Clay-Coated Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

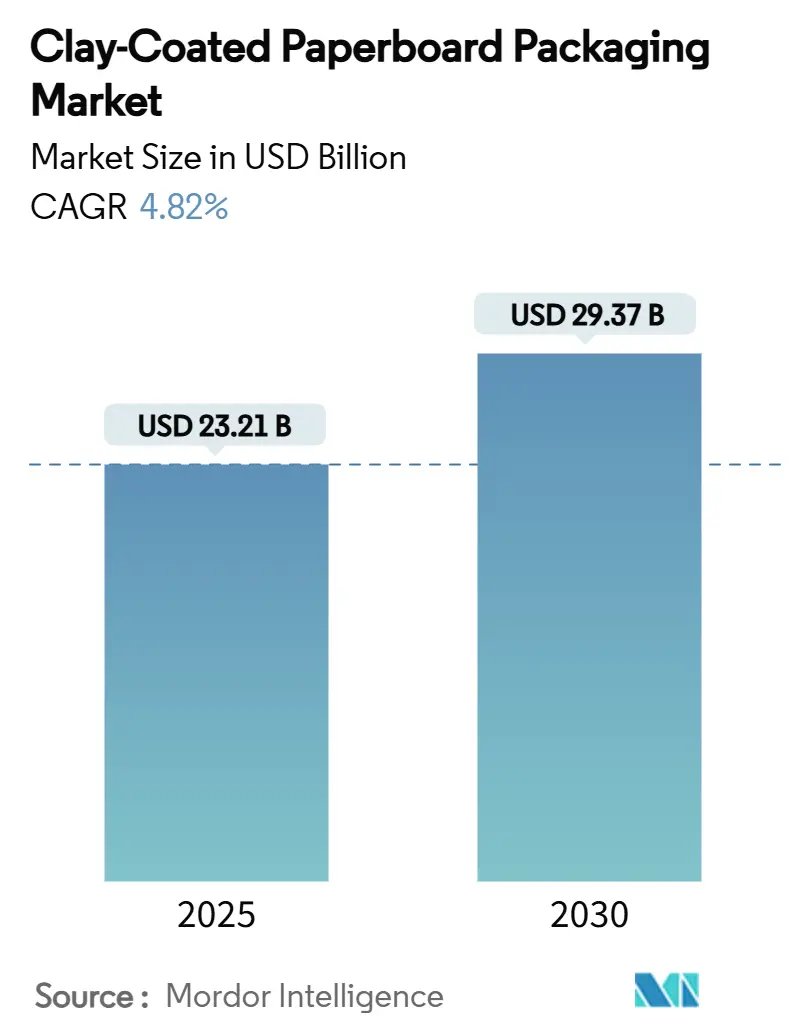

| Market Size (2025) | USD 23.21 Billion |

| Market Size (2030) | USD 29.37 Billion |

| Growth Rate (2025 - 2030) | 4.82% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clay-Coated Paperboard Packaging Market Analysis by Mordor Intelligence

The clay-coated paperboard packaging market size stands at USD 23.21 billion in 2025 and is forecast to climb to USD 29.37 billion by 2030, advancing at a 4.82% CAGR over the period. Strengthening restrictions on single-use plastics, rapid phase-outs of PFAS coatings and long-term brand commitments to fiber solutions align to keep the clay-coated paperboard packaging market on a clear expansion path. Corporate investment in PFAS-free barrier chemistries, combined with consumer preference for plastic-free formats, is lifting conversion volumes across both recycled and virgin grades. Capacity rationalization among global integrated producers is tightening supply in mature regions, elevating pricing leverage for mills that can guarantee regulatory compliance. Meanwhile, direct-to-consumer fulfilment, where multi-color corrugated shippers dominate, underpins incremental demand for high-printability liners an attribute that clay-coated paperboard supplies better than uncoated alternatives. Together, these forces reinforce the clay-coated paperboard packaging market’s role as an enabler of the circular economy transition.

Key Report Takeaways

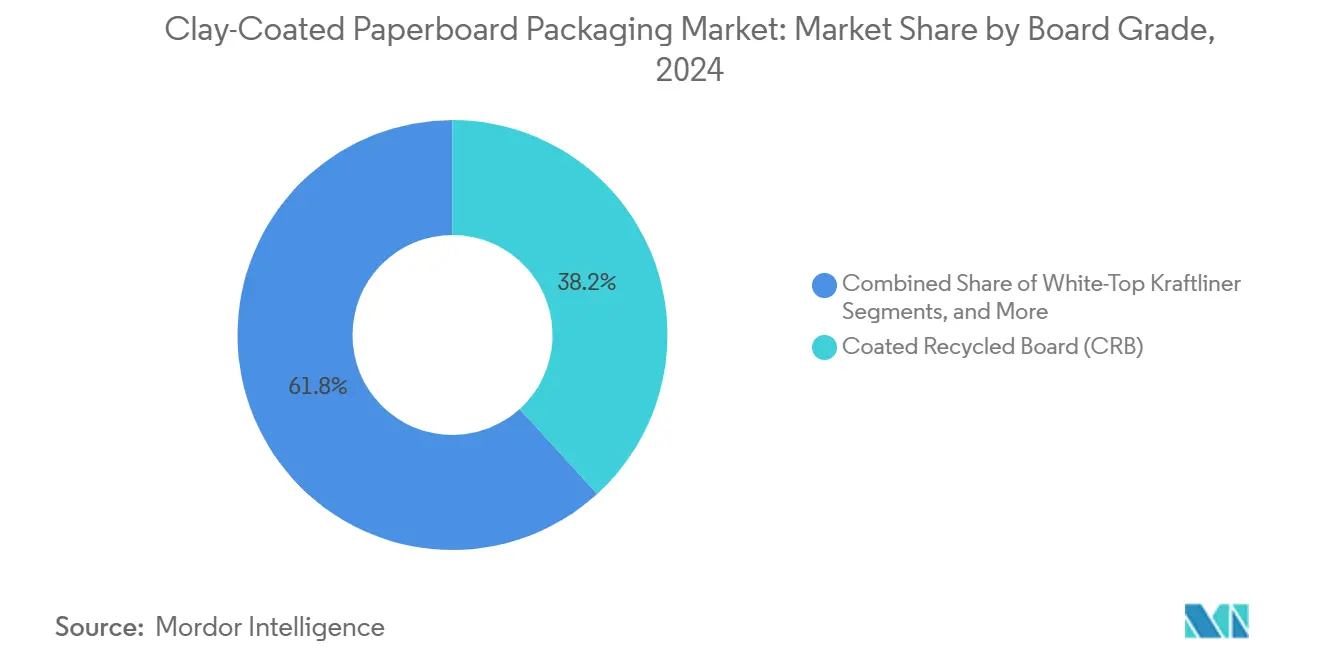

- By board grade, Coated Recycled Board captured 38.24% of the clay-coated paperboard packaging market share in 2024.

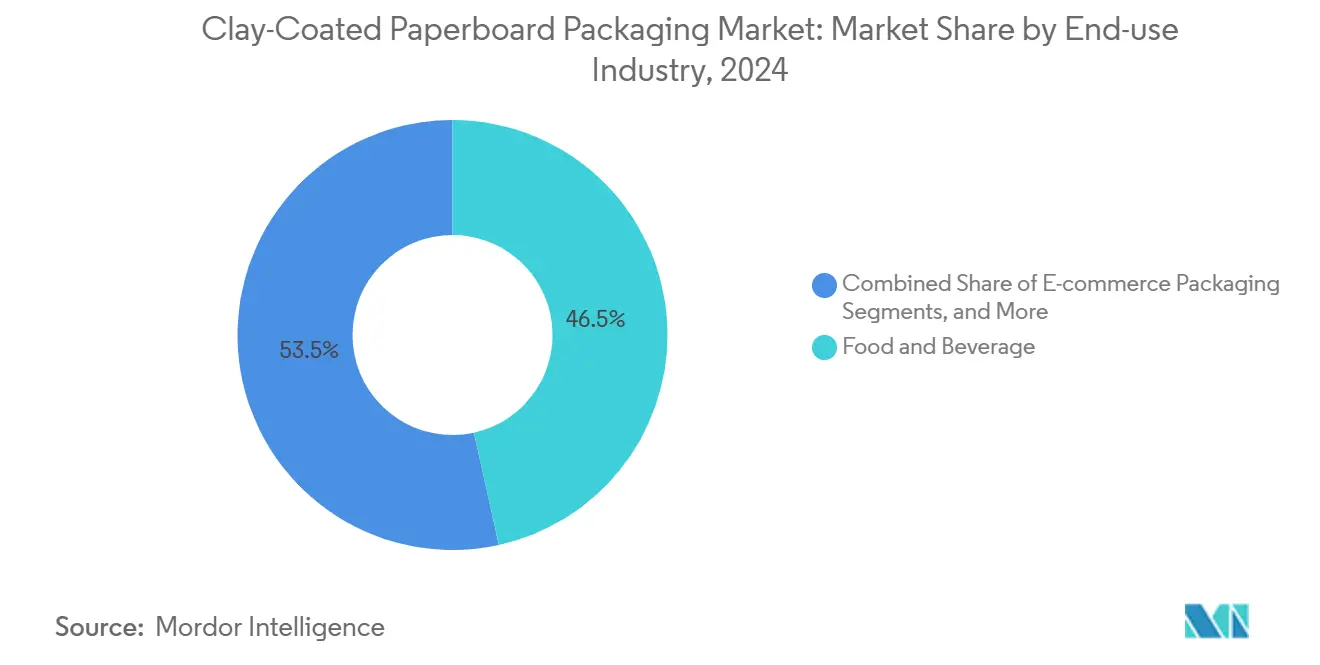

- By end-use industry, the clay-coated paperboard packaging market size for the e-commerce packaging segment is projected to grow at a 7.80% CAGR between 2025-2030.

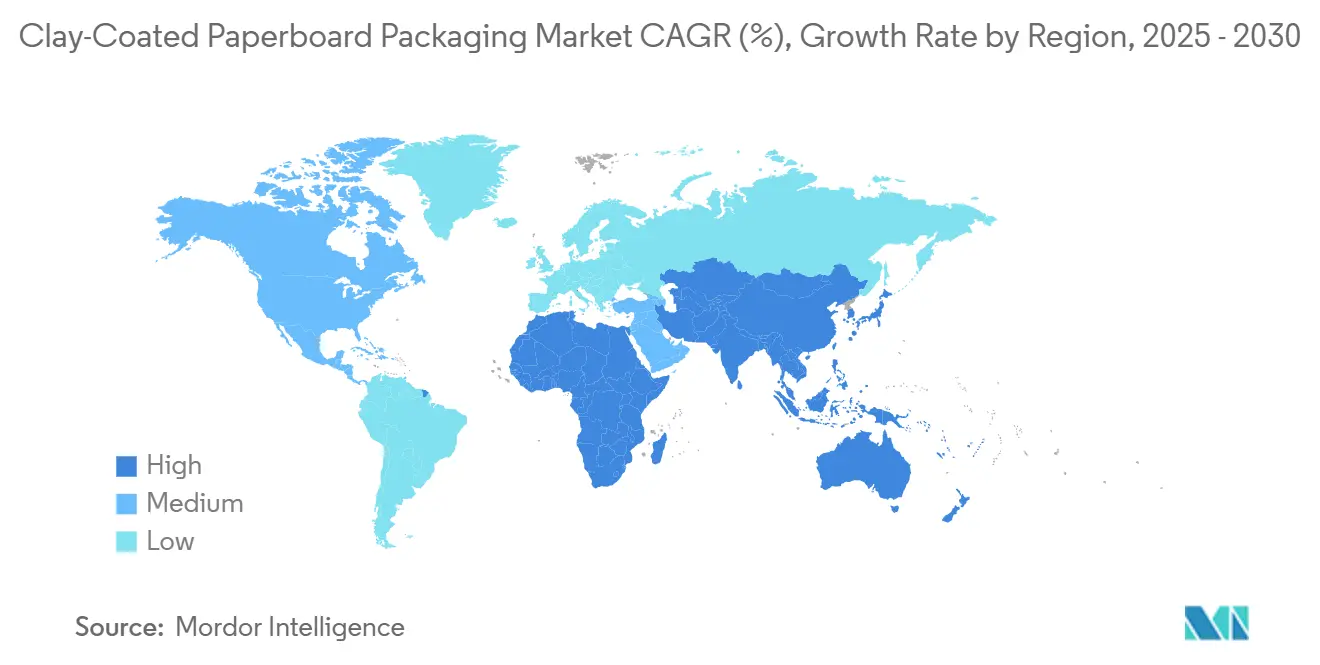

- By geography, Asia-Pacific captured a 41.21% of the clay-coated paperboard packaging market share in 2024.

Global Clay-Coated Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for plastic-free foodservice disposables | +1.2% | Global (EU and North America lead) | Medium term (2-4 years) |

| Brand-owner commitments to fiber-based retail packaging | +0.9% | Developed markets | Long term (≥ 4 years) |

| E-commerce shift boosting multi-color corrugated shippers | +0.8% | APAC and North America | Short term (≤ 2 years) |

| Lightweighting via high-stiffness clay-coated grades | +0.6% | Global hubs | Medium term (2-4 years) |

| Mills retrofitting for PFAS-free barrier coatings | +0.5% | EU and North America | Long term (≥ 4 years) |

| Emerging integrated Asian capacity expansions | +0.4% | APAC core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Plastic-Free Foodservice Disposables

Foodservice operators are fast abandoning fluorinated grease barriers after the EU’s 25 ppb PFAS cap and California’s 100 ppm limit converged on a narrow compliance window.[1]RRMA, “EU Packaging Law to Impose Strict PFAS Restrictions in Food Packaging by 2026,” rrma-global.org With the United States Food and Drug Administration withdrawing 35 historic food-contact notifications by June 2025, the clay-coated paperboard packaging market gained a powerful demand shock that favors fiber substrates meeting direct-food-contact rules. Converters that invested in mineral-and-biopolymer barrier chemistries now command premium pricing, as quick-service chains rush to qualify suppliers. Volume migration from extruded polyethylene wraps and PFAS-laden wraps is already visible in QSR pilot programs across Europe, amplifying material shifts in advance of the August 2026 EU enforcement date. As a result, manufacturers capable of running dual-blade coaters with water-based dispersions are logging higher mill utilization and stronger contract backlogs than peers tied to legacy wax or fluorochemical systems.

Brand-Owner Commitments to Fiber-Based Retail Packaging

Leading consumer-goods companies have embedded recyclable-paperboard targets into procurement scorecards that extend through 2030. Graphic Packaging realized USD 200 million in 2023 revenue tied to these sustainable formats, validating the commercial depth of this pipeline. Procurement teams now specify minimum recycled content thresholds, FSC certification, and curbside recyclability, directing steady orders toward mills whose clay-coated paperboard grades satisfy each criterion. For producers, these multi-year commitments translate into predictable baseload volumes that mitigate pulp and energy price swings, stabilizing asset-utilization rates across economic cycles.

E-Commerce Shift Boosting Multi-Color Corrugated Shippers

The structural pivot toward direct-to-consumer channels has elevated unboxing aesthetics into a brand-differentiation lever, pushing demand toward printable white-liner and mottled-white tops. Packaging Corporation of America reported record Q1 2025 containerboard output of 1.25 million tons evidence of sustained e-commerce flow even amid macro headwinds. Clay-coated liners outperform uncoated kraft in litho-lamination and digital-print applications, enabling richer color saturation and tight registration. As shipping boxes double as marketing canvases, brand managers pay premiums for high-stiffness white surfaces that survive parcel networks without scuffing. Consequently, the clay-coated paperboard packaging market captures incremental tonnage from legacy brown grades, reinforcing its growth moat in parcel commerce.

Lightweighting via High-Stiffness Clay-Coated Grades

Mills are engineering kaolin-rich coatings and multi-ply constructions that preserve bending stiffness at lower basis weights, trimming fiber usage and freight costs. Billerud expects its efficiency program to lift EBITDA by SEK 1.5 billion (USD 143 million) in 2025, with lightweighting cited as a critical lever. Stora Enso’s Oulu conversion will dedicate high-speed coaters to fine-tune stiffness-to-weight ratios once ramp-up is complete in 2027. Down-gauging directly lowers greenhouse-gas intensity per package while freeing mill capacity for more saleable rolls, reinforcing cost and sustainability value propositions to converters seeking total cost of ownership reductions.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile OCC and virgin-pulp prices squeezing margins | -0.8% | Global | Short term (≤ 2 years) |

| Regulatory uncertainty on recyclability labelling | -0.4% | EU and North America | Medium term (2-4 years) |

| Capital intensity of high-gloss coating lines | -0.3% | Developed markets | Long term (≥ 4 years) |

| Competition from polymer-coated frozen-food cartons | -0.2% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile OCC and Virgin-Pulp Prices Squeezing Margins

Recycled fiber shortages and elevated energy costs have destabilized mill economics. Sonoco responded with a EUR 60 per-ton list-price increase across Europe in March 2025, citing tight OCC supply paired with high gas prices. Graphic Packaging’s 2024 revenue slide to USD 8.8 billion illustrates how input inflation still depresses topline even when volumes remain firm. While long-term contracts help transfer some burden downstream, margin compression remains the chief near-term headwind for the clay-coated paperboard packaging market as mills juggle volatile recycle flows and fresh-pulp spikes.

Regulatory Uncertainty on Recyclability Labelling

Converging yet inconsistent definitions of “widely recyclable” create compliance friction for multinational converters. The EU’s Packaging and Packaging Waste Regulation sets a 2030 recyclability mandate but continues to refine design-for-recycling test protocols, delaying capital decisions on new coating lines. Australia’s draft scheme layers minimum PCR thresholds of 60% from Year 1 without finalizing certification bodies, adding parallel complexity. Until harmonized standards emerge, producers hedge by over-engineering substrates to pass multiple regional hurdles, inflating formulation costs and elongating innovation lead times within the clay-coated paperboard packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Board Grade: CRB Dominance Reflects Sustainability Priorities

The clay-coated paperboard packaging market size attributable to Coated Recycled Board was the largest in 2024, capturing 38.24% revenue on the strength of corporate recycled-content mandates.[2]Cascades Inc., “Annual Report 2023,” cascades.com Integrated mills leverage closed-loop OCC collections to anchor cost advantages while meeting brand recyclability pledges. Graphic Packaging’s USD 1 billion Waco mill, scheduled to start production in 2026, exemplifies large-scale CRB investment aimed at lowering unit costs and shrinking carbon footprints simultaneously. White-Top Kraftliner is scaling fastest at a 6.90% CAGR, reflecting e-commerce brand owners’ willingness to pay for premium cap-layers that enhance print appeal. Solid Bleached Sulfate retains niche share in pharma and cosmetics, where virgin fiber purity is non-negotiable, while Coated Unbleached Kraft remains entrenched in heavy-duty beverage carriers demanding wet-strength attributes. Clay-Coated Newsback persists as a budget choice for folding cartons, yet quality constraints limit upside.

CRB’s ascent is underwritten by retrofit economics: converting legacy newsprint or fine-paper machines into recycled paperboard costs significantly less than greenfield virgin lines. Cascades’ Bear Island restart added 465,000 short tons of 100% recycled containerboard in Virginia, illustrating capital-light pathways to scale. Conversely, SBS growth is tempered by high bleached-pulp costs and the expense of meeting PFAS-free barrier mandates. On balance, a portfolio approach—pairing CRB for mass markets with WTKL for premium print—positions converters to capture the widest spread of volume across the clay-coated paperboard packaging market.

By End-Use Industry: Food Packaging Drives Volume Growth

Food and beverage maintained 46.54% of 2024 clay-coated paperboard packaging market share, anchored in frozen meals, bakery trays and QSR clamshells that rely on grease resistance and direct-food-contact approvals. The FDA’s withdrawal of key PFAS clearances accelerates substrate shifts, locking in higher order books for barrier-coated grades through mid-decade. In parallel, the e-commerce channel is forecast to log a 7.80% CAGR, fueled by brand adoption of multi-color shipper boxes that exploit the stiffness and print gloss of clay-coated liners. Consumer-goods and personal-care companies increasingly substitute rigid plastics with folding cartons to boost recyclability claims, supporting SBS and CRB demand. Healthcare packaging remains a steady adopter of virgin grades, as pharmaceutical blister cards and diagnostic kits prioritize purity. Industrial users value CUK’s wet-strength and puncture resistance, but growth is modest compared with visually oriented segments benefiting from the clay-coated paperboard packaging market’s print advantages.

Across end-use cases, sustainability messaging is now inseparable from functional specification. Nippon Paper’s plan to generate JPY 650 billion (USD 4.29 billion) sales from liquid and household packaging by FY 2030 underscores how clay-coated paperboard facilitates both barrier performance and brand ESG statements. Sappi’s 22% year-on-year jump in North American packaging volumes confirms a broader pivot among converters away from plastic-lined cups toward fiber cartons. These data points collectively reinforce demand visibility for the clay-coated paperboard packaging market through 2030.

Geography Analysis

Asia-Pacific contributed 41.21% of revenue to the clay-coated paperboard packaging market in 2024. China dominates installed capacity, leveraging scale economies and government-backed recycling mandates to anchor regional supply chains. Japanese and Korean mills export premium SBS and specialty liners built on advanced coating know-how, while Southeast Asian producers supply cost-advantaged CRB to global brand owners. Shandong Sun Paper’s CNY 20.5 billion (USD 2.8 billion) half-year revenue evidences China’s heft in both output and domestic absorption.[3]Shandong Sun Paper, “2024 Half-Year Report,” finance.sina.com.cn Nevertheless, tighter environmental permits and export tariff uncertainty inject volatility into Asian trade flows, prompting some multinationals to near-shore supply into North America and Europe.

Africa offers the highest regional growth, projected at a 7.20% CAGR to 2030. Rising middle-class incomes in Nigeria, Kenya and South Africa are spurring adoption of packaged foods and hygiene products, intensifying demand for folding cartons and corrugated shippers. Limited local board mills necessitate imports, inflating costs but also motivating joint ventures that localize capacity. Governments in Egypt and Ghana have signaled duty relief for machinery imports, paving the way for modular coating lines that match regional fiber availability. While currency fluctuations and logistics bottlenecks persist, the underlying consumption trajectory keeps the clay-coated paperboard packaging market’s African opportunity compelling.

North America and Europe, though mature, will continue to pivot spending toward PFAS-compliant grades and lightweight CRB replacements. The European Union’s PPWR, in force since February 2025, clarifies recyclability targets and sets the foundation for harmonized eco-modulation fees, incentivizing innovation investments. North America benefits from NAFTA-aligned recovery systems, yet raw-material price volatility challenges profit pools. Both regions show limited volume upside but meaningful value upside as converters turn to high-gloss, digital-ready linerboards that command premium pricing inside the clay-coated paperboard packaging market.

Competitive Landscape

The top 10 producers control roughly 60-65% of global machine tonnage, confirming a moderately concentrated structure. WestRock’s merger with Smurfit Kappa and International Paper’s announced acquisition of DS Smith reshaped the league tables, delivering scale that supports greater purchasing power in recovered fiber and chemicals. Post-merger entities are closing high-cost capacity 500,000 tons shuttered in North America during Q1 2025 alone to streamline asset footprints. Mid-tier players like Billerud and Sappi differentiate through specialty coating recipes and service agility, targeting customers seeking faster product-development cycles. Asian conglomerates, meanwhile, pursue greenfield expansions to supply both domestic growth and export volume, banking on lower labor and energy inputs.

Investment intensity remains high. Graphic Packaging’s USD 1 billion Waco facility, optimized for recycled board, illustrates the substantial capital required to compete in the clay-coated paperboard packaging market. Mills are also dedicating multi-million-dollar retrofits to eliminate PFAS and swap to water-based barriers, betting regulatory certainty will deliver price premiums. Digital-twin platforms and closed-loop moisture controls further separate leading mills from laggards, lowering trim waste and improving gloss uniformity. Competitive gaps are most evident in Africa and parts of Latin America, where local supply is sparse, encouraging multinationals to form JV mills or deploy portable coaters to shorten lead times.

Strategic focus areas across incumbents converge on three vectors: vertical fiber integration, PFAS-free coating mastery and geographic diversification. Companies unable to secure affordable OCC or virgin pulp are susceptible to margin swings, while those late to PFAS compliance risk customer attrition. Consequently, portfolio pruning, M&A and innovation partnerships are likely to continue reshaping the clay-coated paperboard packaging market’s pecking order through the decade.

Clay-Coated Paperboard Packaging Industry Leaders

Smurfit Westrock plc

Graphic Packaging Holding Company

International Paper Company

Stora Enso Oyj

Metsä Board Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cascades closed its Niagara Falls, New York board mill, eliminating 100+ jobs to rationalize North American capacity amid margin pressure.

- May 2025: Smurfit Westrock posted USD 7.66 billion Q1 revenue and confirmed closure of 500,000 tons of paper capacity to lift asset efficiency.

- April 2025: Packaging Corporation of America delivered record USD 204 million quarterly profit on 1.25 million tons of containerboard production.

- March 2025: Sonoco raised European core-board prices by EUR 60 (USD 64.9) per ton as OCC shortages intensified.

Global Clay-Coated Paperboard Packaging Market Report Scope

| Solid Bleached Sulfate (SBS) |

| Coated Unbleached Kraft (CUK) |

| Coated Recycled Board (CRB) |

| Clay-Coated Newsback (CCNB) |

| White-Top Kraftliner (WTKL) |

| Food and Beverage |

| Consumer Goods and Personal Care |

| Healthcare and Pharmaceuticals |

| Industrial and Chemical |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Board Grade | Solid Bleached Sulfate (SBS) | ||

| Coated Unbleached Kraft (CUK) | |||

| Coated Recycled Board (CRB) | |||

| Clay-Coated Newsback (CCNB) | |||

| White-Top Kraftliner (WTKL) | |||

| By End-use Industry | Food and Beverage | ||

| Consumer Goods and Personal Care | |||

| Healthcare and Pharmaceuticals | |||

| Industrial and Chemical | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the clay-coated paperboard packaging market?

The clay-coated paperboard packaging market size is USD 23.21 billion in 2025.

How fast will the clay-coated paperboard packaging market grow through 2030?

The market’s forecast CAGR is 4.82%, carrying revenue to USD 29.37 billion by 2030.

Which board grade holds the largest market share?

Coated Recycled Board leads with 38.24% clay-coated paperboard packaging market share in 2024.

What end-use segment is expanding the quickest?

E-commerce packaging is projected to post a 7.80% CAGR between 2025 and 2030.

Why are PFAS-free coatings critical for market growth?

Regulations in the EU and several U.S. states set strict PFAS limits, creating immediate demand for compliant barrier chemistries and accelerating mill retrofits.

Page last updated on: