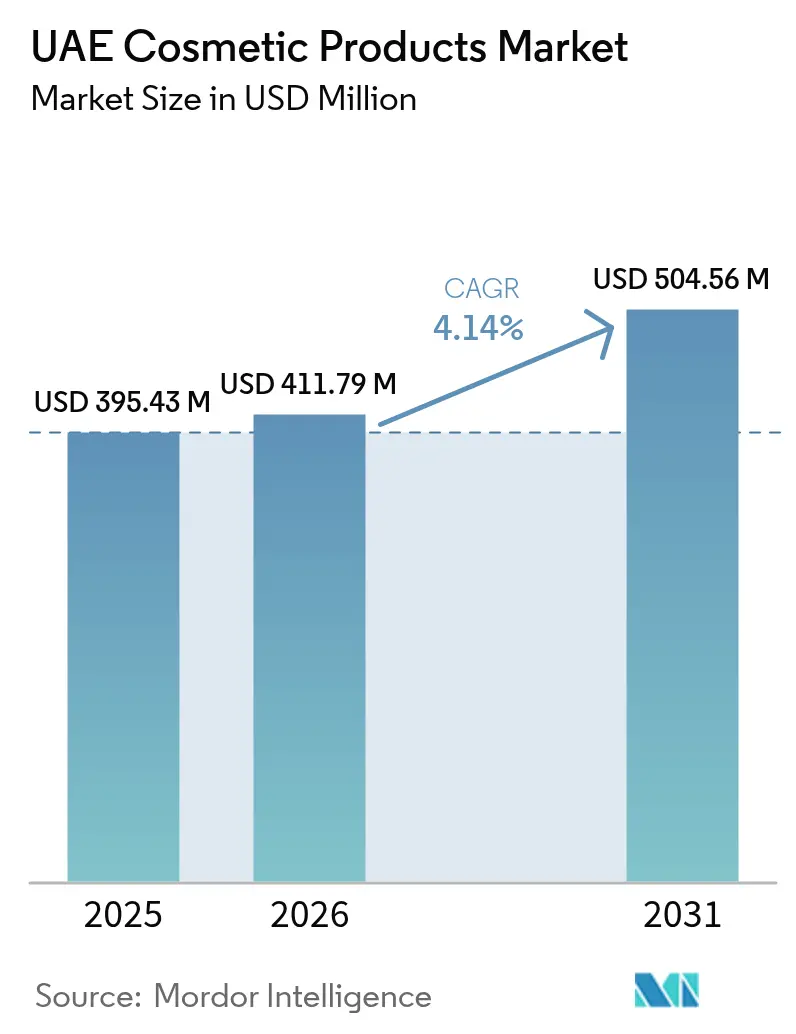

| Base Year Market Size (2025) | USD 395.43 Million |

| Market Size (2026) | USD 411.79 Million |

| Market Size (2031) | USD 504.56 Million |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Cosmetic Products Market Analysis by Mordor Intelligence

The UAE cosmetic products market size is expected to grow from USD 395.43 million in 2025 to USD 411.79 million in 2026 and is forecast to reach USD 504.56 million by 2031 at 4.14% CAGR over 2026-2031. This growth is driven by multiple factors, including the country's position as a tourism hub and evolving consumer preferences. The market expansion is particularly notable in the color cosmetics segment, where increasing appearance consciousness among younger generations, especially millennials, plays a significant role. These consumers, influenced by social media and celebrity beauty trends, show a willingness to invest in premium products. The market also benefits from consumers' focus on addressing age-related skin concerns and their pursuit of improved lifestyle quality. Additionally, the shift toward online shopping has enhanced product accessibility and demand through digital channels, while attractive packaging and evolving fashion trends continue to support industry growth. The UAE's strategic location and robust retail infrastructure further strengthen its position as a key market for international cosmetic brands. The presence of numerous luxury shopping destinations and beauty-focused retail outlets across major cities like Dubai and Abu Dhabi contributes significantly to market development. Moreover, the increasing adoption of natural and organic cosmetic products reflects the growing consumer awareness about ingredient safety and environmental sustainability.

Key Report Takeaways

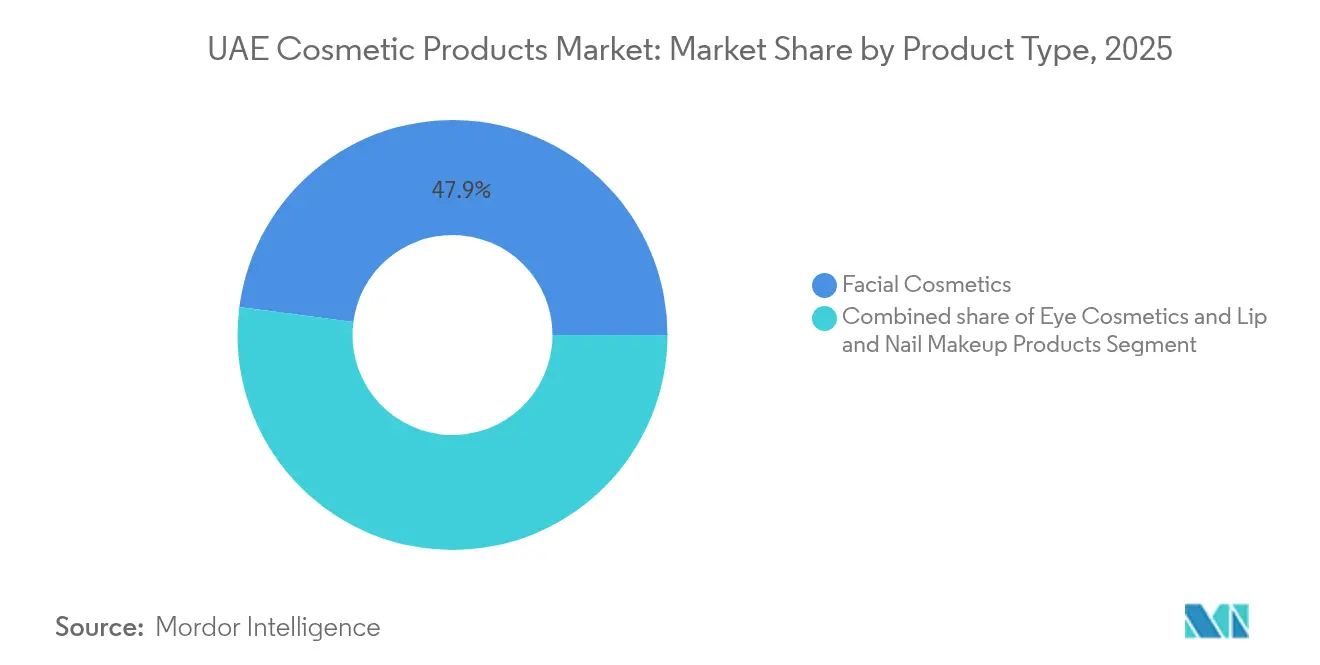

- By product type, facial cosmetics captured 47.92% of the UAE cosmetic products market share in 2025, whereas lip and nail products are poised to clock a 6.05% CAGR through 2031.

- By category, mass-market lines held 67.65% of the UAE cosmetic products market size in 2025, while premium ranges are forecast to climb at a 7.1% CAGR to 2031.

- By ingredient type, conventional/synthetic formulations commanded 68.72% of the UAE cosmetic products market share in 2025, yet natural and organic variants are projected to grow at a 7.6% CAGR during 2026–2031.

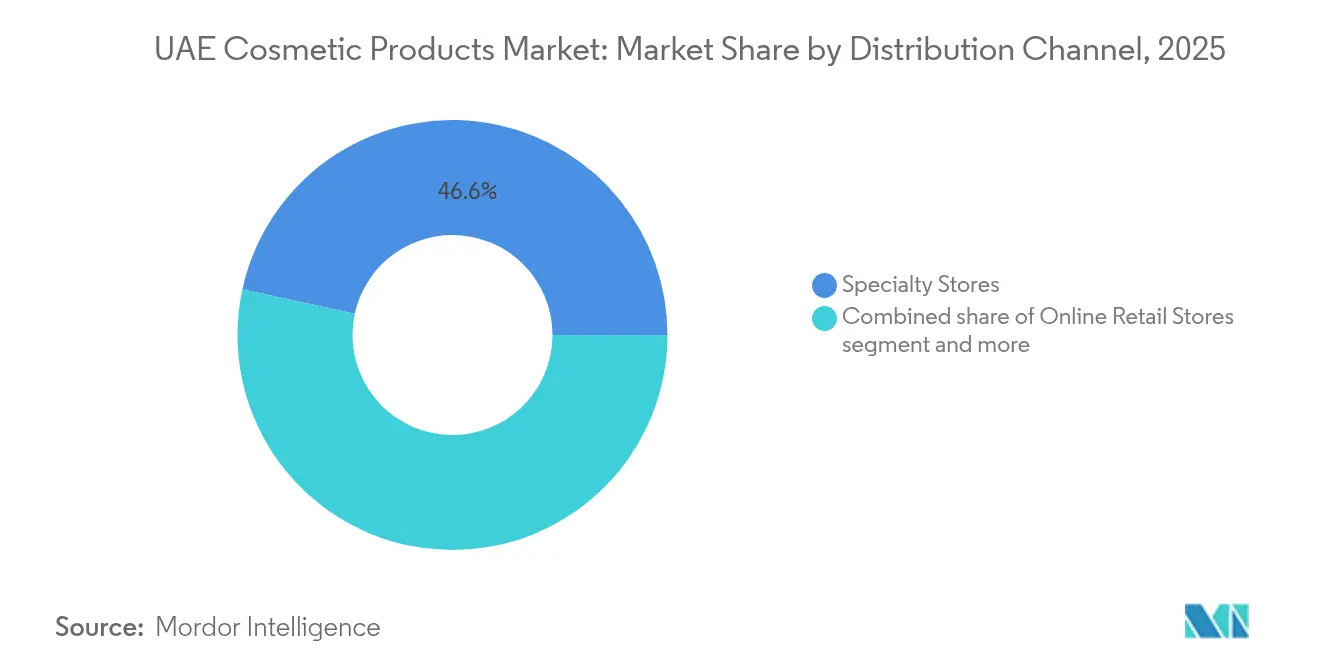

- By distribution channel, specialty stores generated 46.58% of the UAE cosmetic products market size in 2025, whereas online retail is expanding fastest at a 9.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong demand from inbound tourists | +1.2% | UAE nationwide, concentrated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Demand for halal-certified beauty products | +0.8% | UAE nationwide | Long term (≥ 4 years) |

| Increasing female workforce participation | +0.6% | UAE nationwide, stronger in urban centers | Long term (≥ 4 years) |

| Strong social media influence and digital marketing | +0.9% | UAE nationwide, particularly Dubai and Sharjah | Short term (≤ 2 years) |

| Consumers’ inclination toward natural and organic products | +0.5% | UAE nationwide, premium segment focus | Medium term (2-4 years) |

| Expansion of retail infrastructure | +0.7% | UAE nationwide, concentrated in major emirates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Demand from Inbound Tourist

Tourism significantly influences the UAE cosmetics market through multiple channels, with Dubai's status as the world's third-ranked destination for international arrivals driving sustained beauty product consumption. The UAE's duty-free infrastructure across five major airports - Abu Dhabi, Dubai, Sharjah, Ras Al Khaimah, and Fujairah - provides extensive opportunities for cosmetics purchases, while the introduction of the world's first VAT refund system for e-commerce tourist purchases in June 2025 enhances the shopping experience. The UAE has established itself as a key regional beauty market for products and services, with the World Travel and Tourism Council projecting international visitor spending to reach AED 228.5 billion in 2025 [1]Source: World Travel & Tourism Council, “International Traveller Spend in the UAE to Reach a Record AED 228BN This Year,” wttc.org . This environment drives premiumization across cosmetics categories, while the integration of digital platforms with physical retail spaces enables tourists to maintain their beauty product relationships beyond their visits. The continuous growth in tourist arrivals has prompted retailers to expand their cosmetics offerings and create immersive shopping experiences tailored to international visitors. Additionally, the strong tourism-retail relationship has encouraged global beauty brands to launch UAE-exclusive products and collections, further strengthening the country's position as a premier beauty shopping destination.

Demand for Halal-Certified Beauty Products

Halal certification requirements in the UAE are reshaping the cosmetics industry landscape, with stringent regulations mandated by the Emirates Standardisation and Metrology Authority for all products claiming halal status by 2025. The halal cosmetics segment is experiencing significant growth, driven by increasing consumer awareness and religious considerations in the predominantly Muslim market. These regulations have spurred innovation in ingredient sourcing and manufacturing processes, with brands investing in dedicated production lines and supply chain transparency. The UAE's position as the global halal economy capital creates structural advantages for compliant cosmetics brands, facilitating their access to Muslim-majority markets while creating entry barriers for non-compliant manufacturers. According to the World Bank, the UAE's population reached 10.48 million in 2023, presenting a substantial market opportunity for cosmetics manufacturers who align with these halal standards [2]Source: World Bank, “Total Population, United Arab Emirates,” worldbank.org . This regulatory framework has established the UAE as a preferred supplier hub for halal-certified cosmetics in the global market.

Increasing Female Workforce Participation

The increasing female workforce participation in the UAE is significantly influencing the cosmetics market growth, driven by rising demand for workplace-appropriate makeup, skincare, and personal care products. The growing disposable income among working women has enhanced their purchasing power for premium cosmetic products, while workplace dress codes and professional appearance requirements have boosted the consumption of everyday makeup and grooming products. The expansion of women in customer-facing roles, particularly in retail and corporate sectors, has accelerated the demand for cosmetics and influenced the growth of retail channels and beauty services that cater to working women's specific needs and time constraints. This trend has also led to the development of specialized cosmetic products designed specifically for professional environments, offering long-lasting formulations and subtle, workplace-appropriate aesthetics. According to the World Bank Gender Data Portal, the labor force participation rate among females in the United Arab Emirates was 54.1% for 2024 [3]Source: World Bank Gender Data Portal, “Labor Force Participation Rate, Female (%) (Modeled ILO Estimate),” genderdata.worldbank.org . This ongoing transformation in the workforce composition is expected to continue driving the growth of the UAE cosmetics market in the coming years.

Strong Social Media Influence and Digital Marketing

Social media platforms, particularly Instagram, TikTok, and Snapchat, have transformed the region's cosmetics market by creating direct-to-consumer channels that bypass traditional retail distribution. Young consumers increasingly make purchase decisions based on beauty influencers, trends, and user-generated content on these platforms. Local and international cosmetics brands have intensified their social media marketing efforts and influencer collaborations to showcase products, engage with consumers, and build brand awareness. The rise of social commerce enables direct purchasing through these platforms, while real-time product demonstrations and reviews enhance transparency and trust. The visual nature of these platforms particularly appeals to the younger demographic, who constitute a significant portion of cosmetics consumers. This digital transformation in cosmetics retail indicates a permanent shift in consumer behavior and marketing strategies, suggesting continued growth in social commerce within the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Religious and cultural considerations in product formulation | −0.4% | UAE nationwide with varying intensity by Emirates | Long term (≥ 4 years) |

| Strict product registration and regulatory requirements | −0.6% | UAE nationwide, affecting all market entrants | Medium term (2-4 years) |

| Rising concerns over counterfeit products | −0.3% | UAE nationwide, concentrated in grey-market channels | Short term (≤ 2 years) |

| Consumer concerns over product safety and ingredients | −0.2% | UAE nationwide, especially among educated consumers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Product Registration and Regulatory Requirements

Regulatory oversight in the UAE cosmetics market, primarily governed by the Emirates Authority for Standardization and Metrology (ESMA), implements comprehensive product registration and compliance requirements through the Emirates Conformity Assessment Scheme. The framework requires all cosmetic products to obtain ESMA approval through detailed product formulation documentation, safety assessments, quality certifications, and halal requirements for specific categories. International manufacturers must ensure their products meet UAE-specific standards, including mandatory bilingual labeling in Arabic and English, while operating through UAE-incorporated entities or local distributors. Dubai Municipality's Technical Guidelines for Cosmetics and Personal Care Products and the upcoming transition to the Emirates Drug Corporation as the federal regulator create multiple compliance checkpoints. While these regulations create significant barriers to entry, particularly affecting smaller brands and new market entrants, they also maintain product quality and consumer safety, establishing a competitive advantage for companies that successfully navigate the compliance requirements.

Rising Concerns Over Counterfeit Products

The prevalence of counterfeit products in the UAE market undermines consumer confidence and creates safety risks, particularly affecting premium and luxury segments where high margins incentivize illegal replication. While the Department of Economic Development conducts regular raids and enforcement actions, and the government has implemented strict regulations and penalties, the sophisticated nature of counterfeiting operations persists. The UAE's position as a major trading hub creates vulnerabilities, as counterfeiters can exploit the established logistics infrastructure. To address these challenges, companies focus on consumer education initiatives and authentication technologies to protect their market position and maintain consumer trust. However, the difficulty in monitoring informal sales channels and the complexity of counterfeiting operations continue to impact market growth, especially in higher-value cosmetics categories. This ongoing challenge of counterfeit products acts as a significant restraint on the UAE cosmetics market, affecting both industry profitability and consumer safety.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skincare Dominance Drives Market Foundation

Facial cosmetics dominate the UAE cosmetics market with a 47.92% share in 2025, driven by the region's harsh climate conditions that necessitate comprehensive skincare routines among residents and expatriates. Eye cosmetics maintain consistent demand due to Middle Eastern beauty traditions favoring dramatic eye makeup, particularly within modest fashion trends, while lip and nail products, though representing a smaller segment, show the highest growth rate at 6.05% CAGR through 2031, influenced by social media and local beauty influencers. This market segmentation reflects the unique cultural and environmental factors shaping consumer preferences in the region.

The UAE cosmetics market reflects a significant shift toward skincare-first beauty routines, accelerated by environmental factors such as extreme heat, air conditioning exposure, and desert climate conditions. This trend is particularly evident among Gen Z consumers, who prioritize products combining skincare and makeup functionalities, such as tinted SPFs and treatment-enhanced lip balms. The demand for these hybrid products creates opportunities for brands developing solutions that address both aesthetic preferences and the specific skincare challenges posed by the local climate. Manufacturers are responding by incorporating advanced UV protection and hydration technologies into their product formulations to meet these evolving consumer needs.

By Category: Premium Segment Accelerates Despite Mass Market Dominance

Mass market products dominate the UAE cosmetic products market with a 67.65% share in 2025, supported by a diverse socioeconomic landscape and price-conscious expatriate communities who form the majority of the population. The mass market segment continues to expand through retail infrastructure development, while benefiting from the UAE's broad consumer base. However, premium products are growing significantly faster at 7.1% CAGR through 2031, driven by the UAE's increasing concentration of high-net-worth individuals and tourists seeking luxury experiences. This growth trajectory in both segments reflects the market's ability to accommodate diverse consumer preferences and purchasing power levels.

The market exhibits a clear bifurcation between premium and mass segments, serving distinct consumer groups with limited overlap. This separation creates opportunities for brands to position themselves strategically within their chosen category. The premium segment, particularly in anti-aging products, maintains robust growth as UAE residents demonstrate a willingness to pay higher prices for products aligned with their values, despite economic fluctuations. International brands hold a significant market share in the premium category, reinforcing the UAE's status as a luxury retail destination. The distinct positioning of these segments enables manufacturers to develop targeted marketing strategies and product innovations specific to each consumer group.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

Specialty stores dominate the UAE beauty and personal care market with a 46.58% share in 2025, capitalizing on the country's robust retail infrastructure and consumer preferences for hands-on product testing and expert consultation. While supermarkets/hypermarkets remain significant distribution channels for mass-market products due to high foot traffic and convenience, online retail stores are experiencing rapid growth at 9.11% CAGR through 2031, led by platforms like Noon, Secret Skin, and Nysaa. This shift in consumer behavior reflects the increasing demand for convenient shopping options and personalized beauty experiences.

The market's distribution landscape is evolving toward integrated omnichannel experiences, where brands combine online and offline touchpoints to create seamless customer journeys. Traditional retailers are adapting to this shift by enhancing their digital capabilities and integrating them with physical retail operations, while maintaining the experiential aspects that drive consumer engagement and sales across all channels. The success of this transformation is evident in the growing adoption of hybrid shopping models that blend the convenience of online shopping with the tactile experience of physical stores.

By Ingredient Type: Natural Revolution Challenges Synthetic Dominance

Conventional/synthetic ingredients command a dominant 68.72% market share in 2025, benefiting from established consumer preferences and cost advantages in the price-sensitive UAE market. However, the natural/organic segment is experiencing rapid growth at 7.6% CAGR through 2031, with local brands developing botanical and organic formulations that cater to regional preferences. This shift in consumer preferences has prompted traditional manufacturers to incorporate natural ingredients into their product lines while maintaining their synthetic base formulations.

The natural and organic segment, while facing challenges such as higher costs and shorter shelf life, leverages the UAE's position as a halal economy hub. The alignment of natural ingredients with Islamic principles of purity creates opportunities for brands to serve both health-conscious consumers and those seeking religiously compliant products. This segment's growth also reflects broader sustainability trends, with companies focusing on ethically sourced ingredients and transparent supply chains to meet consumer demands for environmental and social responsibility. The integration of advanced preservation technologies is helping natural and organic products overcome shelf-life limitations, making them more viable for mainstream retail distribution.

Geography Analysis

The UAE cosmetics market demonstrates concentrated growth patterns across its seven emirates, with Dubai and Abu Dhabi serving as the primary drivers through their established positions as commercial and tourism hubs. Abu Dhabi's evolution as a luxury retail destination, marked by the increased presence of premium brands, complements Dubai's market strength, collectively positioning the UAE as a comprehensive beauty destination. The northern emirates of Sharjah, Ajman, and Ras Al Khaimah contribute to market expansion through developing retail infrastructure and growing expatriate populations, while Fujairah and Umm Al Quwain present emerging opportunities with their expanding consumer bases.

The UAE's strategic geographic location as a bridge between East and West creates distinctive market dynamics, establishing the country as a regional hub for cosmetics distribution across the GCC and broader Middle East. The concentration of market activity in Dubai and Abu Dhabi generates economies of scale for retailers and brands while offering expansion opportunities in developing emirates. The country's world-class logistics infrastructure and duty-free zones, combined with favorable free trade agreements, facilitate efficient cosmetics trade throughout the region.

The implementation of advanced digital infrastructure, including the pioneering VAT refund system for e-commerce tourist purchases, enhances the UAE's geographic advantages beyond physical boundaries. This comprehensive positioning enables the UAE to generate value from both regional consumption and international transit, creating multiple revenue streams that support consistent market growth across all emirates. The continuous investment in digital transformation and smart retail solutions further strengthens the UAE's position as a leading cosmetics market in the region.

Regulatory Landscape

Cosmetics and personal care products in the United Arab Emirates are regulated under the Ministry of Industry and Advanced Technology (MoIAT), with the control framework anchored in Cabinet Decision No. 18 of 2014. Market access commonly runs through the Emirates Conformity Assessment Scheme (ECAS), where regulated cosmetics require a Certificate of Conformity for customs clearance, along with core compliance items such as Arabic and English labeling and technical documentation (including test reports and formula declarations).

A key compliance layer comes from Gulf standards used in the UAE, including GSO 1943:2024 on general safety requirements and GSO 2528:2024 on criteria for allowed claims for cosmetics and personal care products. MoIAT operationalizes registration and conformity certification through its digital Conformity Hub and related e-services. The optional Emirates Quality Mark (EQM) also offers a higher-assurance pathway for brands that undergo more comprehensive manufacturer auditing, which can serve as a trust and quality differentiator in trade and retail discussions.

Competitive Landscape

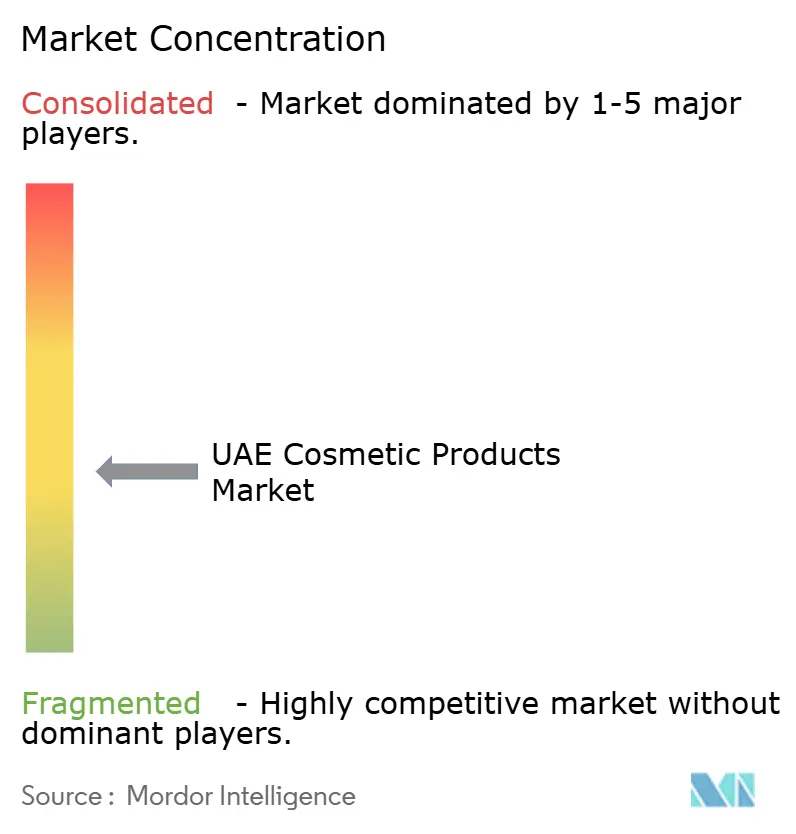

The UAE cosmetics market exhibits moderate fragmentation, with established multinationals like The Estée Lauder Companies, L'Oréal S.A., and LVMH Moët Hennessy Louis Vuitton competing alongside emerging local brands. The market's competitive dynamics are evolving rapidly as digitally native brands utilize social media influence and direct-to-consumer models to gain market share. This evolution is particularly significant as 90% of e-commerce purchases are influenced by online content, prompting companies to adopt various strategies from premium positioning through luxury retail partnerships to mass market penetration via hypermarket distribution.

UAE-based beauty brands have implemented market penetration strategies. Huda Beauty's evolution from a beauty blog to a significant Instagram presence demonstrates the capacity for regional companies to achieve international expansion through social media and cultural authenticity. The market dynamics are influenced by regulatory frameworks requiring local establishment and halal certification. Companies are establishing strategic partnerships, as evidenced by ASTERI Beauty's collaboration with Saudi artist Sara Alnamlah in September 2024, which integrated Saudi cultural elements in product packaging.

Moreover, technology integration has emerged as a key competitive differentiator in the UAE cosmetics market. Companies implementing AI-driven personalization, AR try-on experiences, and omnichannel retail strategies are gaining advantages in the digital marketplace. Success in the UAE cosmetics industry is increasingly determined by the effective combination of technological adoption, regulatory compliance, and digital marketing strategies. These technological advancements not only enhance customer experience but also provide valuable data insights for product development and marketing optimization.

UAE Cosmetic Products Industry Leaders

The Estée Lauder Companies

Huda Beauty LLC

L'Oréal S.A.

LVMH Moët Hennessy Louis Vuitton

Shiseido Company, Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory compliance is also a commercialization lever for brands that compete on safety, transparency, and claims discipline, especially where UAE requirements emphasize conformity certification (ECAS) and tighter control of claims (GSO 2528:2024). This creates headroom for brands that can run documentation cycles quickly, support robust lab testing, and scale bilingual labeling across high-velocity online retail, where consumer scrutiny of ingredients and claims is elevated.

Two shifts are shaping channel and product opportunities in the UAE cosmetics market. First, retail strategies are moving toward beauty-tech enabled shopping journeys, including AR try-on and digital consultation tools, consistent with the report's emphasis on social media influence and online retail expansion. Second, sustainability and circular beauty are becoming more concrete, with large players scaling refillable formats locally. That supports refill-compatible packaging, in-store refill partnerships, and SKU architectures designed for omnichannel replenishment.

Recent Industry Developments

- June 2026: L'Oreal Middle East signed the UAE Climate-Responsible Companies Pledge with the Ministry of Climate Change and Environment at the 3rd L'Oreal For the Future Summit in Dubai. The agreement aligned L'Oreal's UAE operations with a national climate framework and reinforced sustainability as an execution priority across its local brand portfolio and retail relationships.

- May 2026: L'Oreal launched the 2026 Big Bang Beauty Tech Innovation Program in the Middle East to support startup pilots spanning AI-powered commerce, creator-economy enablement, and circular beauty solutions. This broadened the pipeline of partners and technologies that can be integrated into omnichannel retail and personalization strategies in the UAE beauty market.

- May 2024: Kay Beauty expanded into the United Arab Emirates through Nysaa, making its range available at the Nysaa store in City Centre Mirdif and via Nysaa's e-commerce platform. The entry increased competitive intensity in mass-to-premium color cosmetics and used a hybrid retail plus online route to accelerate availability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers cosmetic products sold in the United Arab Emirates for personal grooming and appearance, tracked as sales value at the market level across retail and online channels.

Scope exclusions: This sizing does not include professional salon service revenue or devices that are used to apply or remove cosmetics.

Segmentation Overview

- By Product Type

- Facial Cosmetics

- Eye Cosmetics

- Lip and Nail Makeup Products

- By Category

- Premium Products

- Mass Products

- By Ingredient Type

- Natural and Organic

- Conventional/Synthetic

- By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure for the UAE market and to anchor the model to public, repeatable data points. We referred to official and open sources such as UAE Federal Competitiveness and Statistics Centre releases, Dubai Statistics Center indicators, UN Comtrade trade flows for finished cosmetics, and World Bank macro series that affect discretionary spend.

To keep the numbers usable for a commercial market model, additional checks were taken from sources such as public customs and port updates, trade association publications, peer reviewed papers on beauty consumption, and company filings and investor presentations from firms with meaningful Middle East exposure. Select paid subscriptions were used only where they added consistency, mainly for company financials, patent lookups, and shipment level import-export checks. The sources listed here are illustrative only, and many other public documents were also reviewed to support collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on translating category level signals into UAE specific assumptions that can be defended. This included channel mix shifts, premium versus mass price ladders, and the pace of online adoption in the United Arab Emirates.

We spoke with a mix of manufacturers, distributors, retailers, and industry specialists, so secondary inputs could be pressure tested. We then used those conversations to address gaps such as unreported discounting and fast moving launches before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | |

| Mid tier: 44% | Functional/Unit leaders: 31% | |

| Smaller Players: 20% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts with a top down reconstruction of the UAE demand pool, where household consumption capacity, inbound tourism spend patterns, and observable trade and distribution signals are used to set the outer market envelope, and then split into cosmetics specific value. Once that ceiling is established, the totals are corroborated with selective bottom up approximations, mainly sample based price per unit checks multiplied by plausible consumption volume, followed by retailer and distributor channel checks that highlight where adjustments are needed.

Inputs that mattered for this market included premiumization rates, online share progression, product mix shifts between face, eye, and lip and nail cosmetics, and import intensity for finished cosmetics, because much of the supply is traded. When a bottom up trail was incomplete, such as for smaller importers and short lifecycle launches, we used channel level proxies and a conservative uplift that was validated through interviews. Forecasts were developed using scenario analysis supported by short time series smoothing, and then the scenarios were filtered through primary feedback on pricing, promotions, and new brand entry, so the final path stayed realistic.

Data Validation & Update Cycle

Outputs were checked against independent signals, including the direction of import values, retail channel growth signals, and macro changes that influence discretionary categories. When mismatches showed up, we traced them back to the exact assumption driving the variance. If results moved outside reasonable bounds, respondents were re contacted and the model was re run with revised price ladders, channel splits, or mix assumptions.

Before sign off, the work goes through a multi step review so calculations, units, and time alignment remain consistent across categories and years. Reports are refreshed annually, and interim updates are made when a material event changes demand, pricing, or supply conditions. Just before delivery, a final analyst pass is completed so the numbers reflect the latest available public releases and field notes.

Mordor Intelligence's United Arab Emirates Cosmetics Products Market Market Estimate Compared With Other Published Estimates

Published market sizes for UAE cosmetics often vary, even when they sound similar, because each publisher draws the boundary differently and uses its own pricing and channel assumptions. Differences also show up when one model relies on broader beauty and personal care totals, while another focuses only on cosmetic product sales captured in the market scope.

The table shows a wide spread mainly because some estimates fold skincare and haircare into the same total, and then apply aggressive value growth from premium pricing without clearly separating discounts and mix changes. In Mordor Intelligence's model, only cosmetic products within the defined product types are counted, and pricing is adjusted using a channel weighted approach that reflects promotions and premium versus mass ladders observed in the UAE.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 395.43 M (2025) | |

| Industry Consultancy A | USD 8.22 B (2024) | Uses a broader cosmetics basket that includes overlapping beauty and personal care categories such as skincare, haircare, and fragrances, which inflates the addressable value versus a cosmetics products only scope. |

| Regional Publisher B | USD 1.50 B (2024) | Appears to include added end uses and wider retail coverage, and then applies a different base year and price build that is less explicit about promotion effects and channel mix shifts. |

Reading the three values together, the main takeaway is that scope and price logic drive most of the gap, not small differences in growth rates. By tying the size to observable UAE demand signals and by keeping inclusions clearly defined, the estimate remains easier to replicate and to update when channel shares or pricing conditions change.

Key Questions Answered in the Report

What is the current value of the UAE cosmetic products market?

The UAE cosmetics market is valued at USD 411.79 million in 2026.

Which product segment holds the largest UAE cosmetic products market share?

Facial cosmetics lead with a 47.92% share in 2025.

Which distribution channel is expanding fastest?

Online retail is growing at a 9.11% CAGR between 2026 and 2031.

What drives the rise of natural and organic beauty products?

Ingredient safety awareness and environmental sustainability concerns push consumers toward botanically based, halal-aligned formulations.

Page last updated on: