Anti-obesity Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

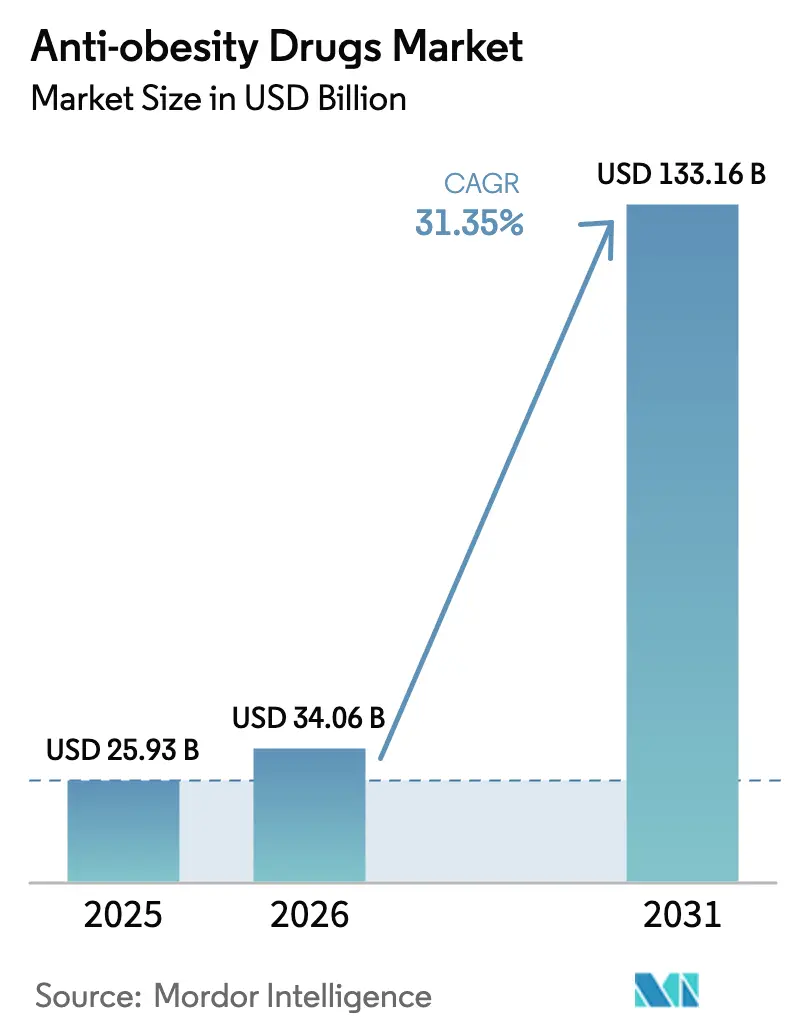

| Market Size (2026) | USD 34.06 Billion |

| Market Size (2031) | USD 133.16 Billion |

| Growth Rate (2026 - 2031) | 31.35% CAGR |

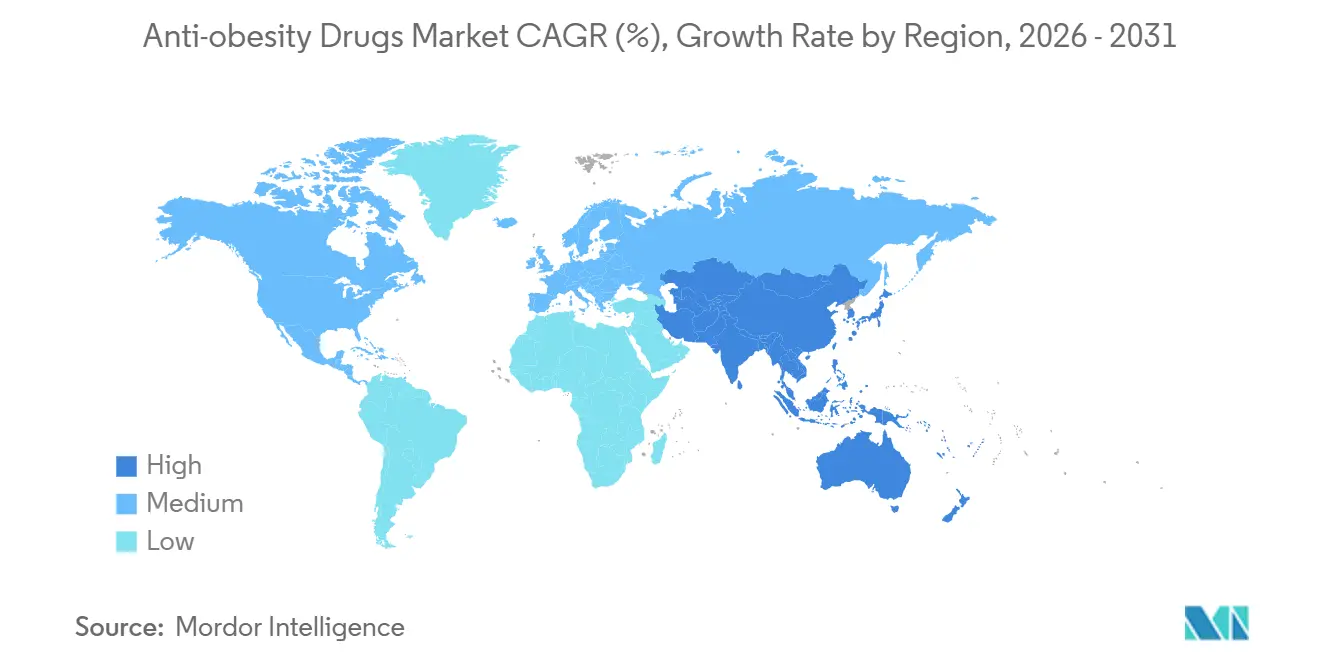

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-obesity Drugs Market Analysis by Mordor Intelligence

The Anti-obesity Drugs Market size is projected to be USD 25.93 billion in 2025, USD 34.06 billion in 2026, and reach USD 133.16 billion by 2031, growing at a CAGR of 31.35% from 2026 to 2031.

Regulatory re-positioning of obesity as a cardiometabolic disease, payer re-classification of GLP-1 receptor agonists as essential therapies after positive cardiovascular-outcome trials, and rapid employer adoption of coverage are converging to accelerate prescription volumes. The October 2024 removal of tirzepatide from the U.S. shortage list redirected revenue from compounders back to branded manufacturers, illustrating how enforcement actions can abruptly reshape channel dynamics. Simultaneously, Novo Nordisk’s SELECT trial confirmed a 20% reduction in major adverse cardiac events with semaglutide, expanding prescriber confidence and unlocking reimbursement across high-risk populations. Capacity expansions worth USD 11.3 billion from Novo Nordisk and Eli Lilly are still catching up with demand, so supply tightness is expected through 2027, sustaining pricing power. Market entrants targeting oral or multi-agonist mechanisms are intensifying competition, but incumbents retain strong negotiating leverage because they control most commercial-scale peptide production.

Key Report Takeaways

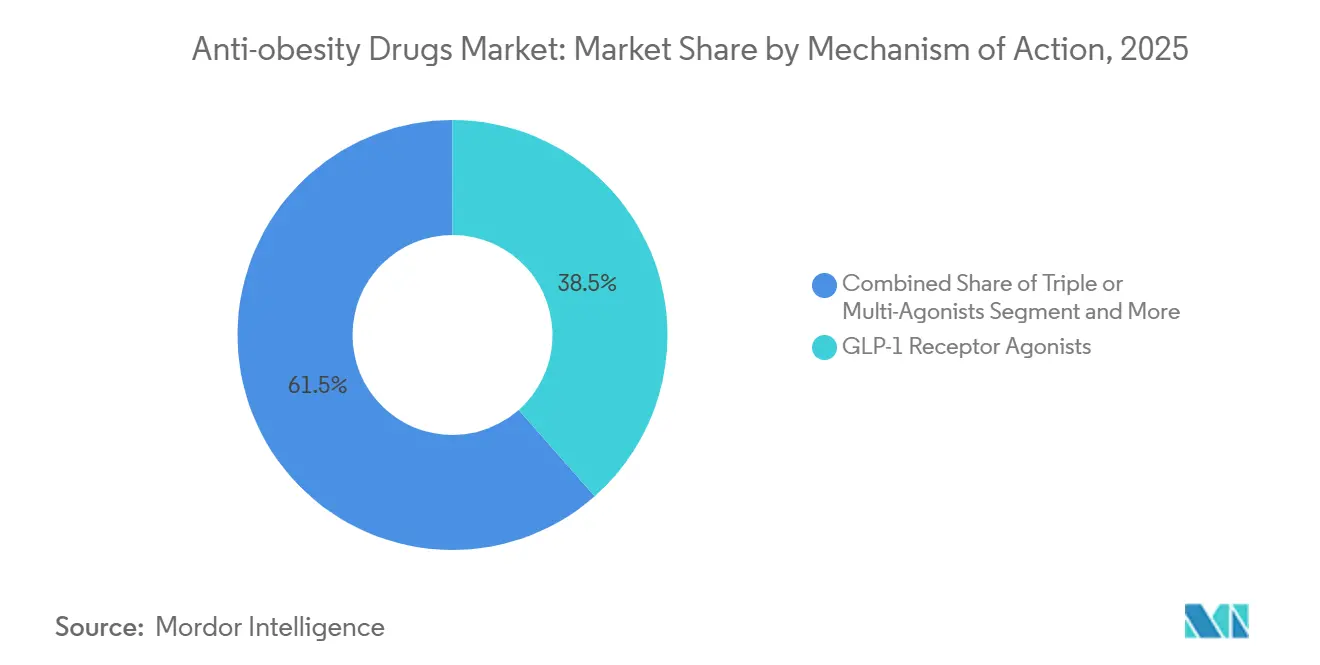

- By mechanism of action, GLP-1 receptor agonists led with 38.55% of the anti-obesity drugs market share in 2025; triple or multi-receptor agonists are forecast to expand at a 32.25% CAGR to 2031.

- By drug type, prescription products accounted for 64.53% of the anti-obesity drugs market in 2025, while the segment is projected to post a 32.85% CAGR through 2031.

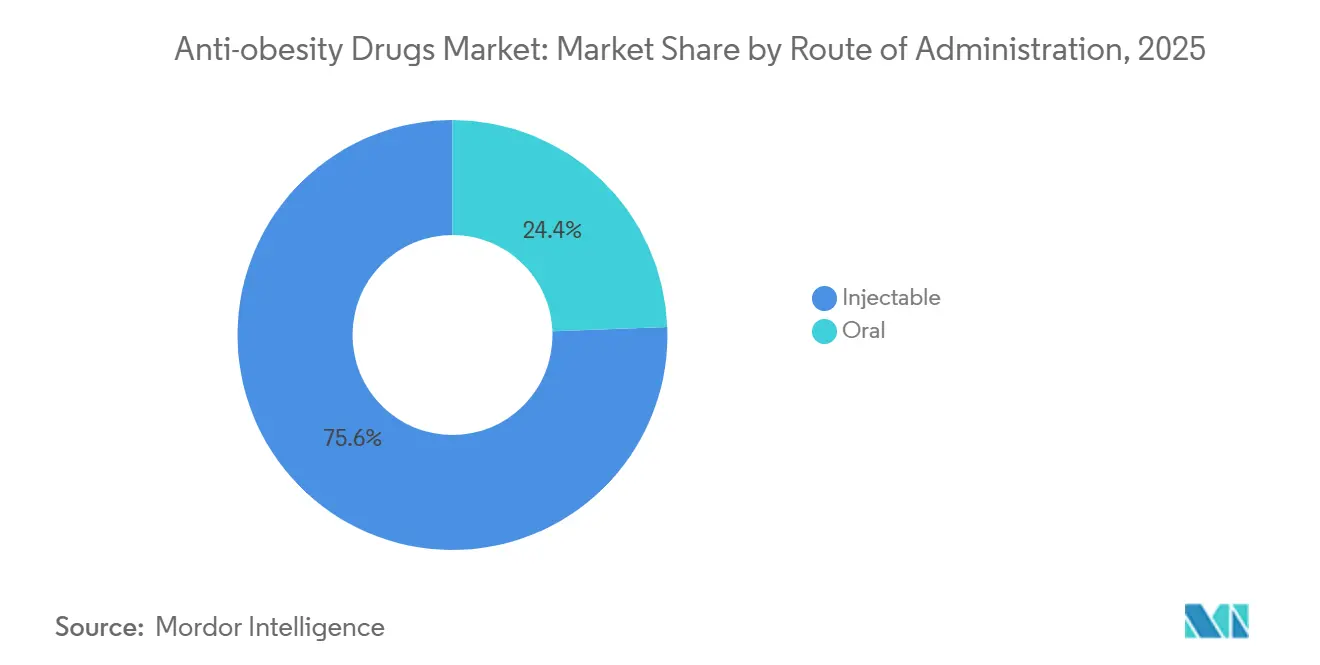

- By route of administration, injectables held 75.63% of the anti-obesity drugs market in 2025; oral formulations are poised to grow at a 34.87% CAGR as late-stage candidates mature.

- By distribution channel, retail pharmacies maintained 41.23% share in 2025, whereas online pharmacies and telehealth platforms are advancing at a 34.7% CAGR to 2031.

- By geography, North America commanded 39.53% share in 2025, but Asia-Pacific is projected to register a 35.21% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Anti-obesity Drugs Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cardiometabolic complications driving early pharmacologic intervention | +6.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rapid employer adoption of GLP-1 coverage as a hedge against long-term healthcare costs | +5.2% | North America, led by large self-insured employers | Short term (≤ 2 years) |

| Breakthrough cardiovascular-outcome data expanding prescriber comfort and payer mandates | +5.9% | Global, influenced by FDA, EMA, PMDA | Medium term (2-4 years) |

| Next-generation oral small-molecule GLP-1s unlocking primary-care and emerging-market volume | +4.7% | Asia-Pacific core, spill-over to Latin America and MEA | Long term (≥ 4 years) |

| Chronic kidney-disease risk-reduction labeling creating multi-specialty pull-through | +3.6% | Global, nephrology-driven in North America and Europe | Medium term (2-4 years) |

| AI-enabled drug-discovery platforms accelerating multi-agonist pipeline productivity | +2.4% | Global, concentrated in U.S. and China biotech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cardiometabolic Complications Driving Early Pharmacologic Intervention

Cardiologists and primary-care physicians now regard obesity as a cardiovascular risk factor comparable to smoking, following the American Heart Association’s 2024 statement that reclassified the condition[1]American Heart Association, “2024 Scientific Statement on Obesity,” heart.org. Semaglutide’s FLOW trial subsequently showed a 24% reduction in kidney-disease progression, prompting payers to waive prior authorizations for diabetic nephropathy cases. As 41.9% of U.S. adults were living with obesity in 2024, clinical guidelines began recommending GLP-1 initiation within six months of diagnosis rather than after lifestyle failure. Employer health plans quickly aligned benefit designs with these guidelines, fueling a surge in first-line prescriptions. This compressed treatment pathway is now mirrored in Europe and Japan, shrinking the time from diagnosis to pharmacologic therapy and expanding the eligible population at scale.

Rapid Employer Adoption of GLP-1 Coverage as a Hedge Against Long-Term Healthcare Costs

A 2024 Employee Benefit Research Institute analysis found that self-insured employers covering semaglutide or tirzepatide cut diabetes-related claims by 12% and cardiovascular hospitalizations by 9% within 18 months, offsetting annual drug costs in the USD 12,000–16,000 range. As a result, 44% of large U.S. employers added GLP-1s to formularies in 2024 versus 25% in 2023. Outcomes-based contracts that peg rebates to sustained weight loss or HbA1c reduction are spreading, shifting risk to manufacturers and motivating adherence programs. Digital coaching bundled with prescriptions improved 12-month persistence rates from 40% to 65%, demonstrating that integrated models can blunt overall cost growth. Parallel moves in Canada and Australia indicate that employers worldwide are replicating the value-based blueprint to manage chronic-disease liability.

Breakthrough Cardiovascular-Outcome Data Expanding Prescriber Comfort and Payer Mandates

The SELECT trial’s 20% reduction in major adverse cardiac events spurred the FDA to add a cardiovascular prevention indication to semaglutide in March 2024. U.S. payers such as UnitedHealthcare and Anthem promptly removed step-therapy hurdles for high-risk patients, accelerating uptake among cardiology practices. Cardiologists, once peripheral to obesity management, now account for roughly one-third of new GLP-1 scripts, broadening the prescriber base. Eli Lilly’s SURMOUNT-MMO data, showing a 38% cut in cardiovascular death and heart-failure hospitalization with tirzepatide, further validated the class. European and Japanese regulators followed with label updates, pushing insurers in those regions to relax prior-authorization rules for secondary prevention. These pivotal datasets elevate obesity drugs from lifestyle adjuncts to disease-modifying therapies with hard-endpoint benefits.

Next-Generation Oral Small-Molecule GLP-1s Unlocking Primary-Care and Emerging-Market Volume

Orforglipron, GSBR-1290, and VK2735 demonstrated double-digit weight-loss efficacy in Phase 2 studies without injection-related barriers, attracting strong interest from primary-care physicians. Emerging markets where cold-chain infrastructure is limited stand to benefit most; a semaglutide tablet introduced in India at 60% below the injectable price captured 12% share within four months. Oral dosing also sidesteps needle aversion and simplifies distribution via traditional pharmacy channels. As Phase 3 data mature, analysts project that oral GLP-1s could lift treated prevalence by 40% globally. Manufacturers are building dedicated oral-formulation capacity to capitalize on this shift, signaling a decisive pivot toward pill-based delivery.

Restraints Impact Analysis of Anti-obesity Drugs Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Manufacturing-capacity bottlenecks for complex peptide APIs | -3.2% | Global, shortages acute in North America and Europe | Short term (≤ 2 years) |

| Regulatory safety surveillance around rare ophthalmic adverse events | -1.8% | Global, heightened scrutiny from FDA and EMA | Medium term (2-4 years) |

| Escalating payer budget-impact controls and step-therapy barriers | -2.6% | North America and Europe | Short term (≤ 2 years) |

| Grey-market compounding eroding branded-drug economics | -1.9% | United States, limited after Oct 2024 enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Manufacturing-Capacity Bottlenecks for Complex Peptide APIs

Solid-phase peptide synthesis, HPLC purification, and lyophilization create long cycle times that cap throughput. Novo Nordisk’s USD 6 billion capacity build announced in 2024 and Lilly’s USD 5.3 billion Indiana plant will not reach full output until 2027, keeping supply constrained. Only eight FDA-approved facilities worldwide can produce GLP-1 peptides at scale, so any disruption, such as the 2024 fire at a Danish supplier, quickly triggers global shortages. The European Medicines Agency responded to recurring deficits by advising prescribers to prioritize cardiovascular patients, effectively rationing therapy. CDMO expansions are underway, but regulatory qualification for complex peptides averages 18–24 months, ensuring that tightness persists in the near term.

Escalating Payer Budget-Impact Controls and Step-Therapy Barriers

With annual per-patient spending exceeding USD 12,000, insurers are tightening utilization controls. A 2024 Academy of Managed Care Pharmacy survey showed 78% of commercial plans require prior authorization, with approval rates below 65% for first-time requests[2]Academy of Managed Care Pharmacy, “Prior Authorization Survey,” amcp.org. Step-therapy mandates that patients fail metformin or orlistat add 3–6 months to initiation timelines, increasing dropout risk. Medicare’s 2024 decision to cover obesity drugs triggered Congressional Budget Office projections of USD 25 billion in annual spending by 2030, prompting discussion of higher co-pays and quantity limits. European payers are even stricter; the U.K. limits semaglutide reimbursement to BMI ≥ 35 kg/m², excluding many high-risk patients. These cost-containment tools temper the adoption curve despite strong clinical evidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Anti-obesity Drugs Market Segment Analysis

By Mechanism of Action:

Multi-Agonists Redefine Efficacy CeilingThe segment generated USD 13.1 billion in 2025, when GLP-1 monotherapies held 38.55% share. Retatrutide’s 24.2% weight-loss profile, disclosed in December 2024, underscores why triple-agonists are expected to expand at a 32.25% CAGR through 2031. Over the next five years, dual GIP/GLP-1 agents should migrate from second-line to first-line therapy as clinicians aim to avert tolerability limits seen with higher-dose GLP-1 monotherapy. The addition of glucagon-receptor activity promises incremental fat-mass reduction and metabolic flexibility, broadening appeal to endocrine, cardiology, and hepatology specialists. Meanwhile, centrally acting sympathomimetics and lipase inhibitors are sliding toward low-volume niches, constrained by modest efficacy and safety trade-offs.

Payers are signaling willingness to reimburse premium-priced multi-agonists if cardiovascular or renal benefits materialize, a possibility under investigation in ongoing SURMOUNT-5 and TRIUMPH-2 outcome studies. Given superior weight loss and comorbidity impact, analysts expect multi-agonists to exceed 45% of the anti-obesity drugs market by 2031. New entrants such as Amgen’s MariTide and Viking Therapeutics’ VK2735 target differentiated dosing intervals or improved GI tolerability to carve share. The escalation in mechanism complexity heightens manufacturing cost but also raises efficacy and, by extension, value-based price ceilings.

By Drug Type:

Prescription Dominance Reinforced by Payer MandatesPrescription products represented 64.53% of the anti-obesity drugs market in 2025, and the cohort is on track for a 32.85% CAGR through 2031. Over-the-counter alternatives like orlistat delivered only 2–3% incremental weight loss in 2024 meta-analyses, reinforcing prescriber reliance on higher-efficacy options. Payer formularies absorb up to 90% of prescription costs for eligible patients, whereas OTC products are fully out-of-pocket, limiting their reach to affluent self-payers. FDA guidance in 2024 also tightened the path for Rx-to-OTC switches by requiring biomarkers for chronic-disease self-selection, effectively closing the door to consumerized GLP-1s.

Going forward, prescription status will likely remain the default for any agent demonstrating double-digit weight loss or cardiometabolic endpoints. Rhythm Pharmaceuticals’ setmelanotide, gated by a REMS and genetic testing, signals how regulators may handle next-generation therapies with complex safety profiles. For OTC players, the viable economic niche is slimming down to adjunctive products such as fiber-based appetite suppressants, which do not threaten branded franchises.

By Route of Administration:

Oral Pills Poised to Disrupt Injectable HegemonyInjectable formulations generated 75.63% of revenue in 2025, yet oral candidates are forecast to grow at a brisk 34.87% CAGR, steadily enlarging their slice of the anti-obesity drugs market size. Orforglipron’s Phase 2 weight-loss efficacy rivaled injectable liraglutide without refrigeration or needle handling, a combination expected to resonate in primary-care settings. Structure Therapeutics’ GSBR-1290 and Viking’s VK2735 join a pipeline of small-molecule orals that promise comparable metabolic benefits with fewer GI events. In India, a generic oral semaglutide captured double-digit share within months, underscoring price elasticity and dosage-form preference in cash-pay markets.

Injectables retain advantages in adherence because weekly or monthly dosing reduces daily pill fatigue, and depot formulations in development could further lower frequency. Yet, as oral bioavailability technology improves, most analysts anticipate an inflection by 2028 where pills erode injectable volume in mild-to-moderate obesity, while high-risk patients continue on depot biologics. For manufacturers, investing in dual supply chains - lyophilized injectables and solid-dose tablets - becomes a strategic imperative.

By Distribution Channel:

Telehealth Platforms Bypass Traditional GatekeepersRetail pharmacies processed 41.23% of prescriptions in 2025, but online and telehealth channels are recording a 34.7% CAGR, rapidly reshaping patient access patterns. Hims & Hers enrolled 50,000 subscribers within three months of launching a compounded-semaglutide cash-pay plan, proving demand for convenience and price transparency before regulators curtailed compounding. Ro surpassed 120,000 GLP-1 patients by mid-2024 with a vertically integrated model that bundles virtual physicians, labs, and doorstep delivery. Amazon Pharmacy’s entry in March 2024 added two-day shipping and competitive pricing, forcing brick-and-mortar chains to upgrade e-commerce capabilities.

Telehealth providers often bypass prior authorization by shouldering drug costs through subscription fees, shifting the expense to consumers but compressing initiation timelines from weeks to days. Hospital outpatient pharmacies and weight-loss clinics are responding by integrating virtual consults and home delivery to retain share. Channel fragmentation will likely persist: insured patients may stay with traditional pharmacies to capture benefits, while under-insured or privacy-seeking consumers gravitate toward digital platforms.

Geography Analysis

North America Anti-obesity Drugs Market

North America dominated with 39.53% of the anti-obesity drugs market in 2025, buoyed by obesity prevalence surpassing 41% of adults and expanding Medicare Part D coverage that raised the eligible pool by 15 million beneficiaries. Still, payer cost pressures remain acute; the Institute for Clinical and Economic Review deemed current GLP-1 prices cost-effective only below USD 7,000 annually, prompting insurers to demand steep rebates. Canada lags the United States, as public plans in only three provinces reimburse obesity drugs, creating reliance on private pay or employer coverage. Mexico’s market is limited by out-of-pocket spend, but Novo Nordisk’s lower-dose semaglutide at 40% below U.S. pricing began expanding access in 2024. Overall, North American growth will hinge on balancing clinical demand with payer affordability thresholds.

APAC Anti-obesity Drugs Market

Asia-Pacific is forecast to post a 35.21% CAGR through 2031, the fastest among all regions, aided by regulatory approvals in China, Japan, and India alongside rapid middle-class expansion. China’s 180 million adults with obesity constitute a massive addressable population, though reimbursement is confined to tier-1 cities and private plans. Japan’s six-month reimbursement cap mandates demonstrable 5% weight loss for continuation, incentivizing high-adherence regimens. In India, a generic tablet priced 60% below the branded injectable quickly captured share, signaling cost-sensitive adoption pathways. South Korea and Australia approved local or imported GLP-1s but apply stringent BMI thresholds for publicly funded access, tempering early uptake. Oral formulations and forthcoming biosimilars are essential to unlocking second- and third-tier city penetration across the region.

EMEA and LATAM Anti-obesity Drugs Market

Europe controlled roughly 25% of the anti-obesity drugs market in 2025, yet reimbursement gatekeeping restrains volume growth. NICE restricts semaglutide to BMI ≥ 35 kg/m², shrinking the eligible population by 60% relative to FDA criteria[3]National Institute for Health and Care Excellence, “Semaglutide Guidance,” nice.org.uk. Germany enforces a 12-month reimbursement cap, requiring self-pay thereafter, while France approves coverage only for diabetic obesity. Shortages prompted an EMA alert in March 2024, leading to rationing protocols prioritizing cardiovascular co-morbid patients. Middle East and Africa remain nascent but show pockets of private-pay demand in Gulf Cooperation Council states. Latin America is led by Brazil, where private insurance, covering 25% of residents, funds semaglutide, but public systems have not prioritized coverage. Overall regional variability highlights how health-technology assessments and budget constraints filter clinical enthusiasm into disparate adoption curves.

Competitive Landscape

Novo Nordisk and Eli Lilly together held a significant share of GLP-1 revenue in 2025, giving the anti-obesity drugs industry a moderately concentrated structure. Both firms invested over USD 11 billion combined between 2024 and 2026 to expand peptide facilities, erecting capacity barriers that delay biosimilar competition. However, the pipeline of oral and multi-agonist assets from Amgen, Viking Therapeutics, Structure Therapeutics, and others is expanding rapidly. Amgen’s MariTide achieved 20% weight loss at 52 weeks with monthly dosing, and Viking’s VK2735 delivered 8.2% loss in a pill format, signaling credible alternative mechanisms. Rhythm Pharmaceuticals carved a profitable niche in rare genetic obesity with setmelanotide’s USD 350 million in 2024 sales, demonstrating that precision-medicine subsegments can coexist alongside mass-market drugs.

Patents will reshape the landscape: semaglutide loses composition-of-matter exclusivity in 2031, while tirzepatide extends to 2036, creating different windows for biosimilar entry. Technology partnerships are shortening development cycles; Insilico Medicine generated a triple agonist candidate in 18 months using generative AI, compared with the historic 3–5-year timeline. Big pharma is increasingly securing AI capabilities via acquisitions, as illustrated by Novo Nordisk’s USD 1.1 billion purchase of Forma Therapeutics in 2024. Licensing deals now feature outcomes-based milestones tied to Phase 2 efficacy targets, reflecting a heightened emphasis on translational proof versus early-stage promise. Against this backdrop, competitive intensity is expected to escalate, but high capital requirements and manufacturing know-how should keep the market from fragmenting rapidly.

Anti-obesity Drugs Industry Leaders

F Hoffmann-La Roche AG

Novo Nordisk AS

Currax Pharmaceuticals LLC

Eli Lilly and Company

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Anti-obesity Drugs Market Companies Covered in this Report

- Altimmune Inc.

- Amgen

- AstraZeneca

- Bayer

- Boehringer Ingelheim Intl. GmbH

- Eli Lilly and Company

- Roche

- GlaxoSmithKline

- Hanmi Pharm. Co., Ltd.

- Innovent Biologics Inc.

- Merck

- Novo Nordisk

- Pfizer

- Rhythm Pharmaceuticals, Inc.

- Structure Therapeutics Inc.

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Viking Therapeutics Inc.

- Zealand Pharma

- Zydus Lifesciences Ltd.

- Currax Pharmaceuticals

Recent Industry Developments in Anti-obesity Drugs Market

- January 2026: Novo Nordisk introduced Wegovy pill, the first oral GLP-1 approved for chronic weight management, across U.S. pharmacies.

- August 2025: Teva Pharmaceuticals launched the first FDA-approved generic of Saxenda (liraglutide injection) in the United States, expanding lower-cost options for prescribers.

Anti-obesity Drugs Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the anti-obesity drugs market as all prescription and over-the-counter pharmacologic agents with an approved or clinically accepted indication for body-weight reduction or maintenance in adolescents and adults. Coverage spans oral and injectable small-molecule or biologic therapies sold through hospital, retail, and digital pharmacies worldwide. According to Mordor Intelligence, compounded semaglutide or non-regulated online formulations are excluded to protect data integrity.

Scope exclusions include bariatric devices, dietary supplements, wellness apps, and compounded medications, which are outside our remit.

Segments Covered in This Report

- By Mechanism of Action

- GLP-1 Receptor Agonists

- Dual GIP/GLP-1 Agonists

- Triple or Multi-Receptor Agonists

- Centrally Acting Sympathomimetics

- Peripherally Acting Lipase Inhibitors

- By Drug Type

- Prescription Drugs

- OTC Drugs

- By Route of Administration

- Injectable (Weekly / Monthly)

- Oral Daily Pills

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies & Tele-health Platforms

- Weight-Loss Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Endocrinologists, payers, pharmacists, and supply-chain executives across North America, Europe, Asia-Pacific, and the Gulf were interviewed to confirm real-world adherence, mark-ups, and production ramp-ups. Short surveys with obesity-clinic dietitians validated price sensitivity and substitution assumptions drawn from secondary data.

Desk Research

Mordor analysts begin with authoritative public sources such as WHO Global Health Observatory, CDC NHANES, OECD obesity datasets, and FDA / EMA approval registries, pairing them with UN Comtrade trade flows to anchor finished-dose export volumes. Revenue disclosures from company 10-Ks and D&B Hoovers refine price corridors that desk data alone cannot show.

Subscription inputs include IQVIA prescription audits, Questel patent counts, Dow Jones Factiva news feeds, and regional reimbursement lists, which help trace launch timing, capacity shifts, and payer coverage patterns. Numerous other references were also reviewed, making the sources cited here illustrative rather than exhaustive.

Market-Sizing & Forecasting

A top-down model multiplies treated patient pools, derived from prevalence and treatment-seeking rates, by annual drug spend reconstructed from price nets and adherence curves; selective bottom-up checks, such as sampled manufacturer sales and online unit estimates, validate totals. Key variables include adult obesity prevalence, new GLP-1 prescription starts, average selling price erosion, reimbursement penetration, pipeline success rates, and fill rate constraints. A multivariate regression informs driver elasticities before ARIMA smoothing projects values through 2030, while scenario analysis tests high and low uptake cases. Data gaps in smaller markets are bridged with regional analogs indexed to purchasing power parity.

Data Validation & Update Cycle

Outputs undergo variance screens against independent spend trackers, with anomalies triggering expert re-contact. A three-layer analyst review precedes sign-off. Reports refresh annually, and interim updates follow material regulatory, safety, or supply events so clients receive our latest view.

How Mordor Intelligence's Anti-obesity Drugs Market Size Compares to Other Published Estimates

Published estimates often diverge because firms vary in counted products, refresh cadence, and uptake curves, leaving buyers to reconcile figures that differ by an order of magnitude.

Gaps widen when other studies fold dietary supplements into prescription totals, hold list prices static despite rapid net erosion, or extrapolate U.S. demand globally without adjusting for reimbursement lags. Mordor includes only approved molecules, revises forecasts once payer or capacity milestones are confirmed, and captures channel-specific pricing, producing a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.93 B (2025) | Mordor Intelligence | - |

| USD 7.14 B (2025) | Global Consultancy A | Narrow indication scope; injectables in limited launch excluded; static price view |

| USD 14.83 B (2024) | Industry Publisher B | Online pharmacy sales omitted; applies uniform 3 % CAGR to extend base year |

| USD 3.20 B (2024) | Trade Journal C | Counts four legacy drugs only; geography limited to US, EU-5, Japan |

These contrasts show that scope breadth, price dynamics, and launch geography shape headline numbers. By anchoring our model in verified sales of every approved molecule and refreshing it annually, Mordor Intelligence delivers a transparent, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the projected global revenue for anti-obesity drugs by 2031?

Sales are expected to reach USD 133.16 billion by 2031, supported by a 31.35% CAGR.

Which therapy class currently generates the largest share of anti-obesity drug sales?

GLP-1 receptor agonists led with 38.55% share in 2025.

How fast are oral GLP-1 candidates anticipated to expand?

Oral formulations are projected to grow at a 34.87% CAGR through 2031 as late-stage trials conclude.

Which region is forecast to record the highest growth in anti-obesity prescriptions?

Asia-Pacific is expected to post a 35.21% CAGR between 2026 and 2031.

What is the primary supply constraint facing anti-obesity drug producers?

Limited peptide manufacturing capacity is likely to keep supply tight until new facilities reach full output in 2027.

Page last updated on: