Weight Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

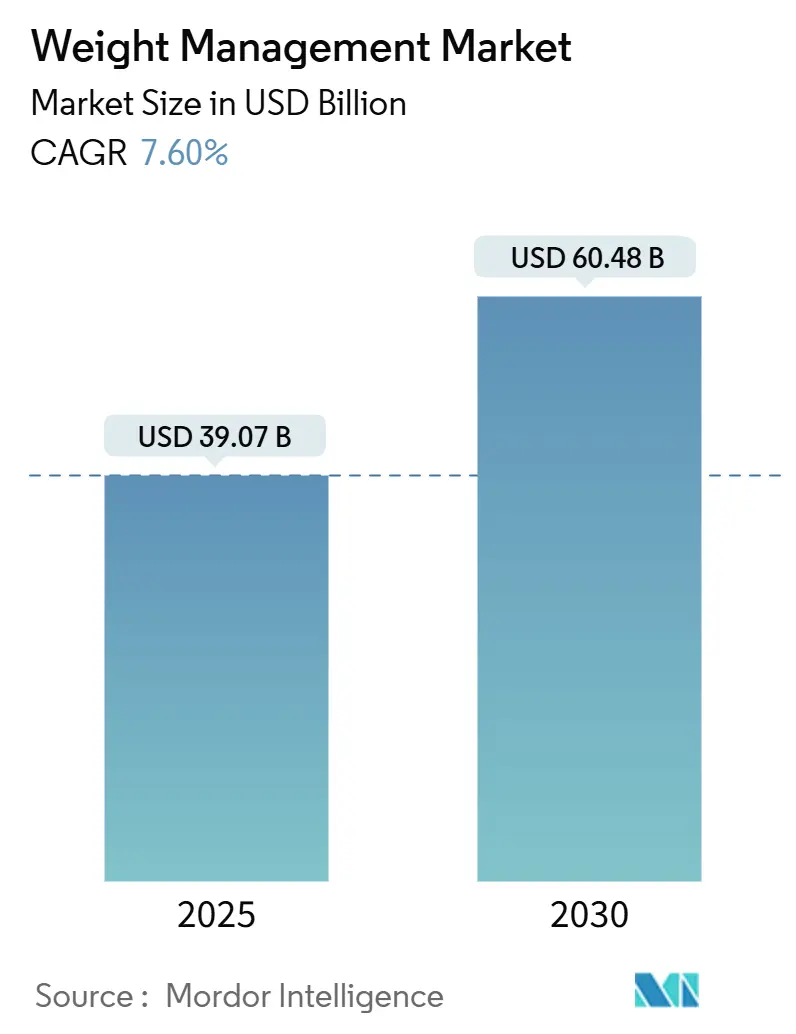

| Market Size (2025) | USD 39.07 Billion |

| Market Size (2030) | USD 60.48 Billion |

| Growth Rate (2025 - 2030) | 7.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

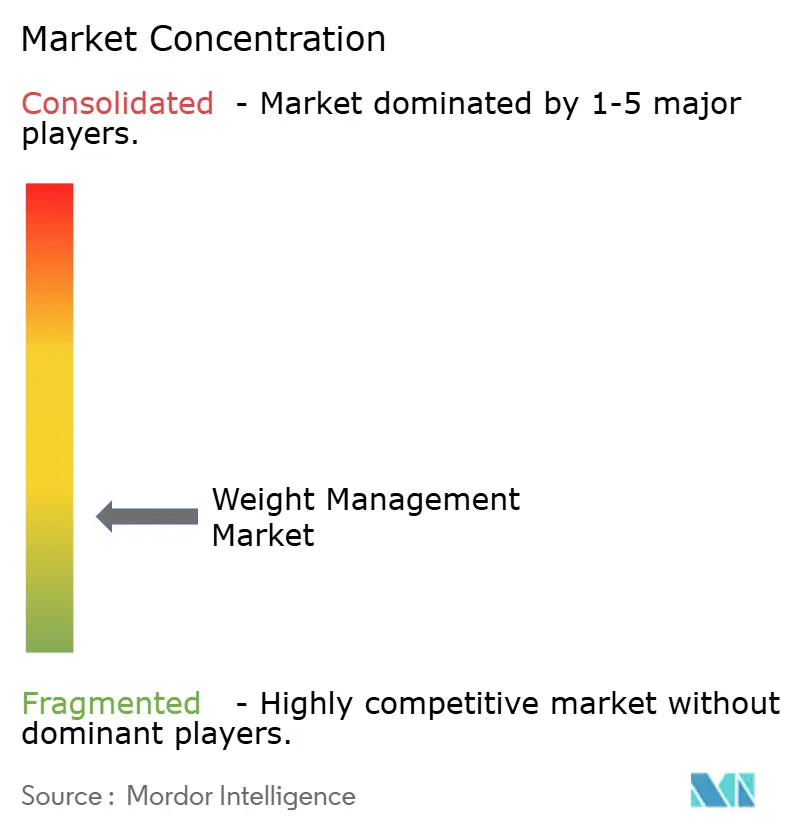

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Weight Management Market Analysis by Mordor Intelligence

The Weight Management Market size is estimated at USD 39.07 billion in 2025, and is expected to reach USD 60.48 billion by 2030, at a CAGR of 7.60% during the forecast period (2025-2030).

Robust demand is arising from a combination of rising obesity rates, greater public health awareness, and the growing availability of digital engagement tools. Innovation clusters around meal replacements, physician-directed GLP-1 therapies, and integrated coaching platforms continue to stimulate competition and new product launches. Players also rely on subscription-based models and data-driven personalization to improve retention, while retail pharmacies and e-commerce channels widen consumer access. Partnerships with employers and payers remain a pivotal lever for volume expansion and reimbursement coverage, especially in the United States. Ongoing product premiumization, however, is prompting consumers in price-sensitive economies to seek lower-cost substitutes or community-based programs.

Key Report Takeaways

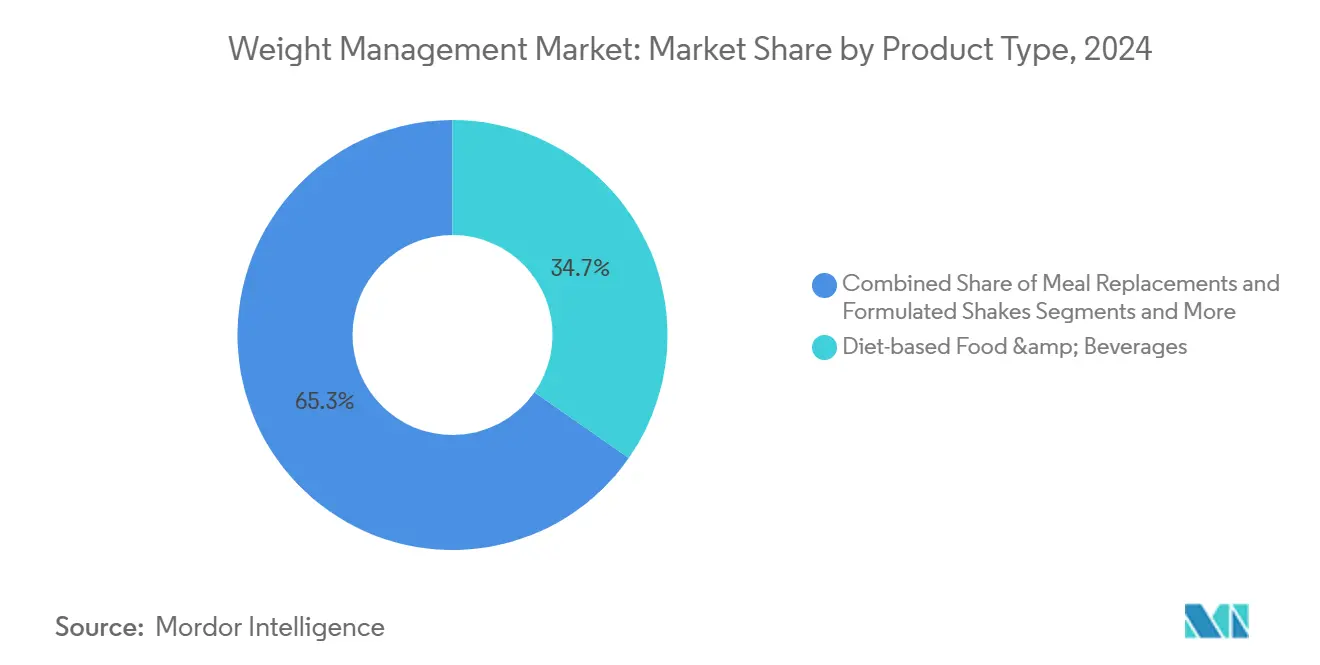

- By product type, diet-based food & beverages accounted for 34.7% of the weight management market share in 2024, while GLP-1 prescription therapies are projected to expand at a 15.2% CAGR through 2032.

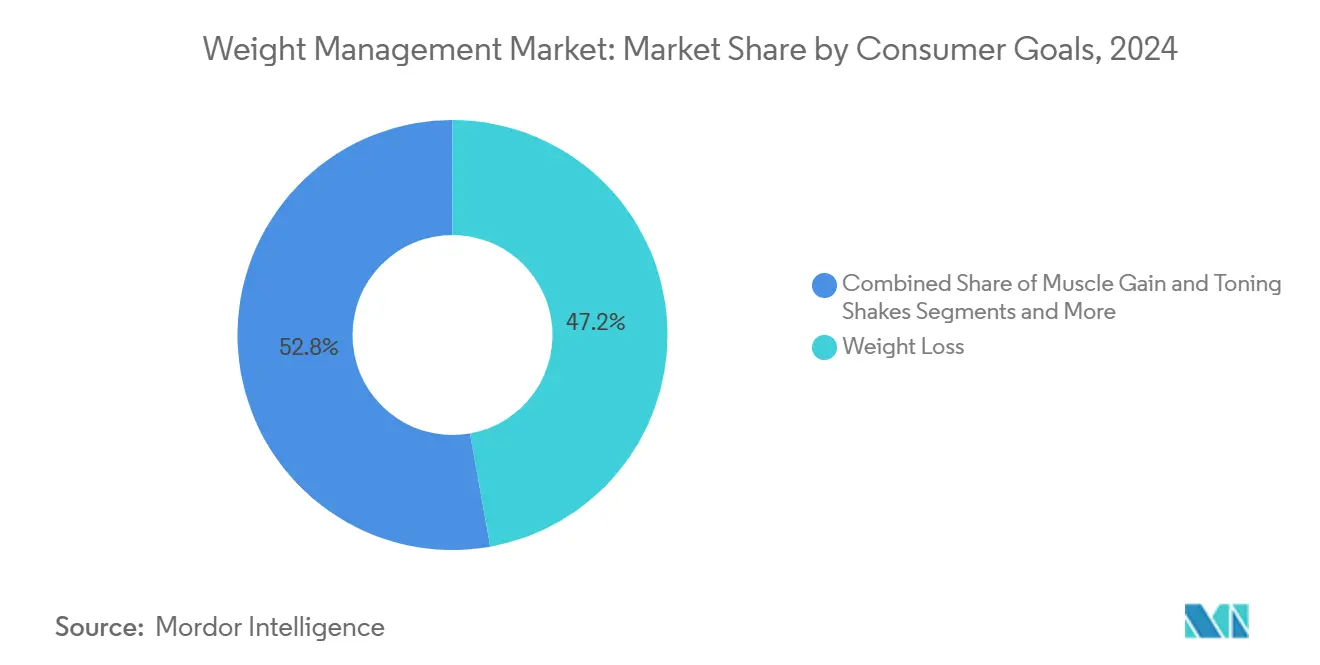

- By consumer goal, weight loss dominated with 47.2% share of the weight management market size in 2024, whereas medical obesity management is poised for a 12.7% CAGR to 2032.

- By geography, North America led with a 34.7% revenue share in 2024, and Asia Pacific is expected to post a 10.4% CAGR through 2032.

Global Weight Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of obesity & lifestyle-related disorders | +1.20% | Global | Long term (≥ 4 years) |

| Increasing disposable incomes & health awareness in emerging economies | +1.00% | Asia Pacific, South America | Medium term (2-4 years) |

| Rapid uptake of GLP-1 weight-loss drugs | +0.80% | North America, Europe | Short term (≤ 2 years) |

| Employer-funded corporate wellness benefits | +0.60% | North America, Europe | Medium term (2-4 years) |

| AI-driven personalized nutrition & coaching platforms | +0.50% | Global | Long term (≥ 4 years) |

| Integration of telehealth with weight-management programs | +0.40% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity & Lifestyle-Related Disorders

Escalating obesity rates in both developed and developing nations continue to underpin the steady expansion of the weight management market. The World Health Organization reports that over 1 billion adults now live with obesity.[1]World Health Organization, “Fact Sheet: Obesity and Overweight,” who.int Elevated body-mass indices have prompted policymakers to declare obesity a public-health emergency, spurring reimbursement for medically supervised interventions and strengthening demand fundamentals in the weight management market. Multinational food manufacturers are reformulating products with reduced calories and cleaner labels, amplifying the appeal of portion-controlled meal replacements. These dynamics collectively propel new users toward subscription plans, connected wearables, and clinical coaching. Consequently, product portfolios that blend nutrition, exercise, and behavioral support are capturing recurring revenue streams while positioning vendors for sustained growth.

Increasing Disposable Incomes & Health Awareness in Emerging Economies

Rising median household earnings across the Asia Pacific and parts of South America are enabling larger discretionary budgets for dietary supplements, smart fitness devices, and premium weight-control foods, reinforcing expansion of the weight management market. Government-sponsored wellness campaigns, such as India’s Fit India Movement and China’s Healthy China 2030 initiative, have expanded the addressable consumer base through mass screenings and public-private partnerships.[2]Ministry of Health & Family Welfare, “Fit India Movement Dashboard,” gov.in Retail pharmacies and convenience stores increasingly dedicate shelf space to portion-controlled snacks and protein shakes, improving last-mile access outside metropolitan hubs. At the same time, cross-border e-commerce platforms allow regional shoppers to purchase international brands at competitive prices. These factors work together to reinforce positive perceptions of evidence-based programs and accelerate revenue growth for global and local operators.

Rapid Uptake of GLP-1 Weight-Loss Drugs

Physician-prescribed GLP-1 receptor agonists such as semaglutide are reshaping the competitive contours of the weight management market. Clinical trials have demonstrated average body-weight reductions of 15%–20%, outperforming legacy pharmacotherapies.[3]Food and Drug Administration, “Warning Letters on Dietary Supplements,” fda.gov Accelerated approvals in the United States, the European Union, and Japan have opened reimbursement channels, spurring double-digit quarterly sales for leading manufacturers. Program providers are bundling these therapeutics with digital-first coaching to capture incremental margin and augment retention. Retail chain pharmacies are integrating nurse-led injection training, further lowering adoption barriers. Although supply constraints persist, expanding production capacity and local licensing agreements are expected to scale volumes over the next two years, supporting continued momentum in the weight management market.

Employer-Funded Corporate Wellness & Weight-Loss Benefits

Employers in high-income regions view obesity as a cost driver for absenteeism and chronic disease expenditure, prompting wider adoption of subsidized weight-control programs. United States data indicate that organizations offering structured benefits experience 18% lower annual healthcare costs per employee. Vendors leverage outcomes-based pricing and biometric monitoring to meet return-on-investment thresholds, while health insurers provide premium discounts to participating firms. As hybrid work models settle, employers allocate additional capital to app-based coaching, meal-planning stipends, and connected exercise equipment. Together, these measures create a predictable source of business-to-business revenue and reinforce brand credibility among individual consumers in the weight management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse effects & safety concerns of supplements/drugs | -0.80% | Global | Short term (≤ 2 years) |

| High program & product costs in low-income groups | -0.60% | Middle East & Africa, South America | Long term (≥ 4 years) |

| Regulatory scrutiny on digital therapeutics & health claims | -0.50% | North America, Europe | Medium term (2-4 years) |

| Social-media backlash eroding trust in “fad” diets | -0.40% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adverse Effects & Safety Concerns of Supplements / Drugs

Reports of hepatotoxicity linked to unregulated herbal blends and gastrointestinal side effects from GLP-1 drugs have generated caution among both consumers and prescribers across the weight management market. Several national agencies, including the U.S. Food and Drug Administration, have issued warning letters and product recalls in 2024. Media coverage emphasizing isolated adverse events can erode brand equity, particularly for smaller direct-to-consumer labels that lack extensive clinical validation. Heightened vigilance has led retailers to tighten quality-control requirements, increasing compliance costs and slowing launch timelines. As scientific consensus evolves, manufacturers must invest in transparent labeling and post-marketing surveillance to mitigate reputational risk.

High Program & Product Costs Limit Adoption in Low-Income Groups

Subscription fees for premium coaching apps, continuous glucose monitors, and prescription injectables can exceed USD 250 per month, placing them beyond the reach of many middle-income households. Government subsidies remain scarce outside high-income nations, prompting NGOs to promote community-based exercise initiatives as cost-effective alternatives. The result is a two-tier market in which high-end offerings thrive in urban centers, while lower-margin commoditized products serve rural consumers. Vendors that fail to develop tiered pricing or micro-insurance models may miss out on untapped populations, moderating aggregate growth in the weight management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diet-based foods hold the lead, GLP-1 therapies gain traction

Diet-based food & beverages generated 34.7% of the weight management market size in 2024 on account of strong demand for portion-controlled snacks, low-carbohydrate meal kits, and protein-fortified drinks. The segment benefits from mature distribution through supermarkets, mass merchandisers, and online grocery portals that allow seamless repeat purchasing. Continued reformulation to lower added sugars and incorporate functional fibers enhances health credentials and shelf appeal. Brand portfolios frequently bundle loyalty apps that track nutrient intake and suggest companion supplements, thereby driving higher basket values. GLP-1 prescription therapies, while accounting for a smaller revenue base, are projected to record a 15.2% CAGR, reflecting rapid prescriber adoption and improving reimbursement. Manufacturers focus on long-acting formulations and auto-injector devices to improve adherence and reduce clinic visits. Strategic alliances between pharmaceutical firms and digital coaching platforms create integrated care pathways, capturing cross-channel synergies in the weight management market.

Premium meal replacements, historically centered on powders and ready-to-drink shakes, now feature plant-based proteins and clean-label ingredients to match evolving consumer preferences. The shift aligns with broader sustainability narratives, attracting eco-conscious millennials. Fitness equipment and wearables remain critical in supporting exercise adherence, yet face price pressure from low-cost Asian imports and maturing demand in early-adopter markets. Weight-management services, including group workshops and app-based programs, have integrated behavioral-therapy modules to differentiate themselves amid commoditization. Vendors that embed AI-enabled progress tracking and community support tend to retain subscribers longer, translating into predictable cash flows. Overall, diversified portfolios that blend consumables, connected devices, and coaching continue to reinforce customer lifetime value across the weight management market.

By Consumer Goal: Weight-loss dominates, medical management accelerates

Weight-loss objectives commanded 47.2% of the weight management market share in 2024, driven by enduring aesthetic motivations, broad cultural acceptance and employer-sponsored initiatives. Commercial programs deploy tiered subscription plans that tailor calorie targets and activity levels to individual profiles, resulting in strong engagement metrics. Weight-maintenance solutions cater to graduates of initial programs by introducing flexible meal-plans that prevent relapse, thus lengthening the customer journey. Muscle-gain and toning goals appeal to fitness enthusiasts and younger demographics; brands leverage influencer marketing and gym partnerships to stimulate trial purchases. Bariatric pre/post-surgery support remains niche but benefits from multidisciplinary hospital pathways that bundle tailored nutrition and physiotherapy packages.

Medical obesity management, projected to grow at a 12.7% CAGR, gains momentum as clinicians shift toward evidence-based interventions for patients with body-mass-index thresholds above 30. Digital therapeutics incorporate remote monitoring of vital signs and medication adherence, facilitating rapid course corrections and improved outcomes. Payers increasingly reimburse hybrid programs that combine GLP-1 pharmacotherapy, dietitian consultations, and cognitive-behavioral therapy modules. As clinical guidelines evolve toward earlier pharmacologic intervention, more participants enter structured medical programs, driving incremental revenue to pharmaceutical firms and digital-health providers. Collectively, the interplay of lifestyle and clinical solutions broadens the total addressable base for the weight management market.

Geography Analysis

North America generated 34.7% of total revenue in 2024 owing to high obesity prevalence, broad insurance coverage, and widespread consumer acceptance of subscription-based applications. United States retailers continue to expand healthy-living aisles, and major pharmacy chains offer on-site nutrition counseling that funnels traffic into digital platforms. The region also leads in employer-funded wellness benefits, which channel a sizeable share of enterprise budgets toward structured programs. Government agencies maintain rigorous regulatory oversight that bolsters consumer confidence, although it also extends development timelines for novel supplements.

Europe remains the second-largest contributor, with Western European countries adopting holistic weight-management strategies that combine behavioral therapy and digital support. Public-health systems in Germany and the United Kingdom reimburse select digital therapeutics upon demonstration of real-world evidence, creating a viable pathway for vendors operating in the weight management industry. Stringent advertising rules limit sensational claims, steering marketing toward clinically validated benefits. Southern European nations lag slightly due to lower discretionary incomes, yet tourism-driven hospitality sectors embrace healthier menu offerings, indirectly promoting low-calorie food lines within the weight management market.

Asia Pacific is forecast to register the fastest 10.4% CAGR to 2032, underpinned by urbanization, smartphone penetration, and rising middle-class aspirations. Chinese online marketplaces prominently feature calorie-controlled ready meals, while Japanese insurers offer premium discounts to policyholders who record daily step counts. India exhibits high growth potential as smartphone-based coaching apps localize content into regional languages and introduce micro-payment options. Governments across the Gulf Cooperation Council are launching national anti-obesity campaigns, boosting demand for professional services in the Middle East, though growth remains constrained by limited reimbursement frameworks.

Competitive Landscape

The competitive matrix features a blend of multinational nutrition houses, specialized pharmaceutical firms, and pure-play digital health start-ups in the weight management industry. Nestlé Health Science leverages its Optifast and Garden of Life franchises to bundle medically supervised meal plans with probiotic supplements, reinforcing its share in clinical channels. Herbalife Nutrition maintains a multi-level distribution network that sustains high-touch engagement, despite growing scrutiny surrounding product claims. WW International and Medifast’s OPTAVIA capitalize on structured coaching communities that yield sticky subscription revenues within the weight management market.

Pharmaceutical entrants accelerate market shifts. Novo Nordisk and Eli Lilly expand production capacity for semaglutide and tirzepatide, respectively, forging co-marketing pacts with platform-based providers to integrate medication management and behavior coaching. Digital innovators such as Noom and MyFitnessPal refine AI-driven analytics to deliver real-time insights and personalized nudges, enhancing user outcomes and retention. Device manufacturers, including Fitbit and Polar Electro, extend their ecosystems through open APIs, allowing seamless syncing with third-party nutrition apps.

Strategic M&A activity remains vibrant. Abbott Nutrition recently acquired a minority stake in a tele-nutrition start-up to embed continuous glucose data into customized meal plans. Omada Health partnered with a leading employer benefits administrator to scale reimbursement pathways for its diabetes-prevention modules. Glanbia acquired a plant-based protein bar maker to expand its functional snacking portfolio. As competition intensifies, firms emphasize clinical validation, diversified revenue models, and localized content to secure a durable edge across the weight management market.

Weight Management Industry Leaders

Herbalife Nutrition Ltd.

Nestlé Health Science

WW International Inc.

Medifast Inc.

Noom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Dr. Morepen launched LightLife weight management solution in India, targeting emerging market demand for affordable digital health platforms integrated with traditional wellness approaches

- May 2025: The Good Bug introduced a synbiotic solution combining probiotics and prebiotics for weight management, representing innovation in microbiome-based approaches to metabolic health.

- April 2025: WeightMate.AI launched an AI-powered weight management app with personalized meal planning and behavioral coaching features, demonstrating continued innovation in digital health platforms.

Global Weight Management Market Report Scope

| Meal Replacements & Formulated Shakes |

| Diet-based Food & Beverages |

| Weight-loss Supplements |

| Fitness Equipment & Wearables |

| Weight-management Services & Programs |

| Weight Loss |

| Weight Maintenance |

| Muscle Gain & Toning |

| Medical Obesity Management |

| Bariatric Pre/Post-Surgery Support |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Meal Replacements & Formulated Shakes | |

| Diet-based Food & Beverages | ||

| Weight-loss Supplements | ||

| Fitness Equipment & Wearables | ||

| Weight-management Services & Programs | ||

| By Consumer Goal | Weight Loss | |

| Weight Maintenance | ||

| Muscle Gain & Toning | ||

| Medical Obesity Management | ||

| Bariatric Pre/Post-Surgery Support | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will the weight management market grow through 2032?

It is projected to advance at an 8.3% CAGR, reaching USD 397.4 billion by 2032.

Which product category currently leads revenue generation?

Diet-based food & beverages account for 34.7% of the global total.

What is driving the surge in GLP-1 prescriptions?

Clinically proven 15%-20% body-weight reductions and expanding reimbursement are accelerating adoption.

Why is Asia Pacific the fastest-growing region?

Rising disposable incomes, smartphone penetration, and national wellness campaigns support a 10.4% CAGR.

How are employers influencing market demand?

Subsidized wellness benefits and outcomes-based contracts channel corporate spending into structured programs.

Which restraint poses the most immediate challenge?

Safety concerns tied to supplements and new drugs prompt heightened regulatory scrutiny and cautious consumer adoption.

Page last updated on: