Women's Swimwear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.05 Billion |

| Market Size (2031) | USD 15.94 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

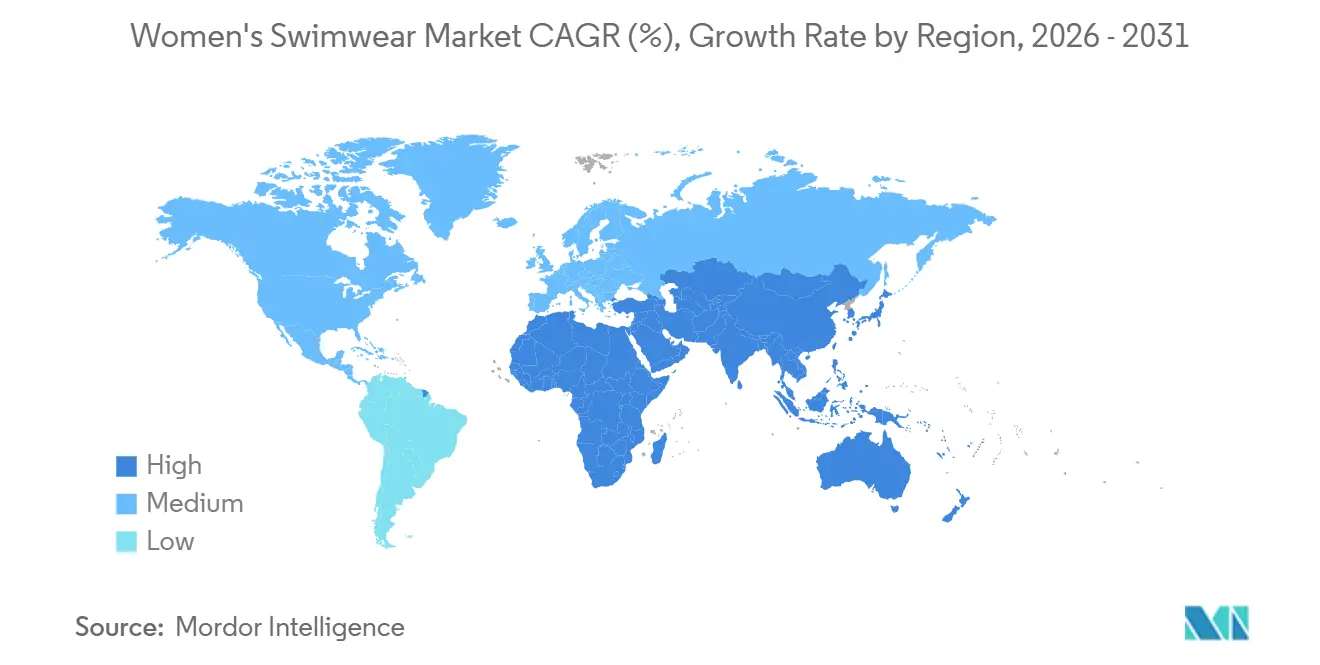

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Women's Swimwear Market Analysis by Mordor Intelligence

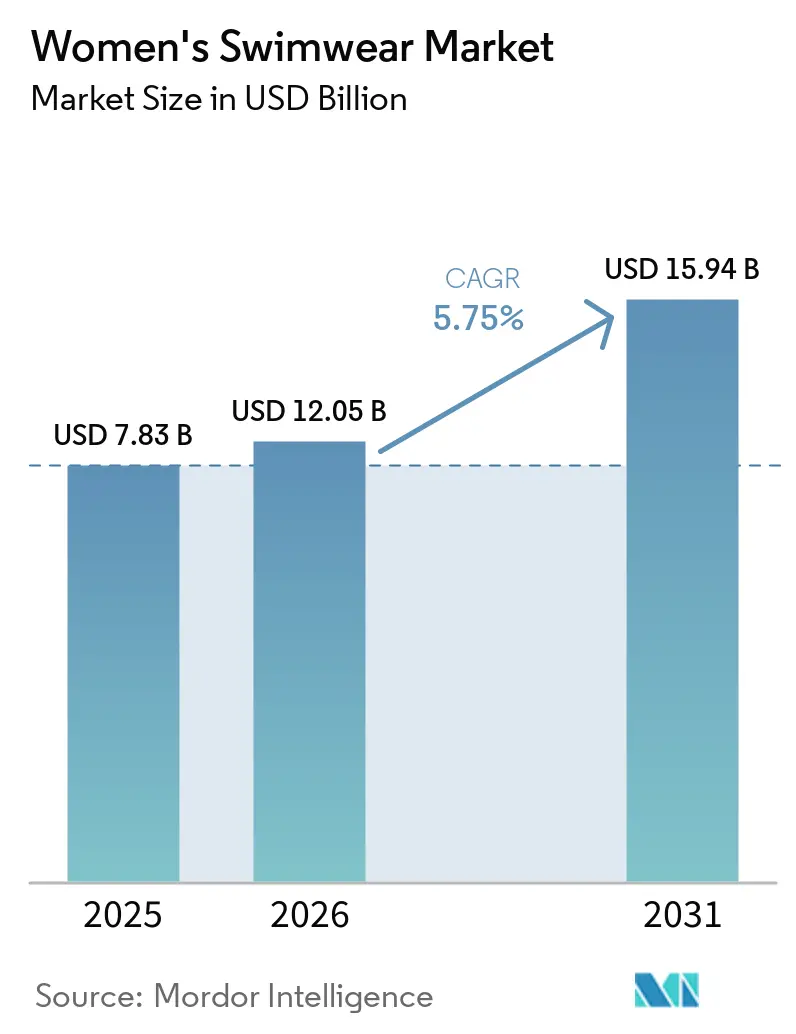

In 2025, the women's swimwear market was valued at USD 7.83 billion. The market is expected to grow from USD 12.05 billion in 2026 to USD 15.94 billion by 2031, registering a CAGR of 5.75% during the forecast period (2026-2031). Rising female participation in water sports, both recreational and competitive, along with the increasing use of eco-friendly textiles and the influence of social media, is driving demand. Digital direct-to-consumer (DTC) channels are disrupting traditional buying patterns. At the same time, advancements like regenerated nylon and PFAS-free finishes are helping brands charge premium prices while complying with stricter regulations. The Asia-Pacific region is contributing the highest incremental volume, while North America and Europe are shaping premium market trends through technology and sustainability benchmarks. Competition remains intense, as low entry barriers allow DTC startups to capture consumer attention faster than established brands can adapt.

Key Report Takeaways

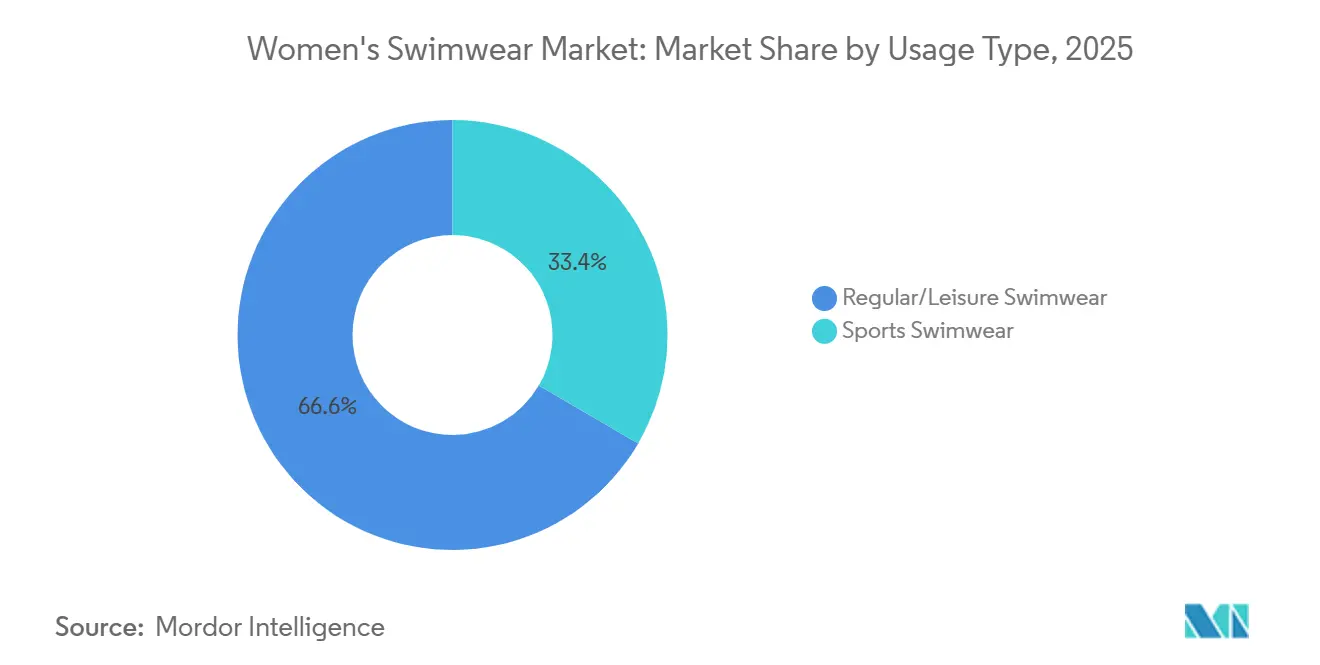

- By usage type, regular/leisure swimwear accounted for 66.59% of the market share in 2025, while sports swimwear is expected to grow at a CAGR of 5.89% through 2031, driven by an increase in female participation in competitive swimming.

- By product type, one-piece swimwear led the segment in 2025 with a 44.51% share. However, bikinis are anticipated to grow the fastest, with a projected CAGR of 5.91%, supported by the growing influence of body-positivity campaigns.

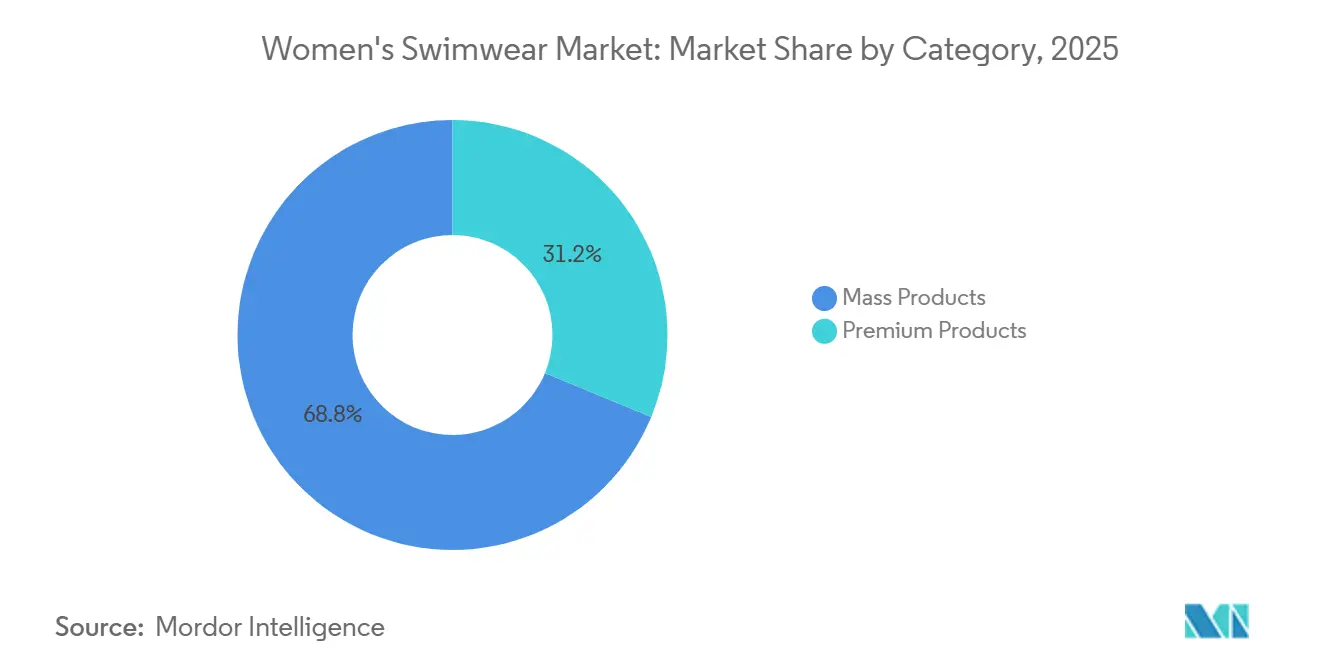

- By category, mass-market products dominated in 2025, capturing 68.78% of sales. Meanwhile, premium swimwear is expanding at a CAGR of 7.98%, as affluent consumers increasingly seek high-performance fabrics.

- By fabric material, polyester was the leading material in 2025, holding a 56.18% share. On the other hand, nylon is expected to witness the fastest growth, with a CAGR of 6.61%, largely due to the popularity of recycled materials like ECONYL.

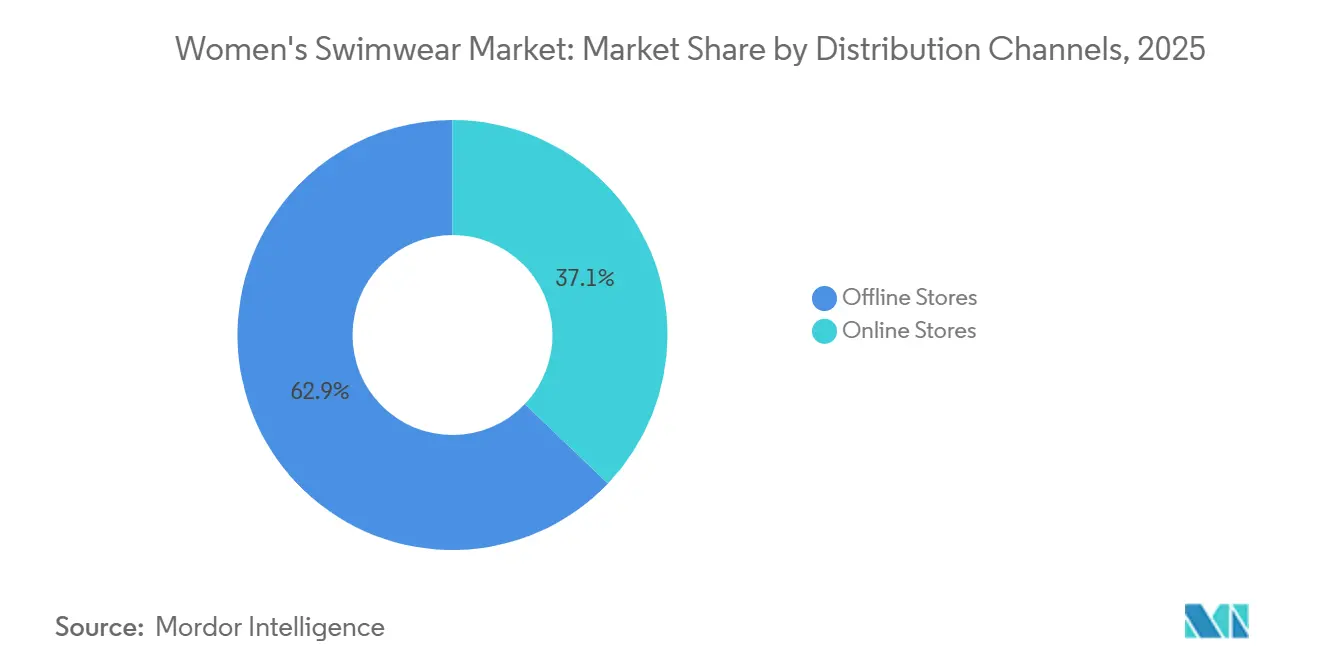

- By distribution channel, offline stores remained the primary channel in 2025, contributing 62.87% of revenue. However, online platforms are growing rapidly, with a CAGR of 7.84%, aided by virtual try-on tools that help reduce return rates, as highlighted by retaildive.com.

- By geography, Asia-Pacific emerged as the largest regional market in 2025, with a 33.92% share. The region is also projected to grow the fastest, at a CAGR of 6.71%, driven by increased investments in coastal tourism across countries like China, Indonesia, and Thailand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Women's Swimwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in female participation in water-based activities | +0.8% | North America, Europe, Asia-Pacific coastal regions | Medium term (2-4 years) |

| Adoption of recycled and bio-based fabrics | +0.9% | Europe, North America manufacturing in Asia-Pacific | Long term (≥ 4 years) |

| Influence of social media and celebrity endorsement | +1.2% | Global with emphasis on North America and Europe | Short term (≤ 2 years) |

| Growth in beach tourism and leisure travel | +0.7% | Asia-Pacific, Middle East and Africa, South America | Medium term (2-4 years) |

| Innovation in fabric technology | +0.6% | Global research and development in Europe and North America, production in Asia-Pacific | Long term (≥ 4 years) |

| Expansion of e-commerce and direct-to-consumer brands | +1.5% | Highest penetration in North America and Europe, rapid adoption in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in female participation in water-based activities

Sport England reports that swimming is the fifth most popular activity in the country. Approximately 4.7 million people swim at least twice a month, underscoring its position as one of the leading physical activities[1]Source: sportsengland, "Swimming", sportengland.org . In 2024, the number of women swimming regularly in England increased significantly, supported by investments in local swimming pools that enhanced accessibility and improved facilities. Meanwhile, in Indonesia and Thailand, regional school programs have been instrumental in teaching swimming skills to students. These programs have not only made swimming a common competency but have also cultivated a growing pool of female athletes. These athletes are now driving demand for performance swimwear, as they seek specialized gear for both training and competition. This trend has directly contributed to the growth of the women’s swimwear market. Additionally, the consistent use of swimwear throughout the year has reduced the market's dependence on seasonal peaks during warmer months, ensuring more stable and sustained growth.

Adoption of recycled and bio-based fabrics

Brands are increasingly being urged by consumers and regulators to minimize their reliance on virgin plastics. In response, producers of regenerated nylons are enhancing their production capabilities to meet the growing demand. Swimwear labels are progressively adopting sustainable practices by reducing the use of virgin materials, aligning with the industry's shift toward environmental responsibility. Companies like Patagonia are integrating natural rubber alternatives into their product lines, aiming to decrease dependence on petroleum-based materials. The EU's upcoming regulations mandating minimum recycled content thresholds for textiles sold within its member states are anticipated to accelerate global compliance efforts. Furthermore, the women's swimwear market is experiencing a shift, with consumers showing a preference for eco friendly options, which is influencing pricing trends.

Growth in beach tourism and leisure travel

In 2025, international tourist arrivals increased by 4%, supported by strong performances across global destinations. The World Tourism Barometer reported that approximately 1.52 billion international tourists were recorded worldwide in 2025, reflecting a rise of nearly 60 million compared to 2024. According to the Ministry of Tourism, the Maldives welcomed over 1.7 million tourists as of October 21, 2025, representing a 10% growth compared to the same period in 2024[2]Source: Visit Maldives Corporation (VMC), "Maldives tourism on track for record arrivals following global recognition wins", visitmaldives.com . The destination is on track to achieve its target of 2.3 million arrivals by the end of the year, with the final quarter expected to see the highest influx of visitors as the country enters its peak travel season. Each trip typically drives swimsuit purchases, maintaining steady demand in the women’s swimwear market despite economic fluctuations.

Innovation in fabric technology

On December 4, Italian swimwear brand arena introduced a new collection of swimsuits, highlighting the increasing focus on innovation in women’s swimwear. The collection features swimsuits made from recycled nylon and LYCRA EcoMade fiber, a spandex containing 70% bio based content[3]Source: The LYCRA Company, "ARENA: A BOLD STEP TOWARD SUSTAINABLE SWIMWEAR", lycra.com. This development marks a significant milestone as it represents the first commercial use of plant based spandex in swimwear, emphasizing the shift toward sustainable and high performance materials in the market. The sports swimsuit line includes three silhouettes in earthy tones and is crafted using Vita Life fabric by Carvico, a global leader in warp knitted fabrics for beachwear, sportswear, and performance garments. Carvico’s collaboration with The LYCRA Company demonstrates how partnerships and advancements in material technology are driving innovation in the women’s swimwear market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.6% | Europe, North America, online marketplaces | Short term (≤ 2 years) |

| Seasonal demand volatility | -0.5% | Temperate regions in North America and Europe | Medium term (2-4 years) |

| Environmental concern over synthetic fabrics | -0.4% | Europe and North America, rising awareness in Asia-Pacific | Long term (≥ 4 years) |

| Price sensitivity in mass segments | -0.5% | Asia-Pacific, South America, Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

In 2024, authorities in the European Union confiscated more than 112 million counterfeit items, valued at an estimated 3.8 billion euro in retail. These statistics, released by the European Commission’s Directorate General for Taxation and Customs Union (DG TAXUD) and the European Union Intellectual Property Office (EUIPO), highlight the growing issue of counterfeit goods. For instance, customs officials intercepted a shipment of fake luxury apparel at a major European port, preventing its distribution. In another case, authorities dismantled a counterfeit production network, seizing millions of fake items, including swimwear, and arresting key individuals. Such incidents underscore the challenges counterfeit products pose to the women’s swimwear market. These fake items, often sold at lower prices, damage the revenue and reputation of authentic brands while failing to meet quality and safety standards. This erodes consumer trust, acting as a significant restraint on market growth.

Seasonal demand volatility

The women's swimwear market continues to be heavily influenced by the seasonal peaks of spring and summer, even as off season travel becomes more common. Retailers often grapple with challenges when unpredictable weather disrupts sales patterns, leading to surplus inventory and the need for discounts to clear stock. To address these issues, strategies such as preorder models and small-batch releases have been adopted to better align production with anticipated demand. However, these approaches can sometimes limit the spontaneity that often drives consumer purchases in the fashion industry. Resort wear collections have emerged as a way to extend the selling season, offering consumers more options beyond the traditional peak periods. Despite these efforts, the market remains deeply tied to its seasonal nature, making it difficult to fully overcome these cyclical patterns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usage Type: Sports Suits Propel Technical Adoption

In 2025, regular/leisure swimwear emerged as the largest segment, capturing 66.59% of the market share. This segment's dominance is primarily due to its versatility and widespread appeal among consumers. Regular/leisure swimwear caters to a broad audience, including individuals engaging in leisure and recreational swimming, which are among the most common water-based activities. Its availability in various styles, designs, and price ranges further enhances its accessibility and popularity. Additionally, the growing trend of water-based tourism and vacations has contributed to the sustained demand for regular/leisure swimwear, solidifying its position as the leading segment in the market.

Sports swimwear is the fastest growing segment, projected to register a robust CAGR of 5.89% through 2031. This growth is driven by the increasing focus on fitness and competitive swimming, which has led to a rising demand for performance oriented swimwear. These products are designed to enhance speed, reduce drag, and improve overall athletic performance, making them essential for professional swimmers and athletes. Furthermore, the expansion of school based swim programs and the growing popularity of swimming as a sport have significantly contributed to the segment's rapid growth. Innovations in fabric technology, such as chlorine resistant and quick-drying materials, are also attracting consumers seeking durable and high quality swimwear options.

By Product Type: Bikini Momentum Grows

In 2025, one-piece designs stood out as the largest segment, accounting for 44.51% of total product sales. Their dominance stems from their broad appeal across various demographics, offering a blend of style, comfort, and functionality. One-piece swimsuits are particularly favored for their versatility, making them suitable for both recreational and professional use. Additionally, their ability to cater to diverse body types and preferences has solidified their position as a staple in the swimwear market. The segment's sustained popularity is further supported by innovations in fabric technology and design, which enhance comfort and durability, ensuring continued consumer interest.

Conversely, bikini sets are anticipated to be the fastest-growing segment, with a projected CAGR of 5.91% during the forecast period of 2026-2031. This growth is primarily driven by the increasing influence of social media platforms, where influencers and celebrities frequently promote bikini styles, encouraging consumers to adopt the latest trends. The rise of body-positivity movements has also played a significant role, empowering individuals to embrace and showcase their unique styles. Furthermore, the growing demand for mix-and-match options and customizable designs has added to the segment's appeal, allowing consumers to create personalized looks. As a result, bikini sets are expected to witness significant traction, making them a key contributor to the overall growth of the swimwear market during the forecast period.

By Category: Premium Tier Outpaces Mass

In 2025, mass products dominated the category, accounting for 68.78% of the total value. This segment's significant share is driven by its affordability and widespread availability, catering to a broad consumer base. Mass products appeal to price-sensitive customers and benefit from economies of scale, enabling manufacturers to offer competitive pricing while meeting diverse consumer needs. Extensive distribution networks further ensure accessibility across regions, solidifying their position as the largest segment in 2025. The versatility of mass products, which cater to various consumer preferences and functional requirements, also contributes to their consistent demand.

Premium collections are projected to be the fastest-growing segment, with a CAGR of 7.98% between 2026 and 2031. This growth is fueled by affluent consumers increasingly opting for sustainable and innovative materials, such as recycled and high-tech fabrics. The rising demand for premium products reflects a shift in consumer preferences toward quality and eco-consciousness. Advancements in textile technology enable the production of high-performance fabrics that cater to both functionality and aesthetics, further boosting this segment. Additionally, the emphasis on brand value and exclusivity among high-income groups encourages manufacturers to invest in premium offerings.

By Fabric Material: Nylon Gains Traction

Polyester is projected to remain the largest segment in 2025, accounting for 56.18% of the total fabric volume. Its dominance can be attributed to its widespread use across various industries, including apparel, home furnishings, and industrial applications. Polyester's durability, cost-effectiveness, and versatility make it a preferred choice for manufacturers and consumers alike. Additionally, advancements in polyester recycling technologies are further bolstering its market position, as sustainability becomes a key focus for both producers and end-users. The segment's ability to cater to diverse applications ensures its continued leadership in the fabric material market.

Nylon, on the other hand, is expected to emerge as the fastest-growing segment, with a projected CAGR of 6.61% during the forecast period. This growth is primarily driven by the increasing adoption of regenerated nylon variants, such as ECONYL, which align with the rising demand for sustainable materials. Nylon's lightweight, high strength, and resistance to wear and tear make it an attractive option for applications in sportswear, outdoor gear, and automotive interiors. The growing emphasis on eco-friendly alternatives and the material's ability to meet performance requirements across industries are key factors fueling its rapid expansion in the market.

By Distribution Channel: Online Keeps Accelerating

Offline stores are expected to remain the largest distribution channel in 2025, contributing 62.87% to the total turnover. This dominance can be attributed to the continued consumer preference for in-store shopping experiences, where customers can physically examine products before purchase. Additionally, offline stores benefit from their ability to provide immediate product availability and personalized customer service, which are key factors driving their sustained popularity. Despite the growing adoption of online channels, the offline segment continues to cater to a significant portion of the market, particularly in regions where digital infrastructure is still developing or where consumers prefer traditional shopping methods.

Online channels are projected to be the fastest-growing distribution channel, with a robust CAGR of 7.84% through 2031. This growth is driven by advancements in technology, such as virtual try-on tools, which enhance the online shopping experience by reducing return rates and increasing customer satisfaction. The convenience of online shopping, coupled with the increasing penetration of smartphones and internet connectivity, has further fueled this segment's expansion. Additionally, the rise of e-commerce platforms offering competitive pricing, diverse product ranges, and seamless delivery services has made online channels a preferred choice for many consumers. As a result, the online segment is rapidly transforming the distribution landscape, challenging the dominance of traditional offline stores.

Geography Analysis

In 2025, the Asia-Pacific region accounted for a 33.92% market share, supported by a CAGR of 6.71%. This growth was attributed to rising disposable incomes, an increase in coastal tourism, and the implementation of school swimming program mandates. Coastal provinces and international tourist arrivals in major countries have contributed to higher local retail spending on swimwear. Furthermore, the development of resorts in destinations such as the Maldives, Vietnam, and the Philippines has fueled growth in the premium segments of the women's swimwear market.

North America continues to lead in terms of market value, despite slower volume growth. This is primarily attributed to its well-developed e-commerce ecosystem, which supports seamless online transactions and efficient delivery networks. Factors such as domestic travel to beach destinations, high smartphone penetration, and robust logistics infrastructure enable direct-to-consumer (DTC) brands to meet consumer demands effectively. Additionally, the region's mature consumer base and preference for convenience further strengthen market loyalty and drive sustained value growth.

Europe, which is expected to contribute a significant share of 2025's revenue, is leveraging regulatory measures to accelerate the adoption of recycled fabrics. Countries such as Italy, Spain, and Greece benefit from significant vacation inflows, while the design expertise of France and Italy continues to reinforce their global style leadership. The Middle East and Africa are experiencing growth fueled by luxury-focused developments in destinations like Dubai, Abu Dhabi, and the Saudi Red Sea. These varied regional trends underscore the multipolar nature of the women's swimwear market, with no single region dominating across all price segments.

Competitive Landscape

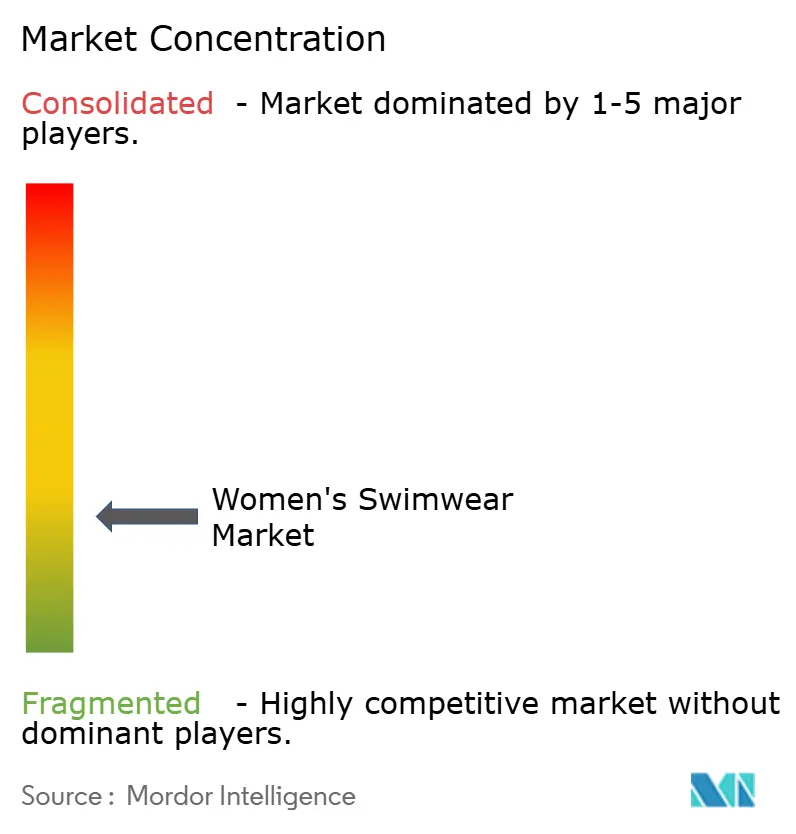

The market is fragmented, with the top five labels accounting for less than 30% of global revenue. Legacy brands like Adidas, Nike, and Puma continue to hold a significant global presence but face mounting competition from newer, Instagram-driven brands such as Triangl and Summersalt. These emerging players leverage micro-influencer networks to achieve lower customer acquisition costs, creating challenges for traditional players. To adapt, established brands are increasingly turning to strategic investments and acquisitions to maintain their relevance and appeal to younger, trend-conscious consumers.

Technology has become a pivotal factor in differentiating brands within the market. Established players are focusing on developing advanced swimwear lines tailored to specific consumer needs, such as performance-focused products for elite athletes. Meanwhile, newer entrants are capitalizing on celebrity endorsements and social media influence to expand their market presence. This emphasis on innovation and targeted marketing strategies is enabling brands to strengthen their competitive positions and cater to evolving consumer demands.

Emerging niches, including adaptive, modest, and sport-specific swimwear, are creating new growth opportunities for smaller players and new entrants. These segments remain relatively untapped, offering significant potential for expansion. As consumer preferences continue to shift and innovation drives the market forward, the women’s swimwear segment is poised for further evolution, ensuring a dynamic and competitive landscape.

Women's Swimwear Industry Leaders

-

Pentland Group PLC

-

Adidas AG

-

LVMH Moët Hennessy Louis Vuitton SE

-

Nike Inc.

-

PVH Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Arena expanded its Arena's Beachwear SS26 collection, beyond competitive swimwear into a broader lifestyle and leisure-focused beachwear segment. The collection emphasizes sport, freedom, and self-expression, blending technical performance with lifestyle aesthetics. It is divided into two primary lines: Arena Evolution, which highlights premium materials, refined design, and high-performance functionality, and Arena Essential, aimed at younger, active consumers with bold colors, graphic designs, and versatile, comfort-oriented pieces.

- December 2025: Authentic Brands Group, a prominent player in sports, media, entertainment, and lifestyle intellectual property, partnered with Blue Sage Accessories to introduce wetsuits under the renowned brands Roxy, Quiksilver, and Volcom.

- May 2025: Andie, a direct-to-consumer swimwear brand celebrated for its premium one-piece suits catering to all body types, announced its acquisition of California-based essentials label Richer Poorer. This marked Andie's first acquisition and a significant step toward its goal of becoming a multi-brand, multi-category lifestyle enterprise.

- April 2025: Parade launched a colorful, size-inclusive swimwear collection, marking its entry into the swimwear market. This expansion highlights the brand's commitment to inclusivity and vibrant designs.

Global Women's Swimwear Market Report Scope

Swimwear is a type of apparel that is worn during water activities like water sports or swimming.

The women's swimwear is segmented by type, product type, price category, fabric, distribution channels, and geography. By type, the market is segmented into sports/performance swimwear, leisure/resort swimwear, maternity swimwear, modest/conservative swimwear, and plus-size / curve swimwear. BY product type, the market is segmented into one-piece suits, bikini sets, tankinis, monokinis/trikinis, and burkini & full-coverage suits. By price category, the market is segmented into economy/mass, premium, and luxury/designer. By fabric/material, the market is segmented into nylon, polyester, neoprene, spandex/elastane blends, and recycled & bio-based textiles. By distribution channels, the market is segmented into online and offline. Online is further segmented into e-commerce marketplace, brand-owned websites, and subscription & rental platforms. Offline is further segmented into specialty swimwear stores, department stores, sports and outdoor retailers, and hypermarkets & supermarkets. By geography, the market is segmented into North America, South America, Europe, Asia, the Middle East, Africa, and Oceania.

For each segment, the market sizing and forecasts have been done based on value (in USD).

| Sports Swimwear |

| Regular/Leisure Swimwear |

| Bikini Sets |

| One-Piece |

| Other Product Types |

| Premium Products |

| Mass Products |

| Nylon |

| Polyester |

| Other Material Types |

| Online Stores |

| Offline Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Usage Type | Sports Swimwear | |

| Regular/Leisure Swimwear | ||

| By Product Type | Bikini Sets | |

| One-Piece | ||

| Other Product Types | ||

| By Category | Premium Products | |

| Mass Products | ||

| By Fabric Material | Nylon | |

| Polyester | ||

| Other Material Types | ||

| By Distribution Channel | Online Stores | |

| Offline Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global revenue for women’s swimwear be by 2031?

The women’s swimwear market is forecast to reach USD 15.94 billion by 2031, reflecting a 5.75% CAGR from 2026.

Which region is set to grow fastest?

Asia-Pacific is projected to post a 6.71% CAGR through 2031, powered by rising incomes and beach-tourism investment.

What is driving premium-segment momentum?

Premium lines gain from eco-friendly fabrics, influencer storytelling, and technology-rich suits that justify USD 150-plus price tags.

How are online channels reshaping sales?

E-commerce already delivers over one-third of revenue and is expanding at 7.84% CAGR as virtual try-on tools cut fit-related returns.

Page last updated on: