Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.07 Trillion |

| Market Size (2031) | USD 3.85 Trillion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

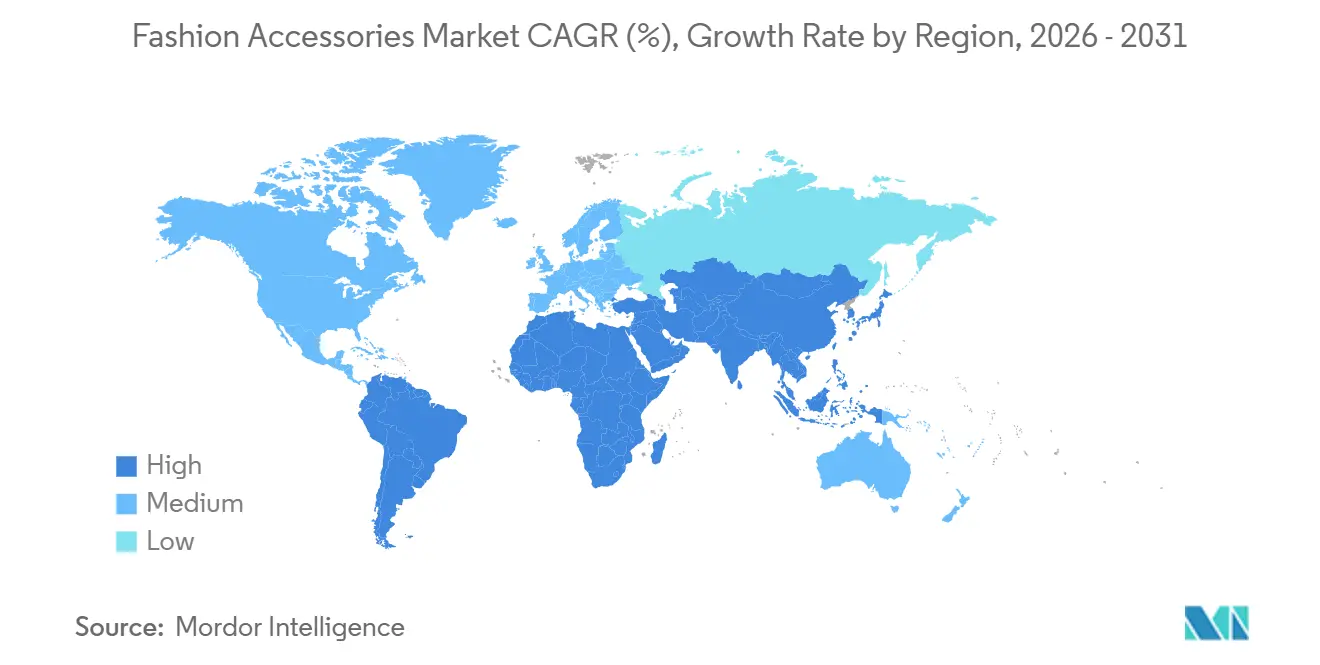

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

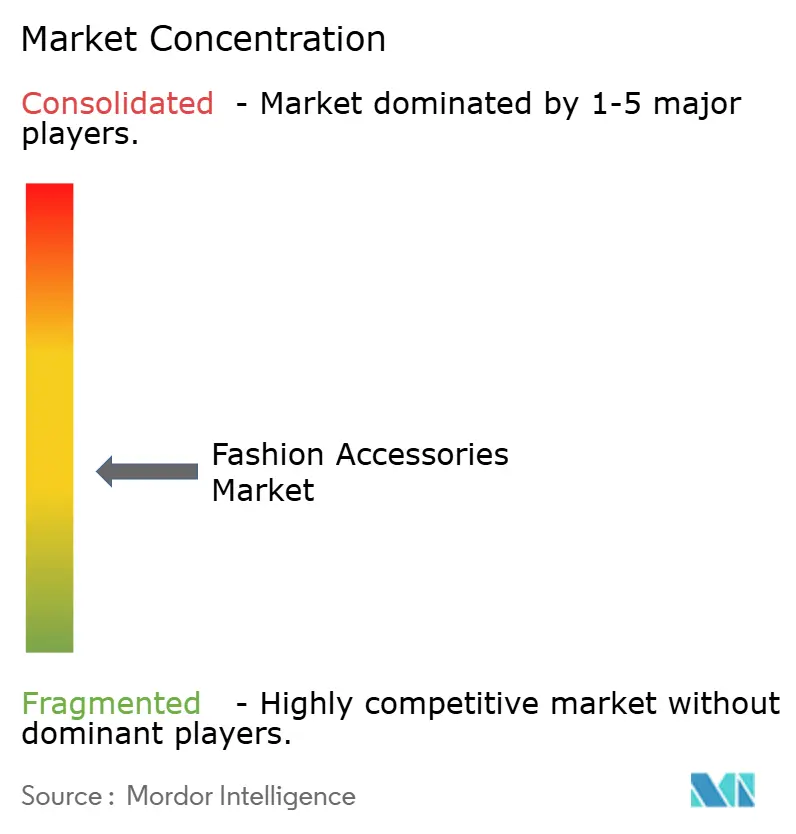

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fashion Accessories Market Analysis by Mordor Intelligence

The Fashion Accessories Market size was valued at USD 2.93 trillion in 2025 and estimated to grow from USD 3.07 trillion in 2026 to reach USD 3.85 trillion by 2031, at a CAGR of 4.62% during the forecast period (2026 to 2031), confirming a resilient trajectory for the market. Hybrid technology, premiumization, and circular business models are steering the shift from purely aesthetic purchases toward functional, durable, and traceable products. Mass players still dominate volumes, yet vertically integrated luxury groups protect margins by controlling tanneries, raw material suppliers, and direct retail. Online channels are eroding the historic advantage of brick-and-mortar stores through same-day delivery and virtual try-on tools. Ultimately, stricter sustainability regulations are prompting brands to disclose provenance, invest in recycled materials, and develop resale or repair services that extend product life cycles.

Key Report Takeaways

- By product type, apparel led the fashion accessories market with a 57.21% market share in 2025, while watches are expected to record the fastest growth at a 5.28% CAGR through 2031.

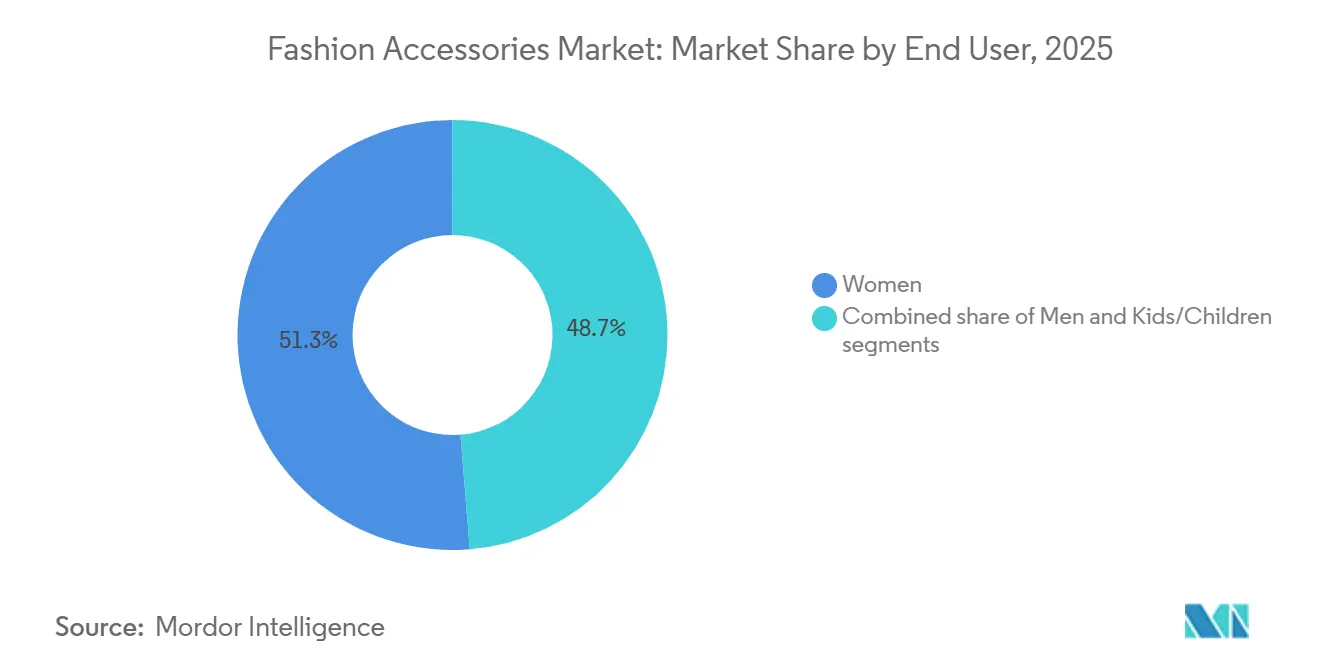

- By end user, women commanded 51.27% share of the fashion accessories market size in 2025, and kids’ lines are forecast to expand at a 5.69% CAGR to 2031.

- By category, mass market continued to hold 66.14% revenue share in 2025, whereas the premium tier is projected to grow at a 6.05% CAGR between 2026-2031.

- By distribution channel, offline stores retained 62.35% share of the fashion accessories market in 2025, yet online channels will accelerate at a 6.36% CAGR through 2031.

- By geography, Asia-Pacific captured a 34.03% revenue share in 2025 and is poised for the highest 6.88% CAGR, powered by India’s rising disposable income.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Fashion Accessories Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in design and materials | +0.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Demand surge for luxury and premium products | +0.9% | Asia-Pacific, Middle East | Long term (≥4 years) |

| Growth of athleisure and sports-inspired fashion | +0.7% | North America, Europe, Asia-Pacific urban centers | Short term (≤2 years) |

| Social-media-led micro-trend acceleration | +0.6% | Global | Short term (≤2 years) |

| Sustainability and circular-economy initiatives | +0.5% | Europe, North America, Asia-Pacific | Long term (≥4 years) |

| Fashion-tech wearables convergence | +0.4% | North America, Europe, Japan, South Korea, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological advancements in design and materials

Additive manufacturing and bio-fabricated materials are reshaping both the cost structure and creative possibilities of accessories production. LVMH’s adoption of 3D-printed watch components shortened prototyping timelines from roughly 12 weeks to just three weeks in 2025, enabling design teams to respond more quickly to fleeting trends. Bio-materials have also moved beyond experimentation: mycelium leather reached commercial viability in 2024 when Hermès introduced the Victoria bag made with Mylo from Bolt Threads, delivering carbon emissions about 60% lower than traditional bovine leather while preserving comparable strength and durability. Technology-driven innovation is also extending into adjacent categories. Electrochromic lenses that automatically adjust tint in response to UV exposure gained momentum in 2025 when Luxottica incorporated the technology into Ray-Ban Meta smart glasses, blending fashion with adaptive functionality. Collectively, these advances are compressing product development cycles and making small-batch, limited-edition launches more viable, enabling brands to test demand without committing to large production volumes. This dynamic increasingly advantages agile players, while legacy manufacturers tied to rigid seasonal calendars face growing pressure to adapt.

Growth of athleisure and sports-inspired fashion

Athleisure's migration from gym to boardroom is reshaping accessory design hierarchies, with performance fabrics and ergonomic silhouettes displacing traditional leather and metal in professional settings. Nike's 2025 launch of the Cortez Crossbody bag, featuring water-resistant ripstop nylon and modular compartments for tech devices, sold 500,000 units within 4 months, validating demand for hybrid accessories that serve both athletic and urban contexts. Adidas reported that its Samba sneaker resurgence in 2024-2025 drove 22% growth in adjacent accessories, lace jewellery, sneaker-care kits, and logo-embossed backpacks, demonstrating how footwear trends cascade into broader accessory categories. The "man bag" category, long stigmatized in Western markets, achieved mainstream adoption in 2025 as remote work blurred the boundary between casual and business attire, prompting brands such as Lululemon and Under Armour to introduce leather-trimmed duffels and laptop sleeves that straddle both functionality and fashion. This trend is compressing product-development cycles, as brands must now design accessories that transition seamlessly from yoga studio to client meeting, requiring materials that resist odor, moisture, and wear while maintaining aesthetic refinement.

Fashion-tech wearables convergence (smart jewellery, smart bags)

The blending of fashion and health-tracking technology is giving rise to a new class of accessories where aesthetics matter as much as functionality, reshaping competition across both luxury goods and consumer electronics. Oura Ring surpassed USD 500 million in revenue in 2025 by embedding sleep and fertility tracking into a slim titanium band designed to resemble fine jewelry, appealing to users who want wellness insights without compromising style. Luxury houses are moving in parallel, discreetly integrating near-field communication (NFC) into bracelets and necklaces to enable contactless payments and digital ID use without visible tech components; Swatch Group’s collaboration with Visa, which added payment capability to 15 watch models across Europe, recorded 100,000 activations within two months of its late-2024 launch. Smart luggage and handbags are also gaining traction as security and connectivity concerns rise in urban markets. Features such as GPS tracking, wireless charging, and biometric locks are no longer novelties: Samsonite’s Proxis smart luggage line, launched in 2025 with Tile trackers and USB-C ports, generated USD 120 million in sales within six months, demonstrating that well-designed utility can justify premium pricing. Still, adoption is constrained by practical challenges, particularly concerns about battery longevity and the issue of electronic waste. A 2025 McKinsey survey found that only 18% of smart-accessory buyers were willing to replace devices every two to three years, signaling that long-term growth will depend on modular designs, repairability, and clearer sustainability pathways.

Social-media-led micro-trend acceleration

TikTok’s algorithm-led discovery has dramatically shortened fashion trend cycles, reducing them from roughly 18 months to as little as six weeks by 2025, and prompting brands to reassess their production speed and inventory management. The rise of the “quiet luxury” look earlier in the year fueled demand for pared-back leather goods and discreet timepieces, lifting labels such as The Row and Brunello Cucinelli, while dampening interest in overtly logo-driven accessories. At the same time, Instagram’s in-app shopping tools have become more effective at converting interest into sales, with 12% of accessory impressions translating into purchases in 2025, up from 8% the previous year, as brands refined their product tagging and influencer strategies. Marketing spend is increasingly shifting toward micro-influencers with 10,000 to 100,000 followers, who deliver engagement rates of 5% to 8%, far outperforming mega-influencers. This reallocation is lowering barriers to entry for emerging accessory brands, enabling them to scale through authentic, community-driven promotion, while established players struggle to maintain credibility among digitally native consumers who are wary of overly polished campaigns.

Restraints Impact Analysis of Fashion Accessories Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and grey-market proliferation | -0.6% | Global, with acute impact in Asia-Pacific, Middle East, Latin America | Short term (≤2 years) |

| Geopolitical supply-chain disruptions | -0.5% | Global, concentrated in Europe (leather), Switzerland (watches), China (manufacturing) | Medium term (2-4 years) |

| Volatile prices of specialty raw materials (leather, rare metals) | -0.4% | Global, with acute impact on mid-tier brands lacking hedging | Short term (≤2 years) |

| Intensifying ESG and trade-tariff compliance costs | -0.3% | EU (CSRD, DPP mandates), North America (tariff adjustments), Asia-Pacific (export compliance) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and grey-market proliferation

The OECD estimates that counterfeit fashion accessories drained approximately USD 98 billion from the industry in 2024, with handbags, watches, and sunglasses accounting for about 65% of all items seized at EU borders[1]Source: OECD, “Trade Topics: Counterfeiting and Piracy,” oecd.org. Counterfeiters are becoming increasingly sophisticated, using tools such as 3D scanning and AI-generated logos to closely replicate originals, which has narrowed the quality gap and made fakes harder to spot for both consumers and customs officials. In response, brands are turning to blockchain-based authentication. For instance, Richemont’s Aura Blockchain Consortium rolled out NFC-enabled verification for watches and handbags in 2024, resulting in an 18% reduction in grey-market leakage among participating labels. Adoption, however, remains uneven, as smaller brands struggle to justify the implementation costs, which can range from USD 500,000 to USD 2 million. At the same time, grey-market activity, where authentic goods are sold through unauthorized channels at discounted prices, continues to weaken brand equity and pricing discipline, particularly in Asia-Pacific markets, where parallel imports from duty-free zones often undercut official retail prices by 20% to 30%.

Geopolitical supply-chain disruptions

The Red Sea shipping disruptions in 2024, sparked by Houthi attacks on commercial vessels, pushed lead times for Italian leather goods and Swiss watch components up by roughly 30%, leaving many brands with little choice but to move inventory by air at costs nearly five times higher than ocean freight. Trade tensions between the U.S. and China continued into 2025, with tariffs of 15% to 25% on Chinese-made accessories accelerating efforts to shift production to countries such as Vietnam, India, and Mexico. While these markets offer cost and geopolitical diversification, they often lack the deep supplier networks and craftsmanship found in long-established hubs, leading to quality variability and longer ramp-up periods. Regulatory pressure is adding another layer of complexity. The EU’s Carbon Border Adjustment Mechanism, set to take effect in 2026, will apply charges of EUR 50 to EUR 150 (USD 55 to USD 165) per ton of embedded CO₂ on imports from countries with weaker carbon-pricing regimes, disproportionately impacting sourcing from India and Turkey, according to the European Commission[2]Source: European Commission, “Digital Product Passport Mandate,” europa.eu. Together, these factors are speeding up nearshoring and reshoring strategies. In 2025, Kering announced a EUR 200 million (approximately USD 220 million) investment in European leather tanneries, aiming to secure its supply, reduce exposure to Asian logistics risks, and regain greater control over quality and sustainability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Fashion Accessories Market Segment Analysis

By Product Type:

Watches Outpace Apparel on Smart IntegrationApparel accounted for 57.21% of the fashion accessories market in 2025, reflecting its widespread presence across both mass-market and premium segments. Watches, however, are emerging as the fastest-growing category, projected to expand at a 5.28% CAGR through 2031, driven largely by hybrid smartwatches that combine traditional mechanical craftsmanship with health-tracking features. TAG Heuer’s Connected Calibre E4, launched in 2024, integrates a Wear OS interface with a Swiss-made case, capturing 12% of the luxury smartwatch segment within six months. Footwear and handbags continue to be key volume drivers, while sneaker-adjacent accessories such as lace jewelry and bag charms are gaining popularity among Gen Z consumers seeking personalized touches. Wallets and sunglasses, in contrast, are seeing slower growth due to market saturation and the rise of contactless payments, which reduce demand for traditional wallets.

Jewelry is carving a distinct niche at the intersection of fashion and wellness, particularly with smart rings and NFC-enabled bracelets. Oura Ring, for instance, surpassed USD 500 million in revenue in 2025 by offering sleep-tracking and fertility-monitoring features that appeal to health-conscious millennials. Sunglasses are also innovating through technology, with Luxottica’s Ray-Ban Meta smart glasses selling 2 million units in 2025 owing to electrochromic lenses and augmented-reality overlays. Apparel-related accessories such as scarves, belts, and hats are increasingly leveraging sustainable materials like organic cotton and recycled polyester to attract eco-conscious buyers. However, higher price points, typically 15% to 25% above conventional alternatives, have limited their adoption in the mass market, keeping them primarily within premium and niche consumer segments.

By Category:

Premium Gains on Heritage StorytellingThe mass category commanded 66.14% of the Fashion Accessories Market in 2025, reflecting the price sensitivity of the majority of consumers. However, the premium segment is expanding at a 6.05% CAGR through 2031, driven by consumers trading up for heritage craftsmanship and provenance storytelling. Hermès' Birkin and Kelly bags, which appreciate in value by 10% to 15% annually, have become investment assets, with resale platforms reporting 3-month waiting lists for authenticated pre-owned units. This dynamic is prompting mass-market brands to introduce "accessible luxury" lines priced between USD 300 and USD 800, bridging the gap between fast fashion and true premium. Coach's Tabby bag, relaunched in 2024 at USD 395, achieved 1 million unit sales within 12 months by leveraging nostalgia and influencer partnerships.

Mass-market accessories are under pressure from rising input costs and margin compression, with brands such as H&M and Zara reporting 200- to 300-basis-point declines in gross margins in 2025 due to volatility in leather and metal prices. Premium brands, insulated by pricing power and vertical integration, maintained or expanded margins by controlling raw-material sourcing and manufacturing. Richemont's ownership of Swiss watch-movement suppliers and Italian leather tanneries enabled it to absorb cost inflation without passing it to consumers, preserving brand positioning. The premium segment is also benefiting from experiential retail, with brands opening flagship stores that double as museums or ateliers, offering customization services and behind-the-scenes tours that justify price premiums.

By End User:

Kids' Segment Accelerates on Durability DemandWomen drove 51.27% of end-user demand in 2025, fueled by higher purchase frequency and a willingness to invest in premium accessories that signal personal style and status. Meanwhile, the kids’ segment is emerging as the fastest-growing category, projected to expand at a 5.69% CAGR through 2031, as parents prioritize durable, sustainable products suited for active lifestyles. Adjustable watch straps, expandable backpacks, and modular jewelry help address the “outgrow problem,” extending product lifecycles from 12 to 24 months and improving cost-per-wear. Brands like Pandora and Fossil are launching dedicated kids’ lines with hypoallergenic materials and safety certifications to address parental concerns over skin sensitivity and choking hazards.

Men’s accessories are growing more slowly but are benefiting from the athleisure trend, with crossbody bags and performance watches gaining acceptance in professional environments. The “man bag” category, long stigmatized in Western markets, saw a 22% year-on-year sales increase in 2025 as remote work blurred the line between casual and business attire. Women’s accessories continue to dominate luxury spending, with handbags and fine jewelry accounting for 60% of premium-category revenue. As the segment matures, brands are exploring personalization services such as monogramming and bespoke colorways to maintain engagement. Kids’ accessories are also benefiting from the “mini-me” trend, where scaled-down versions of adult luxury items cultivate early brand affinity that can translate into long-term loyalty.

By Distribution Channel:

Online Gains on Virtual Try-OnOffline stores held 62.35% of distribution in 2025, reflecting the tactile nature of accessories and the importance of in-person consultation for high-ticket purchases, yet online channels are growing at 6.36% CAGR through 2031, the fastest among distribution types. Virtual try-on tools, powered by augmented reality, reduced return rates for sunglasses and watches by 35% in 2025, addressing a key friction point in online accessory sales. Warby Parker's virtual try-on feature, which uses facial mapping to simulate frame fit, converted 18% of app users into buyers in 2025, double the industry average. Same-day delivery, enabled by micro-fulfillment centers in metropolitan hubs, is eroding the immediacy advantage of physical stores, with 40% of online accessory purchases in New York and London delivered within 4 hours in 2025.

Offline stores are evolving into experiential destinations rather than transactional spaces. LVMH's Louis Vuitton flagship in Seoul, opened in 2024, features a rooftop café, art gallery, and customization atelier, generating 30% higher sales per square foot than traditional stores[3]Source: LVMH, “Annual Report 2025,” lvmh.com . Omnichannel integration, where customers can browse online and pick up in-store or return online purchases at physical locations, is becoming table stakes, with brands reporting that omnichannel customers spend 2.5 times more than single-channel customers. Social commerce, particularly live-streaming sales on platforms such as Douyin (TikTok's Chinese counterpart) and Instagram, is blurring the line between content and commerce, with luxury brands achieving conversion rates of 8% to 12% during live events, compared to 2% to 3% for static posts.

Geography Analysis

APAC Fashion Accessories Market

Asia-Pacific accounted for 34.03% of the global fashion accessories market in 2025 and is projected to grow at a 6.88% CAGR through 2031, the fastest among all regions, fueled by rising disposable incomes, urbanization, and digital-first consumer behavior. China’s luxury market rebounded as domestic spending shifted from overseas travel to local boutiques amid geopolitical tensions, with Hainan’s duty-free zone attracting 10 million visitors in 2025 and offering goods at up to 30% below mainland prices. India’s premium accessories segment expanded 14% in 2025, driven by millennials and Gen Z favoring brand heritage over fast fashion, with Titan Company reporting 18% growth in its luxury watch division. Japan’s mature market benefited from inbound tourism, with Chinese and Southeast Asian visitors accounting for 25% of luxury accessory sales in Tokyo and Osaka. Southeast Asia, including Indonesia, Thailand, and Singapore, is emerging as a high-growth frontier, supported by over 60% e-commerce penetration and social commerce driving impulse purchases of mid-tier accessories, according to McKinsey and Company.

North America and Europe Fashion Accessories Market

North America and Europe, while experiencing slower growth, remain key profit centers due to high per-capita spending and established luxury ecosystems. The United States represented 28% of global luxury accessory sales in 2025, with handbags and watches leading consumer spend. Inflation and interest-rate increases, however, restrained discretionary purchases, leading mid-tier brands to report flat or negative same-store sales. Europe, led by Germany, France, Italy, and the UK, benefited from inbound tourism, with Chinese and Middle Eastern visitors contributing 35% of luxury accessory purchases in Paris and Milan. Supply-chain digitization is accelerating in response to the EU’s Digital Product Passport mandate, effective 2026, with brands investing EUR 5–20 million (USD 5.5–22 million) in traceability infrastructure. The UK’s VAT-free shopping scheme for tourists, introduced in 2025, boosted accessory sales in London by 12%.

MEA and South America Fashion Accessories Market

Middle East and Africa and South America are smaller but fast-growing markets, concentrated in urban centers and fueled by high-net-worth individuals. The UAE and Saudi Arabia, supported by government initiatives positioning Dubai and Riyadh as global luxury hubs, saw double-digit growth in watch and jewelry sales in 2025. South Africa’s premium accessories market expanded 9%, aided by a rising middle class and growing e-commerce penetration. Brazil and Argentina, despite economic volatility, maintained resilient demand for mass-market accessories, with local brands like Arezzo and Havaianas capturing share through affordable, trend-driven offerings. Emerging markets in Nigeria and Egypt are witnessing rising demand among young, digitally native consumers, primarily via social commerce platforms.

Regulatory Landscape

Sustainability and product-traceability rules are tightening for accessories sold into Europe, which increases documentation and end-of-life obligations for brands and their suppliers. Under the EU Ecodesign for Sustainable Products Regulation (EU) 2024/1781, large companies face a prohibition on destroying unsold apparel, clothing accessories, and footwear from 19 July 2026, shifting inventory, returns, and liquidation workflows toward resale, donation, recycling, and documented derogations. At the same time, EU digital product passport (DPP) requirements are moving from brand-level programs to component-level compliance, with hardware traceability rules for items such as zippers, buckles, and eyelets cited as effective 1 July 2026. This raises the need for item-level identifiers and upstream data capture across trims and materials.

In the United States, consumer-protection and import-compliance requirements continue to affect labeling, advertising, and landed-cost decisions. The Federal Trade Commission (FTC) clothing and textiles guidance remains a key reference point for claims and disclosures, while tariff classification and duty assessment follow the US International Trade Commission (USITC) Harmonized Tariff Schedule framework for categories spanning leather goods, jewelry, watches, and eyewear. Trade measures and customs processing changes in 2026, including tariff actions on key industrial inputs such as metals, heighten cost and lead-time sensitivity for metal-intensive accessories and for supply chains reliant on cross-border small-parcel fulfillment.

Competitive Landscape

The fashion accessories market exhibits moderate consolidation, driven by major conglomerates such as LVMH, Kering, Hermès, Richemont, and Inditex. These companies leverage vertical integration, controlling raw materials, manufacturing, and retail distribution, to safeguard margins from input-cost fluctuations and quickly respond to shifts in consumer demand. LVMH, for instance, owns tanneries, watch-movement suppliers, and a network of 5,600 stores worldwide, giving it end-to-end operational control that smaller brands cannot match. Yet, the market remains fragmented at the mid-tier and mass-market levels, where regional players and digitally native brands are gaining market share by offering niche products, faster turnaround times, and direct-to-consumer models that bypass traditional wholesale markups.

Athleisure giants Nike and Adidas are pushing the boundaries of traditional accessory categories with performance-inspired handbags and sneaker-adjacent jewelry, compelling luxury houses to defend market share through collaborations with streetwear labels such as Supreme and Off-White. Technology is increasingly shaping competitive advantage, with investments in blockchain authentication, AI-driven demand forecasting, and augmented-reality try-on tools enhancing both customer experience and operational efficiency. Richemont’s Aura Blockchain Consortium, including brands like Prada and Cartier, enables real-time product verification and resale tracking, helping to reduce counterfeit activity and legitimize secondary markets.

White-space opportunities are emerging in smart accessories, circular-economy solutions, and untapped emerging markets where incumbents are slow to adapt. Startups such as Oura (smart rings) and Warby Parker (virtual try-on eyewear) are capturing disproportionate attention among digitally native consumers, showing that agility and innovation can offset the scale advantages of established players. Regulatory requirements, including the EU’s Corporate Sustainability Due Diligence Directive, are raising entry barriers, favoring companies with the resources to implement robust traceability, reporting systems, and sustainable supply-chain practices.

Fashion Accessories Industry Leaders

LVMH Moet Hennessy Louis Vuitton

Kering Group

Hermes International S.A.

Richemont SA

Inditex SA

- *Disclaimer: Major Players sorted in no particular order

Fashion Accessories Market Companies Covered in this Report

- LVMH Moet Hennessy Louis Vuitton

- Inditex SA

- Kering SA

- Richemont SA

- Hermes International SA

- Tapestry Inc.

- Capri Holdings

- Prada SpA

- Giorgio Armani SpA

- Dolce & Gabbana SRL

- Chanel SA

- Ramsbury Invest AB

- Swatch Group

- Fossil Group Inc.

- Luxottica Group SpA

- Pandora A/S

- Tory Burch LLC

- Nike Inc.

- Adidas AG

- VF Corporation

- Under Armour Inc.

Market Opportunities and Future Outlook

Traceability infrastructure is increasingly a commercially actionable whitespace as EU DPP compliance work expands beyond finished goods into accessories-relevant components (trims, fasteners, labels) and item-level identity. Brands and solution providers are adopting unique identifiers (QR, NFC, RAIN RFID) and linking them to PLM and supplier data to support compliance, authentication, resale, and repair. On Running provides an illustrative case, implementing item-level RAIN RFID tagging across footwear, apparel, and accessories in March 2026, which highlights the demand for scalable serialization and data-sharing models that multi-brand groups and mass players can replicate.

Materials and circular supply chains for accessory inputs also create partnering and sourcing opportunities, particularly for recycled fibers and responsible trims that fit premiumization and sustainability requirements. In June 2026, Harnest announced a partnership with Indorama Ventures and Ambercycle to expand its Responsible Trims Collection, including sewing threads, elastics, labels, and drawcords, aimed at a high-volume but often overlooked part of accessories manufacturing. On the feedstock side, Circulose moved to restart commercial-scale production at its Ortviken facility in Sundsvall, Sweden, with output resuming in Q4 2026 and new brand partners named in June 2026, supporting broader availability of recycled cellulose inputs that can be translated into linings, textiles, and packaging used across handbags, small leather goods, and lifestyle accessories.

Recent Industry Developments in Fashion Accessories Market

- April 2026: Kering formed a strategic partnership with ICCF and acquired a minority stake to support the development of ICICLE. The move strengthens Kering’s exposure to a China-origin brand platform and supports localized growth levers across adjacent categories, including accessories-led premium positioning.

- March 2026: Kering completed the first step in the staged acquisition of Raselli Franco Group by acquiring a 20% stake for EUR 115 million. The investment deepens access to jewelry manufacturing capability and supply assurance, aligning with luxury groups’ efforts to control craftsmanship capacity and reduce supplier risk.

- February 2024: Richemont’s Aura Blockchain Consortium rolled out NFC-enabled product verification for watches and handbags. Expanded authentication and provenance tooling supports brand-controlled resale and helps reduce grey-market leakage, reinforcing trust in higher-value accessories.

Fashion Accessories Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the fashion accessories market covers retail and brand revenues from new, non-apparel personal adornment items sold to consumers through offline and online channels, across all price tiers and regions.

Scope exclusions: We exclude second-hand resale value, replacement parts (such as straps or lenses sold as spares), and purely technology wearables with no fashion purchase intent.

Segments Covered in This Report

- By Product Type

- Footwear

- Apparel

- Wallets

- Handbags

- Watches

- Sunglasses

- Jewelery

- By End User

- Men

- Women

- Kids/Children

- By Category

- Mass

- Premium

- By Distribution Channel

- Offline Stores

- Online Stores

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what counts as an accessory purchase and to anchor the model to observable demand signals. We relied on public statistics and reference series such as national accounts and consumer spending releases (for example, from the World Bank and OECD), international trade data from UN Comtrade, and inflation and exchange-rate series from the IMF.

To avoid building estimates on a single angle, the desk phase also pulled checks from trade bodies and category-focused sources, such as World Jewellery Confederation publications, along with brand annual reports, investor presentations, and earnings call notes that describe category exposure and regional mix. Patent databases were used selectively to understand product innovation intensity (smart features, materials, and closures) without treating it as a direct revenue input. The sources listed here are illustrative, and many additional public references were consulted to fill gaps and confirm assumptions.

Primary Interviews and Surveys

Primary work focused on validating what is being counted as a fashion accessory at the cash register, and then pressure-testing pricing and channel shifts that desk sources cannot show cleanly. We spoke with a mix of brand-side leaders, distributors, retailers, and materials and component stakeholders across major demand regions, so assumptions on mix, promotion intensity, and premiumization could be adjusted before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | APAC: 44% |

| Mid tier: 54% | Functional/Unit leaders: 40% | EMEA: 31% |

| Smaller Players: 19% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build that reconstructs the addressable demand pool using consumer spending signals, trade flows for key accessory groups, and category-level price inflation, and then aligns that structure to retail channel splits. Once the structure is in place, we corroborate totals using selective bottom-up approximations, such as sampled average selling price by category times implied unit volumes, and supplier and retailer channel checks that help correct for over-counting.

Inputs used in the model include accessory category mix (handbags, small leather goods, jewelry, watches, eyewear, belts, scarves, headwear, and similar items), online share movement versus offline, premium versus mass price mix, promotional intensity and discount depth, and region-level currency movements that affect reported revenues. Where direct unit indicators are weak, we handle gaps by using proxy variables such as import value trends and consumer goods inflation, followed by interview-based adjustments.

For forecasting, we apply scenario analysis around a core path, because the category is sensitive to disposable income, fashion cycles, and pricing actions that change quickly. Assumptions on category growth rates and price progression are cross-checked with what channel and brand respondents expect to hold over the next few seasons, and then smoothed to avoid step changes that cannot be justified with real-world signals.

Data Validation & Update Cycle

Validation is done through multiple checks so the final value is not dependent on one dataset or one assumption. Model outputs are compared against independent signals such as reported accessory revenue exposure from public companies, trade value directionality for relevant HS categories, and the implied per-capita spend trend by region, after which outliers are reviewed and corrected.

Before sign-off, the full workbook is reviewed by another analyst to catch math breaks, inconsistent currency timing, or mix shifts that do not reconcile with the narrative. Reports are refreshed annually, and interim updates are triggered when material events occur, such as sharp currency moves, abnormal discounting cycles, or major demand disruptions. Right before delivery, a final pass is performed so clients receive the latest updated view.

Mordor Intelligence's Fashion Accessories Market Size Compared Against Other Published Estimates

Published market values for fashion accessories can differ a lot, even when the topic name looks the same. In practice, the spread usually comes from how each publisher defines accessories versus apparel, whether resale is counted, and how pricing and currency are handled across regions.

By tracking category-level retail demand signals and refreshing currency timing assumptions, Mordor Intelligence keeps the total tied to new, non-apparel accessory purchases, whereas some estimates expand the scope into apparel or second-hand value, which changes the denominator quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.07 T (2026) | |

| Global Consultancy A | USD 0.80 T (2024) | Uses a narrower category set and pricing basis that appears closer to fashion jewelry and selected accessories, which can exclude parts of leather goods and broader adornment items, and it anchors on a different base year. |

| Industry Publisher B | USD 0.81 T (2024) | The scope shown includes adjacent categories such as apparel and footwear under fashion accessories in its segmentation, and it extends the forecast horizon with a higher price-growth curve, which makes cross-year comparisons uneven. |

The table shows that the biggest drivers are scope boundaries and base-year alignment, not just forecasting math. When the counted basket is limited to selected accessory types, the total lands much lower, and when adjacent categories are folded in, growth rates can look inflated. We keep the steps transparent so buyers can trace the number back to clear demand indicators and repeat the logic when assumptions change.

Key Questions Answered in the Report

What is the projected value of the Fashion Accessories market by 2031?

The market is forecast to hit USD 3.67 trillion by 2031 on a 4.61% CAGR.

Which product type is expected to grow fastest through 2031?

Watches, especially hybrid smartwatches, are slated for a 5.28% CAGR, the quickest among major categories.

Why is Asia-Pacific considered pivotal for accessories growth?

Rising income, digital-first shopping, and local duty-free zones will lift Asia-Pacific sales at a 6.88% CAGR, outpacing every other region.

How are brands addressing sustainability mandates in Europe?

Companies are investing in Digital Product Passport compliance, recycled materials, and circular hubs to meet EU rules effective 2026.

Which segment among end users is currently expanding quickest?

The kids’ segment, driven by durable, adjustable designs, is growing at 5.69% CAGR and attracting new product lines.

Page last updated on: