Massage Oil Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

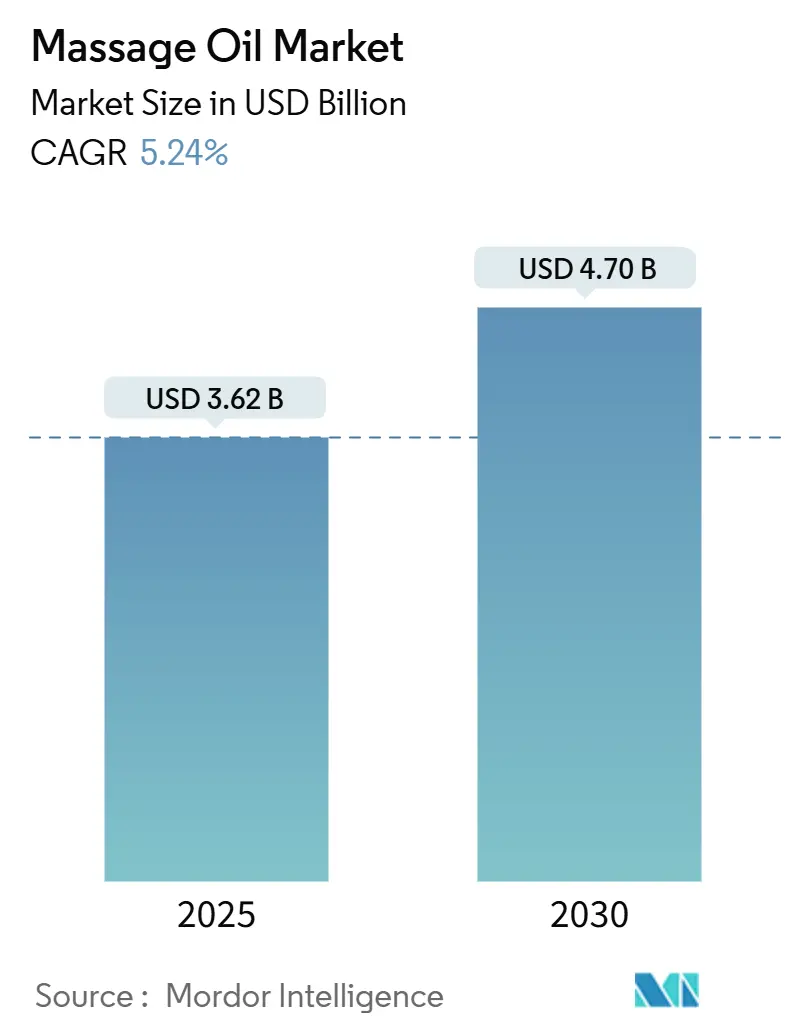

| Market Size (2025) | USD 3.62 Billion |

| Market Size (2030) | USD 4.70 Billion |

| Growth Rate (2025 - 2030) | 5.24% CAGR |

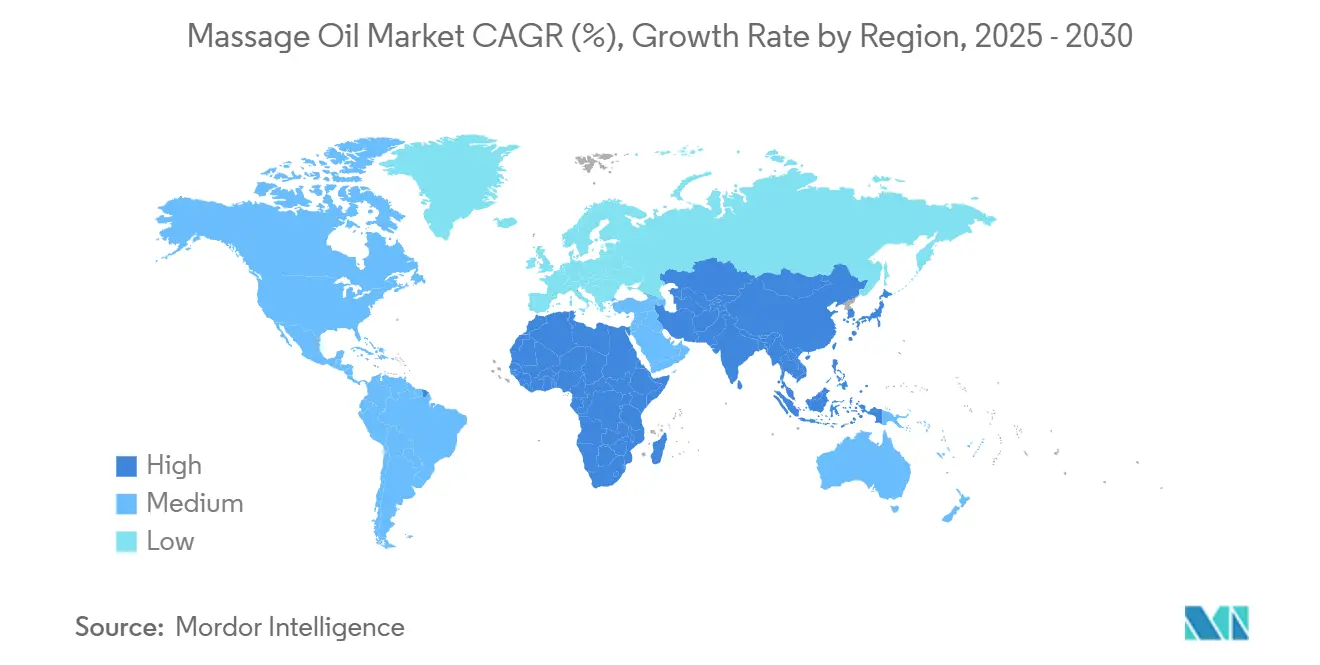

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Massage Oil Market Analysis by Mordor Intelligence

The Massage Oil Market size is estimated at USD 3.62 billion in 2025, and is expected to reach USD 4.70 billion by 2030, at a CAGR of 5.24% during the forecast period (2025-2030).

A confluence of rising wellness tourism, proliferating spa infrastructure, and the appeal of clean-label botanicals keeps demand resilient even as raw-material prices swing. Institutional buyers prefer bulk procurement of certified oils that guarantee purity, fuelling long-term supplier relationships, while e-commerce makes premium blends more visible to home users. Europe’s regulatory clarity sustains high-value positioning, but Asia-Pacific now contributes the strongest incremental volumes as middle-class consumers treat massage as part of everyday self-care. Intensifying product innovation—whether CBD-infused muscle-relief blends or aromatherapy hybrids—underlines a pivot from single-ingredient commodity oils to experience-driven formulations.

Key Report Takeaways

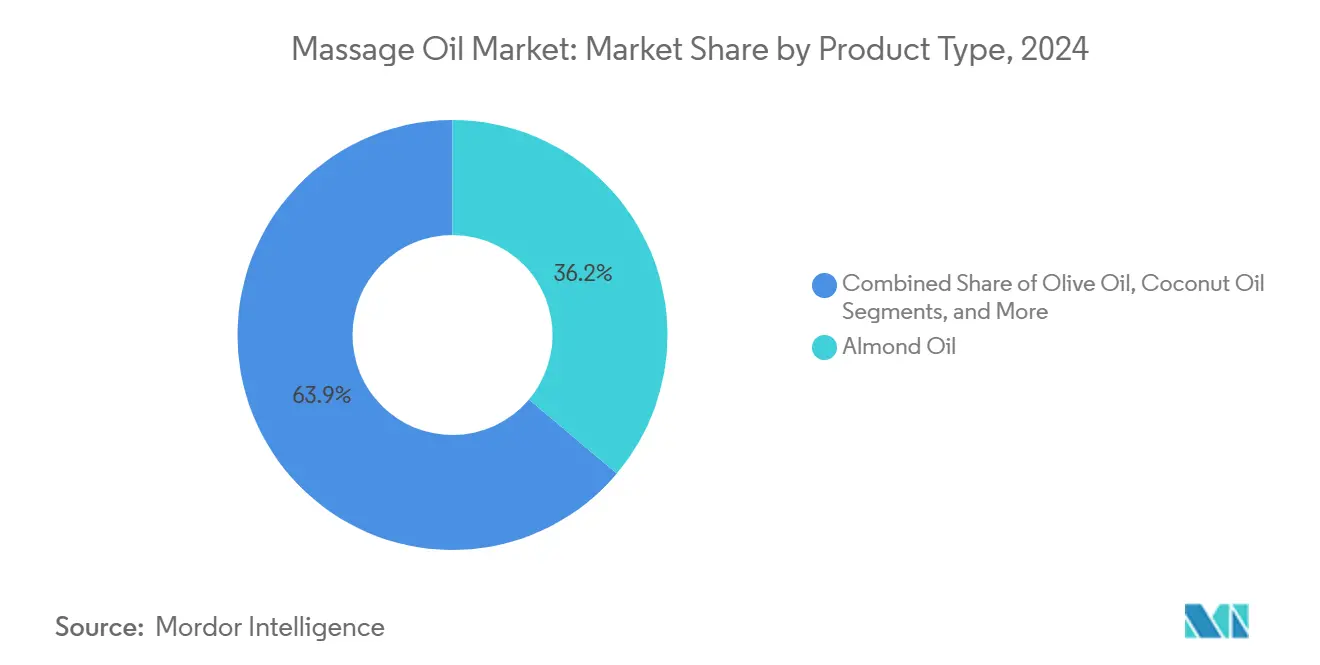

- By product type, almond oil led with 36.15% revenue share in 2024; coconut oil is projected to advance at a 6.35% CAGR to 2030.

- By application, spa and wellness centers accounted for 52.79% of the massage oil market share in 2024, while sports and fitness recovery records the fastest CAGR at 6.85% through 2030.

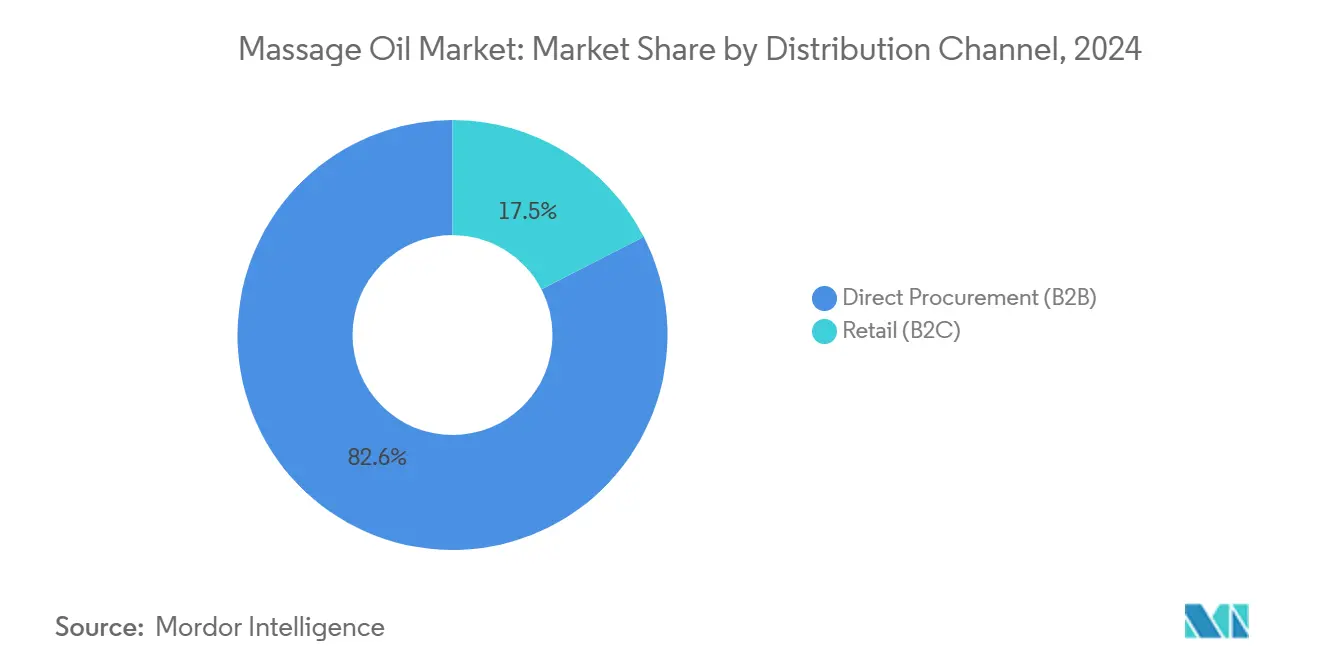

- By distribution channel, B2B direct procurement controlled 82.55% of the massage oil market size in 2024, and B2C retail is forecast to climb at a 5.72% CAGR between 2025-2030.

- By geography, Europe captured 34.79% of 2024 revenue, whereas Asia-Pacific is slated to post the highest regional CAGR at 6.11% through 2030.

Global Massage Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of spas and wellness centers | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing consumer preference for natural and organic oils | +0.9% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Medical and therapeutic adoption | +0.7% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| Surge in CBD-infused functional massage oils | +0.6% | North America primary, limited EU adoption | Short term (≤ 2 years) |

| Aromatherapy and essential oil infusion | +0.5% | Global, traditional markets in APAC | Medium term (2-4 years) |

| Diversity in product offerings and ingredients | +0.4% | Global, innovation-driven markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Spas and Wellness Centers

The growth in massage oil consumption is primarily driven by the expansion of spa and wellness facilities, supported by increased focus on wellness after the pandemic and changing consumer preferences toward experiential services. According to ISPA, US spa visits reached 182 million in 2023, with an average revenue of USD 117.2 per visit, demonstrating consistent consumer spending on therapeutic services[1]Source: "ISPA Research - Rate of recovery," Spa Business, spabusiness.com. The ongoing labor shortage has led spa facilities to invest in premium massage oils to differentiate their services and retain therapists. The Global Wellness Institute reports that wellness tourism is growing at 9.1% annually and accounts for 14% of global tourism expenditure[2]Source: "The Global Wellness Tourism Economy," Global Wellness Institute, globalwellnessinstitute.org . The integration of massage services into corporate wellness programs has created new business-to-business procurement channels beyond traditional retail distribution.

Growing Consumer Preference for Natural and Organic Oils

The increasing consumer preference for natural and organic formulations aligns with clean-label trends in both food and personal care sectors, enabling organic massage oil manufacturers to implement premium pricing strategies. The Botanical Adulterants Prevention Program has identified significant adulteration issues in essential oil supply chains, particularly in high-value ingredients such as Damask rose oil, where manufacturers often substitute authentic botanical extracts with synthetic chemicals and lower-cost oils. This quality concern has increased demand for vertically integrated suppliers who maintain transparent sourcing practices and hold third-party certifications. The FDA regulations under 21 CFR 582.20 establish safety guidelines for essential oils, specifying approved botanical sources including alfalfa, allspice, and almond extracts[3]Source: "21 CFR 582.20 -- Essential oils, oleoresins (solvent-free), and natural extractives (including distillates)," U.S. Government, ecfr.gov. The World Health Organization's digital platform for monitoring plant-derived product safety validates the therapeutic benefits of natural oils, supporting their adoption in medical applications. The younger consumer demographic, particularly Millennials and Gen Z, shows a higher willingness to pay premium prices for organic-certified products with transparent ingredient sourcing.

Medical and Therapeutic Adoption

The integration of massage therapy into healthcare institutions creates demand channels that prioritize efficacy and regulatory compliance over cost considerations. This environment supports premium product positioning and recurring procurement contracts. The FDA's classification of therapeutic massage devices as Class II medical equipment under 21 CFR Part 890, intended for muscle pain relief and circulation improvement, establishes regulatory pathways for massage oils in clinical applications. Sports medicine applications generate demand for specialized formulations targeting muscle recovery and inflammation reduction, with athletic performance centers providing significant procurement opportunities. The FDA's De Novo classification process for therapeutic massage devices demonstrates growing regulatory acceptance of massage therapy's medical applications, enabling oil manufacturers to develop clinically validated formulations. While insurance reimbursement for massage therapy services further validates medical applications, coverage remains restricted to specific conditions and provider categories.

Surge in CBD-Infused Functional Massage Oils

The CBD massage oil segment demonstrates significant growth potential, despite regulatory uncertainties limiting widespread adoption and distribution channels. The US hemp-derived CBD market reached USD 4.7 billion in 2020, growing by 14%. According to Hemp Industry Daily, the market could expand to USD 16.8 billion by 2025 if regulatory frameworks are established[4]Source: "US CBD Market Report," Hemp Industry Daily, hempindustrydaily.com. Current FDA inaction on dietary supplement regulations restricts market growth. CBD product prices face downward pressure due to oversupply and economic conditions, leading manufacturers to incorporate functional ingredients to maintain premium pricing and market differentiation. The FDA continues to assess safety data while developing comprehensive CBD product regulations, creating opportunities for companies that develop compliant formulations early. Due to retail distribution constraints, CBD massage oil sales primarily occur through e-commerce channels, where direct-to-consumer models enable higher profit margins and enhanced customer education. Companies continue to innovate by combining CBD with adaptogens, terpenes, and other functional ingredients to create enhanced formulations and maintain premium market positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw-material (essential oil) prices | -0.8% | Global, acute in tropical oil-producing regions | Short term (≤ 2 years) |

| Increasing prevalence of counterfeit and low-quality products | -0.6% | Global, concentrated in unregulated markets | Medium term (2-4 years) |

| Regulatory grey areas around therapeutic claims | -0.4% | North America and Europe primarily | Long term (≥ 4 years) |

| Short shelf life and storage challenges for natural oils | -0.3% | Global, climate-sensitive regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw-Material (Essential Oil) Prices

Raw material price fluctuations create margin pressure and supply chain disruptions, particularly affecting smaller manufacturers without hedging capabilities and long-term supplier contracts. Coconut oil prices increased during November 2024 due to adverse weather conditions in major producing countries - Sri Lanka, the Philippines, and Indonesia. This increase compelled manufacturers to raise retail prices, potentially impacting price-sensitive customer segments. Olive oil prices reached USD 9,127.83 per metric ton in May 2024, affecting premium massage oil formulations in luxury spa applications, according to the International Monetary Fund[5]Source: "Global price of Olive Oil [POLVOILUSDM]," International Monetary Fund, fred.stlouisfed.org. However, soybean oil prices are projected to decrease through July-August 2025, driven by increased inventories and favorable weather conditions. This decline offers potential cost benefits for manufacturers using soybean-derived carrier oils. While government interventions, such as Sri Lanka's controlled price distribution programs, provide temporary market stabilization, they present supply allocation challenges for international buyers. The Coconut Cultivation Board anticipates market stabilization through increased production capacity. However, climate change impacts on tropical agriculture suggest continued volatility in essential oil commodity markets.

Increasing Prevalence of Counterfeit and Low-Quality Products

Product adulteration affects consumer trust and creates unfair competition for manufacturers who invest in quality control and authentic ingredient sourcing. The Botanical Adulterants Prevention Program has identified extensive adulteration of Damask rose essential oil, where manufacturers substitute authentic Rosa × damascena extracts with lower-cost oils and synthetic chemicals to avoid the resource-intensive production process. Many products labeled as 'Damask rose oil' contain no genuine oil, indicating the necessity for clear labeling and independent authentication systems to safeguard consumers and legitimate producers. These counterfeit products often fail to meet safety testing and quality standards, creating potential risks for distributors and users while reducing the market value of authentic products. The growth of online marketplaces has increased the distribution of counterfeit products, making regulatory enforcement difficult for authorities and brand owners. While industry associations and certification organizations are implementing authentication technologies and supply chain monitoring systems to address adulteration, the associated costs may burden smaller manufacturers who lack resources for comprehensive quality control programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Almond Oil Dominance Faces Coconut Innovation

Almond oil holds the largest product segment share at 36.15% in 2024, due to its established therapeutic applications and consumer acceptance. Coconut oil demonstrates the fastest growth rate at 6.35% CAGR through 2030, supported by its antimicrobial properties and increasing wellness trends. Almond oil's market leadership stems from its hypoallergenic properties and neutral scent, making it suitable for sensitive skin applications in medical and therapeutic environments where risk minimization is essential. Coconut oil's growth reflects increasing demand for versatile products offering multiple skincare benefits, with fractionated variants gaining popularity due to their stability and enhanced absorption properties.

Citrus oils occupy a distinct market position in aromatherapy applications, where essential oil-infused products command higher prices despite smaller market shares. Specialty oils, including jojoba, argan, and avocado, serve specific applications in premium spa treatments and therapeutic protocols. The FDA's regulation under 21 CFR 582.20 provides clear guidelines for essential oil ingredients, facilitating product development and market entry for compliant formulations. Market opportunities exist in developing blended formulations that combine carrier oils with functional additives, creating enhanced effects that support premium pricing and differentiation from basic single-ingredient products.

By Application: Spa Dominance Challenged by Sports Recovery Growth

Spa and wellness centers hold 52.79% of the market share in 2024, supported by their established infrastructure and networks of trained therapists. The sports and fitness recovery segment is growing at a 6.85% CAGR through 2030, driven by increased awareness of massage therapy's role in athletic performance. The spa segment's market leadership reflects the industry's recovery. According to the International Spa Association, professional massage services cost an average of USD 116 per session in 2023, generating significant oil consumption that supports premium product pricing and stable procurement relationships.

The medical therapeutic segment operates under FDA device classifications outlined in 21 CFR Part 890, which categorizes therapeutic massage equipment as Class II medical devices, establishing regulatory frameworks for clinical oil applications. Sports and fitness recovery applications show the highest growth rate, supported by athletic performance trends and expanding corporate wellness programs. The home and personal use segment has grown through direct-to-consumer channels and increased wellness routines adoption. According to the Global Wellness Institute, wellness tourism is expected to reach 14% of total tourism spending, maintaining demand for spa applications. The integration of sports medicine expands therapeutic applications, while products designed for multiple uses allow manufacturers to serve various segments and help distributors optimize inventory management.

By Distribution Channel: B2B Procurement Maintains Control Despite B2C Acceleration

Direct procurement through B2B channels holds 82.55% market share in 2024, as spa and medical facilities maintain bulk purchasing patterns and established supplier relationships. Meanwhile, B2C retail channels are growing at a 5.72% CAGR through 2030, supported by increasing home wellness adoption and e-commerce expansion. The B2B segment's leadership position results from institutional requirements that favor suppliers with quality certifications, regulatory compliance, and the capacity to serve large operations. Professional buyers emphasize consistency, safety documentation, and technical support rather than price, enabling premium positioning and long-term contracts. In the B2C segment, specialty spa retailers serve both professional therapists and wellness enthusiasts who seek commercial-grade products for home use.

E-commerce platforms are driving B2C channel expansion by facilitating direct manufacturer-to-consumer sales that eliminate traditional retail markups while offering product education opportunities. Online stores benefit from subscription programs and repeat purchases that generate consistent revenue streams. Supermarkets and hypermarkets provide convenience for consumers, though their limited shelf space restricts product variety. Pharmacies and drug stores lend credibility for therapeutic applications and attract customers seeking medical-grade products, allowing for wellness product cross-selling. The diverse B2C channel landscape requires targeted marketing and positioning strategies, distinct from centralized B2B procurement approaches.

Geography Analysis

Europe holds the largest regional market share at 34.79% in 2024, supported by established spa traditions, regulatory frameworks, and healthcare system integration of therapeutic massage. The region's developed wellness infrastructure enables premium product positioning, particularly in Germany and France, which have high spa facility density and widespread acceptance of alternative wellness practices. The European Union's clear regulatory guidelines for cosmetics and medical devices create market stability, attracting international manufacturers. However, Brexit has introduced trade complexities affecting UK market access for EU-based suppliers. The European massage oil market benefits from organic and natural product certifications, meeting consumer demand for authentic, sustainably sourced products.

Asia-Pacific demonstrates the highest growth rate at 6.11% CAGR through 2030, driven by urbanization, expanding middle-class populations, and government support for traditional medicine. The China Hot Spring Tourism Association's standardization efforts strengthen the wellness tourism sector by establishing quality standards. In India, significant market developments include Dabur's 7.6% operating income growth in 2023-24 and its acquisition of Sesa Care for Rs 315-325 crore, targeting the Rs 900 crore ayurvedic hair oil market. The Global Wellness Institute identifies Asia-Pacific as a primary region for wellness tourism expansion, supported by increasing consumer interest and rising disposable income.

North America maintains a strong market position through its established spa infrastructure and sports medicine applications. The FDA's regulatory guidelines under 21 CFR for essential oils and therapeutic applications provide clear compliance pathways for medical and clinical massage oil use. South America and Middle East and Africa show growth potential through developing wellness tourism infrastructure, though their market shares remain modest due to economic limitations and developing regulatory frameworks. These regions display positive growth trajectories as wellness tourism infrastructure expands and therapeutic massage awareness increases.

Competitive Landscape

The massage oil market exhibits fragmented competition, with no single player commanding a dominant market share. Key companies including Bon Vital, Biotone, The Body Shop, Aura Cacia, and Dabur operate across professional spa, medical, and consumer segments. Each segment requires specific product formulations, packaging, and distribution approaches, creating niche market opportunities while limiting economies of scale. The market fragmentation enables established companies to pursue acquisitions for scale advantages and vertical integration benefits.

Companies prioritize quality differentiation and regulatory compliance over price competition. Successful market participants invest in organic certifications, therapeutic claims validation, and supply chain transparency to maintain premium positioning. Growth opportunities exist in CBD-infused formulations, sports recovery applications, and medical-grade products that comply with FDA device compatibility requirements under 21 CFR Part 890. Companies implement supply chain authentication and quality assurance systems through blockchain technology and third-party testing to ensure ingredient authenticity. New market entrants utilize e-commerce platforms and subscription models to reach consumers directly while reducing distribution costs.

The market experiences increased merger and acquisition activity as companies pursue geographic expansion and complementary capabilities. For example, Dabur's acquisition of Sesa Care enhanced its ayurvedic formulations portfolio and distribution network access. Companies implement vertical integration strategies through plantation ownership and long-term supply contracts to manage raw material costs and quality. Product development focuses on multifunctional formulations that combine therapeutic and sensory benefits to maintain premium pricing. The market remains distributed among multiple players, with regional specialists maintaining strong local presence while global brands leverage procurement and distribution advantages.

Massage Oil Industry Leaders

-

Bon Vital (Performance Health)

-

Biotone

-

The Body Shop

-

Aura Cacia (Frontier Co-op)

-

Dabur

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Global Wellness Institute launched "Massage Makes Me Healthy and Happy" initiative, outlining wellness trends for 2025, emphasizing therapeutic massage applications and creating market validation for medical-grade massage oil formulations.

- October 2024: Dabur India announced acquisition of 51% stake in Sesa Care Private Limited for Rs 315-325 crore (USD 38-39 million), strengthening its position in the Rs 900 crore ayurvedic hair oil market and expanding therapeutic massage oil capabilities through Sesa's established Ayurvedic product portfolio

- June 2024: Federal Reserve Bank of St. Louis reported olive oil prices at USD 9,127.83 per metric ton in May 2024, reflecting continued price elevation affecting premium massage oil formulations

Global Massage Oil Market Report Scope

| Almond Oil |

| Olive Oil |

| Coconut Oil |

| Citrus Oil |

| Other Specialty Oils |

| Spa and Wellness Centers |

| Medical Therapeutics |

| Home and Personal Use |

| Sports and Fitness Recovery |

| Direct Procurement (B2B) | |

| Retail (B2C) | Specialty Spa Retailers |

| Supermarkets/Hypermarkets | |

| Pharmacies and Drug Stores | |

| Online Retails Stores | |

| Other |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Almond Oil | |

| Olive Oil | ||

| Coconut Oil | ||

| Citrus Oil | ||

| Other Specialty Oils | ||

| By Application | Spa and Wellness Centers | |

| Medical Therapeutics | ||

| Home and Personal Use | ||

| Sports and Fitness Recovery | ||

| By Distribution Channel | Direct Procurement (B2B) | |

| Retail (B2C) | Specialty Spa Retailers | |

| Supermarkets/Hypermarkets | ||

| Pharmacies and Drug Stores | ||

| Online Retails Stores | ||

| Other | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What are the top-selling massage oils in the market?

Almond oil leads the massage oil market with 36.15% share in 2024, followed by coconut oil which is growing fastest at 6.35% CAGR through 2030.

How big is the global massage oil industry?

The global massage oil market is valued at USD 3.62 billion in 2025 and is projected to reach USD 4.70 billion by 2030, growing at a 5.24% CAGR.

Which massage oils are best for professional spa use?

Professional spas primarily use hypoallergenic options like almond oil (36.15% market share) for general applications, while specialized treatments utilize coconut oil for antimicrobial benefits, olive oil for luxury positioning, and essential oil blends for aromatherapy effects.

Which region shows the highest potential for massage oil sales?

Asia-Pacific shows the highest growth potential at 6.11% CAGR through 2030, driven by expanding middle-class wellness spending in China and India, traditional medicine integration, and government support for wellness tourism infrastructure development.

Page last updated on: