Market Overview

| Study Period | 2020 - 2031 |

|---|---|

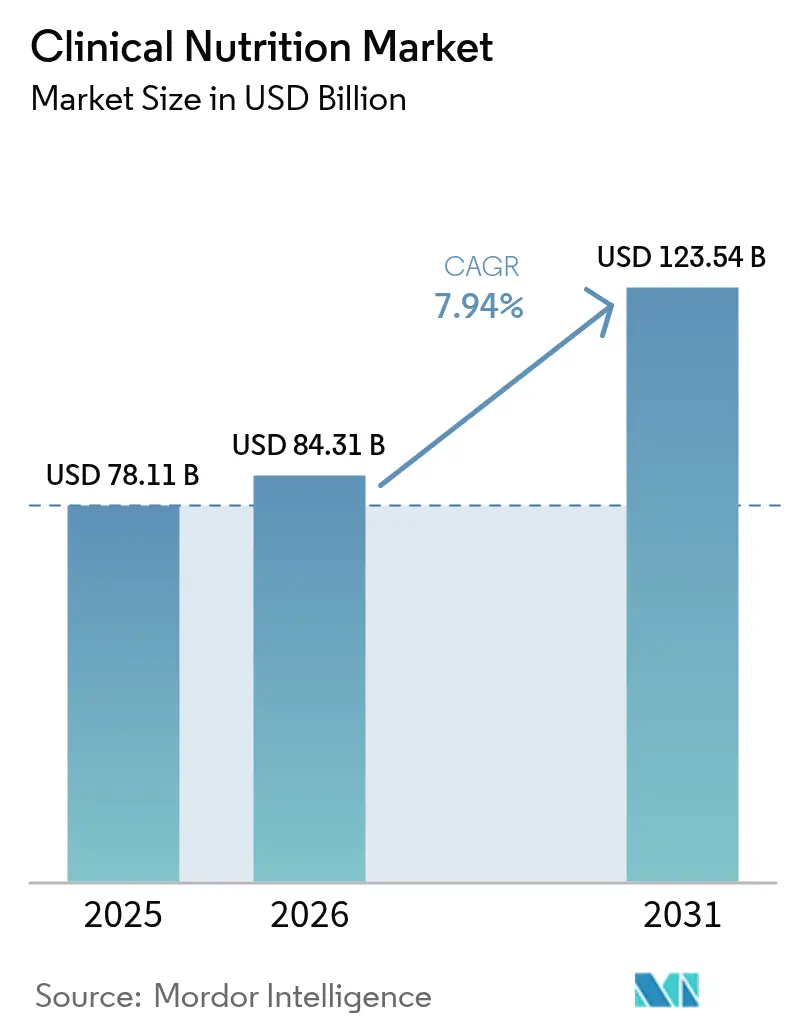

| Market Size (2026) | USD 84.31 Billion |

| Market Size (2031) | USD 123.54 Billion |

| Growth Rate (2026 - 2031) | 7.94% CAGR |

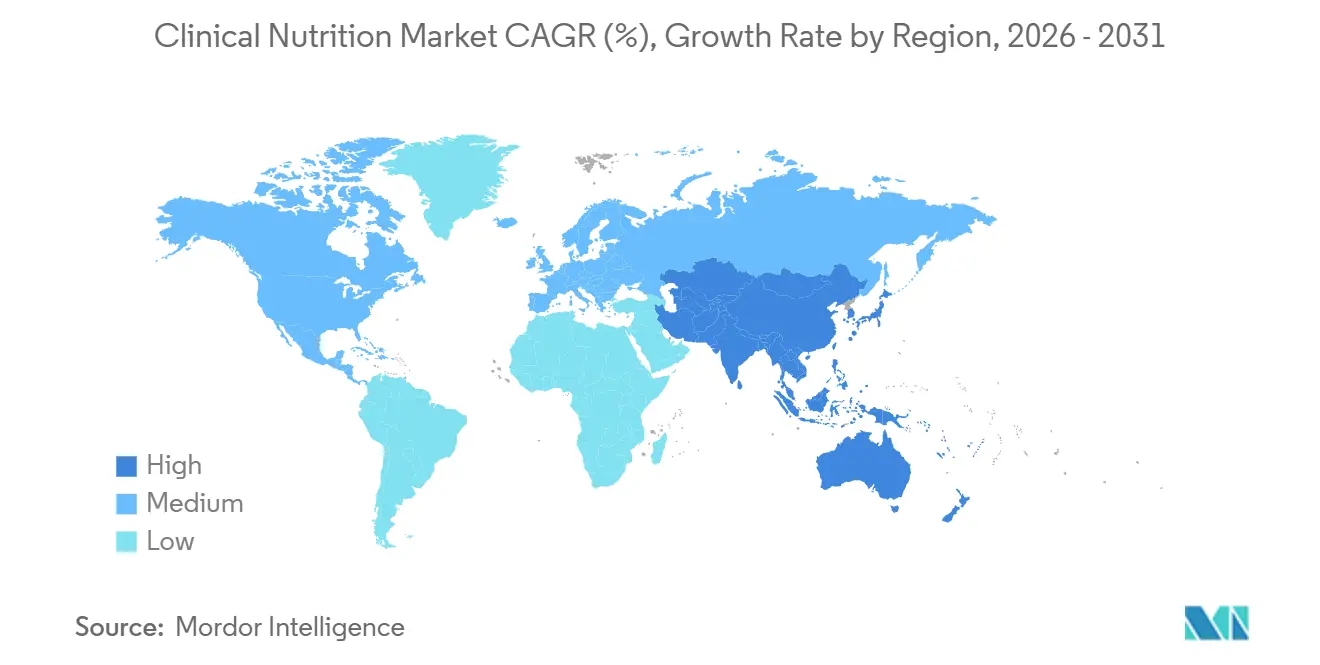

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

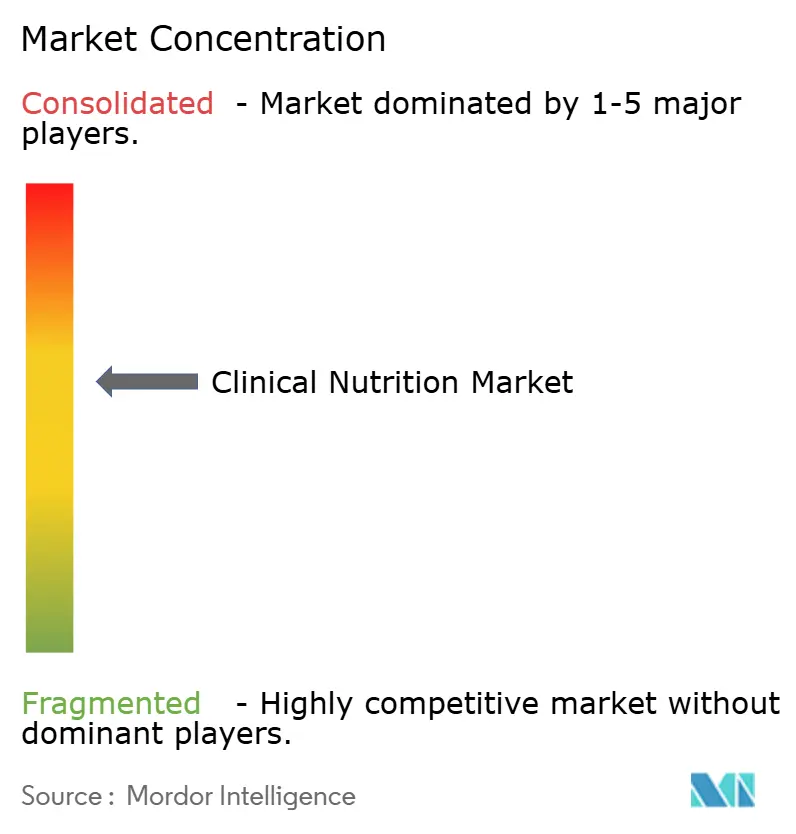

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Nutrition Market Analysis by Mordor Intelligence

The clinical nutrition market size in 2026 is estimated at USD 84.31 billion, growing from 2025 value of USD 78.11 billion with 2031 projections showing USD 123.54 billion, growing at 7.94% CAGR over 2026-2031. The rising prevalence of metabolic disorders like diabetes and dysphagia is boosting the clinical nutrition market. These specialized formulations meet the growing need for essential nutrients, aiding recovery and improving health outcomes. The geriatric segment is intersecting with the rapid expansion of clinical nutrition use in oncology. As cancer cases rise, the inclusion of dietitians in pre-admission planning becomes essential, as specialized formulas are gaining importance in multidisciplinary treatment pathways. This shift creates more opportunities for the manufacturers operating in the clinical nutrition market.

Key Report Takeaways

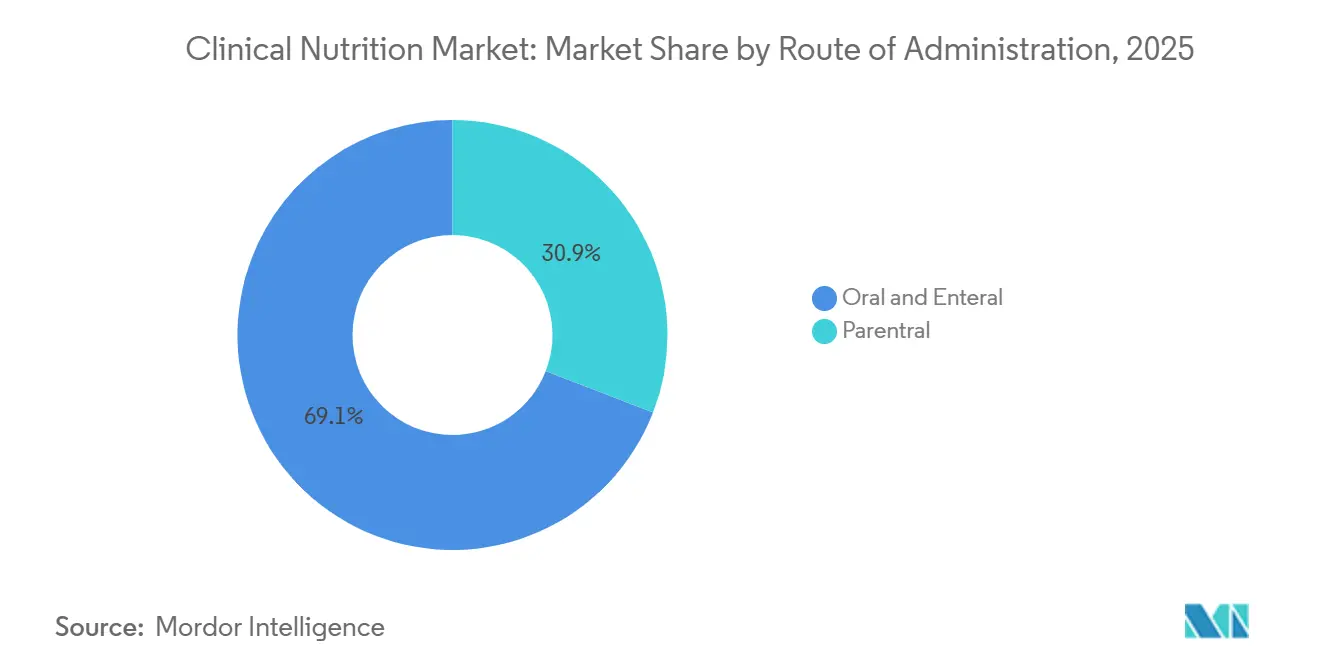

- By route of administration, enteral nutrition captured 69.15% of the clinical nutrition market share in 2025, while parenteral nutrition is projected to expand at an 8.42% CAGR through 2031.

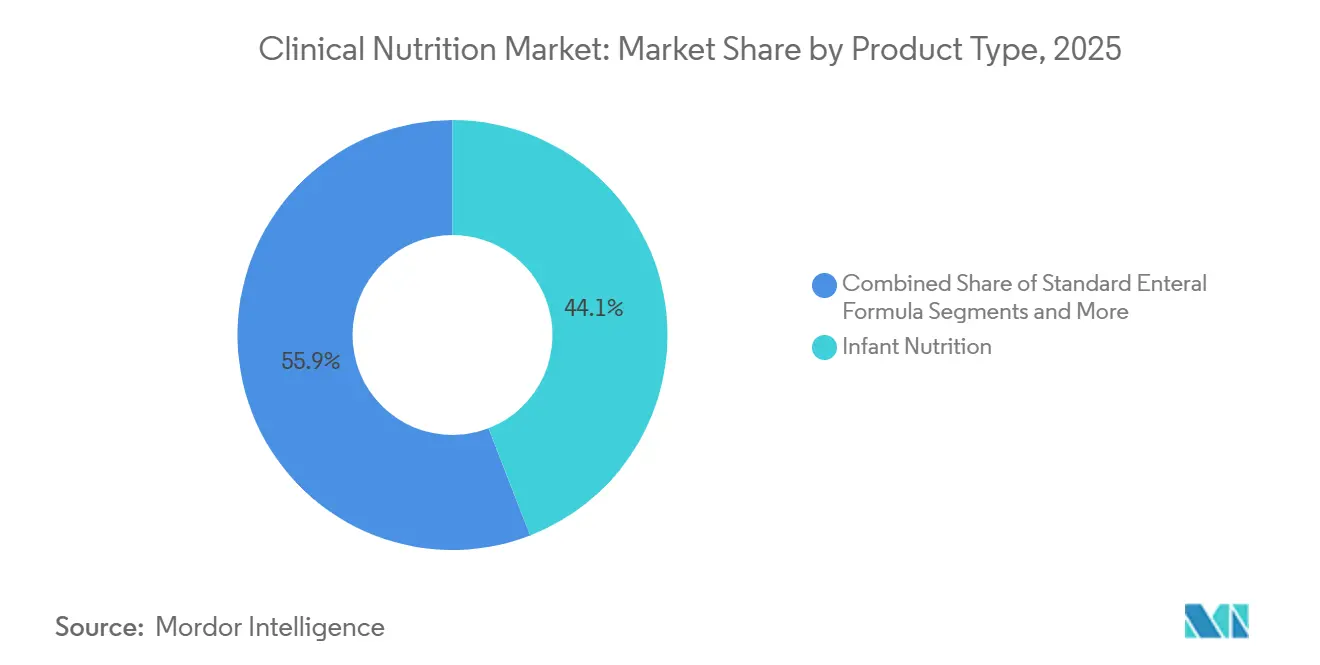

- By product type, infant nutrition products led with a 44.12% share in 2025; disease-specific enteral formulas are forecast to advance at a 8.98% CAGR to 2031.

- By form, liquid formulations accounted for 60.05% of 2025 revenue, and semi-solid products are projected to grow at an 8.52% CAGR through 2031.

- By application, malnutrition support represented 30.72% of the market size in 2025, whereas cancer-related nutrition solutions show the fastest momentum with a 8.97% CAGR during 2026-2031.

- By end user, adults accounted for 50.24% of demand in 2025, and the geriatric segment is expected to grow at a 9.16% CAGR through 2031.

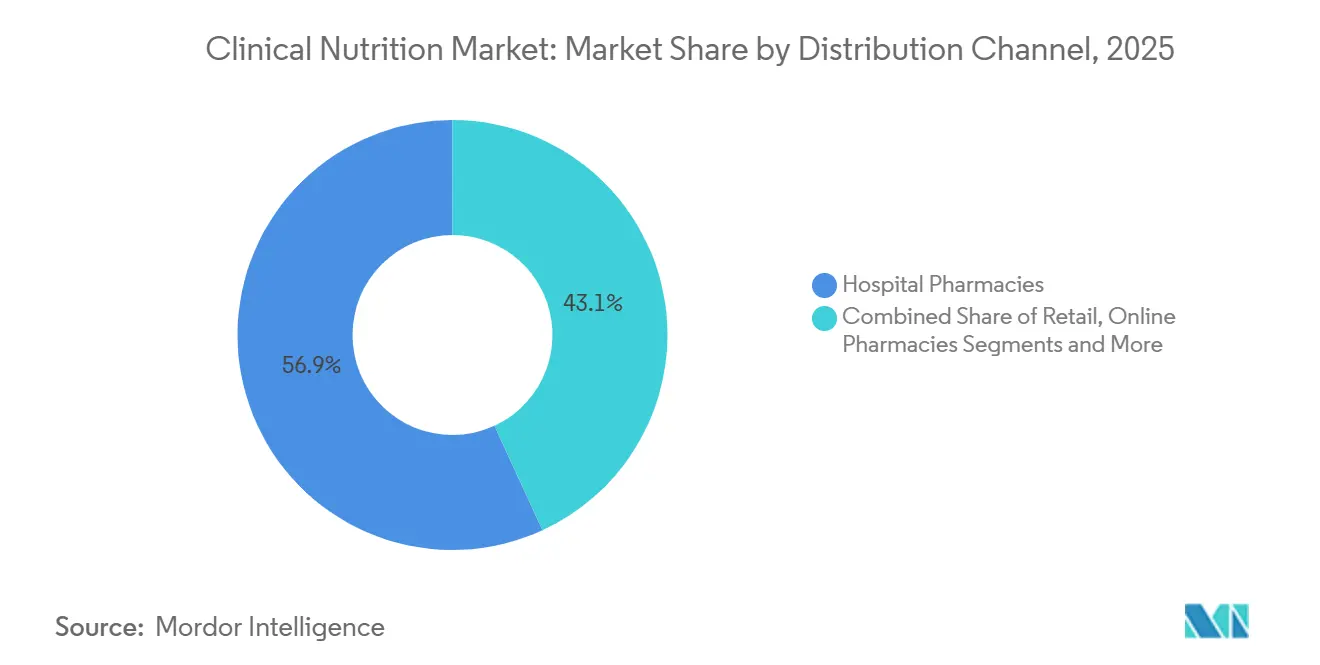

- By distribution channel, hospital pharmacies controlled 56.85% of sales in 2025, while online pharmacies are set to post a 9.95% CAGR through 2031.

- By geography, North America captured 34.55% of the market share in 2025, whereas the Asia-Pacific region holds the strongest growth outlook with an 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Clinical Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift Toward Home-Based Enteral Feeding in Post-Acute Care | +0.8 | North America & EU, early adoption in APAC metros | Short term (≤2 yrs) |

| Increased Adoption of Immunonutrition Formulas for Post-Surgery Recovery | +0.7 | Global | Medium term (~3-4 yrs) |

| Government-Funded Pediatric Malnutrition Programs | +0.5 | South Asia & Sub-Saharan Africa | Medium term (~3-4 yrs) |

| Increasing Prevalence of Chronic Disease | +1.0 | Global | Long term (≥5 yrs) |

| Bundled-Payment Reimbursement Incentives for Early Parenteral Nutrition | +0.4 | North America, selective EU payers | Short term (≤2 yrs) |

| Integration of AI-Enabled Nutrient Dosing Platforms in ICU Pharmacies | +0.6 | APAC core, spill-over to MEA | Medium term (~3-4 yrs) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Home-Based Enteral Feeding in Post-Acute Care

Efforts by hospitals to shorten patient stays without compromising care quality are reshaping post-acute care, steering it towards home enteral nutrition. For example, a December 2024 article in BMC Surgery examined how different energy levels in supplementary parenteral nutrition (SPN) affect recovery for gastric cancer surgery patients. The findings linked energy intake to recovery speed, complication rates, and overall health, offering valuable insights for refining nutritional strategies in cancer treatment. This study highlights opportunities for the clinical nutrition market to develop and offer personalized nutritional solutions that improve patient recovery and outcomes. As a result, there's a heightened demand for innovative nutritional products and services, especially in cancer care.

Increased Adoption of Immunonutrition Formulas for Post-Surgery Recovery

A December 2023 study in the Journal of Surgery[1]Arved Weimann et al., “ESPEN Practical Guideline: Clinical Nutrition in Surgery,” Clinical Nutrition, espen.orghighlights that perioperative blends with arginine, glutamine, and omega-3 fatty acids reduce complications after major abdominal surgeries. Hospitals are now using automated prompts in electronic admission checklists to ensure timely use, making nutritional products as essential as antibiotic prophylaxis. This shift is boosting demand in the clinical nutrition market, as procurement officers link product access to clinical outcomes. Suppliers are co-funding surgery registries to gather real-world data, speeding up evidence generation and driving market growth without relying on lengthy randomized trials.

Government-Funded Pediatric Malnutrition Programs

The World Bank has highlighted the urgent need for an annual investment of an additional USD 13 billion over the next decade to scale up childhood nutrition interventions and avert millions of potential deaths. This long-term commitment has prompted manufacturers to secure forward contracts on essential commodities, thereby mitigating risks associated with price fluctuations. UNICEF, wielding significant influence, procures about 75% of the globe's ready-to-use therapeutic food (RUTF). This dominance not only guarantees suppliers a stable baseline demand but also allows them to optimize production runs for enhanced efficiency. Recognizing the immense returns on investment, ministries of finance are increasingly reallocating nutrition budgets. With every dollar invested in nutrition promising over twentyfold returns in future productivity, these budgets are transitioning from mere social-sector allocations to pivotal economic-development line items, thus insulating them from periodic austerity reviews.

Increasing Prevalence of Chronic Disease

As the incidence of conditions such as diabetes, cardiovascular disorders, obesity, and gastrointestinal diseases continues to rise globally, the demand for specialized nutritional therapies and interventions has surged. Healthcare providers are increasingly recognizing the vital role of clinical nutrition in managing and preventing these chronic conditions, leading to a heightened adoption of targeted nutritional products and services. According to the World Health Organization (WHO), chronic diseases account for approximately 71% of all global deaths, equating to over 41 million people annually. The rising incidence of such diseases is attributed to factors including sedentary lifestyles, unhealthy dietary habits, aging populations, and urbanization. This trend underscores the critical importance of personalized nutrition strategies in improving patient outcomes, thereby fueling innovation and expansion within the clinical nutrition sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Requirements and Lengthy Approval Processes | −0.9 | Global | Medium term (~3-4 yrs) |

| Limited Insurance Coverage for Out-of-Hospital Parenteral Nutrition | −0.6 | United States | Short term (≤2 yrs) |

| Frequent Supply Shortages of Sterile Lipid Emulsions | −0.4 | North America & EU | Short term (≤2 yrs) |

| Rising Raw-Material Prices for Medical-Grade Maltodextrin | −0.5 | Global | Medium term (~3-4 yrs) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Requirements and Lengthy Approval Processes

Novel clinical nutrition products must meet extensive safety and efficacy standards set by the U.S. Food and Drug Administration, with the European Food Safety Authority imposing similarly rigorous benchmarks. Assembling a submission-ready file is capital-intensive, prompting smaller entrants to forge partnerships with established manufacturers. These seasoned manufacturers, equipped with experienced regulatory teams, often trade their expertise for equity. Consequently, regulatory proficiency has emerged as a competitive asset, leading investors to scrutinize a company's dossier roadmap with the same intensity as its scientific innovations.

Limited Insurance Coverage for Out-of-Hospital Parenteral Nutrition

Despite evident clinical benefits, Medicare's historical criteria for home parenteral nutrition have sidelined many potential beneficiaries, stunting market growth. Trade associations have conducted cost-offset analyses, showcasing that home infusions not only reduce catheter-related infection rates but also minimize emergency visits. This data-driven approach lays the groundwork for potential policy revisions. Meanwhile, suppliers are emphasizing features like anti-microbial lipid emulsions, which offer easily quantifiable claims data, ensuring their product pipelines resonate with evolving health-economic discussions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Enteral Dominates While Parenteral Accelerates

Oral and enteral nutrition commands 69.15% of the clinical nutrition market in 2025, reflecting its established position as the preferred administration route when the gastrointestinal tract remains functional. Meanwhile, parenteral nutrition is projected to grow at a faster rate of 8.42% CAGR during 2026-2031, driven by expanding applications in critical care and oncology settings. The parenteral segment's growth is further accelerated by innovations in lipid emulsions, particularly the integration of fish oil rich in omega-3 fatty acids, which has demonstrated clinical benefits, including reduced infection rates and shorter hospital stays in critically ill patients.

Infant Nutrition Leads While Disease-Specific Formulas Surge

In 2025, infant nutrition products held a 44.12% market share. However, disease-specific enteral formulas are projected to grow at a 8.98% CAGR through 2031. Government-led initiatives aimed at improving infant health and nutrition, such as funding for nutritional programs and guidelines for infant and child dietary needs, are significantly enhancing the availability and accessibility of nutritional formulations tailored for children. These efforts create awareness and promote compliance among caregivers, thereby driving market growth. For instance, in September 2023, the National Nutrition Council of the Philippines launched the Philippine Plan of Action for Nutrition (PPAN) 2023-2028. This strategic framework aims to combat stunting, childhood obesity, and malnutrition, driving the demand for clinical nutrition products. Such government support not only fosters innovation in clinical nutrition products tailored to combat malnutrition and obesity but also encourages investment from both public and private sectors, thereby expanding market opportunities.

Liquid Formulations Maintain Dominance in the Market

In 2025, liquid formulations constituted 60.05% of the market. Their versatility with both enteral tubes and intravenous lines solidifies their leading position. Meanwhile, semi-solid products targeting dysphagia are set to grow at an annual rate of 8.52%. Suppliers are increasingly adopting a strategy of packaging high-calorie liquids in retort pouches. This innovation not only extends the ambient shelf life but also enables community pharmacies to maintain leaner safety stocks, potentially enhancing working capital metrics throughout the distribution chain.

Malnutrition Support Dominates While Cancer Care Accelerates

In 2025, malnutrition therapy accounted for 30.72% of applications. However, nutrition solutions tailored for cancer care are on track for a 8.97% CAGR. Oncology centers are now integrating specialized formulas into Enhanced Recovery After Surgery (ERAS) pathways. This collaboration positions nutrition companies as integral players in perioperative protocols, paving the way for cross-licensing deals with device firms that provide surgical staplers or wound-closure systems. Such partnerships could unveil additional revenue streams beyond just the nutritional formulas.

Adult Segment Leads While Geriatric Growth Accelerates

Adults made up 50.24% of demand in 2025 due to the increasing prevalence of chronic diseases among the adult population, which necessitates specialized nutritional support for different conditions like diabetes and cancer. Whereas the geriatric nutrition market is set to grow at an annual rate of 9.16%. Long-term-care operators are increasingly mandating high-leucine blends to combat sarcopenia. In response, suppliers are crafting lower-volume, higher-density drinks tailored for residents with reduced appetites. For about half of the surveyed nursing-home chains, geriatric-specific SKUs might account for nearly one-third of the overall nutrition spend by 2029, amplifying their bargaining power in supplier contracts.

Hospital Pharmacies Dominate While Online Channels Surge

In 2025, hospital pharmacies were responsible for 56.85% of clinical nutrition dispensation. Yet, online pharmacies are set to grow at a robust 9.95% CAGR, fueled by home-care discharges and an increasing consumer trust in telehealth. If current trends persist, online sales of medical nutrition could surpass 15% market share by 2031. This potential shift is prompting manufacturers to rethink packaging, emphasizing direct-to-patient shipping integrity over traditional palletized hospital deliveries.

Geography Analysis

Chronic illnesses are a significant driver of the United States' staggering USD 4.5 trillion annual healthcare expenditure, accounting for nearly 90% of the total, as reported by the U.S. Centers for Disease Control and Prevention. In light of these figures, payer organizations are shifting their stance, increasingly opting to reimburse disease-specific nutrition formulas. These formulas not only address nutritional needs but also play a pivotal role in delaying more expensive medical interventions.

According to the U.S. Centers for Disease Control and Prevention, heart disease and stroke alone cost the U.S. healthcare system more than USD 250 billion annually, while diabetes imposes costs above USD 400 billion. As life expectancy climbed to 78.4 years in 2023, hospital groups intensified focus on sarcopenia and metabolic health, prompting suppliers to highlight amino-acid ratios and glycemic indices in product dossiers. For regional integrated-delivery networks, adult-diabetes formulations already account for a significant share of annual nutrition-therapy budgets, an allocation that re-prioritizes formulary reviews around metabolic metrics.

Europe stands as a sophisticated market for clinical nutrition, marked by stringent regulatory frameworks and well-established clinical practice guidelines. In March 2024, Germany launched several initiatives to enhance clinical nutrition as part of its "Good Food for Germany" strategy. This strategy, adopted by the Cabinet in January 2024, aims to improve the overall health and nutrition of the population. The German government's strategic implementation of comprehensive nutrition policies to combat malnutrition is anticipated to drive significant growth in the clinical nutrition market.

The Asia Pacific region is rapidly emerging as a lucrative market for clinical nutrition, spurred by increasing health awareness among consumers, driving demand for nutritional solutions that support overall well-being. Furthermore, government initiatives and policies promoting nutrition education and public health campaigns are fostering the adoption of healthier dietary practices. In May 2024, Fudan University School of Public Health highlighted the crucial role of food safety through a series of activities and educational programs. The initiative emphasized the importance of nutrition, particularly focusing on nutritional supplements for vulnerable populations such as the elderly and individuals with health issues. Additionally, in October 2024, the Union Health Minister (India) introduced key initiatives aimed at strengthening nutrition support for tuberculosis (TB) patients and their families. These initiatives focus on addressing the critical nutritional deficiencies often experienced by TB patients, which can hinder recovery and exacerbate health complications. By providing targeted nutritional interventions, these measures aim to enhance patient recovery rates, improve treatment adherence, and reduce the overall burden of the disease.

Competitive Landscape

The market remains moderately concentrated around Abbott Laboratories, Nestlé Health Science, Fresenius Kabi, and Baxter International. These incumbents use a global scale to absorb compliance costs and to fund multi-country post-marketing studies that smaller firms cannot afford.

Niche players such as Kate Farms and Ajinomoto Cambrooke differentiate through plant-based or rare metabolic-disorder portfolios, positioning themselves as takeover targets for strategics seeking depth in high-growth micro-segments. Recent M&A activity signals that buyers value platform technologies, such as adaptive lipid emulsions or modular packaging, over simple geographic reach, indicating a strategic pivot toward scientific depth.

Technological differentiation is becoming a game changer. Suppliers embed RFID or QR codes into packaging to integrate with hospital inventory systems, and some offer clinician dashboards that correlate nutrient delivery with lab results. This integration elevates nutrition vendors from commodity suppliers to data partners, increasing switching costs and fortifying pricing power during tender renewals.

Clinical Nutrition Industry Leaders

Abbott Laboratories

Nestlé Health Science

Fresenius Kabi

Danone (Nutricia)

Baxter International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Abbott Laboratories launched a new immunonutrition formula specifically designed for oncology patients undergoing chemotherapy, incorporating a proprietary blend of arginine, omega-3 fatty acids, and nucleotides to support immune function during treatment.

- March 2025: Nestlé Health Science completed the acquisition of a specialized pediatric nutrition company for USD 1.2 billion, expanding its portfolio of products for children with rare metabolic disorders.

- February 2025: Fresenius Kabi received FDA approval for a next-generation parenteral nutrition solution featuring an improved lipid emulsion with enhanced stability and reduced inflammatory potential.

- January 2025: Baxter International announced a USD 500 million investment to expand its clinical nutrition manufacturing capacity in Asia Pacific, targeting growing demand in China and India.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the clinical nutrition market as the annual revenue generated worldwide from medically prescribed oral, enteral, and parenteral formulas, covering infant, adult, and geriatric preparations that support disease-related malnutrition, metabolic disorders, gastrointestinal impairment, oncology care, and other clinically diagnosed conditions. Products intended purely for general wellness or sports enhancement are not included in this accounting.

Scope Exclusion: Dietary supplements sold over the counter for healthy consumers lie outside this report's boundary.

Segmentation Overview

- By Route of Administration

- Oral & Enteral

- Parenteral

- By Product Type

- Infant Nutrition

- Standard Enteral Formula

- Disease-Specific Enteral Formula

- Total Parenteral Nutrition (TPN) Components

- By Form

- Powder

- Liquid

- Semi-Solid

- By Application

- Nutritional Support for Malnutrition

- Metabolic Disorders

- Gastrointestinal Diseases

- Cancer

- Neurological Diseases

- Other Diseases

- By End User

- Pediatric

- Adult

- Geriatric

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Homecare & Specialty Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

To validate numbers and close data gaps, Mordor analysts interviewed clinical dietitians, neonatal ICU pharmacists, purchasing heads at large hospital chains, and distributors across North America, Europe, Asia-Pacific, and Latin America. Structured questionnaires clarified average selling prices, formula utilization shifts toward home-based enteral pumps, and emerging demand for immunonutrition blends.

Desk Research

Analysts began with wide-ranging desk work that pulled recent datasets from publicly accessible, gold-standard bodies such as the World Health Organization, UNICEF's child nutrition dashboards, OECD Health Statistics, the United Nations Comtrade shipment files, and the U.S. Centers for Disease Control. These helped estimate treated patient pools and trade flows. Company 10-Ks, hospital procurement disclosures, and leading trade association briefings (European Society for Clinical Nutrition & Metabolism, ASPEN) enriched price points and therapy protocols. Subscriber content from D&B Hoovers and Dow Jones Factiva offered revenue splits that were later screened against open-source figures. The sources listed illustrate the breadth of secondary inputs; many additional materials were reviewed for clarification and spot checks.

Market-Sizing & Forecasting

A top-down construct, anchored in prevalence to treated cohort calculations and reconstructed trade statistics, set the core 2024 baseline. Select bottom-up supplier roll-ups (sampled ASP × volume from key manufacturers) served as a cross-check, after which totals were adjusted. Key variables like preterm birth rates, major GI surgery incidences, the 65+ population pool, per capita health spend, and ICU bed additions feed a multivariate regression model that projects demand through 2030. Gaps in bottom-up volumes were bridged with region-specific import values normalized by average landed prices.

Data Validation & Update Cycle

Outputs undergo anomaly scans, variance thresholds, and two-step peer review before sign-off. Models refresh every 12 months, with interim revisions triggered by regulatory changes, large-scale recalls, or material M&A; an analyst rechecks all figures immediately prior to client delivery.

Why Our Clinical Nutrition Baseline Commands Reliability

Published estimates often diverge because firms choose different product mixes, care settings, and update cadences.

Key gap drivers include excluding infant formula revenue, focusing solely on hospital parenteral feeds, or applying static price curves, whereas Mordor Intelligence reports the full clinical spectrum and updates annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 78.11 B | Mordor Intelligence | - |

| USD 63.7 B | Global Consultancy A | Omits home care enteral and liquid oral formulations |

| USD 34.1 B | Trade Journal B | Counts only enteral and parenteral, excludes infant segment |

| USD 60.08 B | Industry Association C | Uses constant ASPs, limited country coverage |

In sum, the disciplined blend of inclusive scope, dual route modeling, and continuous source validation makes our baseline the most dependable starting point for strategic decisions.

Key Questions Answered in the Report

How big is the Clinical Nutrition Market?

The Clinical Nutrition Market size is expected to reach USD 84.31 billion in 2026 and grow at a CAGR of 7.94% to reach USD 123.54 billion by 2031.

Which is the fastest growing region in Clinical Nutrition Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Clinical Nutrition Market?

In 2026, the North America accounts for the largest market share in Clinical Nutrition Market.

What years does this Clinical Nutrition Market cover, and what was the market size in 2025?

In 2025, the Clinical Nutrition Market size was estimated at USD 78.11 billion. The report covers the Clinical Nutrition Market historical market size for years: 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Clinical Nutrition Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: