Tissue Towel Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

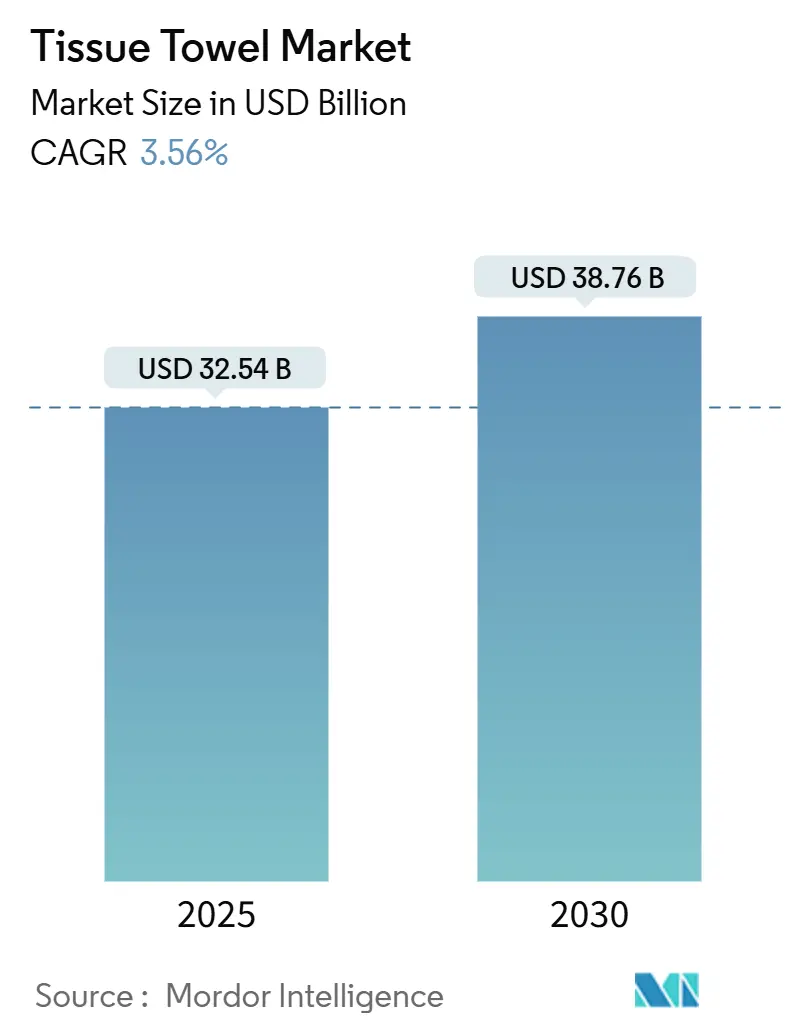

| Market Size (2025) | USD 32.54 Billion |

| Market Size (2030) | USD 38.76 Billion |

| Growth Rate (2025 - 2030) | 3.56% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tissue Towel Market Analysis by Mordor Intelligence

The global tissue towel market size is valued at USD 32.54 billion in 2025 and is projected to expand to USD 38.76 billion by 2030, registering a compound annual growth rate (CAGR) of 3.56% during the forecast period. This measured growth trajectory reflects the market's maturation while highlighting sustained demand driven by evolving hygiene standards and demographic shifts across key regions. The tissue towel sector demonstrates resilience amid raw material volatility, with manufacturers increasingly pivoting toward sustainable fiber alternatives and operational efficiency improvements to maintain profitability.

Key Report Takeaways

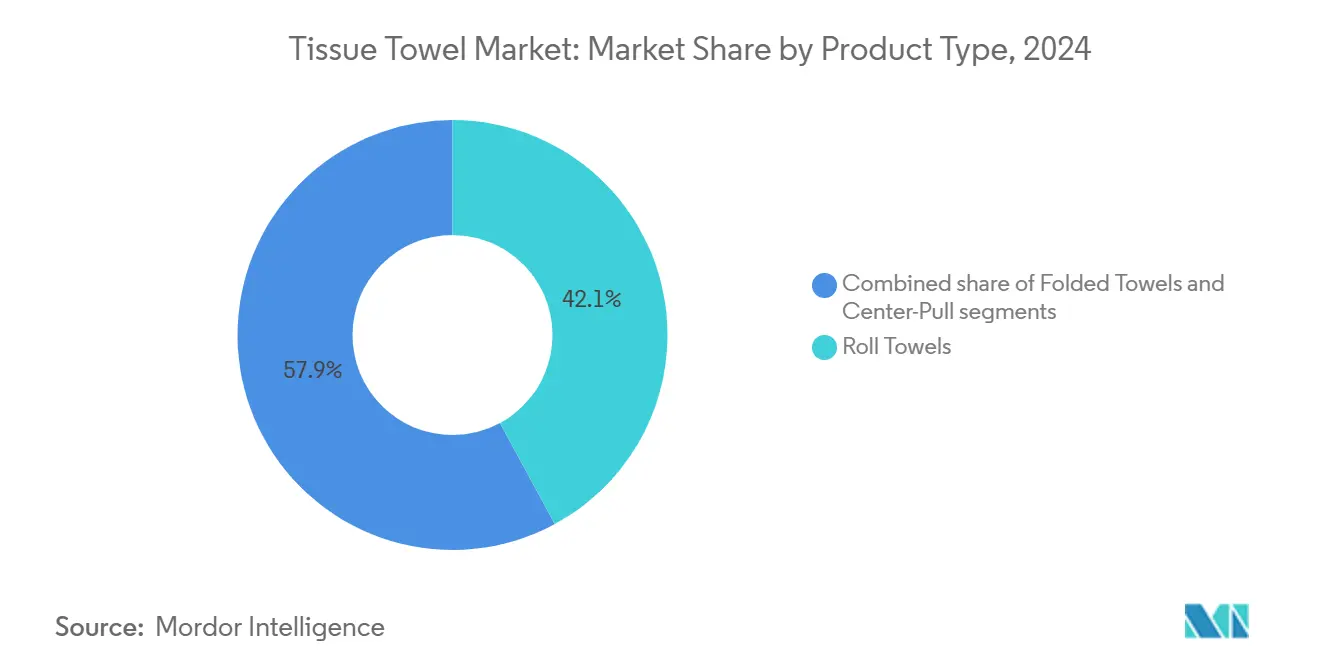

- By product type, roll towels dominated the tissue towel market with a 42.11% share in 2024. The center-pull towels segment is expected to grow at a CAGR of 4.23% through 2030.

- By end-user, the commercial segment held a 58.43% revenue share in 2024, while the residential segment is expected to grow at a 4.65% CAGR during 2025-2030.

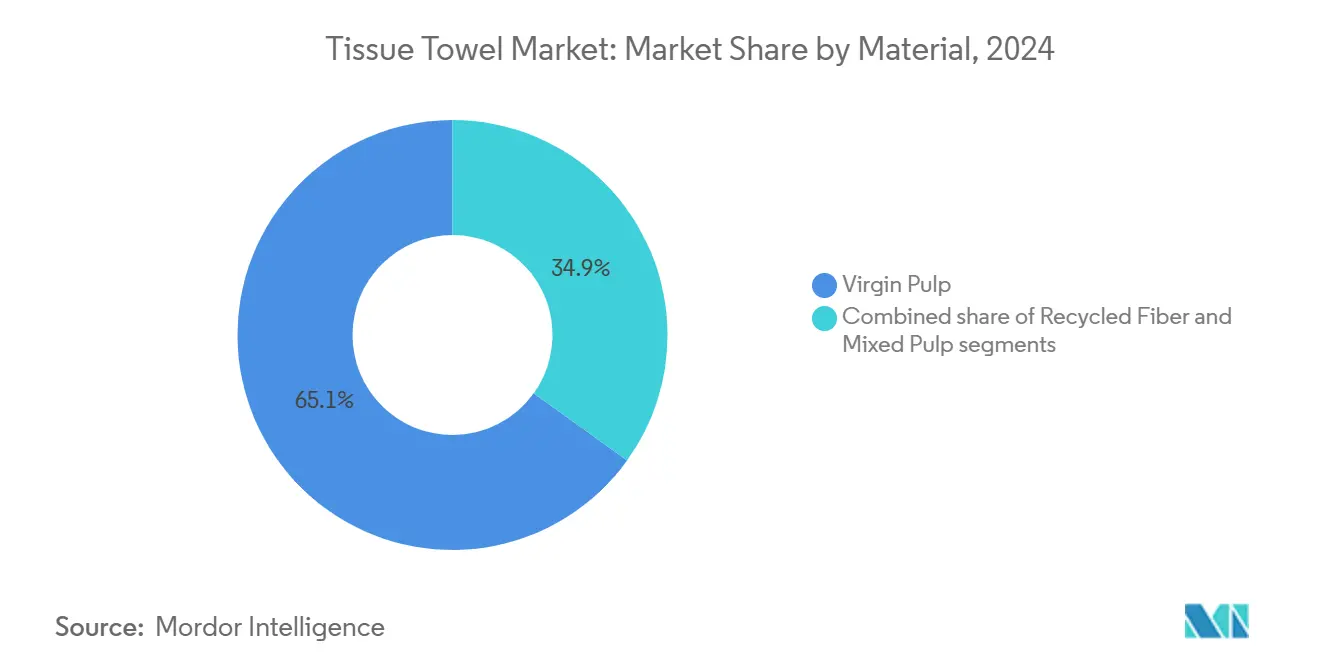

- By material, virgin pulp accounted for a 65.08% share of the tissue towel market size in 2024, while recycled fiber is poised to grow at a 5.06% CAGR over the same outlook.

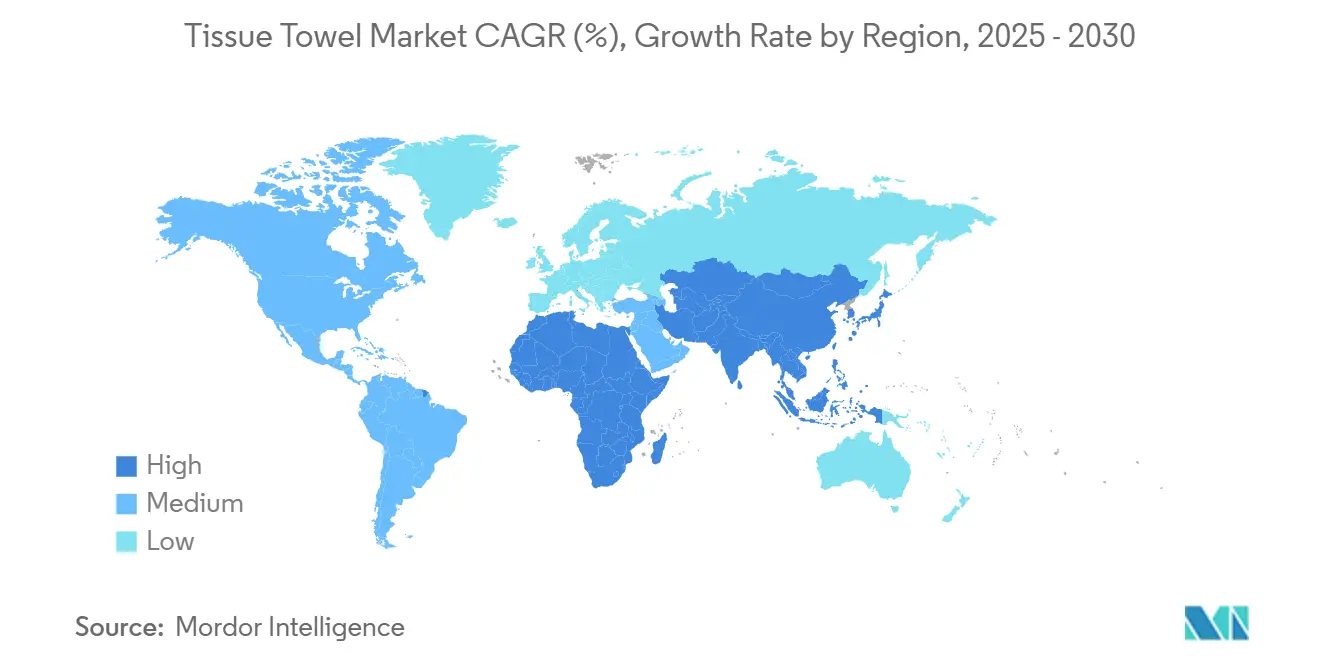

- By geography, Asia-Pacific held a 35.21% share of the market in 2024, while the Middle East and Africa region is projected to grow at the highest CAGR of 4.89% during 2024-2030.

Global Tissue Towel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in away-from-home hygiene installations | +0.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Convenience and portability | +0.6% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Innovation in product features | +0.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth of hospitality and healthcare sectors | +0.7% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Bamboo and bagasse fiber substitution momentum | +0.4% | Asia-Pacific and South America, early adoption in Europe | Long term (≥ 4 years) |

| Sustainability and eco-friendly trends | +0.5% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in away-from-home hygiene installations

Enhanced hygiene protocols have become standard practice across commercial facilities, evolving beyond temporary pandemic measures. The healthcare and food service industries show strong demand, as facilities upgrade to high-capacity roll towel and center-pull dispensing systems. These infrastructure investments in dispensing equipment establish sustained tissue towel consumption patterns. The North American away-from-home tissue market has returned to pre-pandemic levels due to increased public mobility and service sector activity. Consumer surveys indicate permanent changes in hygiene expectations. Stricter regulatory compliance requirements, combined with IoT and AI technologies, are transforming facility management practices to improve tissue product usage and inventory control.

Convenience and portability

Consumer preferences have shifted toward grab-and-go formats, reflecting lifestyle changes that emphasize convenience and single-use products over traditional bulk purchases. According to AFRY AB survey data, 30% of consumers purchase smaller pack sizes, while 44-50% choose private-label tissue products, indicating both price sensitivity and functional requirements. The COVID-19 pandemic increased kitchen paper towel consumption, with 40% of consumers reporting higher usage - a trend that continues post-pandemic. Portable dispensing solutions have gained popularity in mobile settings like food trucks and outdoor events where traditional washroom facilities are not available. Manufacturers now focus on developing compact, high-absorption products that maximize performance per unit weight to address transportation and storage efficiency. Consumers' willingness to pay for convenience-oriented products has enabled manufacturers to maintain margins despite increased raw material costs.

Bamboo and bagasse fiber substitution momentum

Alternative fiber adoption is increasing as manufacturers prioritize cost stability and sustainability, with bamboo and bagasse providing higher growth rates and reduced environmental impact compared to wood pulp sources. Bamboo fibers demonstrate a liquid absorbency capacity of 22.5 g/g, exceeding commercial pads while maintaining porosity levels above 99%[1]Source: BioResources, “Bamboo Fiber Absorbency Study,” bioresources.ncsu.edu. In India, sugarcane bagasse-based manufacturing proves economically viable with a reduced carbon footprint compared to conventional materials[2]Source: E3S Web of Conferences, “Bagasse-Based Tissue Manufacturing in India,” e3s-conferences.org. Government regulations against single-use plastics further support the adoption of biodegradable alternatives. The diversification into alternative fibers reduces dependence on volatile wood pulp markets. Bamboo cultivation requires minimal water and pesticide usage compared to traditional forestry operations. As alternative fiber processing technologies mature, manufacturing cost benefits emerge. AFRY reports that manufacturers are investigating recovered paperboards and alternative virgin fibers to address increasing input costs. The transition requires significant capital investment and technical validation, resulting in a multi-year implementation timeline for equipment modifications and supply chain partnerships.

Sustainability and eco-friendly trends

Environmental compliance requirements are increasing across major markets, with California's emissions trading system affecting tissue manufacturers and indicating potential nationwide carbon cost implementation that may alter competitive dynamics. Life cycle assessment studies show that disposable facial tissues have 5 to 7 times lower environmental impact than reusable cotton handkerchiefs in climate change, human health, ecosystem quality, and resource categories, challenging traditional sustainability perceptions. The Green Seal GS-1 standard for sanitary paper products sets certification requirements that guide institutional purchasing decisions, creating market advantages for compliant products[3]Source: Green Seal, “GS-1 Sanitary Paper Products,” greenseal.org. Regional variations exist in consumer willingness to pay sustainability premiums, with European and North American consumers showing higher acceptance of certified eco-friendly product pricing compared to emerging markets, where product functionality and cost remain the primary purchase factors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility and supply shocks | -0.9% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Competition from reusable alternative | -0.4% | Europe and developed markets, expanding globally | Medium term (2-4 years) |

| Environmental concerns and waste management | -0.3% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Stringent and varied environmental regulations | -0.5% | Europe leading, North America following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw material price volatility and supply shocks

Fluctuating pulp prices create margin pressures that require manufacturers to adjust prices frequently, affecting long-term contracts and customer relationships throughout the value chain. The price difference between hardwood and softwood pulp remains substantial, with hardwood gaining market share due to softwood's rising costs and environmental constraints. This shift influences traditional fiber blend compositions. Supply chain vulnerabilities emerged from geopolitical events and labor strikes, highlighting risks of concentrated regional production. US fiber prices doubled from 2023 levels, indicating fundamental changes in raw material availability. This situation requires companies to diversify their sourcing strategies and optimize inventory management to maintain operations.

Environmental concerns and waste management

The limitations of waste management infrastructure in developing markets create disposal challenges, leading to environmental issues that may prompt regulatory restrictions on single-use products. Municipal waste systems face difficulties managing increasing tissue towel volumes, especially in urban areas where limited landfill capacity and inadequate recycling infrastructure cause environmental strain. Environmental advocacy groups conduct consumer awareness campaigns focusing on tissue products' environmental impact, promoting recycled-content alternatives and reduced consumption, which may affect long-term demand. The concern over ocean plastic pollution extends to tissue packaging, creating demand for biodegradable wrappers that increase production costs and may affect product protection during distribution. The implementation of climate change regulations and carbon pricing mechanisms could significantly impact tissue manufacturing due to its energy-intensive production processes and the transportation requirements of bulky, low-value-density products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Roll Towels Lead Despite Center-Pull Innovation

Roll towels command 42.11% market share in 2024, maintaining dominance through established infrastructure compatibility and cost-effective dispensing solutions across commercial and residential applications. Their market position is strengthened by universal dispenser compatibility and bulk purchasing advantages that appeal to institutional buyers. Center-pull variants show the highest growth rate at 4.23% CAGR through 2030, due to efficient dispensing that reduces waste and improves hygiene compliance in high-traffic facilities. These products prevent cross-contamination through single-sheet dispensing, making them essential for healthcare and food service environments with strict hygiene requirements.

Folded towels serve specialized applications where pre-folded convenience supports premium pricing, particularly in upscale hospitality and executive washrooms. This segment benefits from portion control and aesthetic presentation that meets high-end facility requirements. Manufacturers focus on improving absorption and dispensing reliability through embossing technologies and multi-layer construction to enhance performance per unit cost. BW Converting's VENTUS-TI interfolder technology enables high-speed production of folded tissue products, while INVISIBLE-O technology supports coreless product development, reducing packaging waste and transportation costs.

By End-User: Commercial Dominance Faces Residential Acceleration

The commercial segment holds 58.43% market share in 2024, driven by institutional purchasing across healthcare, hospitality, and office environments. The segment's strength comes from regulatory requirements for single-use products in hygiene-critical applications, resulting in consistent demand that is less sensitive to price changes than residential use. Away-from-home facilities maintain strict hygiene protocols that have become standard practice. Healthcare and food service sectors show strong demand, with facilities adopting high-capacity dispensing systems to reduce maintenance needs and ensure product availability.

The residential segment grows at a 4.65% CAGR, driven by consumers' increased focus on home hygiene and convenience. Post-pandemic consumption patterns remain elevated, with 40% of consumers maintaining higher kitchen paper towel usage. Consumers show preferences for smaller pack sizes and private-label options, balancing cost considerations with performance requirements. Remote work arrangements and increased home activities create ongoing residential demand. The segment shows greater openness to innovation, with consumers more likely to try new formats and sustainable options that match their values and lifestyle needs.

By Material: Virgin Pulp Supremacy Challenged by Recycled Growth

Virgin pulp holds a 65.08% market share in 2024, due to its superior absorption, strength, and processing consistency across quality-sensitive applications. The material's market position remains strong through established supply chains and manufacturing processes optimized for virgin fiber, creating significant switching costs despite increasing sustainability pressures. Recycled fiber alternatives show a 5.06% CAGR through 2030, supported by cost optimization needs and sustainability regulations. The market dynamics are influenced by the price difference between hardwood and softwood pulp, with hardwood currently dominating due to higher costs and environmental concerns in softwood production.

Mixed pulp formulations provide balanced performance for mid-tier applications. These blends enable manufacturers to adjust fiber composition according to material availability and price fluctuations while maintaining product quality. The industry is witnessing increased adoption of alternative fibers, particularly bamboo and bagasse. Research shows bamboo fibers deliver higher liquid absorbency capacity with enhanced porosity levels. While alternative fibers help reduce dependence on volatile wood pulp markets, their implementation requires significant capital investment for equipment modifications and technical validation. This material diversification reflects the industry's shift toward sustainable sourcing and operational flexibility, balancing environmental requirements with economic feasibility.

Geography Analysis

Asia-Pacific holds a 35.21% market share in 2024, establishing itself as the dominant region in the tissue towel market. This position stems from its role as both the largest consumer and the primary manufacturing center. The region's growth is driven by urbanization and expanding middle-class populations in China, India, and Southeast Asian nations. Manufacturing advantages include lower labor costs and readily available raw materials. China's real estate sector fluctuations affect wood demand, creating volatility in pulp markets and regional pricing. South Korea's market shows significant import reliance. Emerging economies continue to show strong demand due to infrastructure development and increasing hygiene awareness.

The Middle East and Africa region is expected to grow at a 4.89% CAGR through 2030. This growth is supported by infrastructure development, hospitality sector expansion, and increasing hygiene awareness in markets with below-average tissue towel adoption. The tourism recovery has increased demand through hotels and restaurants, with international hospitality brands implementing standardized hygiene protocols. Healthcare facility expansion and modernization include high-capacity dispensing systems, while regulations increasingly favor disposable over reusable products. In South America, Brazil's significant pulp production provides cost advantages for local tissue manufacturing, while regional trade agreements create export opportunities.

North America and Europe, as mature markets, exhibit established consumption patterns and strict environmental regulations. The European Union's Deforestation Regulation (EUDR) requires stringent sourcing standards, increasing demand for recycled materials. North American tissue demand has returned to pre-pandemic levels, supported by increased mobility and sustained commercial consumption. California's emissions trading system affects tissue manufacturers and indicates potential future carbon cost regulations. These markets show reduced price sensitivity and higher willingness to pay for sustainable products compared to emerging markets, where cost and functionality remain key purchasing factors.

Competitive Landscape

The tissue towel market exhibits moderate fragmentation with a score of 5 out of 10, indicating balanced competition between established multinational players and regional specialists who compete through operational scale, brand recognition, and distribution network advantages. Recent consolidation activities reshape competitive dynamics through acquisitions and joint ventures. These strategic moves reflect industry recognition that scale economies and geographic diversification provide competitive advantages in managing raw material volatility and regulatory compliance costs.

Private label brands are gaining market share as they demonstrate a better ability to manage cost fluctuations compared to branded products. Consumers are increasingly choosing private-label tissue products due to inflationary pressures. Manufacturers are focusing their technology investments on operational efficiency and sustainability rather than product differentiation. They are implementing digital solutions and AI integration to optimize production processes and reduce greenhouse gas emissions.

The market presents growth opportunities in alternative fiber applications and emerging markets, where established companies can use their manufacturing expertise and distribution networks to expand in underserved regions. Small companies target specialized applications and sustainable products. The industry's competitive landscape has matured, with success now depending on operational efficiency, regulatory compliance, and market positioning rather than product innovation.

Tissue Towel Industry Leaders

Sofidel Group

Georgia-Pacific

Essity AB

Kimberly-Clark

Procter & Gamble

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Kimberly-Clark announced a USD 3.4 billion joint venture with Brazilian pulp maker Suzano, creating a global tissue company operating in over 70 countries with 22 manufacturing facilities and approximately 1 million tonnes of annual tissue production capacity. Suzano will hold a 51% stake after paying USD 1.734 billion, while Kimberly-Clark retains 49% ownership in the venture that includes brands like Kleenex, Scott, and Viva across international markets.

- November 2024: Sofidel finalized the acquisition of Clearwater Paper Corporation's tissue division for USD 1.06 billion, positioning itself as the fourth largest tissue paper producer in North America. The transaction includes four U.S. manufacturing facilities and strengthens Sofidel's market presence after more than a decade of North American operations.

- August 2024: Azzurra Capital acquired a strategic stake in Pasfin S.p.A., the holding company controlling Lucart S.p.A., a leading European manufacturer of tissue, airlaid, and MG paper products.

Global Tissue Towel Market Report Scope

| Roll Towels |

| Folded Towels |

| Center-Pull/Hardwound |

| Residential |

| Commercial |

| Virgin Pulp |

| Recycled Fiber |

| Mixed Pulp |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | South America |

| Brazil | |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Roll Towels | |

| Folded Towels | ||

| Center-Pull/Hardwound | ||

| By End-User | Residential | |

| Commercial | ||

| By Material | Virgin Pulp | |

| Recycled Fiber | ||

| Mixed Pulp | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | South America | |

| Brazil | ||

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the tissue towel market in 2025?

The tissue towel market size reached USD 32.54 billion in 2025 and is projected to grow to USD 38.76 billion by 2030.

Which region currently leads global demand?

Asia-Pacific holds the largest 35.21% share of global consumption owing to rapid urbanization and robust manufacturing capacity.

What is driving faster growth in the Middle East and Africa?

The Middle East and Africa market is expected to grow at a CAGR of 4.89% through 2030, driven by infrastructure expansion, hospitality sector development, and increased hygiene awareness.

Which product format is expanding the quickest?

Center-pull towels are registering the fastest 4.23% CAGR due to single-sheet dispensing that minimizes waste.

Page last updated on: