Fitness Platforms For The Disabled Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

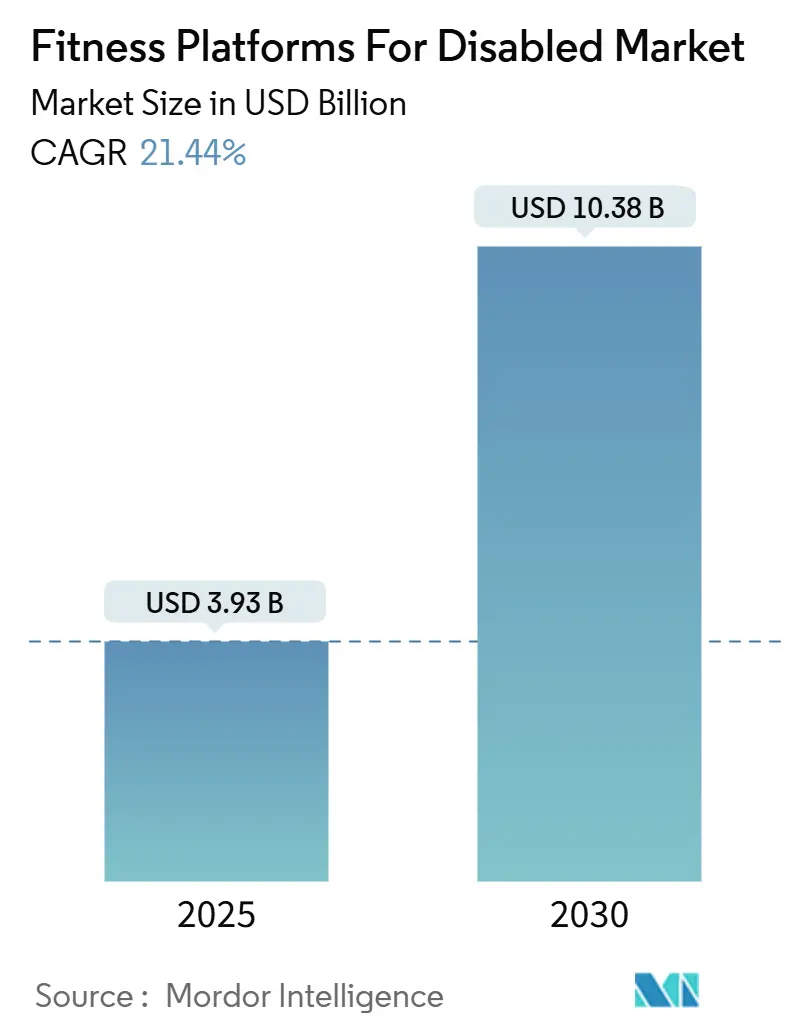

| Market Size (2025) | USD 3.93 Billion |

| Market Size (2030) | USD 10.38 Billion |

| Growth Rate (2025 - 2030) | 21.44% CAGR |

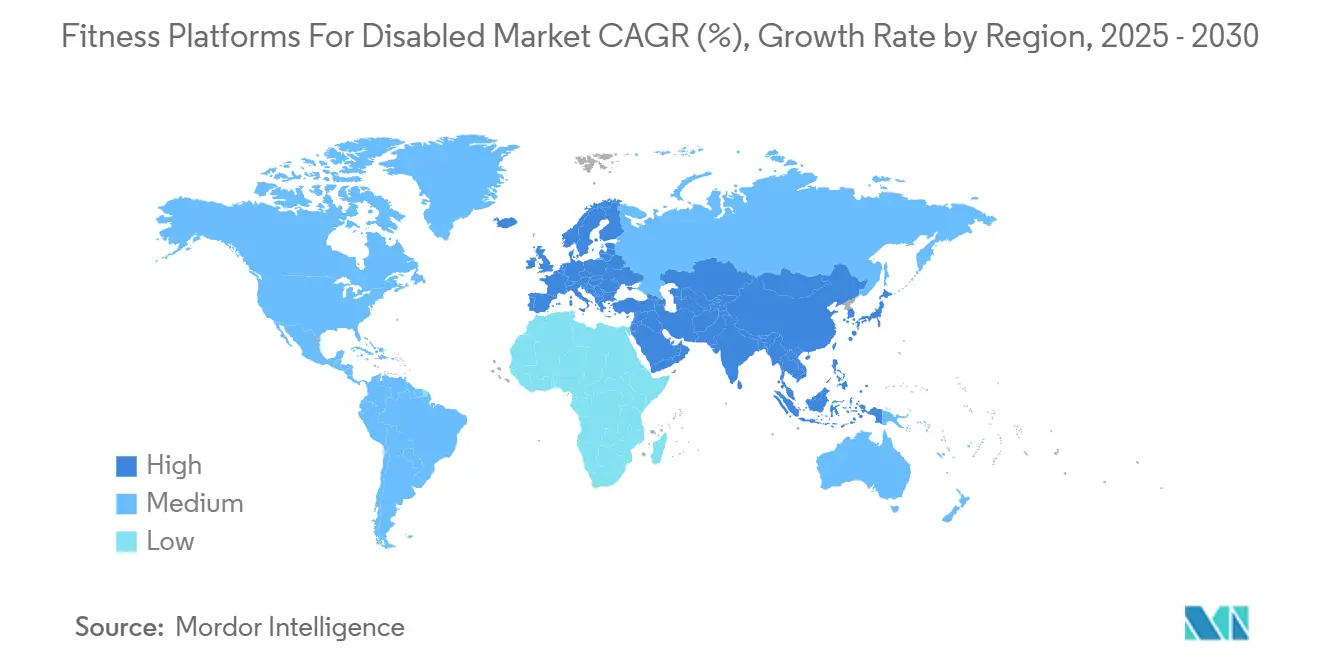

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fitness Platforms For The Disabled Market Analysis by Mordor Intelligence

The Fitness Platforms For The Disabled Market size reached USD 3.93 billion in 2025 and is forecast to advance at a 21.44% CAGR to USD 10.38 billion by 2030. Accelerated growth reflects strict digital-accessibility mandates, rapid innovation in adaptive interfaces, and expanding corporate diversity programs that now treat accessible wellness as a workforce imperative. AI-driven personalization engines are enabling unprecedented workout custom-tailoring, while haptic feedback and voice-controlled inputs are redefining user interaction patterns. Payer acceptance is rising as telerehabilitation studies continue to demonstrate measurable functional-recovery gains, encouraging insurers to reimburse digital interventions and thereby lowering out-of-pocket costs for disabled users. Cybersecurity readiness is emerging as a competitive differentiator because platforms that protect highly granular biometric data inspire greater user trust and brand loyalty.

Key Report Takeaways

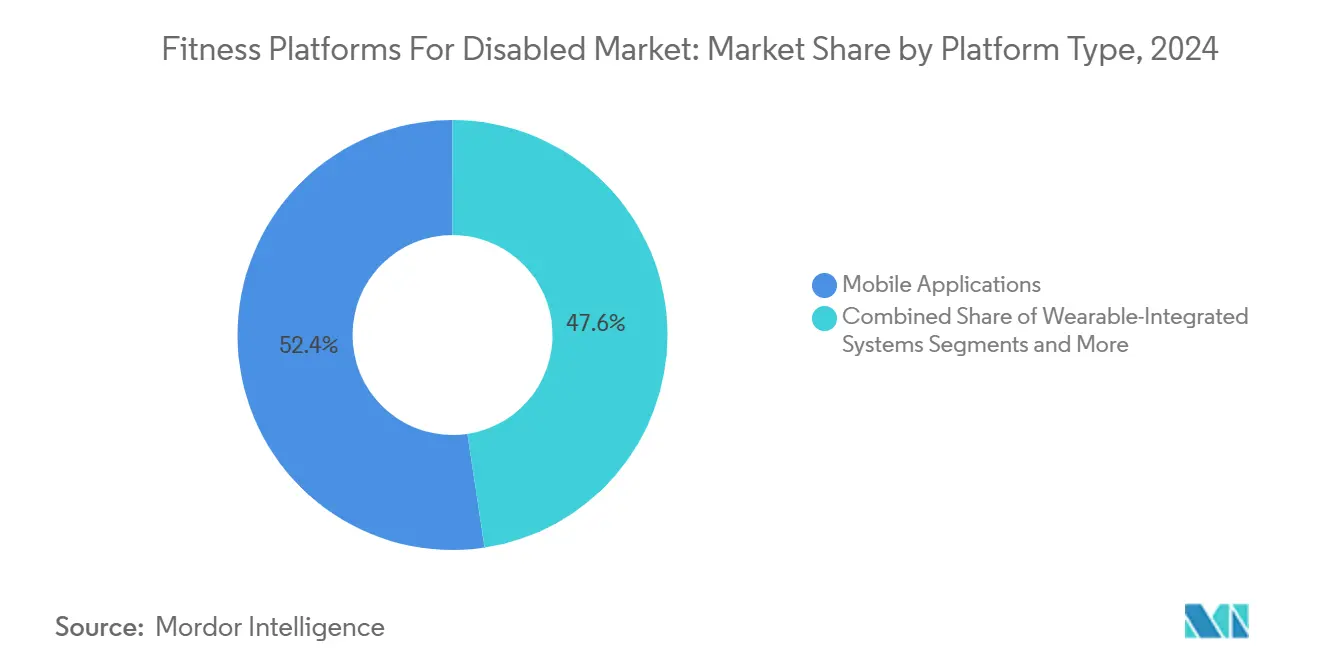

- By platform type, mobile applications captured 52.38% of revenue in 2024; virtual reality and immersive systems are projected to scale at a 25.56% CAGR to 2030.

- By disability type, physical disabilities accounted for 59.69% of the Fitness Platforms For The Disabled Market share in 2024, whereas cognitive-disability solutions are expanding at a 24.62% CAGR across the forecast window.

- By end user, individual consumers led with 57.36% of spending in 2024; corporate wellness and insurers are poised to grow at a 23.04% CAGR as diversity, equity, and inclusion mandates deepen.

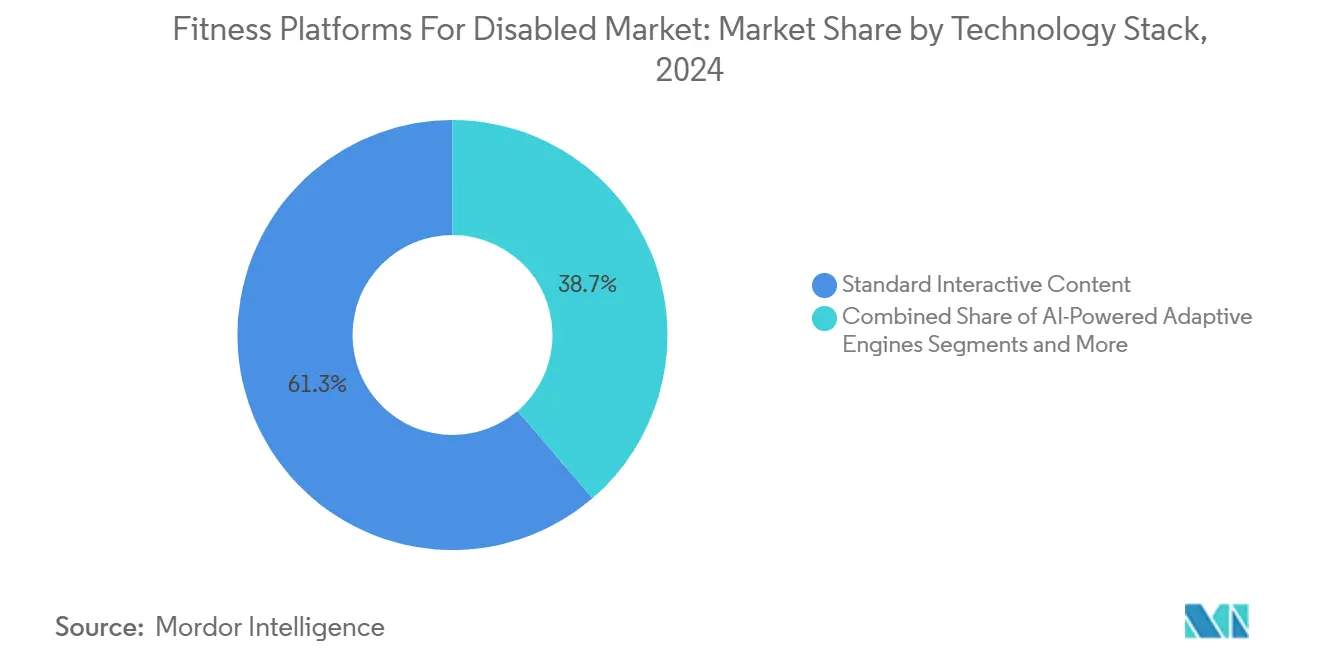

- By technology stack, standard interactive content represented 61.29% of the Fitness Platforms For The Disabled Market size in 2024, while AI-powered adaptive engines are advancing at a 25.78% CAGR through 2030.

- By revenue model, subscriptions delivered 46.28% of value in 2024; enterprise licensing is expected to post a 22.63% CAGR as B2B2C distribution gains momentum.

- Geographically, North America held 36.44% of the Fitness Platforms For The Disabled Market share in 2024, whereas Asia-Pacific is on track for a 24.39% CAGR led by robotics innovation and rapidly aging populations.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Fitness Platforms For The Disabled Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global disabled population with internet access | +4.2% | Global, strongest growth in emerging Asia-Pacific | Long term (≥ 4 years) |

| Expansion of virtual fitness and telerehabilitation | +3.8% | North America and EU first adopters; APAC catching up | Medium term (2-4 years) |

| Regulatory mandates on digital accessibility compliance | +3.1% | EU core, North America secondary, gradual APAC uptake | Short term (≤ 2 years) |

| Growing integration of adaptive wearables and IoT sensors | +2.9% | Developed economies initially; global diffusion later | Medium term (2-4 years) |

| Corporate DEI-driven wellness programs | +2.7% | North America and EU enterprises, selective APAC markets | Short term (≤ 2 years) |

| AI-driven hyper-personalized workout engines | +2.4% | Technology-advanced markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Disabled Population With Internet Access

Expanding broadband coverage and affordable smartphones are connecting millions of disabled individuals who previously lacked any remote rehabilitation options. Urban Indonesia illustrates this shift as more than 23 million residents with disabilities gain access to adaptive mobile apps that eliminate the need for costly in-person therapy. Higher engagement times recorded for disabled users indicate strong lifetime-value potential for platforms that integrate inclusive design from the outset. Rural deployments of telerehabilitation are becoming essential primary-care touchpoints, widening reach beyond traditional hospital networks. In parallel, community-level NGOs are forming referral partnerships that funnel first-time users toward subsidized subscription tiers, enlarging the total addressable base for the Fitness Platforms For The Disabled Market.

Expansion Of Virtual Fitness & Telerehabilitation Solutions

Clinical evidence keeps mounting in favor of telerehabilitation. A meta-analysis covering 1,577 hip-fracture patients confirmed superior functional independence scores when digital follow-up supplanted conventional care.[1]Xiao Huangyi et al., “Effectiveness of Telerehabilitation in Hip-Fracture Patients,” BMC Sports Science Medicine and Rehabilitation, biomedcentral.comStroke-rehabilitation VR programs now classify exercise motions with 93.4% accuracy, trimming therapist supervision needs by 40%.[2]Shiqi Xu, “Virtual-Reality Enhanced Training for Stroke Rehabilitation,” Journal of Medical Internet Research, jmir.org With reimbursement expanding, platforms that combine AI monitoring and licensed clinician oversight are able to command premium enterprise licensing fees, boosting profitability inside the Fitness Platforms For The Disabled Market. Beyond cost benefits, the always-on nature of remote sessions is encouraging more consistent patient adherence, translating into better outcomes and higher payer willingness to cover digital modalities.

Regulatory Mandates On Digital Accessibility Compliance

The European Accessibility Act that went live in June 2025 compels any fitness software distributed in the bloc to meet strict perceivability, operability, understandability, and robustness tests. U.S. enforcement of the Americans with Disabilities Act is extending to digital platforms, exemplified by Department of Justice actions against non-compliant chain gyms. Early movers are investing in WCAG 2.2-aligned redesigns, thereby reducing future legal exposure and enhancing brand equity. Smaller competitors lacking capital for rapid compliance upgrades risk market exit, which could spur consolidation inside the fitness platforms for disabled industry over the next 24 months. Harmonizing standards is also lowering development costs because a single compliant codebase can be rolled out across multiple jurisdictions.

Growing Integration Of Adaptive Wearables & IoT Sensors

Next-generation sensors can now capture nuanced biomechanical and physiological data that traditional trackers missed. Northwestern University researchers produced a haptic interface that recreates directional touch, enabling blind athletes to navigate immersive workouts with confidence.[3]Northwestern University News Staff, “Feeling the Future: New Wearable Tech Simulates Realistic Touch,” Science Daily, sciencedaily.comKAIST engineers eliminated sweat-induced noise in electromyography signals, allowing accurate muscle monitoring during intense sessions. Smart garments developed at Cornell University achieve 93.4% posture-tracking accuracy and survive repeated wash cycles. These breakthroughs let platforms tailor exercises to dynamic ability levels, elevating user retention and subscription upsell rates across the Fitness Platforms For The Disabled Market.

Restraints Impact Analysis of Fitness Platforms For The Disabled Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordability and digital-literacy gaps | -2.8% | Global, sharper in emerging and rural locales | Long term (≥ 4 years) |

| Lack of unified accessibility standards | -2.1% | Worldwide, fragmented regulatory landscape | Medium term (2-4 years) |

| Biometric data-privacy and cybersecurity concerns | -1.9% | EU and North America first, spreading globally | Short term (≤ 2 years) |

| Limited reimbursement pathways | -1.7% | Primarily North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Affordability & Digital-Literacy Gaps Among Disabled Users

Lower-income households where disability prevalence is high often struggle to justify premium subscription costs. Older adults with disabilities face wider digital-literacy hurdles, increasing onboarding expenses for platform providers. Advertiser reluctance to target small, specialized demographics weakens freemium economics, limiting free-tier availability. Disability benefits formulas differ by country, complicating pricing strategies and potentially delaying mass penetration for the Fitness Platforms For The Disabled Market. Some providers are experimenting with micro-payments and NGO sponsorships to widen access, but scale remains elusive.

Biometric Data-Privacy & Cybersecurity Concerns

Granular health metrics collected by adaptive wearables escape Health Insurance Portability and Accountability Act protection in the United States, leaving a regulatory vacuum. In 2024, 93% of healthcare institutions suffered data breaches, and fitness apps are emerging as enticing targets. Disabled users often transmit more sensitive data—such as range-of-motion profiles and cardiac telemetry—raising the potential impact of a breach. Platforms that embed end-to-end encryption and transparent consent dashboards can offset these fears, but the extra safeguards inflate development budgets and lengthen release cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Fitness Platforms For The Disabled Market Segment Analysis

By Platform Type:

Mobile Apps Retain Scale, While VR Ignites New EngagementMobile applications captured 52.38% of the Fitness Platforms For The Disabled Market share in 2024 because smartphones remain the most ubiquitous digital gateway. A decade of operating-system accessibility upgrades—voice-control APIs, haptic shortcuts, and native screen readers—helped apps achieve near-universal baseline usability. Virtual-reality suites, although still nascent, are racing ahead at a 25.56% CAGR as headset prices fall and clinical validation grows. Projects like MotionBlocks allow users with limited mobility to remap VR game controls to individual capability spectra, reducing fatigue and elevating adherence.

Continued adoption of immersive systems is also being fueled by rehabilitation studies such as Osaka Metropolitan University’s Boccia XR program, which reports measurable improvements in hospital in-patients. Web-based portals accommodate users who prefer keyboard navigation and larger displays, while wearable-integrated ecosystems pair proprietary sensors with curated content to deliver closed-loop biofeedback. As 5G coverage deepens, multi-modal hybrids that hand off seamlessly between mobile, web, and VR contexts are likely to become the default experience across the wider Fitness Platforms For The Disabled Market.

By Disability Type:

Physical Needs Dominate Today as Cognitive Solutions Gain MomentumPhysical disabilities accounted for 59.69% of the Fitness Platforms For The Disabled Market size in 2024 thanks to well-established musculoskeletal therapy protocols and straightforward outcome tracking. Telerehabilitation frameworks—especially for stroke and orthopedic recovery—translate easily into digital content and have won early payer reimbursement. Cognitive-disability solutions, though smaller in absolute terms, are expanding at a 24.62% CAGR as AI coaches adapt in real time to attention spans and learning styles characteristic of ADHD and autism spectrum conditions.

Evidence continues to build: a recent randomized study showed VR stroke programs bolster upper-limb motor function when users receive more than 15 hours of exercises over six weeks. Meanwhile, the HELF tactile script is enabling deaf-blind athletes to decode coach instructions via vibration patterns, widening inclusivity beyond sight and sound. Multiple-disability users still face product gaps because designing for complex impairments requires costly modular architectures that few vendors can yet afford, underscoring an innovation opportunity within the fitness platforms for disabled industry.

By End User:

Consumer Subscriptions Lead; Corporate Wellness Shows Rapid UpsideIndividual subscribers contributed 57.36% of revenue in 2024, as many disabled users search for flexible home-based alternatives to crowded public gyms. Corporate wellness and insurer contracts, however, are climbing at a 23.04% CAGR, bolstered by high-profile inclusion pledges at Fortune 500 employers. UnitedHealth Group, for example, earned Disability Equality Index recognition after embedding accessible programming across its internal wellness suite.

Rehabilitation clinics and therapy centers leverage B2B2C white-label versions of top platforms to extend post-discharge care, while NGOs funnel grant funding to marginalized communities, acting as distribution partners in remote regions. Enterprises appreciate that disabled employees display higher engagement and lower churn when wellness solutions are accessible by default rather than retrofitted, a trend that should sustain growth across the Fitness Platforms For The Disabled Market.

By Technology Stack:

Standard Content Still Rules, Yet AI Engines Create DifferentiationStandard video-led workouts remained the entry point for 61.29% of users in 2024 because production costs are low and smartphone decoding is frictionless. AI-powered adaptive engines, though, are registering a 25.78% CAGR by continuously learning from sensor feedback and modifying routines in session. Sword Health’s Phoenix AI specialist has already logged 3 million interactions across 10,000 employers, demonstrating scalable clinical efficacy and cost savings.

Voice-command interfaces are particularly valuable for users with limited hand mobility or visual impairments; however, ambient-noise misrecognition still hampers high-intensity group classes. Haptic feedback wearables that convey real-time posture corrections are moving from laboratory prototypes to pilot deployments. Over the forecast horizon, platforms that integrate multi-sensor fusion—vision, electromyography, and ultrasound—could set new performance benchmarks inside the Fitness Platforms For The Disabled Market.

By Revenue Model:

Subscriptions Anchor Cash Flow While Enterprise Licensing AcceleratesSubscriptions accounted for 46.28% of 2024 receipts, favored for predictable monthly budgeting and frequent content refreshes. Enterprise licensing, projected to deliver a 22.63% CAGR, stands out for superior unit economics: multiyear corporate contracts often carry 3-5 times the lifetime value of a single retail subscription. Recent Medicare coverage for seven FDA-cleared digital therapeutics, including Big Health’s SleepioRx, formalizes reimbursement pathways and raises provider confidence.

Freemium models struggle under limited advertiser appetite, and pay-per-class options appeal mainly to users with episodic conditions. Outcome-based pricing—where fees escalate only after clinically validated improvements—could become an equitable compromise for public payers wary of upfront commitments, ultimately enlarging funding inflows to the Fitness Platforms For The Disabled Market.

Geography Analysis

North America Fitness Platforms For The Disabled Market

North America held 36.44% of the Fitness Platforms For The Disabled Market share in 2024, underpinned by strong Americans with Disabilities Act enforcement, mature telehealth infrastructure, and January 2025 Medicare reimbursement for certain digital therapeutics. U.S. payers are demanding pharmaceutical-grade evidence before extending coverage, prompting vendors to invest in randomized trials that prove cost offsets and functional gains. Canada’s provincial pilots integrate virtual rehab into universal healthcare, while Mexico’s rising middle-income population and high smartphone penetration open fertile territory for Spanish-language apps. Despite federal clarity, divergent state benefit structures complicate pricing and reimbursement strategies across the region, making local partnerships essential for scale.

Europe Fitness Platforms For The Disabled Market

Europe is racing ahead in regulatory cohesion after the European Accessibility Act unified digital standards across 27 member states in mid-2025. Germany’s inclusive social-insurance framework and vigorous disability-rights activism drive rapid adoption, whereas the United Kingdom mirrors EU norms via domestic statutes despite Brexit. France channels public grants into assistive-tech incubators, and Italy’s aging demographic accelerates demand for home-based therapy. The General Data Protection Regulation, while imposing higher compliance costs, also differentiates platforms that can engineer privacy-by-design, a feature highly valued by disabled users wary of data misuse.

APAC Fitness Platforms For The Disabled Market

Asia-Pacific is projected to deliver a 24.39% CAGR through 2030, propelled by advanced robotics in South Korea and elder-care programs in Japan. Korea’s WalkON Suit F1 exoskeleton lets paraplegic users strap in directly from wheelchairs, highlighting the region’s inventive edge. Japan-based Lifehub will commercialize a stair-climbing electric wheelchair by 2026, priced at 1.5 million yen (USD 11,700). China’s central government recently folded virtual rehab into its Healthy China 2030 agenda, and Australia’s National Disability Insurance Scheme subsidizes adaptive tech purchases. Diverse regulatory landscapes demand localized compliance roadmaps, yet the sheer volume of disabled consumers positions APAC as the growth frontier of the Fitness Platforms For The Disabled Market.

Competitive Landscape

Competition remains fragmented because deep disability-specific expertise is difficult to amass quickly. Sword Health’s narrow focus on musculoskeletal therapy demonstrates how specialization coupled with rigorous clinical trials can carve premium niches. Technology conglomerates leverage platform scale, bundling accessibility features into broader fitness suites, but they often lack the granular insights needed for complex impairments, giving smaller pioneers room to thrive. Voice-driven interfaces and haptic-feedback add-ons can lock users into proprietary ecosystems, heightening switching costs.

White spaces persist, especially in cognitive-disability and multi-impairment segments where clinical psychology and AI intersect. Several startups are filing patents for adaptive-workout algorithms that learn from individual motion signatures, as evidenced by University of Hong Kong-backed soft microelectronics enabling ultra-light wearable AI chips. Convergence with rehabilitation robotics blurs the line between medical devices and consumer wellness, yet regulatory hurdles slow time to market, deterring fast followers.

Strategic activity centers on three levers: 1) clinical-grade evidence generation to unlock reimbursement, 2) cross-border compliance frameworks that accelerate launches in multi-jurisdiction rollouts, and 3) privacy-first architectures to assuage data-sovereignty concerns. Mergers remain selective because platform owners prefer partnership models over outright acquisitions to preserve agility, but cost pressures linked to EAA and ADA compliance could tip smaller providers toward consolidation over the next two years inside the fitness platforms for disabled industry.

Fitness Platforms For The Disabled Industry Leaders

Kakana

Accessercise

SPIRIT Club

WheelWOD

Inclusive Fitness

- *Disclaimer: Major Players sorted in no particular order

Fitness Platforms For The Disabled Market Companies Covered in this Report

- Kakana

- Accessercise

- SPIRIT Club

- WheelWOD

- Inclusive Fitness

- Zuk Fitness

- ParaVida Sport

- Exero

- ParaPer4mance

- TruFit

- IncludeHealth

- AdaptX

- Able Digital Wellness

- Blue Run PWDs

- Assistfit

- Be Fit Be Able

- Move United

- WheelPower

- Active Adapt

- Access Sport Corp

Recent Industry Developments in Fitness Platforms For The Disabled Market

- July 2025: Dentsu Research Institute introduced DigSports Fraimo, an AI-based frailty-risk visualization tool for senior citizens that feeds municipal wellness dashboards.

- July 2025: Kokoromiru Co. renewed its deal with the Kanagawa Vanguards wheelchair-basketball team to supply Home Heart Dock pro ECG wearables for 24-hour monitoring.

- February 2025: GolfNavi signed an exclusive Japanese distribution agreement with RONFIC, a Korean AI-robotic fitness-machine producer optimized for Asian body structures.

Global Fitness Platforms For The Disabled Market Report Scope

Segmentation Overview

| Mobile Applications |

| Web-based Portals |

| Wearable-Integrated Systems |

| Virtual-Reality & Immersive Platforms |

| Physical Disabilities |

| Sensory Disabilities |

| Cognitive Disabilities |

| Multiple / Complex Disabilities |

| Individual Consumers (Home-based) |

| Rehabilitation & Therapy Centres |

| Corporate Wellness & Insurers |

| Community Organisations & NGOs |

| Standard Interactive Content |

| AI-Powered Adaptive Engines |

| Voice-Controlled Interfaces |

| Haptic Feedback & Sensor-Based Systems |

| Subscription-Based |

| Freemium / Ad-Supported |

| Pay-Per-Class |

| Enterprise Licensing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Platform Type | Mobile Applications | |

| Web-based Portals | ||

| Wearable-Integrated Systems | ||

| Virtual-Reality & Immersive Platforms | ||

| By Disability Type | Physical Disabilities | |

| Sensory Disabilities | ||

| Cognitive Disabilities | ||

| Multiple / Complex Disabilities | ||

| By End User | Individual Consumers (Home-based) | |

| Rehabilitation & Therapy Centres | ||

| Corporate Wellness & Insurers | ||

| Community Organisations & NGOs | ||

| By Technology Stack | Standard Interactive Content | |

| AI-Powered Adaptive Engines | ||

| Voice-Controlled Interfaces | ||

| Haptic Feedback & Sensor-Based Systems | ||

| By Revenue Model | Subscription-Based | |

| Freemium / Ad-Supported | ||

| Pay-Per-Class | ||

| Enterprise Licensing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global Fitness Platforms For The Disabled Market today?

The Fitness Platforms For The Disabled Market size reached USD 3.93 billion in 2025 and is projected to climb to USD 10.38 billion by 2030.

Which platform type generates the highest revenue?

Mobile applications led with 52.38% of 2024 revenue thanks to smartphone ubiquity and mature accessibility features.

What region will grow the fastest through 2030?

Asia-Pacific is expected to register a 24.39% CAGR as robotics innovation and aging-population policies drive adoption.

How are enterprises using these platforms?

Corporations are integrating accessible fitness apps into wellness programs, supporting a 23.04% CAGR in the corporate-wellness segment.

Why are AI-powered adaptive engines important?

They personalize workouts in real time, which improves clinical outcomes and fuels a 25.78% CAGR for this technology layer.

What is the biggest barrier to wider adoption?

Affordability and digital-literacy gaps among low-income and rural disabled users continue to restrain long-term growth.

Page last updated on: