Weight Loss Diabetes Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

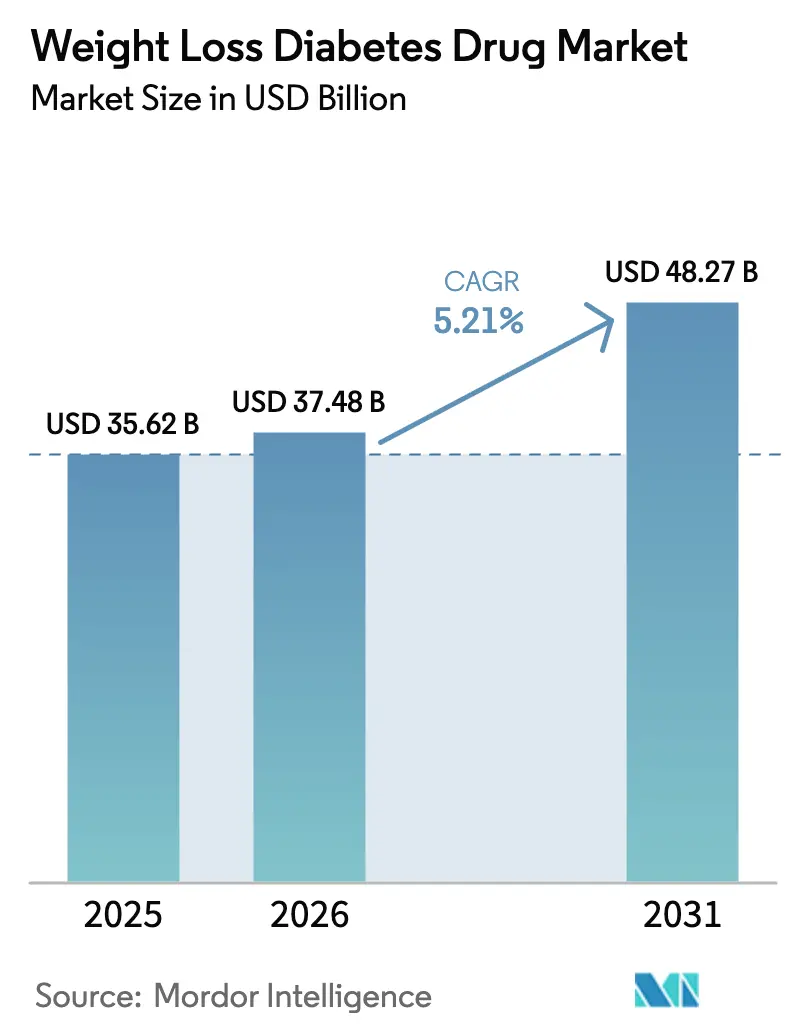

| Market Size (2026) | USD 37.48 Billion |

| Market Size (2031) | USD 48.27 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

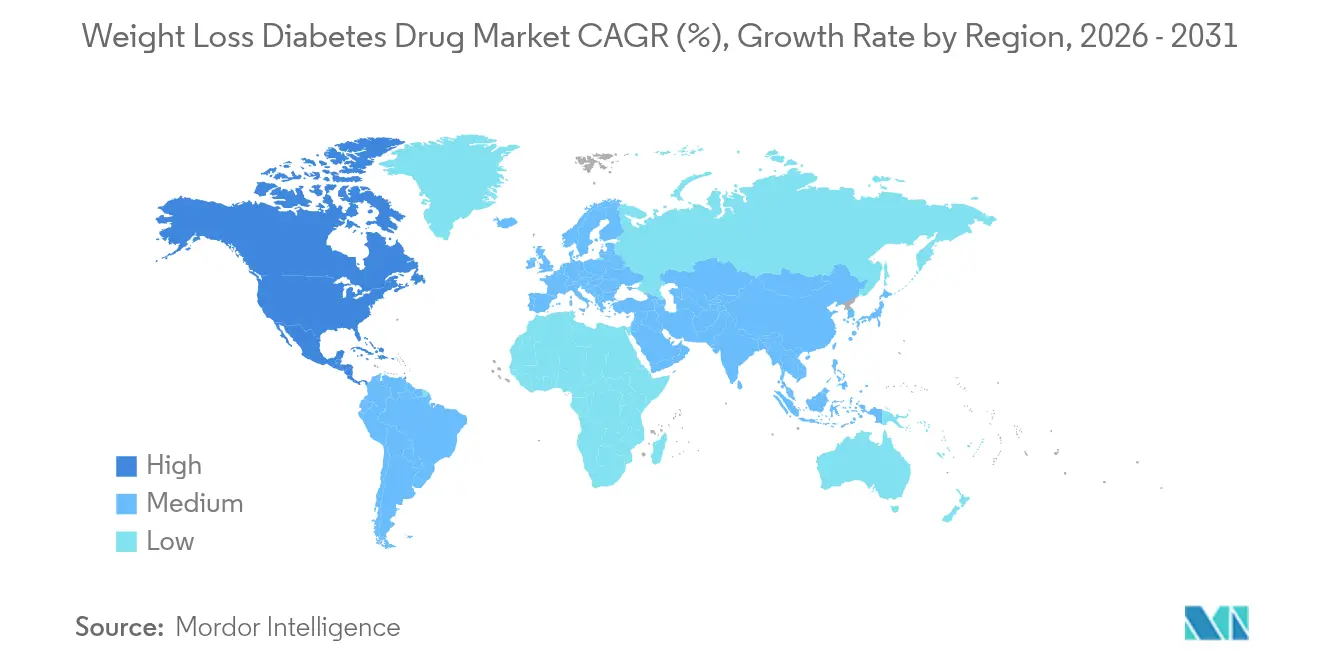

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Weight Loss Diabetes Drug Market Analysis by Mordor Intelligence

The Weight Loss Diabetes Drug Market size is expected to grow from USD 35.62 billion in 2025 to USD 37.48 billion in 2026 and is forecast to reach USD 48.27 billion by 2031 at 5.21% CAGR over 2026-2031.

Sustained growth rests on expanding dual-agonist portfolios, broadening obesity–diabetes overlap, and accelerated regulatory pathways that add renal and cardiovascular indications. Competitive intensity is rising as Chinese long-acting entrants trigger global price resets and U.S. payers impose stricter outcome-based reimbursement. Telehealth-enabled direct-to-consumer models further widen patient reach while reshaping traditional pharmacy economics. Simultaneously, supply expansions such as Novo Nordisk’s Catalent acquisition aim to ease lingering shortages and stabilize distribution costs.

Key Report Takeaways

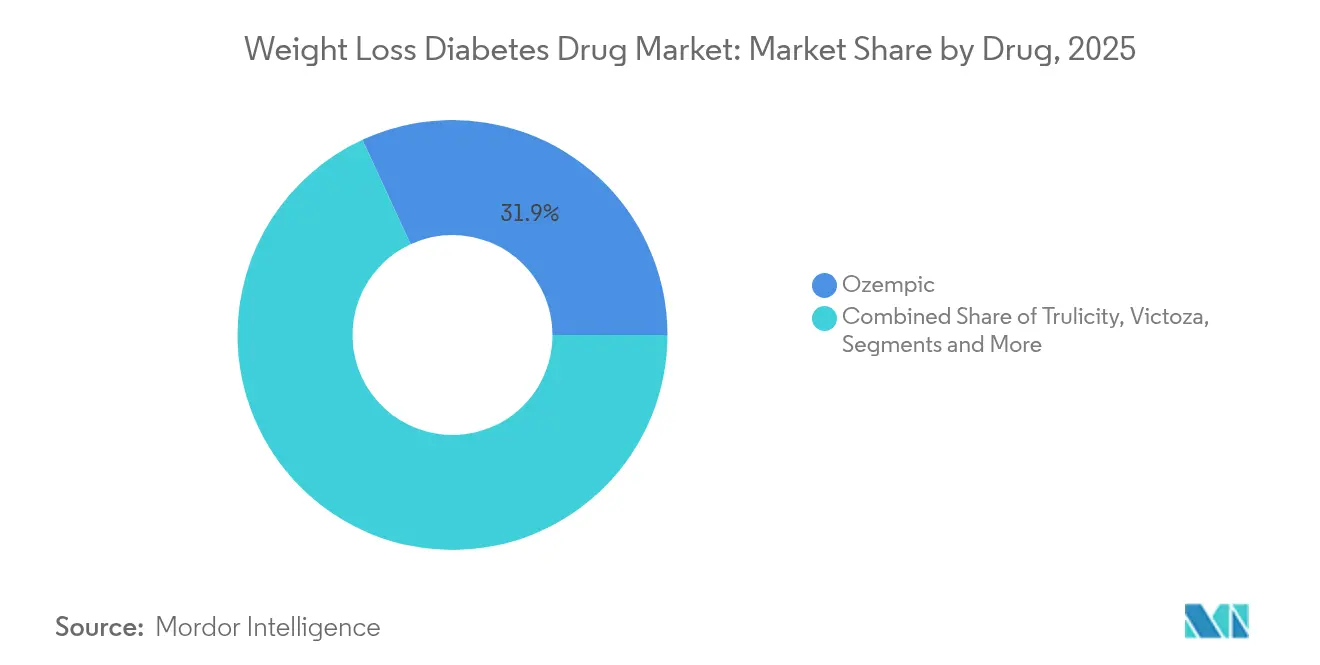

- By drug, Ozempic held 31.88% of GLP-1 diabetes drugs market share in 2025, while Mounjaro is projected to expand at a 5.86% CAGR through 2031.

- By mechanism of action, GLP-1 receptor agonists commanded 81.62% revenue share in 2025; dual GIP/GLP-1 agonists register the fastest growth at 6.02% CAGR to 2031.

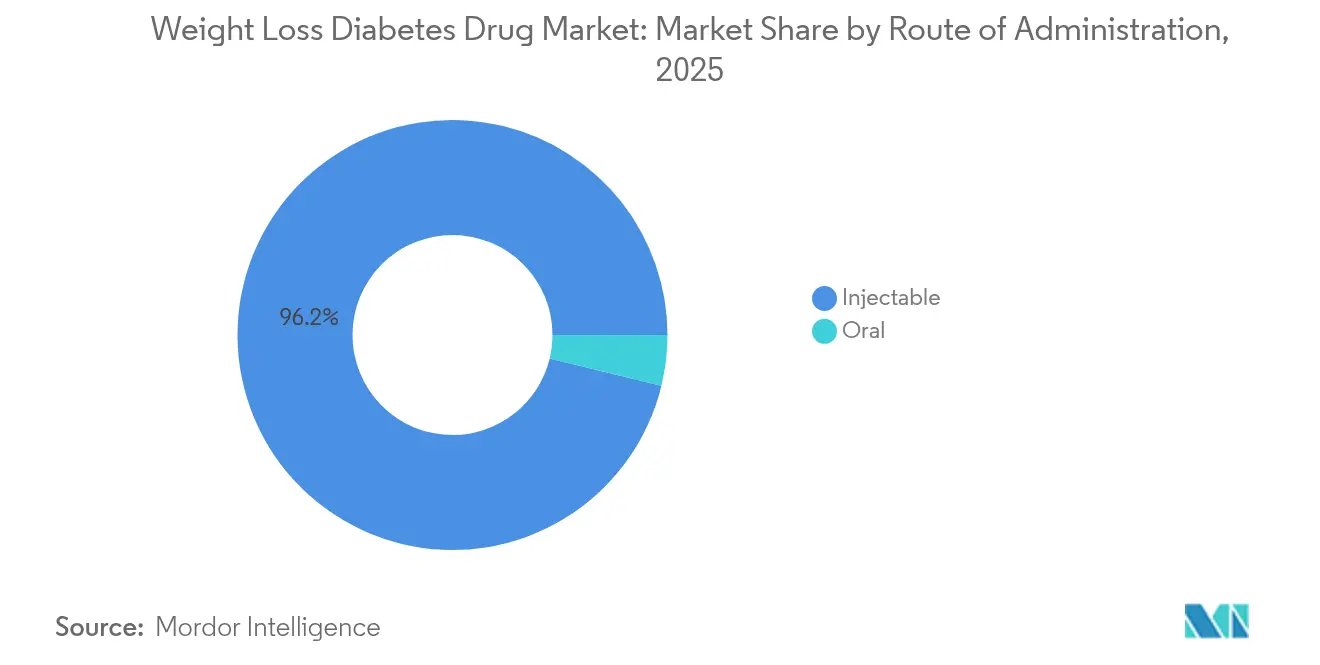

- By route of administration, injectables accounted for 96.21% of GLP-1 diabetes drugs market size in 2025; oral formulations are poised to rise at a 6.39% CAGR over the same period.

- By distribution channel, hospital pharmacies led with 64.72% revenue share in 2025, whereas online and tele-pharmacies record the highest projected CAGR at 6.88% to 2031.

- By geography, North America captured 43.02% GLP-1 diabetes drugs market share in 2025 and Asia-Pacific is forecast to grow at 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Weight Loss Diabetes Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Obesity–Diabetes Comorbidity | +1.8% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Breakthrough GLP-1 & Dual Agonist Efficacy | +1.5% | Global | Short term (≤ 2 years) |

| Faster Regulatory Approvals & Label Expansions | +1.2% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Employer-Driven GLP-1 Coverage Carve-Outs | +0.9% | North America core, expanding to EU | Medium term (2-4 years) |

| Telehealth-Enabled D2C Prescribing Surge | +0.7% | Global, with concentration in developed markets | Short term (≤ 2 years) |

| Chinese Long-Acting Innovation Driving Price Resets | +0.6% | APAC core, spill-over to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Obesity–Diabetes Comorbidity

Escalating obesity rates now exceed 40% among U.S. adults and intersect with an estimated 88 million individuals living with prediabetes [1]Centers for Disease Control and Prevention, “National Diabetes Statistics Report 2025,” cdc.gov. GLP-1 therapies uniquely tackle both conditions, delivering the 20.2% weight loss observed with tirzepatide compared with 13.7% for semaglutide in pivotal trials. Payers recognize the long-term cost offsets of early metabolic intervention, prompting broader benefit coverage across employer and commercial plans. Clinicians increasingly prescribe GLP-1 agents as first-line therapy for metabolic syndrome, driving prescription growth beyond traditional diabetes confines. The resulting demand underpins the near-term expansion of the GLP-1 diabetes drugs market even as pricing pressure intensifies.

Breakthrough GLP-1 & Dual Agonist Efficacy

Superior outcomes from dual agonists such as tirzepatide reinforce a shift toward multi-target innovation. Head-to-head data show HbA1c reductions of 2.0–2.3 percentage points versus 1.6–1.9 points for single-receptor comparators [2]Eli Lilly, “SURPASS Program Results,” lilly.com. Chinese developers add further momentum; Gan & Lee’s GZR18 produced up to 2.32 point HbA1c declines alongside greater weight loss than Ozempic. Pipeline triple agonists targeting GLP-1, GIP, and glucagon reveal early metabolic gains that could reset therapeutic benchmarks after 2027. These efficacy advantages support premium pricing, fortify physician confidence, and propel the GLP-1 diabetes drugs market toward higher competitive complexity.

Faster Regulatory Approvals & Label Expansions

U.S. FDA priority reviews continue to shorten approval cycles, as seen in semaglutide’s 2025 chronic kidney disease indication and tirzepatide’s 2024 obstructive sleep apnea approval. European Medicines Agency alignment cuts historical launch lags, hastening market penetration across the Atlantic. Label extensions into cardiovascular, renal and neuro-metabolic disorders expand the addressable population without new molecules, offering cost-efficient revenue growth. The wider therapeutic scope sustains the GLP-1 diabetes drugs market when core diabetes growth moderates and competitors crowd first-line positions.

Employer-Driven GLP-1 Coverage Carve-Outs

Employers now fund 36% of benefit plans that cover GLP-1 drugs for both diabetes and weight loss, up from 2023’s 24%. Advanced utilization management integrates step therapy and digital coaching, tying reimbursement to measurable outcomes. The shift affects formulary negotiations, compelling manufacturers to demonstrate tangible productivity gains and total cost savings. As employer contracts grow, the GLP-1 diabetes drugs market witnesses new commercial models emphasizing data-validated value over list price.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Therapy Cost & Patchy Reimbursement | -1.4% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Ongoing GLP-1 Supply Constraints | -0.8% | Global | Short term (≤ 2 years) |

| Intensified Safety-Signal Surveillance (E.G., Sarcopenia) | -0.6% | Global, with stricter oversight in EU | Medium term (2-4 years) |

| Proliferation Of Compounded Generics Eroding ASPs | -0.5% | North America core, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Patchy Reimbursement

Monthly therapy costs ranging from USD 1,000 to USD 1,600 restrict access outside affluent economies. Medicare excludes weight loss indications, while U.S. Medicaid coverage variegates by state, causing marked uptake disparity. In emerging markets reimbursement gaps curb initial prescriptions despite rising prevalence, capping near-term volumes. Employer cost controls intensify: 78% already impose prior authorizations or step therapy. Without broad financing reforms, price sensitivity will temper the otherwise strong GLP-1 diabetes drugs market growth trajectory.

Ongoing GLP-1 Supply Constraints

Demand still outpaces output despite Novo Nordisk’s USD 11 billion Catalent acquisition to scale fill-finish capacity. The World Health Organization logged a 101% spike in shortage alerts since 2021, particularly in lower-income regions [3]World Health Organization, “Global Medicine Shortage Alerts Dashboard,” who.int . Cold-chain logistics add bottlenecks where infrastructure lags. Shortages encourage gray-market imports and compounded alternatives, diluting branded revenues and undermining patient safety. Manufacturers must synchronize facility expansions, raw-material sourcing, and temperature-controlled distribution to safeguard GLP-1 diabetes drugs market credibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug: Ozempic Dominance Faces Dual-Agonist Challenge

The GLP-1 diabetes drugs market size for brand-level competition shows Ozempic at USD 11.36 billion revenue in 2025, translating to a 31.88% GLP-1 diabetes drugs market share. Mounjaro follows with lower absolute sales but a leading 5.86% CAGR outlook to 2031 on the strength of dual-receptor efficacy. Physicians continue prescribing Trulicity due to familiarity, yet payer formularies increasingly pivot to Mounjaro as outcomes data accumulate. Victoza’s first generic entry in 2024 depresses branded volume though maintains relevance among patients intolerant to newer agents. Saxenda’s growth remains constrained by weight-loss coverage gaps despite clinical benefits. Emerging Chinese molecules such as GZR18 promise to disrupt incumbents by pairing high efficacy with aggressive pricing, reinforcing global competition and fostering broader access.

Early adoption curves from 2020-2024 highlight Ozempic’s rapid climb, but forecast dynamics favor dual and triple agonists. The GLP-1 diabetes drugs market consequently balances mature blockbuster sustainability against next-wave innovation cycles. As Mounjaro collects longer safety datasets and real-world evidence, formulary positions may shift, accelerating its share gain at Ozempic’s expense. Generic liraglutide also nudges pricing downward in older patient cohorts, broadening entry points but pressuring originator margins.

By Mechanism of Action: Single Receptors Yield to Multi-Target Innovation

Single-target GLP-1 receptor agonists generated USD 29.07 billion in 2025, preserving 81.62% share of the GLP-1 diabetes drugs market size. However, dual GIP/GLP-1 agonists, though still small by value, deliver 6.02% CAGR and anchor most late-stage pipelines. Clinical enthusiasm stems from superior HbA1c and weight reductions that boost adherence and extend dosing intervals. Triple agonists enter mid-stage trials with potential to broaden metabolic benefits, including lipid lowering and energy expenditure increases. SGLT-2 inhibitors retain adjunctive roles, often combined for cardiorenal protection, while amylin analogues remain niche given specificity to postprandial control.

Market evolution underscores the strategy shift from marginal formulation tweaks to receptor-synergistic breakthroughs. As multi-agonists secure approvals, reimbursement authorities may reward stronger risk-reduction profiles, underpinning sustained GLP-1 diabetes drugs market expansion in the latter half of the decade.

By Route of Administration: Injectable Dominance Challenged by Oral Innovation

Injectables captured USD 34.27 billion revenue in 2025, equal to 96.21% of GLP-1 diabetes drugs market size. Patient familiarity with weekly pens sustains high adoption, and long-acting depots under development aim to reduce dosing to monthly or quarterly intervals. Concurrently, oral candidates advance rapidly; orforglipron showed 1.3-1.6 point HbA1c reductions and 7.9% body-weight loss in Phase 3 studies. Oral semaglutide high-dose extensions (25 mg and 50 mg) also target injection-averse segments. The 6.39% CAGR projected for orals reflects both convenience appeal and pipeline breadth.

Formulation science centers on overcoming peptide degradation in the gastrointestinal tract and ensuring consistent absorption. Success will dilute injectable dominance yet expand the GLP-1 diabetes drugs market by attracting adherence-challenged patients. Over the forecast, modality choice will hinge on balancing efficacy, dosing frequency, and coverage parity.

By Distribution Channel: Hospital Dominance Erodes to Digital Innovation

Hospital pharmacies recorded USD 23.06 billion sales in 2025 or 64.72% of total GLP-1 diabetes drugs market size because endocrinologists initiate most complex cases within integrated settings. However, online and tele-pharmacies grow at 6.88% CAGR, reinforced by LillyDirect and similar platforms that ship medication directly to consumers at discounted prices. Retail chains struggle with diminishing margins as pharmacy benefit managers narrow spreads. Specialty providers such as Shields Health Solutions add adherence coaching and prior authorization support, carving a premium niche.

During 2020-2024 shortages, compounded pharmacies temporarily filled gaps, yet subsequent legal and regulatory challenges curbed that channel. The 2026-2031 period is likely to witness blended distribution where digital direct-to-consumer solutions coexist with specialty hubs for complex titration and monitoring, diversifying revenue streams within the GLP-1 diabetes drugs market.

Geography Analysis

North America produced USD 15.33 billion sales in 2025, equal to 43.02% of the GLP-1 diabetes drugs market. Employer-led carve-outs accelerate uptake, while the FDA fast-tracks new indications, sustaining premium prices despite payer controls. Canada mirrors U.S. prescription momentum though reimburses more conservatively, whereas Mexico’s private sector drives growth as public funding remains fragmented. Telehealth prescribing proliferates, particularly within the United States, where LillyDirect and Teladoc alliances expand reach beyond brick-and-mortar settings.

Asia-Pacific represents the fastest-growing territory with 7.52% CAGR. China spearheads progress through regulatory modernization that backs domestic candidates like GZR18, amplifying competitive pricing. India’s diabetes burden sparks parallel growth with expected CAGR of 24.7% to 2034 per government data, supported by expanding manufacturing infrastructure. Mature markets such as Japan and South Korea adopt newer molecules quickly due to universal coverage systems, while Australia leverages a progressive Pharmaceutical Benefits Scheme to list breakthrough therapies soon after approval.

Europe contributes steady incremental gains. Germany, United Kingdom, and France comprise the lion’s share, leveraging robust diabetes management programs. The European Medicines Agency’s speedier reviews narrow the historical gap with the FDA, encouraging synchronized launches. Southern European countries, including Italy and Spain, amplify demand as public systems widen obesity coverage. The rest of Europe market benefits from structural funds bolstering cold-chain capacity, facilitating broader therapy availability and propelling the GLP-1 diabetes drugs market regionwide.

Competitive Landscape

Competition in the GLP-1 diabetes drugs market remains intense yet moderately concentrated. Novo Nordisk and Eli Lilly jointly hold about 70% share, commanding scale advantages in manufacturing, clinical trial infrastructure, and global distribution. Novo Nordisk leverages legacy semaglutide franchises but invests heavily in oral and long-acting iterations to defend its base. Eli Lilly rides Mounjaro’s dual-agonist momentum and pioneers direct-to-consumer channels to diversify revenue capture.

Chinese firms such as Gan & Lee and Hansoh aggressively progress dual and triple agonists, capitalizing on cost-efficient R&D and favorable domestic policies. Their head-to-head efficacy gains threaten incumbent premium pricing, particularly in emerging markets. Western incumbents respond with strategic manufacturing investments, exemplified by Novo Nordisk’s Catalent acquisition, to alleviate shortages and strengthen supply resilience. Partnerships around novel delivery technologies proliferate; Camurus’s sustained-release depot collaboration with Eli Lilly targets monthly dosing that could solidify brand loyalty.

Intellectual-property cliffs loom, with liraglutide generics already approved and semaglutide patents due to face challenges by 2027. Biosimilar pathways may compress prices yet widen access, potentially enlarging patient pools and partially offsetting unit erosion. Overall, innovation cadence and capacity scale will dictate winner profiles over the forecast period as the GLP-1 diabetes drugs market navigates a transition from high-margin exclusivity to broader affordability.

Weight Loss Diabetes Drug Industry Leaders

Eli Lilly

Novo Nordisk

Boehringer Ingelheim

Amylin Pharmaceuticals

Harman Finochem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Drugmaker Eli Lilly announced that oral GLP-1 candidate orforglipron cut HbA1c by 1.3–1.6 points and induced 7.9% body-weight loss in Phase 3 trials.

- November 2023: The U.S. Food and Drug Administration approved Eli Lilly’s weight-loss drug Zepbound, which enabled up to 52 pound reduction over 16 months.

- July 2023: The FDA disclosed limited availability of Novo Nordisk’s Saxenda due to surging demand amid Wegovy, Ozempic, and Mounjaro shortages.

Global Weight Loss Diabetes Drug Market Report Scope

Certain medications used to treat diabetes can impact an individual's body weight. This can result in either a decrease or an increase in weight. However, it is important to note that not all diabetes medications lead to changes in weight. Some medications have minimal impact on weight for the majority of individuals who use them. Weight Loss Diabetes Drug Market is set to witness a CAGR of more than 5% during the forecast period. Weight Loss Diabetes Drug Market is segmented by drug ( Trulicity, Victoza, Ozempic, Saxenda, Mounjaro, Jardiance, Symlin, Metfromin) and by geography (North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America). The report offers the value (in USD) and volume (in units) for the above segments.

| Trulicity |

| Victoza |

| Ozempic |

| Saxenda |

| Mounjaro |

| Others |

| GLP-1 Receptor Agonists |

| Dual GIP/GLP-1 Agonists |

| SGLT-2 Inhibitors |

| Amylin Analogues |

| Injectable |

| Oral |

| Hospital Pharmacies |

| Retail & Community Pharmacies |

| Online/Tele-pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug | Trulicity | |

| Victoza | ||

| Ozempic | ||

| Saxenda | ||

| Mounjaro | ||

| Others | ||

| By Mechanism of Action | GLP-1 Receptor Agonists | |

| Dual GIP/GLP-1 Agonists | ||

| SGLT-2 Inhibitors | ||

| Amylin Analogues | ||

| By Route of Administration | Injectable | |

| Oral | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail & Community Pharmacies | ||

| Online/Tele-pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Weight Loss Diabetes Drug Market?

The Weight Loss Diabetes Drug Market size is expected to reach USD 37.48 billion in 2026 and grow at a CAGR of 5.21% to reach USD 48.27 billion by 2031.

Which drug leads the GLP-1 diabetes drugs market?

Ozempic leads with 31.88% share in 2025, though Mounjaro is growing fastest at a 5.86% CAGR.

Who are the key players in Weight Loss Diabetes Drug Market?

Eli Lilly, Novo Nordisk, Boehringer Ingelheim, Amylin Pharmaceuticals and Harman Finochem are the major companies operating in the Weight Loss Diabetes Drug Market.

How fast are oral GLP-1 therapies expected to grow?

Oral formulations are forecast to expand at a 6.39% CAGR between 2026 and 2031 as products like orforglipron near approval.

Which region has the biggest share in Weight Loss Diabetes Drug Market?

In 2025, the North America accounts for the largest market share in Weight Loss Diabetes Drug Market.

Page last updated on: