Winter Wear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 218.66 Billion |

| Market Size (2031) | USD 269.76 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

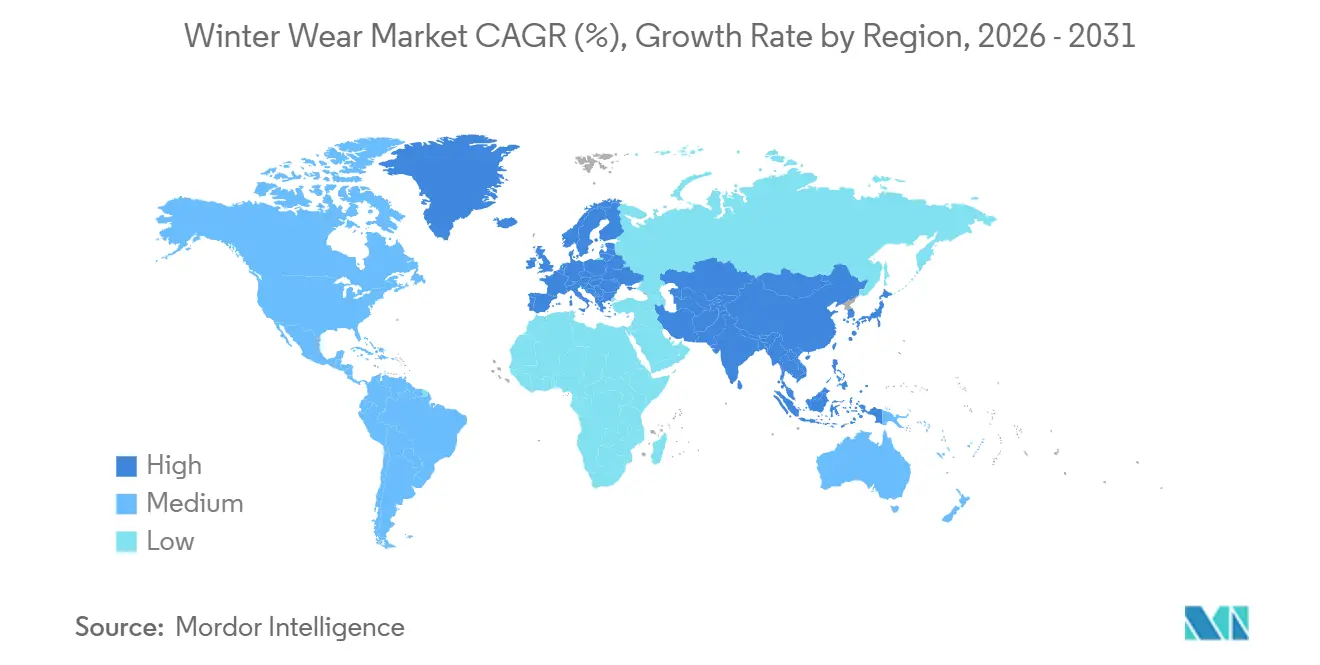

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

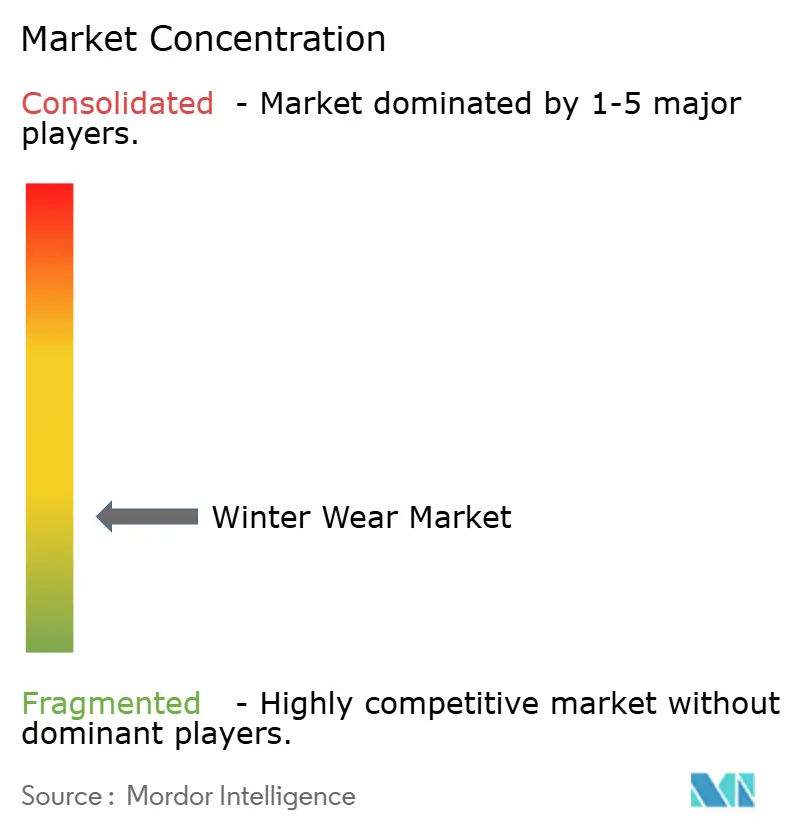

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Winter Wear Market Analysis by Mordor Intelligence

The winter wear market size was USD 210.21 billion in 2025, and is projected to reach USD 218.66 billion in 2026, and USD 269.76 billion by 2031, growing at a CAGR of 4.29% from 2026 to 2031. This measured trajectory signals a mature arena in which growth depends less on volume and more on responsiveness to climate volatility, material science, and policy shifts. Brands that link demand spikes to real-time weather analytics, invest in smart fabrics, and embed end-of-life accountability into product design now set the competitive tempo. Europe retains supremacy through an entrenched winter-sports culture, yet Asia-Pacific generates the steepest incremental gains as rising incomes intersect with an emerging appetite for outdoor recreation. For instance, according to Sport England, approximately 298,500 people participated in winter sports in England between November 2023 and November 2024 [1]Source: Sport England, "Number of people participating in winter sports in England", sportengland.org. This marked an increase from the previous year, during which 290,500 individuals participated in winter sports. Synthetic textiles dominate because they marry performance and cost control, while specialty retailers flourish by pairing technical advice with immersive store experiences, a mix that online-only outlets still struggle to replicate.

Key Report Takeaways

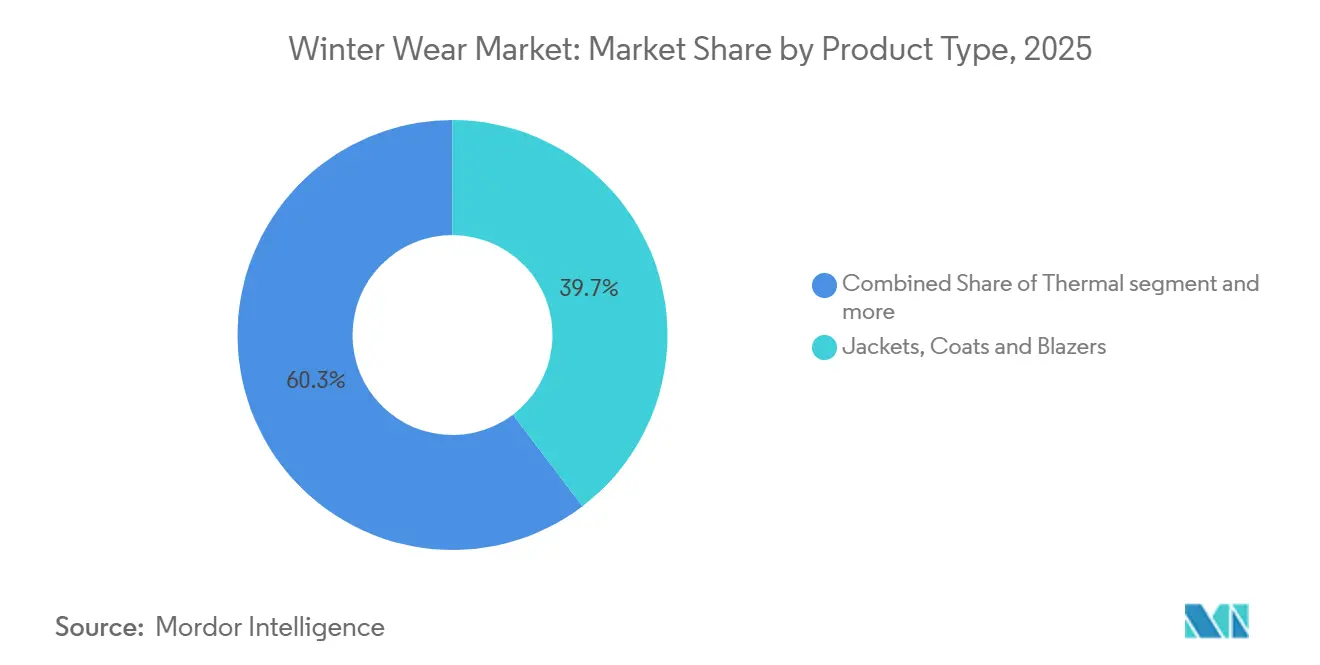

- By product type, jackets, coats, and blazers accounted for 39.67% of revenue in 2025, whereas thermals are progressing at a 6.04% CAGR to 2031.

- By end-user, adult demand had a 81.23% share in 2025, but the kids segment is poised for the quickest expansion at a 5.78% CAGR through 2031.

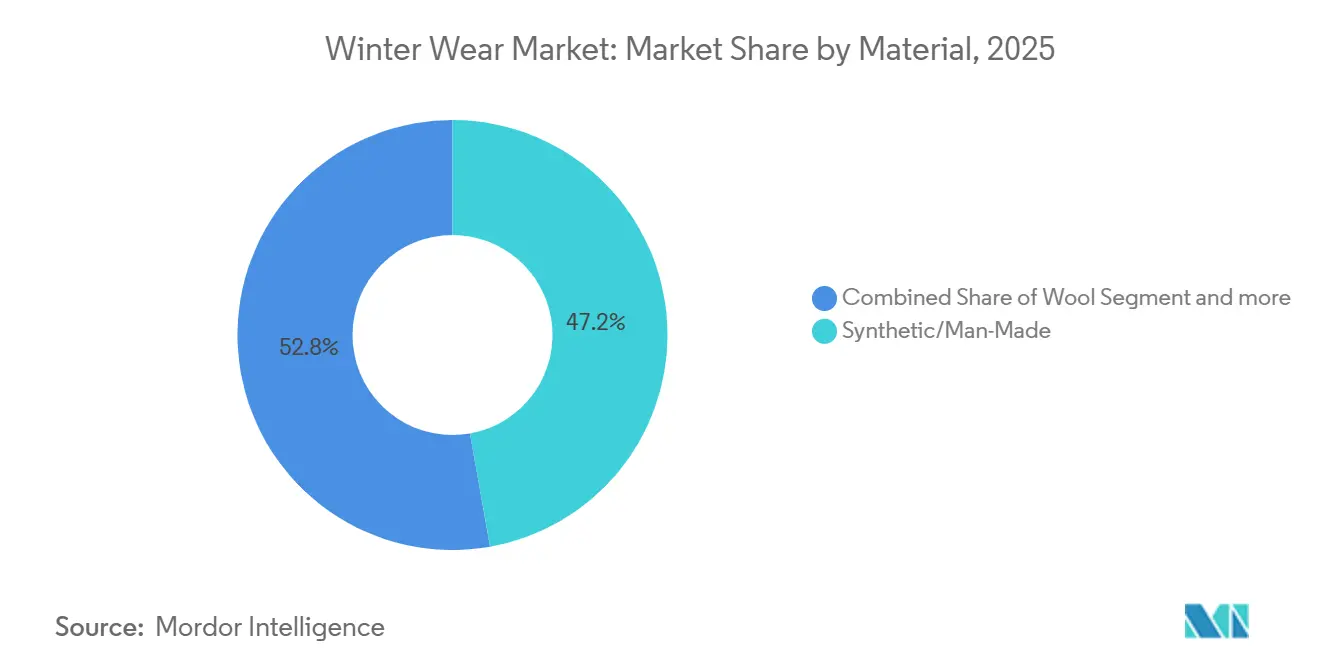

- By material, synthetic/man-made fibers captured 47.21% of 2025 sales, and wool held the fastest growing at a 5.57% CAGR, largely because performance advances outweigh natural-fiber price premiums.

- By distribution channel, specialty stores held 37.21% of 2025 turnover and are forecast to climb at a 6.29% CAGR on the strength of in-store expertise and tailored fit services.

- By geography, Europe dominated with 41.24% of global value in 2025, while Asia-Pacific is on track to widen the pie at a 6.24% CAGR thanks to urbanization, discretionary spending, and winter-tourism promotion.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Winter Wear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Changing climatic conditions influencing demand patterns | +0.8% | Global, with acute impacts in the Northern Great Plains and Arctic regions | Medium term (2-4 years) |

| Technological advancements in fabric development | +0.6% | Global, with innovation centers in North America and Europe | Long term (≥ 4 years) |

| Growth in winter tourism and outdoor recreational activities | +0.5% | North America, Europe, and emerging Asia-Pacific markets | Short term (≤ 2 years) |

| Rising focus on sustainability and eco-friendly product innovations | +0.4% | Europe and North America are leading, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Advances in heated and functional wearable apparel | +0.3% | North America and Europe core markets | Long term (≥ 4 years) |

| Evolving fashion trends and shifting consumer lifestyles | +0.2% | Global, with fashion capitals driving adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Changing climatic conditions influencing demand patterns

Shorter, warmer winters run parallel to more frequent extreme events that can drop temperatures overnight and trigger sudden storms. The Fifth National Climate Assessment recorded an uptrend in severe winter incidents across North America, while field reports from New Hampshire found 75% of outdoor-recreation operators contending with truncated seasons. For instance, according to Environment and Climate Change Canada, in 2023, the average temperature in Canada was 2.8 degrees Celsius, which was the lowest in the past decade after 2010 [2]Source: Environment and Climate Change Canada, "Temperature Change In Canada - Canadian Environmental Sustainability Indicators", canada.ca. Consumers are reacting by favoring versatile outer layers capable of coping with irregular temperature swings and precipitation bursts. Retailers now use hyper-local weather modeling to fine-tune replenishment, reducing markdown risk and accelerating time-to-shelf for climate-adaptive stock. In turn, suppliers with digital design pipelines can revise insulation weight or waterproof coatings almost in real time, an agility that traditional seasonal planners lack. The result is a demand curve for the winter wear market that is no longer smooth but punctuated, rewarding players that pivot quickly.

Technological advancements in fabric development

Smart textiles are reshaping the performance baseline. University of Waterloo engineers created a polymer-nanoparticle knit that self-heats by 30°C after ten minutes of direct sun, eliminating batteries and wires. In parallel, dual-modal photonic fabrics published in Science Advances widen user comfort bands by 8.5°C through automatic toggling between solar heating and infrared cooling. Such breakthroughs recast garments from passive insulation to active thermal-management systems, opening premium price tiers and licensing opportunities. Moreover, polar-bear-inspired aerogel fibers weigh one-fifth of down yet deliver comparable warmth. The shift spurs collaborative R&D between fiber chemists and heritage outerwear labels, bringing lab-bench innovation straight into storefront displays.

Growth in winter tourism and outdoor recreational activities

Outdoor recreation in the United States contributed USD 639.5 billion in 2023, equal to 2.3% of national GDP and supporting 5 million jobs, according to the U.S. Bureau of Economic Analysis (BEA). Snow-sports activity in Wyoming alone generated USD 2.2 billion and 15,798 positions in 2024, according to Wyoming's Office of Outdoor Recreation. These flows cushion the winter wear market against weather variability by fostering multi-activity wardrobes that traverse skiing, backcountry hiking, and shoulder-season trail use. Resort operators and local governments channel funding into snow making, all-season trail networks, and indoor ice complexes, assuring a baseline of foot traffic even when natural snowfall ebbs. Brands seize the chance to bundle modular layering systems, thermals, mid-layers, and accessories that suit cross-season use, thus lifting average selling price and smoothing revenue seasonality.

Rising focus on sustainability and eco-friendly product innovations

Regulation is turning eco-conscious design from virtue signaling into a legal necessity. The European Union rolled out an Ecodesign for Sustainable Products Regulation in 2025, flagging textiles as a priority category and requiring durable construction, recyclability, and tracer-enabled materials. Similarly, California’s Senate Bill 707 extends producer responsibility to apparel sold within the state, demanding collection and recycling schemes by 2026. On the supply side, Mitsubishi Corporation now feeds CO₂-derived monomers into polyester chains for The North Face jackets, demonstrating a cradle-to-gate greenhouse-gas reduction pathway. These moves tilt competitive advantage toward first movers that can document fiber origin, chemical inputs, and recyclability, reshaping how the winter wear industry defines quality and price.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal demand fluctuations restricting year-round sales | – 0.2% | North America, Europe | Short term (≤ 2 years) |

| Volatile raw material price fluctuations | – 1.3% | Global | Medium term (2-4 years) |

| Low market penetration in emerging regions | – 0.4% | Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Intense competition among global apparel brands | – 0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonal demand fluctuations restricting year-round sales

Seasonal demand fluctuations lead to highly concentrated sales during the autumn and winter months, resulting in uneven revenue generation across the year. Retailers and manufacturers often face inventory buildup during off-seasons, increasing storage and carrying costs. This also creates pricing pressure, leading to heavy discounting at the end of the season to clear unsold stock. Additionally, production planning becomes challenging due to the short sales window, impacting supply chain efficiency and profitability. It also forces companies to rely heavily on forecasting accuracy, where even small demand miscalculations can lead to either stockouts or overstock situations. Marketing and promotional activities are also compressed into a limited time frame, increasing seasonal competition among brands. As a result, cash flow remains cyclical, with strong peaks during winter months and weaker performance in the rest of the year.

Volatile raw material price fluctuations

Cotton futures bounced between USD 0.77 and USD 0.92 per pound during 2024 as floods hit Punjab and drought plagued Texas, undermining cost predictability, according to the U.S. Department of Agriculture. Polyester feedstocks tethered to petrochemical volatility; Brent crude’s 12-month range of USD 70–97/barrel over 2024 inflated filament prices used in performance shells. On top of mid-stream turbulence, the EU’s deforestation-free supply-chain law obliges apparel importers to certify traceable origin for plant-based fibers, driving compliance spend, according to the European Parliament. Brands hedging with recycled synthetics face capacity bottlenecks: global rPET demand outran supply by 22% last year, forcing spot-market premiums. Collectively, these variables compress gross margin and curtail the winter wear market’s headroom for aggressive promotion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Outerwear Dominance Drives Innovation

Jackets, coats, and blazers claimed the largest slice of 2025 revenue at 39.67%, reflecting their role as the first line of defense against temperature swings and gusty precipitation. The segment thrives on the integration of three-layer laminates, laser-cut vents, and PFC-free water repellents that lengthen wear life while catering to eco-mandates. Premium labels frequently embed avalanche beacons, NFC garment IDs, and smartphone-synchronized heat panels, elevating average unit value. Sweaters and Cardigans remain wardrobe staples for transitional climates, bolstered by merino-blend knits that self-regulate moisture and resist odor. Meanwhile, shawls, scarves, wraps, stoles, and mufflers occupy a sweet spot where culture, fashion, and function intersect, especially in India and the Middle East during evening cold snaps. The results show a long-tail structure: core outerwear guards market share, but peripheral niches inject faster velocity, ensuring the winter wear market stays vibrant across pricing ladders.

Thermals, though smaller, outpace overall growth at a 6.04% CAGR. Thermal wear is the fastest-growing segment due to rising demand for lightweight yet highly effective insulation in cold climates. Increasing participation in outdoor activities such as trekking, skiing, and winter sports is driving adoption of performance-based base layers. Consumers are also shifting toward multi-layer dressing, where thermals serve as the essential foundation layer. Technological advancements in moisture-wicking, stretchable, and breathable fabrics are further enhancing comfort and functionality. Additionally, growing preference for affordable cold-weather protection in emerging markets is expanding the consumer base for thermal wear.

By End-User: Women Lead While Kids Accelerate

Adults maintained the lion’s share at 81.23% in 2025, a reflection of higher wardrobe turnover, occupational fashion codes, and differentiated fit requirements from petite to plus-size. Brands catering to women incorporate articulated elbows, cinchable waists, and colorways aligned with seasonal runways. Loyalty programs built around personalization apps anchor repeat purchases, while influencer tie-ins drive cross-border e-commerce traffic. Yet the most vigorous momentum lies in kids’ apparel, forecast to accelerate at a 5.78% CAGR. Parental willingness to pay a premium for safety and comfort catalyzes sales of reflective trims, GPS-enabled ski jackets, and grow-with-me cuff extensions that prolong wear life.

The outdoor recreation boom documented by the Bureau of Economic Analysis has encouraged family participation in snow parks and urban ice rinks, feeding demand for multi-activity youth gear, according to the U.S. Bureau of Economic Analysis (BEA). For instance, in the 2023/24 season, there were 2,860 indoor and 5,000 outdoor ice hockey rinks located in Canada, according to the International Ice Hockey Federation [3] Source: International Ice Hockey Federation, "IIHF Season Summary, 2023-24", blob.iihf.com. Children’s lines now mirror adult tech specifications, for instance, 20,000 mm waterproof ratings and RECCO reflectors, closing the historical gap between miniaturized fashion pieces and genuine performance wear. Men’s products hold steady growth by focusing on ruggedness and utility: abrasion-resistant shells, work-wear crossovers, and urban commuter styling. Overall, the demographic breakdown underlines how lifestyle shifts orchestrate the re-mix of spend within the winter wear market.

By Material/Fabric: Synthetic Leadership Accelerates

Synthetic/man-made fibers represented 47.21% of the 2025 value while wool expanded at a 5.57% clip, propelled by continuous filament innovations such as hollow-core yarns that trap air yet shed bulk. Synthetic and man-made fabrics dominate the winter wear market because they are cost-effective, scalable, and highly versatile. Materials like polyester and nylon offer strong insulation, durability, and water resistance at a much lower cost than natural fibers. They are widely used across mass-market jackets, thermals, and sportswear, making them the preferred choice for large-scale production. Additionally, their ease of blending with other fibers and compatibility with performance-enhancing treatments further increase adoption across brands.

Wool is growing fastest due to rising demand for natural, sustainable, and premium winter wear materials. Consumers are increasingly shifting toward eco-friendly and biodegradable fabrics, boosting wool adoption. Merino and fine wool variants offer superior warmth, breathability, and odor resistance, making them ideal for both outdoor and luxury winter apparel. Premiumization trends in Europe and North America, along with rising preference for high-quality thermal comfort, are further accelerating wool’s growth.

By Distribution Channel: Specialty Stores Maintain Advantage

Specialty retailers secured 37.21% of global revenue in 2025. Shoppers seek fit verification, layering guidance, and after-sales repair services that are harder to replicate online. Flagship stores increasingly host altitude chambers, digital ski-boot analyzers, and RFID-activated product walls, converting visits into experiential storylines. Online retail, growing at 6.29% CAGR, has been turbo-charged by pandemic buying habits, offers an unmatched assortment breadth, yet still battles return rates near 28% for insulated outerwear, mainly due to sizing uncertainty and color misrepresentation.

Supermarkets/Hypermarkets capture budget-conscious consumers through immediate availability, particularly in emerging markets where winter events are infrequent yet sudden. Direct-to-consumer pop-ups, subscription boxes, and mobile van fit-outs sit in the “other channel” bracket, each carving micro-pockets of loyalty by blending digital convenience with tactile testing. Collectively, the interplay keeps the winter wear market omnichannel, urging brands to synchronize inventory data, pricing, and promotions across touchpoints. Supermarkets and hypermarkets play a key role in the winter wear market by offering affordable and readily available seasonal apparel, particularly catering to mass-market and impulse buyers during peak winter months.

Geography Analysis

Europe’s 41.24% grip in 2025 reflects Alpine and Scandinavian winter-sport legacies paired with affluent shoppers who prize eco-certified technical wear. Germany, France, and Spain absorb a significant share of the continent’s apparel imports, and policy momentum, such as the January 2025 Extended Producer Responsibility directive, makes supply-chain transparency a passport to shelf space. Italian mills perfect low-PFC laminates, while Nordic brands pilot take-back schemes financed through up-front surcharges. Rising demand for recycled polyester base layers shows that sustainability no longer cancels performance but amplifies it.

Asia-Pacific leads the growth tables at a 6.24% CAGR, emerging from a fusion of middle-class expansion, government-funded ski resorts ahead of events like the 2029 Sapporo Asian Winter Games, and aggressive brand rollouts. China’s Ministry of Industry and Information Technology aims for maximum production digitalization in the coming years, accelerating responsiveness to trend signals. Amer Sports lifted technical-apparel sales year-on-year within Greater China, proving premium categories can thrive despite macro headwinds. In India, hill-station tourism spikes during December-February, bolstering demand for modular layering kits.

North America remains the bellwether of experiential retail and material science research. The outdoor economy’s contribution to GDP furnishes a robust customer base, yet climate instability obliges retailers to shorten lead times and widen assortments. Canadian winters warm more rapidly than the global average, compelling cities like Calgary to phase in variable insulation signage on municipal alerts, indirectly nudging residents to diversify outerwear wardrobes. South America and the Middle East and Africa register nascent but promising pockets: Chile’s Patagonia sees expanding glacier-trek circuits requiring technical shells, while high-altitude hubs in Morocco drive sales of lightweight down. Such idiosyncratic climates add regional texture to the winter wear market.

Competitive Landscape

The winter wear market is fragmented. Luxury spheres orbit around a handful of heritage names, Moncler, Canada Goose, and Arc’teryx, whose combined cachet locks in multi-year collaborations with alpine resorts and global fashion weeks. Their moat is reinforced by proprietary textile licenses and vertically integrated down-tracing programs. Mid-tier and mass-market tiers, by contrast, teem with fast-fashion giants, sportswear incumbents, and digital natives that copy silhouettes within weeks. The result is price stratification rather than winner-takes-all control.

Strategic moves in 2025 underline category convergence. Kontoor Brands’ USD 900 million purchase of Helly Hansen broadens denim stalwart Wrangler’s reach into technical outerwear, signaling cross-category synergy. Authentic Brands Group granted Outdoor Collective a multi-year Spyder license to sharpen go-to-market agility, tethering design and distribution within one ecosystem. Amer Sports’ USD 6.5 billion IPO injects capital for material R&D, store footprints, and digital analytics expansion.

Technology partnerships accelerate differentiation. University of Waterloo’s sunlight-heating fabric is under evaluation by multiple premium brands for Fall 2026 capsule collections. Mitsubishi Corporation’s CO₂-derived polyester debuted in The North Face Japan line, and pilot volumes sold out within three weeks. Competitive intensity is thus surfacing not only in marketing spend but in patents, life-cycle-assessment metrics, and supply-chain traceability dashboards accessible to end consumers through QR codes. In this environment, brand equity hinges on demonstrable functional advantage, authenticity, and transparent stewardship of social and planetary impacts.

Winter Wear Industry Leaders

-

VF Corporation

-

Patagonia, Inc.

-

Columbia Sportswear Company

-

Canada Goose Holdings Inc.

-

Moncler S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Etcetera unveiled its sophisticated Winter Edit, designed for fashion-forward women seeking both style and functionality. Featuring meticulously tailored coats, textured jackets, and bold statement cardigans, the line effortlessly blends luxury fabrics with practical designs.

- February 2025: Max Mara’s 2025 collection, themed “Untamed Heroine,” debuted with an emphasis on neo-gothic outerwear rooted in literary inspiration from the Brontë sisters. Centerpiece styles include statement coats, sweeping capes, tailored gilets, and frock coats rendered in luxurious Italian wools and cashmeres.

- January 2025: Kontoor Brands, known for iconic apparel labels like Wrangler and Lee, announced a definitive agreement to acquire Helly Hansen, a prestigious global outdoor and workwear brand, for approximately USD 900 million. The transaction involved the complete acquisition of Helly Hansen from Canadian Tire Corporation, marking Kontoor’s largest portfolio expansion since its inception.

- September 2024: The Wearable Art Store launched its winter drop, centered around the “All Warm & Cozy” series, known for two-tone v-neck knit tops, asymmetric tunics, and lightweight trench coats. Each design fused artful color-blocked patterns with practical layering forms, catering to those seeking unique statement pieces.

Global Winter Wear Market Report Scope

The winter wear market comprises clothing and accessories designed to provide warmth and protection in cold weather, including jackets, sweaters, thermals, gloves, and scarves. The Winter Wear Market is Segmented by Product Type (Sweaters and Cardigans, Coats and Blazers, Scarves, Wraps, Stoles, Thermals, Gloves, and More), End-User (Kids, Adults), Material/Fabric (Wool, Leather, and More), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail Stores, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Sweaters and Cardigans |

| Jackets, Coats and Blazers |

| Shawls, Scarves, Wraps, Stoles and Mufflers |

| Thermals |

| Gloves |

| Headwear |

| Wool |

| Leather |

| Synthetic/Man-Made |

| Other Material Types |

| Kids |

| Adults |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Product Type | Sweaters and Cardigans | |

| Jackets, Coats and Blazers | ||

| Shawls, Scarves, Wraps, Stoles and Mufflers | ||

| Thermals | ||

| Gloves | ||

| Headwear | ||

| By Material/Fabric | Wool | |

| Leather | ||

| Synthetic/Man-Made | ||

| Other Material Types | ||

| By End-User | Kids | |

| Adults | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the winter wear market?

The winter wear market size reached USD 210.21 billion in 2025 and is projected to climb to USD 269.76 billion by 2031.

Which region is expanding the fastest?

Asia-Pacific leads with a 6.24% CAGR, driven by urbanization, rising disposable incomes, and policy-supported winter-sports tourism.

Why are synthetic fabrics dominant?

Synthetic/man-made fibers captured 47.21% of 2025 revenue because they deliver high thermal efficiency, durability, and cost advantages compared with natural alternatives.

Which product category commands the greatest share?

Jackets, Coats and Blazers held 39.67% of global revenue in 2025 thanks to their versatility and capacity to integrate advanced materials.

Page last updated on: