Treadmill Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

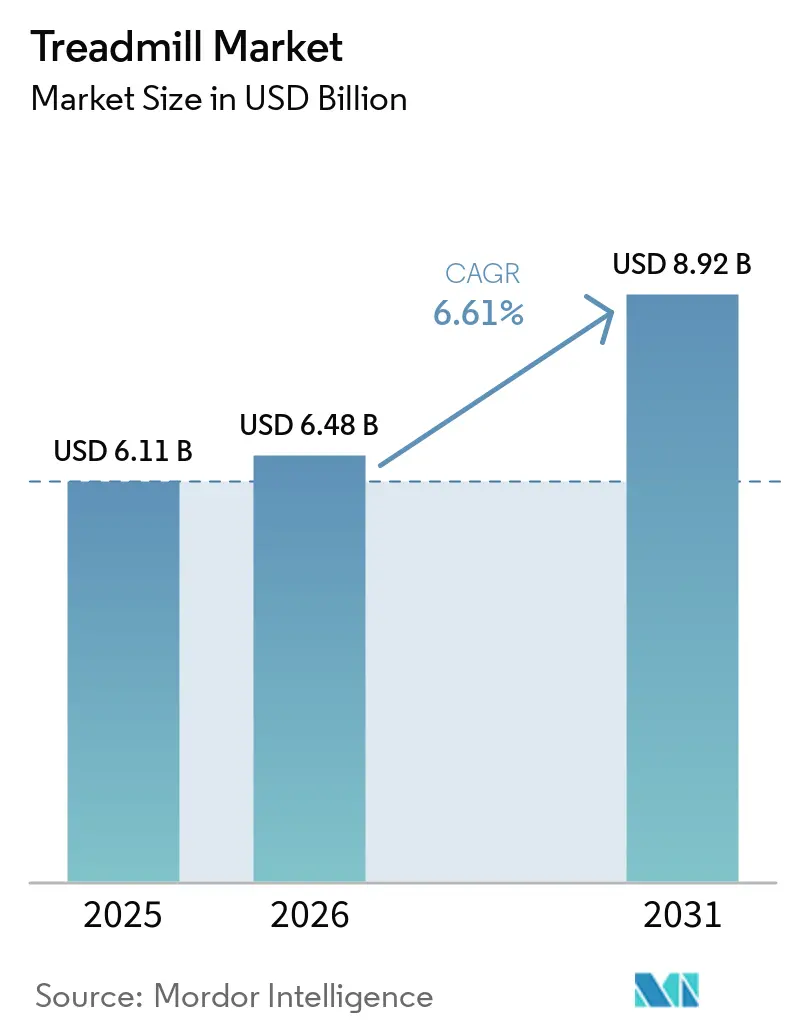

| Market Size (2026) | USD 6.48 Billion |

| Market Size (2031) | USD 8.92 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

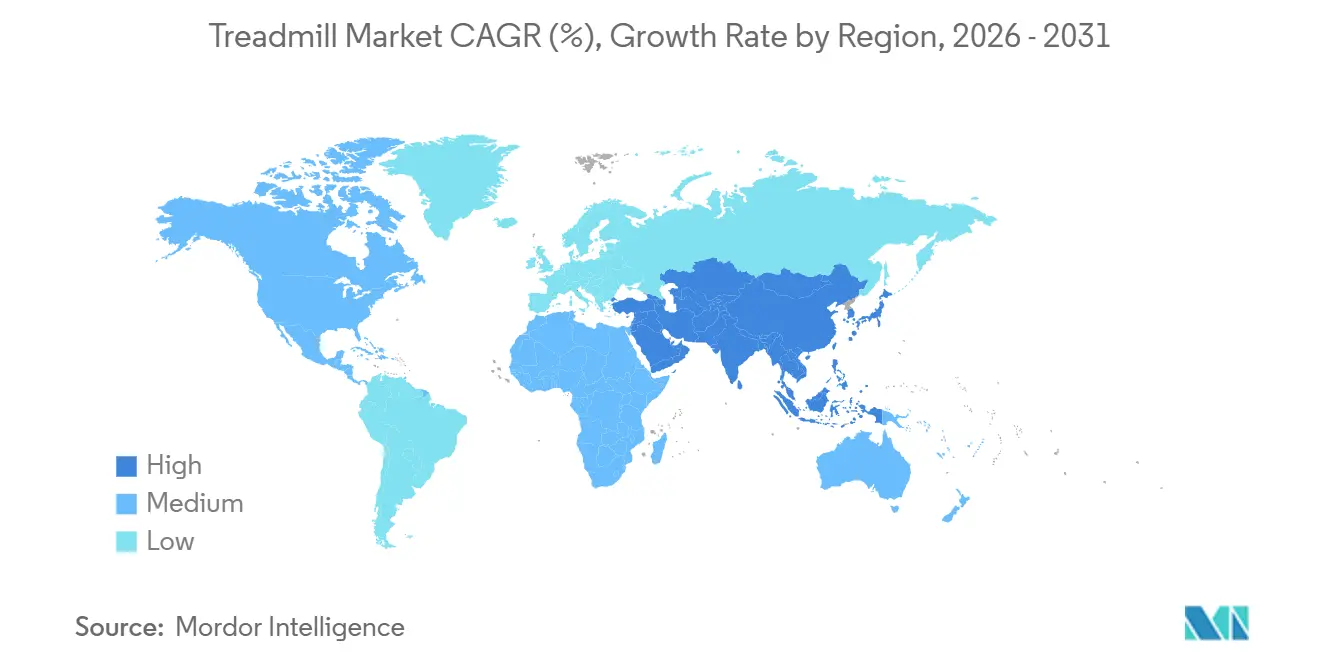

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Treadmill Market Analysis by Mordor Intelligence

The treadmill market size is expected to increase from USD 6.11 billion in 2025 to USD 6.48 billion in 2026 and reach USD 8.92 billion by 2031, growing at a CAGR of 6.61% over 2026-2031. This growth is primarily driven by the rising prevalence of lifestyle-related diseases, continuous technological advancements leading to innovative product upgrades, and government initiatives promoting physical activity. The increasing penetration of smartphones has seamlessly integrated treadmills into digital fitness ecosystems, allowing users to monitor performance metrics, access virtual coaching, and participate in online fitness challenges. While commercial gym construction remains robust, residential adoption is accelerating as consumers seek the convenience of home-based workouts and flexible schedules. To cater to this demand, manufacturers are focusing on developing treadmills with space-saving designs, quieter motors, and affordable financing options to lower entry barriers. Furthermore, supply chains are increasingly shifting towards the Asia-Pacific region to capitalize on cost efficiencies and address the growing demand in this rapidly expanding market.

Key Report Takeaways

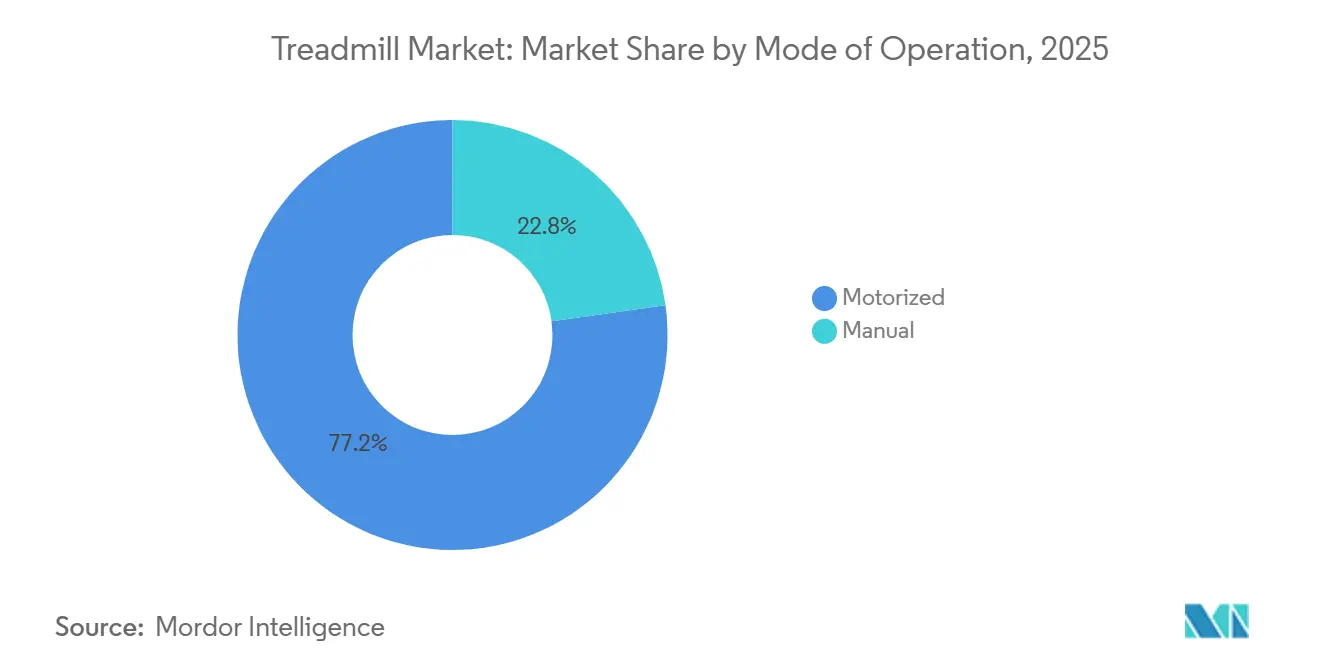

- By mode of operation, motorized treadmills led with 77.21% revenue share in 2025, while manual models are projected to grow at a 7.24% CAGR to 2031.

- By end-user, the commercial segment held 61.29% of the treadmill market share in 2025; the residential segment is forecast to expand at 6.89% CAGR through 2031.

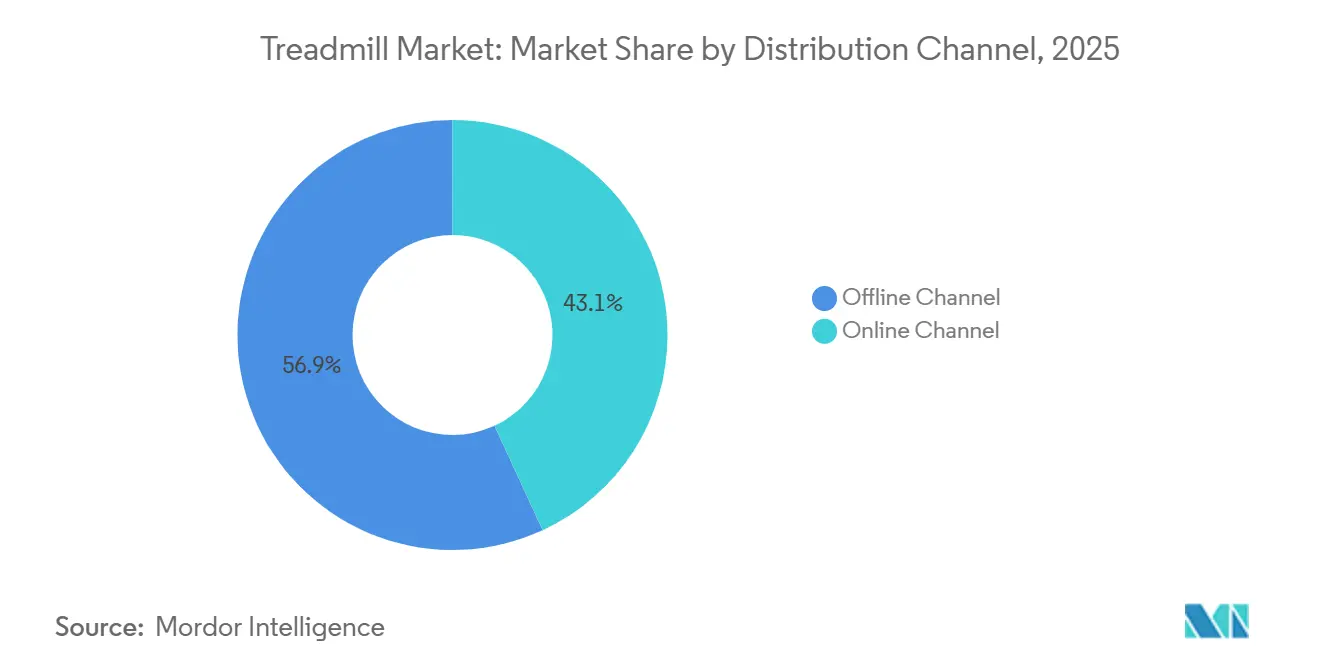

- By distribution channel, offline retail commanded 56.89% share of the treadmill market size in 2025, with online sales poised for a 8.05% CAGR to 2031.

- By geography, North America captured 36.67% of global revenue in 2025; Asia-Pacific is expected to record the fastest 6.74% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Treadmill Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of lifestyle diseases | +1.5% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Integration with fitness apps | +0.8% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Popularity of functional and virtual training | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Government health campaigns | +0.6% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Corporate wellness programs driving equipment demand | +0.5% | Asia-Pacific, Middle East, urban centers globally | Long term (≥ 4 years) |

| Increasing demand for convenient indoor workouts | +0.4% | Asia-Pacific, Middle East and Africa, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of lifestyle diseases

Non-communicable diseases (NCDs) are significantly influencing the demand for fitness equipment. According to the World Health Organization (WHO), NCDs are responsible for 41 million deaths annually, accounting for 71% of global fatalities. In the United States, the Centers for Disease Control and Prevention (CDC) reports that 38.4 million Americans are living with diabetes, with 31.9% of these individuals being physically inactive. This highlights a substantial market opportunity for home fitness solutions. A CDC study, scheduled for release in 2025, analyzed chronic disease trends from 2013 to 2023 and found that 76.4% of adults reported having at least one chronic condition [1]Source: Centers for Disease Control and Prevention, "Trends in Multiple Chronic Conditions Among US Adults, By Life Stage, Behavioral Risk Factor Surveillance System, 2013–2023", cdc.gov. Notably, young adults experienced the steepest increase, with rates rising from 52.5% to 59.5%. The American Heart Association's 2024 Statistical Update reveals that only 24.2% of U.S. adults meet national physical activity guidelines, emphasizing the gap between health needs and current activity levels [2]Source: American Heart Association, “2024 Statistical Update,” heart.org. This growing health crisis is driving investments in accessible fitness solutions. Treadmills, in particular, are becoming a key tool for improving cardiovascular health. A 2024 study by the National Heart, Lung, and Blood Institute (NHLBI) demonstrated that adults at risk for cardiovascular issues increased their daily steps by over 1,500 when participating in structured exercise programs, reinforcing the role of home fitness equipment in preventing diseases.

Integration with fitness apps

Fitness equipment manufacturers are increasingly collaborating with digital platforms, leveraging the convergence of hardware and software to enhance workout experiences. Matrix Fitness has integrated its equipment with Apple GymKit, iFIT, and EGYM, enabling seamless connectivity with existing technologies and improving service delivery for fitness facilities. In November 2024, Technogym expanded its partnership with Garmin, offering enhanced connectivity and personalization for both indoor and outdoor training sessions. SOLE Fitness has partnered with Garmin to deliver real-time biometric data via touchscreen consoles and has integrated with Kinomap to provide geolocated training videos, making indoor workouts more engaging and interactive. The U.S. Health Secretary announced a significant campaign by HHS to promote wearable device adoption, marking one of the largest initiatives in the agency's history, to achieve widespread adoption within four years. In September 2024, iFIT introduced a new lineup of smart equipment featuring an upgraded operating system and AI Coach, reflecting the industry's focus on technological innovation. Peloton Interactive, Inc.'s patent portfolio highlights its technical sophistication, including innovations like treadmills with cushioned decks and systems that adjust exercise machine operations during online gaming, showcasing the advancements driving app integration.

Popularity of functional and virtual training

As the fitness industry pivots towards immersive and functional training, treadmill designs are evolving. Manufacturers are now embedding features that not only mimic real-world running scenarios but also offer interactive coaching. Technogym's Skillrun commercial treadmill boasts speeds reaching 18.6 mph and gradient adjustments from +25% to -3%. It also introduces distinctive training modes, including sled and parachute training, aimed at fostering explosive power. Antonio Citterio's Personal Line for Technogym melds aesthetics with functionality, entertaining and guided workouts via the Technogym Live console. NordicTrack's 2025 models, the X24 and X16, come equipped with a 40% incline and -6% decline, upgraded iFit programming for Netflix and Spotify access, and AI coaching for real-time workout tweaks. Life Fitness, in collaboration with Studio, is rolling out audio group running classes on treadmills, underscoring a trend towards community-centric virtual experiences. The fitness realm is also witnessing a surge in virtual and augmented reality tech adoption. Notably, ISO/IEC 5927:2024 has laid down guidelines for the safe use of AR and VR devices in workplaces, fitness centers included. Peloton Interactive, Inc.'s, Q2 2025 report highlighted a rise in subscription rates for its Tread products, coinciding with the rollout of new software features aimed at boosting user experience and community interaction.

Government health campaigns

Federal and state health initiatives are fostering a supportive environment for the fitness equipment market through policy backing, funding initiatives, and campaigns that raise public awareness about the importance of physical activity. In a move underscoring the government's dedication to public health, President Trump declared May 2025 as National Physical Fitness and Sports Month, urging Americans to prioritize physical activities. In February 2025, the White House launched the President's Make America Healthy Again Commission, a body poised to shape public health policies, potentially bolstering the treadmill market by championing fitness. Backed by the Health and Fitness Association, the Personal Health Investment Today (PHIT) Act proposes that Americans can utilize pre-tax funds from FSAs and HSAs for fitness-related expenses. This means individuals could allocate up to USD 1,000 annually (or USD 2,000 for families) towards fitness equipment and health club memberships. In May 2024, the NIH spotlighted the importance of physical activity, issuing a Notice of Special Interest to promote research on multi-level interventions, especially targeting those less active. The Office of Disease Prevention and Health Promotion is actively seeking input for the upcoming 2028 edition of the Physical Activity Guidelines, underscoring the federal government's sustained commitment to fitness advocacy [3]Source: The Office of Disease Prevention and Health Promotion, "Get Involved: Contribute to the Next Edition of the Physical Activity Guidelines", odphp.health.gov. On an international front, NSW Health in Australia is championing fitness, offering diverse programs and complimentary health coaching services, echoing global governmental endorsement of fitness initiatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial cost limiting mass adoption | -0.8% | Global, particularly emerging markets and price-sensitive segments | Short term (≤ 2 years) |

| Space constraints in small urban households | -0.6% | Urban centers globally, developed markets with abundant fitness infrastructure | Medium term (2-4 years) |

| Competition from gyms and fitness studios | -0.4% | Global, with highest impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Availability of low-cost alternative fitness options | -0.3% | Asia-Pacific urban centers, European metropolitan areas, North American cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High initial cost limiting mass adoption

Market penetration remains constrained by the hefty upfront investment demanded for quality treadmills. This challenge is especially pronounced in price-sensitive segments and emerging markets, where limited disposable incomes shape purchasing choices. Premium offerings, such as NordicTrack's X24 and X16 models, are priced at USD 3,999 and USD 3,499, respectively. Meanwhile, the Commercial 1750 retails for USD 2,499, firmly placing these treadmills in the upper-middle to high-end market brackets. In a notable industry shake-up, BowFlex Inc. declared Chapter 11 bankruptcy in March 2024. The company subsequently offloaded the majority of its assets to Johnson Health Tech for a reported USD 37.5 million, underscoring the financial strains on fitness equipment manufacturers amid fierce pricing competition. Yet, the industry is witnessing the rise of innovative financing models aimed at surmounting these cost hurdles. Notably, Peloton Interactive, Inc.'s, "Fitness-As-A-Service" rental initiative, alongside its "Certified Refurbished" bikes, has made significant waves, accounting for connected fitness hardware sales. This highlights a shift towards alternative market access strategies. In a testament to its commitment to value, Planet Fitness has kept its classic membership rate at a steady USD 10 for three decades.

Availability of low-cost alternative fitness options

The availability of alternative fitness options significantly impacts the global treadmill market by providing consumers with a diverse range of exercise choices beyond traditional treadmills. Options such as stationary bikes, rowing machines, elliptical trainers, and group fitness classes have gained popularity due to their varied workout experiences and lower impact on joints. The rise of boutique fitness studios, outdoor activities, and digital fitness platforms offering interactive and on-demand workouts further intensifies competition for treadmills. As consumers seek more engaging, versatile, and sometimes cost-effective fitness solutions, demand for treadmills can be constrained, especially among younger demographics looking for novelty and community. Additionally, the convenience and accessibility of home workout apps and wearable fitness technology have broadened the appeal of non-treadmill exercise. This diversification in fitness preferences challenges treadmill manufacturers to innovate and differentiate their offerings to maintain market relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Operation: Motorized Dominance Drives Innovation

In 2025, motorized treadmills dominate the market, holding a significant 77.21% share. Motorized treadmills are more in demand due to their ability to provide adjustable speed and incline settings, allowing users to customize workouts for different fitness levels. They offer consistent pacing and smoother motion, reducing the risk of injury compared to manual treadmills. Many models include digital displays, heart rate monitors, and pre-set workout programs, enhancing convenience and motivation. Motorized treadmills save time by simulating outdoor running conditions indoors, which is especially appealing in urban areas with limited outdoor space. They are suitable for both beginners and advanced fitness enthusiasts, making them versatile for home and commercial use. Additionally, the rise in health awareness and busy lifestyles has increased the preference for motorized models that deliver efficient, effective workouts.

Manual treadmills are experiencing the fastest growth, with a projected CAGR of 7.24% through 2031. This growth is driven by cost-conscious consumers, compact designs that save space, and the appeal of self-powered exercise, which eliminates electricity costs. Reflecting ongoing innovation in this segment, Woodway USA secured a patent for its "Manually powered treadmill" in September 2024. The manual treadmill segment attracts minimalist fitness enthusiasts, budget-conscious buyers, and users in regions with unreliable electricity, particularly in emerging markets. Recognizing this demand, SOLE Fitness introduced the SRVO treadmill in August 2024. The revival of manual treadmills aligns with fitness trends emphasizing functional movement and natural running mechanics. Users increasingly appreciate the direct relationship between their effort and speed, a defining feature of manual operation.

By End-User: Commercial Leadership Meets Residential Surge

In 2025, commercial end-users dominate the treadmill market, accounting for 61.29% of sales. This trend underscores the purchasing power of fitness facilities, corporate wellness programs, and institutional buyers, all of whom prioritize durability, advanced features, and high-utilization capacity. Demonstrating this robust commercial demand, Planet Fitness has expanded to 2,722 clubs, with its equipment segment revenue soaring 49.2% to USD 105.1 million in Q4 2024. Manufacturers cater to the commercial segment with bulk purchasing agreements, extended warranty programs, and specialized service support tailored for institutional customers. Technogym, as the Official Supplier for the Paris 2024 Olympic Games, bolstered its brand visibility and commercial credibility.

Residential adoption of treadmills is on the rise, boasting a 6.89% CAGR through 2031. This surge is attributed to the normalization of home fitness, the rise of remote work, and a growing consumer preference for private workout spaces that offer convenience and flexibility. The company asserts that the at-home treadmill market dwarfs that of stationary bikes. The residential segment showcases a demand for space-efficient designs, quiet operation, and aesthetics that harmonize with home décor. This trend is epitomized by Technogym's Personal Line, crafted by Antonio Citterio. SOLE Fitness is also making strides, emphasizing Bluetooth connectivity and seamless integration with the SOLE Fitness App, Garmin devices, and the Kinomap platform to elevate the home workout experience.

By Distribution Channel: Traditional Retail Dominance Meets Digital Disruption

In 2025, offline distribution channels dominate with an 56.89% market share, highlighting the critical role of physical retail in high-consideration purchases. Consumers value hands-on product testing, immediate availability, and personalized sales support. This segment includes franchise stores, specialty fitness retailers, and big-box outlets, which provide essential services such as product demonstrations, financing options, and localized support for treadmill sales. Life Time's shift to an asset-light expansion strategy, focusing on leasing properties instead of owning them, reflects the changing retail landscape while maintaining a strong physical presence. Additionally, the offline segment leverages established relationships with commercial buyers, bulk purchasing agreements, and the ability to offer immediate delivery and installation services, which remain challenging for online channels to replicate.

Online distribution channels are experiencing robust growth, with a 8.05% CAGR projected through 2031. This expansion is driven by the effectiveness of direct-to-consumer strategies, advancements in digital marketing, and increasing consumer confidence in making significant purchases online. The online segment benefits from lower operational costs, a wider geographic reach, and the ability to provide comprehensive product information, customer reviews, and comparison tools that aid in purchase decisions. BowFlex's strong partnership with Amazon.com underscores the importance of major e-commerce platforms in fitness equipment distribution. Furthermore, the online channel continues to evolve with innovations such as virtual reality showrooms, augmented reality product visualization, and enhanced logistics networks, addressing traditional barriers to online fitness equipment purchases.

Geography Analysis

In 2025, North America holds a significant 36.67% market share, characterized by a well-established fitness culture, high penetration of commercial fitness facilities, and strong adoption of home fitness solutions. These factors ensure steady demand for both premium and mid-range treadmill segments. Government health initiatives play a crucial role, including the CDC's "Active People, Healthy Nation" program, which aims to help 27 million Americans increase physical activity by 2027. In 2025, the U.S. Department of Health and Human Services launched the "Take Back Your Health" campaign, a multimillion-dollar initiative promoting physical activity, which is expected to boost the adoption of fitness equipment. Life Time Group Holdings, operating 171 athletic country clubs across the U.S. and Canada, reported total revenue of USD 2.22 billion in 2023 and plans to open 9-10 new centers in 2024. While some market segments face saturation, opportunities exist in underserved demographics and emerging fitness trends that require specialized equipment solutions.

Asia-Pacific is emerging as the fastest-growing region, with a projected CAGR of 6.74% through 2031. This growth is driven by rapid urbanization, increasing disposable incomes, a growing middle class, and heightened health awareness, all of which contribute to substantial demand for fitness equipment across commercial and residential segments. The region's growth is further supported by significant manufacturing investments, such as Johnson Health Tech's USD 100 million investment in Vietnam to establish the world's largest fitness equipment manufacturing center, expected to generate USD 120 million in annual revenue by 2026. China leads global gym equipment production due to its cost-effective manufacturing and strong export infrastructure, while Taiwan is recognized for its precision engineering and high-quality fitness equipment. Government health initiatives across the region, aimed at promoting physical activity and addressing the rising prevalence of lifestyle diseases in urban areas, further drive market growth.

Europe is supported by its advanced fitness infrastructure, high disposable income levels, and strong governmental initiatives promoting health and wellness. The region's leadership is further reinforced by its established fitness culture, preference for premium products, and stringent regulatory frameworks ensuring equipment safety and quality. LifeFit Group's acquisition of SportsUp in Germany and its rebranding as Fitness First Black reflect the growing demand for premium fitness solutions, with the COO noting a significant rise in interest for such offerings post-pandemic. The region benefits from the development of ISO standards, with ISO/TC 83, managed by DIN in Germany, focusing on standardizing sports and recreational equipment to ensure high safety and performance. Despite the market's maturity, Planet Fitness's planned expansion into Spain in 2025 indicates continued growth opportunities within Europe.

Competitive Landscape

The global treadmill market is moderately consolidated, with a handful of key players such as Peloton Interactive, Inc., Life Fitness Inc., Technogym S.p.A., iFIT Inc., Johnson Health Tech Co., Ltd. These companies benefit from strong brand recognition, broad product portfolios, and well-established distribution networks across commercial and residential segments. While there is still room for regional and niche brands, competitive barriers such as high R&D and manufacturing costs limit new entrants. This structure supports consistent innovation and pricing stability, while still allowing some competitive flexibility within emerging markets.

Significant opportunities exist in underserved geographic regions, specialized fitness applications, and the integration of advanced technologies such as AI-driven coaching and virtual reality-based training environments. For example, Greenlite Ventures has partnered with Woodway USA to market simulated altitude chambers and establish altitude fitness centers, showcasing a strategic approach to niche market development.

The rapid adoption of technology is driving competitive differentiation. Matrix Fitness, for instance, has enhanced user experience and facility management by integrating with multiple platforms, including iFIT, and EGYM. The competitive landscape is evolving due to the rise of direct-to-consumer models, subscription-based services, and the convergence of hardware and software platforms. This integration is fostering recurring revenue streams and strengthening customer engagement.

Treadmill Industry Leaders

-

Life Fitness Inc.

-

Technogym S.p.A.

-

iFIT Inc.

-

Johnson Health Tech Co., Ltd

-

Peloton Interactive, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Peloton Interactive, Inc. launched the Repowered resale marketplace for used treadmills, initially available in New York City, Boston, and Washington, D.C., with nationwide expansion planned. According to the brand, the platform offers AI-assisted pricing, 70% seller revenue share, and reduced activation fees for buyers, addressing the 16% year-over-year growth in members purchasing used equipment.

- April 2025: Sunny Health and Fitness has expanded its connected equipment portfolio with the launch of new Wi-Fi-enabled treadmills, designed to deliver an immersive and engaging at-home fitness experience. According to the brand, these treadmills integrate seamlessly with the SunnyFit app, offering users access to thousands of workouts, virtual global routes, real-time health metrics, and professional trainers directly on their TV, all supported by the reliability and stability of Wi-Fi connectivity over Bluetooth.

- March 2025: NordicTrack has expanded its product line with the launch of its new Ultra 1 Luxury Treadmill, a machine featuring a striking architectural design with white oak and metal accents, a cushioned deck that absorbs up to 52% of running impact, and a quiet brushless motor capable of sustaining a four-minute-mile pace.

- January 2025: PitPat and DeerRun launched an innovative fitness equipment series, including multifunctional treadmills, designed for seamless integration with PitPat’s global online competition platform, enabling users to participate in interactive events and track real-time performance data from anywhere. According to the brand, the new product line, available in North America and Europe, emphasizes user experience, advanced connectivity, and anti-cheating technology, with over one million units sold and strong adoption in Europe, the United Kingdom, and Southeast Asia.

Global Treadmill Market Report Scope

The treadmill market refers to the global industry involved in the manufacturing of treadmills for residential (home) and commercial (gym/hospital) use. The Treadmill Market is Segmented by Mode of Operation (Manual, Motorized), End-User (Residential, Commercial), Distribution Channels (Online Retail Stores and Offline Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Manual |

| Motorized |

| Residential |

| Commercial |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Mode of Operation | Manual | |

| Motorized | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the treadmill market?

The treadmill market is valued at USD 6.11 billion in 2025 and is expected to reach USD 8.92 billion by 2031.

Which region holds the largest treadmill market share?

North America leads with 36.67% of global revenue in 2025, supported by mature fitness infrastructure and high purchasing power.

Which region is growing fastest?

Asia-Pacific is projected to register the quickest 6.74% CAGR through 2031 due to urbanization, rising incomes, and government wellness initiatives.

What segment of treadmills is expanding most rapidly?

Manual treadmills are forecast to grow at 7.24% CAGR as budget-minded and electricity-independent users expand the customer base.

Page last updated on: