Web Content Management (WCM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.57 Billion |

| Market Size (2031) | USD 32.18 Billion |

| Growth Rate (2026 - 2031) | 14.21% CAGR |

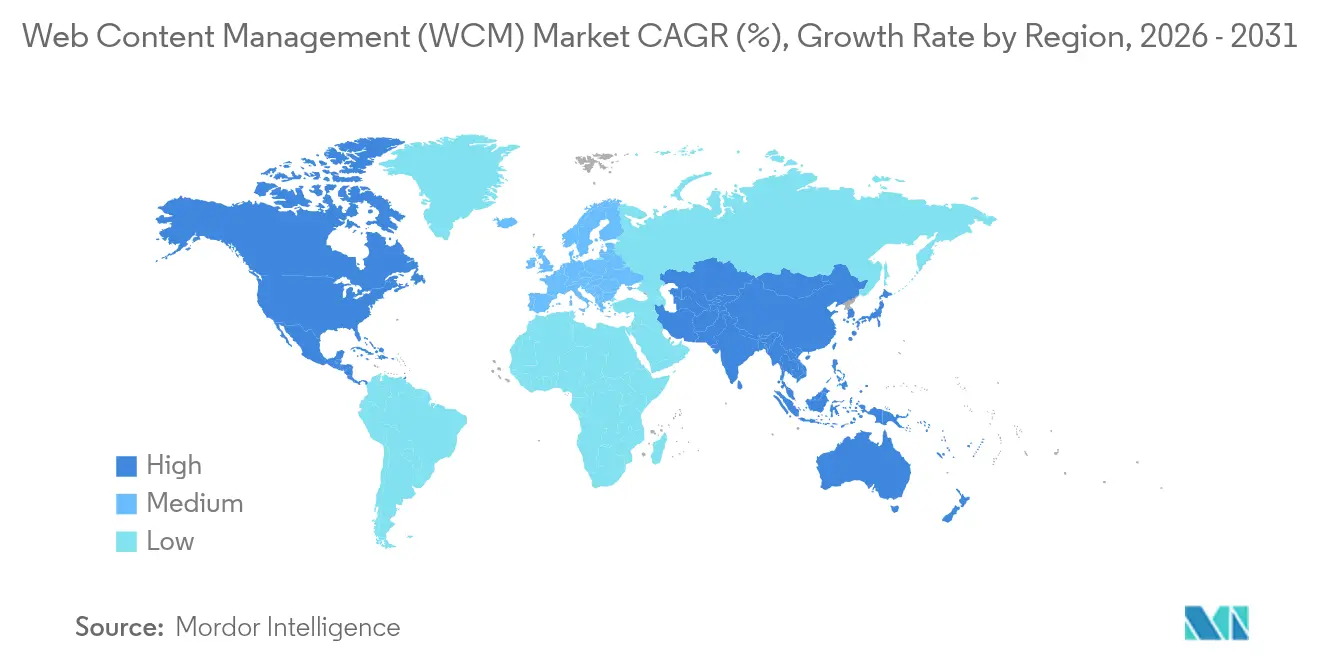

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

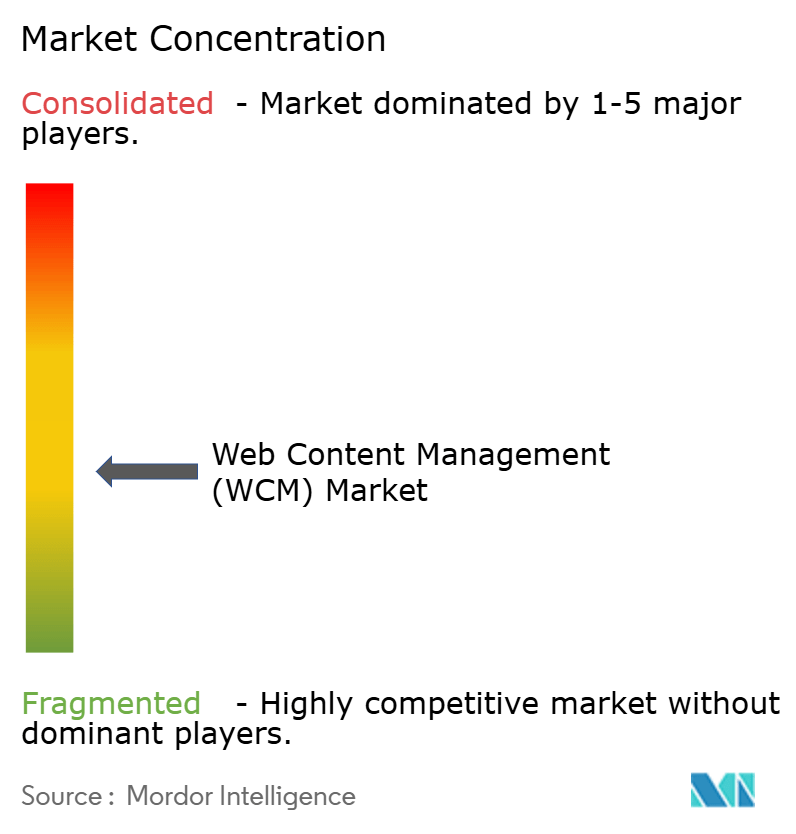

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Web Content Management (WCM) Market Analysis by Mordor Intelligence

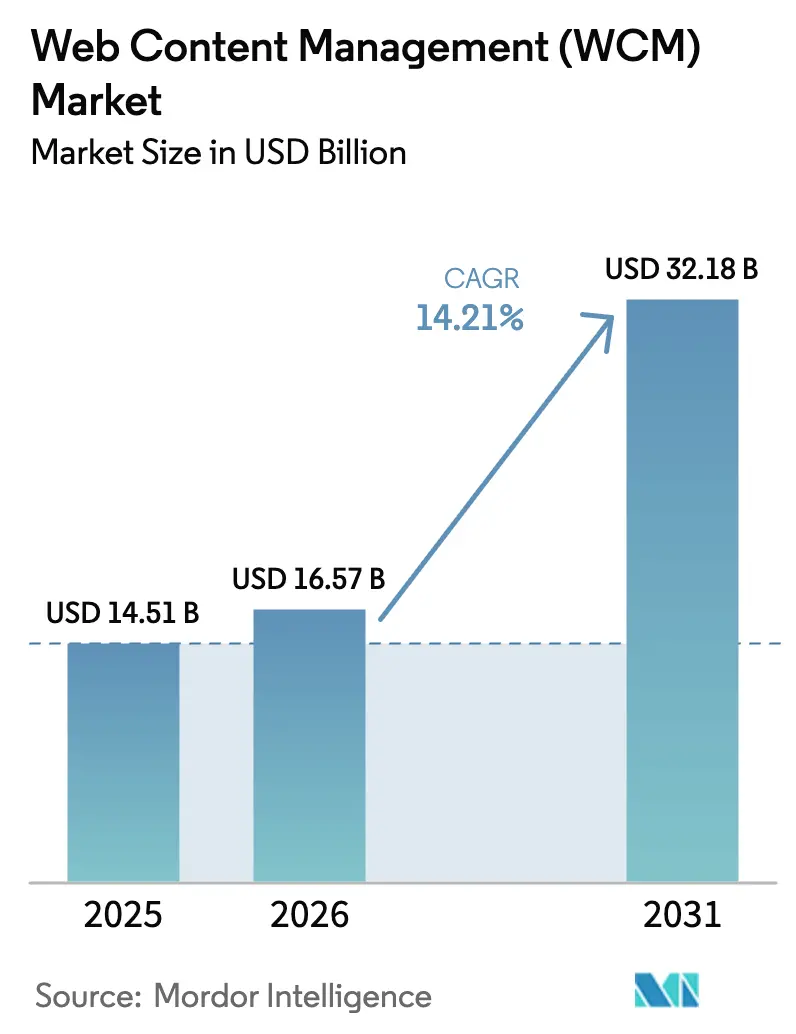

The Web Content Management market size was valued at USD 14.51 billion in 2025 and estimated to grow from USD 16.57 billion in 2026 to reach USD 32.18 billion by 2031, at a CAGR of 14.21% during the forecast period (2026-2031). This momentum stems from enterprises racing to deliver consistent omnichannel content, embed artificial intelligence (AI) in everyday workflows, and meet stringent data-privacy mandates. A decisive pivot toward cloud-native architectures, headless and hybrid content management systems, and accessibility-first redesigns is visible across industries. Vendors are intensifying AI capabilities that automate tagging, translation, and experience orchestration, while customers demand open APIs that slot neatly into modern digital-experience (DX) stacks. On the demand side, retail, healthcare, and regulated services are investing heavily to personalize journeys, improve Core Web Vitals scores, and de-risk compliance exposure, fuelling sustained double-digit expansion of the Web Content Management market..

Key Report Takeaways

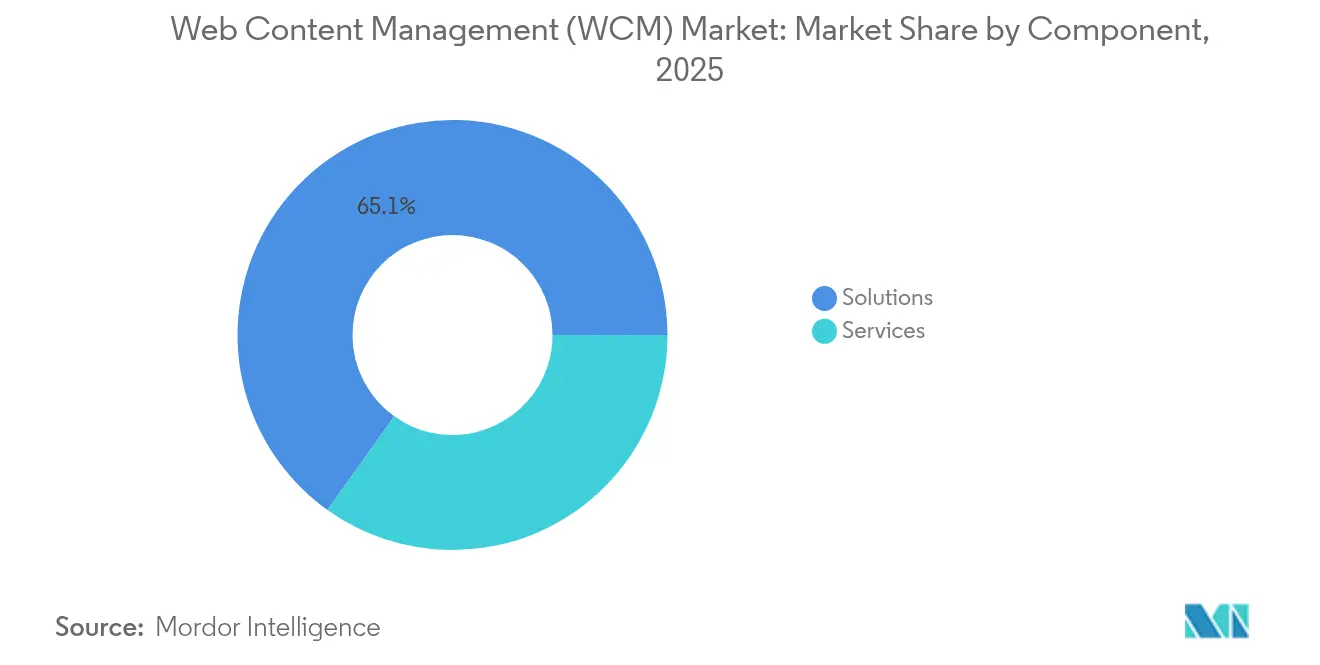

- By component, Solutions led with 65.12% revenue share in 2025; Services is projected to expand at a 19.62% CAGR through 2031.

- By deployment model, Cloud captured 55.47% of Web Content Management market share in 2025 and is surging at a 22.35% CAGR to 2031.

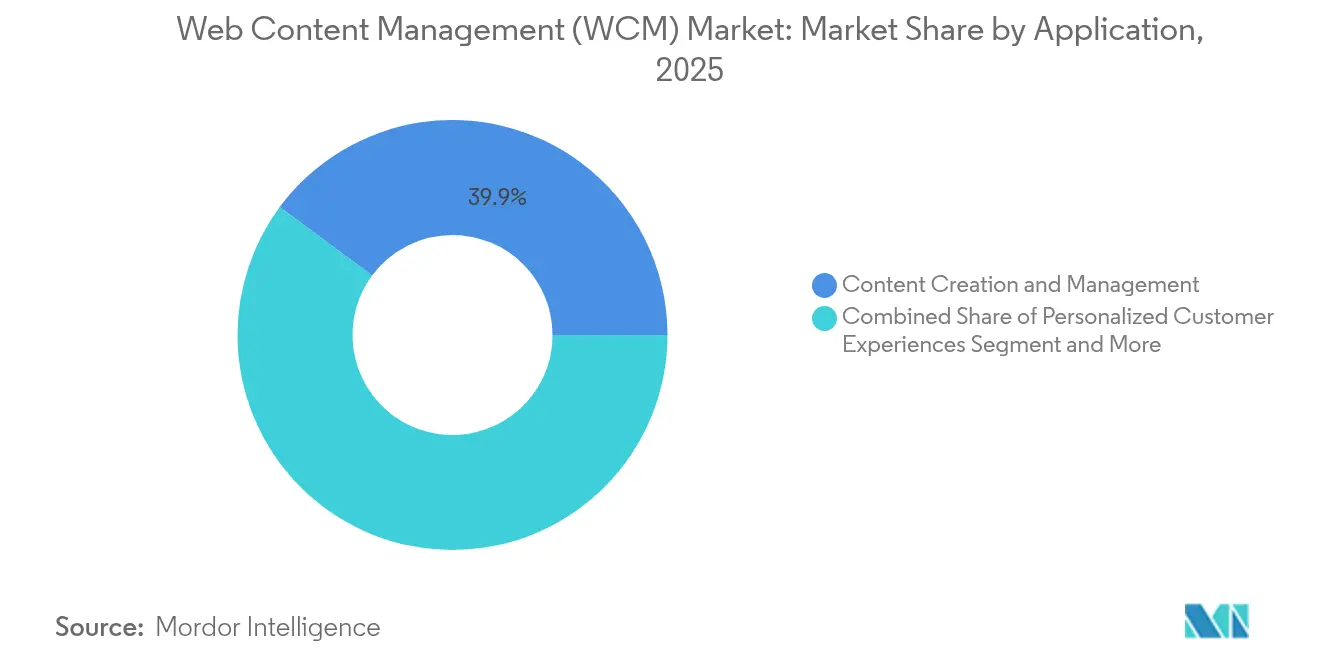

- By application, Content Creation and Management held 39.86% share of the Web Content Management market size in 2025, while Personalized Customer Experiences is tracking the highest CAGR at 24.98% to 2031.

- By industry vertical, Retail and eCommerce commanded 26.74% share of the Web Content Management market size in 2025 and Healthcare is advancing at a 23.85% CAGR to 2031.

- By geography, North America accounted for 39.65% revenue share in 2025; Asia-Pacific is the fastest-growing region at a 21.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Web Content Management (WCM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of cloud-based WCM solutions | +4.2% | Global; North America and EU lead | Medium term (2-4 years) |

| Rising demand for personalized digital experiences | +3.8% | Global; retail-heavy regions | Long term (≥4 years) |

| Headless and hybrid CMS architectures gain traction | +2.9% | Asia-Pacific core; spill-over to North America | Medium term (2-4 years) |

| Generative-AI-driven content automation | +2.1% | North America and EU early adopters | Short term (≤2 years) |

| Accessibility-first redesigns to meet WCAG 2.2 | +1.8% | EU and North America regulatory pressure | Short term (≤2 years) |

| Omnichannel commerce integration | +1.5% | Global; retail-concentrated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing adoption of cloud-based WCM solutions

Two-thirds of global enterprises now rate cloud as the default for new content-platform investments, citing faster deployment, elastic scalability, and lower maintenance overhead. Organizations report smoother cross-team collaboration and quicker feature roll-outs compared with legacy on-premises stacks. Cloud deployment also unlocks integrated AI services—such as auto-tagging and predictive insights—without costly hardware refresh cycles. Providers extend zero-trust security, regional data-residency options, and FedRAMP or ISO 27001 certifications that reassure IT risk teams. The resulting agility lets marketing teams experiment with micro-sites, progressive web apps, and seasonal campaigns in days instead of months, making cloud the bedrock of future Web Content Management market expansion.

Rising demand for personalized digital experiences

Eight in ten consumers favor brands that anticipate their needs, and frustration spikes when interactions feel generic[3]Credera Insights Team, “The Personalization Imperative,” credera.com. Enterprises are weaving real-time behavioral data into content-delivery logic, enabling site components, in-app messages, and email sequences to adapt dynamically. Headless architectures route content through APIs to any device—smartphones, kiosks, or automotive screens—while AI recommendation engines fine-tune offers, layouts, and copy. Success hinges on tight integration between content management systems, customer data platforms, and analytics hubs that quantify lift in engagement, tenure, and cart value. As user expectations rise, personalized experiences become a prerequisite rather than a differentiator, propelling the Web Content Management market.

Headless and hybrid CMS architectures gain traction

With 57% of firms planning headless commerce adoption, the API-first approach is moving from early adopter to mainstream. Decoupling the back-end repository from front-end rendering frees developers to choose frameworks like React, Vue, or Flutter while preserving editorial ease through visual content editors. Hybrid variants add previews, templates, and workflow controls on top of headless flexibility, mitigating marketer resistance. Benefits include cleaner code bases, faster performance via static-site generation and CDN delivery, and future-proofing as new touchpoints—from smart speakers to augmented-reality displays—emerge. The shift fuels demand for integration services, governance models, and packaged accelerators, underpinning healthy growth for the Web Content Management market.

Generative-AI-driven content automation

Adobe’s contract-intelligence rollout inside Acrobat AI Assistant illustrates how generative AI is moving beyond copy generation to structured-document analysis, summarization, and risk redlining. Marketing teams now spin out localized product descriptions, SEO snippets, and alt-text at scale while enforcing brand tone. Early adopters report double-digit productivity gains and quicker campaign cycles, yet governance remains critical. Successful programs embed human-in-the-loop review, bias checks, and legal sign-off before publishing. Tool vendors differentiate via prompt-engineering tooling, usage metering, and enterprise data-protection safeguards, reinforcing the strategic value of AI inside the Web Content Management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration complexity with legacy DX stacks | -2.3% | Global; established enterprises | Long term (≥4 years) |

| Escalating data-privacy and security compliance costs | -1.9% | EU and North America | Medium term (2-4 years) |

| Vendor-license inflation amid platform consolidation | -1.4% | Global; enterprise segments | Short term (≤2 years) |

| Core Web Vitals performance penalties for heavy CMS | -1.1% | Global; search-dependent firms | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Integration complexity with legacy DX stacks

Many Fortune 500 firms still run tightly coupled commerce, CRM, and ECM platforms built a decade ago. Connecting modern, composable content services to those systems exposes brittle dependencies, undocumented APIs, and data-migration hurdles. Project timelines stretch as teams refactor workflows, re-map metadata, and retire custom code without disrupting daily operations. Budget over-runs result, and talent shortages in legacy languages slow progress further. The challenge is acute in regulated sectors where every change triggers audits and validation cycles, tempering the Web Content Management market’s upside.

Escalating data-privacy and security compliance costs

Proposed amendments to the HIPAA Security Rule underscore the escalating cost of safeguarding personally identifiable and health information[2]U.S. Office of the Federal Register, “HIPAA Security Rule Proposed Modifications,” federalregister.gov. Content platforms must deliver finer-grained access controls, encryption key management, and immutable audit trails, driving both software and services spend. Ongoing tasks—penetration testing, breach-notification readiness, staff re-certification—add operational overhead. In multi-jurisdiction roll-outs, firms juggle GDPR, CCPA, and sector-specific mandates simultaneously, complicating architecture choices and vendor selection. The burden weighs heaviest on mid-size organizations, moderating overall Web Content Management market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Implementation Demand

The market’s Solutions tier remained dominant in 2025 with a 65.12% revenue share as enterprises renewed core licenses and expanded into digital-experience suites. However, services spend is growing quicker, recording a 19.62% CAGR as firms lean on partners to orchestrate complex migrations, connectivity, and optimization roadmaps. Services often bundle discovery workshops, agile CMS builds, and governance playbooks, converting license value into measurable business outcomes.

Specialist integrators also offer managed services that deliver continuous upgrades, security patching, and Core Web Vitals tuning. As organizations pivot to composable stacks, they require reference architectures, accelerators, and change-management programs. This pull for expert guidance keeps the services opportunity buoyant, adding depth to the Web Content Management market.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployment captured 55.47% Web Content Management market share in 2025 and is expanding at a brisk 22.35% CAGR, underscoring a structural migration away from appliance-centric models. Cloud-native platforms bundle autoscaling, global CDN nodes, and integrated AI micro-services, giving customers performance and innovation without capex burdens.

Hybrid options—local-rendering paired with SaaS authoring—ease data-sovereignty fears and help phased transitions. Enterprises note shorter pilot cycles, higher release cadence, and easier disaster-recovery configurations. Providers respond with consumption-based tiers and service-level agreements aligned to customer digital KPIs, reinforcing cloud’s gravitational pull across the Web Content Management market.

By Application: Personalization Drives Innovation

Content Creation and Management remained pivotal, holding 39.86% of 2025 revenues, but the Personalized Customer Experiences segment is the clear accelerator with a 24.98% CAGR. Omnichannel orchestration funnels unified profiles into decision engines that surface context-aware offers, boosting click-through, average order value, and loyalty metrics.

AI-powered testing tools dynamically adjust copy, layout, and assets, feeding insights back into segmentation logic. As cookieless targeting intensifies, first-party data infused into content strategies gives marketers lift without breaching privacy norms. These developments elevate personalization from aspiration to table stakes, cementing its role in propelling the Web Content Management market.

By Industry Vertical: Healthcare Transformation Accelerates

Retail and eCommerce led in 2025 with 26.74% share of the Web Content Management market size thanks to continual storefront refreshes and high SKU velocity. Healthcare is forecast to be the standout, advancing at a 23.85% CAGR amid virtual-care expansion, patient-portal roll-outs, and multi-language educational-content hubs. Compliance-ready templates, granular consent management, and clinical-content review workflows make purpose-built platforms attractive to providers.

Banks, insurers, and governments follow suit, modernizing portals to meet accessibility and privacy mandates. Media and telecom players, meanwhile, invest in video-centric and subscriber-entitlement modules to protect revenue streams. The cross-vertical momentum keeps the Web Content Management market diverse and resilient.

Geography Analysis

North America commanded 39.65% of 2025 revenues, reflecting early SaaS adoption, deep marketing-technology budgets, and a culture of rapid experimentation. US enterprises pioneer AI-assisted authoring and headless frameworks, setting benchmarks later emulated elsewhere. Canadian organizations emphasize bilingual delivery and compliance with the Personal Information Protection and Electronic Documents Act, while Mexican retailers invest in localized checkout flows as cross-border commerce surges.

Asia-Pacific is the growth engine, clocking a 21.95% CAGR through 2031. China’s platform giants push mini-program ecosystems that hinge on scalable, multilingual content services. India’s small and midsize businesses leapfrog straight to cloud-first CMS setups to reach mobile-first audiences. Japan’s aging demographics spur banks to automate branch content distribution and offer voice-assisted self-service, while Australia and Singapore build privacy-enhanced portals for government and education. Such heterogeneity necessitates flexible taxonomies, unicode support, and region-tailored governance, enlarging the Web Content Management market.

Europe records steady midteen expansion bolstered by GDPR, WCAG 2.2, and digital-sovereignty imperatives. Germany and France favor solutions hosting data inside EU borders, and Nordic firms pioneer sustainable hosting by tapping renewable-powered data centers. Southern European tourism boards adopt multi-language, rich-media sites to capture traveler demand. In the Middle East and Africa, GCC smart-city projects embed content services into citizen-experience layers, while South African telcos deploy customer-self-care portals to reduce call-center loads. Collectively, regional initiatives reinforce the global breadth of the Web Content Management market.

Competitive Landscape

The Web Content Management market remains moderately fragmented. Adobe, Microsoft, and Oracle front-run with integrated DX clouds bolstered by analytics, commerce, and AI features. Adobe generated USD 21.51 billion revenue in 2024, underscoring the draw of its Creative Cloud and Experience Cloud synergies[1]Adobe Communications, “Adobe Reports Fiscal 2024 Results,” adobe.com. Microsoft amassed USD 245 billion, exploiting Microsoft 365 entrenchment to cross-sell SharePoint Premium and Fabric analytics. Oracle extends Fusion and Advertising services around its WCM core to lock in enterprise workloads.

Specialists such as Contentstack, Strapi, and Bloomreach capture developer mindshare through API-driven, schema-less repositories and generous free-tier sandboxes. Speed and performance metrics create new battlegrounds; RebelMouse’s headless engine consistently tops Core Web Vitals charts, winning media migrations. Vendor consolidation pressures intensify as SaaS license inflation averages 11.4% in 2025, prompting merger activity aimed at capability expansion or regional entry.

Healthcare-specific vendors add HIPAA templates and de-identification plug-ins, while SME-focused entrants emphasise low-code site builders and marketplace integrations. Competitive advantage is increasingly defined by the depth of generative-AI orchestration, breadth of API catalogues, and clarity of usage-based pricing, all shaping customer choice across the Web Content Management market.

Web Content Management (WCM) Industry Leaders

Adobe Inc.

Sitecore Corporation A/S

Automattic (WordPress VIP & open-source services)

Acquia Inc.

Optimizely (EPiServer)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Contentstack acquired Lytics, adding a customer-data platform to deepen real-time personalization.

- April 2025: Sitecore partnered with Microsoft to open an AI Innovation Lab for marketers focused on experience orchestration.

- February 2025: Microsoft launched a community hub inside Microsoft 365 that unifies SharePoint Premium and Backup for AI-driven content processing.

- February 2025: Adobe introduced contract-intelligence capabilities to Acrobat AI Assistant, automating clause detection for its 650 million-user ecosystem.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global web content management market as all licensed software and hosted platform subscriptions that let organizations create, store, organize, and deliver digital content across websites and allied digital touchpoints, spanning coupled, decoupled, and headless architectures. It tracks revenue earned directly from software licenses or SaaS seats; any one-off implementation fees are counted only when contractually inseparable from the core platform sale.

Scope Exclusion: Standalone digital asset management suites, generic site-hosting plans, and on-premises document repositories lacking native web-publishing capability are excluded.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premises

- By Application

- Content Creation and Management

- Personalized Customer Experiences

- Multi-Channel Content Delivery

- Digital Asset Management

- SEO and Analytics Integration

- By Industry Vertical

- Banking, Financial Services and Insurance (BFSI)

- Government

- Healthcare

- IT and Telecommunications

- Media and Entertainment

- Retail and eCommerce

- Education

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed platform product heads, digital-agency integrators, CIOs, and procurement managers across North America, Europe, and Asia-Pacific. Their inputs on license discounting, headless CMS adoption rates, and regional budget outlooks close secondary-data gaps and ground our assumptions before final triangulation.

Desk Research

We start by mapping spend signals from tier-1 public sources such as W3Techs CMS usage charts, UNCTAD e-commerce statistics, the World Bank ICT Adoption Index, OECD digital economy dashboards, and governmental trade data. Company 10-Ks, investor decks, product price lists, and customs shipment logs refine volume and pricing assumptions, after which D&B Hoovers and Dow Jones Factiva help us reconcile vendor revenues and contract wins. These sources are illustrative, not exhaustive; many additional references inform data capture, validation, and clarification.

Market-Sizing & Forecasting

A top-down build begins with the live universe of enterprise websites, multiplies it by average WCM spend per site, and is sanity-checked through selective bottom-up vendor revenue roll-ups. Key variables like cloud-migration velocity, headless CMS share, median license ASP, marketing-technology budget growth, generative-AI plug-in attach rates, and regional GDP-linked IT spend feed a multivariate-regression model, while scenario analysis captures regulatory or currency shocks. Where disclosures are thin, proxy ratios from comparable vendors are applied before integration.

Data Validation & Update Cycle

Outputs face variance and anomaly checks against external benchmarks, followed by multi-level analyst review and sign-off. Reports refresh every twelve months, with interim updates triggered by material events, ensuring clients receive the latest calibrated view.

Why Mordor's Web Content Management Baseline Commands Reliability

Published estimates often vary; the mix of counted services, price corridors, and refresh cadence typically drives gaps. By locking scope, blending ASPs verified with buyers, and updating yearly, we minimize drift and deliver a figure users can trace back to observable drivers.

Principal gap sources include whether professional services are counted, treatment of open-source distributions, the inclusion of adjacent digital-asset tools, and currency-conversion years. Mordor's disciplined bundle, driver-tested model, and fast refresh narrow these differences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.51 B (2025) | Mordor Intelligence | - |

| USD 10.65 B (2024) | Global Consultancy A | Excludes cloud services; constant-2023 FX rates |

| USD 12.40 B (2024) | Market Research Publisher B | Adds digital-asset suites; omits APAC SME uptake |

| USD 10.98 B (2024) | Industry Analyst C | Relies on limited vendor survey; under-represents headless CMS |

The comparison shows that Mordor's consistent scope, mixed-method validation, and rapid refresh cadence supply a balanced, transparent baseline that decision-makers can depend on.

Key Questions Answered in the Report

What is the current market size of Web Content Management platforms?

The Web Content Management market size stood at USD 16.57 billion in 2026 and is projected to reach USD 32.18 billion by 2031.

Which deployment model is expanding the fastest?

Cloud deployment is the clear frontrunner, holding 55.47% share in 2025 and growing at a 22.35% CAGR through 2031.

Why is healthcare a high-growth vertical?

Hospitals and clinics need HIPAA-compliant portals, telemedicine content, and multilingual patient education, pushing the vertical at a 23.85% CAGR.

How are vendors differentiating in a crowded field?

Leaders weave generative AI, headless APIs, and Core Web Vitals optimisation into offerings while pricing on flexible, usage-based models.

What are the main barriers to WCM modernisation?

Legacy-system integration, escalating data-privacy compliance costs, and rising SaaS licence fees are the top constraints holding back some projects.

Page last updated on: