Weight Loss Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

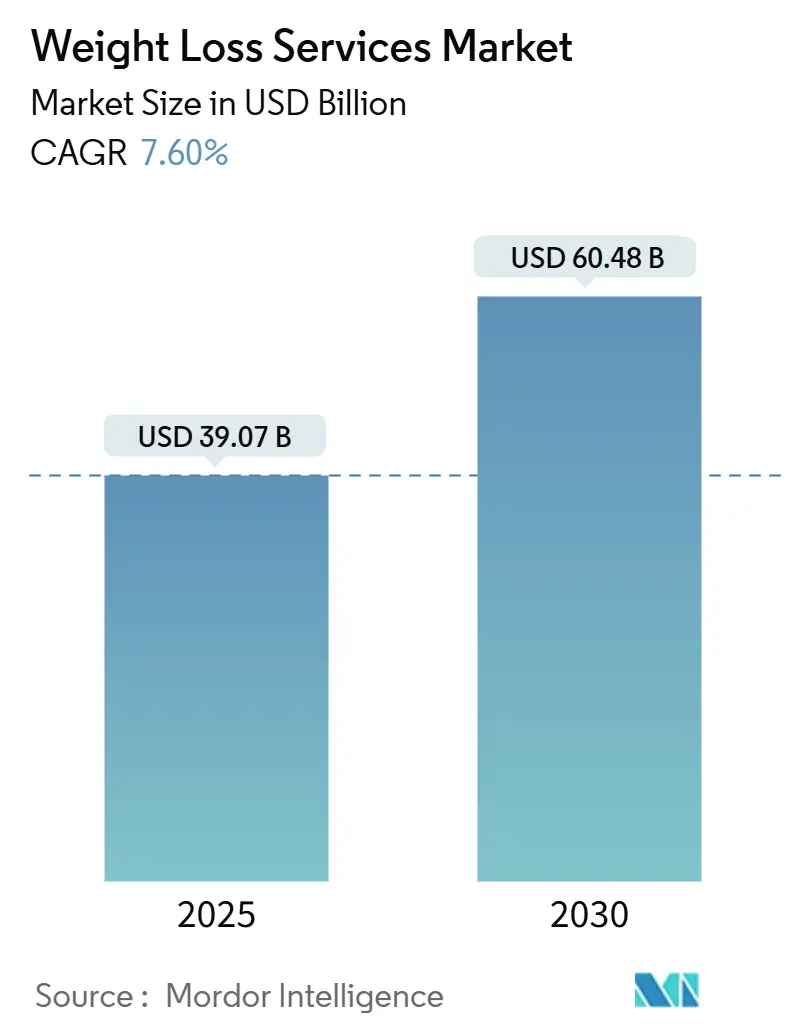

| Market Size (2025) | USD 39.07 Billion |

| Market Size (2030) | USD 60.48 Billion |

| Growth Rate (2025 - 2030) | 7.60% CAGR |

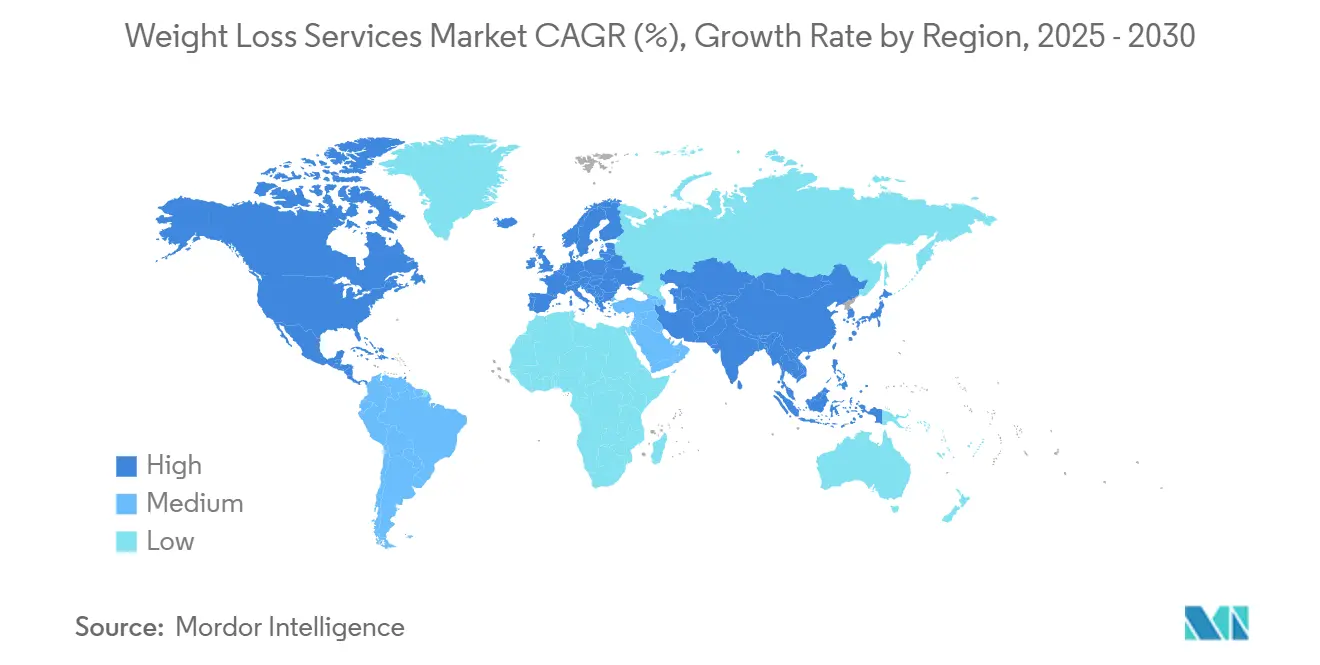

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Weight Loss Services Market Analysis by Mordor Intelligence

The weight loss services market reached USD 39.07 billion in 2025 and is forecast to advance to USD 60.48 billion by 2030, reflecting a 7.6% CAGR. The upward trajectory stems from an unprecedented convergence of prescription GLP-1 therapies, digital engagement platforms, and employer-sponsored wellness benefits. More than 40% of U.S. adults currently live with obesity, a figure that validates sustained demand for medically oriented weight management programs. Pharmaceutical breakthroughs have expanded the eligible population for evidence-based interventions, while AI-driven coaching tools personalize behavior‐change plans at scale. Employer health plans are simultaneously broadening coverage for anti-obesity medicines, creating a robust reimbursement foundation for service providers. Investments in omnichannel delivery—combining clinics, telehealth, wearable integration, and app-based coaching—have become the primary competitive lever as consumers seek seamless, round-the-clock access to support.

Key Report Takeaways

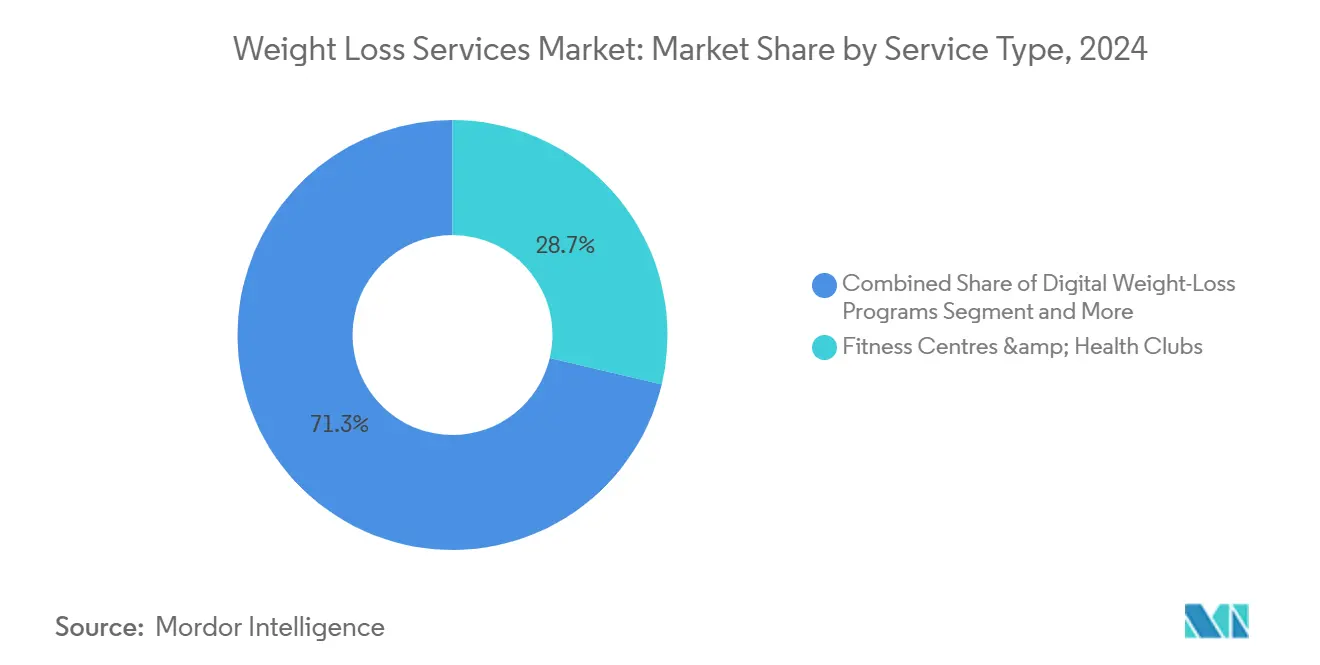

- By service type, Fitness Centres & Health Clubs led with 28.7% revenue share in 2024; Digital Weight-Loss Apps are projected to grow at an 18.4% CAGR through 2030.

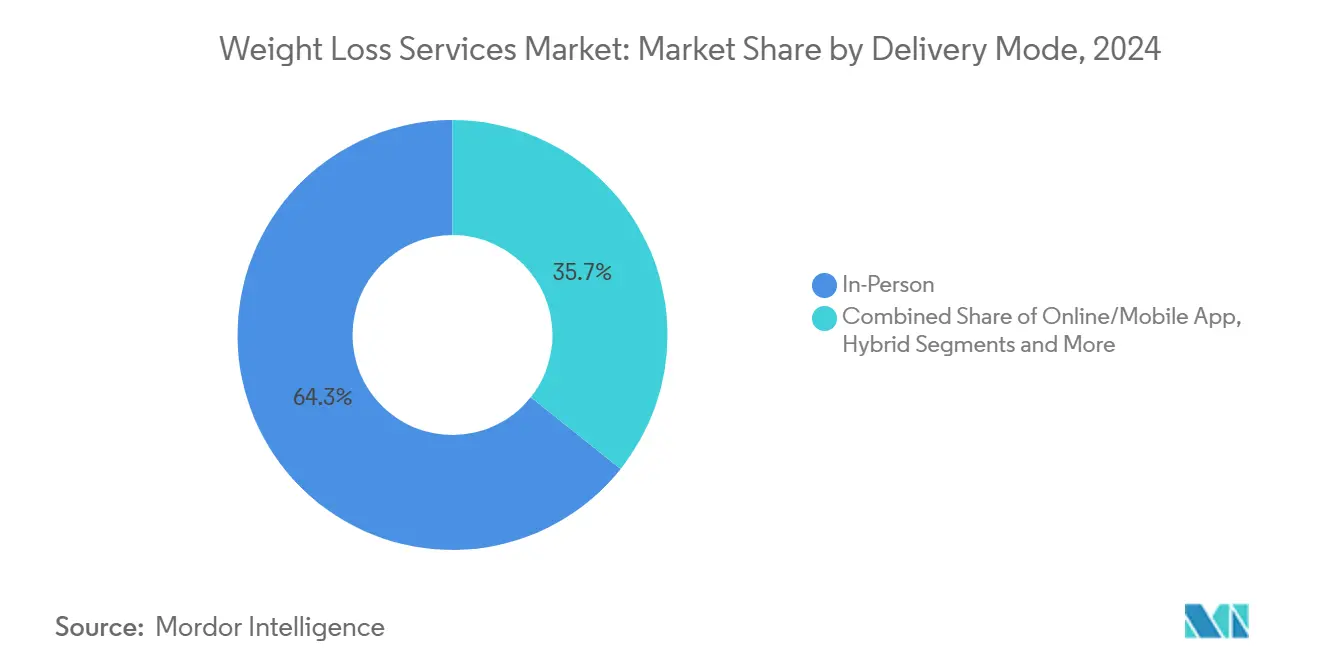

- By delivery mode, the in-person model held 64.3% of the Weight loss services market share in 2024, while online/mobile platforms are expanding at a 19.5% CAGR to 2030.

- By geography, North America accounted for a 37.9% share of the Weight loss services market size in 2024; Asia Pacific is advancing at an 8.6% CAGR through 2030.

Global Weight Loss Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Obesity Prevalence | 1.80% | Global, with highest impact in North America and Asia Pacific | Long term (≥ 4 years) |

| Growing Health Awareness & Discretionary Income | 1.20% | North America & EU, expanding to APAC urban centers | Medium term (2-4 years) |

| Digital Health & Fitness App Proliferation | 1.50% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Expansion Of Employer Wellness Incentives | 0.90% | North America & EU, emerging in APAC corporate sectors | Medium term (2-4 years) |

| GLP-1 Drug–Programme Partnerships | 1.40% | North America and Europe, expanding globally | Short term (≤ 2 years) |

| AI-Driven Hyper-Personalised Coaching | 0.80% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Obesity Prevalence

Obesity rates are climbing across developed and emerging economies, and prevalence in the Asia Pacific is forecast to rise from 14% in 2020 to 24% by 2035.[1]David Tak Wai Lui et al., “Obesity in the Asia-Pacific Region: Current Perspectives,” Journal of Asian Pacific Society of Cardiology, japscjournal.com The economic toll is stark: U.S. employers incur average obesity-related medical costs of USD 16,000 per worker each year. Governments are responding—new 2025 federal rules in the United States elevate obesity to a reimbursable public-health priority, encouraging insurers to fund comprehensive weight-management regimens.[2]Alexandra Schultz, “Biden Administration Introduces New Rule Intended to Curb Obesity,” The Regulatory Review, theregreview.org Expanded reimbursement removes a key financial barrier, accelerating the adoption of structured programs that combine medication with lifestyle intervention.

GLP-1 Drug–Programme Partnerships

GLP-1 receptor agonists such as semaglutide and tirzepatide routinely deliver 15–20% body-weight reductions, but durable success hinges on behavioral support. Novo Nordisk is forging alliances with digital-health firms to integrate coaching dashboards and adherence analytics into GLP-1 care pathways. Digital platform Noom introduced a micro-dose GLP-1 plan priced at USD 119 for initiation, bundling remote physician oversight with AI habit coaching to mitigate gastrointestinal side effects. Telehealth leader Teladoc Health now offers pharmacist-led GLP-1 titration services embedded in multidisciplinary obesity clinics.

Digital Health & Fitness-App Proliferation

Calorie-log utilities have evolved into machine-learning engines that deliver decision-support nudges in real time. Fred Fitness opened the world’s first AI-powered gym, where adaptive algorithms adjust resistance and tempo after every repetition. Meta-analyses confirm that digital adherence predicts superior GLP-1 outcomes, with high-engagement cohorts losing 6 kg more than low-engagement peers over six months. Successful apps weave in coach messaging, social accountability loops, and wearables data, a combination that sustains user retention beyond the critical 90-day mark.[3]E. Fatti, S. Khawaja, and K. Weis, “The Dark Side of Fluorescent Protein Tagging—The Impact of Protein Tags on Biomolecular Condensation,” Molecular Biology of the Cell, pmc.ncbi.nlm.nih.gov

Expansion of Employer Wellness Incentives

Corporate purchasers view weight management as a cost-containment lever: every USD 1 invested can yield USD 2.53–5.00 in claims savings. Real Appeal analyzed claims of 15,000 employees and verified a 2:1 ROI within three years. Employers are adding GLP-1 coverage and pairing prescriptions with structured coaching programs. Medifast’s OPTAVIA ASCEND line blends protein-rich mini-meals and micronutrient packs explicitly formulated for GLP-1 users, demonstrating how vendors tailor offerings to enterprise buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advertising-Claim Regulatory Scrutiny | -0.70% | Global, with strictest enforcement in North America and EU | Short term (≤ 2 years) |

| High Programme & Meal-Kit Costs | -1.10% | Global, with highest impact in price-sensitive markets | Medium term (2-4 years) |

| Shift To Free Social-Media Communities | -0.90% | Global, accelerated by social platform algorithm changes | Short term (≤ 2 years) |

| GLP-1 Supply Shortages Disrupting Hybrid Models | -0.80% | North America and Europe primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Advertising-Claim Regulatory Scrutiny

The U.S. Federal Trade Commission now demands randomized trials to substantiate weight-loss claims, placing legacy slogans like “lose 10 lb in 2 weeks” under threat of litigation. The FDA’s 2025 “healthy” labeling rule further requires companies to document nutrient profiles for every packaged snack they promote. Rising compliance costs favor well-capitalized incumbents with in-house scientific teams, accelerating consolidation.

Shift to Free Social-Media Communities

TikTok clips tagged #Ozempic have amassed more than 70 million views, spawning peer-led advice groups that undercut paid programs. Research finds 51% of Gen Z respondents adopt diet changes recommended by influencers, shrinking the addressable pool for subscription models. Commercial providers must now prove superior safety oversight, professional credibility, and outcome measurement to justify fees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Disruption Accelerates

The fitness centres & health clubs category captured 28.7% of the Weight loss services market share in 2024. Digital Weight-Loss Apps, while smaller in revenue today, are scaling at an 18.4% CAGR that outpaces every other format. Hybrid models now merge app analytics with in-studio coaching, creating omnichannel accountability loops that improve session adherence. Consulting and coaching specialists report rising demand for medication-optimization curricula, reflecting consumer anxiety about post-GLP-1 weight regain. Medical Weight-Loss Programs exhibit stable double-digit growth as swallowable balloons and remote vitals monitoring increase procedure convenience. Tightened FDA guidance—requiring ≥ 5% incremental weight reduction versus placebo for approval—has raised the bar for efficacy claims, steering consumers toward clinically validated providers.

The digital cohort’s retention hurdle persists: churn spikes after day 60 unless apps deliver live coach feedback and community features. Gamification and social-leaderboard functions have helped extend average subscription life by two months. Meanwhile, brick-and-mortar chains invest in body-composition scanners and metabolic testing pods to create data streams that complement their own mobile apps. The evolving consensus is that pure-play digital or in-person constructs leave engagement gaps; hence, investors are channeling capital toward platforms that demonstrate seamless hand-offs between virtual and physical touchpoints.

By Delivery Mode: Hybrid Models Gain Traction

In-person delivery secured 64.3% of the Weight loss services market size in 2024, underscoring enduring consumer appetite for human coaching and accountability. Yet online/mobile programs are advancing at a 19.5% CAGR, propelled by lower price points and convenience for time-starved professionals. Regulatory frameworks for digital therapeutics in the United States now require evidence of clinical benefit, a stipulation that weeds out shallow “diet-tip” apps and lifts credible interventions. Online leaders deploy machine-learning algorithms that personalize calorie ceilings in real time, boosting week-12 weight-loss differentials by 1.4 kg over static plans.

Hybrid architectures are winning over employers and payers. LifeMD’s partnership with Withings pipes connected-scale readings into clinician dashboards, enabling dosage adjustments for GLP-1 users without office visits. WeightWatchers’ acquisition of Sequence brings prescription management into its legacy group-coaching ecosystem, reflecting sector-wide convergence. Over the forecast window, hybrid delivery is positioned to erode standalone in-person share. Still, physical venues will remain pivotal for biometric testing, group accountability, and high-marginal-profit personal-training add-ons.

Geography Analysis

North America retained 37.9% of global revenue in 2024. The region’s early GLP-1 uptake—6% of adults used a prescription anti-obesity drug by mid-2024—boosted demand for wraparound coaching and meal-planning services. Employer wellness ROI metrics, ranging from 2.5× to 5×, convinced large corporations to scale incentives for biometric screenings and anti-obesity drug copays. Pending Medicare coverage would further widen access, potentially adding 4 million beneficiaries by 2030. Competitive intensity is high as chains, telehealth startups, and health insurers compete for overlapping target groups.

Asia Pacific is the fastest-growing territory, expanding at 8.6% CAGR through 2030. Rising disposable incomes and the westernization of diets are pushing obesity prevalence toward 24% by 2035. India’s adult overweight rate now exceeds 23%, catalyzing demand for semaglutide plus traditional Ayurveda-infused diet plans. Digital adoption is especially pronounced; 3% of urban consumers already use GLP-1 drugs, and companion probiotics have gained traction to mitigate gastrointestinal events. Regulatory heterogeneity persists, yet multinational clinic operators are adapting by localizing menu offerings and leveraging remote-monitoring kits to serve rural patients.

Europe delivers steady mid-single-digit growth underpinned by universal healthcare coverage and strict evidence thresholds for reimbursement. Novo Nordisk’s manufacturing expansion in Denmark and the United Kingdom guarantees adequate drug supply to support hybrid programs. The United Kingdom’s Weight loss services market is projected to reach GBP 1.5 billion by 2027, aided by private-equity roll-ups of regional clinics. EU regulators rigorously police advertising, elevating entry barriers for newcomers but favoring incumbents with published outcome data.

Competitive Landscape

Competition is moderate yet intensifying as pharmaceutical entrants reshape consumer expectations. Wellful, owner of Nutrisystem and Jenny Craig, began debt restructuring after GLP-1 uptake eroded demand for meal-replacement plans. WeightWatchers countered by buying telehealth firm Sequence, instantly gaining prescriber status for semaglutide and tirzepatide. Medifast launched OPTAVIA ASCEND, supplementing its portion-controlled meal kits with high-protein snacks for GLP-1 users. Noom’s micro-dose program differentiates through side-effect minimization and price transparency.

Allurion Technologies packages a swallowable gastric balloon with AI-driven remote weight-monitoring; early adopters average 14% total weight loss over six months. Teladoc Health weaves obesity care into its chronic-condition suite, giving payers a single platform for diabetes, hypertension, and weight management. Private-equity groups funnel capital into clinic chains offering bundled GLP-1 prescriptions plus behavior coaching. Heightened FTC and FDA scrutiny favors firms with robust clinical‐trial data and established pharmacovigilance systems, squeezing out under-capitalized single-solution providers.

Weight Loss Services Industry Leaders

WW International

Herbalife Nutrition

Noom Inc.

Nutrisystem

Slimming World

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Noom launched a Microdose GLP-1Rx program at USD 119 upfront and USD 199 per month, reporting 70% side-effect-free usage and 11 lb average loss in 30 days.

- May 2025: CheqUp partnered with WeightWatchers in the United Kingdom to embed medication access into lifestyle coaching.

- April 2025: Wondr Health rolled out GLP-1 support programs across employer benefit plans, broadening workplace access.

Global Weight Loss Services Market Report Scope

| Digital Weight-Loss Programs |

| Fitness Centres & Health Clubs |

| Slimming / Commercial Weight-Loss Centres |

| Consulting & Coaching Services |

| Medical Weight-Loss Programs (non-surgical) |

| On-site / In-Person |

| Online / Mobile App |

| Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Digital Weight-Loss Programs | |

| Fitness Centres & Health Clubs | ||

| Slimming / Commercial Weight-Loss Centres | ||

| Consulting & Coaching Services | ||

| Medical Weight-Loss Programs (non-surgical) | ||

| By Delivery Mode | On-site / In-Person | |

| Online / Mobile App | ||

| Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Weight loss services market in 2025?

The market stands at USD 39.07 billion in 2025 and is set to reach USD 60.48 billion by 2030.

Which service type grows the fastest through 2030?

Digital Weight-Loss Apps expand at an 18.4% CAGR, the highest among all service categories.

Why are GLP-1 drugs reshaping provider strategies?

Medications such as semaglutide deliver 15-20% weight reduction, prompting legacy programs to embed prescription management and clinical coaching.

Which region records the quickest revenue growth?

Asia Pacific leads with an 8.6% CAGR, driven by urbanization, rising incomes, and escalating obesity prevalence.

What is the primary restraint facing providers?

Intensified regulatory scrutiny on advertising claims imposes higher compliance costs and penalizes unsubstantiated efficacy statements.

How are employers influencing market expansion?

U.S. corporations demonstrate 2.5×5× ROI on wellness spending, motivating them to fund anti-obesity drug coverage and structured coaching programs.

Page last updated on: