Plus Size Clothing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

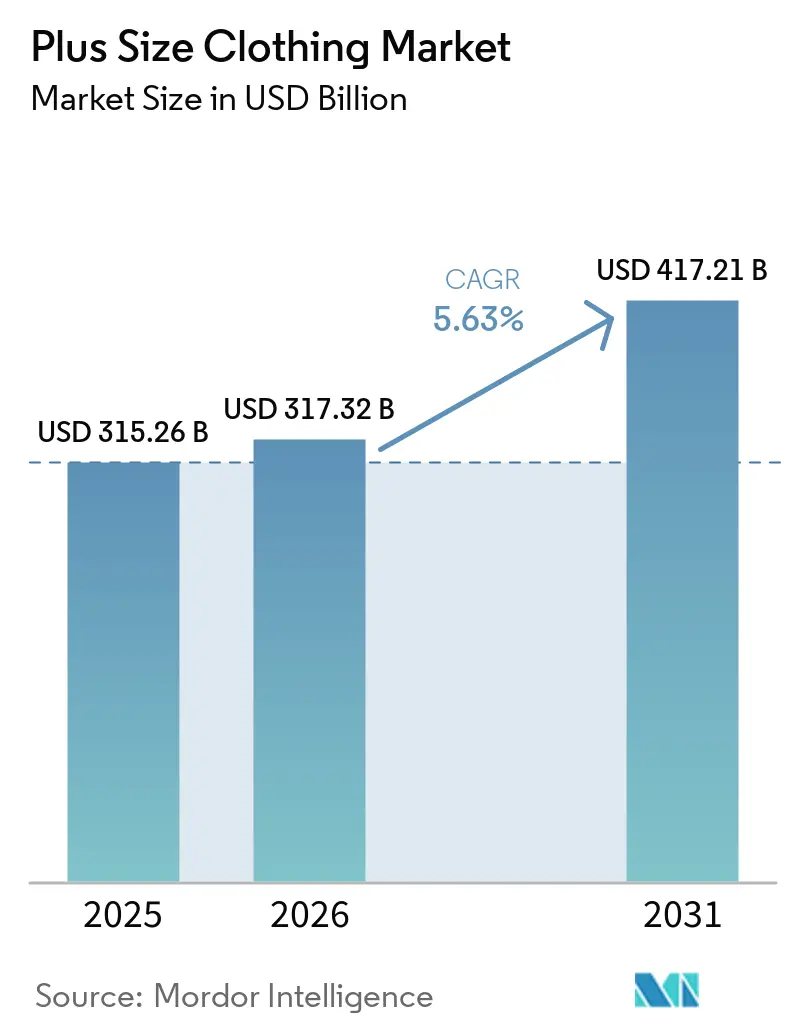

| Market Size (2026) | USD 317.32 Billion |

| Market Size (2031) | USD 417.21 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

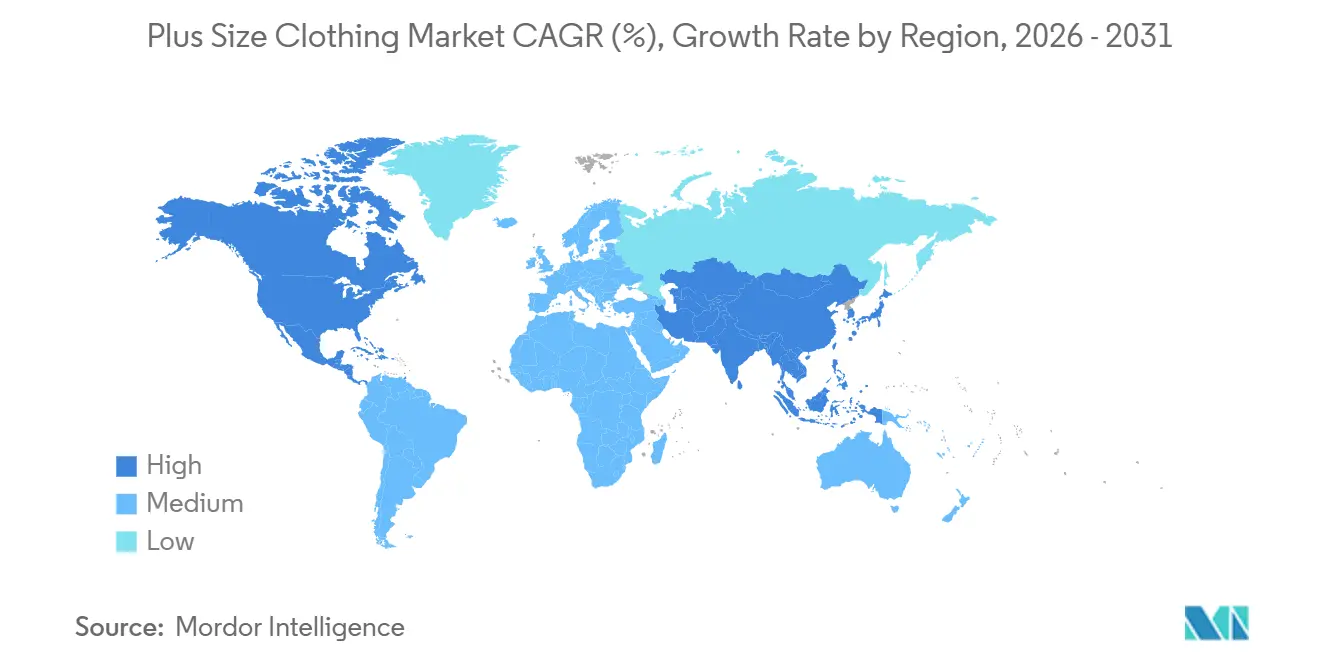

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Plus Size Clothing Market Analysis by Mordor Intelligence

The plus-size clothing market size is projected to expand from USD 315.26 billion in 2025 and USD 317.32 billion in 2026 to USD 417.21 billion by 2031, registering a 5.63% CAGR between 2026 and 2031. Growing demand for extended sizing is reshaping merchandising strategies as rising obesity rates intersect with a powerful body-positivity culture that celebrates diverse body types. Brands are embedding inclusive design into core product development, moving beyond token capsule lines and reducing costly returns that once stemmed from simply “scaling up” standard patterns. Digitally native labels reinforce this change by proving that superior fit and aspirational styling can command premium prices regardless of size. Meanwhile, virtual fitting tools are narrowing the confidence gap that traditionally kept many consumers in physical stores. Competitive intensity remains high, yet fragmentation leaves room for niche entrants to address adaptive wear, maternity, and region-specific fit variations.

Key Report Takeaways

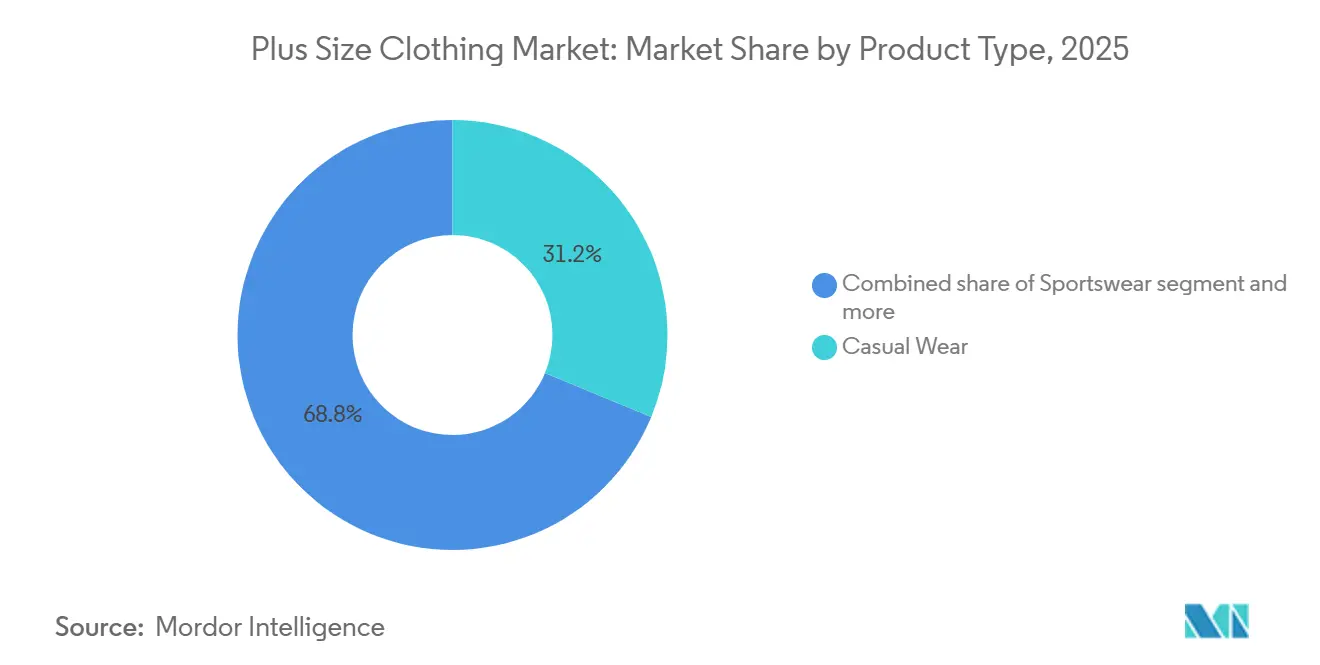

- By product type, casual wear led with 31.22% of plus-size clothing market share in 2025; sportswear is advancing at a 7.65% CAGR through 2031, fueled by athleisure adoption and inclusive performance fabrics.

- By end-user, men commanded 69.32% of the plus-size clothing market in 2025, while women’s apparel is expanding at a 7.58% CAGR on the back of influencer visibility and designer collaborations.

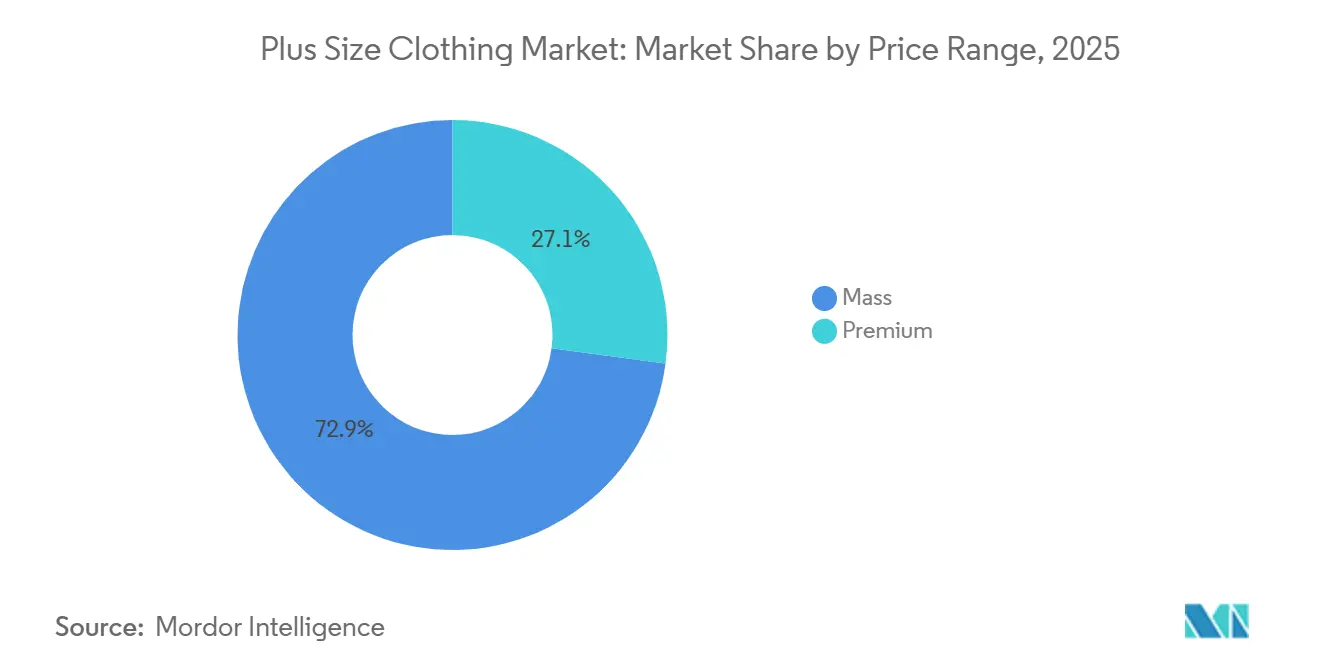

- By price range, mass products captured 72.89% share in 2025, yet premium and luxury offerings are growing at 6.44% CAGR as consumers pay for superior fabrics and precise grading.

- By distribution channel, offline stores accounted for 72.43% of 2025 sales, whereas online retail is rising at a 9.75% CAGR, enabled by Augmented Reality fitting rooms and social-commerce discovery.

- By geography, North America held 45.12% share in 2025, while Asia-Pacific is the fastest-growing region at a 5.48% CAGR as global brands enter historically into high potential markets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plus Size Clothing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Body-positivity movement | +0.9% | North America, Europe, spreading globally | Medium term (2-4 years) |

| Expanded brand sizing programs | +1.2% | North America, Europe, Asia-Pacific core markets | Short term (≤ 2 years) |

| Social-media driven demand spikes | +0.8% | Global urban centers with high digital penetration | Short term (≤ 2 years) |

| Increasing demand for luxury plus-size lines | +0.7% | North America, Europe, select Asia-Pacific cities | Medium term (2-4 years) |

| Rise of adaptive plus-size apparel | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Sports and activewear inclusivity | +1.0% | North America, Europe, growing globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Body positivity movement

Cultural shifts toward body acceptance are reconfiguring demand patterns, particularly among millennial and Gen Z consumers who reject traditional beauty standards. The young consumers actively seek brands that feature diverse body types in marketing campaigns, translating advocacy into purchasing power. This movement has compelled legacy brands to expand size ranges not as a corporate social responsibility gesture but as a revenue imperative. The impact extends beyond marketing; it influences product development cycles, with brands now designing for extended sizes from the outset rather than scaling up standard patterns, which historically resulted in poor fit and higher return rates. Regulatory bodies like the Federal Trade Commission in the United States have begun scrutinizing size-labeling practices, adding compliance pressure that reinforces the business case for authentic inclusivity.

Expanded brand sizing programs

Responding to consumer demand and competitive pressures, major apparel companies are expanding their size ranges. Nike's women's activewear in extended sizes has seen revenue growth surpassing the company's overall apparel growth. These initiatives extend beyond merely adding SKUs (Stock Keeping Units); they encompass retooling supply chains, retraining fit models, and fine-tuning inventory algorithms to avert stockouts in popular extended sizes. This heightened focus on size inclusivity signals a significant shift in the apparel market, where consumer demands for diversity and representation are reshaping product strategies. The trend highlights the growing importance of catering to a broader demographic, as consumers increasingly prioritize brands that reflect their values. The message is clear: brands that delay may cede ground to digitally native competitors like Universal Standard, which has built its entire value proposition around size inclusivity from the outset.

Social-media driven demand spikes

Influencer marketing has emerged as a primary demand driver, with plus-size content creators commanding engagement rates that rival or exceed mainstream fashion influencers. Platforms like Instagram and TikTok enable micro-influencers to showcase styling tips, haul videos, and brand reviews that directly convert followers into customers. A 2025 study, "A Study on plus-size Market and Plus-size Marketting", found that 70% of those surveyed expressed a greater inclination to buy from brands that consistently champion body diversity in their marketing efforts[1].Source: Zhuzao/Foundry Journal, "A Study on Plus-Size Market and Plus-Size Marketting", foundryjournal.net This underscores that embracing inclusive marketing isn't merely a fleeting trend; it's a strategic edge for brands looking to capture the loyalty of plus-size shoppers. Brands are capitalizing on this dynamic through affiliate partnerships and co-designed collections, effectively outsourcing trend forecasting to influencers who possess real-time insights into consumer preferences. This model is particularly potent in Asia-Pacific markets, where social commerce infrastructure allows seamless in-app purchasing.

Increasing demand for luxury and premium plus-size clothing

Plus-size fashion is undergoing a premiumization, breaking away from its historical ties to budget-tier offerings. Designer brands, such as Christian Siriano, have carved out a niche with their commitment to inclusive sizing. Siriano's 2024 runway showcased models ranging from sizes 0 to 22, a bold statement that garnered extensive media attention and translated into significant retail orders. This trend reflects a broader industry shift, where inclusivity is becoming a cornerstone of brand identity and market differentiation. In 2024, the demographic aged 45 to 60 emerged as the leading spenders in the women's and girls' clothing segment, averaging an expenditure of USD 942[2]Source: U.S. Bureau of Labor Statistics, “Consumer Expenditure Survey 2024,” bls.gov. This shift towards premium positioning is altering consumer expectations. This evolution highlights a crucial insight: plus-size consumers are not merely seeking fit; they desire premium aesthetics, high-quality fabrics, and a compelling brand narrative. The growing demand for premium plus-size fashion underscores the importance of addressing this market segment with innovation and authenticity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited shelf space for extended sizes | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Higher fabric and logistics costs per garment | -0.8% | Global, heaviest in mass-market segments | Medium term (2-4 years) |

| Inconsistent international sizing standards | -0.5% | Global, challenging cross-border e-commerce | Long term (≥ 4 years) |

| Supply-chain and inventory management hurdles | -0.7% | Global, amplified in fast-fashion operating models | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited shelf space for extended sizes

Physical retail environments impose strict limits on assortment breadth, compelling merchandisers to balance size range with style variety. This challenge arises from a cautious approach to inventory; historically, extended sizes have seen higher return rates and slower turnover, prompting buyers to limit their exposure. This limitation creates a cycle: a restricted selection pushes consumers online, reinforcing retailers' hesitance to broaden in-store offerings. In response, brands are testing "endless aisle" models, showcasing one size in-store while providing the full range through in-store tablets for home delivery. However, this method forgoes the tactile assessment crucial for apparel purchases. Retailers are also exploring hybrid approaches, such as offering limited in-store inventory for trial while integrating online fulfillment to cater to broader preferences. These strategies aim to strike a balance between operational efficiency and customer satisfaction.

Higher fabric and logistics costs per garment

Plus-size apparel faces unique challenges in unit economics, primarily due to material and shipping costs that escalate with size. For instance, a 3XL garment demands 30-40% more fabric than its medium counterpart. However, brands hesitate to adjust prices accordingly, fearing backlash from price-sensitive shoppers. This challenge deepens with logistics: larger garments take up more space in warehouses and shipping containers, driving up fulfillment costs per unit. Fast-fashion retailers, known for their slim margins, feel this pinch acutely. While some brands toy with tiered pricing to mirror actual costs, they've faced pushback on social media, stalling broader implementation. Additionally, the lack of standardized pricing strategies across the market further complicates efforts to address these issues. As raw material prices swing and sustainability regulations tighten, these challenges are poised to grow, potentially reshaping the competitive landscape for plus-size apparel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sportswear Accelerates on Athleisure Momentum

Casual wear retained the largest slice at 31.22% of plus size clothing market share in 2025, thanks to joggers, oversized tees, and hoodies that anchor everyday wardrobes. Elevated time at home during and after the pandemic entrenched comfort-first dressing habits, generating frequent replenishment cycles. Yet commoditization pressures margins, pushing mid-range retailers to experiment with elevated trims, gender-neutral styling, and limited-edition drops to sustain newness. Formal, nightwear, intimate, and maternity segments remain smaller but are diversifying quickly as brands recognize profit potential in well-served niches.

Sportswear’s contribution to the plus-size clothing market size climbed steadily and is projected to expand at 7.65% CAGR during 2026-2031, the highest across categories. Performance-grade leggings, moisture-wicking tops, and high-support sports bras are now engineered up to 6XL, closing the quality gap that once deterred active consumers. Nike and Adidas have partnered with plus-size athletes to validate technical credibility, while upstarts like Girlfriend Collective leverage recycled fabrics to capture eco-conscious shoppers. This wave lifts average selling prices and fortifies brand storytelling around empowerment and wellness.

By End-User: Women’s Growth Outpaces Men’s Scale

Men dominated revenue with 69.32% plus size clothing market share in 2025, supported by higher average order values and longer product lifecycles for shirts, denim, and outerwear. This trend is underscored by CDC (Centers for Disease Control and Prevention) data revealing that over 40% of United States adults grapple with obesity, with men notably more affected in various states[3].Source: World Obesity Federation, “World Obesity Atlas 2024,” World Obesity, worldobesity.orgSpecialty chains such as DXL and Johnny Bigg curate deep assortments that mainstream retailers rarely match, bolstering loyalty and reducing return risk.

Women’s apparel is the plus-size clothing market’s fastest-advancing end-user segment, registering a 7.58% CAGR for 2026-2031. Social-media personalities spotlight aspirational styling, amplifying demand for trend-driven blazers, slip dresses, and statement denim in sizes up to 40. Digitally native brands like Universal Standard embed “fit liberty” guarantees that let shoppers exchange garments as body shapes evolve, reinforcing trust. Unisex lines add modest incremental sales, attracting Gen Z consumers who value gender-fluid expression.

By Price Range: Premium Upshift Gains Momentum

In 2025, fast-fashion and value retailers, leveraging their scale purchasing power, dominated the plus-size clothing market with mass offerings capturing 72.89% of the share. While aggressive promotions boost foot traffic, they also squeeze profit margins. In response, retailers are channeling investments into advanced allocation systems to mitigate markdown risks. As sustainability concerns mount, even budget chains are feeling the pressure to incorporate recycled materials, a shift that strains their financials. The growing emphasis on eco-friendly practices is reshaping operational strategies, with companies exploring innovative ways to balance cost efficiency and environmental responsibility.

Meanwhile, the premium and luxury segments are on a growth trajectory, expanding at a 6.44% CAGR. This surge is driven by consumers increasingly viewing high-quality garments as valuable investments. Designer capsules, featuring luxurious materials like Italian wool and silk blends, along with couture-level draping, command prices that can easily be twice that of their mass-market counterparts. Furthermore, this premium tier enjoys limited discounting, bolstering brand equity and enhancing the average gross margin across the entire plus-size clothing market.

By Distribution Channel: Digital Leapfrogs Infrastructure Gaps

In 2025, offline venues dominated the plus-size clothing market, capturing 72.43% of sales, thanks to their appeal for tactile evaluations and instant purchases. Department stores are now adopting size-inclusive mannequins and expanding fitting rooms, aiming to elevate the in-store shopping experience. However, limited shelf space leads to curated selections, often leaving shoppers seeking specific fits or colors dissatisfied and pushing them towards online options. Despite these challenges, offline stores remain a preferred choice for many consumers who value the ability to try on clothing before purchasing.

Online retail is racing ahead at a 9.75% CAGR, thanks to AR-powered try-ons and creator-led merchandising that replicate word-of-mouth at scale. Subscription boxes such as Dia & Co ship personalized edits, letting customers keep what works and return the rest, shrinking friction in size discovery. Cross-border marketplaces also widen choice, though sizing discrepancies trigger elevated return rates. Even so, digital share will continue climbing as younger cohorts age into higher spending brackets and mobile commerce infrastructure matures.

Geography Analysis

North America contributed the largest regional block, holding 45.12% of plus size clothing market share in 2025. High obesity prevalence, robust discretionary income, and advanced e-commerce ecosystems together sustain top-line momentum. United States regulators have begun scrutinizing deceptive size labeling, nudging brands toward transparent measurement charts that ease cross-brand shopping. Canada mirrors these trends, with domestic labels like Addition Elle leveraging local fit data to improve pattern accuracy, while Mexico offers untapped upside as middle-income consumers seek branded alternatives to bespoke tailoring.

Asia-Pacific is projected to log the fastest regional growth at a 5.48% CAGR during 2026-2031, underpinned by rapid urbanization and evolving diets. China’s rising middle class demands Western-inspired streetwear extended to 6XL, whereas India’s nascent segment benefits from indigenous brands adapting kurtas and saree blouses for larger frames. Japan and South Korea show smaller absolute opportunity given lower obesity rates but exhibit outsized social-commerce uptake, which boosts visibility for inclusive labels. Australia, aligned culturally with North America, already houses specialty retailers like City Chic that export expertise throughout the region.

Europe, South America, and the Middle East and Africa collectively supply the remaining revenue. Europe’s stringent consumer-protection climate and initiatives such as the SizeEU project push companies toward standardized sizing, gradually building trust for cross-border digital sales. Brazil leads South America on the back of a vibrant influencer scene promoting body diversity, while Chile and Colombia follow. The Middle East’s opportunity is clustered in cosmopolitan centers like Dubai where international chains pilot inclusive offerings, though cultural sensibilities still moderate marketing approaches. Africa remains early stage, but textile capacity in countries like Ethiopia may emerge as a sourcing alternative for global players seeking cost efficiencies in the plus size clothing market.

Competitive Landscape

The plus-size clothing market exhibits fragmented competition, scoring low concentration metrics, with no single player commanding a dominant share. This fragmentation reflects the diversity of consumer preferences across product types, price points, and geographies, creating space for both global apparel giants and niche specialists. Legacy brands like Nike and Adidas are leveraging their scale and brand equity to expand into plus-size activewear, while fast-fashion retailers like ASOS and Boohoo compete on assortment breadth and rapid trend adoption. Digitally native brands such as Universal Standard and Eloquii have carved out positions by prioritizing fit innovation and inclusive marketing, often achieving higher customer lifetime values than mass-market competitors.

The competitive dynamic is further complicated by the entry of luxury brands like Ralph Lauren, which are repositioning plus-size apparel as aspirational rather than functional. The white-space opportunities abound in adaptive plus-size apparel, where brands like Tommy Hilfiger have demonstrated proof of concept but face limited competition. Maternity wear in extended sizes remains underserved, as does the intersection of plus-size and sustainable fashion, where brands that can credibly address both inclusivity and environmental responsibility will capture values-driven consumers.

Technology is emerging as a competitive differentiator, with companies investing in AI-powered sizing algorithms, virtual fitting rooms, and 3D body-scanning tools to reduce return rates and improve customer satisfaction. Patent filings in fit-prediction technologies have increased, with companies like Amazon and Walmart seeking to protect proprietary algorithms that match consumers to optimal sizes based on purchase history and body measurements. Smaller contenders are unsettling incumbents by leveraging influencer partnerships and community-building strategies that foster brand loyalty, a dynamic particularly evident in the women's segment where social media engagement translates directly into sales.

Plus Size Clothing Industry Leaders

-

Nike Inc.

-

Adidas AG

-

Ralph Lauren Corporation

-

Yours Clothing Limited

-

Universal Standard Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Parfait Pluss launched a plus-size lifestyle marketplace in India. The platform offers a range of inclusive fashion, wellness, and lifestyle products. This initiative signifies a pivotal moment in India's retail landscape, addressing a long-ignored void in size-inclusive offerings.

- May 2025: JCPenney, in collaboration with Ashley Graham, unveiled a new plus-size collection, offering sizes 12–24 in various categories. This launch aims to cater to the growing demand for inclusive sizing in the fashion market.

- February 2025: Lucy and Yak, in collaboration with True Fit, harnessed AI-driven sizing for its United States e-commerce platform, tapping into insights from 82 million shoppers. This partnership is expected to enhance the online shopping experience by providing more accurate size recommendations.

Global Plus Size Clothing Market Report Scope

The plus-size clothing market caters to individuals whose body measurements exceed standard sizing. This segment of the apparel industry is responding to the rising demand for inclusive fashion, providing stylish and comfortable options for those seeking extended sizes. The market is segmented by product type, end-user, price range, distribution channel, and geography. By product type, the market is segmented into formal wear, casual wear, sportswear, nightwear and loungewear, intimate and shapewear, and maternity wear. By end user, the market is segmented into women, men, and unisex. By price range, the market is segmented into mass-market and premium or luxury offerings. By distribution channel, the market is segmented into online retail platforms and offline retail stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report offers market size and forecasts in value (USD billion) for the above segments.

| Formal Wear |

| Casual Wear |

| Sportswear |

| Nightwear and Loungewear |

| Intimate and Shapewear |

| Maternity Wear |

| Women |

| Men |

| Unisex |

| Mass |

| Premium /Luxury |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Formal Wear | |

| Casual Wear | ||

| Sportswear | ||

| Nightwear and Loungewear | ||

| Intimate and Shapewear | ||

| Maternity Wear | ||

| By End-user | Women | |

| Men | ||

| Unisex | ||

| By Price Range | Mass | |

| Premium /Luxury | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the plus size clothing market become by 2031?

It is projected to reach USD 417.21 billion by 2031, expanding at a 5.63% CAGR from 2026 to 2031.

Why does men’s plus-size apparel still dominate revenue?

Higher average order values, earlier retail adoption, and lower return rates keep men at 69.32% share, even as women’s segment grows faster.

What is driving premiumization in extended sizes?

Consumers pay for superior fabrics and precise grading; luxury launches like Ralph Lauren’s 2024 line show margins four points above standard collections.

Which product category is growing fastest?

Sportswear leads with a 7.65% CAGR thanks to athleisure demand and inclusive performance fabrics.

Page last updated on: