Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

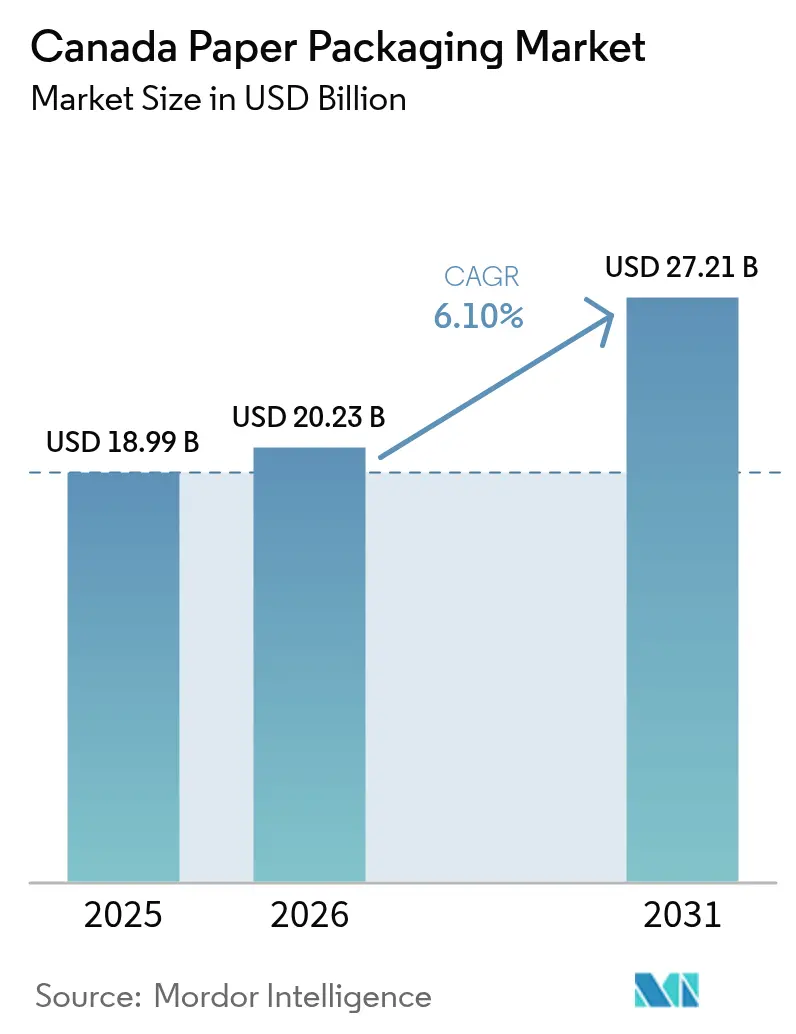

| Base Year Market Size (2025) | USD 18.99 Billion |

| Market Size (2026) | USD 20.23 Billion |

| Market Size (2031) | USD 27.21 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Paper Packaging Market Analysis by Mordor Intelligence

The Canada paper packaging market size is projected to be USD 18.99 billion in 2025, USD 20.23 billion in 2026, and reach USD 27.21 billion by 2031, growing at a CAGR of 6.11% from 2026 to 2031. Demand is buoyed by provincial extended producer responsibility rules that transfer curbside-recycling costs from municipalities to brand owners, accelerating the shift toward mono-material fiber formats that earn higher recovery revenues. Federal prohibitions on single-use plastics continue to redirect food service, grocery and quick-service restaurant applications toward moulded-pulp clamshells, kraft wraps and barrier-coated board. E-commerce parcel volume remains elevated as omnichannel retailers optimize right-sized corrugated boxes and paper-based cushioning, while the food-delivery boom expands usage of grease-resistant cartons and branded clamshells. Volatility in northern-bleached-softwood-kraft pulp prices and rising electricity tariffs pressure mill margins, yet integrated producers leverage captive fiber and co-generation assets to defend profitability. Rail-service disruptions and rural recycling gaps expose supply-chain risks, prompting large buyers to dual-source and encouraging converters to build capacity closer to Prairie grain and British Columbia forest clusters.

Key Report Takeaways

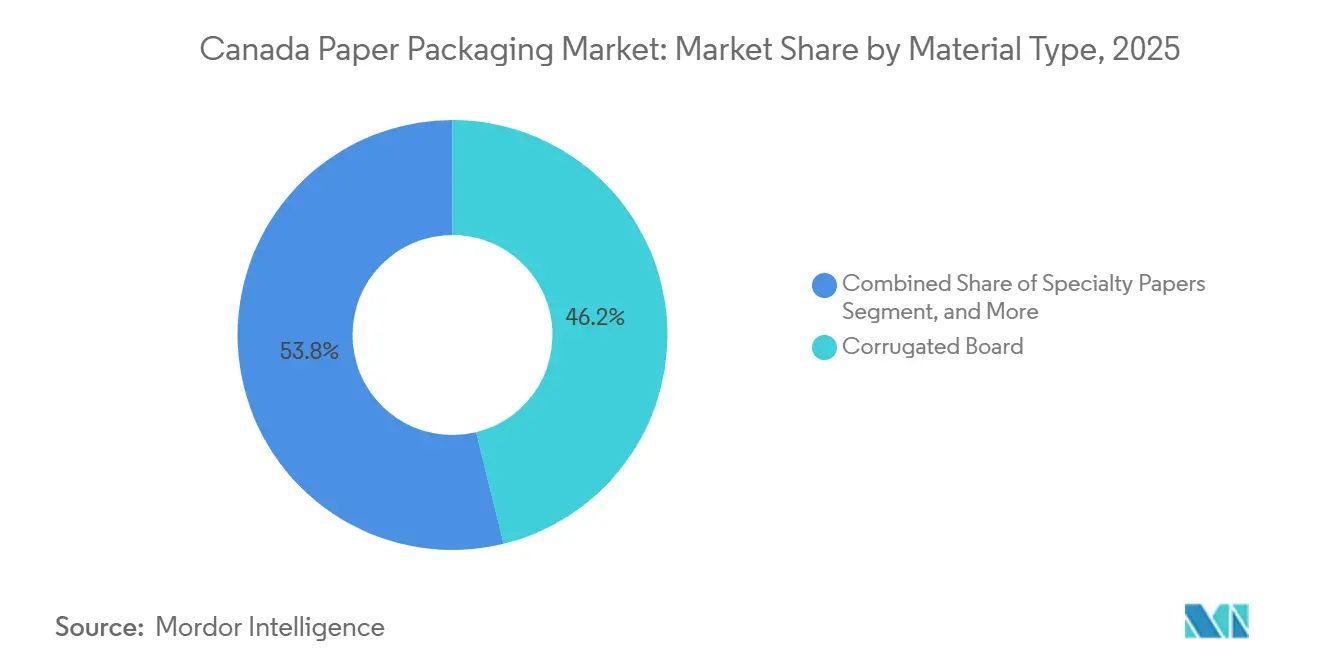

- By material type, corrugated board led with 46.19% of Canada's paper packaging market share in 2025, while specialty papers are forecast to expand at a 6.78% CAGR through 2031.

- By product type, rigid formats accounted for 58.57% of 2025 revenue, whereas flexible paper packaging is projected to grow at 6.93% through 2031.

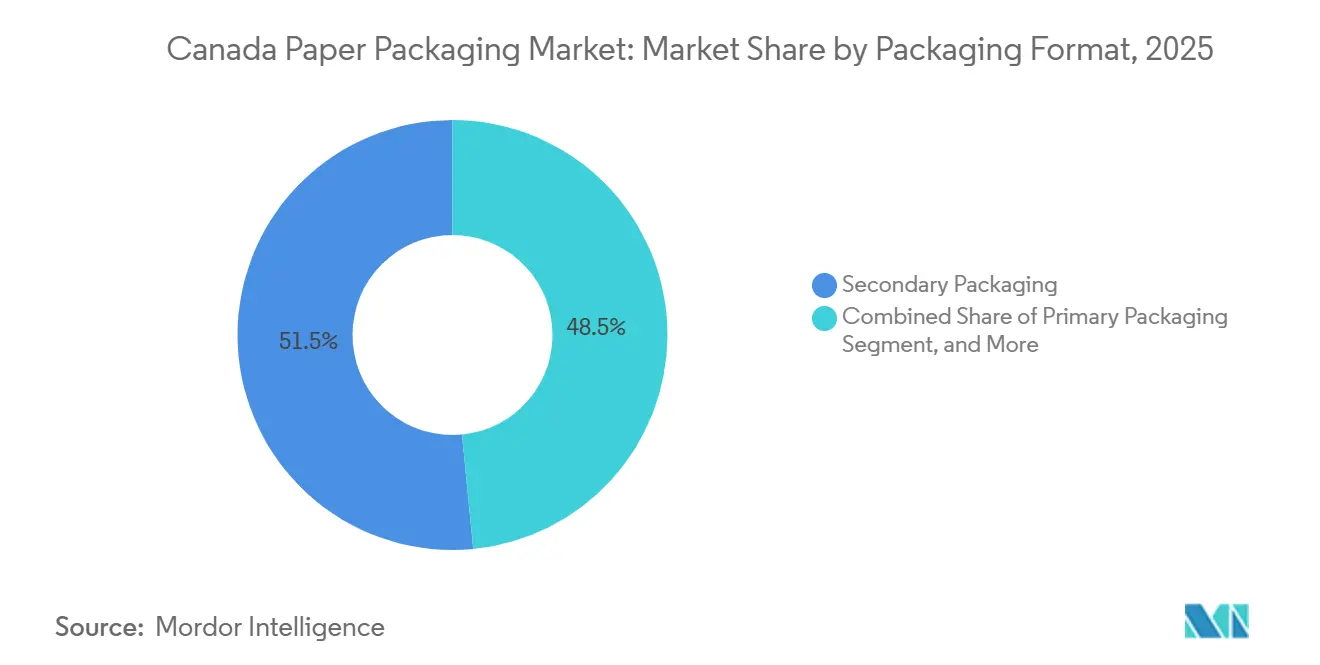

- By packaging format, secondary packaging commanded 51.53% share in 2025; primary formats are advancing at a 6.56% CAGR to 2031.

- By end-use industry, food held 27.58% of demand in 2025, and e-commerce and retail end-uses are expected to post a 6.71% CAGR to 2031.

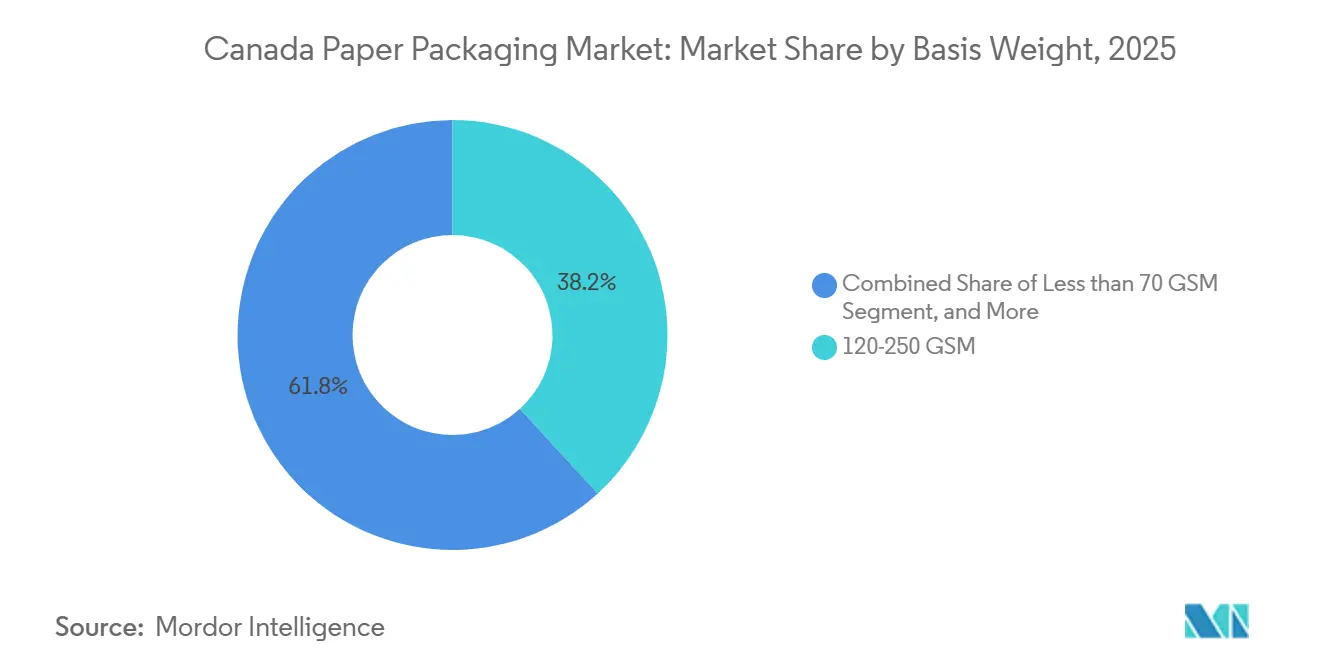

- By basis weight, the 120-250 GSM segment captured 38.19% of 2025 revenue, while sub-70 GSM grades are set to rise at a 7.11% CAGR through 2031.

- By printing technology, flexography represented 42.61% of 2025 spend, yet digital printing is predicted to climb at a 7.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Circular Economy Mandates | +1.30% | National, led by Quebec, Ontario, British Columbia | Medium term (2-4 years) |

| Government Bans on Single-Use Plastics | +1.10% | National, enforced federally with provincial variations | Short term (≤ 2 years) |

| Surge in E-commerce Parcel Volumes | +1.40% | National, concentrated in Ontario, Quebec, British Columbia urban centers | Short term (≤ 2 years) |

| Expansion of Food Delivery and Take-out Culture | +0.90% | National, urban-centric with spillover to suburban markets | Medium term (2-4 years) |

| Cannabis Packaging Compliance Requirements | +0.40% | National, regulated by Health Canada | Long term (≥ 4 years) |

| Retail Demand for Carbon-Neutral Labels | +0.60% | National, early adoption in Ontario, Quebec, British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Circular Economy Mandates

Provincial extended producer responsibility programs compel brand owners to pay 100% of municipal recycling costs, pushing converters toward mono-material designs that yield higher recovery rates.[1]Gowling WLG, “Extended Producer Responsibility in Canada: Key Developments and Compliance Strategies,” gowlingwlg.com Quebec implemented full producer funding in 2025, with Ontario and British Columbia following comparable blueprints, creating a harmonized compliance landscape. The Canadian Council of Ministers of the Environment issued 2024 guidance that standardizes “recyclable” definitions, pressuring manufacturers to eliminate poly-windows and adopt water-based coatings.[2]Canadian Council of Ministers of the Environment, “Guidance on Extended Producer Responsibility for Packaging and Printed Paper,” ccme.ca Investments in dispersion-coated board and micro-fibrillated cellulose additives improve moisture resistance without compromising repulp ability, favouring specialty papers over multi-layer plastics. Brand owners view these changes as cost-effective because recovered fiber commands a premium in provincial recycling auctions, offsetting higher substrate prices.

Government Bans on Single-Use Plastics

Canada’s phased federal prohibition covering checkout bags, cutlery and certain food-service ware triggered immediate substitution toward moulded-pulp trays and kraft carriers.[3]Environment and Climate Change Canada, “Single-Use Plastics Prohibition Regulations: Overview and Compliance,” canada.ca Quick-service restaurants adopted fiber sleeves and napkin bands, while grocery chains shifted to reinforced kraft bags. Enforcement actions in 2024 demonstrated penalty risk for non-compliant importers, cementing long-term demand for paper alternatives. The regulations exclude medical and accessibility segments, but their breadth exceeds earlier voluntary commitments, ensuring sustained volume gains for paper-based food-contact formats. Equipment suppliers report record bookings for pulp-moulding lines, and converters are adding coating capacity for grease-resistant wraps.

Surge in E-commerce Parcel Volumes

Statistics Canada recorded CAD 63.7 billion (USD 49.88 billion) in online sales in 2022, with cardboard-box manufacturing revenue reaching CAD 7.9 billion (USD 6.19 billion).[4]Statistics Canada, “Retail E-commerce Sales in Canada,” 150.statcan.gc.ca Fulfilment centers demand right-sized corrugated, frustration-free designs and paper cushioning that lower dimensional-weight fees. Cascades Inc. highlighted customer preference for on demand box making systems in its 2024 annual report. Amazon’s pledge to eliminate plastic air pillows in North America by end-2025 further lifts demand for paper void fill. Regional converters with flexible order quantities gain share as omnichannel networks fragment shipment sizes and cut lead times.

Expansion of Food Delivery and Take-Out Culture

DoorDash, Uber Eats and SkipTheDishes retained elevated order volumes beyond the pandemic, intensifying the need for packaging that retains temperature and prevents leakage. The Canadian Restaurant Association stated that take-out represents a growing revenue share, particularly in dense urban markets. Kraft clamshells with grease-barrier coatings and windowed cartons have become standard for premium meal kits and ghost kitchens. Converters deploy short-run digital presses to enable menu-specific graphics and QR codes linking to loyalty programs. Restaurants also demand compostable seals, aligning with municipal organic-waste programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Pulp Prices | -0.80% | National, acute in provinces reliant on imported pulp | Short term (≤ 2 years) |

| Energy-cost Inflation in Manufacturing | -0.60% | National, concentrated in Ontario, Quebec, Atlantic Canada | Medium term (2-4 years) |

| Freight Rail Service Interruptions | -0.40% | National, critical for Western Canada to Eastern markets | Short term (≤ 2 years) |

| Limited Rural Recycling Infrastructure | -0.30% | Northern Canada, Atlantic Canada, rural Prairie regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Pulp Prices

Northern-bleached-softwood-kraft pulp fluctuated between USD 1,100 and USD 1,400 per tonne in 2024-2025 as Asian buyers tightened global supply. Integrated producers cushion volatility through captive mills, yet independents endure margin compression when contract pricing trails spot increases. Specialty grades, including high-brightness board for pharmaceuticals, rely on premium chemical pulp, limiting substitution with recycled fiber. Uncertain input costs delay capital expansion decisions and compel converters to negotiate pass-through clauses that strain customer relationships. Currency swings add complexity given the industry’s exposure to USD-denominated pulp transactions.

Energy-Cost Inflation in Manufacturing

Electricity accounts for 15-20% of mill operating expenses, and Ontario’s 2024 nuclear-refurbishment surcharge elevated industrial tariffs, while Hydro-Québec narrowed its cost advantage by raising large-power rates. Mills without biomass cogeneration, particularly in Atlantic Canada, face greater exposure to volatile natural-gas prices. Producers respond by lightweighting grades, installing heat-recovery systems and accelerating mergers that spread fixed energy costs over larger volumes. However, capital requirements for high-efficiency dryers or turbine upgrades challenge small converters and could trigger capacity rationalization in high-cost regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Corrugated Board Dominates Amid Specialty Paper Innovation

Corrugated board captured 46.19% of Canada paper packaging market share in 2025, buoyed by e-commerce shipping, agricultural exports and retail-ready displays. Its multilayered structure delivers stacking strength and cushioning at competitive cost, securing loyalty from omnichannel retailers and produce shippers. Specialty papers are projected to grow at a 6.78% CAGR, aided by dispersion-coated liners that withstand moisture without poly-laminates. The Canada paper packaging market size for specialty papers is poised to expand as brand owners pursue recyclable greaseproof sheets and metalized papers for premium chocolates.

Converters now integrate inline water-based coatings that rival plastic films in frozen-food and produce wraps. Cascades announced a 2024 partnership to commercialize compostable barrier papers, while mills test micro-fibrillated cellulose additives that enable lighter cartons without sacrificing strength. Pharmaceutical cartons increasingly specify bleached board with tight extractables limits, whereas industrial shipments favour recycled linerboard aligned with corporate sustainability targets. Investments in domestic specialty-paper machines broaden material choice and reduce reliance on European imports, supporting regional supply security.

By Product Type: Rigid Packaging Leads While Flexible Formats Accelerate

Rigid formats held 58.57% of 2025 revenue, anchored by folding cartons and corrugated boxes used across food, beverage and consumer goods. Corrugated variants span E-flute displays to double-wall containers for heavy components, while folding cartons dominate cereals, frozen meals and OTC pharmaceuticals. The Canada paper packaging market size for flexible formats is smaller but expanding at 6.93% as pouches displace rigid jars in coffee and pet treats.

Flexible papers offer weight savings, reseal ability and shelf appeal, leveraging advances in heat-sealable coatings and thin aluminium barriers. Mondi scaled recyclable paper pouches in 2024 targeting brands phasing out multi-material laminates. Wraps and films for candies, bakery release sheets and liner less labels round out the category. Brands pursue shipping cost cuts and lower carbon footprints by shifting from rigid composite cans to stand-up kraft pouches, compelling converters to install new slitters and pouch lines.

By Packaging Format: Secondary Packaging Anchors Demand While Primary Gains Momentum

Secondary cartons and shelf-ready trays commanded 51.53% share in 2025 as retailers value packaging that doubles as display and transit protection. Pallet stability, logistics labelling and easy shelf replenishment reinforce demand for robust outer cartons. Primary formats are forecast to grow at 6.56% as direct-to-consumer brands invest in premium mailer boxes with branded tissue and moulded-pulp inserts.

The Canada paper packaging market share within primary formats benefits from social-media unboxing trends that turn packaging into a marketing asset. Tertiary packaging remains vital for bulk moves, yet shippers adopt paper-based edge protectors and strap replacements to simplify recycling. Cross-format innovation blurs boundaries, with folding cartons serving as both shelf unit and e-commerce mailer following minor insert changes. Rail-service disruptions in 2024 pushed Western shippers to specify heavier-grade corrugated with moisture-barrier coatings to withstand long-haul vibration and condensation.

By End-Use Industry: Food Leads While E-Commerce Accelerates

Food retained 27.58% of 2025 demand, leveraging fiber’s breathability for produce and printability for branding. Beverage multipacks now use fiber can carriers that replace plastic rings, and coffee chains shift to fiber cup carriers. The Canada paper packaging market size allocated to e-commerce and retail is set to rise at 6.71% as online grocery and click-and-collect converge. Parcel packaging must endure conveyor drops and porch exposure while carrying bold branding that replaces in-store merchandising.

Personal care favours soft-touch cartons and embossing, whereas industrial and electronics specify anti-static corrugated liners. Cannabis cartons require child-resistant locks that rigid paperboard can accommodate under Health Canada rules. Meal-kit services blend food and e-commerce needs by bundling insulated liners, recipe cards and portion sachets, sustaining multi-format paper demand.

By Basis Weight: Mid-Range Grades Dominate While Lightweight Expands

Grades between 120-250 GSM held 38.19% share in 2025, powering folding cartons that endure automated filling and retail handling. Sub-70 GSM papers are projected to advance at 7.11% CAGR as brands lightweight inner liners and wrap films to cut freight emissions. The Canada paper packaging market size for sub-70 GSM grades supports multi-wall sacks that combine several thin plies to achieve burst strength.

Calendaring upgrades boost smoothness and opacity for high-graphics printing on lighter paper. Smurfit WestRock commercialized micro-flute corrugated using thinner liners, reducing material by 10-15% while meeting compression standards. Above-250 GSM board remains critical for frozen-food cartons requiring polyethylene coatings, though innovations in water-based barriers may allow thickness reductions. Lightweight grades also aid provincial diversion targets by trimming material entering waste streams.

By Printing Technology: Flexography Prevails While Digital Gains Share

Flexography accounted for 42.61% of 2025 spend, valued for plate longevity, high speed and water-based inks that satisfy food-contact rules. Offset lithography retains hold in high-graphic folding cartons, and gravure remains for ultra-long flexible runs, though capital intensity limits adoption. Digital printing is forecast to rise at 7.23% as variable data and small-batch personalization gain traction.

HP partnered with Canadian converters in 2024 to install PageWide web presses capable of mid-volume runs. The Canada paper packaging industry applies digital modules in hybrid lines that lay down base colors via flexo then add QR codes digitally, marrying cost efficiency with customization. Digital eliminates plate waste, cuts lead times and reduces obsolescence, aligning with brand sustainability and just-in-time supply goals.

Geography Analysis

Ontario and Quebec anchor most national capacity thanks to proximity to consumers, abundant hydro power and established pulp integration. Integrated mills in Windsor-Toronto-Ottawa and Saint-Jean-sur-Richelieu produce everything from linerboard to barrier-coated board, while co-packing clusters serve food and personal-care brands.

Harmonized EPR rules announced in 2024 spurred fresh investments in material recovery facilities, boosting recycled-fiber supply for Canada paper packaging market size expansion in recycled grades. Rest of Western Canada is building capacity faster, with British Columbia pulp mills adding corrugators and Prairie grain elevators integrating bag-making lines to service agricultural exports.

Regional plants reduce exposure to transcontinental rail delays and capitalize on Asian equipment imports via Pacific ports. Atlantic and Northern Canada struggle with small markets, higher energy costs and limited recycling networks, constraining recycled-content output. Federal infrastructure grants and territorial waste-diversion programs provide initial funding for balers and reverse logistics, but freight distance still favours collapsible, lightweight formats that reduce cost. Indigenous-owned start-ups in Nunavut seek to localize folding carton production for traditional food packaging, representing emerging opportunities.

Competitive Landscape

Canada’s paper packaging sector is moderately concentrated. Cascades Inc., Kruger Inc. and Smurfit WestRock control a large share of integrated capacity, while dozens of independents compete on lead time, design and regional service. Integrated producers leverage captive pulp and co-generation to buffer energy and fiber volatility, and they invest in proprietary barrier grades commanding premium margins.

Independents differentiate through micro-flute die-cutting, rapid structural prototyping and digital print capability attractive to craft beverage and specialty food customers. Technology adoption accelerates the arms race: inline machine-vision inspection cuts waste, while cloud-based order systems enable same-day artwork changes. Cross-border competition from U.S. mills remains strong under CUSMA, but Canadian converters also export to northern U.S. states leveraging currency advantages.

Regulatory expertise in food-contact compliance forms a barrier to entry, yet specialized consultancies now help smaller firms bridge gaps. Patented moulded-pulp clamshells with integrated locking tabs filed by Cascades in 2024 showcase innovation that eliminates metal fasteners, simplifying recycling. Meanwhile, regional converters collaborate with logistics providers to offer warehousing and kitting, embedding themselves deeper in brand supply chains.

Canada Paper Packaging Industry Leaders

Cascades Inc.

Smurfit WestRock

Graphic Packaging Holding Company

Crown Holdings Inc.

Tetra Pak International SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Cascades announced the sale of its Flexible Packaging plant activities to Five Star Holding for CAN 31 million (USD 22.23 million).

- July 2024: Smurfit Kappa and WestRock closed their USD 11.2 billion merger, creating Smurfit WestRock with expanded Canadian corrugated capacity.

- June 2024: Anti-greenwashing provisions under Bill C-59 took effect, mandating proof for recyclability claims on packaging.

- May 2024: British Columbia implemented its EPR framework, requiring 75% paper packaging recovery by 2026.

Canada Paper Packaging Market Report Scope

The Canada Paper Packaging Market Report is Segmented by Material Type (Kraft Paper, Paperboard, Corrugated Board, Specialty Papers), Product Type (Flexible and Rigid Paper Packaging), Packaging Format (Primary, Secondary, Tertiary), End-Use Industry (Food, Beverage, Healthcare, Personal Care, Industrial, E-commerce, Other), Basis Weight (Sub-70 GSM, 70-120 GSM, 120-250 GSM, Above-250 GSM), Printing Technology (Flexographic, Offset, Digital, Gravure), and Geography (Ontario, Quebec, Rest of Western Canada, Atlantic Canada, Northern Canada). Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Kraft Paper |

| Paperboard |

| Corrugated Board |

| Specialty Papers |

By Product Type

| Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | |

| Other Flexible Paper Packaging | |

| Rigid Paper Packaging | Folding Carton |

| Corrugated Boxes | |

| Other Rigid Paper Packaging |

By Packaging Format

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transit Packaging |

By End-Use Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Electronics |

| E-commerce and Retail |

| Other End-Use Industries |

By Basis Weight

| Less Than 70 GSM |

| 70-120 GSM |

| 120-250 GSM |

| More Than 250 GSM |

By Printing Technology

| Flexographic Printing |

| Offset Lithography |

| Digital Printing |

| Gravure Printing |

| By Material Type | Kraft Paper | |

| Paperboard | ||

| Corrugated Board | ||

| Specialty Papers | ||

| By Product Type | Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | ||

| Other Flexible Paper Packaging | ||

| Rigid Paper Packaging | Folding Carton | |

| Corrugated Boxes | ||

| Other Rigid Paper Packaging | ||

| By Packaging Format | Primary Packaging | |

| Secondary Packaging | ||

| Tertiary / Transit Packaging | ||

| By End-Use Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial and Electronics | ||

| E-commerce and Retail | ||

| Other End-Use Industries | ||

| By Basis Weight | Less Than 70 GSM | |

| 70-120 GSM | ||

| 120-250 GSM | ||

| More Than 250 GSM | ||

| By Printing Technology | Flexographic Printing | |

| Offset Lithography | ||

| Digital Printing | ||

| Gravure Printing | ||

Key Questions Answered in the Report

What is the current value of the Canada paper packaging market?

The market stands at USD 20.23 billion in 2026 and is projected to reach USD 27.21 billion by 2031.

How fast is corrugated board demand growing in Canada?

Corrugated board already leads with 46.19% share in 2025 and continues to rise as e-commerce and agricultural exports expand.

Which segment is expanding fastest within paper packaging?

Flexible paper packaging is forecast to grow at 6.93% CAGR through 2031, driven by pouches and lightweight bags.

How do federal plastic bans influence paper packaging?

The bans directly shift food-service and retail applications to fiber-based clamshells, trays and bags, locking in long-term paper demand.

What role does digital printing play in Canadian converters strategies?

Digital presses enable short runs and variable graphics, helping converters win craft beverage, meal-kit and promotional work while supporting sustainability through reduced plate waste.

Why are energy costs a concern for Canadian paper mills?

Electricity and natural-gas prices comprise up to 20% of operating expenses, and recent tariff hikes in Ontario and Quebec squeeze margins unless mills invest in co-generation or energy-efficient

Page last updated on: