Product Information Management (PIM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

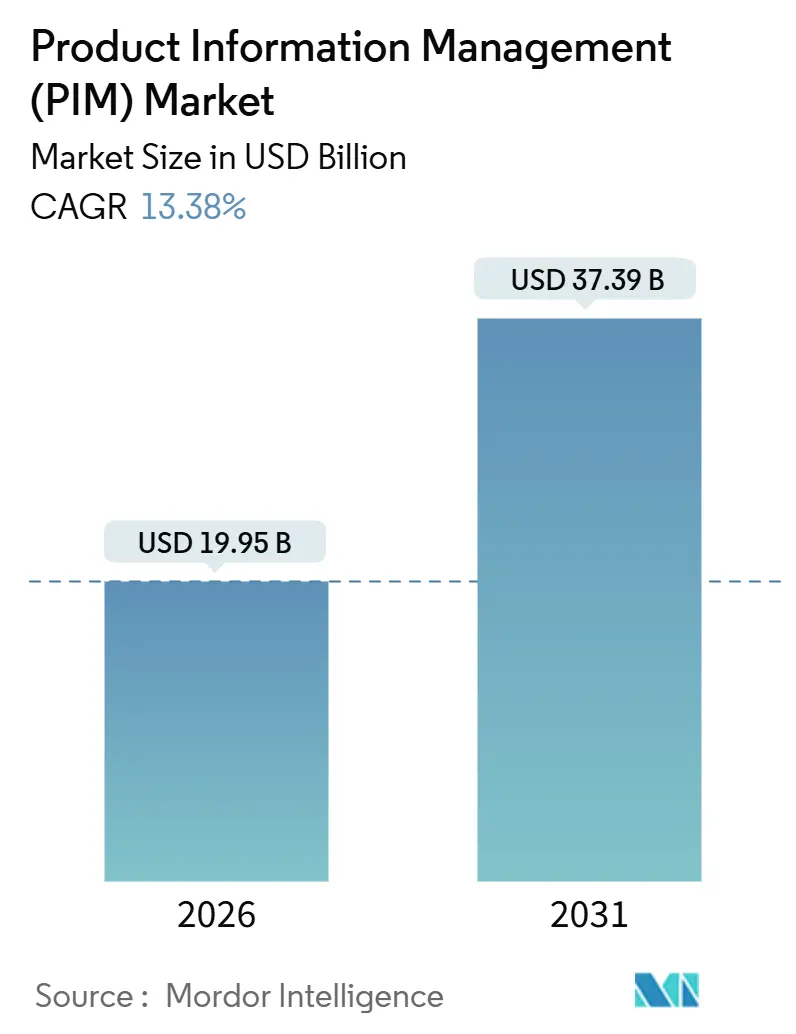

| Market Size (2026) | USD 19.95 Billion |

| Market Size (2031) | USD 37.39 Billion |

| Growth Rate (2026 - 2031) | 13.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Product Information Management (PIM) Market Analysis by Mordor Intelligence

The Product Information Management market size stands at USD 19.95 billion in 2026 and is projected to reach USD 37.39 billion by 2031, registering a 13.38% CAGR through the forecast period. The growth reflects a decisive migration from fragmented spreadsheets toward unified, AI-native hubs that meet simultaneous demands for regulatory traceability and omnichannel speed. Investment is accelerating as European Digital Product Passport deadlines approach, as quick-commerce marketplaces mandate sub-hour catalog refresh cycles, and as large language models automate attribute enrichment at scale[1]European Health and Digital Executive Agency, “Digital Product Passport,” europa.eu. Competitive intensity is rising because platform vendors are bundling master data management and generative AI into single suites, raising the switching costs for incumbent on-premise users. Long-term expansion is further anchored in the proven link between accurate product data and higher conversion, lower returns, and stronger brand equity.

Key Report Takeaways

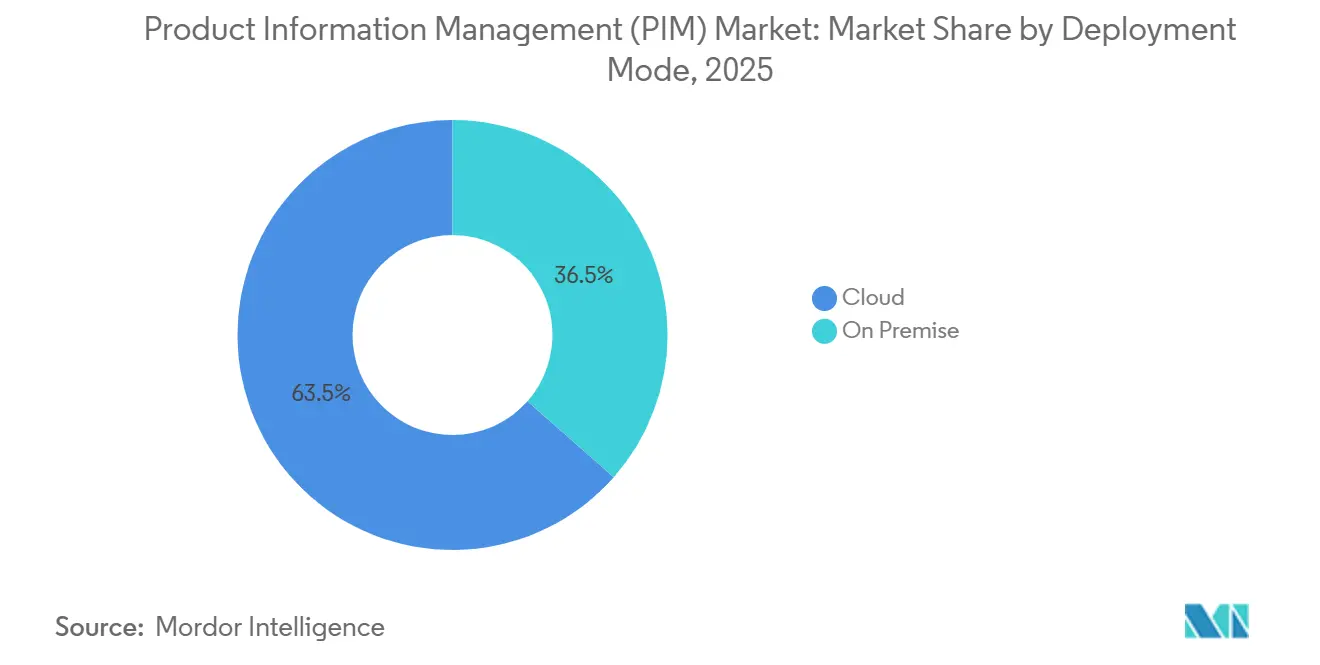

- By deployment model, cloud captured 63.50% of Product Information Management market share in 2025 and is expanding at an 18.50% CAGR through 2031.

- By offering, solutions held 63.14% revenue share in 2025 while services are advancing at a 23.40% CAGR to 2031.

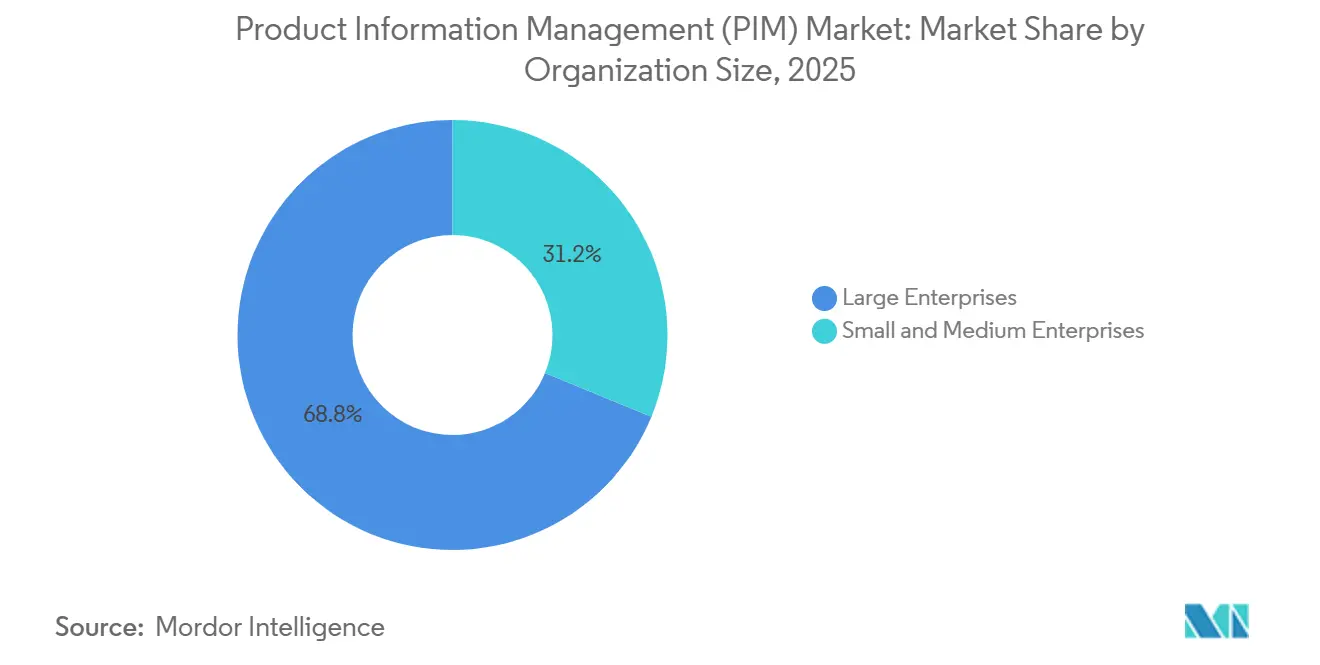

- By organization size, large enterprises accounted for 68.80% share of the Product Information Management market in 2025, and small and medium enterprises are growing at an 18.43% CAGR through 2031.

- By end-user industry, retail and e-commerce led with a 33.20% share in 2025, whereas IT and telecom records the highest 19.50% CAGR over the forecast horizon.

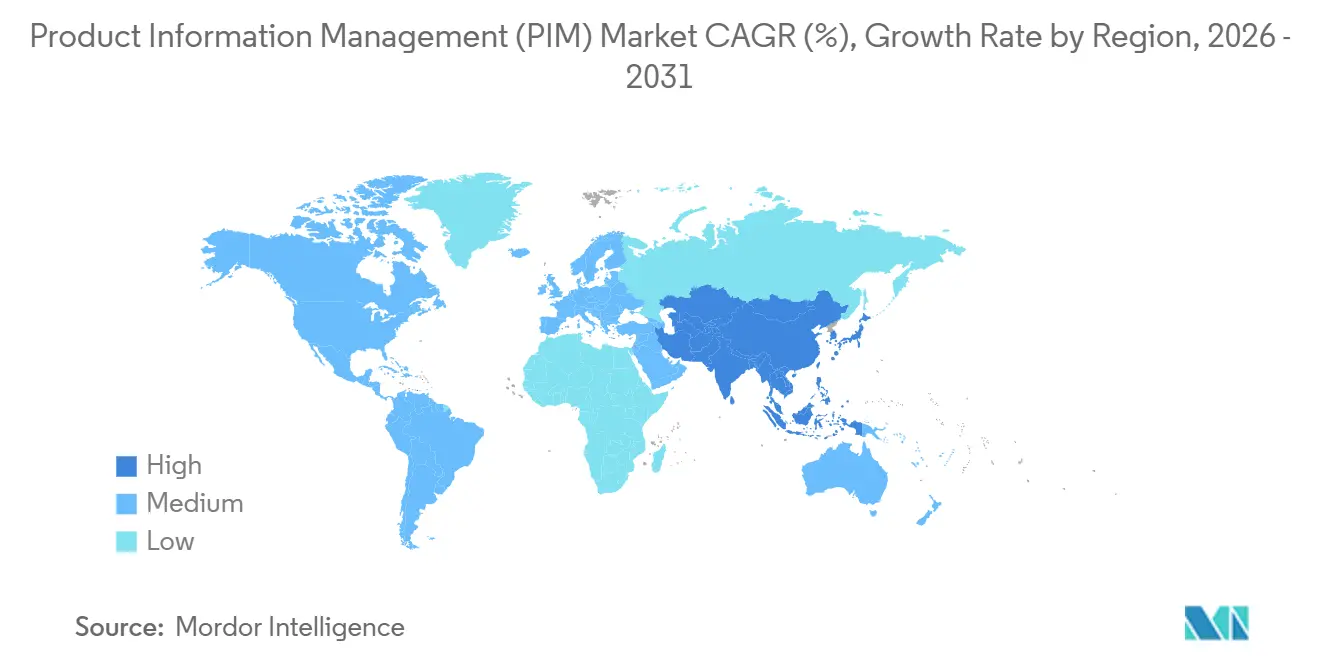

- By geography, North America contributed 39.80% of revenue in 2025, while Asia-Pacific is set to expand at a 20.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Product Information Management (PIM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Boom and SKU Proliferation | +3.2% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Cloud Adoption Lowering TCO | +2.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Omnichannel Customer-Experience Mandates | +2.1% | Global, notably North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| EU Digital Product Passport Compliance | +1.9% | Europe primary, spillover to Asia-Pacific and North America exporters | Long term (≥ 4 years) |

| Gen-AI-Ready Product-Content Pipelines | +1.7% | Global, early adopters in North America and Europe | Short term (≤ 2 years) |

| Marketplace Quick-Commerce API Requirements | +1.5% | Global, clusters in North America, Europe, select Asia-Pacific metros | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom And SKU Proliferation

Explosive SKU counts strain legacy spreadsheets, prompting retailers to centralize product attributes in cloud hubs that syndicate accurate data to web, mobile, and store systems. Shopify merchants handling more than 10,000 SKUs experienced a 23% revenue loss when information was incomplete, a gap closed by automated enrichment and marketplace feeds. Instacart and other quick-commerce operators require sub-hour API updates, so suppliers integrate real-time PIM webhooks to stay listed. AI engines from Akeneo extract attributes from supplier PDFs and translate descriptions, cutting manual effort 60% and shrinking onboarding cycles from weeks to days. Demand peaks in Asia-Pacific, where Lazada and Tokopedia rapidly expand assortments, and in North America, where buy-online-pick-up-in-store programs require synchronized product and inventory views.

Cloud adoption lowering TCO

Enterprises shifting to cloud platforms avoid hardware capital expense, reduce IT head-count, and match operating cost to seasonal volume. Total cost of ownership falls 30-40% within three years by eliminating manual upgrades and by automating security patches. Mid-market firms with fewer than 1,000 employees adopt cloud PIM twice as fast as large peers because subscription tiers and pre-built Shopify or Salesforce connectors compress deployment from 12-18 months on-premise to as little as 12 weeks. Industry templates such as GS1-compliant data models speed integration with suppliers. These benefits drive the 18.50% CAGR in cloud deployments yet raise data-residency and sovereignty questions that vendors mitigate through regional hosting options and ISO 27001 controls.

Omnichannel customer-experience mandates

Modern shoppers expect consistent imagery, specs, and sustainability facts across web, mobile, social, voice, and in-store screens. Retailers therefore merge siloed product, asset, and pricing data into a single PIM that applies channel-specific transformation rules. Voice assistants need concise spoken descriptions, while TikTok Shop demands shoppable video metadata. Embedded digital asset management and rules engines automatically resize images, map attributes, and publish feeds to each endpoint, raising conversion 15-25% and lowering return rates 10-20%. Adoption is widest in North America and Europe, yet Singapore and Seoul demonstrate equally high omnichannel expectations due to mobile-first shopping cultures.

EU Digital Product Passport Compliance

The Ecodesign for Sustainable Products Regulation forces manufacturers selling into Europe to attach machine-readable passports that disclose carbon footprint, material origin, and recyclability for batteries by February 2027 and textiles by 2026. PIM platforms must capture supplier sustainability data, map it to delegated acts, generate GS1 Digital Link QR codes, and retain provenance logs for audits. Exporters in China and Southeast Asia upgrade systems to maintain EU access, creating global spillover demand. Brands such as Pangaia embed NFC tags that link to cloud passports, turning compliance into a circular-economy marketing asset. The regulation therefore adds long-tail growth that extends beyond the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and Data-Breach Concerns | -1.4% | Global, elevated in Europe and North America | Short term (≤ 2 years) |

| Integration Complexity With Legacy ERPs | -1.2% | Global, most acute in large enterprises | Medium term (2-4 years) |

| Rising ESG Data-Audit Costs | -0.9% | Europe, North America, multinationals | Long term (≥ 4 years) |

| Shortage of PIM-Skilled Data Stewards | -0.8% | Global, notably North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity And Data-Breach Concerns

Centralized cloud repositories become attractive to ransomware groups because they store proprietary formulations, prices, and supplier terms. The EUR 1.2 billion GDPR penalty levied on Meta in 2023 underscores potential exposure when data crosses borders without airtight controls. Vendors answer with zero-trust architectures, granular encryption, and optional regional hosting, yet every API link to Shopify, Amazon, or Instagram multiplies the attack surface. Regulated verticals such as banking and pharma demand configurable masking and consent modules, adding deployment friction. The near-term drag is strongest in Europe and North America where disclosure laws force rapid public reporting of breaches.

Integration complexity with legacy ERPs

Most large enterprises still run SAP ECC or Oracle E-Business Suite, systems designed before REST APIs. Custom middleware is often required to synchronize item masters with modern cloud PIMs, and buried customizations can derail projects. Cleaning duplicate records and aligning taxonomy eats 30-40% of implementation budgets. Composable commerce approaches relieve pressure by piloting PIM on one brand or channel, but full real-time bidirectional sync remains challenging until ERP upgrades to S/4HANA or Oracle Cloud mature. The integration hurdle disproportionately slows highly customized manufacturers and global retailers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Platforms Cement Majority Position

Cloud deployments generated 63.50% revenue share in 2025, outstripping on-premise alternatives through subscription economics and elastic scale that match peak demand around shopping holidays. The Product Information Management market size attributable to cloud solutions is forecast to rise at an 18.50% CAGR, making cloud both the largest and quickest-growing model. Retailers appreciate managed upgrades and 24-hour global availability that support always-on catalog syndication. On-premise share continues to fall because capital expense, extended implementation, and laborious patching no longer match board-level mandates for speed and resilience.

Hybrid configurations persist in pharmaceuticals, aerospace, and defense where data sovereignty or air-gapped networks remain non-negotiable. These firms keep sensitive BOM data on internal servers while leveraging cloud-based enrichment and distribution micro-services. Generative AI modules now bundled with Salsify, Stibo Systems, and Syndigo run more economically at cloud scale, further widening the capability gap. The market story therefore shifts from a binary cloud versus on-premise debate to a continuum in which full SaaS dominates routine use cases while edge deployments serve regulated corners.

By Offering: Services growth reflects implementation complexity

Solutions still delivered 63.14% of Product Information Management market revenue in 2025, covering software subscriptions and license maintenance. However, services - implementation, custom integration, training, and managed operations - are rising at a 23.40% CAGR through 2031, outpacing software itself. Organizations repeatedly underestimate the taxonomy design, data-quality remediation, and stakeholder alignment needed to operationalize PIM. Consulting firms step in to cleanse legacy catalogs, build MuleSoft connectors, and coach category teams on attribute governance. As a result, the Product Information Management market size for services is expanding faster than licenses.

Managed services answer the chronic shortage of PIM data stewards. Brands outsource routine content health checks, marketplace feed monitoring, and compliance audits to specialists for a monthly fee. This outsourcing trend will taper only when low-code workflow builders, AI data-quality bots, and self-service mapping reduce human intervention. Until then, services revenue remains the primary tailwind because Digital Product Passport mandates and omnichannel feeds require ongoing updates rather than one-time projects.

By Organization Size: SMEs Close The Gap

Large enterprises accounted for 68.80% of 2025 spending, reflecting complex product hierarchies that demand deep workflow orchestration and integration. Yet small and medium enterprises are posting an 18.43% CAGR because cloud subscription tiers remove entry barriers, and retailer templates eliminate expensive custom mapping. The Product Information Management market share of SMEs will edge upward as platforms such as Plytix enable non-technical staff to import CSV files, enrich attributes, and push listings to Amazon or Walmart within one browser session.

For conglomerates, generative AI and master data convergence make platform depth more critical than price. Salesforce’s Informatica acquisition demonstrates how top-tier buyers expect unified governance across product, customer, and supplier domains. SMEs, meanwhile, prize fast time-to-value over configurability, gravitating toward opinionated interfaces and guided data-quality wizards. This dichotomy sustains a bifurcated vendor landscape: enterprise suites fight on breadth, while lightweight SaaS firms fight on simplicity and cost.

By End-User Industry: Retail Dominates, Telecom Accelerates

Retail and e-commerce delivered 33.20% of 2025 revenue because conversion, return rates, and search rankings depend directly on high-quality product data. The Product Information Management market size for retail will continue to expand as social commerce and video shopping multiply content variants. IT and telecom, however, post the fastest 19.50% CAGR. Operators launch 5G bundles, IoT device plans, and edge-computing services that demand synchronized catalogs across billing, self-service portals, and API marketplaces. Accurate attribute mapping is critical for automated provisioning and real-time quote-to-cash flows.

Manufacturing adoption follows close behind as configure-price-quote solutions rely on a single source of truth for dimensions, materials, and compliance certificates. Financial services and insurance employ PIM to manage SKU-like offerings—credit cards, mutual funds, policies—under rising disclosure rules. Media companies archive video and music metadata within specialized PIM variants. Each vertical imposes distinct taxonomy and compliance constraints, prompting vendors to release industry accelerators that shrink deployment timelines.

Geography Analysis

North America contributed 39.80% of global revenue in 2025, buoyed by concentrated retail chains, high digital-adoption rates, and early uptake of master data governance. Many large enterprises completed first-generation PIM rollouts and now upgrade to AI-native versions that generate copy, translate descriptions, and score data quality automatically. Vendor competition intensifies in mid-market tiers, where Shopify-based brands and Amazon third-party sellers demand low-friction onboarding and affordable licenses. U.S. privacy proposals, such as the California Consumer Privacy Act, also increase demand for lineage tracking and consent auditing within PIM workflows.

Asia-Pacific is the growth engine, posting a 20.10% CAGR as China, India, and Southeast Asia digitize trade and payments. GS1 standards integrated into Baidu search improve discoverability while filtering counterfeits, driving manufacturers to structure product data rigorously[2]GS1 China, “Standardized Data in Baidu,” gs1cn.org. India’s Open Network for Digital Commerce sets open catalog formats that small merchants must adopt to participate. Japan and South Korea embed QR codes with recycling instructions to support sustainability goals for an aging population. Language diversity, proprietary schemas on Lazada or Coupang, and varied data-hosting laws compel vendors to deliver multi-tenant, rules-driven transformation logic.

Europe remains compliance-centric. The Corporate Sustainability Reporting Directive and Digital Product Passport scheme force PIM upgrades that add carbon footprint, repairability, and circularity fields. Export-oriented manufacturers in Turkey, Morocco, and Vietnam also modernize to maintain EU access, creating secondary demand pockets. South America’s adoption concentrates in Brazil and Argentina where Mercado Libre and Falabella enforce structured listing rules. The Middle East shows momentum in UAE and Saudi Arabia, catalyzed by state-sponsored e-commerce strategies and fast-growing regional marketplaces. Africa remains nascent but rising smartphone penetration in Nigeria and South Africa signals early green shoots for PIM vendors targeting mobile-first catalogs.

Competitive Landscape

The top five vendors command roughly 35-40% combined revenue, reflecting moderate concentration. Syndigo’s September 2025 purchase of 1WorldSync for an enterprise value above USD 3.5 billion and Salesforce’s USD 8 billion takeover of Informatica underscore an accelerating pivot toward composable data fabrics that encompass PIM, master data management, and AI-powered content optimization. These deals heighten entry barriers for pure-play PIM start-ups because buyers now expect governance, lineage, and omnichannel feeds in a single invoice.

Strategic alliances supplement M&A. Syndigo partnered with Productsup in February 2025 to link syndication networks with global feed management, expanding retailer reach beyond 3,500 endpoints[3]Syndigo, “Acquisition of 1WorldSync,” syndigo.com. Adobe positions Experience Manager Assets as a PIM-adjacent platform that layers AI metadata tagging over digital asset repositories, targeting brand marketers who already use Adobe Creative Cloud. Open-source alternatives like Akeneo and Pimcore win projects where enterprises want code-level customization and to avoid subscription escalation.

White-space opportunities surface in vertical-specific niches. Pharmaceutical vendors need structured dosage and interaction data, while automotive aftermarket catalogs require compatibility matrices covering millions of part-vehicle combinations. Foodservice distributors track allergens and nutrition for regulatory menus. Agentic AI inside PIM is a frontier technology: autonomous bots detect missing attributes, recommend improvements based on marketplace analytics, and execute fixes. Vendors that master agent workflows may leapfrog rivals in both efficiency and differentiation.

Product Information Management (PIM) Industry Leaders

SAP SE

IBM Corp.

Oracle Corp.

Informatica LLC

Akeneo SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Salesforce completed its USD 8 billion acquisition of Informatica to embed cloud data management, catalog, and master data capabilities into the Agentforce AI platform, creating an autonomous data foundation.

- September 2025: Syndigo acquired 1WorldSync, forming a USD 3.5 billion enterprise serving 18,000 customers and 3,500 retailers with integrated PIM, syndication, and user-generated content services.

- September 2025: GS1 issued a provisional Digital Product Passport standard to guide manufacturers on identification and data carrier formats ahead of EU mandates.

- August 2025: Baidu integrated GS1 China standards into search results, connecting 100 million users to structured product data to curb counterfeit listings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the product information management (PIM) market as all revenues earned from purpose-built software and associated services that centralize, enrich, and syndicate structured and unstructured product data across digital and physical sales channels. Solutions that bundle digital asset management or master-data domains only become part of our scope when they are sold primarily as PIM platforms.

Scope exclusion: we deliberately leave out broader master-data suites that manage customer, supplier, or finance records when PIM is not the lead use case.

Segmentation Overview

- By Deployment Model

- Cloud

- On-Premise

- By Offering

- Solutions

- Services

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Industry

- Retail and E-commerce

- BFSI

- Manufacturing

- Media and Entertainment

- IT and Telecom

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with software product heads, systems integrators, and retail IT managers across North America, Europe, and fast-growing Asia Pacific markets. These conversations clarified real license pricing, cloud migration timelines, and typical product-catalog sizes that secondary sources rarely spell out.

Desk Research

We gathered foundational numbers from well-regarded public sources such as the U.S. Census Bureau's retail e-commerce series, Eurostat's online sales index, the UN Comtrade trade codes that track software exports, and position papers from trade bodies like GS1 and the National Retail Federation. Regulatory notes on the EU's Digital Product Passport and SEC cyber-risk filings added context on compliance-driven demand. Subscription databases, D&B Hoovers for vendor revenue splits and Dow Jones Factiva for deal flow, helped us size vendor cohorts and spot growth signals. These sources illustrate, rather than exhaust, the broad evidence base our analysts reviewed.

Market-Sizing & Forecasting

A top-down model begins with global retail and B2B e-commerce spending, then applies PIM adoption ratios that vary by region and industry before being further filtered through cloud penetration rates. We cross-check this with sampled bottom-up estimates built from leading vendors' reported users, average selling price tiers, and partner channel data. Key variables include online SKU counts, cloud subscription renewal rates, midsize enterprise IT spend, and regulatory milestones such as mandatory traceability labels. Multivariate regression combined with scenario analysis projects 2025-2030 growth, letting us stress-test high-adoption and slowdown cases. Where supplier roll-ups left gaps, conservative proxy ratios from similar SaaS categories filled the blanks.

Data Validation and Update Cycle

Outputs run through variance checks against independent retail tech indices and quarterly vendor filings. Senior reviewers sign off, and reports refresh yearly; interim updates trigger after major acquisitions or regulatory shifts to ensure clients always receive the latest view.

Why Mordor's Product Information Management Baseline Commands Reliability

Published PIM estimates often diverge because firms pick different solution mixes, price points, and refresh cadences. Our disciplined scope, live interviews, and annual recalibration keep our baseline firmly anchored.

Key gap drivers include whether adjacent MDM modules are folded into totals, how free-to-paid migrations are counted, the currency-conversion cut-off quarter, and how aggressively each publisher layers in AI-driven upsell premiums.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.56 B (2025) | Mordor Intelligence | - |

| USD 12.20 B (2023) | Global Consultancy A | Older base year; excludes service revenues |

| USD 4.47 B (2024) | Industry Portal B | Focuses on software licenses, omits cloud subscriptions |

| USD 17.40 B (2024) | Regional Analytics C | Rolls product-domain MDM and PXM modules into scope |

Taken together, the comparison shows that when scope breadth, latest currency rates, and balanced forecast assumptions are aligned, Mordor's numbers offer decision-makers the most transparent and repeatable starting point.

Key Questions Answered in the Report

What is the 2026 value of the Product Information Management market?

The market is valued at USD 19.95 billion in 2026.

How fast will the market grow between 2026 and 2031?

It is forecast to expand at a 13.38% CAGR, reaching USD 37.39 billion by 2031.

Which deployment model holds the largest share?

Cloud platforms led with 63.50% share in 2025 and are projected to remain dominant.

Which end-user segment is expanding the fastest?

IT and telecom posts the highest 19.50% CAGR as operators digitize 5G and edge-computing catalogs.

Page last updated on: