Sleepwear and Loungewear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

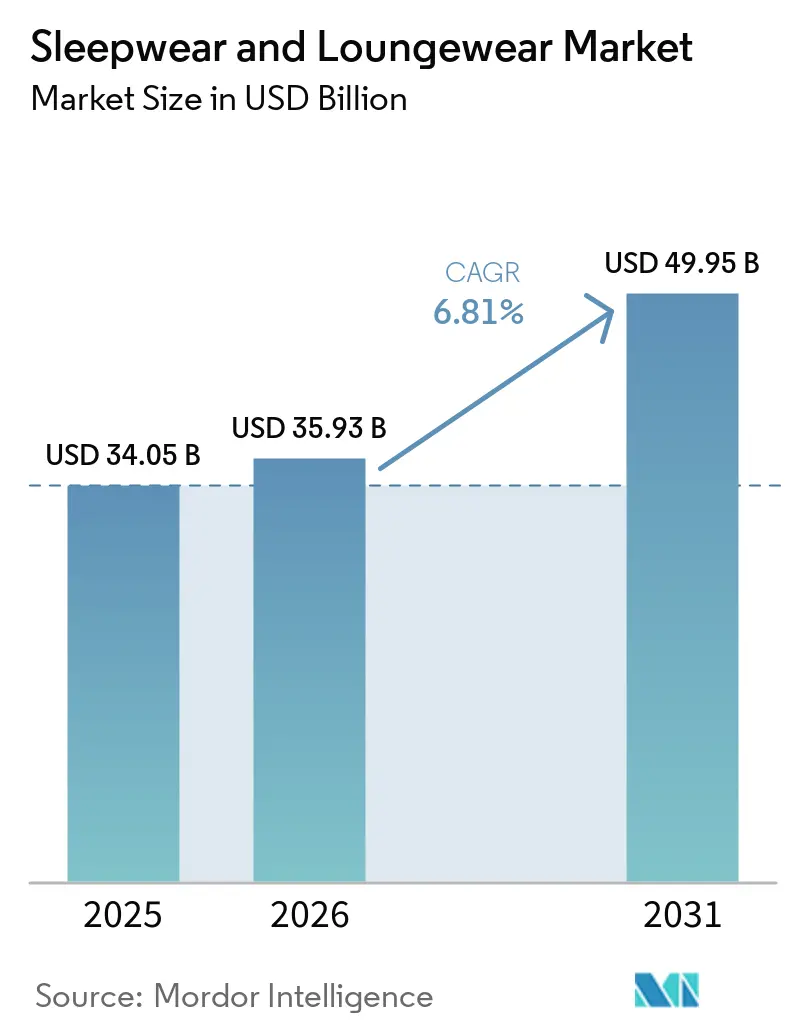

| Market Size (2026) | USD 35.93 Billion |

| Market Size (2031) | USD 49.95 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

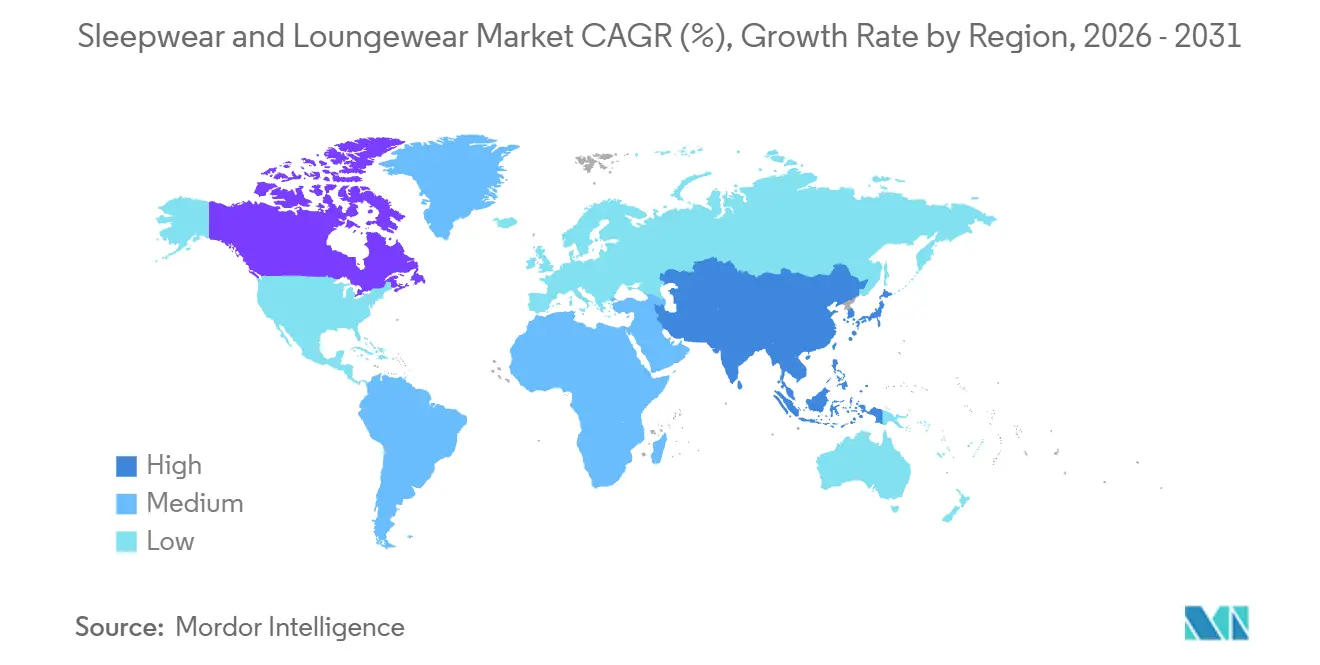

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sleepwear and Loungewear Market Analysis by Mordor Intelligence

The sleepwear and loungewear market, valued at USD 34.1 billion in 2025, is projected to reach USD 49.9 billion by 2031, growing at a CAGR of 6.8% from 2026 to 2031. Hybrid work patterns have increased time spent at home, boosting demand for comfort-led clothing and expanding its use beyond nighttime. As sleep health becomes a priority, consumers are willing to invest in products that enhance comfort, recovery, and rest. This shift has driven acceptance of premium fabrics, better designs, and improved silhouettes, benefiting brands that focus on quality, safety, and sourcing. The market now aligns more with wellness and casual apparel, moving away from occasional gifting, resulting in stable repeat purchases across consumer groups. However, rising textile and logistics costs due to geopolitical disruptions pose a challenge, particularly for blended and polyester-heavy materials.

Key Report Takeaways

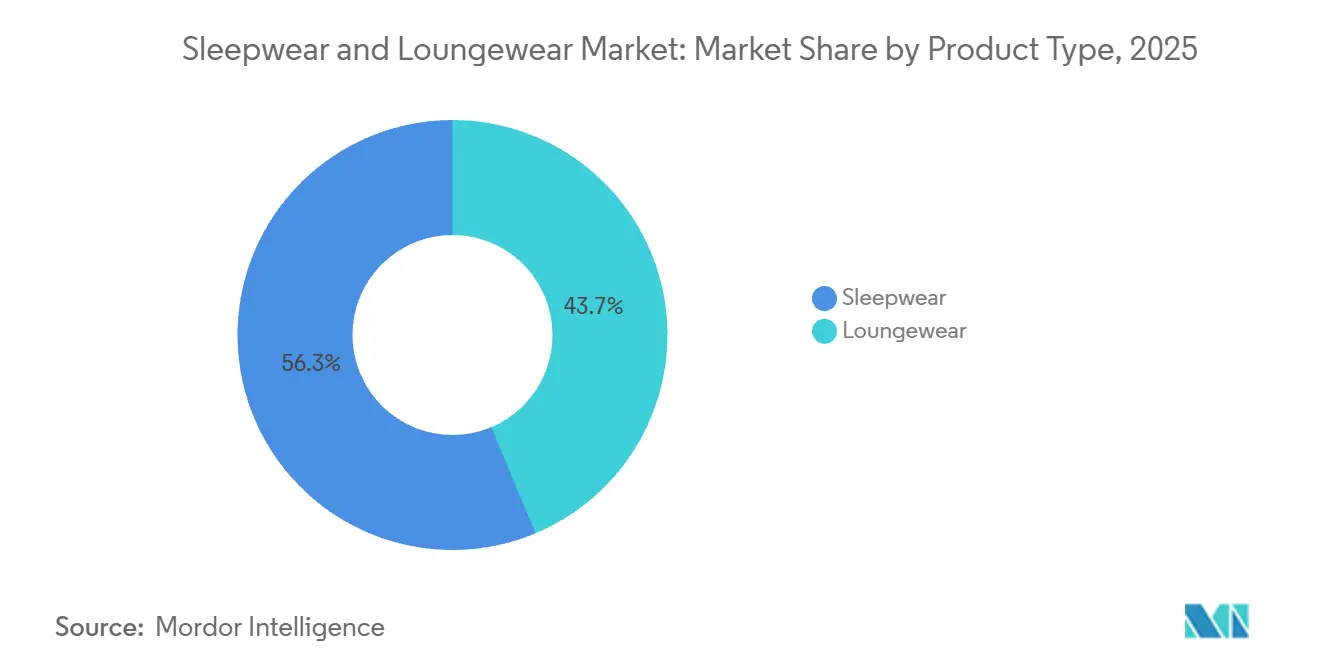

- By product type, sleepwear held 56.3% of market value in 2025, while loungewear is projected to expand at an 8.18% CAGR through 2031.

- By material, cotton accounted for 43.3% of market value in 2025, while bamboo is forecast to grow at a 7.98% CAGR through 2031.

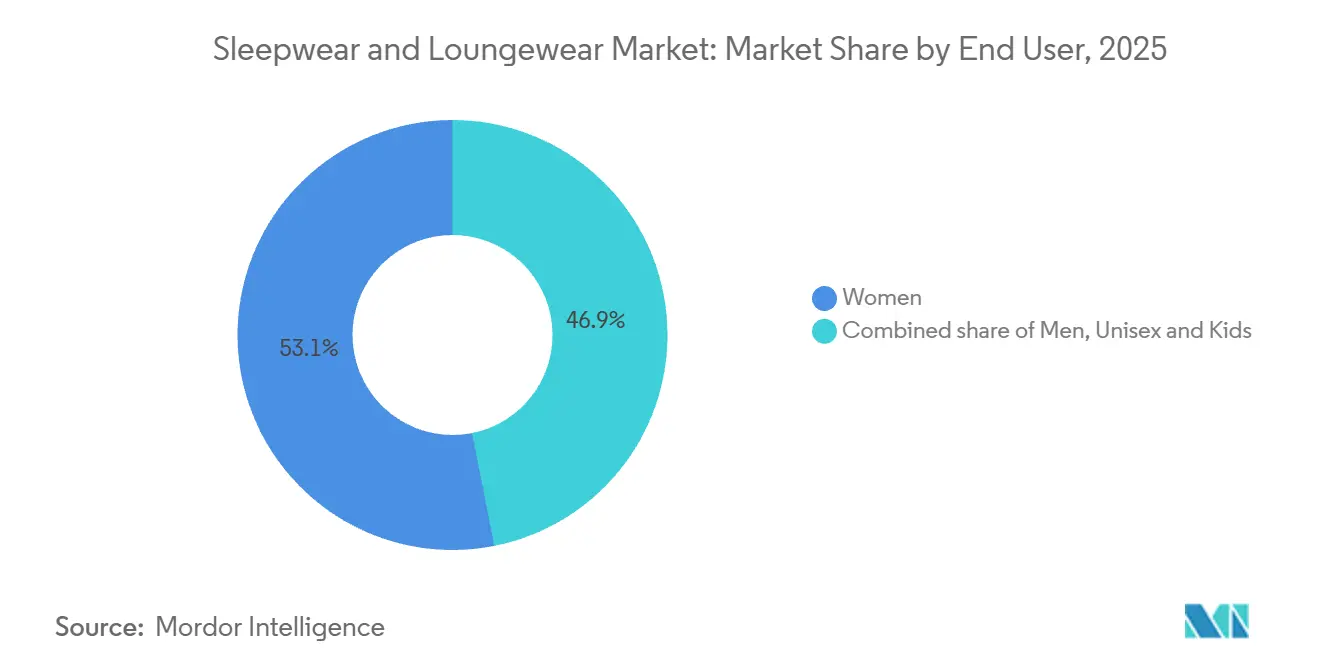

- By end user, women represented 53.1% of market value in 2025, while kids are projected to advance at a 8.45% CAGR through 2031.

- By distribution channel, online retail captured 38.5% of market value in 2025, while supermarkets and hypermarkets are expected to rise at a 7.95% CAGR through 2031.

- By geography, North America held 35.3% of the sleepwear and loungewear market share in 2025, while Asia-Pacific is projected to grow at a 9.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sleepwear and Loungewear Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remote Work And Telecommuting Lifestyle Shifts | +1.4% | North America, Europe, APAC urban centers | Short term (≤ 2 years) |

| Growing Focus On Sleep Wellness And Comfort | +1.2% | Global, strongest in North America and China | Medium term (2-4 years) |

| Sustainable And Eco-Friendly Material Preferences | +0.9% | Europe, North America, emerging in APAC | Medium term (2-4 years) |

| Fabric Innovation And Temperature-Regulating Materials | +0.8% | Global, led by North America and APAC R&D hubs | Long term (≥ 4 years) |

| Social Media And Digital Platform Influence | +0.6% | Global urban centers with high smartphone penetration | Short term (≤ 2 years) |

| Demand For Inclusive Sizing And Minimalist Aesthetics | +0.4% | North America, Europe, growing in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Remote Work and Telecommuting Lifestyle Shifts

As hybrid work becomes the norm, it's reshaping how consumers approach dressing at home and on less formal workdays, benefiting the sleepwear and loungewear market. A survey conducted in June 2025 by the International Workplace Group revealed that 92% of U.S. hybrid workers value clothing that seamlessly transitions between work and leisure. Furthermore, 31% of respondents emphasized the importance of garments suitable for the office, home, and relaxation, indicating a shift towards a demand for refined comfort over merely functional nightwear. This evolution has carved out a broader daytime loungewear niche, positioned between traditional pajamas and casual wear. This niche is particularly significant for brands that already straddle the line between sleepwear and athleisure. Consequently, the sleepwear and loungewear market is not only seeing an uptick in regular wear cycles but is also expanding its role in wardrobes, moving beyond its previous association with gifting.

Growing Focus on Sleep Wellness and Comfort

The growing connection between sleep quality and wellness is driving the sleepwear and loungewear market. According to a 2025 survey by the American Academy of Sleep Medicine, 55% of U.S. consumers aged 18 to 44 spent between USD 100 and USD 500 on sleep-related products in the previous year[1]Source: American Academy of Sleep Medicine, “Sleep Prioritization Survey 2025: Consumer Spending on Sleep Products”, aasm.org. Younger adults were particularly willing to spend over USD 100, showing that premium sleep products are becoming a regular part of their discretionary spending. Additionally, the Global Wellness Institute reported that hospitality operators are enhancing sleep programs with environmental design and coaching, reflecting the rising importance of sleep optimization in consumer culture. This trend boosts the demand for features like moisture control, thermal balance, and skin comfort in sleepwear and loungewear, making premium fabric performance more justifiable at retail.

Sustainable and Eco-Friendly Material Preferences

In the sleepwear and loungewear market, there's a notable shift towards materials with credible sustainability credentials, particularly in premium and family-oriented product lines. Bamboo and organic cotton are reaping the rewards, resonating with consumers' preferences for softness, eco-friendly sourcing, and product safety. USDA data highlighted that global cotton consumption is projected to hit 118.1 million bales in 2025/26, marking a five-year peak. This underscores cotton's entrenched role in textile demand, even as fabric preferences evolve[2]Source: U.S. Department of Agriculture, “Cotton and Wool Outlook, April 2026”, usda.gov. Concurrently, brands in the sleepwear and loungewear sector are being rewarded for certified sourcing and transparent fabric claims, as mere sustainability claims fall short in premium markets. This shift is propelling bamboo, once seen as a niche wellness material, into the spotlight as a mainstream growth driver.

Social Media and Digital Platform Influence

The sleepwear and loungewear market is increasingly shaped by social platforms that influence discovery, preference, and purchase timing. Peer-reviewed research published in 2025 found that both brand-generated and user-generated social content can materially influence fashion purchase intention, with engagement serving as an important mediator. That matters because comfort apparel is highly visual in coordinated sets, fabric drape, and lifestyle presentation, which makes it well suited to short-form content and creator-led merchandising. Public sharing of cozy and at-home style routines has also increased the aspirational value of items that were once treated as private basics. As a result, the sleepwear and loungewear market is seeing faster conversion from inspiration to purchase, especially where brands pair strong visuals with direct checkout pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Disruptions Affecting Timely Delivery | -1.2% | Global, most acute for Asia-sourced brands | Short term (≤ 2 years) |

| Competition From Alternative Apparel Categories | -0.7% | Global, driven by athleisure and fast fashion | Medium term (2-4 years) |

| Consumer Price Sensitivity In Price-Sensitive Markets | -0.5% | South Asia, Southeast Asia, Latin America, MEA | Medium term (2-4 years) |

| Counterfeit Products Undercutting Authentic Brands | -0.3% | Global, concentrated in South and Southeast Asia and online marketplaces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions Affecting Timely Delivery

In 2026, the sleepwear and loungewear market grappled with significant supply pressures, largely due to geopolitical disruptions affecting textile and shipping flows. According to the Business and Human Rights Resource Centre, ship transits through the Strait of Hormuz plummeted by 97% post late February 2026. Concurrently, all four major container lines halted their operations in the region. The Centre also highlighted a doubling of bunker fuel costs and a projected 10% to 15% surge in global textile production costs. Notably, polyester-linked supply chains bore the brunt of these increases. This is particularly consequential for the sleepwear and loungewear market, as mass-market loungewear heavily relies on polyester and blended fabrics. Any delivery delays can lead to markdowns, especially if seasonal goods arrive late. Consequently, retailers exhibit diminished confidence in reorders and face tighter margins in price-sensitive product tiers.

Counterfeit Products Undercutting Authentic Brands

As social commerce and marketplace models expand access to imitation products, the sleepwear and loungewear market grapples with the challenge of counterfeit apparel. The Anti-Slavery Collective projected that in 2025, the global trade in counterfeit goods would be valued at a staggering USD 550 billion, with fake fashion accounting for a significant 63% of that figure. Highlighting the gravity of the issue, the American Apparel and Footwear Association revealed in 2026 that a concerning 41% of tested counterfeit apparel, footwear, and accessory items did not meet U.S. and international safety standards. This concern is magnified in children’s sleepwear, where adherence to safety and flammability standards is paramount for maintaining brand trust and gaining retail acceptance. In light of these challenges, brands in the sleepwear and loungewear sector that prioritize digital authentication, vigilant marketplace monitoring, and traceable sourcing are positioning themselves to uphold premium pricing and bolster consumer confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sleepwear Anchors Value, Loungewear Leads Growth

In 2025, sleepwear commanded a dominant 56.32% share of the global market value, solidifying its top position in the sleepwear and loungewear sector. This prominence can be attributed to its close ties with gifting cycles, household replenishments, and its appeal across various age groups. The segment's strength lies in its diverse sub-categories, including pajama sets, nightgowns, robes, sleep tops, and bottoms. This variety enables retailers to curate a year-round assortment without being tethered to a singular silhouette. Such depth fosters repeat purchases, especially in women's and children's lines, where holiday collections and family matching themes consistently drive demand peaks. Highlighting the segment's vitality, Victoria’s Secret & Co. reported an 8% growth in comparable sales for Q4 of fiscal 2025, singling out sleepwear as a standout category. This underscores how brand allure and social sharing can maintain premium pricing in a saturated apparel market.

Loungewear is set to surge at a robust 8.18% CAGR through 2031, emerging as the fastest-growing segment in the sleepwear and loungewear market. Consumers are increasingly adopting joggers, leggings, hoodies, and soft separates for both home and casual outings. The appeal of loungewear lies in its versatility, straddling the line between relaxation wear and everyday essentials, thus catering to a broader spectrum of weekly clothing needs. HanesBrands recognized this trend, launching 'Hanes Moves' in March 2025, an athleisure line tailored for comfort-driven, all-day wear. As loungewear's popularity surges, it's attracting heightened competition from activewear and fast-fashion brands, intensifying the industry's focus on fabric quality, brand identity, and consistent fit execution.

By Material: Cotton Maintains Volume Lead, Bamboo Accelerates on Credentials

In 2025, cotton held a 43.33% share of the global market value, reinforcing its key role in the sleepwear and loungewear sectors. Consumers prefer cotton for its breathability and ease of care across both mass and premium price tiers. Its qualities also make it ideal for children's products and family collections, where softness and wash durability are crucial. The USDA reported global cotton mill usage at 118.1 million bales in 2025/26, a five-year high, highlighting strong demand across textile applications. Cotton remains the primary material, even as brands explore specialized performance and sustainability features.

Bamboo is projected to grow at an 7.98% CAGR through 2031, making it the fastest-growing material in the sleepwear and loungewear market. Premium buyers value bamboo for its softness, moisture management, and modern sustainability appeal. As its price premium becomes more acceptable, bamboo is expanding in categories focused on rest and skin comfort. Hanes emphasized this trend with its SuperSoft Originals line, using viscose-from-bamboo fabric to promote enhanced comfort in basics. To maintain bamboo's premium status, brands must ensure clear communication about processing methods and sourcing quality, avoiding its perception as a passing trend.

By End User: Women Drive Value, Kids Lead Growth

In 2025, women accounted for 53.12% of the global market value, maintaining their position as the leading end-users in the sleepwear and loungewear sector. Their frequent purchases and faster style updates surpass other demographics. Coordinated sets, seasonal launches, and blending nightwear with upscale home dressing ensure women's products dominate shelf space and digital assortments. Victoria’s Secret & Co. demonstrated the impact of strong sleepwear positioning by reporting notable category performance in fiscal 2025, driving broader customer engagement. While men's demand remains smaller, a study by the American Academy of Sleep Medicine found 20% of men aged 18 to 34 spent USD 200 to USD 500 on sleep products, indicating untapped premium demand rather than low interest.

Kids are projected to grow at an 8.45% CAGR through 2031, making them the fastest-growing end-user segment in the sleepwear and loungewear market. Parents prioritize safety, softness, and familiar licensed designs for children. As kids quickly outgrow sizes, the category benefits from repeat purchases. Franchise or character-driven styles often lead to direct requests instead of simple replacements. Safety concerns, more critical in children's apparel than in other categories, strengthen established brands with compliant sourcing and testing. Hanna Andersson’s December 2025 collaboration with Oeuf highlighted how children's sleepwear can boost adult purchases through family-focused designs and coordinated sets.

By Distribution Channel: Digital Leads, Mass Retail Accelerates

In 2025, online retail captured 38.54% of the global market value, establishing itself as the dominant channel in the sleepwear and loungewear sector. This trend is largely attributed to the category's inherent digital nature, where activities like gifting, browsing, and style discovery thrive online. The online platform proves particularly advantageous for coordinated sets and repeat purchases, especially among younger shoppers who seamlessly transition from viewing content to making a purchase, often bypassing physical stores. The influence of social content amplifies this online advantage. Comfort apparel, being visually driven, benefits immensely from styling showcases, presentations led by creators, and direct endorsements. Supporting this trend, research from Frontiers in Communication highlights the tangible impact of social media content on shaping fashion purchase intentions.

Supermarkets and hypermarkets are set to expand at an 7.95% CAGR through 2031, emerging as the quickest-growing avenue in the sleepwear and loungewear market. This surge is due to mass retailers positioning comfort clothing alongside household essentials during routine shopping trips. Such positioning is significant, as items like sleepwear and basic loungewear often follow the same replenishment patterns as bedding, personal care products, or seasonal home goods. Moreover, this channel appeals to value-conscious households that might not frequent specialty apparel stores but still purchase comfort-driven essentials during their weekly shopping. For brands, the rapid growth in mass retail not only presents a broader distribution opportunity but also intensifies scrutiny on pricing strategies, packaging decisions, and merchandising practices.

Geography Analysis

In 2025, North America held 35.31% of the global sleepwear and loungewear market, driven by the strong presence of branded comfort apparel in the U.S. and Canada. The region benefits from a solid direct-to-consumer network, high apparel spending, and a concentration of established sleepwear and intimate brands, supporting premium and mid-market sales. The U.S. leads with brand-focused merchandising, extensive digital reach, and frequent seasonal updates, while Canada boosts demand for certified, comfort-driven products in urban retail, favoring premium fabrics and ethical sourcing. Despite slower growth than Asia-Pacific, North America remains the key value hub in the market.

Europe ranked as the second-largest region in 2025, with Germany, the UK, France, Italy, and Spain driving demand. The UK stands out, as Marks & Spencer reported in April 2026 that it sells a bra every two seconds and serves one in three women for underwear and sleepwear, highlighting its dominance in related categories. Europe’s regulatory influence pushes brands toward better traceability, consistent certifications, and clear fabric standards. South America and the Middle East & Africa are smaller markets but show growth potential due to younger consumers, rising social visibility, and increasing demand for branded comfort apparel.

Asia-Pacific is the fastest-growing region, with a projected 9.25% CAGR through 2031, driven by urban middle-class growth, rising disposable incomes, and e-commerce adoption. China, India, Indonesia, and Vietnam lead this expansion, embracing comfort-focused dressing. lululemon’s December 2025 franchise agreements in India and other markets reflect global brands prioritizing these high-growth regions. Japan and South Korea remain mature, high-value markets favoring technical fabrics and minimalist designs, while Asia-Pacific’s manufacturing base keeps it central to the sleepwear and loungewear supply chain.

Competitive Landscape

The sleepwear and loungewear market is moderately fragmented, driven by brand recognition, product innovation, comfort-focused designs, and expanding omnichannel retail presence. Key players like Victoria’s Secret and Co., Gildan Activewear (Hanesbrands Inc), Hennes and Mauritz AB, PVH Corp., and American Eagle Outfitters Inc. maintain strong positions through diverse product portfolios, established distribution networks, and broad consumer reach. These companies serve various customer segments by offering sleepwear and loungewear across different price points, styles, and fabrics.

Competition focuses on comfort, functionality, and evolving fashion trends, as consumers prefer versatile apparel for relaxation and casual wear. To stand out, companies are expanding collections with sustainable fabrics, inclusive sizing, seasonal designs, and premium comfort features. Digital transformation is also critical, with leading brands investing in e-commerce, direct-to-consumer channels, personalized marketing, and social media to strengthen customer relationships and boost brand visibility.

Strategic product launches, collaborations, and geographic expansion are key growth strategies. Established brands leverage strong brand equity and global retail networks to introduce new collections and meet rising demand for athleisure-inspired loungewear. Meanwhile, regional brands and private-label manufacturers contribute to market fragmentation, driving innovation and price competition. As consumer preferences shift toward comfort-driven fashion and home-centric lifestyles, companies are expected to focus on sustainability, premium products, and omnichannel retail strategies to enhance competitiveness.

Sleepwear and Loungewear Industry Leaders

Victoria’s Secret and Co.

Hennes and Mauritz AB

PVH Corp.

American Eagle Outfitters Inc.

Gildan Activewear

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Aizome has expanded into the apparel segment with the launch of Second Skin, a new collection of sleepwear and loungewear designed using the company's plant-based and sustainably sourced textile materials. The collection aims to provide consumers with comfortable, skin-friendly apparel while extending Aizome's presence beyond its established bedding products.

- June 2026: Wacoal has strengthened its presence in India with the launch of a new 450-square-foot flagship store on Linking Road, Khar West, Mumbai. The store serves as the brand’s flagship retail destination in the country and marks an important step in expanding its footprint, bringing its total number of exclusive brand outlets in India to 18. The flagship outlet is designed to offer Wacoal’s most comprehensive brand experience, featuring an extensive range of premium lingerie, shapewear, sleepwear, and loungewear products.

- June 2025: Four Seasons has expanded its sleepwear portfolio with the launch of the Resort Pajamas Collection. The new collection is inspired by the brand’s luxury resort destinations and is designed to extend the Four Seasons Signature Sleep Experience beyond its properties and into consumers' homes. The Resort Pajamas Collection features Women’s, Men’s, and Unisex linen-cotton pajama sets, created for comfort during warmer seasons.

- May 2025: Ammarzo has entered the premium sleepwear segment with the launch of its first sleepwear and loungewear collection, available through its direct-to-consumer website and Myntra. Crafted from natural fibers such as organic cotton, linen, and modal blends, the range includes pyjama sets, robes, slip dresses, kaftans, and loungewear designed to enhance comfort, sleep quality, and skin wellness. The brand has also expanded into romantic nightwear and bridal sleepwear, offering premium designs featuring silk, satin, lace, embroidery, and other luxury detailing.

Global Sleepwear and Loungewear Market Report Scope

| Sleepwear | Pajama Sets |

| Nightgowns and Sleepshirts | |

| Robes | |

| Sleep Tops | |

| Sleep Bottoms | |

| Others | |

| Loungewear | Hoodies and Sweatshirts |

| Joggers and Sweatpants | |

| Leggings | |

| Shorts | |

| Others |

| Cotton |

| Silk |

| Bamboo |

| Polyester and Blended Fabrics |

| Other Materials |

| Women |

| Men |

| Kids |

| Unisex |

| Supermarkets and Hypermarkets |

| Specialty Stores |

| Department Stores |

| Online Retail |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Sleepwear | Pajama Sets |

| Nightgowns and Sleepshirts | ||

| Robes | ||

| Sleep Tops | ||

| Sleep Bottoms | ||

| Others | ||

| Loungewear | Hoodies and Sweatshirts | |

| Joggers and Sweatpants | ||

| Leggings | ||

| Shorts | ||

| Others | ||

| By Material | Cotton | |

| Silk | ||

| Bamboo | ||

| Polyester and Blended Fabrics | ||

| Other Materials | ||

| By End User | Women | |

| Men | ||

| Kids | ||

| Unisex | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Specialty Stores | ||

| Department Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for sleepwear and loungewear?

The category is projected to reach USD 49.95 billion by 2031 from USD 34.05 billion in 2025, growing at a 6.81% CAGR from 2026 to 2031.

Which product category is growing faster, sleepwear or loungewear?

Loungewear is growing faster at a 8.18% CAGR through 2031, while sleepwear remained larger in 2025 with 56.32% of market value.

Which material is expanding the quickest?

Bamboo is the fastest-growing material at a 7.98% CAGR through 2031, while cotton remained the largest material segment with 43.3% share in 2025.

Which end-user group creates the most value today?

Women generated the largest value share at 53.12% in 2025, supported by higher purchase frequency and stronger seasonal refresh behavior.

Page last updated on: