Asia-Pacific Online Clothing Rental Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

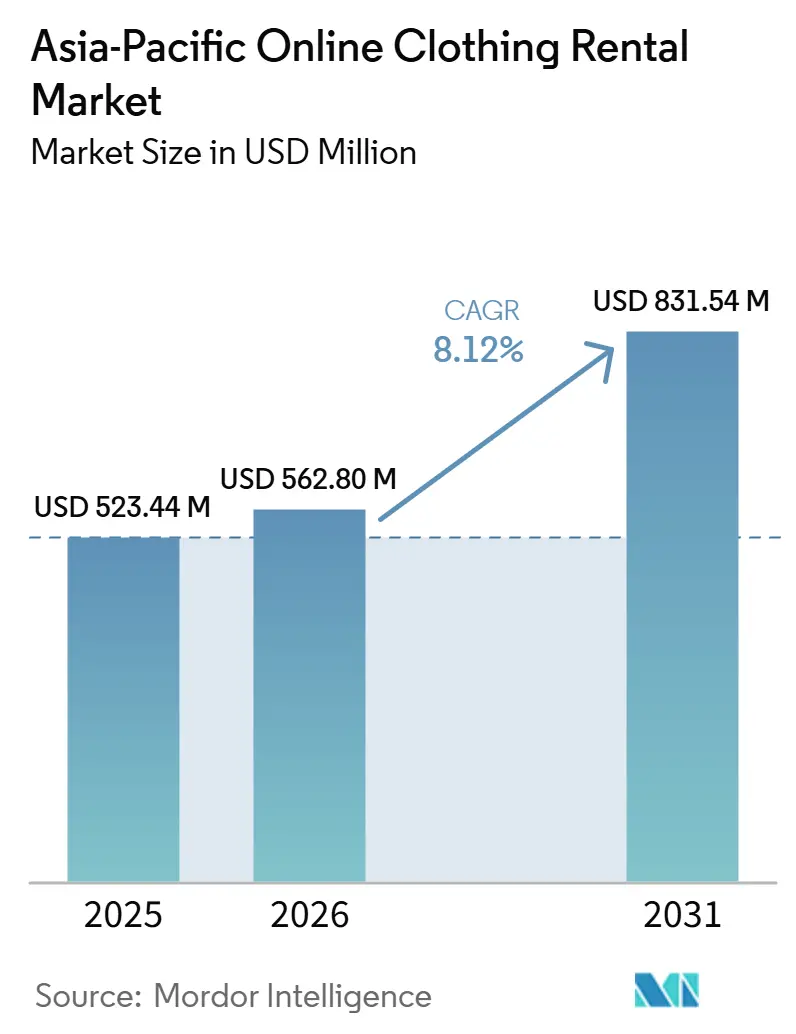

| Base Year Market Size (2025) | USD 523.44 Million |

| Market Size (2026) | USD 562.80 Million |

| Market Size (2031) | USD 831.54 Million |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Online Clothing Rental Market Analysis by Mordor Intelligence

The Asia-Pacific online clothing rental market is expected to grow from USD 523.4 million in 2025 to USD 562.8 million in 2026, and is forecast to reach USD 831.5 million by 2031, at a CAGR of 8.1% over 2026-2031. Rising environmental awareness, wider digital access, and 77% internet penetration in 2025 are driving younger consumers toward renting over owning clothes. Demand is largely occasion-led, driven by weddings, festivals, and corporate events, rather than casual subscriptions. Local operators hold an advantage due to varying language preferences, fit standards, and delivery conditions across countries. Following Style Theory's closure in 2025, premium subscription models face pressure, while peer-to-peer and hybrid models continue to grow. Platforms offering better fit tools, garment-condition transparency, and circular fashion credentials are well-positioned to retain customers as environmental awareness matures across the region.

Key Report Takeaways

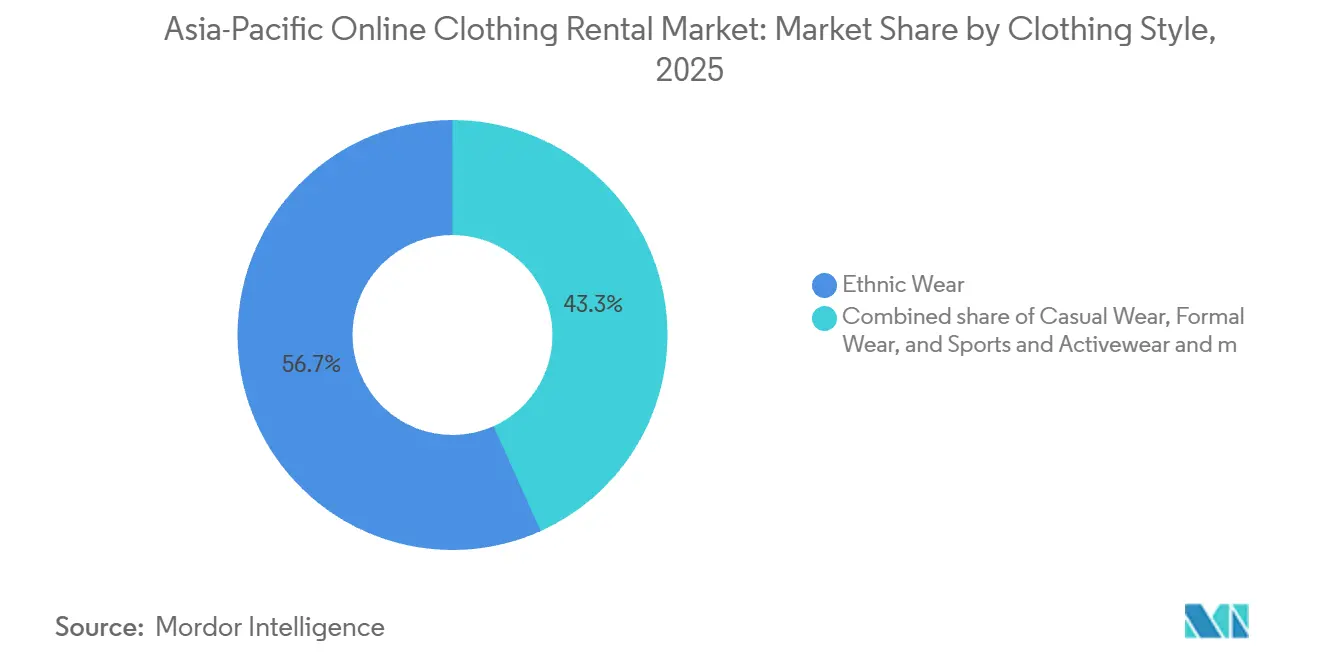

- By clothing style, Ethnic Wear led with 56.7% of the Asia-Pacific online clothing rental market share in 2025, while Sports and Activewear is projected to expand at a 9.4% CAGR through 2031.

- By end user, Women held 65.4% of platform revenue in 2025, while Kids and Teens is forecast to advance at a 9.9% CAGR through 2031.

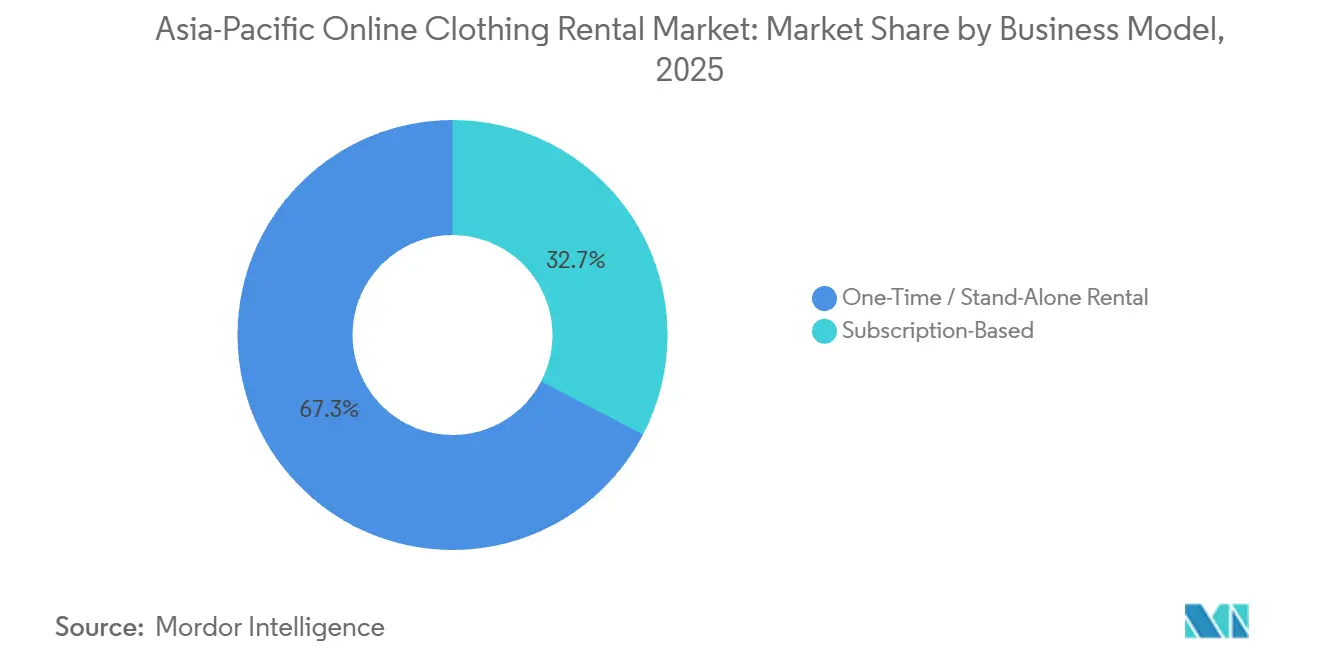

- By business model, One-Time / Stand-Alone Rental accounted for 67.3% of the Asia-Pacific online clothing rental market size in 2025, while Subscription-Based Rental is growing at an 11.1% CAGR through 2031.

- By geography, China held 27.7% share in 2025, while Australia recorded the highest projected CAGR at 10.6% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on online clothing rental market by Mordor Intelligence reflects how these regional layers combine into a single system.

Asia-Pacific Online Clothing Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Awareness of Sustainable Fashion | +1.5% | Global, particularly strong in Japan, Australia, and urban India | Medium term (2-4 years) |

| Growing Environmental Concerns | +1.0% | Global, with fast traction in emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Increasing Internet Penetration | +1.8% | Core Asia-Pacific markets, especially India, Indonesia, and the Philippines | Short term (≤ 2 years) |

| Growth of the Sharing Economy Mindset | +1.2% | China, South Korea, and urban Southeast Asia | Medium term (2-4 years) |

| Influence of Social Media and Fashion Trends | +1.5% | China, Indonesia, Vietnam, and the Philippines, with spillover into India and Thailand | Short term (≤ 2 years) |

| Preference for Convenience and Flexibility | +1.0% | Australia, Japan, Singapore, and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Awareness of Sustainable Fashion

The environmental burden of apparel is making sustainability a direct demand driver for the Asia-Pacific online clothing rental market. In March 2025, the United Nations stated that fashion accounts for up to 8% of global greenhouse gas emissions, and that clothing is discarded at the rate of 1 garbage truck per second[1]Source: United Nations News, “Fast Fashion Fuelling Global Waste Crisis, UN Chief Warns”, news.un.org. That message is pushing rental platforms to position themselves less around savings and more around circular use, especially in Japan and Australia. The Volte's 2025 collaboration with the University of Technology Sydney gave the Australian rental space an academic basis for the environmental value of circular fashion rental. In Thailand, a UNEP-backed fashion initiative in 2025 cut 98,000 kg of CO2 emissions and saved 33 million liters of water, which supports the wider case for rental and reuse in regional fashion systems.

Increasing Internet Penetration

Digital infrastructure remains the clearest structural enabler for the Asia-Pacific online clothing rental market. The region reached 77% internet penetration in 2025, and no other major world region matched its pace of expansion[2]Source: International Telecommunication Union, “Measuring Digital Development, Facts and Figures 2025”, itu.int. GSMA reported that mobile technologies generated USD 950 billion in regional economic value in 2024, while 5G connections represented 18% of all mobile connections and are projected to reach 50% by 2030, supported by USD 254 billion in operator investment. GSMA also noted that 48% of the regional population remained offline in mid-2025, which leaves India, Indonesia, and the Philippines as the largest near-term user pools for rental platforms. Platforms that keep their user experience mobile-first and usable on lower bandwidth are better placed to win early demand before access levels narrow across markets.

Influence of Social Media and Fashion Trends

Social media now shapes how consumers discover, evaluate, and book rental clothing across the region. Research published in Future Business Journal in 2025 found that both brand-generated and user-generated content significantly influence Gen Z sustainable fashion purchase intention, with social media engagement acting as the main amplifier. This matters for the Asia-Pacific online clothing rental market because rental decisions are often tied to visible occasions where consumers want a distinct look for a short period. Influencer content that shows the full wear-and-return process reduces hesitation around hygiene and makes rented clothing appear normal and aspirational. The effect is strongest where short-form video and creator-led commerce already shape fashion discovery, which helps online rental platforms compete more directly with physical retail.

Growth of the Sharing Economy Mindset

The move from ownership to access is supporting repeat use of rental platforms across major Asia-Pacific cities. In Southeast Asia, the digital economy passed USD 300 billion in gross merchandise value in 2025, which shows how payment, logistics, and verification systems are becoming strong enough to support adjacent access-based services. That wider infrastructure reduces friction for fashion rental, especially where consumers already use shared or on-demand services in other parts of daily life. Cultural garments often serve as the first rental touchpoint, because Hanfu, sarees, and hanboks are worn for defined events and carry high purchase costs for limited use. Once consumers become comfortable renting traditional attire, platforms have a clearer route into broader occasion wear and everyday categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Consumer Trust in Rented Apparel | -1.2% | Across Asia-Pacific, strongest in first-time rental markets such as Indonesia and India Tier 2 and Tier 3 cities | Medium term (2-4 years) |

| Concerns over Garment Condition and Fit | -0.9% | Across Asia-Pacific, stronger on online-only platforms without try-before-rent options | Medium term (2-4 years) |

| Damage and Late-Return Risks | -0.7% | Australia, India, and China, especially in higher-value garments and bridal categories | Short term (≤ 2 years) |

| Seasonal and Occasion-Based Demand | -0.5% | Across the region, especially where casual-wear rental remains limited | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Consumer Trust in Rented Apparel

Consumer hesitation around hygiene and stigma remains the most persistent demand-side barrier in the Asia-Pacific online clothing rental market. A 2025 review in Frontiers in Sustainability found that hygiene standards and visible assurances are among the strongest factors shaping rental adoption. The issue is stronger in markets where rental is still a new behavior, including Indonesia and India's Tier 2 and Tier 3 cities, because many shoppers lack a prior reference point. Style Theory's 2025 closure also showed how trust can weaken quickly when customers perceive garment quality to be falling as operating pressures rise. Platforms that make cleaning protocols, inspection steps, and damage disclosures easy to see are better positioned than low-cost rivals whose claims are harder to verify.

Sizing/Fit-Related Reverse-Logistics Losses

Fit uncertainty is a major barrier for online-only operators, especially in the ethnic and occasion wear categories that dominate regional demand. Garments such as lehengas, sarees, cheongsams, and hanboks often vary in drape, embellishment, and cut, so standard size charts do not fully remove risk. A 2025 study in Circular Economy and Sustainability found that rental adoption improves when platforms pair the price case for renting with clear service assurances on maintenance, repair, and washing. Platforms in Japan, South Korea, and Australia are responding with virtual try-on tools, better sizing support, and garment-specific condition photography. AirCloset's March 2026 Self-Select feature gave subscribers more control over specific item choice, which directly addressed a common concern around fit and certainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Clothing Style: Ethnic Occasions Anchor Platform Revenue

Ethnic Wear held 56.7% of the Asia-Pacific online clothing rental market share in 2025, which made it the clear revenue anchor for the region. The segment is supported by weddings, festivals, religious events, and cultural travel occasions where consumers want premium traditional dress without the full ownership cost. Rental becomes especially attractive when bridal and festive outfits carry high purchase prices for limited use. In India, Flyrobe shifted its focus toward ethnic and bridal wear after finding that many early Western-wear users eventually moved into ethnic rental, which confirmed the category's conversion strength. This position looks durable because cultural attire is tied to recurring social events rather than short fashion cycles.

Sports and Activewear is projected to grow at a 9.4% CAGR from 2026 to 2031, which makes it the fastest-expanding clothing style in the Asia-Pacific online clothing rental market. Growth comes from wider athleisure use, rising fitness participation, and a reluctance to buy specialized apparel for limited-use activities. The category also fits the sustainability case, because technical garments often have high material intensity and irregular usage patterns. GlamCorner's activewear rental offer shows that operators known for occasion wear are testing adjacent categories with higher repeat-use potential.

By End User: Women Sustain Platform Revenues, Young Consumers Accelerate

Women accounted for 65.4% of platform revenue in 2025, which kept them at the center of demand across the Asia-Pacific online clothing rental market. The segment benefits from higher event frequency, stronger preference for outfit variation, and heavier social-media-driven demand for distinct looks. Leadership is especially visible in India and Australia, where women's ethnic, bridal, gala, and bridesmaid categories drive a large share of transactions. Flyrobe's expansion into more than 30 cities reflects how strong the women's occasion wear base has become in India, alongside its broader ethnic rental focus. Women's rentals also tend to support higher order values and stronger referral patterns than male categories.

Kids and Teens is forecast to expand at a 9.9% CAGR through 2031, which makes it the fastest-growing end-user group in the Asia-Pacific online clothing rental industry. The case for rental is strong because children outgrow clothing quickly, which limits the value of ownership for formal and occasion wear. The wider childrenswear base in Asia-Pacific remained large in 2025, with the region accounting for 40.7% of global share and the segment growing at a 7.9% CAGR through 2031. Formal children's attire for ceremonies and milestone events gives rental platforms a practical entry point as parents look for quality, fit, and lower cost.

By Business Model: Stand-Alone Rentals Lead, Subscription Models Define the Growth Frontier

One-Time / Stand-Alone Rental accounted for 67.3% of the Asia-Pacific online clothing rental market size in 2025, which made it the main commercial format in the region. The model fits demand centered on weddings, festivals, graduations, and corporate events, where consumers need one outfit for one date rather than ongoing access. It also suits first-time renters who want a low-commitment transaction before moving to recurring plans. For operators, stand-alone rental lowers holding risk because inventory turnover follows identifiable event demand rather than uncertain monthly usage. This keeps the format central to how many platforms enter new cities and new categories.

Subscription-Based Rental is projected to grow at an 11.1% CAGR from 2026 to 2031, which makes it the fastest-growing model in the Asia-Pacific online clothing rental industry. Growth depends on better curation, cleaner logistics, and stronger inventory utilization as platforms scale. AirCloset expanded this model in 2026 through Self-Select and the launch of airCloset Men's, which widened both user control and addressable demand. At the same time, Style Theory's closure in 2025 showed that subscription models remain exposed when cleaning, logistics, and depreciation rise faster than member revenue. Hybrid models that combine stand-alone rental with optional subscription upgrades are gaining attention because they balance occasion peaks with recurring baseline demand.

Geography Analysis

China accounted for 27.7% of the Asia-Pacific online clothing rental market in 2025, making it the largest country market in the region. This position is supported by strong rental acceptance, a large social commerce base, and growing demand for Hanfu and bridal attire tied to cultural occasions. Douyin-led discovery and affiliate commerce provide rental platforms with an established route for visibility and bookings among urban consumers. India followed as a major demand center, driven by ethnic and bridal wear, maturing digital commerce, and expansion beyond metro areas. Flyrobe's move into Bilaspur in January 2025 reflected the view that physical touchpoints remain important for building consumer trust before online rental scales in smaller cities.

Australia is projected to grow at a CAGR of 10.6% through 2031, the fastest pace in the Asia-Pacific online clothing rental market. The country has the most mature fashion rental ecosystem in the region, with operators that have already established recurring revenue, designer relationships, and profitable business models. The Volte strengthened its market position in 2025 through a collaboration with the University of Technology Sydney, which supported the environmental case for rental and reinforced platform credibility. Its expansion into the United Kingdom demonstrated that Australian platform models can extend beyond the domestic market. Japan remains strategically important, with AirCloset extending rental beyond its established women's subscriber base through men's subscriptions, in-store collection points, and wedding guest services in 2026.

South Korea is building demand through K-fashion influence and strong creator reach among younger consumers, particularly in occasion-led categories. Indonesia represents the largest untapped volume pool by population, but Style Theory's exit in 2025 highlighted the challenges of logistics density and cost control in an archipelagic market. Thailand is receiving stronger institutional support for circular fashion through UNEP-backed programs, while Singapore serves as a logistics and fintech hub for premium designer rental activity across the region. The rest of Asia-Pacific, including Vietnam and the Philippines, is forming an early demand base as smartphone penetration and social commerce behavior expand across the region.

Competitive Landscape

China accounted for 27.7% of the Asia-Pacific online clothing rental market in 2025, making it the largest country market in the region. Strong rental acceptance, a large social commerce base, and growing demand for Hanfu and bridal attire drive this position. Douyin-led discovery and affiliate commerce help rental platforms reach urban consumers effectively. India followed as a major demand center, driven by ethnic and bridal wear, growing digital commerce, and expansion beyond metro areas. Flyrobe's move into Bilaspur in January 2025 showed that physical stores still help build consumer trust before online rental scales in smaller cities.

Australia is projected to grow at a CAGR of 10.6% through 2031, the fastest in the region. It has the most mature fashion rental ecosystem, with operators that have built recurring revenue, designer relationships, and profitable models. The Volte's 2025 collaboration with the University of Technology Sydney reinforced the environmental case for rental and boosted platform credibility. Its expansion into the United Kingdom showed that its model can work beyond the domestic market. Japan remains important, with AirCloset expanding into men's subscriptions, in-store collection points, and wedding guest services in 2026.

South Korea is growing demand through K-fashion influence and strong creator reach among younger consumers, especially in occasion-led categories. Indonesia has the largest untapped population base, but Style Theory's 2025 exit highlighted the difficulty of managing logistics and costs in an archipelagic market. Thailand is receiving institutional support for circular fashion through UNEP-backed programs, while Singapore serves as a logistics and fintech hub for premium rental activity. Vietnam and the Philippines are forming an early demand base as smartphone use and social commerce expand across the region.

Asia-Pacific Online Clothing Rental Industry Leaders

GlamCorner

AirCloset

Flyrobe

The Volte

Mechakari

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: AirCloset and Anniversaire (Japan) launched wedding guest dress rental gift service. The collaboration enables couples to gift formal dress rental experiences to wedding guests via the airCloset Dress platform in e-gift format. Guests select a dress fitting their personal style and size through an online system. The initiative shifts Japan's wedding industry toward more sustainable event experiences and expands AirCloset's occasion-based revenue streams beyond its core daily-wear subscription.

- May 2026: AirCloset (Japan) commercially launched Men's subscription fashion rental service (airCloset Men's). Opened for reservations on April 15, 2026, and commercially launched on May 28, 2026, the service addresses one of the platform's most frequently requested feature additions. It leverages AirCloset's 11-year styling knowledge base, cleaning infrastructure, and AI recommendation capability to enter a subscription segment previously unserved in Japan.

- March 2026: AirCloset Mall introduced take-away rental at Bic Camera's new store in Japan. The service enables visitors to the electronics retailer to access fashion rental from a physical touchpoint, extending AirCloset's omnichannel reach and positioning fashion rental within everyday consumer electronics shopping environments.

Asia-Pacific Online Clothing Rental Market Report Scope

| Ethnic Wear |

| Casual Wear |

| Formal Wear |

| Sports and Activewear |

| Others (Maternity, Kids’ Formal, etc.) |

| Women |

| Men |

| Kids and Teens |

| Subscription-Based Rental |

| One-Time / Stand-Alone Rental |

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Clothing Style | Ethnic Wear |

| Casual Wear | |

| Formal Wear | |

| Sports and Activewear | |

| Others (Maternity, Kids’ Formal, etc.) | |

| By End User | Women |

| Men | |

| Kids and Teens | |

| By Business Model | Subscription-Based Rental |

| One-Time / Stand-Alone Rental | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the forecast value of the Asia-Pacific online clothing rental market by 2031?

The Asia-Pacific online clothing rental market is forecast to reach USD 831.5 million by 2031, rising from USD 562.8 million in 2026 at an 8.1% CAGR.

Which clothing style leads rental demand across Asia-Pacific?

Ethnic Wear leads demand with 56.7% share in 2025, supported by weddings, festivals, and other culturally important occasions.

Which business model is growing the fastest in online clothing rental across Asia-Pacific?

Subscription-Based Rental is the fastest-growing model, with an 11.1% CAGR through 2031, even though stand-alone rental still leads current revenue.

Which country leads the region and which one is growing the fastest?

China held the largest share at 27.7% in 2025, while Australia is projected to record the fastest growth at a 10.6% CAGR through 2031.

Page last updated on: