Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

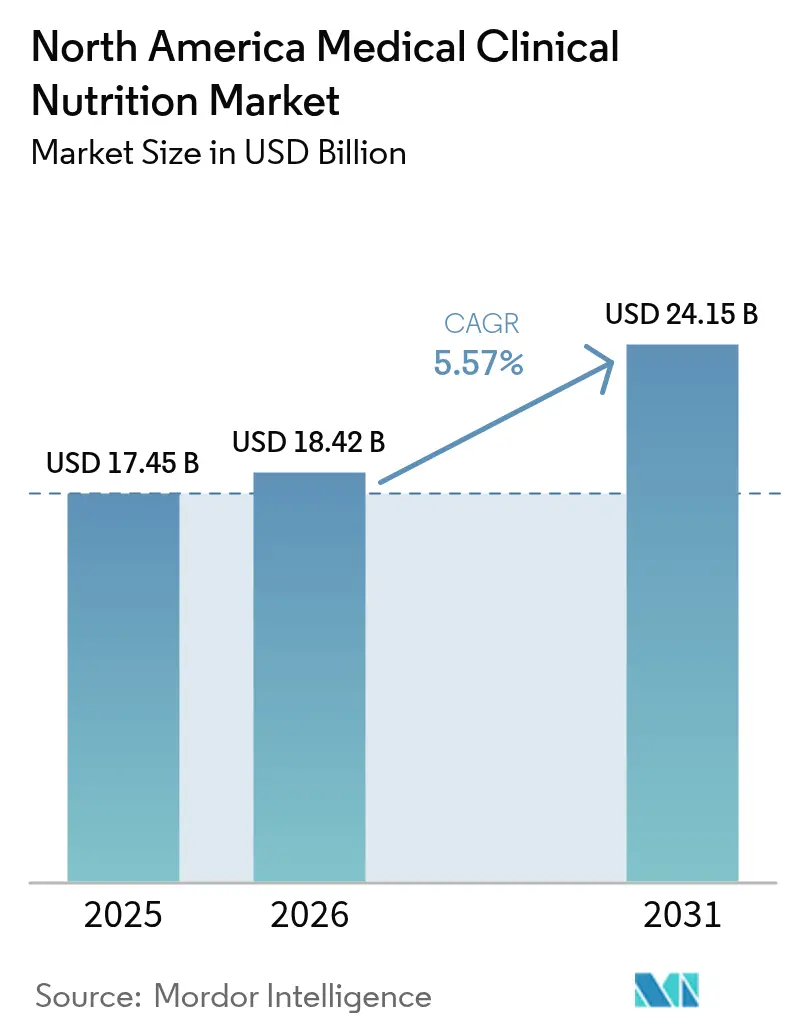

| Base Year Market Size (2025) | USD 17.45 Billion |

| Market Size (2026) | USD 18.42 Billion |

| Market Size (2031) | USD 24.15 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Medical Clinical Nutrition Market Analysis by Mordor Intelligence

North America medical clinical nutrition market size in 2026 is estimated at USD 18.42 billion, growing from 2025 value of USD 17.45 billion with 2031 projections showing USD 24.15 billion, growing at 5.57% CAGR over 2026-2031. Demand is supported by an aging population that presents multiple comorbidities and higher malnutrition risk, by payer alignment around home-based care, and by steady innovation in disease-specific enteral formulas and next-generation parenteral components. Care pathways in oncology and surgery are integrating immunonutrition modules to reduce complications and length of stay, which increases clinical adoption and formulary pull-through across hospital and home settings. Distribution is also changing as online channels build direct-to-consumer models supported by telehealth, while hospital pharmacies retain control of complex compounding and inpatient dosing. Policy updates in coverage and quality reporting continue to embed nutrition within value-based care, which raises the floor for utilization in acute and post-acute environments.

Key Report Takeaways

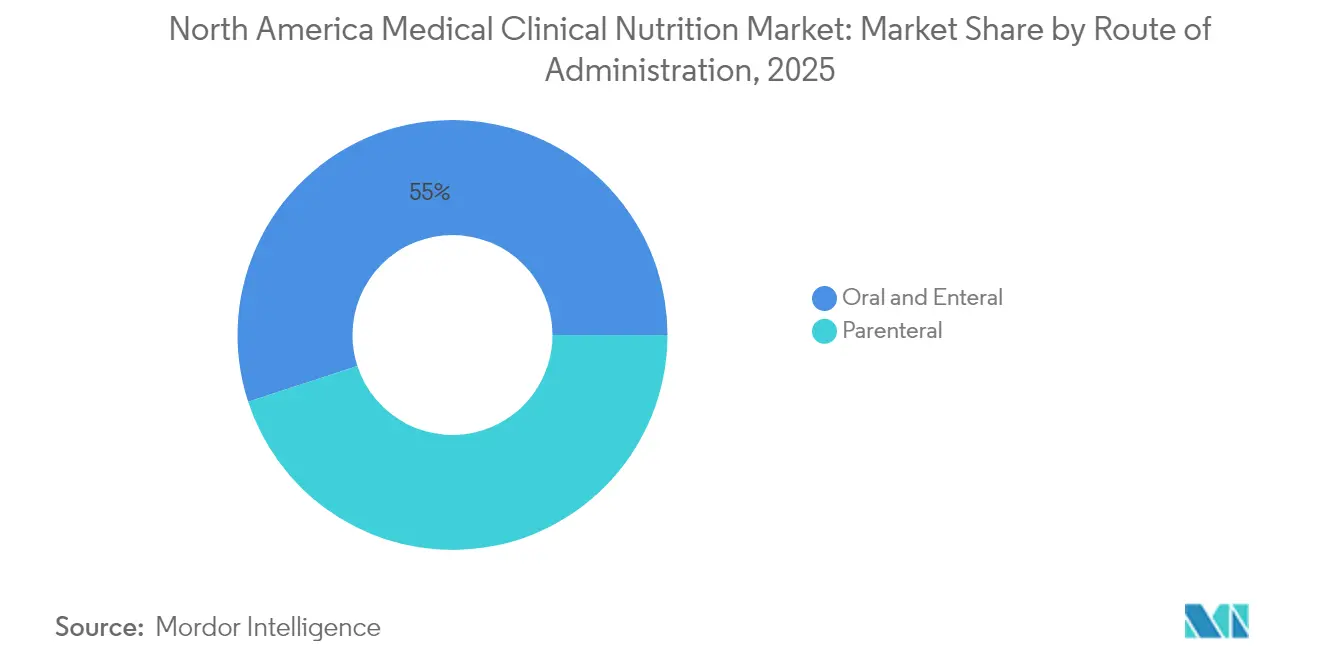

- By route of administration, oral and enteral therapies commanded a 55.02% revenue share in 2025, while Parenteral solutions are forecast to grow at a 7.40% CAGR through 2031.

- By product type, infant nutrition accounted for a 45.02% share in 2025, and the Disease-Specific Enteral Formula segment is expected to register a 7.22% CAGR from 2026 to 2031.

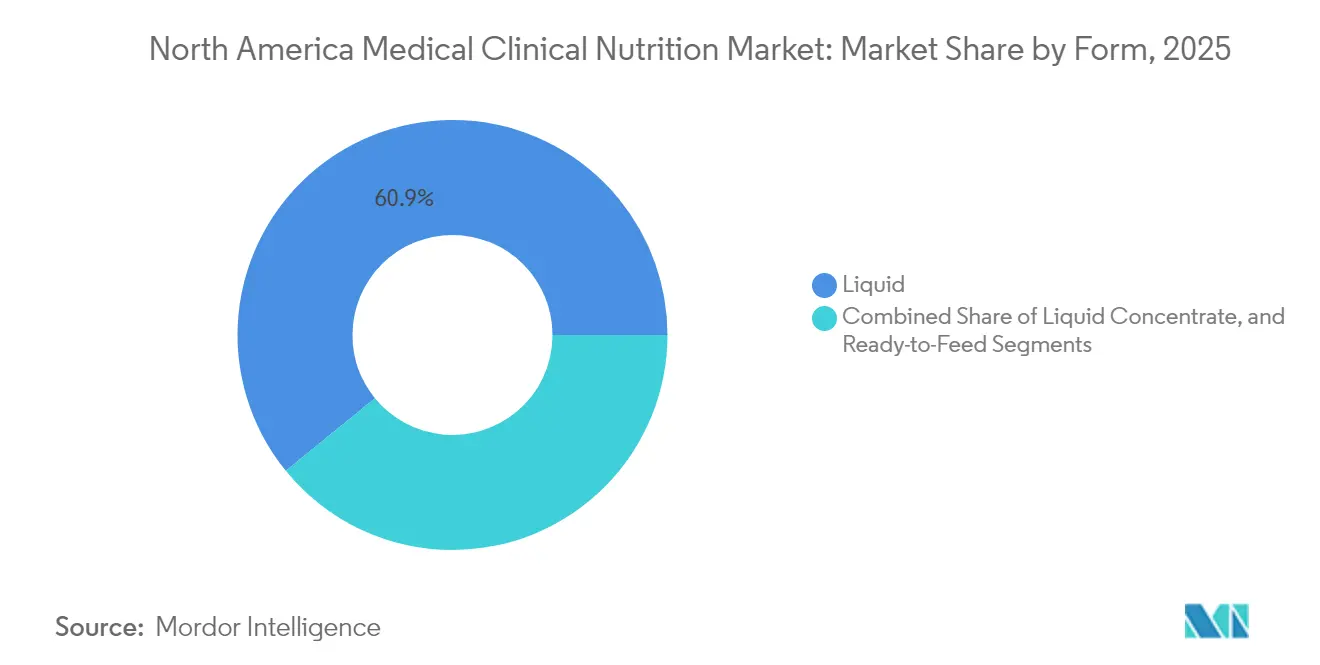

- By form, liquid formats dominated at a 60.88% share in 2025, while Semi-Solid formats are projected to grow at a 6.33% CAGR through 2031.

- By application, nutritional support for malnutrition accounted for a 33.98% share in 2025, while Cancer applications are set to expand at a 7.52% CAGR through 2031.

- By end user, hospitals and clinics represented a 56.92% share in 2025, while Home Care Settings are forecast to surge at an 8.22% CAGR through 2031.

- By distribution channel, hospital pharmacies held 55.21% of volume in 2025, while Online Pharmacies are projected to climb at an 8.52% CAGR to 2031.

- By geography, the United States anchored 82.12% of regional revenue in 2025, while Mexico is anticipated to grow at a 6.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Medical Clinical Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated chronic disease burden in North American care settings | +1.2% | United States, Canada | Long term (≥ 4 years) |

| Aging population and longer survivorship with comorbidities | +1.4% | United States, Canada, Mexico urban centers | Long term (≥ 4 years) |

| Shift toward home-based nutrition support and outpatient care pathways | +1.1% | United States, Canada | Medium term (2-4 years) |

| Innovation in disease-specific enteral formulas and next-gen PN components | +0.9% | United States, early spillover to Canada | Medium term (2-4 years) |

| CMS and payer policy changes expanding coverage for HEN/HPN and malnutrition coding | +0.7% | United States | Short term (≤ 2 years) |

| ERAS and oncology pathways integrating prehabilitation nutrition and immunonutrition | +0.3% | United States academic medical centers, Canada pilot sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated Chronic Disease Burden in North American Care Settings

Diabetes, chronic kidney disease, heart failure, and chronic obstructive pulmonary disease together create persistent malnutrition risk in hospital and community care, which heightens the need for medical clinical nutrition when standard oral diets are inadequate. Hospitals have reinforced admission screening protocols with validated tools, and positive screens increasingly trigger same-day dietitian consults and orders for enteral nutrition, aligning care processes with quality and readmission metrics[1]American Society for Parenteral and Enteral Nutrition, “Malnutrition Quality Improvement Initiative,” American Society for Parenteral and Enteral Nutrition, nutritioncare.org. Hospital readmissions policies and value-based purchasing programs press administrators to address nutrition earlier in stays and at transitions of care, which steers more patients to structured oral, enteral, or parenteral regimens when indicated. Specialty societies have disseminated guidance on disease-specific formulas, including renal formulas with controlled electrolytes and diabetes formulas with lower glycemic impact, though coverage inconsistencies continue to push facilities to absorb costs within bundled payments. Penalties linked to hospital-acquired conditions such as pressure injuries also encourage early enteral nutrition to support skin integrity and mobility goals where clinically appropriate. Provider accreditation standards that require documented nutrition care plans have embedded clinical nutrition into routine quality metrics, which supports sustained demand across the North America medical clinical nutrition market.

Aging Population and Longer Survivorship with Comorbidities

Population aging in North America increases the share of older adults living with multimorbidity, which raises prevalence of dysphagia, anorexia, and other contributors to inadequate oral intake that require clinical nutrition support in acute, post-acute, and home settings. Long-term care facilities report high baseline malnutrition rates on admission, which leads to escalation from oral supplements to enteral tube feeding when adherence and tolerance falter despite counseling and flavor rotation. Payment models in skilled nursing tie reimbursement to documented malnutrition status and treatment, which incentivizes more consistent screening, diagnosis, and product use among residents who are at sustained risk. Cancer survivorship trends have extended nutrition needs well beyond active treatment due to late effects that impair intake or absorption, which strengthens ongoing demand for disease-specific enteral options and, when necessary, parenteral nutrition[2]National Cancer Institute SEER, “Cancer Stat Facts,” National Cancer Institute, cancer.gov. Home health programs increasingly embed dietitians and leverage telehealth for counseling and e-prescribing of oral supplements to reduce logistical barriers for older adults and caregivers, a shift that aligns with broader virtual care adoption in Medicare and commercial plans.

Shift Toward Home-Based Nutrition Support and Outpatient Care Pathways

Enrollment growth in Medicare Advantage has encouraged health plans and integrated delivery networks to shift eligible patients from inpatient care toward home enteral nutrition and home parenteral nutrition support programs, which improves cost containment while maintaining clinical oversight through remote monitoring and nursing support. Specialty pharmacies have expanded home parenteral nutrition capabilities including sterile compounding, patient education, and around-the-clock support, which broadens access for conditions beyond short-bowel syndrome when supported by medical necessity documentation and payer approval. National coverage policies for enteral and parenteral nutrition define medical necessity for beneficiaries with impaired gastrointestinal function, and alignment across Medicare Administrative Contractors continues to shape documentation practices that home infusion providers must satisfy to ensure compliant billing. Durable medical equipment suppliers now deliver pumps, sets, and formula in integrated arrangements that simplify ordering and billing for prescribers and patients in eligible scenarios. Outpatient infusion centers that operate within hospital systems or as independent clinics have become an intermediate option for patients who need episodic parenteral support during cancer treatment or inflammatory disease flares, which reduces inpatient stays while preserving clinical supervision[3]American Society of Health-System Pharmacists, “Sterile Compounding Guidelines,” American Society of Health-System Pharmacists, ashp.org. Several states have clarified or expanded Medicaid medical nutrition benefits for pediatric and adult beneficiaries with defined conditions, which supports adoption of home enteral nutrition within family-centered care models.

Innovation in Disease-Specific Enteral Formulas and Next-Gen PN Components

Product development has shifted toward functional ingredient combinations that address disease-specific needs, including prebiotics, probiotics, omega-3 fatty acids, and HMB, which reflects a more targeted approach to clinical nutrition. Immunonutrition protocols in gastrointestinal cancer surgery have shown benefits for infection rates and length of stay in randomized trials, which has heightened interest among surgeons and dietitians in perioperative nutrition programs built around arginine-enriched and omega-3-supplemented formulas. Renal formulas are being reformulated to align with updated electrolyte recommendations from nephrology guidelines, including phosphorus management targets, which supports safer energy delivery without fluid overload in advanced kidney disease populations. Parenteral nutrition now incorporates structured lipid emulsions and multi-oil blends that aim to improve hepatic tolerance and reduce inflammatory markers in long-term support, and recent regulatory approvals have expanded the options available to hospital and home infusion programs. Guidance on medical foods outlines the evidentiary and labeling expectations for disease-specific products, which heightens documentation rigor for manufacturers bringing new formulas to market in the United States. Multi-chamber PN bags promising lower compounding error rates and faster throughput continue to gain adoption in hospitals and ambulatory infusion centers that face pharmacy staffing constraints, although clinicians still weigh the trade-off between fixed ratios and personalized dosing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of clinical nutrition products and specialized formulas | -0.6% | United States, Canada, Mexico | Medium term (2-4 years) |

| Coverage gaps and reimbursement variability across payers and states | -0.8% | United States, state-level Medicaid programs | Short term (≤ 2 years) |

| PN amino acid/lipid supply disruptions and domestic capacity constraints | -0.5% | United States, Canada | Short term (≤ 2 years) |

| Sterile compounding (USP <797>) burden and pharmacy staffing limiting PN availability | -0.4% | United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Clinical Nutrition Products and Specialized Formulas

Disease-specific enteral formulas are priced at a premium relative to standard polymeric options, which creates affordability challenges for patients who do not have coverage for medical foods or who lack eligibility for durable medical equipment benefits in outpatient settings. Medicare Part B coverage is limited to enteral nutrition administered via a feeding tube for beneficiaries with documented gastrointestinal impairment, and oral nutritional supplements are generally excluded from coverage, which shifts costs to patients or facilities upon discharge. Home parenteral nutrition imposes a significant cost burden when factoring compounded solutions, equipment, nursing, and monitoring, and high deductibles or coinsurance can become a barrier to access for insured patients without targeted benefit design. Long-term care facilities operate with per-diem reimbursement and often face a gap between the incremental cost of disease-specific formulas and the financial recognition available through case-mix adjustments, which constrains upgrades from standard formulas despite clinical indications. Prior authorization and formulary workflows remain complicated for enteral products that do not carry standard pharmacy identifiers, and operational friction delays therapy initiation during care transitions. Patients leaving the hospital may encounter retail prices that far exceed institutional contract rates negotiated through group purchasing organizations, which can depress adherence and increase the risk of readmission.

Coverage Gaps and Reimbursement Variability Across Payers and States

State Medicaid programs apply variable quantity limits and documentation requirements for enteral formula, which can constrain access for beneficiaries who rely on exclusive tube feeding if prescribers and clinics lack dedicated administrative capacity to meet prior authorization demands. Commercial payer policies increasingly use step therapy for disease-specific formulas, and delays in approval can expose patients to avoidable complications when standard formulas are not tolerated or are contraindicated. Medicare Administrative Contractors maintain LCDs that interpret national coverage for parenteral nutrition differently, which leads to variable acceptance of oncology indications such as cancer-related cachexia relative to short-bowel syndrome or irreversible motility disorders, and appeals may be required to secure coverage for eligible patients. Lack of a distinct outpatient code for malnutrition assessment by registered dietitians reduces reimbursement for nutrition counseling visits, and many plans bundle these services under broader evaluation and management codes, which understates the clinical complexity of medical nutrition therapy. State insurance mandates commonly cover pediatric amino acid formulas for severe allergies, while adult patients with analogous conditions may face exclusions based on plan design and lack of parity in benefit coverage. Self-insured employer plans governed by ERISA are exempt from state benefit mandates, which creates variability in coverage and leaves gaps for working-age patients who need enteral or parenteral support outside of Medicare or Medicaid.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Outpatient Migration Lifts Parenteral Segment

Oral & Enteral modalities captured 55.02% of North America medical clinical nutrition market share in 2025, while Parenteral nutrition is forecast to expand at a 7.40% CAGR from 2026 to 2031. Growth in parenteral reflects critical-care demand when enteral access is contraindicated, including oncology and surgical ICU scenarios, and rising enrollment in structured home parenteral nutrition programs that are justified by clinical necessity and supported by payer programs. In parallel, the North America medical clinical nutrition market is responding to product innovation in lipid emulsions that move away from pure soybean oil toward mixed-oil or structured lipid systems intended to mitigate hepatic stress and inflammation in long-term use. Oral & Enteral therapies retain primacy because they preserve gut integrity and align with enteral-first guidelines for nutrition support where feasible. Utilization trends show moderating growth in long-term tube feeding in mature U.S. and Canadian facility markets, where skilled nursing penetration is already high and care models are optimizing transitions to home. The North America medical clinical nutrition market continues to benefit from standardized nutrition screening and intervention requirements in hospitals, which systematically identify candidates for enteral therapy earlier in the episode.

Parenteral pathways face longer regulatory timelines because components are regulated as drugs, which elongates development cycles and increases evidence and manufacturing requirements for new entrants. Enteral products marketed as medical foods can proceed under a distinct framework provided they meet criteria for dietary management of a disease under physician supervision, which lowers barriers for formulation updates that address disease-specific needs. The North America medical clinical nutrition market is also shaped by conditions of participation and accreditation that require hospitals to have enteral feeding protocols to prevent malnutrition-linked complications and readmissions. As home infusion capabilities have grown, parenteral support has become more viable for select patients outside the hospital, which supports the projected 7.40% growth trajectory with the added benefit of patient preference and autonomy in administration schedules. Documentation demands from Medicare Administrative Contractors continue to shape HPN access, which solidifies appropriate utilization while increasing administrative workload for pharmacies that manage complex cases. This combined regulatory and clinical landscape reinforces a measured shift toward parenteral growth while preserving enteral predominance where gastrointestinal function allows.

By Product Type: Disease Precision Overtakes Volume Commodities

Infant Nutrition commanded 45.02% share in 2025, while Disease-Specific Enteral Formula is expected to register a 7.22% CAGR through 2031 as oncology, diabetes, and renal populations adopt formulas designed for metabolic and functional needs. Standard enteral formulas remain widely used in long-term care and home settings, but price competition through group purchasing channels is compressing margins and encouraging differentiation via clinical outcomes data. The North America medical clinical nutrition market is seeing ongoing supply vigilance for parenteral components, including amino acid solutions and lipid emulsions listed on drug shortage databases in 2024, which prompted allocation policies and, in some cases, deferral of elective procedures that rely on post-operative PN. Disease-specific products are backed by published evidence of improved glycemic control in diabetes formulas and electrolyte balancing in renal formulas, which improves formulary positioning and supports premium pricing in institutions that measure outcome-linked value. Infant Nutrition demand is sustained by clinical need in preterm and allergy-prone populations despite broader fertility trends, and pediatric specialty formulas continue to receive attention around safety, quality, and recall responsiveness due to the unique vulnerability of infants. The North America medical clinical nutrition market is also influenced by public programs such as WIC, which shape product access and competitive dynamics through state contracting and distribution arrangements.

Disease-Specific Enteral Formula growth is tied to oncology protocols that embed immunonutrition during perioperative care and survivorship, which increases patient eligibility over time as more cancer programs standardize nutrition pathways. Formulations now often include immunity-supporting nutrients and microbiome-oriented prebiotic fibers to support gut integrity during treatment. Manufacturers face evolving expectations for clinical substantiation, labeling, and claims for medical foods, and companies with robust clinical development programs can differentiate through outcomes and safety profiles. In parallel, the North America medical clinical nutrition market benefits from strengthened safety surveillance and recall readiness under the Infant Formula Act, which has raised quality controls and transparency for pediatric products. Pediatric coverage through WIC and private payers continues to support baseline volume in the Infant Nutrition category, while disease-specific adult formulas drive the incremental growth story as clinicians target narrower indications with higher acuity needs. This mix of volume categories and high-value disease-specific niches defines product strategy and portfolio management across manufacturers.

By Form: Semi-Solid Gains as Dysphagia Prevalence Climbs

Liquid formats held a 60.88% share in 2025 given their ready-to-use convenience for tube feeding and oral supplementation, while Semi-Solid formats are projected to grow at a 6.33% CAGR from 2026 to 2031 due to the needs of dysphagia populations who cannot tolerate thin liquids. Powder forms grow at the market rate based on their extended shelf life and lower shipping costs that fit home delivery and export channels. Semi-Solid options, including puddings, thickened beverages, and hybrid gels, have gained traction in long-term care with the spread of standardized texture-modified diets and consistency levels to reduce aspiration risk. Liquids retain dominance due to ease of administration with enteral pumps and infection control advantages with ready-to-hang closed systems in inpatient and skilled nursing settings. The North America medical clinical nutrition market reflects growing caregiver education around reconstitution accuracy, which has helped reduce variability for powders through unit-dose packaging and clearer instructions. Facilities and accrediting bodies continue to monitor aspiration rates and feeding protocols, which strengthens the role of consistent texture standards and supports the shift to semi-solids when indicated.

Powder products remain relevant for infant formulas and several disease-specific items that require onsite mixing to tailor caloric density or osmolality. Manufacturers have worked to minimize preparation errors through pre-measured packets and visual guides that reduce the risk of under- or over-dilution. The North America medical clinical nutrition market is also impacted by state-level requirements around dysphagia screening in nursing homes and hospitals, which influence the demand for thickening agents and pre-thickened liquids used to prevent aspiration events. Food additive rules that apply to thickeners require safety documentation and Generally Recognized as Safe status, which shapes product formulations offered in the United States. As facilities standardize IDDSI-based protocols, procurement teams adjust the mix of liquids, powders, and semi-solids to meet diet orders while maintaining staff efficiency and patient acceptance. This balance is likely to keep liquids at the core of inpatient use while semi-solids carve out a faster growth lane in long-term care and home environments.

By Application: Oncology Integration Rewrites Treatment Algorithms

Nutritional Support for Malnutrition represented 33.98% of application share in 2025, while Cancer applications are projected to expand at a 7.52% CAGR through 2031 as perioperative and supportive care pathways embed prehabilitation and immunonutrition. Gastrointestinal diseases such as inflammatory bowel disease and short-bowel syndrome continue to require elemental enteral nutrition and, in defined cases, home parenteral nutrition that is documented against medical necessity criteria. Administrative scrutiny and audits by payers around appropriate-use standards have slowed volume growth in some indications even as clinical need persists. Metabolic disorders represent smaller but higher value niches, with specialized formulas designed for inborn errors and mitochondrial dysfunction that require tight composition controls. Neurological diseases including ALS and Parkinson’s disease sustain long-term enteral demand, bolstered by advocacy and Medicaid policy updates that improve access to home-based care for patients with gastrostomy needs. Other use cases in surgical recovery and trauma continue to grow within hospital quality frameworks that link malnutrition intervention to outcome metrics, which keeps enteral nutrition embedded in perioperative checklists.

Cancer programs are adopting structured nutrition interventions across surgical, radiation, and medical oncology, with protocols that use arginine-enriched and omega-3-supplemented formulas to mitigate surgical stress and reduce infectious complications. Oncology nutrition needs often persist into survivorship due to late effects like radiation enteritis and neuropathies that impair intake, which sustains demand for both oral and enteral support beyond acute treatment. The North America medical clinical nutrition market benefits from the inclusion of nutrition screening in survivorship guidance and accreditation standards, which reinforces routine assessment and early intervention. Hospitals and ambulatory oncology centers adapt order sets in their electronic records to include nutrition consult triggers, which reduces missed opportunities for early support. For patients who cannot meet needs enterally due to treatment-related impairment, outpatient PN and home PN provide a safety net under carefully documented medical necessity, adding to the momentum in cancer-related applications. As more institutions implement Enhanced Recovery After Surgery pathways, immunonutrition moves from optional to standard in select disease sites, which accelerates adoption across the North America medical clinical nutrition market.

By End User: Home Settings Eclipse Institutional Growth

Hospitals & Clinics accounted for 56.92% of end-user share in 2025, while Home Care Settings are forecast to grow at an 8.22% CAGR to 2031 as value-based care moves eligible patients to outpatient and home environments. Specialty pharmacies coordinate enteral and parenteral deliveries, durable medical equipment, and nursing support that enables rapid transition to home for clinically stable patients. Hospitals prioritize early discharge to lower-cost sites of care within bundled payment models, which drives consistent referral to home enteral and parenteral nutrition and reduces readmission risk through closer therapy management. Long-term care growth is moderated by staffing constraints and occupancy trends, even as facilities adopt point-of-care tools that speed enteral tube placement confirmation and feeding initiation. Home Care adoption is supported by remote monitoring for weight and intake, which allows clinicians to adjust plans and preempt complications that would otherwise result in emergency visits. The North America medical clinical nutrition market also benefits from state pharmacy and home health regulations that formalize dietitian involvement and patient education, creating more predictable care standards.

Licensure and accreditation requirements for home infusion and home health agencies set operational baselines for sterile compounding, infection control, and patient training, which contributes to standardized quality in home settings. Hospitals maintain dominance in the highest-acuity cases and in complex parenteral dosing protocols that require individualized compounding and lab monitoring. The North America medical clinical nutrition market is seeing enhanced interoperability between hospital electronic health records and specialty pharmacy systems, which supports accurate order translation and continuity of care. Long-term care facilities absorb enteral formula costs within per-diem payments, which influences product selection and may favor standard formulas when clinical differentiation is not explicitly reimbursed. Home settings continue to grow as telehealth reimbursement stabilizes and remote care technology becomes commonplace in nutrition support, which helps maintain adherence and safety while lowering total cost of care. This end-user mix illustrates how the North America medical clinical nutrition market aligns with payer incentives to move care to the lowest appropriate site while sustaining hospital expertise for the most complex cases.

By Distribution Channel: Digital Direct-to-Consumer Rewires Access

Hospital Pharmacies held 55.21% of distribution-channel volume in 2025, while Online Pharmacies are projected to climb at an 8.52% CAGR by 2031 as subscription models and telehealth ordering connect patients directly to therapy. Retail Pharmacy growth is steady but constrained by shelf-space limitations and pharmacist training gaps in medical nutrition counseling relative to disease-specific selection and prior authorization pathways. Homecare and specialty clinics leverage bundled reimbursement to coordinate product, administration, and lab monitoring in one episode of care, which fits payer expectations around total cost control and patient satisfaction. Hospital Pharmacies remain central due to formulary authority, sterile compounding infrastructure, and tight integration with electronic health records that prompt nutrition orders following malnutrition diagnosis capture, though net margins are pressured by 340B dynamics and group purchasing contracts. The North America medical clinical nutrition market is also benefiting from online portals that allow personalization, automated refills, and secure messaging with dietitians, which can reduce abandonment and improve adherence. Retail chains are piloting in-store nutrition counseling partnerships to raise awareness among commercially insured patients, and these models could improve product selection for complex cases pending reimbursement.

Homecare and specialty clinics are expanding via consolidation that spreads capital costs for compounding and clinical staff over a larger patient base, which yields better manufacturer pricing and steadier access during supply constraints. State pharmacy boards regulate mail-order and sterile compounding activities, which sets baseline expectations for safe distribution of parenteral components. Track-and-trace requirements under the Drug Supply Chain Security Act apply to relevant parenteral products and support supply integrity across hospital and ambulatory channels. The North America medical clinical nutrition market is watching payer outcomes measures for home infusion providers, which link payment to infection rates and patient-reported outcomes, and these expectations are shaping vendor selection and quality oversight. As digital engagement matures, online channels are likely to capture a larger share of oral and enteral products while PN remains largely coordinated by hospital pharmacies and accredited home infusion providers. This evolution will give patients more control over ordering and refills while preserving safety-critical handling for parenteral therapies.

Geography Analysis

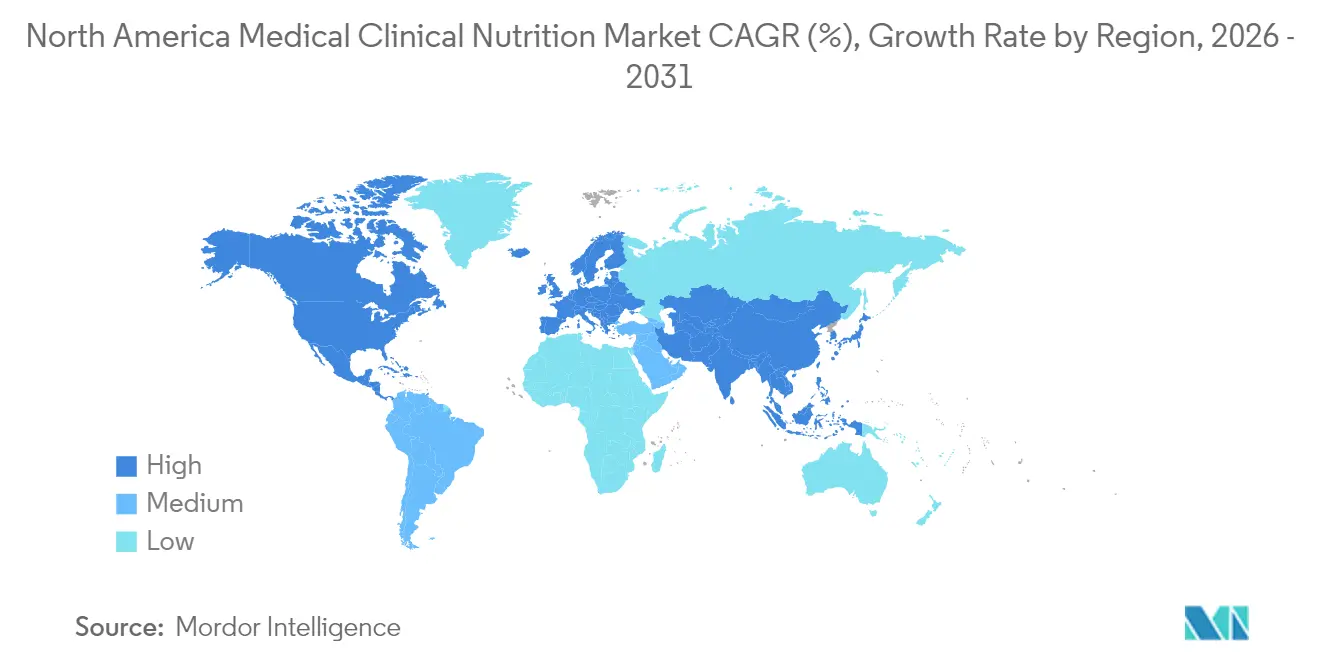

The United States anchored 82.12% of regional revenue in 2025, reflecting the scale of Medicare and Medicaid programs and a large hospital infrastructure where standardized nutrition screening and intervention are embedded in quality reporting. Mexico is projected to grow at a 6.45% CAGR from 2026 to 2031 due to national prevention strategies that integrate malnutrition screening in public clinics and expanding private insurance uptake in major urban centers. Canada posts steady growth near the regional average under provincial programs that cover home enteral and parenteral nutrition for defined indications, and a federal regulatory framework that aligns well with U.S. standards for medical foods and parenteral drugs. The North America medical clinical nutrition market benefits from U.S. quality programs that incentivize accurate malnutrition coding and earlier nutrition intervention, which links to purchasing behavior for enteral formulas and staffing for nutrition services. Canada’s reliance on U.S.-manufactured parenteral components can expose facilities to allocation stress during U.S. shortages, which underscores the importance of diversified sourcing and regional compounding capacity. Mexico’s regulatory reforms to streamline import permits for medical foods have reduced lead times and improved availability for distributors that serve hospitals and home care, which aids adoption of disease-specific products.

In the United States, oncology programs tied to NCI-designated centers are expanding perioperative immunonutrition protocols, and these standards flow to community networks through integrated care pathways and professional society education. The North America medical clinical nutrition market is also influenced by FDA guidance for medical foods and PN drugs, which sets evidentiary floors and shapes manufacturer development plans. Provincial coverage in Canada commonly includes HEN and HPN for eligible conditions, which supports continuity between hospital discharge and home settings. Mexican demand is further supported by rising diabetes burden and by private insurers that add disease-specific nutrition coverage to differentiate benefits in competitive metro markets. National screening and labeling standards enforced by health authorities in each country continue to shape product claims and marketing practices for both oral and enteral nutrition. As providers and payers harmonize their expectations around outcomes, nutrition support remains integral across acute, post-acute, and home environments in all three countries.

The North America medical clinical nutrition market size for the United States reflects strong hospital utilization due to standardized malnutrition screening and ties to value-based purchasing, while Canada and Mexico are building capacity in home-based models that open access to HEN and HPN in more regions. Supply reliability and cross-border logistics remain central to Canadian planning for PN components, and provincial systems continue to invest in compounding capability and pharmacy staffing to mitigate risks. Mexico’s reforms on import authorization and labeling transparency help streamline entry for global manufacturers that provide specialized enteral products, which reduces costs and broadens formulary choice in hospitals and retail. The North America medical clinical nutrition market continues to track policy developments in each country’s reimbursement and regulatory schemes because these directly shape clinical adoption, site-of-care decisions, and procurement across inpatient and outpatient pathways. Collectively, these geographic differences define where growth outperforms the regional average and where stability grants predictability for budget planning and product allocation. As cross-border collaboration increases around standards and best practices in clinical nutrition, product portfolios and care models are likely to converge across North America over the forecast horizon.

Competitive Landscape

The North America medical clinical nutrition market shows moderate consolidation, with four scaled incumbents maintaining broad portfolios and established relationships with hospitals, long-term care facilities, and home infusion networks. Abbott Laboratories, Fresenius Kabi, Nestlé Health Science, and Baxter International defend their positions through R&D, manufacturing depth, and distribution breadth, and together they hold an estimated 60% share in 2024. Challenger brands are growing by addressing patient preferences for plant-based and hypoallergenic ingredients, which wins adoption in pediatric and adult intolerance cases when clinical parity is demonstrated. Kate Farms and Functional Formularies have gained formulary consideration through clinical and tolerance data and through alignment with clean-label preferences in many health systems. Incumbents invest in vertical integration that improves supply resiliency, with Fresenius Kabi’s API manufacturing and Baxter’s compounding footprint being examples of structural advantages during PN component shortages. Strategic partnerships between manufacturers and home infusion providers are expanding to coordinate education, automation, and logistics, which reduces operating costs and enhances patient outcomes in home PN programs.

Recent announcements reflect continued investment and portfolio expansion across product categories and sites of care. Abbott expanded specialized enteral formula manufacturing capacity to support export to North America and to improve responsiveness to hospital formulary shifts toward immunonutrition. Fresenius Kabi secured FDA approval for a structured lipid emulsion designed for long-term PN use, which addresses infection and tolerance concerns that have constrained adoption in home settings. Nestlé Health Science is pursuing digital enablement through partnerships with national pharmacy chains for direct-to-patient subscription models that integrate dietitian consults, which improves adherence and reduces abandonment. Baxter deepened its presence in compounding and home PN by acquiring a specialty network across multiple states, which supports growth in outpatient parenteral support under Medicare Advantage and commercial plans. The North America medical clinical nutrition market also sees capital directed to new compounding facilities for multi-chamber PN bags, which increase supply resilience and reduce in-hospital compounding burdens.

Competitive dynamics are shaped by policy, safety, and economics. The 340B Drug Pricing Program and group purchasing contracts influence net pricing and margin profiles for hospital pharmacies that coordinate inpatient nutrition support. USP <797> revisions raise expectations for sterile compounding, which requires incremental investment and staffing that incumbents can absorb more easily than smaller entrants. FDA enforcement on labeling and evidence for medical foods sets clear expectations for disease-specific products, which advantages companies with clinical trial infrastructure. As product portfolios shift toward higher-acuity segments with stronger clinical evidence, incumbents and disruptors are likely to converge on hybrid models that combine hospital, home infusion, and digital direct channels. The North America medical clinical nutrition market is expected to remain competitive with innovation centered on immunonutrition, structured lipids, microbiome-informed formulations, and digital adherence tools that meet payer and provider expectations for measurable outcomes.

North America Medical Clinical Nutrition Industry Leaders

-

Danone Nutricia

-

Fresenius Kabi

-

Nestlé Health Science

-

Baxter International Inc.

-

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: OmniActive received FDA GRAS clearance for Lutemax Free Lutein in infant-formula applications, enabling brain and eye development support.

- April 2025: Abbott Laboratories launched a new immunonutrition formula specifically designed for oncology patients undergoing chemotherapy.

- March 2025: Nestlé Health Science completed the acquisition of a specialized pediatric nutrition company for USD 1.2 billion, expanding its portfolio of products for children with rare metabolic disorders.

- February 2025: Fresenius Kabi received FDA approval for a next-generation parenteral nutrition solution featuring an improved lipid emulsion with enhanced stability and reduced inflammatory potential.

- December 2024: Danone (Nutricia) launched a comprehensive digital platform for healthcare professionals to monitor patients on home enteral nutrition, featuring remote adjustment capabilities and integration with electronic health records.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the North American clinical nutrition market as the aggregate spending on science-based oral, enteral, and parenteral nutrition products that are prescribed or recommended to manage disease-related malnutrition, metabolic disorders, or recovery-critical conditions across hospitals, long-term care, and home-care settings. All figures are recorded at manufacturer selling price and expressed in constant 2024 US dollars.

Scope exclusion: Sports nutrition powders, standard multivitamin tablets, and over-the-counter wellness drinks not marketed for clinical use are kept outside the model.

Segmentation Overview

-

By Route of Administration

- Oral & Enteral

- Parenteral

-

By Product Type

- Infant Nutrition

- Standard Enteral Formula

- Disease-Specific Enteral Formula

- Total Parenteral Nutrition (TPN) Components

-

By Form

- Powder

- Liquid

- Semi-Solid

-

By Application

- Nutritional Support for Malnutrition

- Metabolic Disorders

- Gastrointestinal Diseases

- Cancer

- Neurological Diseases

- Other Diseases

-

By End User

- Hospitals & Clinics

- Long-term Care Facilities

- Home Care Settings

-

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Homecare & Specialty Clinics

-

Geography

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

We interviewed dietitians in tertiary hospitals, procurement heads at group purchasing organizations, and product managers from leading suppliers across the United States, Canada, and Mexico. These conversations validated average selling prices, patient penetration rates, and reimbursement dynamics, filling gaps that secondary data alone could not bridge.

Desk Research

Our analysts mapped publicly available datasets such as CDC's National Health Interview Survey, CMS hospitalization statistics, UN Comtrade import codes for HS 2106.90, and the American Society for Parenteral and Enteral Nutrition's adoption surveys. Company 10-Ks, FDA 510(k) clearances, and peer-reviewed journals in Clinical Nutrition further informed product mix shifts. Paid utilities, including D&B Hoovers for manufacturer revenue splits and Dow Jones Factiva for transaction news, helped refine baseline shares. The sources cited here are illustrative; a wider pool was examined for cross-checks and clarification.

Market-Sizing & Forecasting

The model starts with a top-down reconstruction of demand from inpatient discharge counts, pre-term birth prevalence, diabetes incidence, and average length of home enteral support. These pools are multiplied by clinically accepted kcal-per-day norms to estimate volume. Selective bottom-up checks, supplier shipment audits, and sampled ASP × volume for high-share formulas adjust totals. Key variables such as Medicare reimbursement ratios, infant formula import volumes, and obesity-linked surgery rates feed a multivariate regression that projects revenue through 2030. Where facility-level figures were partial, assumptions were normalized using three-year moving averages before final triangulation.

Data Validation & Update Cycle

Outputs pass two analyst reviews, anomaly screens against external trade values, and variance tests versus prior editions. The study refreshes annually, with interim updates triggered by material recalls, reimbursement code changes, or mergers. A final pre-publication sweep ensures clients receive the latest vetted view.

Credibility Corner: Why Mordor's North America Clinical Nutrition Baseline Stands Firm

Published estimates differ because firms pick divergent product sets, pricing bases, and refresh rhythms.

Key gap drivers include exclusion of home-care channels, omission of parenteral bags, or reliance on single-year supplier revenues, all of which understate the region's true demand captured by Mordor's broader scope and annual model recalibration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 31.73 B (2025) | Mordor Intelligence | - |

| USD 17.92 B (2024) | Regional Consultancy A | Leaves out parenteral nutrition and Mexico; models hospital procurement only |

| USD 10.53 B (2024) | Global Consultancy B | Uses top-supplier revenue extrapolation; omits OTC oral supplements and home-care sales |

These contrasts show that our disciplined variable selection and twice-validated mix of top-down and bottom-up logic deliver a balanced, transparent baseline that decision-makers can reproduce and trust.

Key Questions Answered in the Report

What is the current size and growth outlook for the North America medical clinical nutrition market?

The North America medical clinical nutrition market size is USD 18.42 billion in 2026 and is forecast to reach USD 24.15 billion by 2031 at a 5.57% CAGR over 2026-2031.

Which application area is growing fastest in North America medical clinical nutrition?

Cancer applications are projected to grow at a 7.52% CAGR through 2031, supported by perioperative and supportive care protocols that adopt immunonutrition.

Which route of administration is expected to outpace overall growth in North America medical clinical nutrition?

Parenteral nutrition is forecast to expand at a 7.40% CAGR through 2031 as critical-care use and home PN programs scale.

Which product types lead usage in North America medical clinical nutrition, and which are accelerating?

Infant Nutrition held 45.02% share in 2025, while Disease-Specific Enteral Formula is set to register a 7.22% CAGR through 2031.

What end-user setting is growing the fastest in North America medical clinical nutrition?

Home Care Settings are expected to grow at an 8.22% CAGR as value-based care shifts clinically stable patients to home-based support.

Which distribution channel shows the strongest growth in North America medical clinical nutrition?

Online Pharmacies are projected to climb at an 8.52% CAGR, supported by subscriptions and telehealth-enabled ordering.

Page last updated on: