Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 52.30 Billion |

| Market Size (2031) | USD 97.45 Billion |

| Growth Rate (2026 - 2031) | 13.26% CAGR |

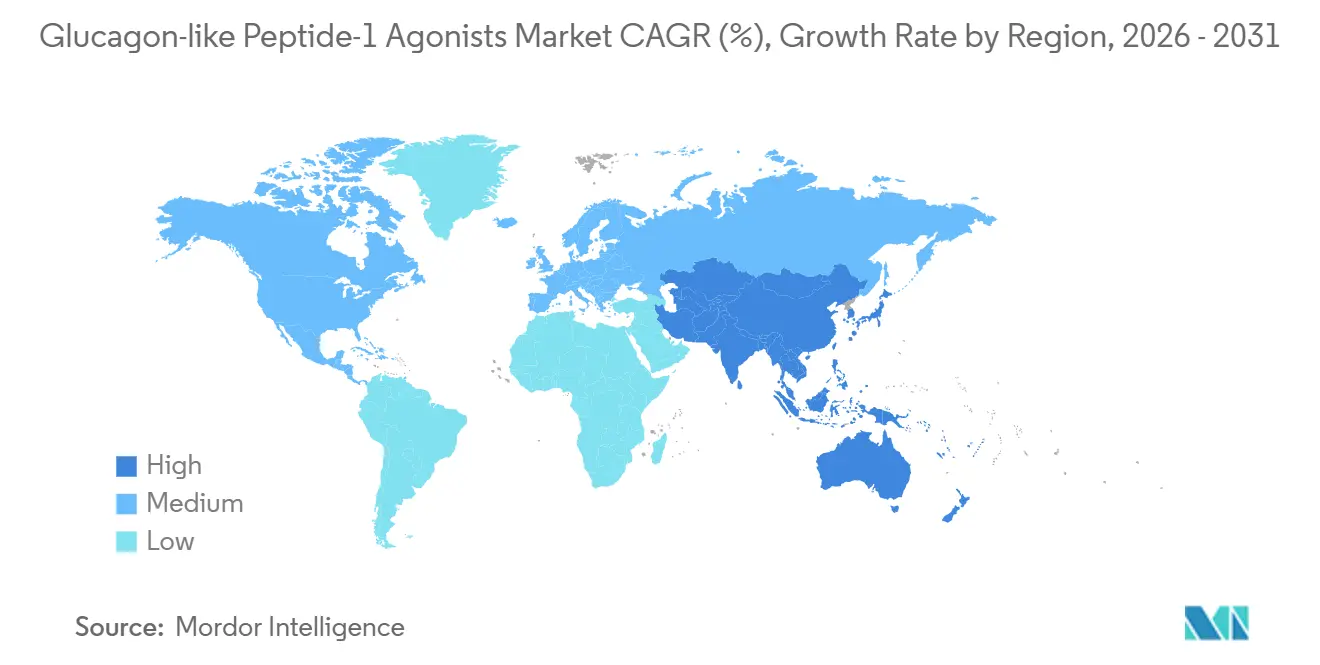

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

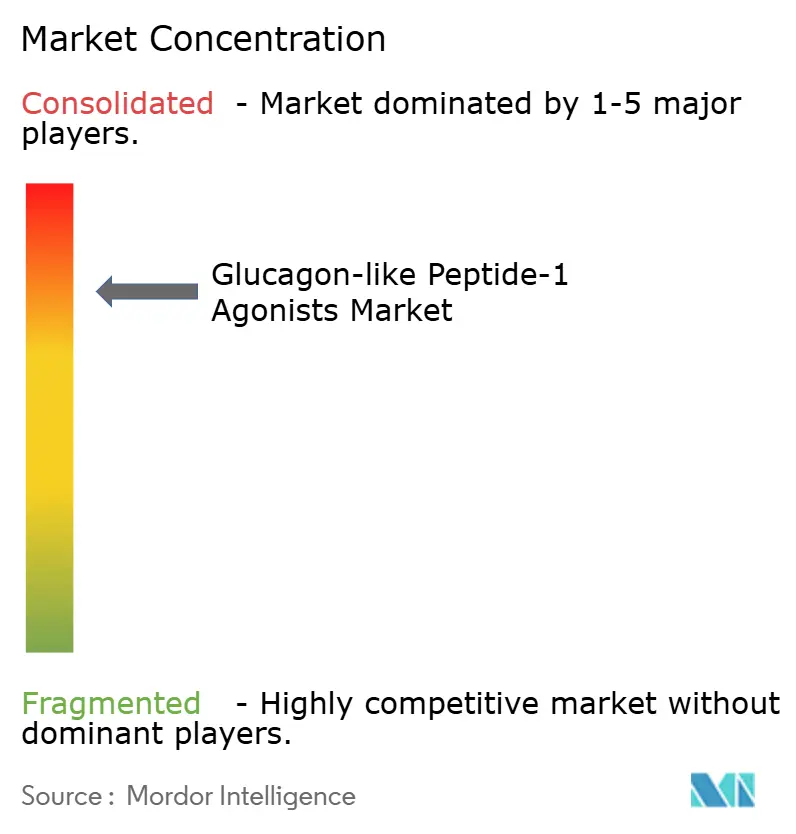

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glucagon-like Peptide-1 Agonists Market Analysis by Mordor Intelligence

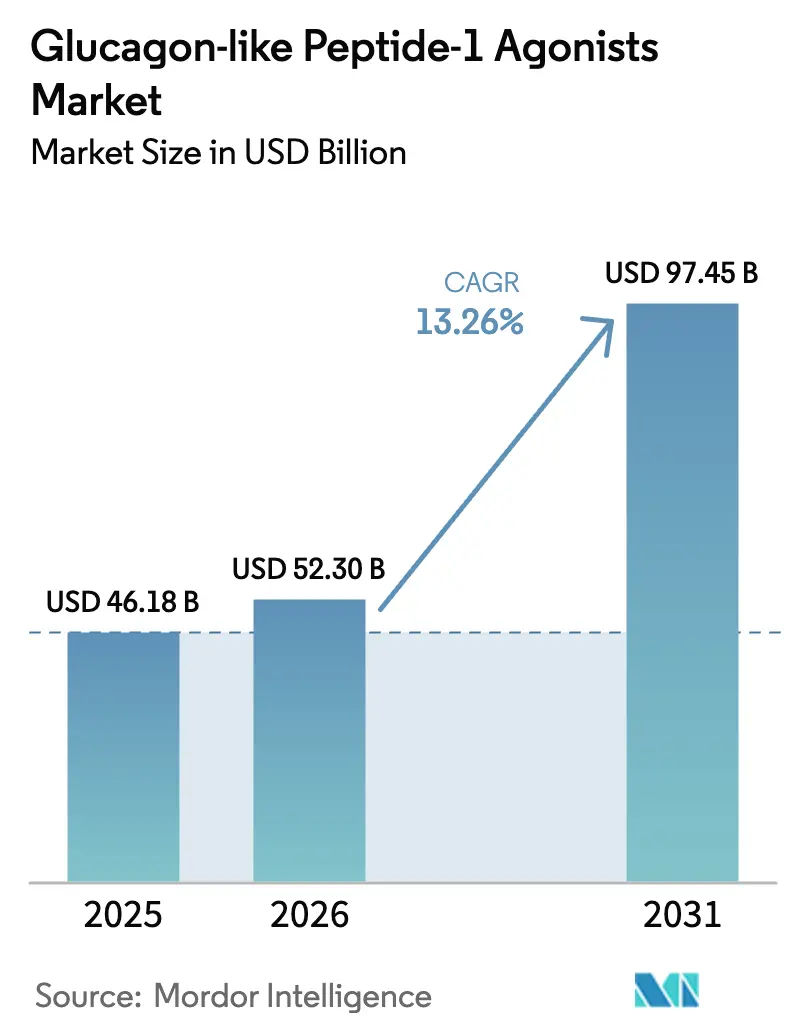

The Glucagon-like Peptide-1 Agonists Market size is expected to grow from USD 46.18 billion in 2025 to USD 52.30 billion in 2026 and is forecast to reach USD 97.45 billion by 2031 at 13.26% CAGR over 2026-2031.

This growth trajectory is propelled by extensive label expansions, expanding payer coverage, and broadening clinical-guideline endorsements that position glucagon-like peptide-1 (GLP-1) agonists as first-line or early combination choices in diabetes, obesity, and cardiovascular risk reduction. Rapid manufacturing scale-ups by incumbent leaders, coupled with ongoing investments by contract manufacturers, are improving product availability and lowering cost of goods, which is critical for emerging-market penetration. Meanwhile, formulary negotiations tied to the U.S. Inflation Reduction Act are poised to compress average selling prices yet simultaneously widen access to millions of Medicare beneficiaries. Biosimilar applications already filed in China, India, and Europe hint at mid-to-late-decade competitive pressure, but originators retain exclusivity around key once-weekly and oral formulations that will support premium pricing in the near term.

Key Report Takeaways

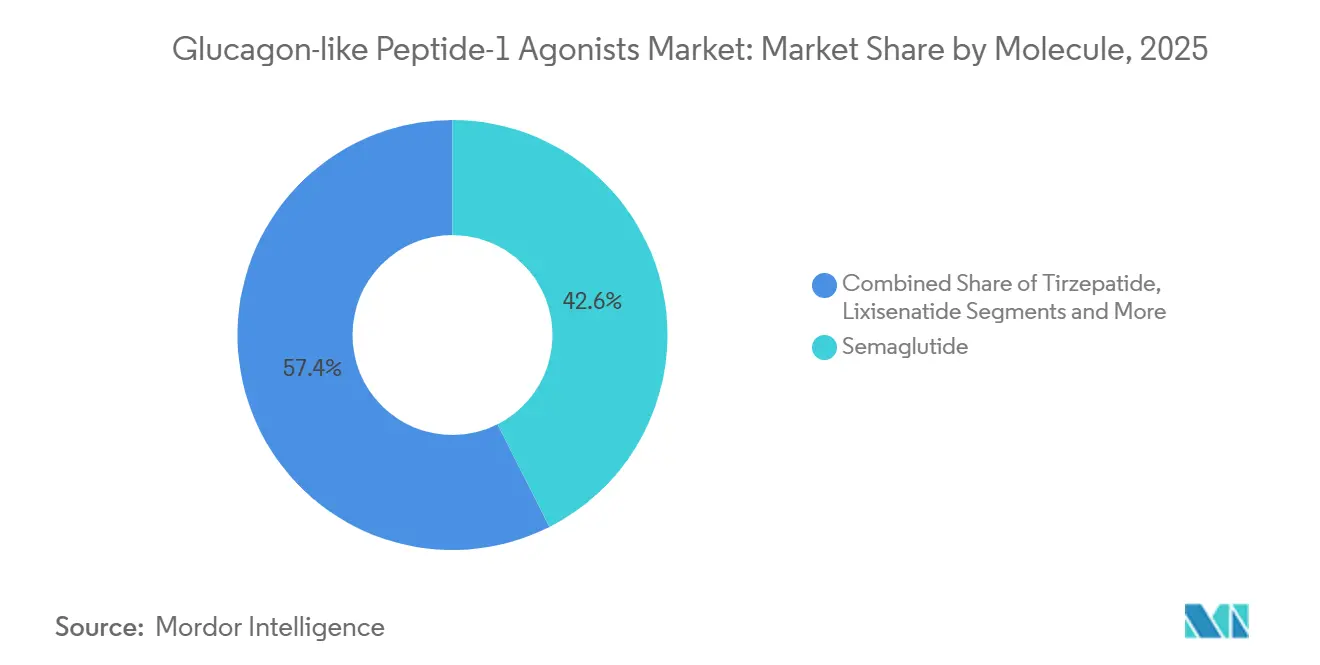

- By molecule, semaglutide led with 42.56% of glucagon-like peptide-1 agonists market share in 2025, while tirzepatide is advancing at a 25.25% CAGR through 2031.

- By route of administration, weekly injectables held 65.53% of the glucagon-like peptide-1 agonists market size in 2025; oral small-molecule formulations are expanding at a 28.85% CAGR to 2031.

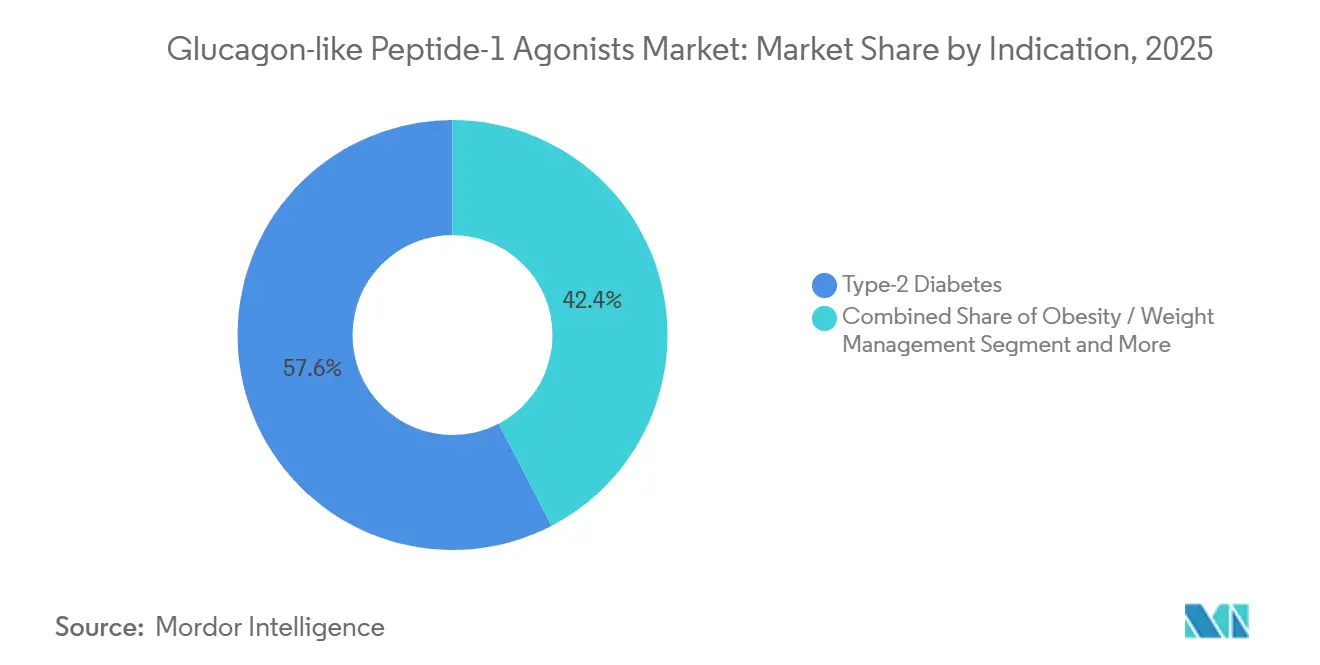

- By indication, type-2 diabetes generated 57.63% of 2025 revenue, whereas obesity prescriptions are expected to rise at a 30.87% CAGR between 2026 and 2031.

- By geography, North America contributed 41.13% of 2025 global revenue, yet Asia-Pacific is projected to lead growth at an 18.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Glucagon-like Peptide-1 Agonists Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of type-2 diabetes | +2.1% | Global, highest burden in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Escalating obesity epidemic and weight-loss approvals | +3.8% | North America and Europe lead, emerging in APAC urban centers | Medium term (2-4 years) |

| Physician shift to once-weekly GLP-1s | +1.9% | Global, accelerated in North America and Western Europe | Short term (≤ 2 years) |

| Reimbursement and guideline expansion | +2.4% | North America and EU, gradual in APAC and LATAM | Medium term (2-4 years) |

| Cardiometabolic-outcomes data broadening access | +2.0% | Global, early uptake in North America and Europe | Long term (≥ 4 years) |

| Peptide manufacturing scale-up lowering COGS | +1.5% | Global supply chain, benefits all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Type-2 Diabetes

International Diabetes Federation projections show diabetes cases climbing from 537 million in 2021 to 783 million by 2045, with 90% classified as type-2[1]International Diabetes Federation, “IDF Diabetes Atlas, 10th Edition,” diabetesatlas.org. Incidence is accelerating fastest across urbanizing Asia-Pacific economies, where lifestyle changes and aging populations converge. China alone documented a 12.4% adult prevalence in 2024, translating into more than 140 million individuals who often remain undertreated. The American Diabetes Association upgraded GLP-1 agonists to preferred second-line agents for patients with cardiovascular comorbidities in its 2024 Standards of Care, elevating the drug class above sulfonylureas and DPP-4 inhibitors for many clinical scenarios. As payers shift toward value-based models, the capacity of GLP-1 agonists to reduce microvascular and macrovascular complications strengthens formulary support, boosting the glucagon-like peptide-1 (GLP-1) agonists market well into the next decade.

Escalating Obesity Epidemic and Weight-Loss Approvals

World Health Organization data confirm that worldwide obesity prevalence nearly tripled between 1975 and 2024, affecting more than 890 million adults. Regulatory momentum is matching the epidemiologic urgency. Eli Lilly’s tirzepatide gained FDA clearance for chronic weight management in late 2023, followed by European approval in early 2024, breaking Wegovy’s early monopoly. In pivotal SURMOUNT-1 data, tirzepatide produced a 20.9% mean weight reduction, outperforming semaglutide’s 14.9% STEP-1 result. The FDA endorsement of semaglutide for obstructive sleep apnea in 2025 further widened the eligible population, encouraging Medicare Advantage plans to drop previous exclusions. Collectively these approvals have catalyzed a surge of obesity prescriptions that now form the single fastest-growing revenue stream inside the glucagon-like peptide-1 (GLP-1) agonists market.

Physician Shift to Once-Weekly GLP-1s

Real-world data show weekly formulations improve persistence by 28% compared with daily injections, translating to superior glycemic and weight outcomes. Prescription volume for semaglutide (Ozempic) climbed 35% year on year in the United States during 2024, largely due to migration from daily agents. Payers reinforce the shift through tier placement that favors once-weekly options, recognizing downstream cost savings. The GLP-1 agonists market therefore continues to tilt toward long-acting injectables, anchoring semaglutide and tirzepatide at the forefront while relegating older daily products to niche status.

Reimbursement and Guideline Expansion

The Centers for Medicare & Medicaid Services mandated that Part D formularies include at least two GLP-1 agonists per administration route from March 2024 onward, curbing historical exclusion practices. Commercial payers followed quickly; UnitedHealthcare eliminated step edits for eligible cardiovascular or renal-risk patients in May 2024. Clinical evidence such as the SELECT outcomes trial, which delivered a 20% reduction in major cardiovascular events among obese adults without diabetes, underpins these policy shifts. The resulting alignment between guidelines and reimbursement accelerates specialist and primary-care adoption, expanding the GLP-1 agonists market to previously untapped populations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost & limited obesity coverage | -2.7% | Global, most acute in emerging markets and U.S. self-pay segments | Medium term (2-4 years) |

| Gastrointestinal side effects & discontinuation | -1.8% | Global, with higher discontinuation in treatment-naïve populations | Short term (≤ 2 years) |

| Supply shortages & grey-market compounded products | -1.2% | North America primarily; spillover to Europe and APAC | Short term (≤ 2 years) |

| Incoming biosimilars after 2027 pressuring prices | -1.5% | Global, with earliest impact in Europe and Asia-Pacific; delayed in U.S. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost and Limited Obesity Coverage

Annual U.S. wholesale acquisition costs range from USD 13,000 to USD 16,000, leaving uninsured and Medicare beneficiaries without diabetes exposed to full list prices[2]Kaiser Family Foundation, “Employer Health Benefits Survey 2024,” kff.org. Only 38% of employer plans covered anti-obesity drugs in 2024; even then, prior authorizations and spending caps remain common. Novo Nordisk’s savings card caps Wegovy copays at USD 500 but does not address the 65-plus population excluded by statute. Across India, median household income of USD 2,400 renders branded GLP-1 therapy out of reach, steering demand toward forthcoming biosimilars. Thus pricing and coverage barriers temper overall GLP-1 agonists market expansion, particularly in obesity-only indications.

Gastro-Intestinal Side Effects and Discontinuation

Real-world data covering 200,000 patients show 42% reporting at least one gastrointestinal event within three months of therapy initiation, with 15% discontinuation by year one. The FDA added a boxed warning to tirzepatide in June 2024, spotlighting severe gastroparesis risk but noting benefits outweigh harms. Dose titration, concurrent antiemetics, and next-generation co-formulations aim to mitigate symptoms, yet side-effect-driven drop-outs continue to moderate real-world uptake, shaving incremental points off the GLP-1 agonists market CAGR in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecule: Tirzepatide Narrows Semaglutide’s Lead

Semaglutide generated 42.56% of 2025 revenue, anchoring the glucagon-like peptide-1 agonists market through its dual diabetes-obesity branding and extensive outcomes data. Tirzepatide’s 25.25% CAGR to 2031 reflects dual GIP/GLP-1 agonism that delivers larger HbA1c and weight reductions, bolstered by Lilly’s discounting strategy that undercuts Wegovy list prices. The GLP-1 agonists market size for tirzepatide could reach USD 38 billion by 2031 if current trial data readouts remain positive and capacity expansions stay on schedule. Dulaglutide and liraglutide are sliding into twilight phases as payer formularies migrate toward higher-efficacy weekly drugs. Meanwhile, retatrutide’s early-stage data suggest even greater weight-loss potential, indicating a pipeline that could further reshape molecule-level rankings within the GLP-1 agonists market.

Second-generation agents exenatide and lixisenatide now serve price-sensitive geographies or patients intolerant to stronger compounds. Biosimilar liraglutide filings in China and India may pressure pricing in value segments, but are unlikely to displace branded products in premium markets that demand proven outcomes data. As a result, the GLP-1 agonists industry remains a two-player race at the molecule level, with semaglutide and tirzepatide setting efficacy benchmarks that newer entrants must match or exceed.

By Route of Administration: Oral Formulations Gain Momentum

Weekly injectables held 65.53% of 2025 revenue, reflecting physician comfort and patient familiarity. Oral semaglutide’s 48% sales growth during 2024 proved primary-care appetite for non-injectable incretins, especially among injection-averse or newly diagnosed patients. The glucagon-like peptide-1 agonists market share for oral products remains modest today, yet pipeline candidates such as GSBR-1290 and danuglipron aim to match injectable efficacy without requiring absorption enhancers. If successful, oral entrants could capture double-digit market share by decade-end, providing a potent convenience advantage.

Daily injectable formats are rapidly contracting. Saxenda prescriptions declined 12% year on year as obesity prescribers pivoted to once-weekly options, illustrating how dosing frequency shapes patient preference. Longer-acting monthly injectables like maridebart cafraglutide are in Phase 2 development and, if approved, could further tilt adherence benefits toward ultra-long-acting regimens, ultimately enlarging the GLP-1 agonists market size in maintenance therapy segments.

By Indication: Obesity Surges Past Diabetes Growth

While type-2 diabetes still produced 57.63% of 2025 sales, obesity prescriptions are advancing at a 30.87% CAGR through 2031. This fast climb owes to broader societal focus on weight management and payer realization that sustained weight loss lowers downstream cardiovascular costs. The glucagon-like peptide-1 agonists market size tied to obesity could eclipse USD 50 billion by 2031 at current acceleration rates. Cardiovascular prevention now forms a third revenue pillar after the 2024 FDA approval enabling semaglutide use in overweight adults with heart disease. New sleep apnea and potential NASH indications further widen therapeutic reach, ensuring multi-specialty penetration that deepens prescriber pool and increases lifetime patient value.

Durability data from SURMOUNT-3 indicate tirzepatide maintains weight loss beyond initial lifestyle interventions, fueling payer confidence in long-term cost offsets. As wider cholesterol-lowering, renal-protection, and potentially cognitive benefits emerge, indication stacking will keep the glucagon-like peptide-1 (GLP-1) agonists market on an upward revenue slope even as individual categories mature.

Geography Analysis

North America maintained 41.13% of 2025 revenue, supported by early approvals, high prevalence of obesity, and premium pricing. Adoption has now moved from specialist to primary-care settings, yet unit growth is plateauing as coverage widens and competition intensifies. Inflation Reduction Act price negotiations, effective 2027, will reduce average selling price but boost volume, providing net positive revenue stability for the glucagon-like peptide-1 (GLP-1) agonists market in the region.

Europe accounted for 28% of global sales in 2025. Centralized approvals speed multinational launches, but national cost-effectiveness reviews temper revenue per patient. Germany’s positive benefit rating for tirzepatide enabled higher negotiated pricing, whereas the United Kingdom’s narrower BMI eligibility dampens total addressable population. Continued reimbursement expansion tied to cardiovascular and renal outcomes is likely to drive mid-single-digit volume growth, preserving Europe as a solid, though mature, profit pool.

Asia-Pacific, recording the fastest 18.81% CAGR, is set to shift the global revenue mix as China, Japan, and India unlock large patient cohorts. China’s late-2024 tirzepatide approval and accompanying USD 1 billion local manufacturing commitment highlight strategic focus on domestic capacity that supports rapid volume ramp-up[3]National Medical Products Administration, “Tirzepatide Approval for Type 2 Diabetes,” nmpa.gov.cn. Japan’s first-in-class obesity approval in early 2024 delivered strong initial uptake; local insurers are now reevaluating reimbursement ceilings, which should foster sustained growth. As regional governments confront soaring cardiometabolic disease costs, broader subsidization is expected, advancing the glucagon-like peptide-1 (GLP-1) agonists market toward leadership status in Asia-Pacific by the early 2030s.

Regulatory Landscape

Regulation for GLP-1 agonists is tightening around product quality, lawful supply, and label governance as demand expands across diabetes and obesity. In the United States, the FDA shifted from shortage-era flexibility toward enforcement in 2026, including a February 2026 announcement to restrict use of non-FDA-approved GLP-1 active pharmaceutical ingredients in compounded products and an April 2026 clarification of compounding policies under sections 503A and 503B as national supply began stabilizing. The FDA also requested removal of suicidal ideation and behavior labeling language for GLP-1 receptor agonists in April 2026 following a comprehensive review, reflecting how post-market safety evaluation continues to shape prescribing confidence.

In Europe, centralized review continues to move line extensions and new formats forward while providing a clearer pathway for follow-on products. In May 2026, EMA's CHMP issued a positive opinion recommending marketing authorization for an oral semaglutide formulation (Wegovy tablets) for weight management, reinforcing regulatory support for oral delivery platforms. The same month, CHMP issued a positive opinion for Ablymico (a hybrid medicine of liraglutide) from STADA Arzneimittel AG, indicating maturing EU pathways for hybrid and biosimilar-like competition in first-generation molecules, alongside continued manufacturing-compliance scrutiny across global supply chains.

Competitive Landscape

Market concentration is high, with Novo Nordisk and Eli Lilly jointly capturing a significant percentage of global revenue in 2025. Both firms continue to invest heavily - Novo Nordisk in Kalundborg and North Carolina, Lilly across Indiana, North Carolina, and Wisconsin - expanding peptide synthesis and fill-finish capacity that fortify supply leadership. Sanofi, AstraZeneca, and Boehringer Ingelheim have exited or deprioritized their first-generation assets, effectively ceding share.

White-space innovation now concentrates on oral small molecules, ultra-long-acting injectables, and combination products. Structure Therapeutics and Pfizer are developing absorption-enhancer-free or twice-daily oral candidates aiming to expand convenience. Amgen’s monthly maridebart cafraglutide and Novo Nordisk’s fixed-dose CagriSema combination target superior efficacy without added injection frequency, signaling competitive dimensions will increasingly pivot on dosing simplicity and multi-pathway synergy.

Regional players in China and India, including Gan & Lee and Hengrui, are advancing biosimilar liraglutide and dulaglutide for 2026 launches. Their primary opportunity lies in local formularies and private cash-pay segments where cost barriers preclude branded agents. Given lingering exclusivity around once-weekly semaglutide and tirzepatide until at least 2031, the GLP-1 agonists industry will likely remain a duopoly in premium markets, with incremental erosion from value-tier competition rather than disruptive share shifts.

Glucagon-like Peptide-1 Agonists Industry Leaders

AstraZeneca

Eli Lilly and Company

Sanofi

Novo Nordisk A/S

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Oral GLP-1 formats are creating an expansion lane that links product innovation with manufacturing investments and regulatory progress. EMA's May 2026 CHMP positive opinion for Wegovy tablets provides a near-term European anchor for oral semaglutide commercialization, and Novo Nordisk followed the oral pivot with a March 2026 announcement of a 432 million euro expansion at its Athlone, Ireland facility specifically for oral GLP-1 treatments. Together, these moves support broader participation by payers and primary-care channels where injection aversion and adherence barriers have historically constrained uptake.

Manufacturing scale-up and localization are also a key whitespace enabler, especially in price-sensitive regions and for future value-tier competition. In March 2026, Neuland Laboratories announced plans for a peptide CMC facility in Bonthapally, India designed to produce GLP-1s with room for expansion, complementing originator-led investment and strengthening the API and intermediate supply base. At the same time, FDA actions in 2026 to restrict non-approved compounded GLP-1 APIs and clarify lawful compounding requirements concentrate demand back toward approved products and compliant supply chains, creating space for contract manufacturing, serialization and cold-chain services, and regulated follow-on competition focused on availability and cost of goods rather than grey-market substitutes.

Recent Industry Developments

- May 2026: Eli Lilly and Company announced an additional USD 4.5 billion investment across two of its three Lebanon, Indiana manufacturing sites, including an API facility plan tailored for producing the oral weight-loss drug orforglipron (Foundayo) and related scale-up needs. The commitment strengthens vertical integration for oral GLP-1 supply and addresses a key constraint in the market, reliable high-volume manufacturing capacity.

- March 2026: Novo Nordisk announced a 432 million euro investment to expand its manufacturing facility in Athlone, Ireland, to increase capacity for oral GLP-1 treatments. The expansion follows the industry shift toward non-injectable options and supports broader geographic supply resilience as demand expands beyond specialist-driven diabetes use into obesity and cardiometabolic indications.

- December 2025: The World Health Organization published its first global guideline on the use of GLP-1 receptor agonists and GIP/GLP-1 dual agonists for treating obesity in adults. By framing obesity as a chronic relapsing disease and addressing access considerations, the guideline supports incorporation of GLP-1 therapy into national chronic care pathways, which can influence reimbursement policy discussions across multiple regions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from GLP-1 receptor agonist therapies used in diabetes and weight management. We count it as sales value for branded, approved class products across the major regions in the study period.

Scope exclusions: We exclude non-GLP-1 drug classes, devices, and general obesity services that do not represent GLP-1 therapy revenues.

Segmentation Overview

- By Molecule

- Exenatide

- Liraglutide

- Dulaglutide

- Lixisenatide

- Semaglutide

- Tirzepatide

- Others

- By Route of Administration

- Daily Injectable

- Weekly Injectable

- Oral Small-Molecule

- Long-acting Monthly (Pipeline)

- By Indication

- Type-2 Diabetes

- Obesity / Weight Management

- Cardiovascular Risk Reduction

- Other Emerging Indications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market and to identify external signals that can be checked each time the model is refreshed. We relied on public sources such as CDC and NIH burden statistics, WHO diabetes and obesity indicators, OECD health spending tables, FDA drug approval and label information, and EMA public assessment reports to understand demand drivers and therapy availability.

On the supply and value side, we reviewed company filings and investor presentations to interpret therapy revenue direction. We also used reputable press and association websites to track policy and reimbursement moves. For normalization, we referenced paid subscriptions for company financials and intelligence, news and financials, and patent databases where they helped confirm timelines and product coverage. These examples are not exhaustive, and we also consulted other public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were completed with a mix of manufacturers, distributors, clinicians, payers, and subject matter experts who track diabetes and obesity prescribing and access. The respondent input was used to verify the treated patient pool direction, typical dosing persistence, price corridor movement, and the regional differences across APAC, EMEA, and the Americas. We then aligned assumptions where desk sources had gaps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 39% | EMEA: 30% |

| Smaller Players: 17% | Managers: 48% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the demand pool is reconstructed from diabetes and obesity prevalence, diagnosis and treatment rates, and the share of patients eligible for GLP-1 therapy under typical guideline and payer rules. Those patient counts are then translated into annual therapy volumes using dosing frequency patterns (daily versus weekly), persistence on therapy, and the expected product mix by region.

To keep the totals realistic, we corroborate the output with selective bottom-up approximations, such as sampled price per therapy course times estimated treated patients, plus channel and payer checks shared in interviews. Key model inputs include new indication and label expansion timing, route of administration split (injectable versus oral), reimbursement breadth, supply availability signals, and list price versus net price direction. For forecasting, we run scenario analysis around uptake speed, access constraints, and pricing pressure, and we adjust scenario weights using expert consensus from the primary conversations.

Data Validation & Update Cycle

Validation is done in steps so that large swings are questioned before figures are finalized. Outputs are compared with independent signals, including public epidemiology trends, regulatory milestones, and observed shifts in prescribing and coverage. We then reconcile variances back to one or two clear drivers.

If a major assumption moves, such as coverage expansion, supply constraints, or a step change in effective pricing, analysts re-contact sources to re-check the direction and timing. Reports are refreshed annually, and interim updates are done when material events occur. Before delivery, a final review pass is completed so clients receive the latest updated view of the market.

Mordor Intelligence's Glucagon Like Peptide 1 Agonists Market Size Compared Against Other Published Estimates

Published numbers for GLP-1 agonists do not always match because the year used, the included indications, and how prices are normalized can differ across studies, even when the drug class label looks the same. Differences also show up when one estimate leans more on list prices or longer forecast horizons, while another stays closer to near-term realized demand signals.

A refresh-led factor is how currency timing and price erosion or rebate assumptions are handled as the market shifts quickly. The checks used to confirm patient uptake and persistence can also move the total. In our case, annual refresh rules, consistent USD conversion timing, and a clear ASP logic tied to observed payer and channel signals keep Mordor Intelligence aligned to a repeatable demand pool rather than a single headline price point.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 46.18 B (2025) | |

| Global Consultancy A | USD 66.38 B (2025) | Often uses a broader value capture that can reflect higher assumed net pricing and faster weight management mix shift, which can lift the same-year total versus models that temper ASPs using payer access and persistence checks. |

| Industry Publisher B | USD 51.60 B (2024) | Uses a different base year and may apply alternative currency timing and category grouping under GLP-1 analogues, which can shift totals when the class is expanding and prices and volumes are moving within the year. |

The benchmark spread is mainly explained by base-year choice and how pricing is converted from list to effective levels when obesity demand accelerates. By keeping assumptions tied to clear treated-patient and dosing drivers, and then re-checking them during updates, the final view remains transparent and easier to reproduce.

Key Questions Answered in the Report

What is the forecast value of the GLP-1 agonists market in 2031?

The market is projected to reach USD 97.45 billion by 2031, reflecting a 13.26% CAGR.

Which molecule currently leads sales among GLP-1 therapies?

Semaglutide held 42.56% of 2025 revenue, maintaining lead status over other agents.

How fast is tirzepatide revenue expected to grow?

Tirzepatide is forecast to expand at a 25.25% CAGR through 2031, driven by superior weight-loss efficacy.

Which region will post the highest growth rate for GLP-1 therapies?

Asia-Pacific is projected to grow at an 18.81% CAGR, outpacing other regions due to rapid regulatory approvals and rising middle-class demand.

What are the main cost barriers for obesity patients seeking GLP-1 therapy?

High list prices, limited insurance coverage, and Medicare's statutory exclusion of weight-loss drugs restrict access for many obese adults.

When are biosimilars likely to enter premium GLP-1 markets?

Patent expirations after 2027 could allow biosimilar dulaglutide and liraglutide in the U.S. and Europe, but exclusivity for weekly semaglutide extends to 2031.

Page last updated on: