Maternity Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 22.09 Billion |

| Market Size (2031) | USD 28.79 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

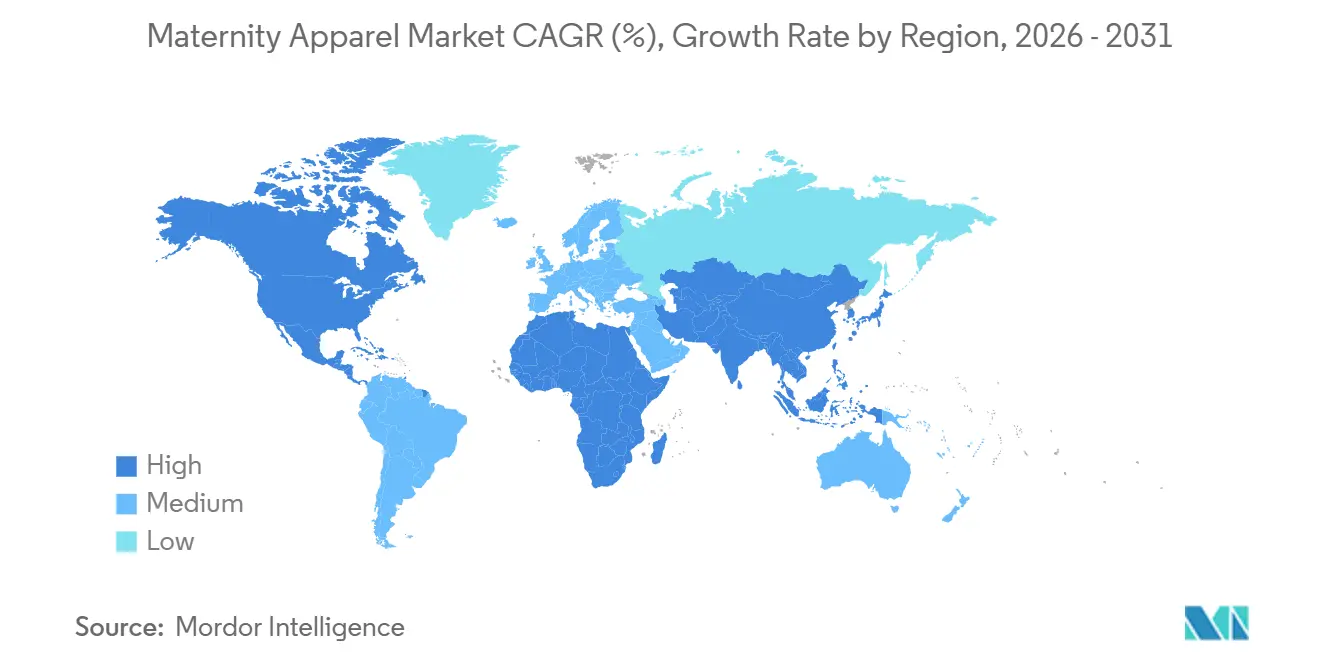

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

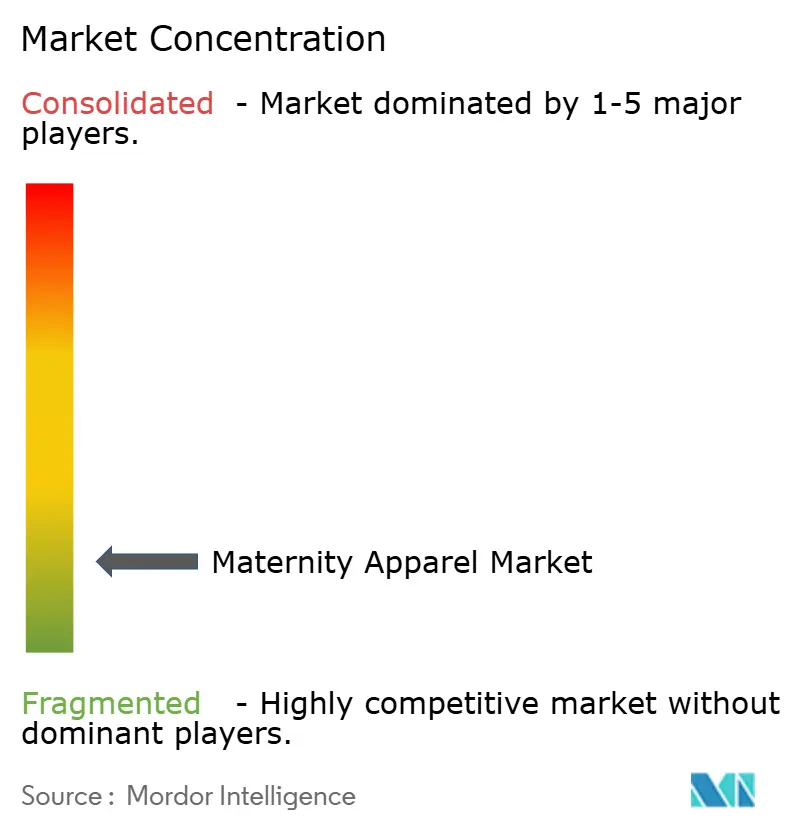

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maternity Apparel Market Analysis by Mordor Intelligence

The maternity apparel market size is projected to expand from USD 21.63 billion in 2025 and USD 22.09 billion in 2026 to USD 28.79 billion by 2031, registering a 5.44% CAGR between 2026 and 2031. While North America stands as the dominant regional player, the Asia-Pacific is witnessing the swiftest expansion, fueled by rising urban incomes and shifting cultural views on pregnancy. Casual wear leads the product categories, yet activewear is on the rise, with more expectant mothers prioritizing fitness and seeking performance-oriented maternity gear. Despite offline retail holding the lion's share of sales, underscoring the consumer's preference for in-person fittings, online channels are swiftly gaining ground, propelled by influencer marketing and the allure of e-commerce convenience. Cotton, celebrated for its comfort and breathability, remains the fabric of choice. However, denim, especially with stretch technology, is making rapid inroads. The market dynamics are further influenced by an uptick in maternal workforce participation and a heightened demand for stylish, functional apparel that seamlessly transitions from prenatal to postpartum. Brands like Hatch and Seraphine are leading the charge, offering trendy maternity lines that expertly blend fashion, comfort, and nursing practicality.

Key Report Takeaways

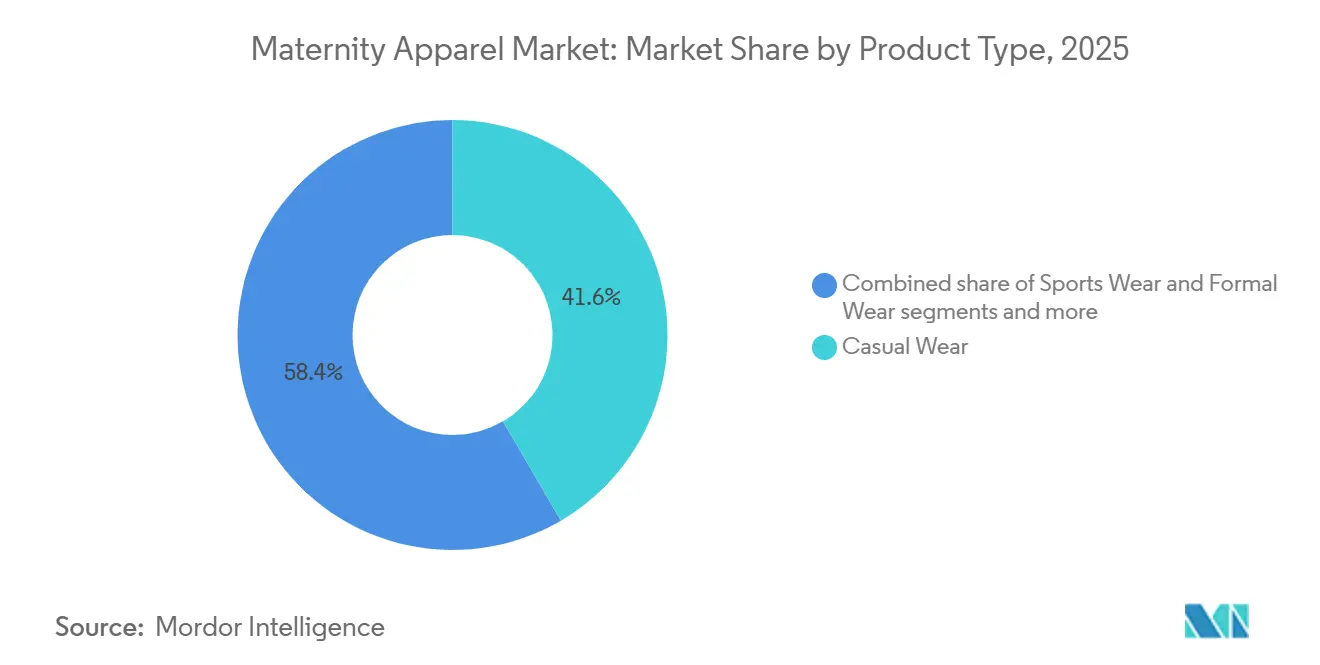

- By product category, casual wear commanded 41.59% revenue share in 2025, while sportswear is advancing at a 6.08% CAGR through 2031.

- By price tier, mass-market offerings held 61.69% of the maternity apparel market share in 2025, whereas premium and luxury lines are expanding at a 6.97% CAGR through 2031.

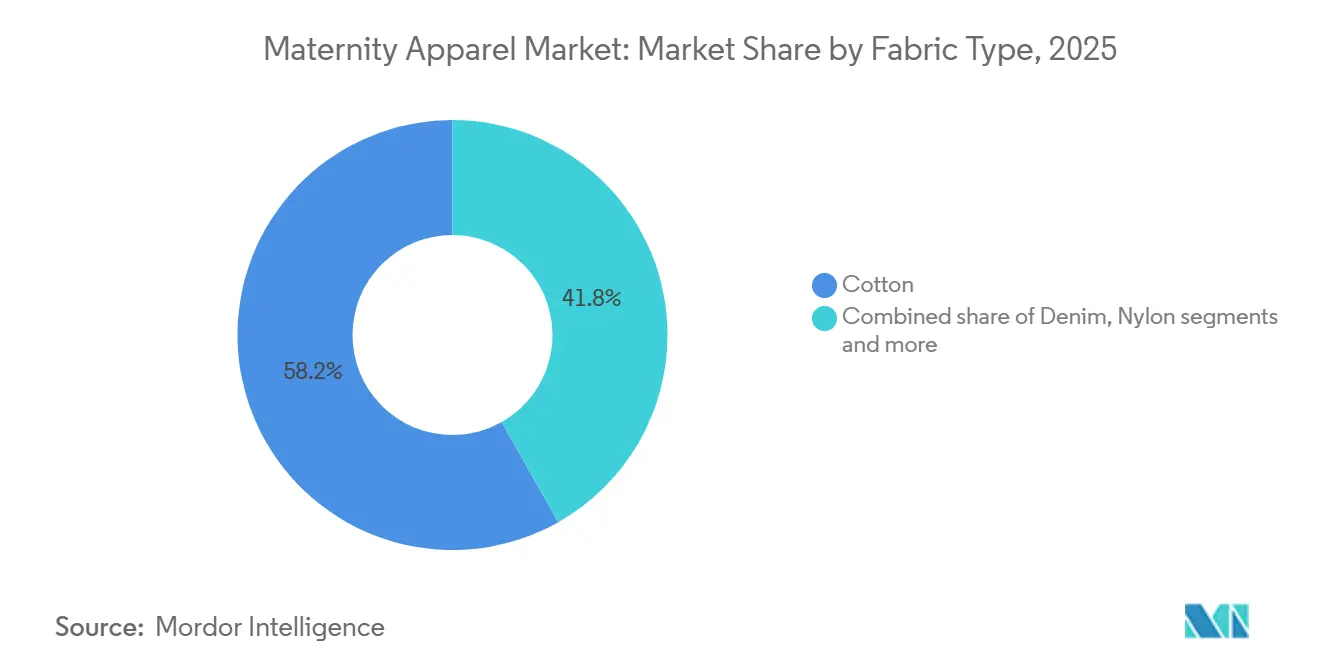

- By fabric type, cotton accounted for 58.18% of the maternity apparel market size in 2025, and denim is projected to grow at a 7.07% CAGR over 2026-2031.

- By distribution channel, offline retail accounted for 70.54% share of the maternity apparel market size in 2025, and online is advancing at a 7.11% CAGR through 2031.

- By geography, North America led with 39.40% revenue share in 2025; Asia-Pacific is set to post the fastest 7.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Maternity Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising number of pregnant working women | +1.2% | Global, with the strongest gains in India, Saudi Arabia, South Korea, Japan | Medium term (2-4 years) |

| Social media and celebrity influence on maternity fashion | +0.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Expansion of online and DTC retail models | +1.0% | Global, led by China, India, and North America | Short term (≤ 2 years) |

| Product innovation in adaptive and sustainable fabrics | +0.9% | North America, Europe, and premium segments in Asia-Pacific | Medium term (2-4 years) |

| Growing demand for active and wellness-focused maternity apparel | +0.7% | North America, Europe, urban China, and India | Medium term (2-4 years) |

| Increasing demand for luxury maternity apparel | +0.6% | North America, Europe, the Middle East, and tier-1 cities in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Social-media and celebrity influence on maternity fashion

Social media is reshaping maternity wear, elevating it from mere functionality to a canvas of personal style, and syncing it with mainstream fashion trends. Influencers and celebrities, from Rihanna's viral maternity moments to Hailey Bieber's minimalist ensembles and Blake Lively's red-carpet flair, are reshaping pregnancy's visibility and aesthetics. This cultural shift is driving demand for garments that echo pre-pregnancy styles, leading to a rise in expressive, body-positive designs. Brands like Di Petsa and Poster Girl are now featuring pregnant models in their campaigns, challenging old norms and celebrating the pregnant form's inherent style. High-street giants like H&M and ASOS have rolled out casual maternity lines, offering oversized blazers, crop tops, and ribbed co-ord sets, ensuring pregnant women can be trendy and comfortable. Luxury labels like Hatch and Isabella Oliver are also leaning into casual-chic with flattering linen tunics, knit sets, and wrap dresses. Consequently, maternity fashion is adopting fast-fashion's pace, pushing brands to quicken their design and production cycles to align with shifting seasonal trends. This transformation not only revitalizes the category but also carries profound psychological benefits, empowering women during this pivotal life stage.

Growing Demand for Active and Wellness-Focused Maternity Apparel

As medical and public health guidance increasingly validates the benefits of exercise during pregnancy, the sportswear segment is being reshaped by a growing demand for active and wellness-focused maternity apparel. While adoption remains relatively low, with CDC data indicating only about 10–13% of pregnant women meeting activity recommendations, this aspirational shift is fueling consumer interest in performance-focused maternity wear [1]Source: Centers for Disease Control and Prevention, “Physical Activity Guidelines During Pregnancy,” cdc.gov. Expectant mothers, now engaging in yoga, strength training, and other low-impact activities, seek apparel that adapts to their changing body mechanics, offers targeted support, and enhances mobility. Innovations in smart textiles are paving the way for features like fetal monitoring and temperature regulation, seamlessly integrating health tracking into garments without sacrificing comfort. Brands like Go Mama are reaping profits in this niche, while industry giants such as Nike (Maternity), Lululemon, and Ingrid & Isabel are rolling out purpose-designed maternity activewear. These offerings boast seamless construction, moisture-wicking fabrics, and four-way stretch. The wellness trend is broadening its horizons, extending beyond just fitness to encompass mental health and body positivity. This evolution is steering the segment towards a comprehensive maternity activewear ecosystem, addressing the movement needs of mothers from prenatal to postnatal stages.

Rising Number of Pregnant Working Women

Female labor-force participation reached 67.1 percent across OECD economies in Q3 2024, compared to 81% for men, and maternal employment rates averaged 71%, creating a structural demand base for workplace-appropriate maternity wardrobes that extend beyond casual loungewear[2]Source: OECD, “Labour Force Statistics Q3 2024,” oecd.org. The International Labor Organization reported in its G20 employment analysis that female participation surged in India, Saudi Arabia, South Korea, and Japan between 2020 and 2024, driven by policy reforms, remote-work normalization, and cultural shifts around maternal employment. Average paid maternity leave stood at 24.7 weeks globally in 2024, versus 2.2 weeks for paternity leave, giving mothers extended periods of workplace visibility during pregnancy and postpartum recovery. This dynamic favors brands that offer modular wardrobes, pieces that transition from office to casual settings, and explains why formal wear and casual wear together account for over 60% of the market despite sportswear's faster growth. The trend also pressures retailers to stock extended size ranges and adaptive fits, as working mothers prioritize comfort and professional appearance over trend-driven silhouettes.

Increasing Demand for Luxury Maternity Apparel

Luxury maternity apparel is witnessing a surge in demand, prompting a shift in consumer expectations from mere functionality to a focus on fashion and premium quality. This evolution is largely driven by affluent consumers, particularly millennials and Gen Z parents, who are emphasizing self-expression, sustainability, and designer aesthetics in their maternity choices. As of April 2025, the International Monetary Fund reported a global rise in disposable income, hitting USD 206.88 thousand per capita, bolstering the purchasing power for premium maternity options [3]Source: International Monetary Fund, World Economic Outlook Database, imf.org.. Brands such as Hatch and Seraphine are seizing this opportunity, curating elevated collections from organic and high-end fabrics. These collections, though priced at a premium, have found favor among style-conscious mothers. In 2024, bolstered by celebrity endorsements and influencer marketing most notably after Meghan Markle donned its tailored coat Seraphine broadened its Luxe Collection in response to heightened demand. In a parallel move, luxury retailer A Pea in the Pod collaborated with designer Monica + Andy, unveiling capsule maternity pieces crafted from premium cotton and adorned with bold prints, catering to those valuing both comfort and elegance. This pivot towards premiumization is not just amplifying average order values but also fostering brand loyalty and encouraging cross-category purchases, especially as numerous luxury maternity brands now cater to postpartum and nursing needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining fertility rates in developed countries | -0.9% | Europe, North America, East Asia (Japan, South Korea, China) | Long term (≥ 4 years) |

| Short product-usage lifecycle limiting repeat sales | -0.6% | Global | Short term (≤ 2 years) |

| High price sensitivity in low-income markets | -0.5% | South Asia, Sub-Saharan Africa, Latin America (excluding urban centers) | Medium term (2-4 years) |

| Online return rates raising logistics costs and carbon footprint | -0.7% | Global, most acute in North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Fertility Rates in Developed Countries

In 2024, the European Union recorded its lowest total fertility rate since 2001, dropping to 1.34. Germany, in 2025, noted a rate of 1.35, resulting in roughly 655,000 births, as reported by Eurostat. The OECD's average fertility rate was 1.43 in 2023. Notably, South Korea lagged at 0.72, the U.S. stood at 1.6, and China registered 1.0, all trailing the replacement rate of 2.1, according to the OECD Fertility Database. The World Bank highlighted a global fertility rate of 2.0 in 2024. Regionally, East Asia and the Pacific were at 1.3, while Sub-Saharan Africa stood out with a rate of 4.3, underscoring significant disparities. Global births, which peaked at 146 million in 2012, dwindled to about 132 million in 2024. This decline represents a nearly 10% shrinkage in the potential customer base over 12 years. Countries like Japan, Italy, Spain, and regions in Eastern Europe felt the brunt of this contraction. Here, aging populations and a trend towards delayed childbearing have narrowed the maternity-apparel market's age demographic. In response, brands are innovating. They're extending product utility, crafting items that seamlessly transition from pregnancy to postpartum use. Furthermore, they're diversifying their offerings, venturing into categories like nursing wear, garments for postpartum recovery, and even family-matching apparel, all to maximize revenue across an extended customer lifecycle.

Online Return Rates Raising Logistics Costs and Carbon Footprint

In 2024, global online apparel return rates surpassed 25%, with fast fashion brands seeing a spike to 35%. This surge was largely attributed to inconsistencies in fit rather than quality issues. When items are returned, they fetch only 40% to 60% of their original value. In the U.S. alone, over USD 23 billion worth of returned inventory became unsellable in 2024, leading to significant financial and environmental repercussions. Maternity apparel is particularly vulnerable to returns; as body dimensions shift weekly during pregnancy, traditional size charts fall short, resulting in increased orders and returns. For digitally native brands, the costs associated with reverse logistics, encompassing warehousing, inspection, repackaging, and restocking, can eat up 15% to 20% of gross revenue. This significantly diminishes the margin edge these brands have over traditional brick-and-mortar stores. Furthermore, carbon emissions from return shipments cast a shadow on sustainability claims. A single returned garment can emit between 20 and 30 kilograms of CO₂ equivalent, factoring in transportation, packaging, and disposal. In response, brands are experimenting with solutions like virtual fitting rooms (utilizing smartphone cameras for body measurements), AI-driven size recommendation tools tailored to pregnancy data, and "keep-it" discounts. These discounts encourage customers to hold onto items that are a marginal fit instead of returning them. Yet, despite their promise, these technologies are still in their infancy, with adoption lagging among older and less tech-savvy consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sportswear Disrupts Casual Dominance

In 2025, casual wear commands a dominant 41.59% market share, underscoring pregnant women's preference for versatile clothing that seamlessly transitions from home to work and casual outings. Responding to this demand, brands like Motherhood Maternity and The Mom Store have introduced offerings such as stretchable leggings, relaxed-fit tops, and bump-friendly dresses, balancing both functionality and aesthetics. The category's stronghold in the market is bolstered by its inherent adaptability, enabling consumers to make fewer yet more practical purchases that cater to various stages of pregnancy.

Sports wear emerges as the fastest-growing segment, boasting a 6.08% CAGR projected through 2031. This surge is largely attributed to the increasing emphasis on prenatal fitness and overall wellness. Brands like Fitta Mamma and Go Mama are at the forefront, providing moisture-wicking leggings and supportive bras, ideal for activities such as yoga and walking. On another front, formalwear remains a staple for working mothers, offering them polished and professional attire during their pregnancy journey. The intimate and shapewear segments are witnessing notable growth, exemplified by Bravado Designs' expansion of its U.S. retail footprint, catering to the rising demand for maternity-specific bras and supportive undergarments.

By Price Range: Premium Luxury Accelerates Despite Mass Dominance

In 2025, mass market segments dominate with a 61.69% share, fueled by cost-conscious consumers prioritizing practicality over fleeting maternity fashion trends. This trend underscores a demographic reality: for many, affordability and functionality take precedence over high fashion. This shift presents significant opportunities for brands like H&M, Mama, and Mothercare. These brands emphasize accessible pricing and efficient supply chains, offering basic styles that address everyday maternity needs without the hefty price tag. For example, H&M Mama's cotton maternity leggings, celebrated for their trimester-spanning versatility, stand out as bestsellers. Meanwhile, Mothercare's value-packed essentials resonate with middle-income families, offering a blend of reliable quality and daily comfort.

On the other hand, the premium luxury segment is witnessing the fastest growth, boasting a CAGR of 6.97% projected through 2031. Brands such as Hatch and Seraphine are at the forefront, capitalizing on high-quality materials, celebrity endorsements, and aspirational marketing strategies to woo affluent shoppers. A notable instance is Meghan Markle's endorsement of a Seraphine maternity dress, which not only spiked global demand but also positioned luxury maternity wear as a beacon of elegance and empowerment. Hatch's maternity dresses, crafted from stretch-enhanced silks and organic fabrics, frequently grace influencer wardrobes, promoting the narrative of pregnancy as a chic journey. Additionally, emerging mid-tier categories are striking a balance, merging functional designs with subtle aesthetic enhancements, appealing to consumers who desire both style and affordability.

By Fabric Material: Denim Innovation Challenges Cotton Leadership

In 2025, cotton commands a dominant 58.18% share of the maternity apparel market, thanks to its natural breathability, softness, and hypoallergenic qualities. These attributes are especially valued during pregnancy when skin sensitivity heightens. Mature supply chains and cost-effectiveness further bolster cotton's appeal, making it the preferred choice in both mass and mid-tier segments. Prominent maternity brands, including Mothercare and FirstCry, heavily incorporate cotton into essentials like nursing tops, lounge sets, and sleepwear, cementing its role as the cornerstone of comfort-centric maternity fashion.

Denim is rapidly gaining traction, with projections indicating a robust 7.07% CAGR growth rate through 2031. As maternity wear shifts from basic to style-centric, brands like Paige Maternity and Seraphine are at the forefront, utilizing stretch technology to craft jeans featuring elastic belly panels and adaptive waistbands. This innovation seamlessly merges structure with flexibility, ensuring extended wear. Additionally, technical fabrics such as spandex and nylon are pivotal in activewear and shapewear, facilitating form-fitting designs that adapt to a changing body. Brands like Blanqi and Kindred Bravely are harnessing these materials, offering performance-driven maternity essentials.

By Distribution Channel: Online Growth Challenges Offline Supremacy

In 2025, offline channels captured 70.54% of sales, led by department stores, specialty maternity retailers, and health-and-beauty outlets offering fitting services and immediate product availability. Online retail is set to grow at a 7.11% CAGR through 2031, driven by convenience for time-constrained expectant mothers and the rise of direct-to-consumer brands. Tmall's maternity and baby category reached 340 million users in 2025, including 100 million new customers and 56 million 88VIP members, showcasing its demand aggregation and data-driven merchandising capabilities. In India, The Mom Store served 300,000 to 500,000 women with over 5,700 products, shipping to 99.9% of pin codes, highlighting digital infrastructure's role in overcoming geographic fragmentation. House of Zelena raised USD 1.2 million in seed funding in September 2025, joining Indian DTC brands like Wobbly Walk, Morph Maternity, and Momzjoy, which target urban millennials with Instagram-first marketing and cash-on-delivery options.

Online expansion faces challenges, with return rates exceeding 25% for general apparel and 35% for fast fashion. Returned items recover only 40 to 60% of their value, contributing to over USD 23 billion in unsellable inventory annually in the U.S. Fit inconsistency drives most returns, prompting investments in virtual fitting rooms, augmented-reality try-ons, and AI-powered size recommendations. Offline channels retain advantages in fitting services, immediate gratification, and lower return rates but face margin pressures from rent, labor, and inventory costs. Hybrid models are emerging, such as Seraphine's Los Angeles boutique in partnership with Leap, which provides turnkey operations and data analytics, enabling physical retail exploration without long-term leases. Janie and Jack's London flagship combines product sales with a community area for events, emphasizing experiential retail's role in customer engagement.

Geography Analysis

In 2025, North America commands a dominant 39.40% share of the global maternity apparel market. This leadership is bolstered by a well-established retail infrastructure, robust consumer purchasing power, and a cultural inclination towards stylish professionalism during pregnancy. Legacy brands, such as A Pea in the Pod, alongside fresh collaborations with high-end designers, further cement the region's preeminence. These brands are reaping the benefits of workplace inclusivity trends and a heightened demand for chic maternity apparel, spanning categories from office attire to loungewear and activewear.

Asia-Pacific is the fastest-growing region, boasting a 7.82% CAGR projected through 2031. This surge is fueled by increasing disposable incomes, swift urbanization, and a burgeoning middle class that's adopting Western maternity fashion. In nations like India and China, there's a noticeable transition from basic, oversized garments to sleek, trend-savvy maternity choices. Indian brands, such as Momsoon and Mamma’s Maternity, are capitalizing on this shift, employing digital-first strategies to broaden access to fashionable maternity wear.

Europe, South America, and the Middle East and Africa are witnessing steady, albeit slower, growth, each influenced by distinct regional factors. In Europe, while demographic challenges like declining birth rates pose hurdles, high sustainability standards and a consumer tilt towards organic materials shape the offerings of premium brands. In contrast, emerging markets such as Brazil and the United Arab Emirates are seeing a surge in maternity wear demand, driven by increased female workforce participation and a rise in e-commerce.

Competitive Landscape

The market is highly fragmented the mainstream and niche players adopt diverse positioning strategies. Global giants like H&M, ASOS, and Gap utilize extensive retail networks and established brand equity to present maternity lines that seamlessly merge affordability with style. On the other hand, specialist brands such as Seraphine and Motherhood Maternity focus on functional designs tailored to the unique needs of pregnancy. Meanwhile, digitally native brands like Hatch employ lifestyle-centric marketing, leveraging influencer partnerships and emotional narratives to connect with image-conscious millennial and Gen Z mothers.

As brands tackle ongoing challenges like inconsistent sizing and evolving body shapes, technology emerges as a pivotal differentiator. Innovations such as AI-driven fit tools, 3D virtual try-ons, and smart fabrics are not only enhancing product performance but also personalizing the shopping experience. Highlighting this trend, activewear titan Nike is infusing its technical innovations into maternity lines, a move underscored in its 2024 SEC filing, signaling a wider industry pivot towards prioritizing comfort and functionality without sacrificing style.

The landscape is witnessing a transformation, driven by strategic maneuvers like mergers and innovative business models. The October 2024 acquisition of Hatch by Go Global Retail underscores a growing investor confidence in premium, digitally native maternity brands. The path to success lies in harmonizing innovation with emotional resonance, all while staying attuned to shifting consumer values.

Maternity Apparel Industry Leaders

H&M Group

Gap Inc.

Destination Maternity Corporation

ASOS

Wacoal Holdings Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Janie and Jack, under parent company Matri Group, opened its first UK flagship on King's Road in Chelsea, London, combining childrenswear with HATCH maternity under one dual-concept roof. The store features a dedicated community area for events and services, positioning the brand for experiential retail and long-term customer engagement.

- January 2026: Kindred Bravely acquired Storq, merging two direct-to-consumer maternity leaders to achieve economies of scale in customer acquisition, logistics, and product development. The combined entity will leverage Kindred Bravely's strength in intimates and nursing bras with Storq's reputation for OEKO-TEX-certified basics and postpartum recovery garments.

- October 2025: MARION and AXK Maternity merged under new parent company Haus of Her Group, consolidating two mid-tier brands to compete against fast-fashion incumbents and premium specialists. The combined portfolio includes work-friendly maternity pieces, jeans, and pajamas, with a focus on natural and recycled fabrics.

Global Maternity Apparel Market Report Scope

Maternity apparel consists of clothing specifically designed and tailored for pregnant women to accommodate the significant physical changes that occur during pregnancy. The global Maternity apparel market is segmented by product type, price range, fabric, distribution channel, and geography. By product type, the market is segmented into formal wear, casual wear, sports wear, night wear and lounge wear, intimate and shapewear, and others. By price range, the market is segmented into mass and premium/luxury. By fabric, the market is segmented into cotton, spandex, nylon, denim, and other fabric types. By distribution channel, the market is segmented into offline and online. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Formal Wear |

| Casual Wear |

| Sports Wear |

| Night Wear and Lounge Wear |

| Intimate and Shapewear |

| Others |

| Mass |

| Premium/Luxury |

| Cotton |

| Spandex |

| Nylon |

| Denim |

| Other Fabric Types |

| Online |

| Offline |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Formal Wear | |

| Casual Wear | ||

| Sports Wear | ||

| Night Wear and Lounge Wear | ||

| Intimate and Shapewear | ||

| Others | ||

| Price Range | Mass | |

| Premium/Luxury | ||

| Fabric | Cotton | |

| Spandex | ||

| Nylon | ||

| Denim | ||

| Other Fabric Types | ||

| Distribution Channel | Online | |

| Offline | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the global maternity apparel market size in 2026?

The maternity apparel market size is USD 22.09 billion in 2026, according to Mordor Intelligence.

How fast is the maternity apparel market expected to grow through 2031?

The market is projected to post a 5.44% CAGR between 2026 and 2031.

Which product type is growing quickest within maternity fashion?

Sportswear leads with a 6.08% CAGR, reflecting the surge in prenatal fitness and athleisure adoption.

Which region shows the strongest future growth?

Asia-Pacific is forecast to register the fastest 7.82% CAGR through 2031, propelled by expanding e-commerce in China and India.

Page last updated on: