Health Check-up Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

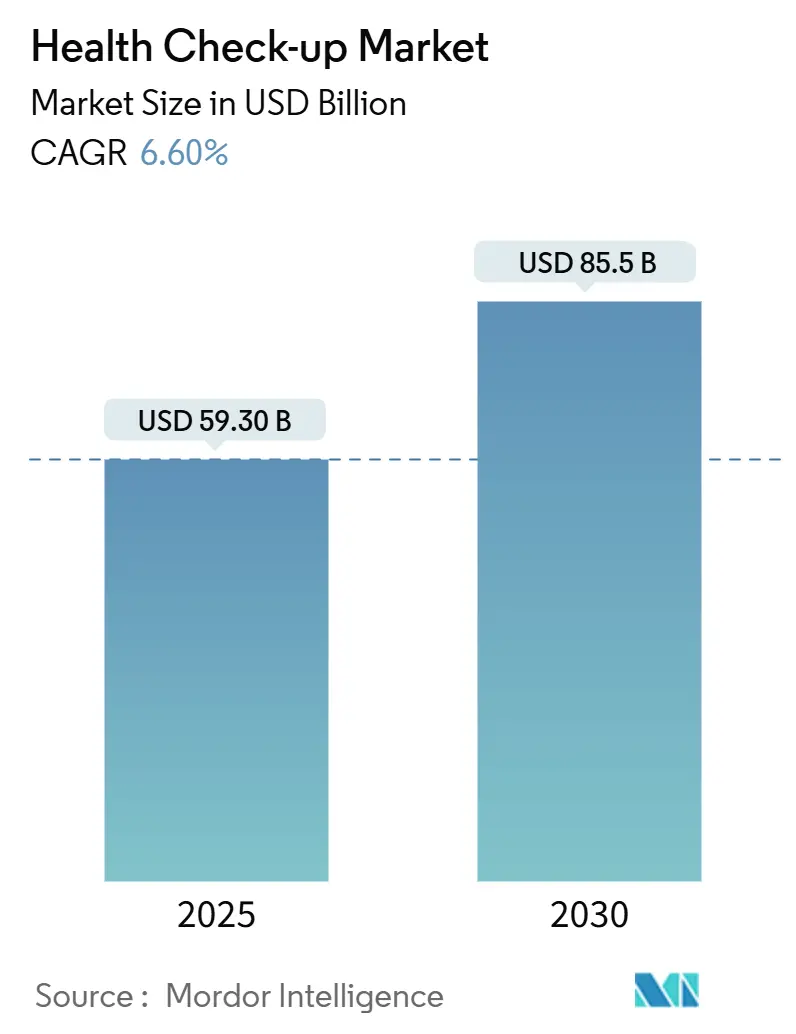

| Market Size (2025) | USD 59.30 Billion |

| Market Size (2030) | USD 85.5 Billion |

| Growth Rate (2025 - 2030) | 6.60% CAGR |

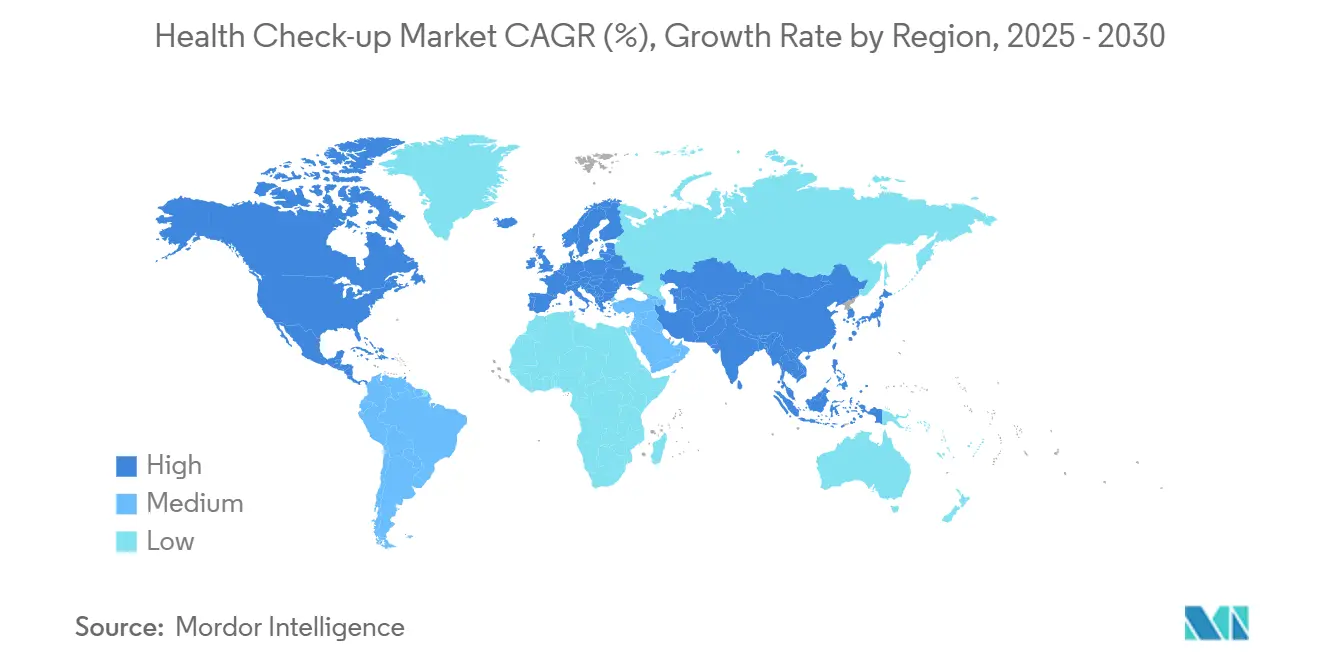

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Health Check-up Market Analysis by Mordor Intelligence

The health check-up market size stands at USD 59.3 billion in 2025 and is projected to grow at a 6.60% CAGR, reaching USD 85.5 billion by 2030. Robust expansion is underpinned by the escalating prevalence of chronic conditions, expanding corporate wellness budgets, and the rapid integration of artificial-intelligence diagnostics. Shifts toward preventive care, reinforced by post-pandemic consumer awareness, continue to stimulate demand even as reimbursement gaps persist. Meanwhile, technology-enabled disruptors intensify competition, lowering screening costs and broadening access as health systems worldwide seek early detection to curb long-term treatment expenditures.

Key Report Takeaways

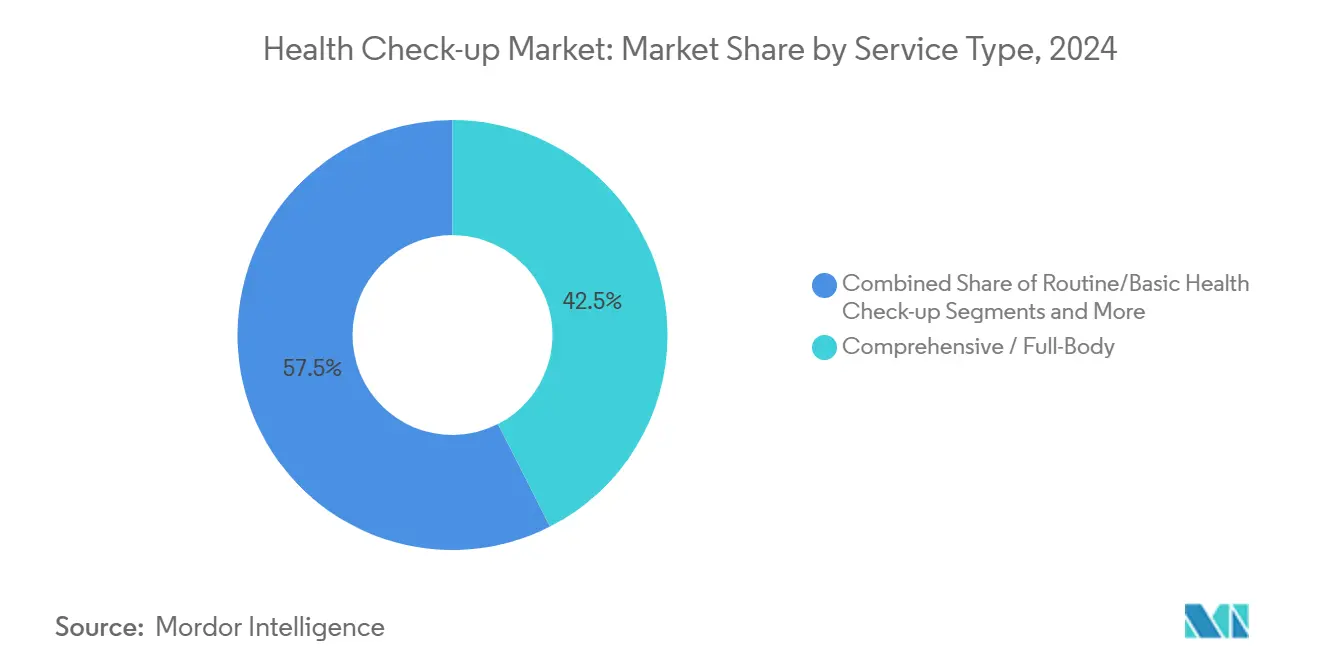

- By service type, comprehensive full-body screenings accounted for 42.5% of the health check-up market share in 2024, while AI-driven full-body scans are forecast to post the highest 4.2% CAGR through 2030.

- By provider type, hospital-based centers held 37.4% of the health check-up market share in 2024; at-home testing startups are expanding fastest at a 5.1% CAGR to 2030.

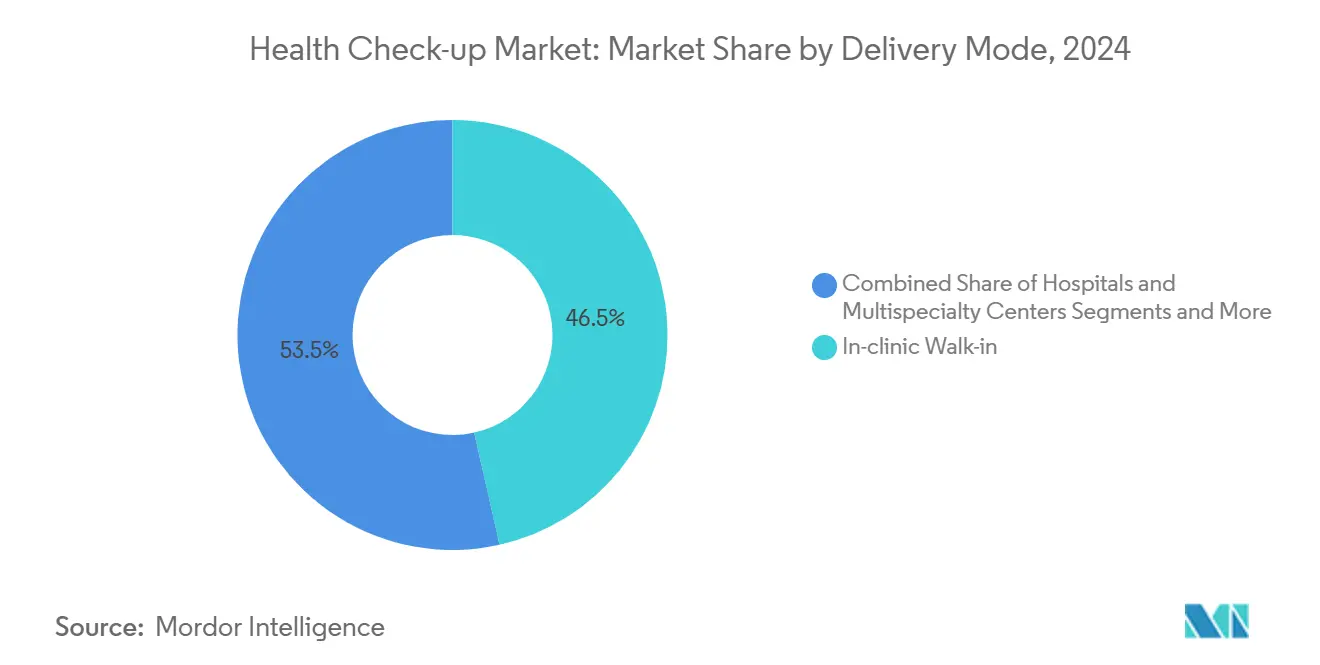

- By delivery mode, in-clinic walk-in services captured 46.5% of the health check-up market size in 2024, whereas telehealth delivery is advancing at a 6.6% CAGR over the forecast period.

- Geographically, North America led with 35.7% of the health check-up market share in 2024; Asia-Pacific is projected to grow quickest, registering an 8.6% CAGR through 2030.

Global Health Check-up Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic-disease prevalence & early-detection shift | +1.80% | Global (highest in North America & Europe) | Long term (≥ 4 years) |

| Rising consumer awareness & preventive-care adoption | +1.20% | Global, stronger in APAC | Medium term (2-4 years) |

| Corporate wellness budgets boosting bulk check-ups | +1.10% | North America & Europe, expanding in APAC | Medium term (2-4 years) |

| AI-powered full-body scan subscriptions gain funding | +0.90% | North America & Europe; select APAC metros | Short term (≤ 2 years) |

| Medical-tourism flows to Turkey & Korea | +0.40% | APAC core; spill-over to MEA & Europe | Medium term (2-4 years) |

| Insurer dynamic-premium programs | +0.30% | North America; pilots in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic-Disease Prevalence & Early-Detection Shift

Hypertension among U.S. adults is expected to climb from 51.2% in 2025 to 61.0% by 2050, while diabetes prevalence rises from 16.3% to 26.8%.[1]American Heart Association, “Forecasting the Burden of Cardiovascular Disease and Stroke in the United States Through 2050,” ahajournals.org Associated cardiovascular costs could triple to USD 1.344 trillion, turning preventive screening from an optional benefit to a fiscal necessity. Health systems embed regular screenings into protocols, recognizing that early intervention mitigates expensive late-stage treatments.

Rising Consumer Awareness & Preventive-Care Adoption

Seventy-three percent of patients report heightened openness to telehealth and proactive health management, a post-pandemic behavior reinforced through social media and mobile health apps.[2]National Institutes of Health, “Telehealth during the pandemic: Patient perceptions and policy implications,” ncbi.nlm.nih.govMillennials and Gen Z increasingly redirect discretionary spending toward full-body assessments, fueling premium demand across emerging APAC economies where disposable incomes accelerate.

Corporate Wellness Budgets Boosting Bulk Check-Ups

U.S. employers will spend USD 1.3 trillion on health benefits in 2025, with each dollar spent on screenings saving USD 3.27 in future medical costs. Mandatory annual assessments broaden beyond executive tiers, securing large-volume contracts for providers and stabilizing revenue streams independent of individual out-of-pocket spending.

AI-Powered Full-Body Scan Subscriptions Gain Funding

AI-enhanced MRI platforms now deliver full-body scans in 22 minutes at USD 499—a one-third price cut—demonstrating accelerated democratization of premium diagnostics. Venture funding channels toward startups integrating AI with imaging and molecular point-of-care tests, boosting scalability and accuracy across screening programs.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-Of-Pocket Costs For Uninsured Populations | -1.40% | Global, acute in developing markets & U.S. | Long term (≥ 4 years) |

| Limited Insurance Cover For Advanced Imaging Packages | -0.80% | North America & Europe primary | Medium term (2-4 years) |

| Data-Privacy Concerns Over Multi-Parametric Biomarker Platforms | -0.60% | Global, strictest in Europe & North America | Medium term (2-4 years) |

| Post-Pandemic "Check-Up Fatigue" Reducing Routine Visits | -0.50% | Global, most pronounced in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Costs for Uninsured Populations

Comprehensive scans priced at USD 3,000 remain prohibitive for uninsured patients, reinforcing disparities even within high-income economies. Inflation and stagnant wages further constrain discretionary healthcare budgets, discouraging asymptomatic individuals from proactive screening.

Limited Insurance Cover for Advanced Imaging Packages

Payers classify many whole-body MRI protocols as investigational, citing concerns over false positives and downstream costs. Prior authorization hurdles delay uptake, compelling providers to pivot toward direct-pay models and subscription pricing to sustain adoption momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Comprehensive Screenings Anchor Premium Demand

Comprehensive packages captured 42.5% of the health check-up market in 2024, underscoring consumer appetite for holistic diagnostics despite premium pricing. Advanced biomarker panels and genomic assays differentiate high-end providers, while AI-enabled imaging trims appointment times, lifting throughput and margins. The AI-driven full-body segment is projected to lead growth at a 4.2% CAGR, reflecting cost-down innovation and superior predictive accuracy.[3]American Hospital Association, “Early Disease Detection: 3 Tech Trends to Watch,” aha.org Routine baseline exams continue serving price-sensitive cohorts, but bundling strategies that merge lab tests, imaging, and consults enlarge revenue per visit. Executive and celebrity-style programs, though niche, deliver outsized profit due to personalized protocols and concierge services. Pediatric packages gain traction as parents embrace preventive pediatrics, and genetic screening integration heightens early-life risk stratification.

Comprehensive providers expand partnerships with wellness platforms to integrate longitudinal data, fostering repeat visits. Cross-selling chronic-disease management subscriptions strengthens lifetime value and embeds providers deeper in patient journeys. As AI curbs reading times, capacity constraints ease, enabling wider geographic penetration of advanced services without proportionate capital outlays.

By Provider Type: Hospital Networks Exploit Continuity of Care

Hospital-based centers controlled 37.4% of the health check-up market share in 2024, using integrated care pathways to convert screening leads into treatment admissions if conditions surface. Scale permits negotiated supply costs and rapid technology adoption, preserving competitive standing.

Stand-alone diagnostic chains battle on speed and price, while at-home testing startups, growing at a 5.1% CAGR, tap convenience trends through courier-collected samples and digital portals. Corporate on-site clinics rise as employers internalize screening for productivity gains, micro-targeting workforce risk profiles. Consolidation accelerates: larger chains acquire regional labs to widen reach and secure payer contracts. Investment in AI decision support and automated analyzers becomes table stakes; laggards risk obsolescence as consumers gravitate toward data-rich, personalized experiences.

By Delivery Mode: Digital Platforms Reconfigure Access

In-clinic walk-in formats remain dominant at 46.5% of the health check-up market size in 2024, thanks to embedded clinical workflows and immediate ancillary services. Telehealth screenings, however, post the highest 6.6% CAGR as regulatory flexibilities converge with consumer digital fluency. Video triage, asynchronous symptom checkers, and app-based results dissemination lower geographic barriers and drive adherence to follow-up protocols.

Hybrid models combine at-home sample kits with virtual consultations, mitigating capacity strain on physical sites while broadening catchment areas. Mobile diagnostic vans penetrate rural settings, bringing ultrasound, X-ray, and rapid labs to underserved populations. Payment parity laws enacted in several U.S. states stabilize reimbursement, cementing telehealth’s position in mainstream screening strategies.

Geography Analysis

North America generated 35.7% of global revenues in 2024, buoyed by employer-funded wellness, high screening awareness, and mature diagnostic infrastructure. Dynamic-premium insurance programs and corporate mandates preserve demand, yet growth tempers as saturation nears and cost inflation pressures discretionary spending.

The health check-up market size in Asia-Pacific is poised for the fastest 8.6% CAGR to 2030, underwritten by expanding middle-income cohorts and rapid urbanization. China and India scale hospital and lab networks aggressively; Apollo’s plan to add 70 diagnostics labs exemplifies the push toward nationwide coverage. Medical tourism funnels patients into Singapore, South Korea, and Thailand, leveraging global-standard care at favorable price points.

Europe sustains steady uptake as universal coverage embeds preventive care; the newly published European Health Data Space Regulation promises frictionless data exchange, accelerating AI adoption across member states. Middle East & Africa and South America offer long-term upside but grapple with infrastructure deficits and affordability hurdles despite isolated public-private screening initiatives.

Competitive Landscape

Competition intensifies between incumbent chains, hospital networks, and tech-first entrants. Function Health’s acquisition of Ezra reflects a strategy to couple AI and MRI competencies, catalyzing price compression that pressures premium providers. PharmEasy’s purchase of Thyrocare illustrates consolidation as platforms seek assay throughput and nationwide logistics capacity. Prenuvo and Neko Health position themselves as direct-pay specialists, skirting coverage frictions through subscription packages and concierge pathways.

Larger hospital systems invest in proprietary AI algorithms and patient portals to maintain relevance, while partnerships with cloud providers accelerate analytic deployment. Laboratories diversify into at-home testing kits, hedging against foot-traffic volatility.

Market entry barriers are moderate: capital expenditure for imaging modalities remains high, but asset-light digital platforms lower hurdles for software-focused challengers. Intellectual-property differentiation centers on machine-learning models trained on multi-omic datasets, creating data-network effects that reward early movers. Regulatory scrutiny rises around algorithm transparency, prompting joint ventures with academic institutions to validate clinical efficacy and build trust.

Health Check-up Industry Leaders

Quest Diagnostics

Labcorp

Apollo Hospitals Enterprise Ltd.

Sonic Healthcare

SRL Diagnostics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Function Health acquired Ezra, introducing a USD 499 22-minute full-body MRI leveraging FDA-cleared AI technology.

- February 2025: Prenuvo raised USD 120 million and debuted expanded assessments, including neurological scans and detailed blood tests.

- October 2024: Labcorp released the First to Know OTC syphilis test, filling a rapidly growing STI screening gap.

Global Health Check-up Market Report Scope

| Routine / Basic Health Check-up |

| Comprehensive / Full-Body Screening |

| Disease-Specific Screening Panels |

| Executive & Celebrity Programs |

| Pediatric & Adolescent Packages |

| Hospitals & Multispecialty Centers |

| Diagnostic Chains & Labs |

| Stand-alone Preventive Clinics |

| At-home Testing Start-ups |

| Corporate On-site Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Routine / Basic Health Check-up | |

| Comprehensive / Full-Body Screening | ||

| Disease-Specific Screening Panels | ||

| Executive & Celebrity Programs | ||

| Pediatric & Adolescent Packages | ||

| By Provider Type | Hospitals & Multispecialty Centers | |

| Diagnostic Chains & Labs | ||

| Stand-alone Preventive Clinics | ||

| At-home Testing Start-ups | ||

| Corporate On-site Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the health check-up market in 2025?

The health check-up market size is USD 59.3 billion in 2025.

What is the projected growth rate through 2030?

The sector is forecast to grow at a 6.60% CAGR, reaching USD 85.5 billion by 2030.

Which region currently leads global revenues?

North America commands 35.7% of worldwide revenue, driven by corporate wellness and established infrastructure.

Which region is expanding fastest?

Asia-Pacific is on track for an 8.6% CAGR to 2030, propelled by rising middle-income populations and medical tourism.

Which service type holds the largest share?

Comprehensive full-body screenings lead with 42.5% of 2024 revenue, reflecting consumer preference for holistic diagnostics.

How are AI technologies influencing the sector?

AI shortens scan times, lowers cost per test, and enhances diagnostic accuracy, accelerating adoption and expanding access.

Page last updated on: