Molecular Weight Marker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

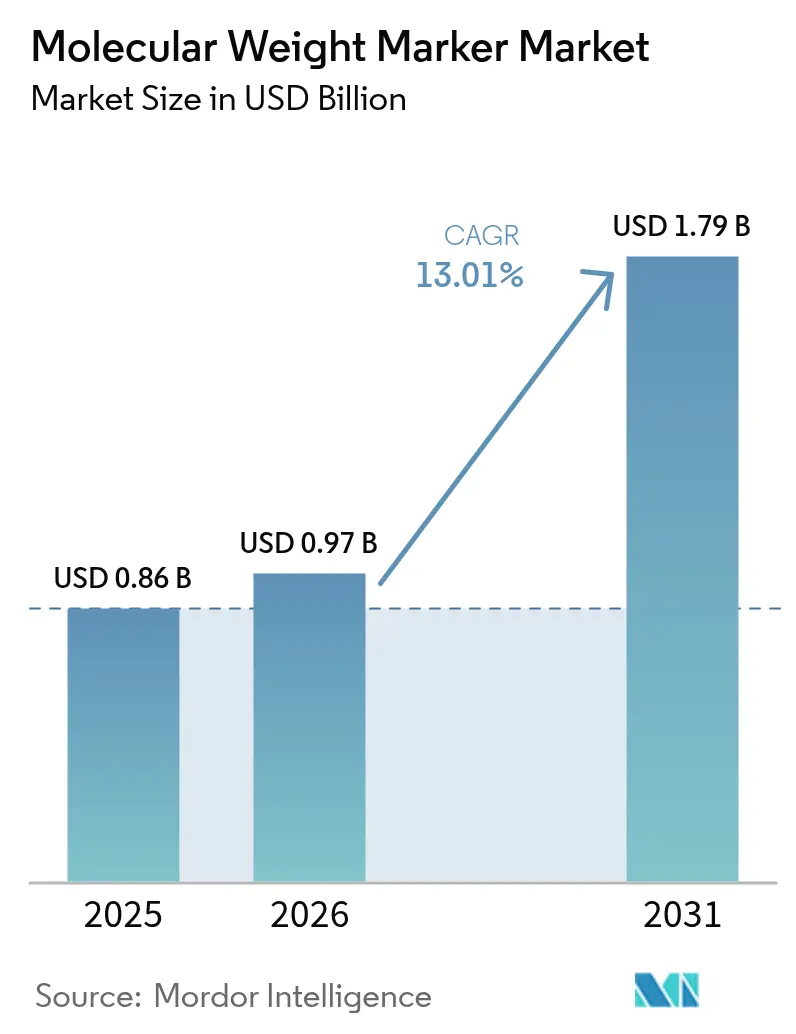

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 13.01% CAGR |

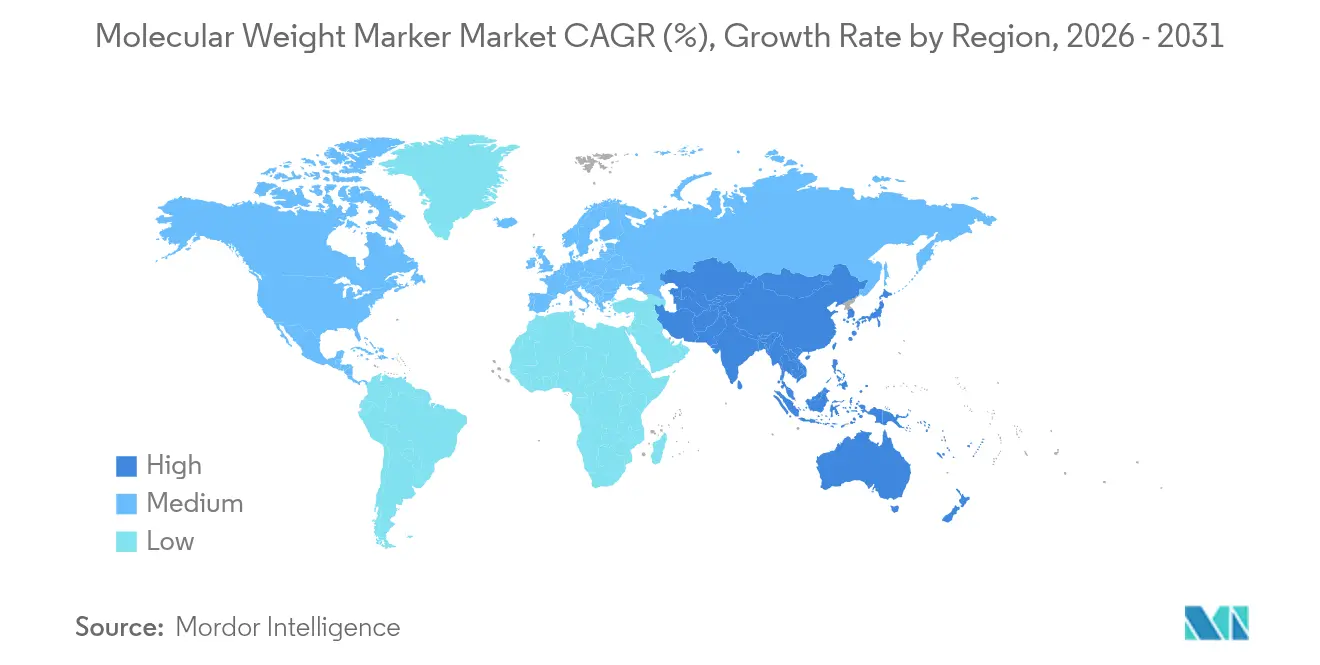

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

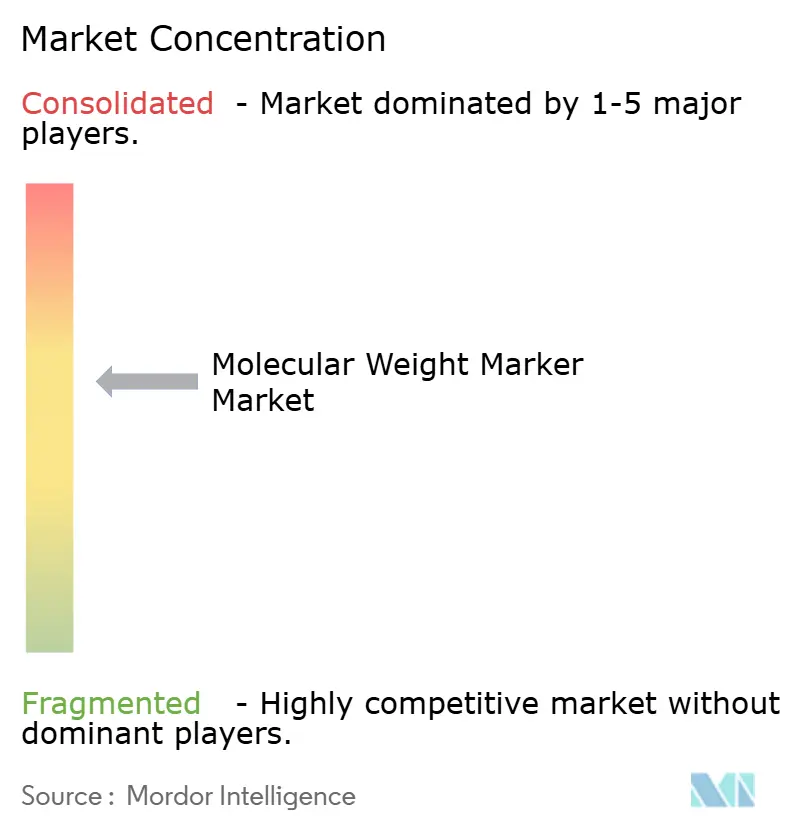

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Molecular Weight Marker Market Analysis by Mordor Intelligence

The global molecular weight markers market size in 2026 is estimated at USD 0.97 billion, growing from 2025 value of USD 0.86 billion with 2031 projections showing USD 1.79 billion, growing at 13.01% CAGR over 2026-2031. This rapid advance reflects the convergence of genomics R&D funding, expanding molecular diagnostics volumes and stringent cell- and gene-therapy quality‐control protocols that elevate demand for highly standardized ladders. AI-ready blot-imaging platforms are reshaping laboratory preferences toward fluorescent protein and DNA ladders that deliver consistent, machine-readable signals. The North American innovation ecosystem anchors early adoption, yet ambitious population-scale genomics programs in Asia-Pacific generate the largest incremental volume gains. Vendors are responding with vertically integrated offerings that bundle traditional electrophoresis consumables with automation, informatics and ready-to-use chemistries to mitigate skilled-labor shortages and regulatory complexity. These competitive moves position the molecular weight markers market at the center of emerging multi-omics workflows, creating new revenue pools as point-of-care (POC) diagnostics, microfluidic devices and continuous bioprocessing migrate from proof-of-concept to commercial deployment.

Key Report Takeaways

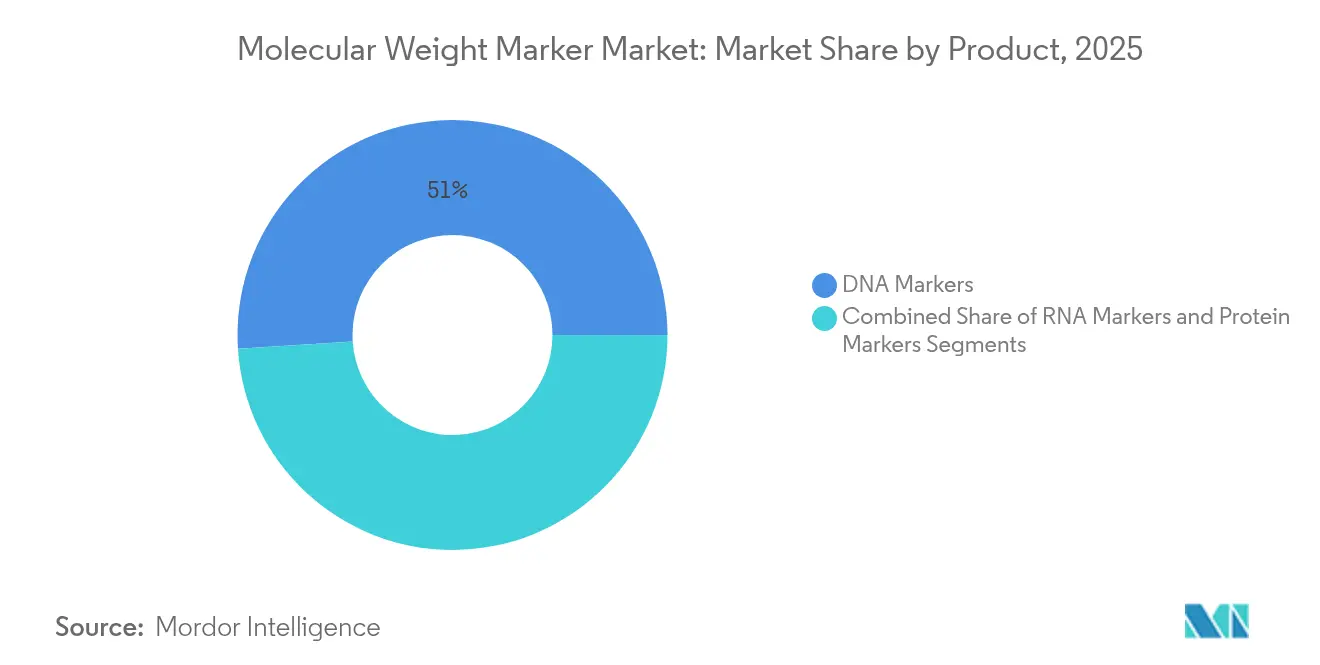

- By product, DNA markers held 51.02% of the molecular weight markers market share in 2025 while RNA markers are projected to expand at a 14.02% CAGR to 2031.

- By application, nucleic-acid assays accounted for 60.10% of the molecular weight markers market size in 2025; proteomics applications are advancing at a 14.52% CAGR through 2031.

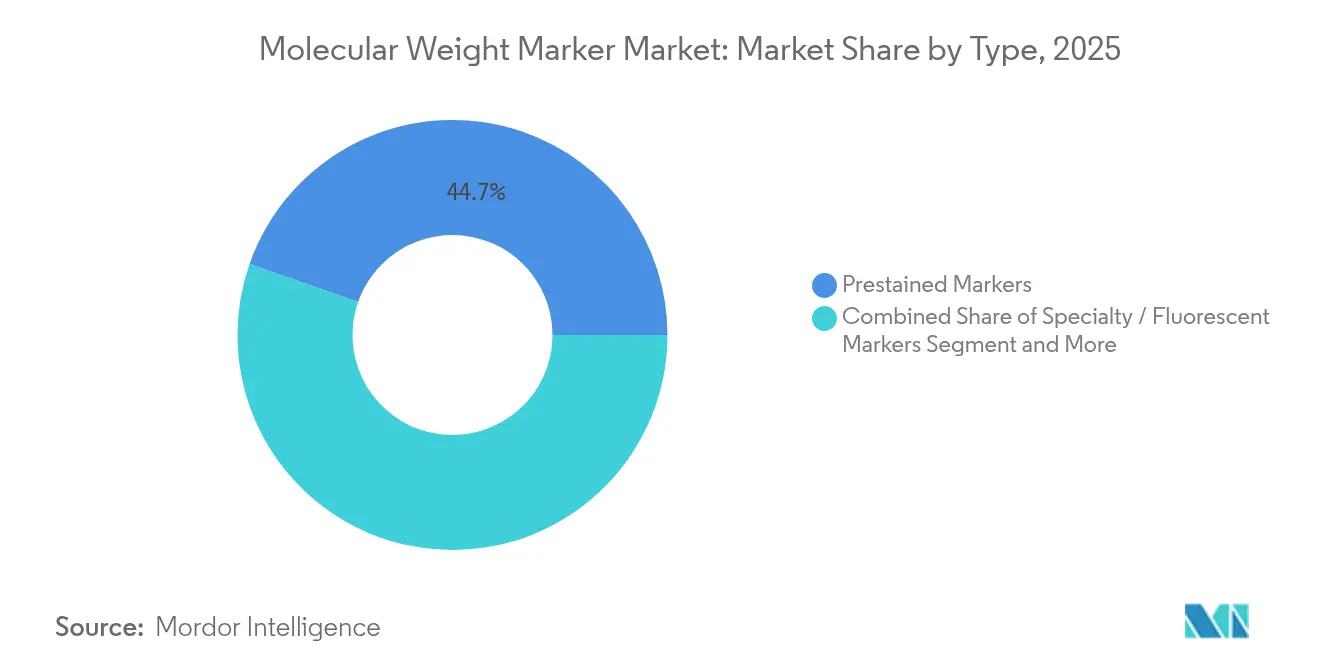

- By type, prestained ladders dominated with a 44.65% revenue share in 2025, whereas specialty fluorescent ladders are forecast to grow at 13.86% CAGR over the same horizon.

- By end-user, pharmaceutical and biotechnology companies captured 34.78% revenue share in 2025; clinical and diagnostic laboratories record the highest projected CAGR at 15.2% to 2031.

- By geography, North America led with 37.95% share of the molecular weight markers market in 2025, and Asia-Pacific posts the fastest-growing regional CAGR at 14.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Molecular Weight Marker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global R&D expenditure in genomics & proteomics | +3.2% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Expanding molecular diagnostics volumes (PCR/NGS) | +2.8% | North America, Europe | Medium term (2-4 years) |

| Wider availability of ready-to-use prestained ladders | +1.9% | Global | Short term (≤ 2 years) |

| Cell- & gene-therapy QC protocols requiring high-accuracy DNA ladders | +2.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Mini-gel platforms in POC devices increasing low-range marker demand | +1.6% | Developed markets first | Short term (≤ 2 years) |

| AI-driven blot-imaging software pushing need for fluorescent protein ladders | +1.4% | North America, Europe expanding worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global R&D Expenditure in Genomics & Proteomics

Government-funded genomics programs are scaling sequencing output and standardizing analytical workflows. Japan plans to profile 100,000 cancer genomes within five years, requiring consistent molecular weight markers to harmonize data across institutions[1]Yuki Katsuya, “Current and Future Trends in Whole Genome Sequencing in Cancer,” cancerbiomed.org. India’s 10,000-genome initiative employs the CARE ethical framework, favoring high-accuracy DNA ladders compatible with community oversight. The US National Nanotechnology Initiative earmarked USD 2.16 billion in 2024, part of which underwrites biotech tools such as molecular weight standards for nano-enabled drug design. AI-centric research budgets further amplify demand because machine-learning pipelines require uniform input quality to train reliable biomarker-discovery models.

Expanding Molecular Diagnostics Volumes (PCR/NGS)

POC and decentralized laboratories are increasing throughput and shortening turnaround times. A PCB-based real-time PCR chip heats at 8°C/s with ±0.1°C accuracy, enabling single-use assays that depend on low-range molecular weight ladders tailored to rapid runs. The Dragonfly LAMP-LAMP platform attains 96.1% viral-detection sensitivity in portable form factors, triggering demand for prestained ladders that remain stable in field conditions. High-throughput NGS workflows, such as the myeloMATCH trial, require robust DNA ladders to confirm library integrity ahead of same-day reporting. Microfluidic “lab-on-a-chip” systems finish nucleic-acid analysis within 28 minutes at USD 9.5 per test, pushing suppliers to package markers in single-use cartridges that align with cost-sensitive diagnostic economics.

Wider Availability of Ready-to-Use Prestained Ladders

Laboratories coping with staffing gaps adopt ready-to-use consumables that cut preparation steps. Vendors now offer color-coded multichannel formats, integrating loading dye and density reagents to shrink run times by 12–15%. Shelf-life optimizations through glycerol-free formulations allow ambient shipping, a feature essential for emerging-market labs lacking cold-chain logistics. Educational institutions lean on these ladders to streamline teaching labs, introducing early-career scientists to standardized molecular weight markers market workflows without elaborate preparation.

Cell & Gene-Therapy QC Protocols Require High-Accuracy DNA Ladders

Regulators mandate precise host-cell DNA quantification for viral-vector and mRNA products. The FDA notes that human-cell residual DNA carries elevated oncogenic risk, enforcing strict variant-size acceptance limits that only high-resolution DNA ladders satisfy. CRISPR-Cas9 edits often insert concatemeric sequences that are detectable only when ladders cover large size ranges with minimal migration variance. Continuous bioprocessing initiatives integrate online electrophoresis to approve batches in real time, pressuring marker vendors to design products compatible with automated sampling interfaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled electrophoresis technicians | −1.8% | North America, Europe | Short term (≤ 2 years) |

| Stringent reagent-grade regulatory certifications (IVDR, USP) | −1.4% | Europe, Global | Medium term (2-4 years) |

| Batch variability triggers reproducibility audits in pharma QA | −1.1% | Global pharma hubs | Medium term (2-4 years) |

| Shift toward microfluidic & capillary-electrophoresis systems | −0.9% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Electrophoresis Technicians

US molecular labs reported 13.4% unfilled positions in 2024, slowing test throughput and prompting automation investments. Recruitment challenges raise labor costs, so managers prefer single-tube, prestained ladders that cut prep steps. Academic collaborations are emerging to expand certification programs, but pipelines will take several years to stabilize. In Europe, retirement waves compound deficits, especially in rural hospitals where travel distances deter potential hires.

Stringent Reagent-Grade Regulatory Certifications (IVDR, USP)

The European IVDR demands extensive clinical evidence for in-vitro reagents, lengthening dossier timelines. In parallel, the US FDA tightened impurity testing for high-risk excipients, requiring batch-specific certificates for diethylene glycol and ethylene glycol[2]Mopa Esuga, “Ensuring Product Safety: FDA Guidance,” qualitymatters.usp.org. Vendors must validate new analytical methods while managing dual auditing cycles, a burden particularly acute for small and medium enterprises active in the molecular weight markers industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: RNA Markers Drive Innovation Wave

RNA markers are registering the fastest 14.02% CAGR to 2031 as mRNA vaccine pipelines mature and next-generation sequencing (NGS) protocols become ubiquitous. Accurate poly(A) tail and capping-efficiency verification relies on well-defined ladders that cover a broad 100–10,000 nt range, elevating adoption among therapeutic developers. DNA markers retained 51.02% molecular weight markers market share in 2025 due to entrenched PCR, cloning and Southern-blot routines. However, demand is shifting toward high-molecular-weight formats that resolve CRISPR-induced genomic alterations in synthetic biology programs. Protein markers benefit from rising proteomics funding, exemplified by Thermo Fisher’s Olink acquisition, which added 5,300 biomarkers to high-throughput screening pipelines and invigorated need for calibrated protein ladders.

Commercial laboratories value prestained protein ladders that remain visible without staining, saving 30 minutes per run and improving lab productivity when technician bandwidth is scarce. Academic groups exploring structural proteomics increasingly adopt fluorescent dual-channel ladders to align with multiplex imaging systems. Meanwhile, RNA researchers prioritize nuclease-free packaging to maintain ladder integrity, prompting suppliers to shift toward foil-wrapped, single-use vials that eliminate freeze-thaw degradation.

By Application: Proteomics Surges Past Traditional Boundaries

Proteomics applications are advancing at 14.52% CAGR, narrowing the historical dominance of nucleic-acid workflows. Western blotting remains the primary use case, yet emerging disciplines such as top-down proteomics, ribosome profiling and thermal-shift assays now employ ladders for size confirmation in complex matrices. Automated gel extraction robots integrated with AI analysis cut sample-band excision time by 40%, driving greater ladder consumption per experiment. Nucleic-acid assays maintain a 60.10% share of the molecular weight markers market size, upheld by pandemic-era PCR capacity that persists for respiratory-virus surveillance.

In POC environments, 15-minute laser-heated PCR cycles require snap-cooling ladders that migrate predictably under rapid thermal transitions. Southern and Northern blotting remain relevant in epigenetics and long-read validation studies, respectively, but sequence-direct detection continues to pull some volume away. Researchers therefore prefer universal ladders covering overlapping size ranges for both nucleic-acid and protein analyses to streamline inventory.

By Type: Specialty Markers Capitalize on Technology Convergence

Prestained ladders held 44.65% revenue share in 2025 because they eliminate post-run staining, a key advantage in high-throughput labs. Specialty fluorescent ladders are growing by 13.86% CAGR as AI-enabled imaging gains traction. Dual-dye formulations allow simultaneous DNA and protein visualization, facilitating combined transcriptomics-proteomics assays within a single gel. Unstained ladders cater to workflows directing gel slices to downstream mass spectrometry, where prestaining chemicals would interfere with ionization efficiency.

Photostable fluorescent markers minimize photobleaching during repeated imaging cycles, crucial for time-course studies spanning several hours. Colorimetric prestaining remains popular in teaching labs where immediate visual confirmation matters more than quantitative precision. Manufacturers are experimenting with lyophilized pellets that rehydrate in sample buffer, extending shelf life to three years without refrigeration—a feature aligned with field diagnostics and low-resource settings.

By End-User: Clinical Labs Accelerate Diagnostic Integration

Clinical and diagnostic laboratories are projected to grow at 15.2% CAGR through 2031 as decentralized testing expands and reimbursement codes cover rapid molecular panels. POC instruments with built-in micro-gels are adopted by urgent-care clinics and mobile health units, increasing ladder demand in ready-made cartridge form. Pharmaceutical and biotechnology firms retained 34.78% market share in 2025 due to active gene-therapy pipelines that mandate rigorous QC, including residual host-cell DNA analysis.

Academic institutes drive fundamental discoveries and often test experimental ladder formats, serving as proving grounds for new formulations before commercial rollout. Contract research organizations (CROs) maintain varied ladder inventories to accommodate client protocols, representing a stable if fragmented demand base. Workforce shortages push all end-users toward automation-friendly consumables, elevating interest in bar-coded vials that integrate with laboratory information systems for traceability.

Geography Analysis

North America controlled 37.95% of the molecular weight markers market in 2025, supported by a mature biotech ecosystem, sustained federal R&D allocations and early adoption of AI-driven laboratory automation. The USD 2.16 billion 2024 National Nanotechnology Initiative budget underwrites molecular analysis tools, including size standards for nanoformulation research. M&A activity, exemplified by Thermo Fisher’s USD 3.1 billion Olink integration, consolidates consumables portfolios and funnels resources into high-throughput proteomics. Yet a 13.4% vacancy rate in molecular diagnostics laboratories compels facilities to adopt turnkey ladders that minimize manual intervention. FDA guidance on batch uniformity further escalates quality expectations, favoring suppliers with validated, lot-stable products.

Asia-Pacific is the fastest-expanding region at 14.3% CAGR through 2031, underpinned by government-sponsored population genomics and the rise of indigenous vaccine manufacturing. Japan’s 100,000-genome program and India’s CARE-guided 10,000-genome initiative call for cross-lab standardization, boosting demand for high-precision DNA ladders. China’s lung-cancer profiling work integrates germline-somatic mutation data, broadening applications for dual-size DNA and RNA ladders. Regional manufacturers focus on cost-optimized POC platforms, stimulating a parallel requirement for compact, lyophilized markers that withstand transit in humid climates.

Europe follows steady growth, benefiting from collaborative research networks and an emphasis on sustainability. IVDR implementation harmonizes quality standards, rewarding companies with robust documentation structures. AI-assisted gel analysis projects from leading universities amplify demand for fluorescent ladders compatible with automated imaging pipelines. Environmental directives prompt suppliers to reduce hazardous dyes and shift toward plant-derived pigments in prestained products, aligning with EU Green Deal objectives.

Regulatory Landscape

Regulatory treatment of molecular weight markers varies by intended use: many products are supplied as research-use-only analytical reagents, while markers packaged or claimed for clinical testing can fall under in vitro diagnostic (IVD) requirements, including the EU IVD Regulation (Regulation (EU) 2017/746, IVDR). The EU borderline and classification framework (European Commission Manual on borderline and classification for medical devices, updated April 2026) and MDCG IVD classification guidance reinforce a case-by-case approach, which increases the documentation burden when markers are used inside regulated diagnostic workflows.

For biopharma quality control and method validation, regulators and standards bodies focus on traceability and method performance rather than the marker alone. In practice, this cascades into supplier expectations for robust Certificates of Analysis (identity, purity, stability, lot numbers, and retest/expiry) and well-characterized in-house reference materials when no compendial or international standard exists. These expectations align with widely used guidance for analytical procedures and bioanalytical method validation (including ICH M10, issued as FDA guidance in 2025) and quality frameworks applied in GMP environments (for example, 21 CFR Part 211), supporting demand for lot-consistent, audit-ready ladder formats in regulated labs and manufacturing QC.

Competitive Landscape

The molecular weight markers market demonstrates moderate consolidation as global suppliers pursue acquisitions to broaden multi-omics portfolios. Thermo Fisher strengthened its proteomics position through the USD 3.1 billion Olink uptake, integrating >5,300 validated protein biomarkers with existing ladder lines. Agilent augmented oligonucleotide and CRISPR services by acquiring BIOVECTRA for USD 925 million, signaling intent to co-develop size standards tuned to gene-editing workflows. QIAGEN’s plan to launch three sample-preparation instruments demonstrates strategic alignment between automation and consumable sales; the QIAsymphony Connect platform processes up to 96 samples, creating a pull-through effect for bar-coded ladder cartridges.

Emergent competitors focus on specialty fluorescent ladders optimized for AI analytics, carving out high-margin niches despite lower absolute volumes. Contract manufacturers in South Korea and Singapore ramp up OEM production, offering private-label prestained ladders with ISO 13485 certification to Western brands seeking cost advantages. Demand-planning data suggest top five vendors command about 55% of global revenues, leaving room for regional specialists targeting clinical labs and academic customers with tailored formulations.

Innovation pipelines emphasize lyophilized, single-dose ladders that reconstitute instantly, addressing cold-chain gaps in sub-Saharan Africa and Southeast Asia. Vendors also explore biodegradable gel capsules to reduce plastic waste, collaborating with academic partners to validate performance parity. White-space opportunities persist in capillary electrophoresis standards, where high-conductivity fluorescent dyes can improve detector sensitivity, especially for peptide mapping.

Molecular Weight Marker Industry Leaders

Promega Corporation

Merck KGaA (MilliporeSigma)

Thermo Fisher Scientific Inc.

QIAGEN N.V.

Bio-Rad Laboratories Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace involves bridging the gap between RUO ladders and documentation-heavy requirements in regulated environments, especially where customers need traceable reference materials and clearly defined performance across specified molecular weight ranges. Standards and guidance used in biopharmaceutical testing, including USP chapters for electrophoresis-based characterization and WHO biological reference standard recommendations, reinforce the need for well-defined sizing references. This creates room for suppliers that pair markers with stronger traceability packages (lot genealogy, stability protocols, and method-fit documentation) and design products for common QC assays, rather than generic gel-only use.

Technology and cost structure also support opportunities in recombinant and synthetic marker production that improve lot-to-lot consistency compared with natural-source preparations, which can reduce friction in reproducibility audits within pharma QA. For customers facing budget constraints or procurement friction, open or academic-developed ladder systems and low-cost production approaches can shift price tiers in research markets. Calibration-grade references such as NIST SRM 2390 point to demand for forensic-traceable benchmarks, supporting portfolio development of markers and companion controls positioned for standardization-driven workflows (for example, forensic sequencing, biomarker verification, and multi-omics pipelines) while maintaining clear labeling boundaries between RUO and diagnostic claims.

Recent Industry Developments

- June 2026: Thermo Fisher Scientific introduced next-generation mass spectrometry innovations at ASMS 2026 aimed at accelerating workflows from drug discovery to development. The upgrades reinforce the surrounding ecosystem of analytical validation and QC activities where calibrated reference materials, including molecular weight standards, are routinely consumed alongside instruments and software.

- April 2026: MilliporeSigma (Merck KGaA) completed the acquisition of JSR Life Sciences chromatography business to expand its downstream Protein A capabilities and broaden its purification portfolio. The acquisition deepens Merck's end-to-end bioprocessing offering and increases pull-through for adjacent analytical and QC consumables used in biotherapeutic characterization workflows.

- March 2025: Nature Communications reported 96.1% sensitivity for the Dragonfly portable diagnostic platform using lyophilized LAMP assays, reinforcing momentum for field-ready molecular workflows. As portable and decentralized testing expands, this supports demand for robust, ready-to-use nucleic-acid sizing references that tolerate simplified storage and handling conditions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the molecular weight markers market covers ready-to-use standards and ladders used to estimate the size of DNA, RNA, and proteins during electrophoresis and related lab workflows, across research and routine testing settings.

Scope exclusions: We exclude electrophoresis instruments and imaging systems, general staining dyes, and other consumables that are not sold as molecular weight marker products.

Segmentation Overview

- By Product

- DNA Markers

- Protein Markers

- RNA Markers

- By Application

- Nucleic-Acid Applications

- PCR

- Northern Blotting

- Southern Blotting

- Molecular Cloning

- Other Nucleic-Acid Apps

- Proteomics Applications

- Western Blotting

- Gel Extraction

- Other Proteomics Apps

- Nucleic-Acid Applications

- By Type

- Prestained Markers

- Unstained Markers

- Specialty / Fluorescent Markers

- By End User

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

- Clinical & Diagnostic Laboratories

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and build a clean demand story before we started modeling. We referenced public science and health sources such as the National Institutes of Health, the US FDA, the Centers for Disease Control and Prevention, and the World Health Organization to understand how molecular testing and proteomics activity is moving over time.

To ground volumes and pricing logic, we also reviewed sources such as UN Comtrade for trade signals, peer-reviewed journals for assay and electrophoresis usage patterns, and association and conference publications that describe laboratory practices. Company filings, investor presentations, and credible press releases helped us track product launches and portfolio shifts, including prestained versus unstained formats. In addition, we used paid subscriptions for company financials and patent search to cross-check supplier scale and innovation intensity. The sources listed above are illustrative only, and we reviewed additional public references during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with lab decision makers and channel participants who regularly buy and use ladders and standards, including research institutes, pharmaceutical and biotech teams, clinical laboratories, and distributor side functions. We also spoke with product and application specialists to confirm how marker types are selected by gel type and workflow, and then we used these inputs to close gaps found in desk research and to settle practical price and mix assumptions across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 16% | APAC: 41% |

| Mid tier: 51% | Functional/Unit leaders: 25% | EMEA: 35% |

| Smaller Players: 21% | Managers: 59% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that links molecular weight marker consumption to electrophoresis run activity and the installed lab base, which is then filtered by marker usage rates per workflow. We used this structure because marker demand is tightly connected to how often gels are run and how labs standardize nucleic acid and protein work.

Key inputs used to shape the model included research funding direction, molecular biology and proteomics workflow adoption, share of labs running routine gel electrophoresis, typical pack sizes and replacement frequency, and observed price ranges by type (prestained, unstained, and specialty). A practical check was added by building selective bottom-up approximations, such as sampled ASP times implied unit demand for common ladder formats, followed by channel checks to correct for undercounted small purchases. When country-level data was thin, gaps were handled by proxying from similar lab intensity markets and then rebalancing using expert feedback on mix and affordability.

For forecasting, we relied on scenario analysis supported by short trend lines for the main drivers, and then we aligned assumptions to what interviewees expected for lab throughput, research spending, and adoption of advanced workflows. After the final clause is pulled together, the forecast remains explainable, since each driver is tied back to a measurable lab activity signal.

Data Validation & Update Cycle

Validation was done through multiple checks so that any single data series did not overly drive the outcome. We compared modeled revenues against independent signals like growth in molecular biology reagent demand, electrophoresis usage commentary in public literature, and trade movement for relevant lab consumables, and then we revisited any large variances.

Before sign-off, the model went through stepwise analyst reviews that checked for sudden price jumps, mix shifts that did not match field feedback, and region splits that conflicted with known lab activity patterns. When an anomaly remained, follow-up calls were triggered to re-check the assumption that caused it. Reports are refreshed annually, with interim updates when material events occur, and a final fresh pass is completed right before delivery so clients receive the most current view.

Mordor Intelligence's Molecular Weight Markers Market Size Measured Against Other Published Estimates

Published market sizes for molecular weight markers can look different even when the topic name is the same, since researchers may not align on the exact product scope, the base year, and how they treat price progression for specialty ladders. Differences also come from how quickly assumptions are updated when lab purchasing patterns shift.

Some external estimates appear to roll adjacent electrophoresis consumables into the total, and others lean on a single base-year value carried forward with a standard CAGR. Those broader totals can move away from the marker-only demand pool once labs shift between prestained and unstained ladders, and Mordor Intelligence counts only DNA, RNA, and protein marker standards sold as ladders or reference mixes, excluding gel boxes, stains, and imaging.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.97 B (2026) | |

| Global Research Publisher A | USD 0.87 B (2025) | Uses a different comparison year and a 2024 estimation base, and its published summary does not clearly show how specialty and prestained marker mix is updated by region, which can shift the revenue total even with similar volumes. |

| Industry Research Publisher B | USD 0.95 B (2025) | Reports a 2025 base value with high-level inputs, which can hide whether some electrophoresis consumables beyond marker standards are included, and whether currency timing and inflation assumptions are kept consistent across geographies. |

The table indicates that most variance comes from what is counted inside marker revenues and from the year being used for the stated market size. By tying the model to electrophoresis run activity and by re-checking price-mix movement for prestained, unstained, and specialty formats during review, the final number stays traceable to repeatable steps and clear lab demand signals.

Key Questions Answered in the Report

What is the current size of the molecular weight markers market?

The molecular weight markers market size stands at USD 0.97 billion in 2026, with a forecast value of USD 1.79 billion by 2031.

Which region leads global revenue?

North America leads with 37.95% share owing to sustained biotech funding and rapid adoption of AI-enabled laboratory automation.

Which product segment is growing fastest?

RNA ladders show the highest growth, registering a 14.02% CAGR through 2031 as mRNA-based therapeutics and NGS workflows scale.

Why are fluorescent protein ladders gaining attention?

AI-driven gel-imaging platforms require consistent fluorescent signals for automated band detection, boosting demand for specialty fluorescent ladders.

How are workforce shortages influencing market demand?

Laboratory staffing gaps push institutions toward ready-to-use, automation-friendly ladders that shorten preparation time and reduce the need for specialized electrophoresis expertise.

Page last updated on: