Women's Non-athletic Footwear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

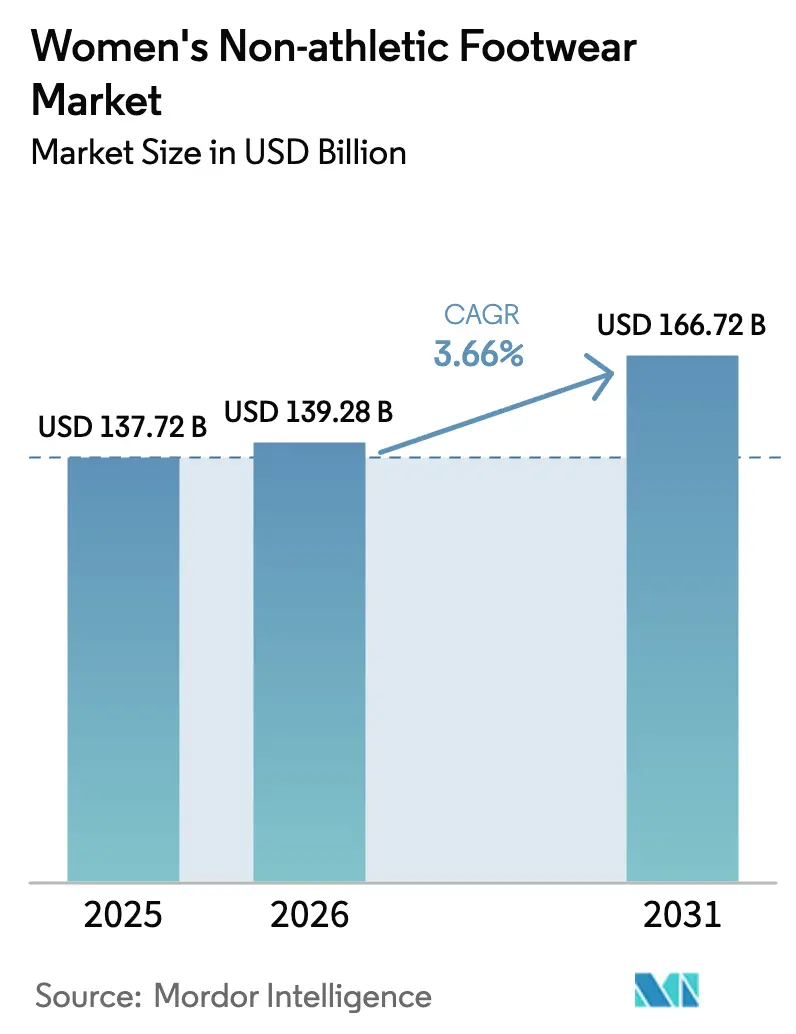

| Market Size (2026) | USD 139.28 Billion |

| Market Size (2031) | USD 166.72 Billion |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

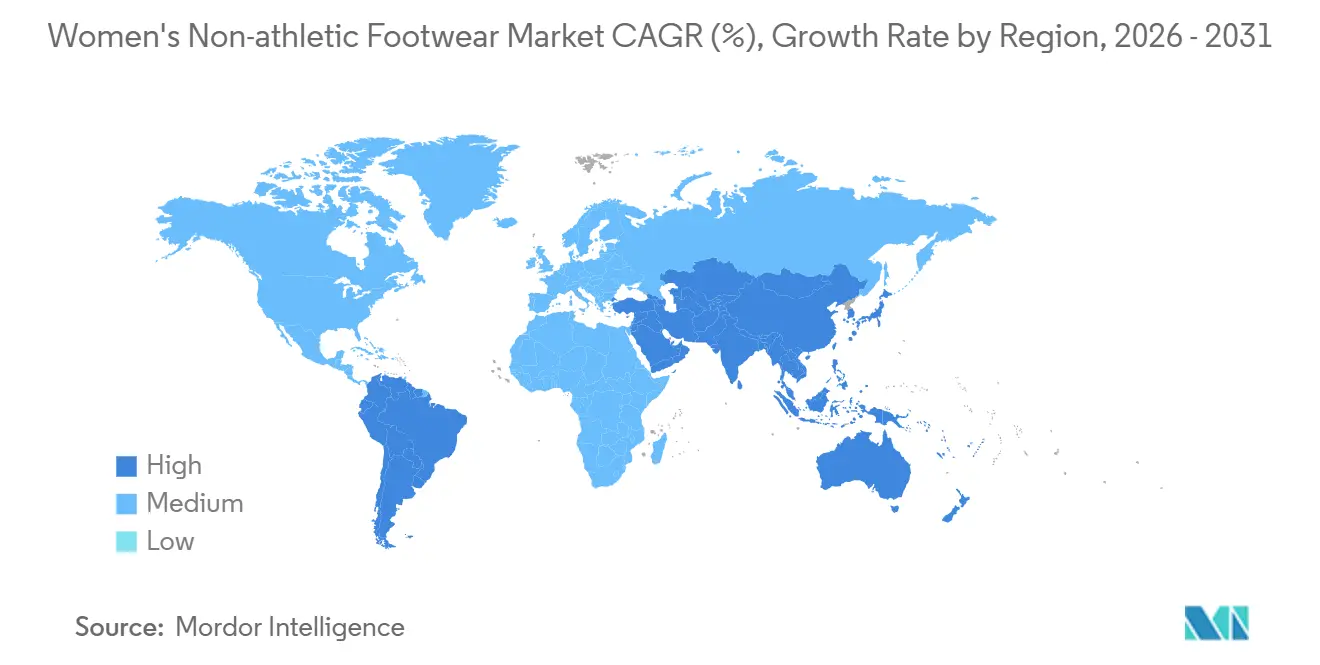

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Women's Non-athletic Footwear Market Analysis by Mordor Intelligence

The women non athletic footwear market size is expected to grow from USD 137.72 billion in 2025 to USD 139.28 billion in 2026 and reach USD 166.72 billion by 2031, growing at a CAGR of 3.66% over 2026-2031. AI-guided fitting engines, premiumization, and circular-economy channels are reshaping competitive economics while offline stores continue to anchor sell-through. Rapid fast-fashion refresh cycles shorten design lead-times to 21 days, letting brands test micro-trends at low markdown risk. AI sizing tools embedded in kiosks, smartphones, and e-commerce checkout flows cut average return rates for boots by 28% and shift margin pools toward data-rich direct sellers. Post-pandemic occasion-wear demand has revived heels and pumps, particularly in Asia-Pacific financial hubs, while vegan leather advances narrow the cost-performance gap with bovine hides. Extended Producer Responsibility (EPR) fees in Europe and volatile Brazilian leather prices add asymmetric cost pressures that favor vertically integrated giants able to hedge sourcing and amortize compliance.

Key Report Takeaways

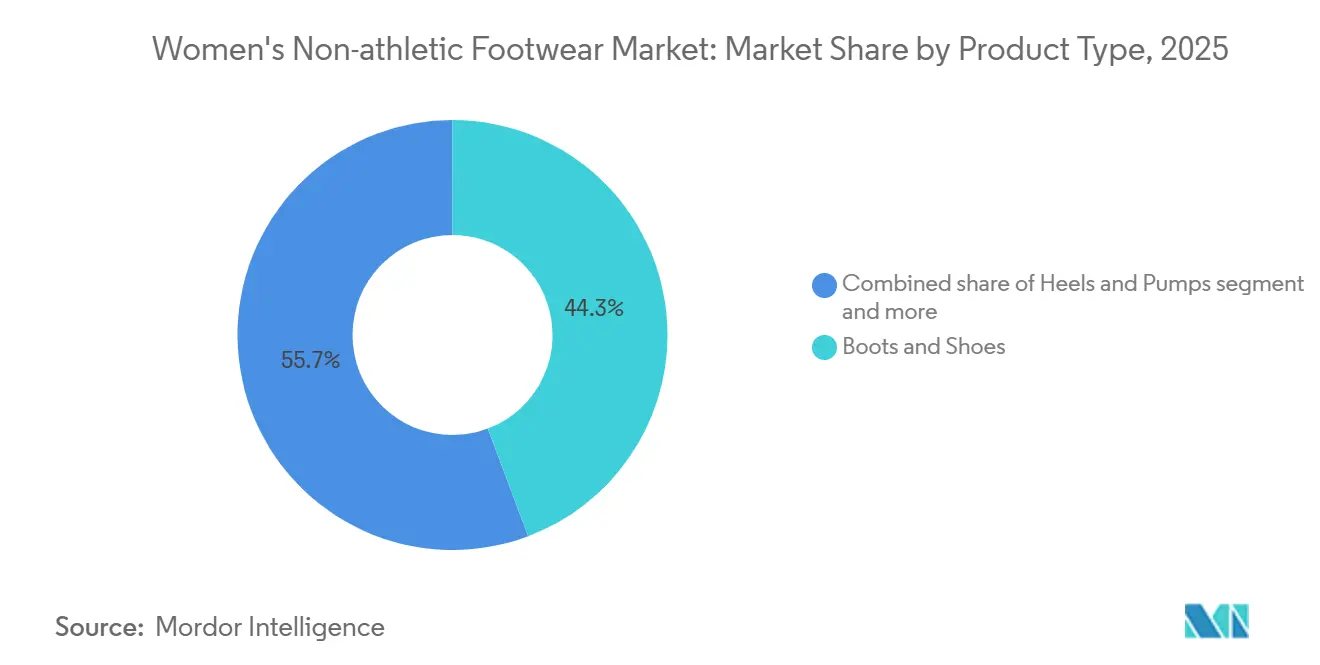

- By type, boots and shoes led with 44.26% of the women non athletic footwear market share in 2025, while heels and pumps are projected to expand at a 5.61% CAGR through 2031.

- By category, the mass segment accounted for 85.52% of the 2025 value; the premium segment is advancing at 5.48% CAGR to 2031.

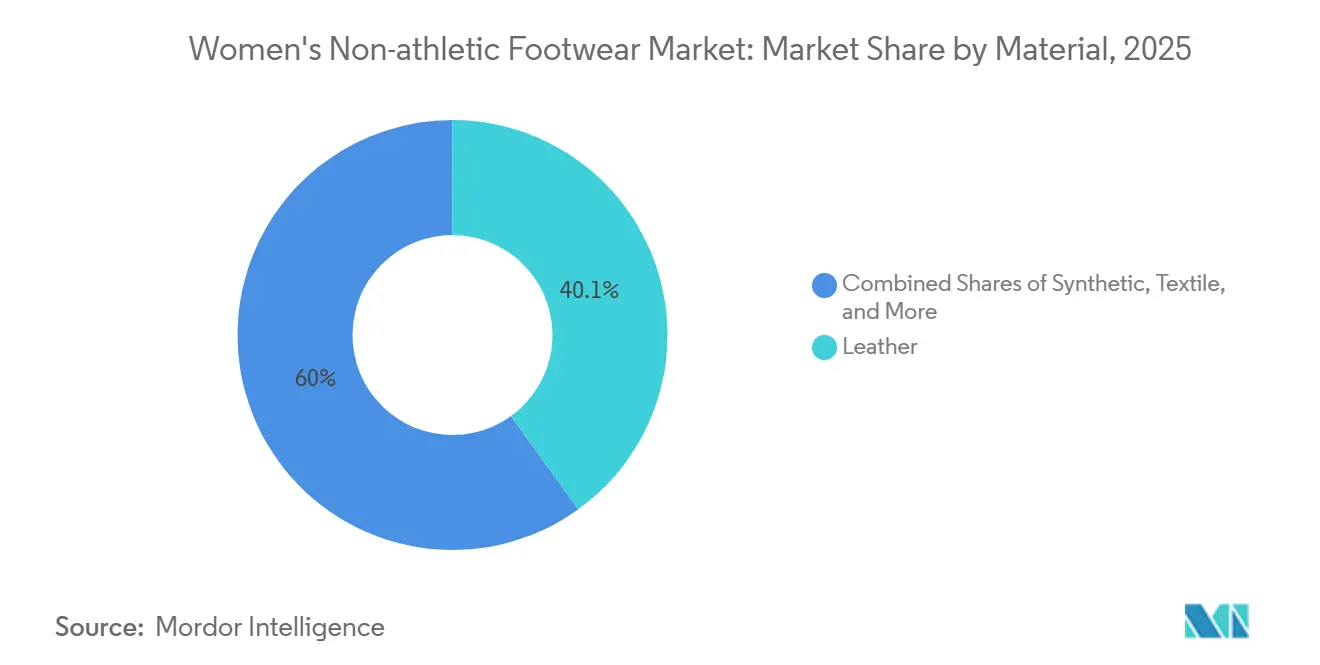

- By material, leather retained 40.05% share of the women non athletic footwear market size in 2025, yet synthetic alternatives are rising at 5.47% CAGR through 2031.

- By distribution channel, offline retail controlled 85.95% of 2025 sales, and online is set to advance at a 5.96% CAGR.

- By geography, Asia-Pacific captured 48.18% revenue in 2025, whereas the Middle East and Africa is forecast to grow at a 5.02% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Women's Non-athletic Footwear Market Trends and Insights

Rapid Fast-Fashion SKU Refresh Cycles

In 2025, Inditex reduced its footwear design-to-shelf cycle to 21 days, an improvement from 35 days in 2023. This faster cycle enables Zara stores to refresh their heel and flat assortments 17 times annually, significantly exceeding the industry average of 6-8 turns. This agility allows brands to test micro-trends, such as kitten-heel mules or square-toe loafers, across 200-store clusters before scaling to full production, cutting markdown risk by 40%. H&M's footwear division adopted a comparable approach in late 2024, collaborating with Vietnamese contract manufacturers to achieve 4-week lead times for synthetic uppers. This strategy challenges mid-tier department-store brands, which operate on 16-week planning cycles, forcing them to lose market share to more agile competitors. Additionally, the rapid SKU refresh has driven demand for modular last designs and digital pattern-cutting technologies. Clarks and Deichmann piloted these innovations in 2025, successfully reducing sample-room waste by half. Although regulatory influence remains limited, ISO 20345 safety standards for occupational footwear require a 6-month certification process, which restricts refresh speeds in industrial segments.

AI-Powered Direct-To-Consumer Sizing Precision

By the end of 2025, Volumental's 3D foot-scanning kiosks, set to be in 3,200 retail locations, achieved a 28% reduction in return rates for women's boots. This was accomplished by mapping 11 biomechanical dimensions and suggesting brand-specific size adjustments. In the UK, startup Laws of Motion embedded gait-analysis sensors into trial shoes. These sensors captured pronation and arch-flex data, leading to comfort score predictions with 91% accuracy. In 2025, the system handled 480,000 fittings, successfully converting 34% of users into buyers within 48 hours. SafeSize's smartphone app, leveraging camera-based photogrammetry, saw 2.1 million downloads in North America in 2025. This allowed direct-to-consumer brands to entirely eliminate the need for physical try-ons, as reported by TechCrunch. Such advancements in technology are reshaping the competitive landscape, favoring data-centric platforms. Brands boasting over 50,000 scans can refine proprietary algorithms, achieving a 15-20 percentage point edge over generic size charts in fit satisfaction. Meanwhile, traditional retailers, like Nine West, highlighted the challenges of lacking a digital infrastructure. In their 2025 Q3 earnings call, they pointed to heightened return rates as a significant drag on their gross margin.

Recovery In Post-Pandemic Occasion Wear Demand

In 2025, wedding attendance in the United States rebounded to 2.4 million ceremonies, reflecting an 18% increase from 2024. This rise in weddings boosted sales of heels and pumps through bridal-party channels. Luxury brands quickly capitalized on this trend: Jimmy Choo's spring 2025 collection, featuring 3.5-inch block heels designed for all-day comfort, sold out within 6 weeks at flagship stores across the Asia-Pacific. Similarly, Europe experienced a 22% growth in concert and festival attendance, reaching 58 million attendees in 2025. This increase, supported by the European Festival Association, drove demand for embellished sandals and platform styles[1]Source: European Festival Association. "Festival Attendance Statistics 2025." efa-europe.eu. However, the recovery has been uneven. In tech hubs like San Francisco and Berlin, the ongoing prevalence of remote work has kept casual footwear sales 9 percentage points above pre-pandemic levels, resulting in a regional decline in formal shoe demand.

Affordable And Competitive Vegan Leather Alternatives

In Q2 2025, startup Nanollose commercialized a bacterial cellulose process from Imperial College London, producing sheet material at USD 12 per square meter. This price undercuts bovine leather's range of USD 18-22, while achieving 92% of leather's tensile strength. In 2025, Allbirds used this material in 180,000 pairs of flats, realizing a 38% reduction in carbon footprint compared to synthetic PU alternatives. Mycelium-based uppers, cultivated by Ecovative and MycoWorks, began mass production in 2025. Stella McCartney and Rothy's introduced pilot collections, priced at a 15% premium over traditional vegan options. The cost disparity is shrinking: Piñatex, made from pineapple-leaf fiber, saw its price drop to USD 14 per square meter in 2025, thanks to Philippine production scaling up to 2.4 million square meters annually. In Europe, consumer acceptance surged in 2025, with 31% of 18-34 year-olds prioritizing material sustainability over brand heritage when buying footwear priced above EUR 100. As brands grapple with scrutiny over greenwashing claims, adherence to ISO 14021 environmental labeling standards is emerging as a key competitive edge.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating And Volatile Leather Prices | -0.5% | Global, acute in South America and Asia-Pacific | Short term (≤ 2 years) |

| Proliferation Of Counterfeits In Cross-Border E-Commerce | -0.4% | Global, concentrated in Europe and North America | Medium term (2-4 years) |

| Stringent EU Extended Producer Responsibility Regulations | -0.3% | Europe, with spillover to UK and North America | Medium term (2-4 years) |

| Athleisure Comfort Trends Eroding Formal Footwear Demand | -0.6% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating And Volatile Leather Prices

In 2024, prolonged droughts in the Mato Grosso and Goiás states caused a 6.2% contraction in Brazilian cattle herds. Consequently, wet-blue leather prices rose to USD 2.80 per square foot in Q1 2025, reflecting a 22% year-over-year increase. This price volatility reduced gross margins for mid-tier brands by 3-5 percentage points. To address this, Clarks increased wholesale prices by 8% in March 2025, but retailer resistance delayed spring shipments. Simultaneously, Indian leather exports, the world's second-largest source, declined by 11% in volume during 2024-2025. This drop resulted from domestic tanneries facing water-use restrictions under revised Central Pollution Control Board guidelines, tightening global supply, as reported by the Indian Leather Industry Association. Synthetic alternatives gained traction, with PU upper adoption increasing by 4 percentage points in 2025 as brands sought cost stability. However, in European markets, consumer perception of synthetic durability remains 18% lower than that of leather. Despite the volatility, hedging instruments in the industry remain underutilized. A 2025 survey indicated that only 12% of footwear brands employed commodity futures to mitigate leather-price risks, leaving most exposed to spot-market fluctuations.

Stringent EU Extended Producer Responsibility Regulations

France's EPR decree, effective January 2025, requires footwear brands to pay EUR 0.12 per pair sold to fund collection and recycling efforts. Non-compliance results in a penalty of EUR 0.50 per unit, according to the European Commission[2]Source: European Commission, “Extended Producer Responsibility for Textiles and Footwear,” ec.europa.eu. For brands shipping 150 million pairs annually to France, this equates to EUR 18 million in compliance costs, representing approximately 1.2% of revenue for mid-tier operators. Similarly, Germany's initiative, starting in July 2025, obligates brands to achieve 25% post-consumer recycled content by 2028. This regulation necessitates investments in reverse-logistics networks, which many non-luxury players have yet to establish, as noted by the German Federal Environment Agency. In September 2025, the Netherlands implemented a digital product passport requirement, compelling brands to disclose material sourcing and carbon intensity for each SKU. These data requirements favor vertically integrated manufacturers while posing challenges for wholesale-dependent distributors. Smaller brands are disproportionately affected, as compliance infrastructure costs are largely fixed. This creates a 2-3 percentage-point margin disadvantage compared to larger players like Inditex and H&M, who can distribute EPR system costs across their extensive apparel and footwear portfolios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Heels Gain as Occasion Wear Rebounds

In 2025, boots and shoes led the market with a 44.26% share, driven by year-round versatility and strong cold-weather demand in Northern Europe and North America. Heels are projected to grow at the fastest rate, with a 5.61% CAGR through 2031. The post-pandemic recovery of occasion-wear, marked by an 18% year-over-year rise in U.S. weddings to 2.4 million in 2025, revived pump and stiletto sales after declines during the remote-work period. Flats, popular for comfort and benefiting from the athleisure trend, hold significant volume but show slower growth at 3.2% as the segment matures. Sandals, while holding a notable share, face seasonal demand risks but are gaining traction in Middle Eastern markets, supported by year-round warm weather. UAE sandal imports rose 14% in 2025.

Innovations in heel construction are transforming the segment. Jimmy Choo's spring 2025 collection, featuring 3.5-inch block heels with gel cushioning, sold out in six weeks across Asia-Pacific flagship stores, highlighting demand for comfort-engineered luxury. In Q3 2025, Steve Madden introduced 3D-printed heel cores, cutting component weight by 22% without reducing load capacity, potentially lowering material costs by USD 1.80 per pair at scale. Boots and shoes, though slower-growing, benefit from hybrid designs. Ankle boots with sneaker-like soles captured 8% of the segment in 2025, appealing to consumers seeking formal looks with athletic comfort, as reported by the Financial Times. Other styles, such as mules and espadrilles, remain niche with a combined share under 8% but serve as platforms for testing materials like cork composites and recycled ocean plastics.

By Category: Premium Gains Despite Mass Dominance

In 2025, mass-market offerings accounted for 85.52% of the volume, driven by price sensitivity in Asia-Pacific and Latin America, where annual per-capita footwear spending remains under USD 45. Meanwhile, premium lines grew at a 5.48% CAGR, supported by resale platforms legitimizing pre-owned luxury and aspirational consumers trading up. TheRealReal reported a 34% year-over-year increase in women's footwear consignment, with Gucci loafers and Prada pumps retaining 68% of their original retail price, offering accessible entry points into premium tiers. Vestiaire Collective's footwear gross merchandise value rose 41%, driven by Gen-Z buyers viewing pre-owned luxury as sustainable and financially practical, as noted by the Financial Times. This trend challenges mid-tier brands as consumers increasingly favor mass-market value or authenticated premium resale over the USD 80-150 price range.

Premium brands are using material innovation to justify higher prices. Allbirds launched bacterial cellulose flats at USD 145, achieving a 38% carbon-footprint reduction compared to synthetic alternatives, appealing to eco-conscious buyers willing to pay 20-25% more for verified sustainability. Rothy's scaled its 3D-knit uppers to 1.2 million pairs in 2025, eliminating cut-and-sew waste and enabling customization, with retail prices at USD 165. Mass-market players counter with cost efficiencies. Bata automated its Bangladeshi facilities in 2025, cutting per-unit labor costs by USD 0.90 and offering retail prices below USD 30 while maintaining 18% gross margins. Deichmann's private-label strategy, which made up 62% of its 2025 footwear sales, used vertical integration to undercut branded mass competitors by 15-20% on similar styles. The bifurcation forces mid-tier brands to either scale down to compete on cost or enhance product storytelling to justify premium positioning.

By Material: Synthetic Alternatives Close the Gap

In 2025, leather accounted for 40.05% of the material market, valued for its durability and breathability in boots and formal shoes. Synthetic alternatives, however, are growing at a 5.47% CAGR, driven by bio-fabrication technologies that reduce performance gaps and costs. For example, Imperial College London's bacterial cellulose, commercialized by Nanollose in Q2 2025, achieved tensile strength within 8% of bovine leather while cutting carbon intensity by 40% and production costs to USD 12 per square meter, compared to leather's USD 18-22 range. Mycelium-based materials, developed by Ecovative and MycoWorks, entered mass production in 2025. Stella McCartney's pilot collection used mycelium uppers in 22,000 pairs, proving their viability for luxury applications. Textile uppers, mainly canvas and knit constructions, dominate casual segments where breathability is key. Rothy's 3D-knit flats, made from recycled plastic bottles, scaled to 1.2 million pairs in 2025.

Leather's dominance is under pressure from more than material innovation. In 2024, Brazilian cattle herds shrank by 6.2% due to drought, driving wet-blue leather prices to USD 2.80 per square foot in Q1 2025, a 22% year-over-year increase that cut mid-tier brand margins by 3-5 percentage points, according to Reuters. Indian tanneries, the second-largest global source, faced water-use restrictions under revised Central Pollution Control Board guidelines in 2025, reducing export volumes by 11% and tightening global supply, as reported by the Indian Leather Industry Association. Synthetic PU adoption rose by 4 percentage points in 2025 as brands sought cost stability, though European consumers still view synthetic durability as 18% lower than leather. Materials like cork, jute, and recycled ocean plastics hold under 8% combined share but help eco-conscious brands differentiate. For instance, Allbirds' sugarcane-based EVA midsoles, used in 480,000 pairs in 2025, cut petroleum dependence by 63% compared to conventional foam. ISO 14021 environmental labeling standards are becoming critical as brands face scrutiny over greenwashing claims.

By Distribution Channel: Online Gains but Offline Anchors Sales

In 2025, offline retail stores accounted for 85.95% of sales, driven by consumers' preference for tactile evaluations and immediate gratification. Online channels, supported by AI-driven sizing tools and augmented-reality try-ons that ease returns, grew at a 5.96% CAGR. Volumental's 3D foot-scanning kiosks, deployed in 3,200 locations by the end of 2025, reduced boot return rates by 28% by mapping 11 biomechanical dimensions and recommending brand-specific adjustments. SafeSize's smartphone app, using camera-based photogrammetry, achieved 2.1 million downloads in North America in 2025, enabling DTC brands to bypass physical try-ons. TikTok Shop converted 18% of Gen-Z viewers into buyers during 2025 holiday campaigns, highlighting social commerce's ability to merge discovery and purchase. Shopify-backed micro-brands, bypassing traditional wholesale, grew to 9% of online footwear sales in 2025, up from 4% in 2023, further fragmenting market share.

Offline channels remain dominant in premium and fitting-intensive categories. In 2025, luxury flagships in Asia-Pacific, where personal service and brand immersion drive sales, generated 78% of revenue for labels like Jimmy Choo and Saint Laurent, as reported by Bloomberg. Department stores, though losing share, are still vital for brand discovery. Nordstrom's 2025 footwear sales rose 6%, supported by curated assortments and in-store stylists countering e-commerce challenges. Outlet centers captured 12% of offline sales in 2025, serving as clearance hubs while maintaining brand control—something online marketplaces struggle to replicate without eroding full-price positioning. Hybrid models are emerging; Clarks' 2025 RFID-enabled stores allowed customers to scan products and complete purchases via mobile apps in-store, combining tactile shopping with digital convenience. By 2031, the channel mix is expected to stabilize at 75-80% offline as online growth slows and brands optimize store networks for same-day delivery.

Geography Analysis

In 2025, the Asia-Pacific region held a 48.18% market share, driven by China's 1.4 billion population and India's rapid urbanization. This dominance is expected to continue, supported by increasing female workforce participation and middle-class growth, sustaining footwear demand. India added 8.3 million women to formal employment in 2024-2025, raising workforce participation from 24.8% to 27.1%, which contributed to a 12-15% annual rise in non-athletic footwear purchases among these workers. China's premiumization trend saw a 19% year-over-year increase in footwear priced above CNY 800 (USD 110) in 2025, reflecting higher disposable incomes in tier-2 cities like Chengdu and Hangzhou. Southeast Asia, including Vietnam, Thailand, Indonesia, and Malaysia, accounted for 18% of regional volume in 2025, driven by manufacturing growth and e-commerce, which made up 38% of urban footwear sales. Japan's market grew modestly at 1.8% in 2025, while luxury resale platforms like Vestiaire Collective saw a 41% GMV increase, indicating rising interest in circular-economy models.

Middle East and Africa recorded the fastest growth at a 5.02% CAGR, supported by Saudi Arabia's Vision 2030 retail investments and the UAE's free-zone expansions, which added 14 new footwear distribution centers in 2025. Saudi Arabia's female workforce participation rose from 33% in 2023 to 37% in 2025, driven by public-sector hiring and relaxed guardianship laws, creating 1.2 million new footwear consumers, according to the World Bank. South Africa's formal retail sector grew 7% in 2025, with Johannesburg and Cape Town contributing 62% of premium footwear sales as the middle class expanded faster than inflation. Egypt's footwear imports increased 22% in volume during 2024-2025, but currency devaluation limited value growth to 9%, highlighting price sensitivity, as noted by the Egyptian Ministry of Trade. Morocco's free-trade agreements with the EU positioned it as a nearshoring hub, with footwear exports to Europe rising 16% in 2025, signaling supply-chain shifts.

Europe accounted for a significantthe revenue, with Germany, France, and the UK representing 58% of regional volume. Growth slowed to 2.1% due to athleisure substitution and economic challenges. Germany's July 2025 EPR scheme, requiring 25% post-consumer recycled content by 2028, led to investments in reverse logistics, benefiting large players like Inditex and H&M while straining smaller brands, according to the German Federal Environment Agency[3]Source: German Federal Environment Agency, “Extended Producer Responsibility for Footwear,” uba.de. The Netherlands' September 2025 digital product passport mandate required brands to disclose material sourcing and carbon intensity for each SKU, creating challenges for smaller brands, as reported by Reuters. North America grew 3.4%, driven by a post-pandemic recovery in occasion-wear. U.S. wedding attendance reached 2.4 million ceremonies in 2025, up 18% year-over-year, boosting demand for heels and pumps. In South America, Brazil and Argentina led growth, but currency volatility and import tariffs raised retail prices 12-18% above Asia-Pacific levels.

Competitive Landscape

The women's non-athletic footwear sector exhibits moderate fragmentation, reflecting a highly competitive landscape. Luxury titans LVMH, Kering, and Prada, known for their high gross margins achieved through curated distribution and compelling narratives, faced a revenue dip in late 2024 due to a slowdown in Chinese outbound tourism. However, Prada rebounded with a 17% retail growth in H1 2024, bolstered by new store openings in Dubai and Seoul, which are key markets for luxury retail expansion.

Mass-market leaders Skechers and Steve Madden harness vertical integration and adaptive sourcing strategies to maintain their competitive edge. Skechers not only boosted sales by 15.9% in Q3 2024 but also inaugurated 75 new stores, with a notable 60% in emerging markets, reflecting its focus on tapping into high-growth regions. Meanwhile, Steve Madden is strategically reducing its Chinese sourcing to 30% to mitigate tariff risks, shifting focus to Cambodia, Vietnam, and Mexico, which offer cost advantages and diversified supply chain options.

Digital innovators Rothy’s and Allbirds prioritize recycled materials and sustainable designs, aligning with the growing consumer demand for eco-friendly products. However, Allbirds faced a revenue downturn in 2024, leading to store closures, highlighting the challenges of scaling sustainability-focused business models. Fast-fashion behemoths, with their six-week product cycles, are shortening product life spans and pressuring wholesalers, creating a fast-paced and cost-sensitive environment. Brands integrating technologies like 3-D scanning, virtual try-ons, and blockchain authentication are reaping rewards, gaining insights that reduce returns, optimize inventory management, and enhance customer lifetime value in the fiercely competitive women's non-athletic footwear arena.

Women's Non-athletic Footwear Industry Leaders

-

Prada SpA

-

Bata Corporation

-

LVMH

-

Capri Holding

-

Chanel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Chanel showcased dipped-toe shoes on the Spring/Summer 2026 runway. The products are available in different styles and designs. Celebrities like Jessie Buckley and Tessa Thompson amplified its popularity, positioning dipped-toe heels.

- March 2025: ALDO launched its Spring and Summer 2025 collection featuring stylish non-athletic shoes including heels, sandals, and sneakers with enhanced comfort and sustainable options perfect for everyday wear.

- January 2025: Miu Miu launched its "Tyre" sneaker collection as part of its Spring/Summer 2025 Prelude line on January 22, 2025, featuring lace-up and ballerina silhouettes inspired by the 1990s with flexible natural rubber soles.

- September 2024: Prada showcased reimagined platform Mary Janes and other non-athletic footwear for Spring 2025 during Milan Ready to Wear Fashion Week, combining luxury materials with ergonomic designs.

Global Women's Non-athletic Footwear Market Report Scope

The women's non-athletic footwear products are worn on their feet for protection and fashion by women. The global women's non-athletic footwear market is segmented by type, distribution channel, category, and geography. By type, the market is segmented into boots and shoes, heels and pumps, flats, sandals, and other footwear types. By distribution channel, the market is segmented into online and offline. By category, the market is segmented into mass and premium. By geography, the global women's non-athletic footwear market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD billion).

| Boots and Shoes | Heels and Pumps |

| Flats | |

| Sandals | |

| Other Types | |

| By Category | Mass |

| Premium | |

| By Material | Leather |

| Synthetic | |

| Textile | |

| Other Materials | |

| By Distribution Channel | Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Sweden | |

| Poland | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Type | Boots and Shoes | Heels and Pumps |

| Flats | ||

| Sandals | ||

| Other Types | ||

| By Category | Mass | |

| Premium | ||

| By Material | Leather | |

| Synthetic | ||

| Textile | ||

| Other Materials | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the women non athletic footwear market be by 2031?

It is projected to reach USD 166.72 billion by 2031 at a 3.66% CAGR from 2026 to 2031.

Which product type is growing fastest?

Heels and pumps are forecast to grow at a 5.61% CAGR as occasion-wear recovers and office mandates tighten.

Which region is the quickest-growing?

The Middle East and Africa is set to expand at 5.02% CAGR, supported by Saudi Vision 2030 retail build-out and rising female employment.

Why are vegan leather alternatives gaining traction?

Bio-fabricated sheets now match 92% of leather strength at lower cost and carbon intensity, prompting rapid brand adoption.

Page last updated on: