Women Wear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

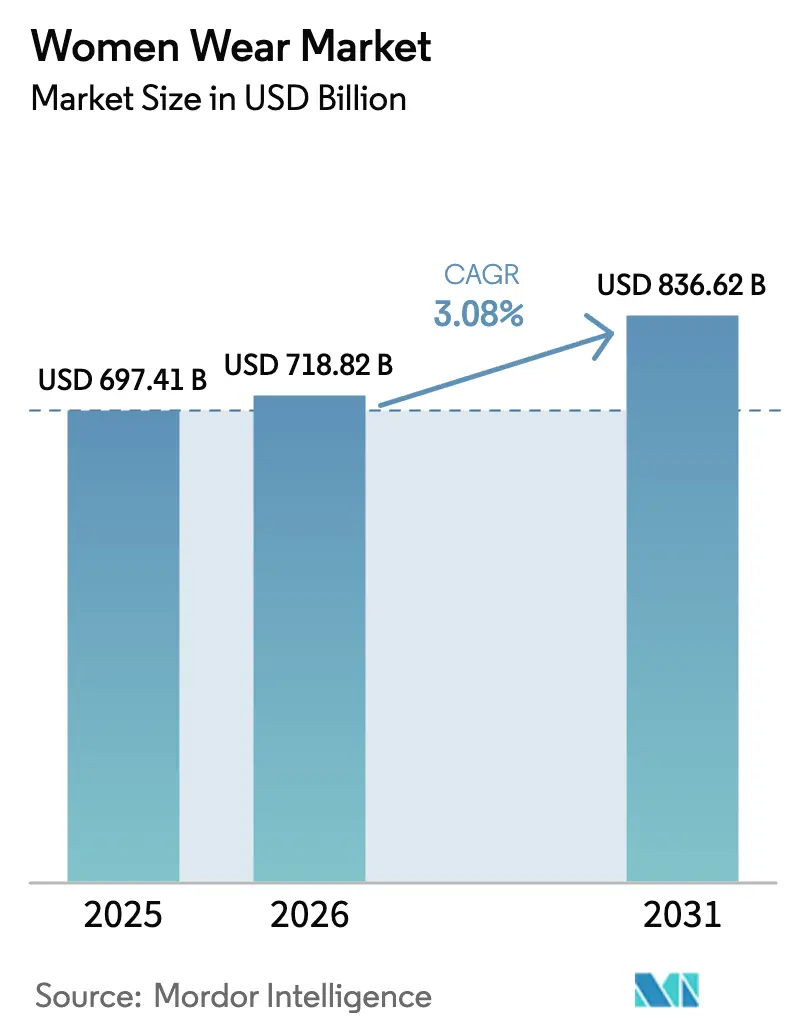

| Market Size (2026) | USD 718.82 Billion |

| Market Size (2031) | USD 836.62 Billion |

| Growth Rate (2026 - 2031) | 3.08% CAGR |

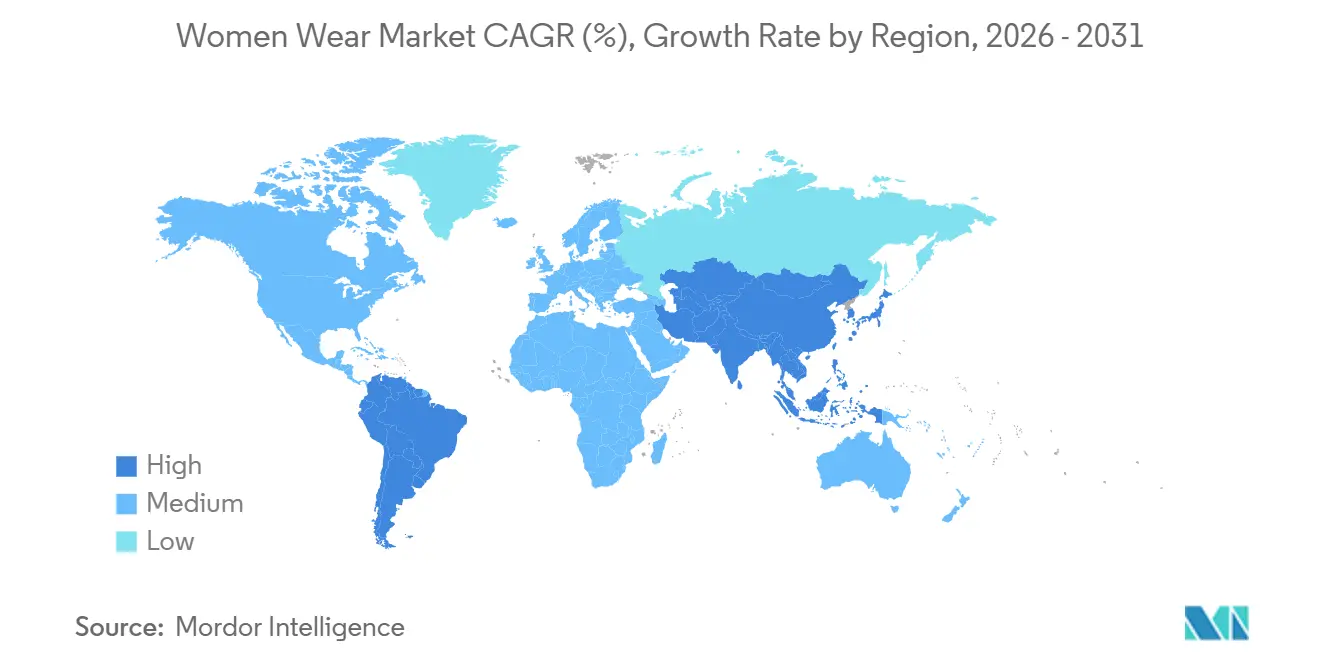

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Women Wear Market Analysis by Mordor Intelligence

The Women Wear Market size is expected to increase from USD 697.41 billion in 2025 to USD 718.82 billion in 2026 and reach USD 836.62 billion by 2031, growing at a CAGR of 3.08% over 2026-2031. Shifting consumer preferences and evolving views on fashion, identity, and lifestyle are transforming the women’s apparel market. Female shoppers today are increasingly focused on value, digital engagement, and sustainability, with greater emphasis on authenticity, ethical sourcing, and inclusivity rather than price or brand alone. Labels that promote body positivity, such as Aerie, along with brands known for transparent sustainability initiatives like Patagonia, are gaining stronger consumer traction. At the same time, wardrobes are becoming more versatile, reflecting lifestyles that blend remote work, wellness, and social activities. This has sustained demand for athleisure and hybrid apparel that offers comfort without sacrificing style. Digital innovation plays a critical role in shaping purchasing decisions, as AI-powered personalization, virtual try-on tools, and influencer-led content enhance online discovery and confidence in buying. Younger consumers, particularly Gen Z women, are at the forefront of this shift, favoring purpose-led brands that align with their social and environmental values. As a result, resale platforms and apparel rental services are gaining momentum, signaling a move toward viewing fashion as a service rather than ownership. Social commerce platforms such as Instagram and Pinterest further amplify this trend by seamlessly combining inspiration, community interaction, and direct purchasing.

Key Report Takeaways

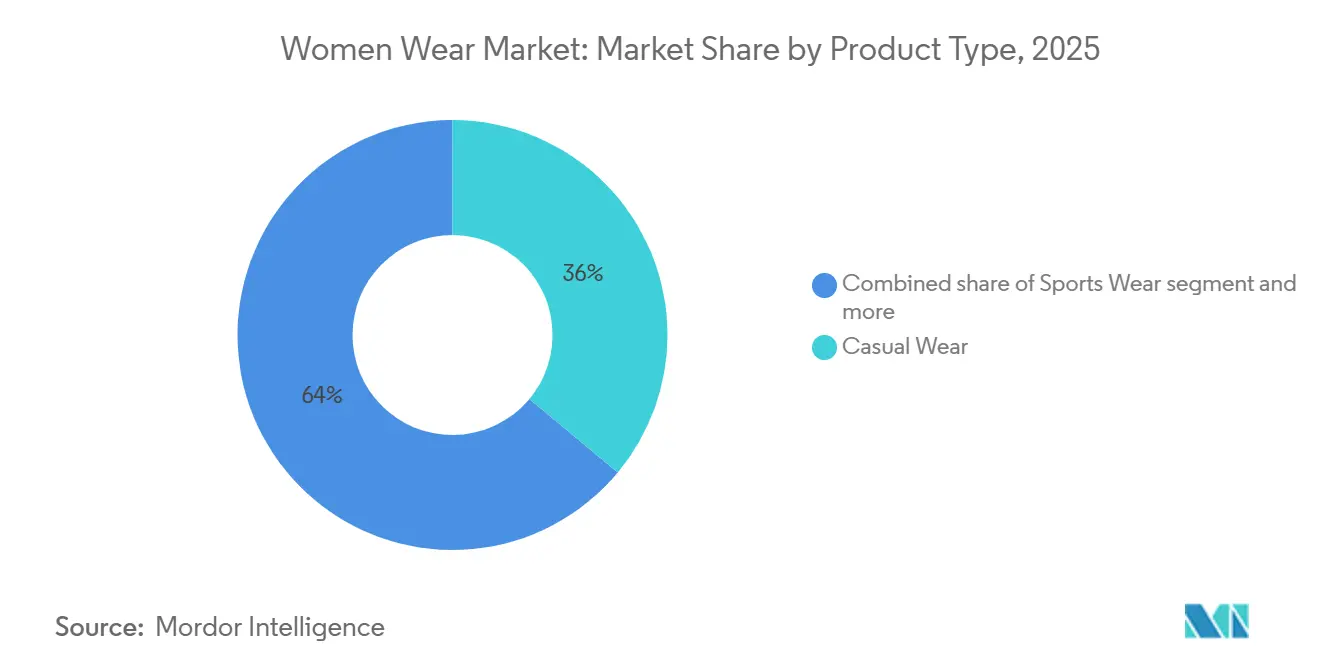

- By product type, casual wear led with 36.04% of the women’s apparel market share in 2025, while sportswear recorded the fastest 4.82% CAGR outlook to 2031.

- By category, normal wear captured 96.70% of the women’s apparel market in 2025, whereas maternity wear is forecast to grow at a 5.2% CAGR over 2026-2031.

- By price range, mass-market labels accounted for 68.47% revenue in 2025; premium and luxury are advancing at a 4.58% CAGR to 2031.

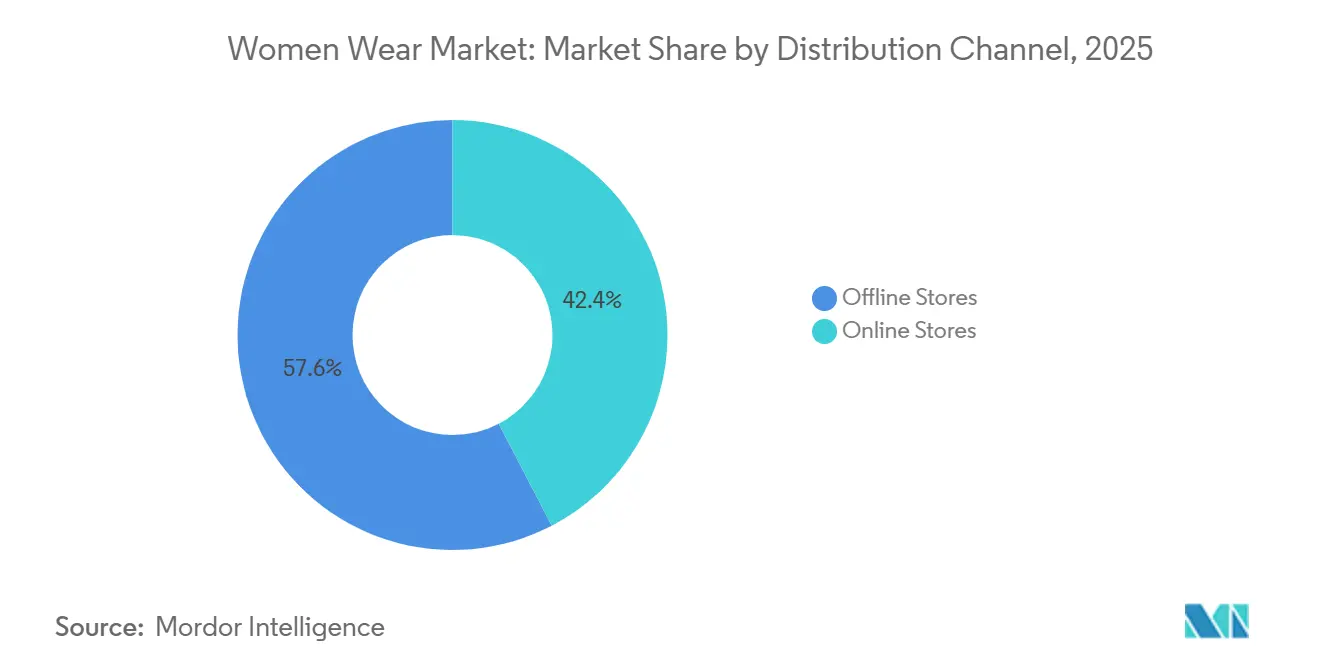

- By distribution channel, offline retail commanded 57.64% of 2025 revenue; online is projected to expand at a 4.15% CAGR through 2031.

- By geography, Asia-Pacific was the largest region, accounting for 36.49% of revenue in 2025, and is tracking a 4.75% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Women Wear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Number of Women in the Workforce | +0.6% | Global, with strongest effects in India, Indonesia, Saudi Arabia, and Southeast Asia | Long term (≥ 4 years) |

| Shifting Fashion Trends | +0.5% | Global, accelerated by social media in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Greater Preference for Luxury Clothing | +0.4% | North America, Europe, Middle East; selective growth in Asia-Pacific tier-1 cities | Medium term (2-4 years) |

| Growing Demand for Sportswear Due to Women's Active Lifestyles | +0.8% | Global, led by North America, Europe, urban Asia-Pacific | Short to Medium term (≤ 4 years) |

| Influence of Social Media and Advertising | +0.7% | Global, highest penetration in North America, Europe, Middle East, urban Asia | Short term (≤ 2 years) |

| Broadening Range of Sizes and Styles with Fashion Innovation | +0.5% | Global, regulatory push in Europe and North America for inclusive sizing | Medium to Long term (2-4+ years) |

| Source: Mordor Intelligence | |||

Rising Number of Women in the Workforce

Female labor-force participation reached 53% across OECD economies in 2024, yet regional disparities create pockets of asymmetric demand, according to the World Bank[1]Source: World Bank, “Labor Force Participation Rate, Female,” worldbank.org . Saudi Arabia's rate surged from 22% in 2018 to 34% in 2022, directly correlating with a 25% share of total retail spending now allocated to women's fashion and a fivefold increase in online penetration since 2019, according to the Saudi Fashion Commission. India's workforce formalization is pulling women into organized retail and e-commerce, with affordable premium segments, priced 20% to 40% above mass offerings, capturing a disproportionate share as disposable incomes rise. This dynamic elevates demand for versatile workwear, athleisure hybrids, and modular wardrobes that accommodate both professional and casual settings. The shift also pressures brands to expand size inclusivity and maternity lines, as working mothers seek garments that transition across life stages without sacrificing style or function.

Greater Preference for Luxury Clothing

Luxury apparel faces a bifurcated outlook, with clothing underperforming jewelry and accessories as consumers prioritize investment pieces over seasonal garments. Yet the premium/luxury segment in women's wear is forecast to grow at 4.58% CAGR through 2031, 49% faster than the market average, because it captures aspirational spending from upper-middle-income cohorts rather than ultra-high-net-worth individuals. Midmarket brands offering elevated design at accessible price points, think COS, Sandro, Maje, are gaining share as traditional luxury houses raise prices to offset volume declines, inadvertently pricing out younger buyers. The Middle East exemplifies this: UAE consumers spend USD 1,600 per capita annually on fashion versus USD 500 in Saudi Arabia, with 34% of Dubai shoppers reporting they purchase without checking cost, yet 69% are attracted by exclusive rewards programs that blend status signaling with value, according to the Dubai Chamber of Commerce[2]Source: Dubai Chamber of Commerce, “UAE Fashion Outlook 2024,” dubaichamber.com.

Influence of Social Media and Advertising

Social platforms now drive the majority of purchase discovery for women under 35, with TikTok and Instagram influencers wielding credibility that surpasses traditional celebrity endorsements by 40% to 60% in conversion metrics. This dynamic compresses the marketing funnel: a viral post can generate 50,000 orders within 72 hours, but also exposes brands to reputational risk if quality or ethics fall short, as seen when design-theft lawsuits against Shein in July 2023 sparked consumer backlash despite the company's 20% global fast-fashion share. Retailers are responding by embedding shoppable content directly into social feeds and deploying micro-influencers with 10,000 to 100,000 followers, who deliver 3x to 5x higher engagement rates than macro-influencers at one-tenth the cost. The Middle East showcases extreme penetration: 75% of Saudi fashion purchases are influenced by digital channels, and 90% of recent growth came from online, underscoring how social commerce can leapfrog physical retail in markets with high smartphone adoption and young demographics, according to the Saudi Fashion Commission[3]Source: Saudi Fashion Commission, “Saudi Fashion Market Report 2024,” fashioncommission.gov.sa.

Broadening Range of Sizes and Styles with Fashion Innovation

Inclusive sizing has shifted from a niche positioning to a competitive necessity, driven by body-positivity movements and regulatory scrutiny. The European Union's textile strategy and evolving ISO standards for garment sizing are pressuring brands to expand beyond traditional size ranges, while plus-size segments in North America and Europe are growing 1.5x to 2x faster than standard sizes. Maternity wear exemplifies this shift: the category is expanding at 5.20% CAGR through 2031, with Asia-Pacific holding 38.5% share, yet product innovation remains concentrated in North America and Europe, where brands like Kindred Bravely reported 30% sales growth in January 2025 after launching an Eco-Luxe line using TENCEL and organic cotton. Shapewear is similarly evolving: Knix introduced customizable shapewear with PerfectCut technology in October 2024, targeting the global market by prioritizing comfort over compression, a pivot that aligns with the 71% of European consumers who express sustainability concerns but the 3% who actually pay premiums, suggesting that functional innovation may unlock willingness-to-pay better than ethical appeals alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Counterfeit and Unorganized Markets | -0.4% | Global, concentrated in Asia-Pacific, Middle East, Africa, Latin America | Short to Medium term (≤ 4 years) |

| High Costs Associated with Luxury Brands | -0.3% | Global, most acute in Europe, North America, select Asia-Pacific cities | Medium term (2-4 years) |

| Volatility in Raw Material Prices | -0.5% | Global, supply-chain dependencies in cotton (US, India), polyester (China, Southeast Asia) | Short term (≤ 2 years) |

| Supply Chain Disruptions and Evolving Regulatory Standards | -0.6% | Global, tariff impacts in North America, forced-labor scrutiny in Asia-Pacific sourcing | Short to Medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit and Unorganized Markets

The OECD and European Union Intellectual Property Office estimate that counterfeit apparel represents 5% to 7% of the global clothing trade, with Asia-Pacific, the Middle East, and Africa bearing disproportionate exposure due to weaker enforcement and fragmented retail landscapes[4]Source: OECD & EUIPO, “Trade in Counterfeit Apparel,” oecd.org. This erosion is compounded by unorganized markets, street vendors, informal e-commerce, and gray-market imports, which undercut branded pricing by 40% to 70%, particularly in India, Indonesia, Nigeria, and Egypt, where formal retail penetration remains below 30%. The proliferation undermines brand equity and margin realization, as consumers who purchase counterfeits often experience quality failures that taint perceptions of the legitimate product. Digital marketplaces amplify the challenge: platforms hosting third-party sellers struggle to verify authenticity at scale, and cross-border shipments exploit regulatory gaps. Brands are investing in blockchain-based authentication, RFID tagging, and direct-to-consumer channels to reclaim control, yet the cost of enforcement, estimated at 2% to 4% of revenue for luxury houses, crimps profitability and diverts capital from innovation.

Volatility in Raw Material Prices

Cotton prices oscillated between USD 0.75 and USD 0.95 per pound during 2024-2025, driven by weather disruptions in the United States and India, geopolitical tensions affecting Black Sea exports, and speculative trading. Polyester, which accounts for over 50% of global fiber consumption, saw crude-oil-linked feedstock costs swing by 20% to 30% quarter over quarter, compressing margins for mass-market players who lack hedging sophistication or vertical integration. The United States Fashion Industry Association documented that 100% of surveyed companies ranked tariffs and input-cost volatility as their top operational challenges in 2024, with proposed de minimis suspension threatening to raise landed costs for direct-to-consumer shipments by 15% to 25%[5]Source: United States Fashion Industry Association, “Benchmarking Survey 2024,” usfia.org. Brands are responding through nearshoring, Mexico, Central America, and Turkey for North American and European markets, and by locking in multi-year contracts with mills, yet these strategies reduce flexibility to pivot toward trending fabrics or sustainable alternatives. The transition to lower-impact fibers adds complexity: Inditex achieved 73% lower-impact fiber usage in 2024, but organic cotton and recycled polyester command 20% to 40% premiums over conventional inputs, forcing trade-offs between sustainability commitments and price competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sports wear Momentum Challenges Casual Dominance

Casual wear held 36.04% of market share in 2025, reflecting its ubiquity across demographics and occasions, yet sportswear is expanding at 4.82% CAGR through 2031, as activewear transcends gym settings to become everyday attire. This divergence signals a structural shift where comfort, versatility, and performance fabrics now define mainstream fashion, eroding the boundaries between casual and athletic categories. Nike's February 2025 partnership with Skims exemplifies this convergence, blending performance textiles with shapewear silhouettes to capture the loungewear-to-gym continuum, while Adidas launched Stay In Play maternity activewear in July 2024, targeting the USD 8.3 billion global maternity innerwear market, which is expanding at a 6.8% CAGR.

Nightwear and loungewear surged during 2020-2022 but have since normalized, growing in line with the market baseline as consumers rebalance wardrobes toward outerwear. Intimate and shapewear are pivoting toward comfort-first designs, wireless bras, seamless construction, and breathable fabrics that align with body-positivity movements and reject traditional compression aesthetics. The "Others" category, encompassing ethnic wear, occasion-specific garments, and niche segments, benefits from cultural celebrations and social events resuming post-pandemic, particularly in Asia-Pacific and the Middle East where festivals and weddings drive concentrated spending. Brands that straddle multiple product types, such as Lululemon's expansion from yoga pants into running, training, and casual lines, are capturing disproportionate share by offering ecosystem solutions rather than standalone items, a strategy that lifts average transaction values by 25% to 40%.

By Category: Maternity Segment Outpaces Traditional Wear

In 2025, normal wear commands a dominant 96.70% share of the women's wear market, underscoring its enduring appeal across diverse age groups and life stages. This segment's supremacy is bolstered by its versatility and consistent year-round demand. Brands such as Zivame and Global Desi curate extensive collections, catering to everyday needs, casual outings, and work-from-home attire. Meanwhile, W by TCNS is evolving its normal wear offerings, seamlessly blending functional fabrics with sustainable materials, ensuring consumers are drawn in by both comfort and style.

On the other hand, maternity wear is the market's rising star, boasting a robust 5.2% CAGR from 2026 to 2031. An increasing appetite for stylish and comfortable maternity apparel drives this growth. Brands like Momsoon and The Mom Store are stepping up, offering size-inclusive collections that marry style with practicality. They're catering to women who desire outfits that evolve with their bodies yet retain aesthetic appeal. Moreover, designs like nursing-friendly wrap dresses and stretchable athleisure are gaining traction, especially among working mothers. Recognizing the segment's potential, major players like H&M MAMA are amplifying their presence in metropolitan areas and online platforms.

By Distribution Channel: Digital Acceleration Reshapes Retail Landscape

As of 2025, offline retail stores command a 57.64% share of the women's wear market, driven by consumers' preference for tactile engagement, immediate gratification, and personalized service. Brands are bolstering this offline dominance by enhancing their brick-and-mortar presence. For example, H&M is rolling out expansive stores with exclusive women's wear sections. Meanwhile, Fabindia has set up experience centers that feature personal styling and wellness areas. In a similar vein, House of Masaba is making strides into Tier 1 and Tier 2 cities via lifestyle malls, boosting the offline presence of contemporary ethnic wear.

On the other hand, online retail is emerging as the fastest-growing channel, boasting a 4.15% CAGR from 2026 to 2031. This growth is attributed to the allure of convenience, AI-driven personalization, and a surge in digital adoption. Brands like Zara are leveraging AI tools to refine product searches, while Nykaa Fashion harnesses real-time analytics for tailored recommendations in women's categories. Additionally, platforms such as Ajio and Tata CLiQ are adopting virtual trial rooms and AR fit tools to minimize returns and bolster shopper confidence. Myntra's MyStylist AI and Amazon's Fashion Feed further amplify engagement by curating style inspirations tailored to user preferences, underscoring a significant shift towards digital-first apparel shopping.

By Price Range: Premium Growth Challenges Mass Market Dominance

In 2025, mass market segments command a dominant 68.47% share of the global women's wear market. This trend highlights the influence of price-driven consumer behavior, a response to ongoing inflation, rising living costs, and stagnant wages in major economies. Retail giants like H&M and Primark spearhead this segment, delivering trend-forward collections at wallet-friendly prices. They achieve this by harnessing their scale, efficient supply chains, and advanced digital inventory systems. Meanwhile, Shein, a brand born in the digital realm, has revolutionized the fast-fashion landscape. With its lightning-speed production cycles and design decisions rooted in data, Shein is not only reshaping the mass market but also winning over the budget-conscious Gen Z demographic worldwide.

On the other hand, the premium and luxury segments are on an upward trajectory, boasting a projected 4.58% CAGR from 2026 to 2031. This growth is largely driven by increasing affluence in the Asia-Pacific and Middle Eastern regions, coupled with a notable shift towards conscious consumption. Esteemed brands like Gucci and Chanel are solidifying their market position by blending their rich heritage with modern innovation, rolling out bespoke and sustainable collections. At the same time, brands positioned in the accessible luxury space, such as Reiss and Sézane, are appealing to aspirational buyers with their limited editions and refined basics. This evident divide in pricing segments paves the way for hybrid brands. These players, like Everlane, adeptly merge the efficiency of mass-market strategies with a premium allure. Everlane, for instance, holds radical transparency, allowing it to command higher price points while still appealing to a broader audience.

Geography Analysis

Asia-Pacific commanded 36.49% of global women's wear sales in 2025 and is forecast to expand at 4.75% CAGR through 2031, outpacing all other regions due to a convergence of demographic, economic, and digital factors that are reshaping consumption patterns. China remains the largest single market, yet growth is moderating as the economy rebalances toward services and consumers prioritize experiences over goods. India is the region's velocity engine, with fast fashion and affordable premium segments, priced 20% to 40% above mass offerings, capturing disproportionate share as female workforce participation rises and urbanization accelerates. Indonesia, Thailand, and Vietnam are emerging as both consumption hubs and sourcing alternatives to China, with the USITC highlighting their competitiveness in garment manufacturing and improving infrastructure for e-commerce fulfillment. Japan and South Korea exhibit mature, saturated markets where growth hinges on premiumization and niche innovation, such as technical fabrics, adaptive clothing, and sustainable lines, that command 30% to 50% price premiums over standard offerings.

North America and Europe collectively account for the majority of global sales in 2025, but both regions face structural headwinds that constrain growth to 2.5% to 3.0% CAGR through 2031, below the market baseline. The United States remains the largest single-country market, yet the USFIA reported that 100% of surveyed companies cited tariffs as their top challenge in 2024, with proposed de minimis suspension threatening to raise landed costs for direct-to-consumer shipments by 15% to 25%, particularly affecting ultra-fast-fashion players like Shein that rely on cross-border micro-shipments. Store traffic declined 26% in the UK, 21% in France, and 18% in Germany between 2019 and 2024, forcing retailers to close underperforming locations and invest in omnichannel integration, with online penetration approaching 60% in the UK and 48% across the EU by 2025 according to Eurostat. Western Europe generated USD 470 billion in fashion sales in 2024, with the UK contributing 22%, Germany 18.5%, and Italy 17.1%, yet Italy's 4.6% household spend on clothing, the highest in the region, underscores how cultural affinity for fashion can sustain demand even amid economic stagnation, according to Eurostat. The European Union's textile strategy and evolving sustainability regulations are pressuring brands to adopt circular models, with 71% of consumers expressing concern but only 3% paying premiums, exposing a 68-percentage-point intention-action gap that complicates long-term positioning.

South America, Middle East, and Africa represent high-growth pockets with distinct dynamics. The Middle East is experiencing a fashion renaissance, driven by female workforce participation rising westernization of dress codes, and digital channels capturing 90% of recent incremental growth. The UAE's fashion market is forecast to expand from USD 23.54 billion in 2024 to USD 41 billion by 2029, with e-commerce penetration climbing from 8.2% to 17.5% by 2027, and women accounting for 80% of Dubai fashion spending, with 34% purchasing without checking cost, according to the Dubai Chamber of Commerce. South America's organized retail penetration remains below 40% in Brazil, Argentina, and Colombia, limiting brand reach but also signaling white-space opportunities for players willing to navigate currency volatility, import tariffs, and fragmented distribution networks. Africa's fashion market is nascent but accelerating, with Nigeria, Egypt, South Africa, and Morocco exhibiting rising middle-class populations, smartphone adoption exceeding 60%, and growing appetite for both global brands and locally designed garments that reflect cultural identity. Regulatory frameworks in these regions are evolving, with the African Continental Free Trade Area (AfCFTA) reducing intra-regional tariffs and potentially unlocking cross-border e-commerce at scale.

Competitive Landscape

Women's wear market is moderately consolidated, with manufacturers opting for distinct marketing strategies to carve out their niche. Established brands lean on their heritage and aspirational branding, while newcomers craft targeted narratives via direct-to-consumer (DTC) models, influencer partnerships, and inclusive campaigns. For example, Savage X Fenty champions body positivity and diversity, resonating with younger audiences. Likewise, Cider and House of CB harness viral social media, swiftly adopt trends, and curate community content, enabling rapid growth despite a limited physical footprint.

Technology has become the linchpin of competitive edge in the women's wear sector, with firms pouring investments throughout the value chain. Leveraging AI for product recommendations, virtual fitting rooms, real-time inventory tweaks, and predictive design, brands harness technology to boost conversions and curtail overproduction. Inditex stands as a testament to this evolution, channeling EUR 1.8 billion in 2025 towards retail digitization and sustainable innovations, including a collaboration with Galy for lab-grown cotton. In a similar vein, H&M Group taps into AI for sharper trend forecasting and a more agile supply chain, cutting down waste and swiftly aligning with consumer desires.

Manufacturers are increasingly focusing on consolidation, international expansion, and sustainability-led collaborations to strengthen their market foothold. Saks Global's formation, stemming from Hudson's Bay Company's USD 2.7 billion takeover of Neiman Marcus, underscores a rising trend of luxury retail consolidations aiming to rejuvenate classic department store formats. Concurrently, firms like PVH Corp are navigating the delicate balance of long-term growth and immediate shareholder returns, employing assertive financial maneuvers such as share buybacks.

Women Wear Industry Leaders

H&M Group

Nike Inc.

Adidas AG

PVH Corp.

Inditex SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Mango invested in The Post Fiber to escalate textile-waste recycling capacity, aligning with circularity targets.

- March 2025: Nike and Skims unveiled NikeSkims inclusive activewear, lifting Nike’s market value by USD 6.7 billion.

- January 2025: Hudson’s Bay Company closed the USD 2.7 billion Neiman Marcus Group deal, birthing Saks Global.

- August 2024: Savage X Fenty entered 16 Nordstrom locations, marking its first U.S. department-store pact.

Global Women Wear Market Report Scope

The scope covers key segments by product type, category, price range, distribution channel, and geography, offering insights into evolving consumer preferences, purchasing behavior, and the competitive dynamics shaping the market. By product type, the market is segmented into casual wear, formal wear, sportswear, nightwear and loungewear, intimate and shapewear, and other apparel categories. This segmentation examines demand trends across everyday wear, occasion-based clothing, performance-oriented apparel, and comfort-focused garments. Based on category, the market is classified into maternity wear and normal wear, capturing variations in design, functionality, and lifecycle-driven demand. By price range, the report analyzes the mass and premium/luxury segments, highlighting differences in brand positioning, pricing strategies, and consumer spending patterns. In terms of distribution channels, the market is divided into online and offline retail stores, highlighting the growing role of e-commerce alongside traditional brick-and-mortar formats in driving sales and brand engagement. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with regional analysis focusing on fashion adoption, income levels, digital penetration, and cultural influences. The report includes historical data and forward-looking estimates for all segments, exclusively in value (USD) terms, along with an assessment of key growth drivers, challenges, trends, and the competitive landscape of the women’s wear market.

| Casual Wear |

| Formal Wear |

| Sports Wear |

| Night Wear and Lounge Wear |

| Intimate and Shapewear |

| Others |

| Maternity Wear |

| Normal Wear |

| Mass |

| Premium/Luxury |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Belgium | |

| Poland | |

| Sweden | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Casual Wear | |

| Formal Wear | ||

| Sports Wear | ||

| Night Wear and Lounge Wear | ||

| Intimate and Shapewear | ||

| Others | ||

| Category | Maternity Wear | |

| Normal Wear | ||

| By Price Range | Mass | |

| Premium/Luxury | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Belgium | ||

| Poland | ||

| Sweden | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the women’s apparel market in 2026?

The women’s apparel market size stands at USD 718.82 billion in 2026 and is set to reach USD 836.62 billion by 2031 at a 3.07% CAGR.

Which region contributes the most revenue?

Asia-Pacific holds the lead with 36.49% revenue in 2025 and is also the fastest-growing region at 4.75% CAGR through 2031.

Which product segment is growing the fastest?

Sports Wear is forecast to expand at a 4.82% CAGR, outpacing all other product categories.

How important is online retail to future growth?

Online channels are projected to grow at 4.15% CAGR as personalization tools and virtual try-ons enhance shopper engagement.

Page last updated on: