White Lined Chipboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

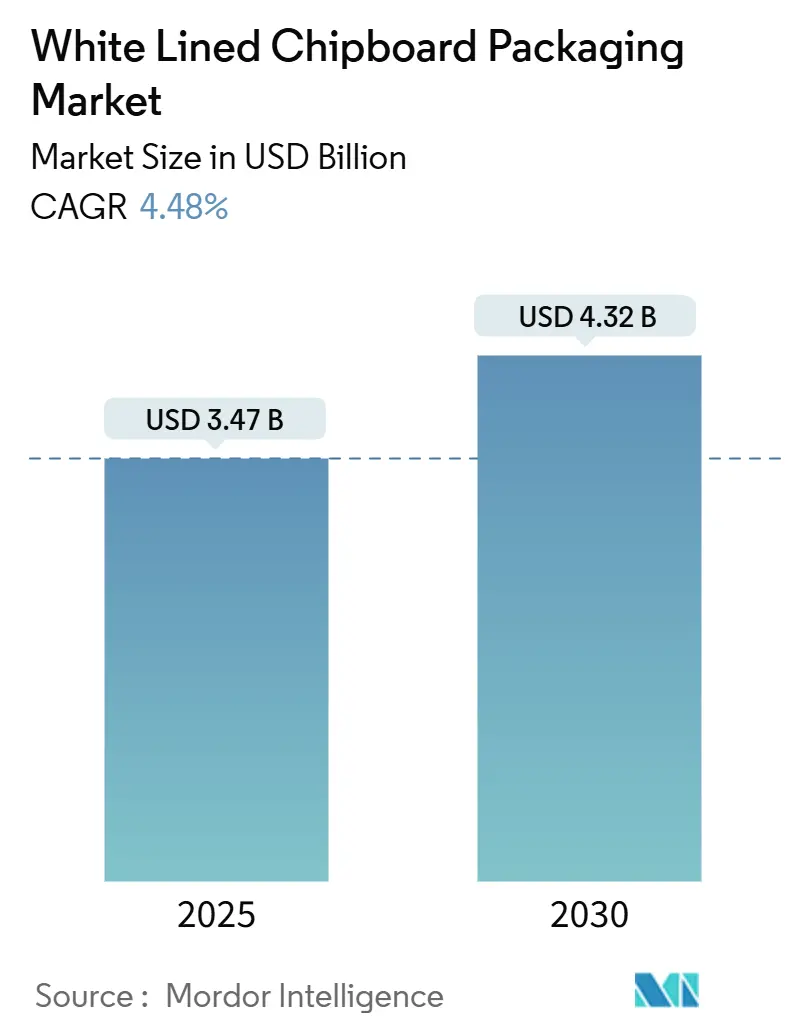

| Market Size (2025) | USD 3.47 Billion |

| Market Size (2030) | USD 4.32 Billion |

| Growth Rate (2025 - 2030) | 4.48% CAGR |

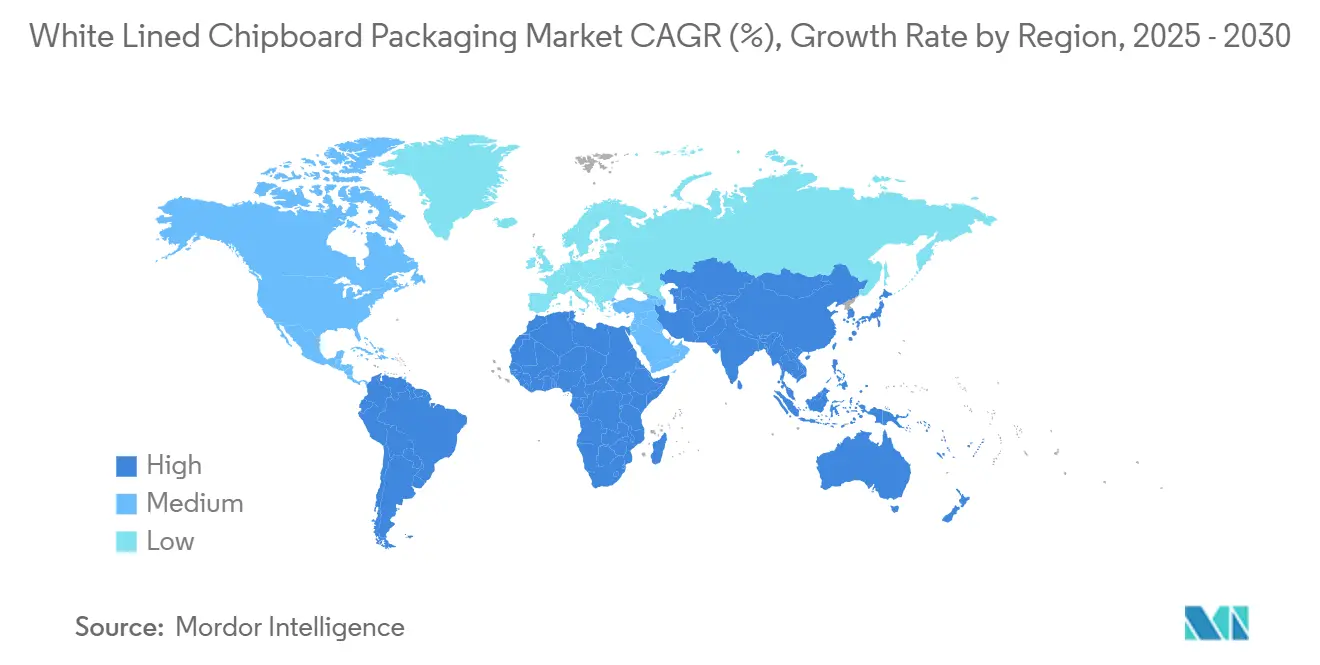

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

White Lined Chipboard Packaging Market Analysis by Mordor Intelligence

The white lined chipboard packaging market size stood at USD 3.47 billion in 2025 and is forecast to reach USD 4.32 billion by 2030, expanding at a 4.48% CAGR. Growing demand for recycled-content folding cartons, regulatory action against single-use plastics, and the rapid rise of e-commerce continue to lift baseline consumption across food, personal-care, and general retail applications. Brand owners increasingly specify mono-material solutions that simplify curb-side recycling, a requirement that favors the use of coated recycled board over multilayer plastic laminates. At the same time, high-speed digital post-print technologies enable shorter production runs, richer graphics, and late-stage customization, extending white lined chipboard’s relevance in just-in-time supply chains. Although Europe presently anchors global volume, Asia-Pacific’s acceleration points to a structural re-balancing as recycling infrastructure and environmental policy tighten across developing economies.

Key Report Takeaways

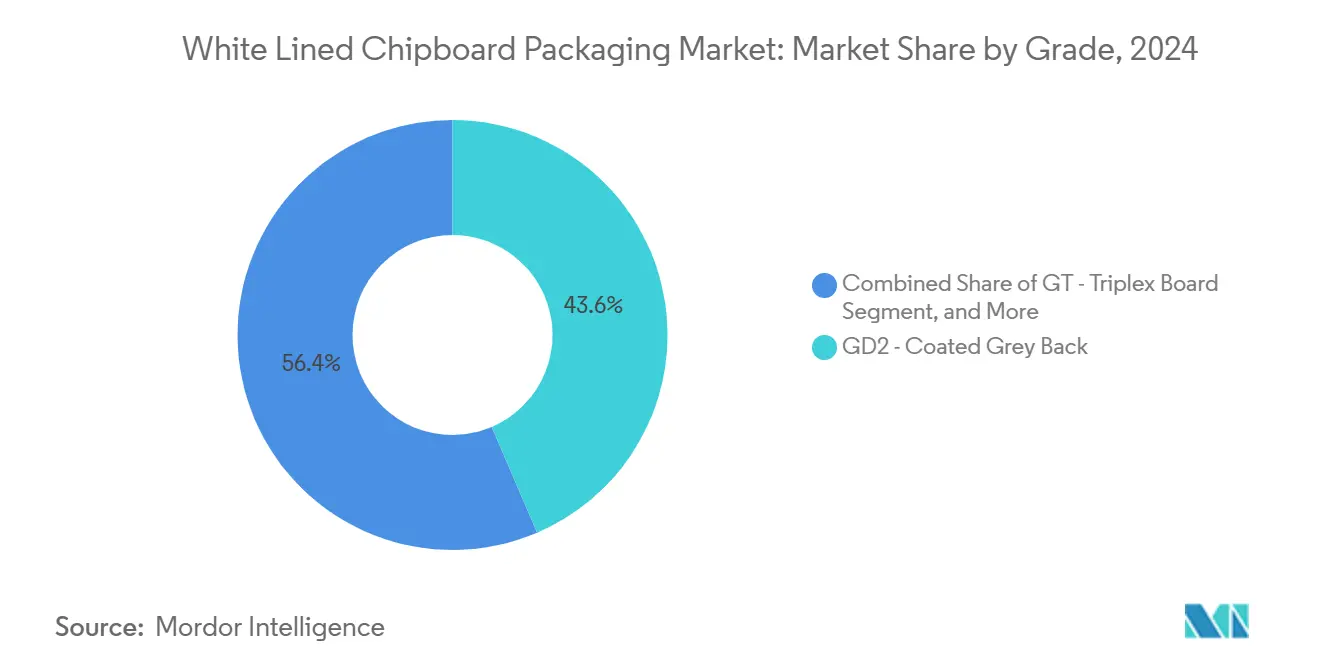

- By grade, the lined chipboard packaging market size for the GT-triplex board segment is projected to grow at a 5.37% CAGR between 2025-2030.

- By end-use, food and beverage applications captured 36.21% of the lined chipboard packaging market share in 2024.

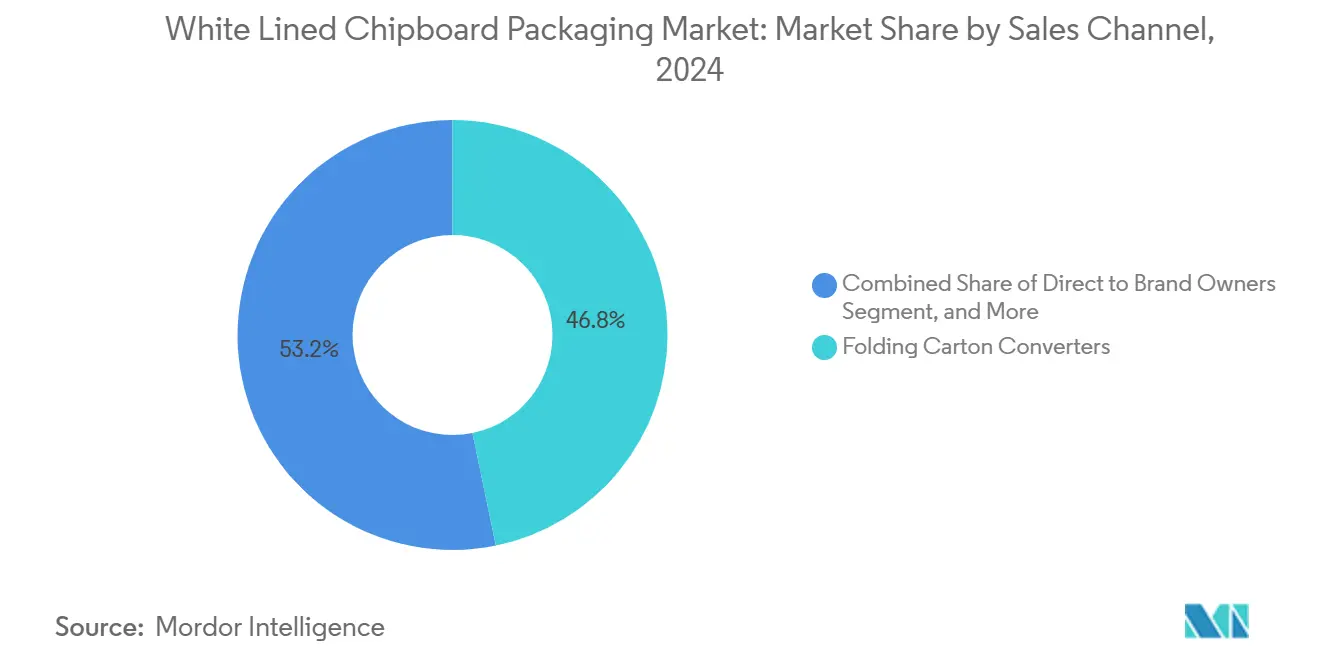

- By sales channel, the lined chipboard packaging market size for the direct-to-brand-owner segment is projected to grow at a 5.45% CAGR between 2025-2030.

- By region, Europe captured 33.89% of the lined chipboard packaging market share in 2024.

Global White Lined Chipboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for recycled content folding cartons in emerging Asia | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| E-commerce packaging volume growth requiring lightweight cartonboard | +0.8% | Global, focus on North America and Europe | Short term (≤ 2 years) |

| Regulatory bans on plastic secondary packaging boosting fiber alternatives | +0.7% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Retail brand shift to single-material mono-pack formats enabling easier recycling | +0.6% | Global, early adoption in Europe and North America | Medium term (2-4 years) |

| Investment in high-speed digital post-print technology improving WLC printability | +0.4% | North America and Europe, selective APAC | Medium term (2-4 years) |

| Access to low-cost OCC and mixed-waste feedstock lowering production cost vs FBB | +0.3% | Global, availability varies by region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in demand for recycled content folding cartons in emerging Asia

Emerging Asia’s fast-growing consumer base, combined with national sustainability mandates, is creating a structural pull for recycled-content cartons. ITC Limited generated INR 2,072.85 crores (USD 249 million) from its paperboard division in 2024 and has started India’s first bleached chemi-thermomechanical pulp line, illustrating the scale of regional capital deployment. Local fiber recovery remains insufficient to satiate demand, prompting producers to build integrated collection networks and secure mixed-waste imports. Tax incentives for recycled inputs in India and import restrictions on virgin grades in China widen the cost gap versus folding boxboard, improving the competitiveness of the white lined chipboard packaging market. Multinational consumer-goods brands, eager to meet 2025 recycled-content pledges, are switching specifications toward GD2 and GT grades, locking in multi-year offtake agreements and underpinning mill utilization across the region.

E-commerce packaging volume growth requiring lightweight cartonboard

Parcel volumes have surged since 2024, forcing brands to curb freight costs that account for up to 20% of total packaging expenditure. White lined chipboard’s relatively low basis weight offers a straightforward route to weight optimization without compromising box rigidity. International Paper processed more than 7 million tons of recovered fiber in 2024 to meet this need, expanding corrugated capacity across its United States system.[1]International Paper Company, “International Paper Company Annual Report,” internationalpaper.com Smaller, digitally native brands also value WLC’s compatibility with multicolor inkjet printing that supports variable data, limited-run promotions, and late-stage personalization. The resulting flywheel lighter packs, lower freight spend, and better graphics positions the white lined chipboard packaging market as an e-commerce enabler, especially for mid-tier merchandise where solid bleached sulfate boards are uneconomical.

Regulatory bans on plastic secondary packaging boosting fiber alternatives

March 2024 amendments to United States food-contact rules, along with the EU Single-Use Plastics Directive, sharply limit plastics in secondary and service-ware formats. Retailers pivot toward mono-material fiber packs that streamline consumer sorting and reduce extended-producer-responsibility fees. Pro Carton’s study showing a 91% end-of-life recycling rate for cartons underpins policymakers’ confidence in fiber solutions. Producers that already hold FDA and EU food-contact certifications are securing specification wins across frozen foods, ready meals, and multipacks, translating regulatory tailwinds into contracted volume. For the white lined chipboard packaging market, the regulatory shift has expanded addressable end-uses and eased competition with plastic laminates, especially where moderate barrier performance suffices.

Retail brand shift to single-material mono-pack formats enabling easier recycling

Global consumer-goods companies are rationalizing complex, multi-layer laminates in favor of single-material board structures to improve recycling metrics. Retail studies demonstrate up to 20% higher curb-side recovery for mono-material packs versus laminated constructs, motivating private-label chains in Germany, France, and the United Kingdom to issue revised specification books favoring GD2 and GD3 substrates. Although the switch sometimes raises per-unit substrate cost, brands offset outlays through lower eco-modulation fees and simpler artwork replenishment cycles. The white lined chipboard packaging market therefore benefits from a demand mix that rewards standard grades delivering consistent print surfaces, predictable die-cutting behavior, and seamless integration with automated erect-fill-seal lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of recovered paper and energy costs | -0.9% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Performance gap versus virgin fiber boards for premium applications | -0.6% | Global, particularly high-end consumer goods | Long term (≥ 4 years) |

| Supply tightness of FDA-grade recycled fiber in NA/EU food contact | -0.4% | North America and Europe | Medium term (2-4 years) |

| Consolidation of carton converters reducing buyer base for small mills | -0.3% | Global, concentrated in mature markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price volatility of recovered paper and energy costs

Average OCC indices swung 35% from peak to trough during 2024-25, eroding gross margins at mills unable to pass surcharges downstream. Billerud’s interim results cited rising energy tariffs among the chief pressures on European operations, even as North American plants achieved an 18% EBITDA margin. Energy represents 15-25% of total board cost, and carbon-pricing mechanisms in the EU elevate exposure further. Forward hedging mitigates spot volatility but compresses upside in low-price cycles, dampening cash-flow optionality for capex projects. Smaller independents in Spain and Poland, lacking purchasing leverage, risk margin compression and potential idling during price spikes, tempering overall expansion of the white lined chipboard packaging market.

Performance gap versus virgin fiber boards for premium applications

Recycled fibers’ shorter length and residual contaminants limit stiffness, brightness, and barrier performance, restricting use in high-end cosmetics, premium chocolate, and fine spirits. Mayr-Melnhof reported that food-and-specialties products comprised 72% of 2023 sales, underscoring ongoing reliance on virgin or hybrid boards for more demanding packs. Despite resin-barrier coatings, WLC grades struggle to match the grease-resistance of solid bleached sulfate in rich butter cookie tins and high-oil snacks. As luxury brands continue to treat packaging as an extension of product identity, virgin fiber boards retain pricing power, capping WLC’s penetration into the top echelon of consumer goods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Cost-efficient GD2 sustains leadership while GT captures premium niches

GD2 coated grey back dominated 2024 sales, supported by its 43.56% white lined chipboard packaging market share across breakfast cereal, snack, and dry-goods cartons. The grade balances acceptable whiteness with a lower-cost grey reverse made from mixed-waste furnish, ensuring competitive price positioning against folding boxboard. During 2025-30, GD2 volume is projected to track overall demand, while the segment’s modest price escalations maintain converter loyalty. Producers continue to refine coating recipes, enhancing offset print gloss and reducing mottling on large solid areas, features valued by fast-moving consumer-goods brands.

GT triplex board, carrying three layers for enhanced stiffness and smoothness, is forecast to log a 5.37% CAGR above the overall white lined chipboard packaging market size growth rate serving perfume sets, confectionery gift packs, and premium personal-care cartons. Although GT’s input cost profile is 10-15% higher than GD2, its bulk stiffness enables downgauging that partly neutralizes price deltas. Multi-coating stations accommodate spot UV varnishes and embossing finishes frequently specified by prestige brands. GD3 coated white back remains a niche for applications requiring near-lithographic reverses, while “other” grades, including barrier-coated WLC, expand gradually as PFAS-free recipes reach industrial maturity.

By End-use Industry: Food drives bulk, cosmetics accelerate on premium positioning

Food and beverage retained 36.21% of 2024 shipments, reflecting the category’s mass-market ubiquity and regulatory acceptance of recycled-content secondary packs. Shelf-stable cereals, frozen meals, and beverage multipacks anchor GD2 tonnage, leveraging white lined chipboard’s machinability on high-speed fill lines. The segment’s scale supports long-run economics and underwrites base-load for many European mills, stabilizing plant utilization even during consumer slowdowns.

Personal-care and cosmetics, posting a 5.14% CAGR, exemplify the migration from rigid plastics to decorated fiber packs that telegraph environmental credentials without sacrificing shelf appeal. Embossing, foil-stamping, and metallic inks find receptive surfaces on GT triplex board, permitting smaller format cartons that still hold structural integrity. Healthcare and pharmaceuticals maintain mid-single-digit growth, buoyed by OTC medicine demand and the universal need for tamper-evident packaging. Household care leverages WLC’s bulk to deliver robust powder-laundry boxes, while electrical-electronics brands evaluate GD3 for light-component trays and accessory wraps, broadening downstream diversity for the white lined chipboard packaging market.

By Sales Channel: Direct engagement reshapes traditional converter hierarchies

Folding-carton converters processed 46.78% of all board in 2024, acting as technical partners that optimize runability, ink laydown, and die-cut precision for global brand owners. However, the direct-to-brand route is projected for a 5.45% CAGR as vertically integrated consumer-goods companies internalize converting to capture margins and improve supply-chain visibility. Multinational food groups now commission on-site converting cells adjacent to filling lines, ordering WLC reels directly from mills under VMI (vendor-managed inventory) programs that reduce floor stock by up to two weeks.

Corrugated-litho-lam specialists consume higher-grammage grades for heavy-duty e-commerce shippers that require laminated board faces. While this channel remains a smaller volume share, its graphics-intensive focus provides above-average EBITDA for compatible mills. As converter consolidation progresses, smaller mills evaluate toll-coating alliances and co-investment deals with high-growth direct-brand customers, seeking to offset risk tied to a shrinking independent converter base. Digital printing also levels the field by allowing converters with compact presses to compete on short-run agility, sustaining a diverse channel mix within the white lined chipboard packaging market.

Geography Analysis

Europe retained 33.89% of 2024 worldwide shipments, its leadership rooted in mature recovery networks and policy instruments such as the EU Circular Economy Action Plan that subsidize recycled-content adoption. Municipal collection schemes deliver consistent quality fiber, while converter clusters in Germany, France, Italy, and the United Kingdom provide scale back-integration. Renewi, for example, achieved a 63.2% group recycling rate in 2024 and targets 75% via advanced sorting lines, reinforcing the feedstock backbone for board mills across Benelux and northern France.[2]Renewi, “Annual Report and Accounts 2024,” renewi.com Producers in Europe also benefit from harmonized food-contact regulations that accelerate multi-market rollouts, maintaining the region’s pull on GD2 and GD3 tonnage.

Asia-Pacific, expected to grow at a 5.28% CAGR through 2030, captures the white lined chipboard packaging market’s most dynamic demand. China and India dominate volume through rising urban middle-class consumption, while ASEAN economies add incremental layers of e-commerce-driven carton demand. APP’s zero-waste-to-landfill initiative and 58% renewable-energy share illustrate the sustainability transition underway among major regional suppliers. As governments implement plastic-tax regimes and import duties on virgin fiber, local WLC capacity accelerates, though recycled fiber shortages still necessitate supplemental imports from Europe and the United States.

North America records steady mid-single-digit growth as brand sustainability goals intersect with technical hurdles surrounding FDA food-contact compliance. The 2025 withdrawal of PFAS notifications forces converters to accelerate qualification of barrier-coated WLC, yet limited availability of low-migration recycled fibers constrains immediate substitution. European entrants such as Billerud are channeling SEK 1.2 billion (USD 0.11 billion) into United States mills to capitalize on that supply gap. South America and MENA remain emergent zones, with capacity additions expected chiefly in Brazil, Turkey, and the Gulf states where consumer-goods localization drives folding-carton demand.

Competitive Landscape

Competitive intensity is moderate: the five largest groups hold roughly 55-60% of global capacity, yet numerous regional specialists thrive on proximity, service speed, and niche technical capabilities. Integration strategies continue to dominate. Heavyweights such as Mayr-Melnhof, Graphic Packaging, and RDM pair recovered-paper collection with board production, minimizing fiber-cost volatility and ensuring supply continuity for strategic converters. Sustainability differentiation now rivals cost leadership; companies boasting cradle-to-cradle certifications and closed-loop recovery programs secure multi-year contracts with multinational brands seeking audited carbon footprints.

Consolidation remains a defining force. The July 2024 closure of the Smurfit Kappa-WestRock deal, creating a USD 34 billion revenue entity, compressed the buyer landscape for smaller mills while unlocking roughly USD 400 million in projected annual synergies.[3] Smurfit Westrock, “Smurfit Westrock Reports Fourth Quarter and Full Year 2024 Results,” smurfitwestrock.com Similarly, Clearwater Paper’s USD 700 million acquisition of Graphic Packaging’s Augusta mill in 2024 expanded its bleached board footprint, signaling a shift toward premium, barrier-coated offerings. Beyond M&A, capex is trending toward digital-ready coating lines and PFAS-free barrier chemistries. Stora Enso’s Oulu start-up represents the largest single investment in consumer board since 2021 and uses AI-driven quality-control loops to achieve nameplate capacity within 24 months benchmark that other mills may emulate.

Regional specialists retain defensible positions by tailoring furnish mixes to local waste streams and offering rapid lead-times that large multinationals find hard to match. Scandinavian players leverage renewable-energy access to market low-carbon board, while Indonesian and Chinese mills blend imported OCC with domestic recovered-paper grades to optimize furnish cost. Competitive advantage is therefore shifting from simple scale toward a composite of sustainability credentials, digital printing compatibility, and supply-chain integration factors that collectively shape the medium-term trajectory of the white lined chipboard packaging market.

White Lined Chipboard Packaging Industry Leaders

Mayr-Melnhof Karton AG

Graphic Packaging Holding Company

Nine Dragons Paper Holdings Ltd.

Georgia-Pacific LLC

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stora Enso commenced operations of its EUR 1 billion (USD 1.08 billion) consumer-board line at Oulu, targeting 750,000 tonnes of annual capacity.

- February 2025: Smurfit Westrock reported USD 7.5 billion Q4 2024 sales and confirmed USD 400 million synergy target.

- January 2025: FDA ruled that 35 PFAS-related food-contact notifications are no longer effective, effective June 30 2025.

- August 2024: Graphic Packaging announced replacement of 450 million plastic packs and a 2050 net-zero commitment.

Global White Lined Chipboard Packaging Market Report Scope

| GD2 - Coated Grey Back |

| GD3 - Coated White Back |

| GT - Triplex Board |

| Other WLC Grades |

| Food and Beverage |

| Personal Care and Cosmetics |

| Healthcare and Pharmaceuticals |

| Household and Detergents |

| Tobacco |

| Electrical and Electronics |

| Other End-use Industries |

| Folding Carton Converters |

| Corrugated and Litho-lam Converters |

| Direct to Brand Owners |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Grade | GD2 - Coated Grey Back | ||

| GD3 - Coated White Back | |||

| GT - Triplex Board | |||

| Other WLC Grades | |||

| By End-use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Healthcare and Pharmaceuticals | |||

| Household and Detergents | |||

| Tobacco | |||

| Electrical and Electronics | |||

| Other End-use Industries | |||

| By Sales Channel | Folding Carton Converters | ||

| Corrugated and Litho-lam Converters | |||

| Direct to Brand Owners | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the white lined chipboard packaging market in 2025 and how fast is it growing?

The market is valued at USD 3.47 billion in 2025 and is projected to grow at a 4.48% CAGR through 2030.

Which grade commands the highest share within white lined chipboard?

GD2 coated grey back leads with 43.56% share, favored for cost-efficient mass-market folding cartons.

Which region offers the strongest growth outlook?

Asia-Pacific shows the highest trajectory, with a projected 5.28% CAGR through 2030 driven by e-commerce and sustainability mandates.

What is driving the shift toward white lined chipboard in e-commerce?

Lightweight board reduces freight costs and supports high-resolution digital printing, meeting both economic and branding needs.

How will recent PFAS rulings affect demand?

The January 2025 withdrawal of 35 PFAS-related food-contact approvals accelerates brand migration to compliant fiber-based boards.

Page last updated on: