Von Willebrand Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

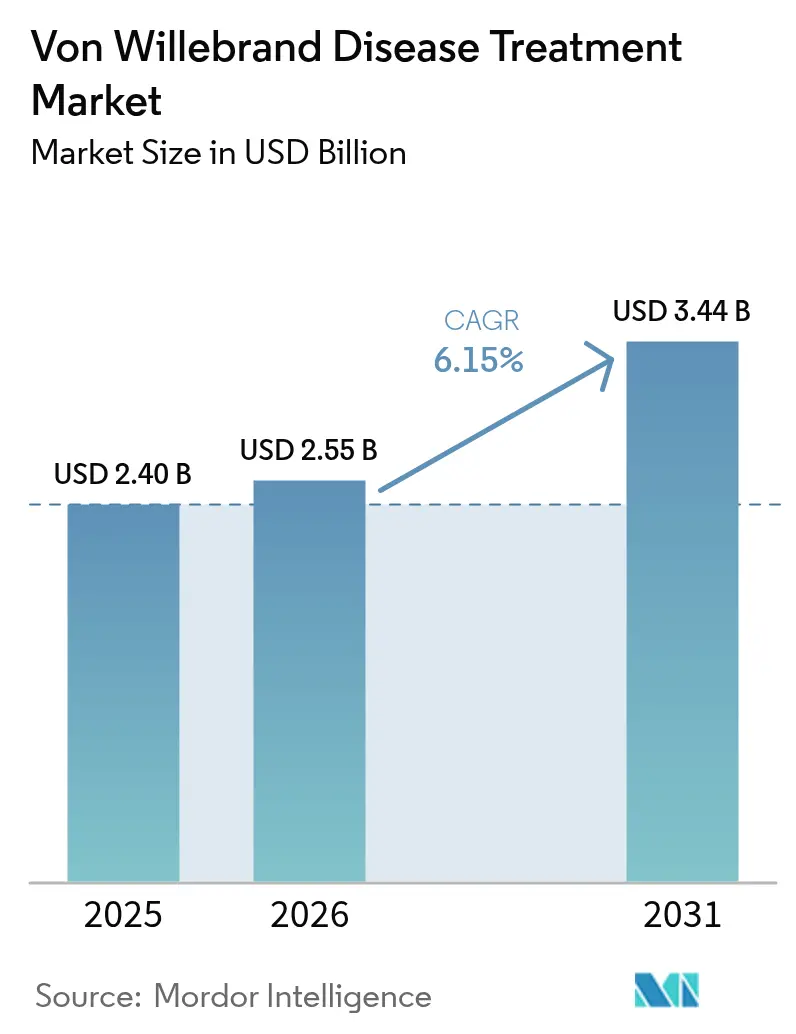

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 3.44 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Von Willebrand Disease Treatment Market Analysis by Mordor Intelligence

The Von Willebrand disease treatment market size was valued at USD 2.40 billion in 2025 and estimated to grow from USD 2.55 billion in 2026 to reach USD 3.44 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031). Uptake of curative gene therapies, rapid adoption of AI-supported diagnostics, and payer acceptance of value-based reimbursement are accelerating revenue growth, while hospital formularies increasingly favor recombinant, pathogen-free concentrates over plasma-derived options. Expansion of federal patient-assistance schemes in North America, wider newborn genetic screening in Asia-Pacific, and fast-track review of subcutaneous desmopressin nano-formulations also deepen addressable demand. Gene therapies such as Pfizer’s BEQVEZ and CSL Behring’s HEMGENIX, both cleared in 2024–2025, create the prospect of one-time interventions that reduce lifelong factor consumption. Despite strong momentum, the Von Willebrand disease treatment market still contends with under-diagnosis in low-income geographies, high upfront gene-therapy costs, and temperature-sensitive supply chains for plasma products.

Key Report Takeaways

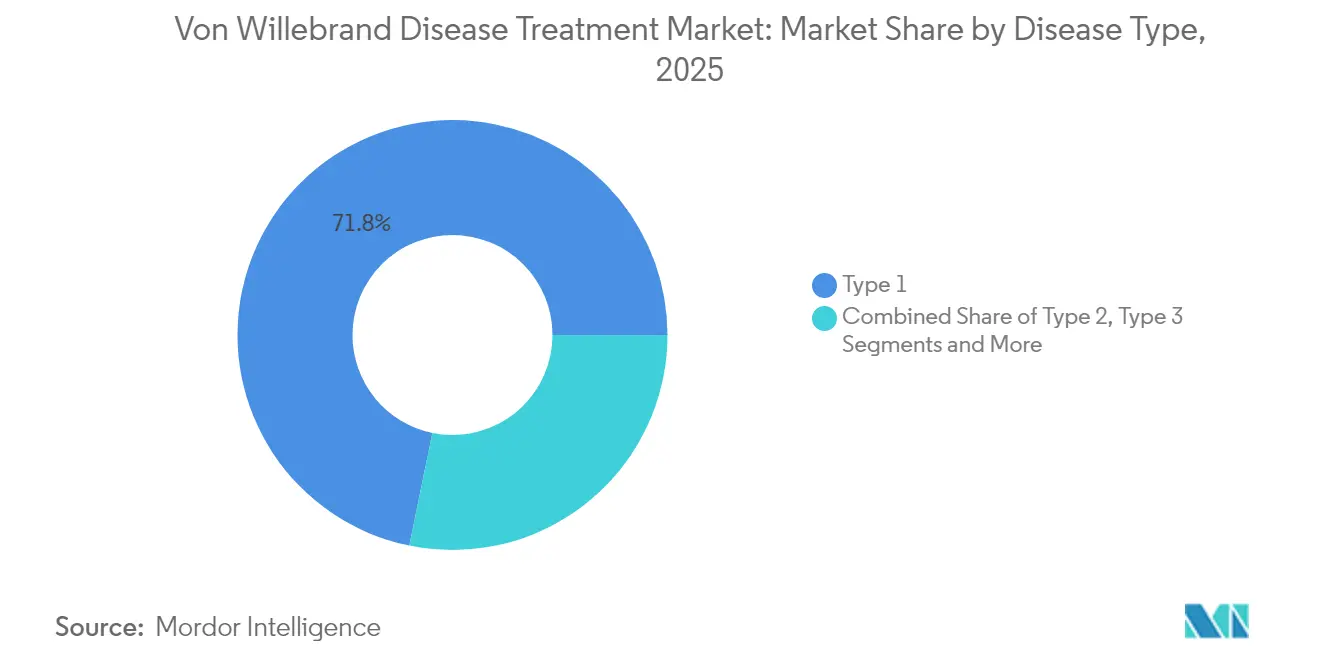

- By disease type, Type 1 held 71.78% of the Von Willebrand disease market share in 2025; Acquired VWD is forecast to grow at 10.78% CAGR to 2031.

- By treatment type, VWF/FVIII combination concentrates led with 46.02% revenue share in 2025; recombinant VWF-only concentrates are expanding at a 13.05% CAGR through 2031.

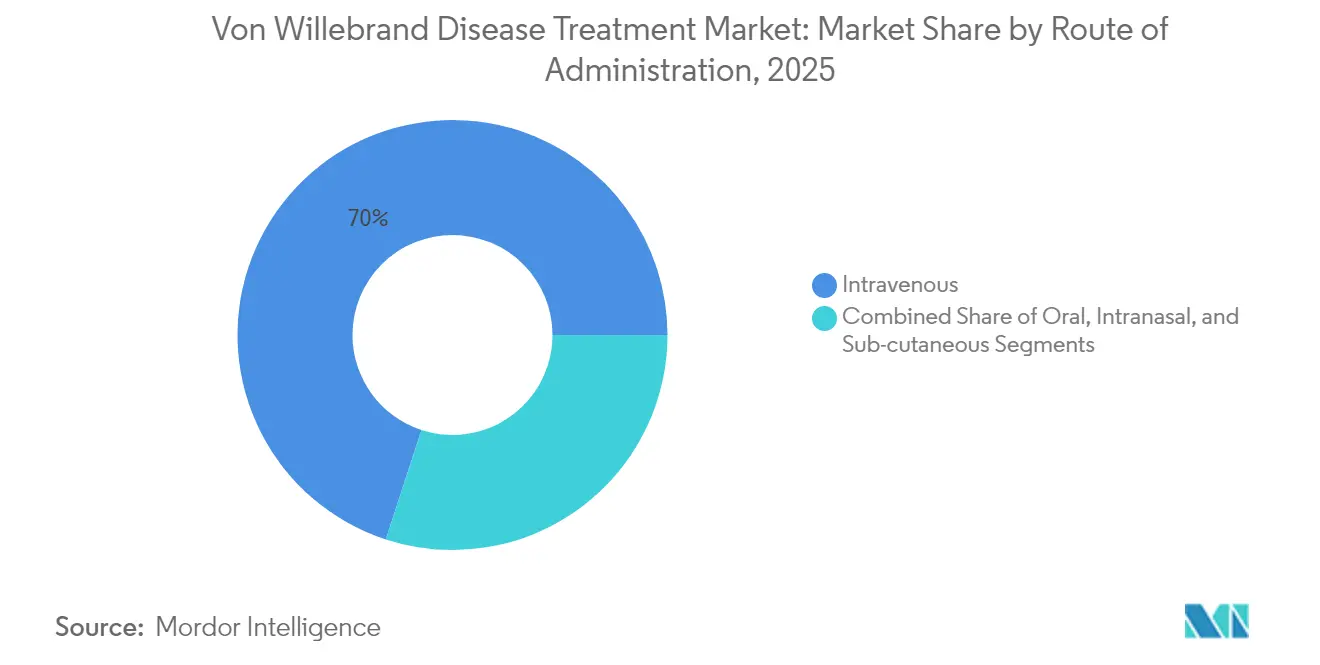

- By route of administration, intravenous therapy commanded 69.98% of the Von Willebrand disease market size in 2025, whereas subcutaneous delivery is rising at 12.78% CAGR to 2031.

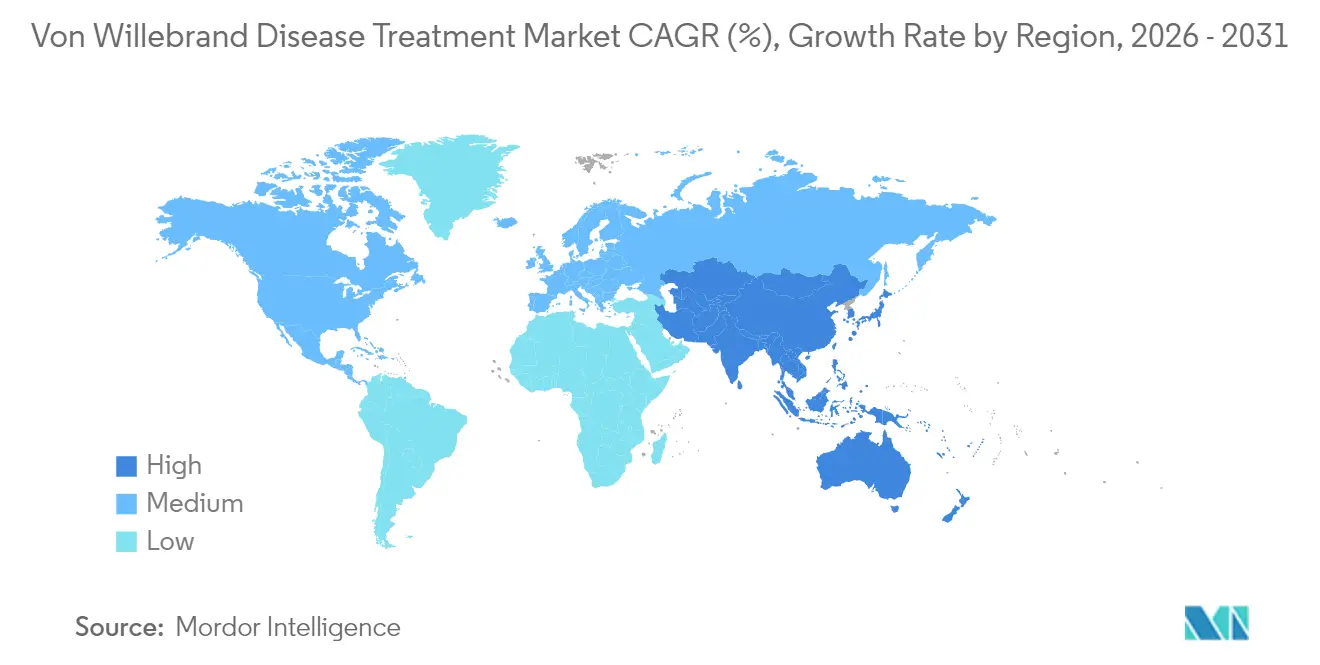

- By geography, North America accounted for 38.36% share in 2025; Asia-Pacific shows the fastest regional CAGR at 10.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Von Willebrand Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Patient-Assistance & Charitable-Access Schemes | +0.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Rising Diagnosis From Wider Prophylactic Genetic Screening | +1.2% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Increasing Hospital Adoption Of Recombinant VWF-Only Concentrates | +0.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| FDA Fast-Track For Sub-Cutaneous DDAVP Nano-Formulations | +0.6% | Global regulatory harmonization | Medium term (2-4 years) |

| Surge In Pay-For-Performance Hemophilia Centers Bundling VWD Care | +0.7% | North America, pilot programs in EU | Short term (≤ 2 years) |

| AI-Enabled Bleeding-Risk Decision Engines Integrated In EHRs | +0.5% | North America & EU, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Patient-Assistance & Charitable-Access Schemes

Federal funding for 141 Hemophilia Treatment Centers lets providers dispense discounted factor products under the 340B program, reducing out-of-pocket costs and improving adherence[1]National Bleeding Disorders Foundation, “Federal Programs for People with Bleeding Disorders,” bleeding.org. State action, such as California’s All Copays Count law, further lowers financial hurdles, while CMS has steadily raised the clotting-factor furnishing fee, ensuring predictable reimbursement. These measures make therapies accessible to underserved patients, sustaining demand across the Von Willebrand disease treatment market. Replication of this multi-stakeholder model in Europe and emerging economies is expected to widen global reach. Charitable foundations also finance prophylaxis for uninsured adults, boosting treatment volume.

Rising Diagnosis From Wider Prophylactic Genetic Screening

Countries adding dried-blood-spot biomarker panels to newborn screening achieve 95% detection accuracy for bleeding disorders that routine tests miss. Asia-Pacific health ministries are scaling similar programs, doubling the recognized VWD population in pilot provinces. Sweden’s inclusion of NT-proBNP and IL-1 RL1 biomarkers illustrates how early detection shifts identification to infancy, prompting timely intervention and enlarging the Von Willebrand disease treatment market. Together with ATHN’s natural-history registry, real-world outcome data now drives payer coverage for proactive treatments. The diagnostic surge builds a stable pipeline of patients requiring lifelong or curative therapies.

Increasing Hospital Adoption Of Recombinant VWF-Only Concentrates

Hospital formularies favor recombinant concentrates because they eliminate blood-borne pathogen risk and show superior multimeric composition recovery, especially in Type 2A cases. FDA expansion of wilate for universal prophylaxis and its 2025 orphan-drug exclusivity accelerate uptake[2]Octapharma USA, “FDA Grants Orphan Drug Exclusivity to wilate,” octapharma.com. Value-based contracts reward reduced emergency visits, so hospitals prioritize agents with 94% bleed-prevention efficacy. As bundled-payment models proliferate, recombinant products win preferred status, enlarging revenue within the Von Willebrand disease treatment market.

FDA Fast-Track For Sub-Cutaneous DDAVP Nano-Formulations

GC Biopharma’s GC1130A secured fast-track review in 2024, signaling regulator commitment to formulations that enhance dosing precision and patient acceptance. Subcutaneous nano-particles promise controlled release that reduces tachyphylaxis and lengthens dosing intervals. Pediatric acceptance rises because injections bypass the discomfort of nasal sprays, while pharmacokinetic modeling supports individualized regimens. When cleared, these assets will reduce hospital chair time and reinforce adherence, adding fresh momentum to the Von Willebrand disease treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Under-Diagnosis In Low-Income Geographies | -1.1% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| High Lifetime Therapy Cost Despite Biosimilar Entries | -0.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Limited Cold-Chain Capacity For Plasma-Derived Products In Africa | -0.4% | Sub-Saharan Africa, selective MEA markets | Medium term (2-4 years) |

| Regulatory Uncertainty Around Gene-Editing Trials For VWD | -0.3% | Global, regulatory harmonization pending | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Under-Diagnosis In Low-Income Geographies

Many developing countries identify fewer than 10% of expected cases, curbing demand growth for therapies. Limited laboratory capacity, scarce coagulation reagents, and low clinician awareness mean VWD symptoms are often misattributed to gynecological or infectious conditions. Investment priorities favor communicable diseases, delaying introduction of specialist diagnostics. International donor partnerships remain small-scale, so coverage gaps are unlikely to close quickly, weighing on the global Von Willebrand disease treatment market.

High Lifetime Therapy Cost Despite Biosimilar Entries

Gene therapies are priced at USD 3.5 million per dose in the United States, generating budget shock for payers despite long-term cost offsets. In Brazil, median annual expenditure for hemophilia A therapy exceeds USD 90,000 equivalent, indicating affordability concerns even in universal healthcare systems. Insurers impose step-therapy rules and prior authorizations that delay treatment initiation. Out-of-pocket requirements erode adherence and can lead to costly bleed-related complications, dampening uptake across the Von Willebrand disease treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Type 1 Dominance Drives Market Stability

Type 1 VWD generated 71.78% of global revenue in 2025, anchoring the Von Willebrand disease treatment market size for that year. Prevalent mild phenotypes rely on affordable desmopressin, sustaining predictable volumes. Acquired VWD, while smaller today, delivers the fastest expansion at 10.78% CAGR through 2031 as oncologists and cardiologists test patients pre-procedure. Type 2 sub-variants together add clinical complexity because they require concentrate prophylaxis; Type 2A cases especially benefit from recombinant VWF-only products that restore high-molecular-weight multimers, reducing annual bleed rate.

The severe but rare Type 3 cohort incurs disproportionate costs due to intensive factor infusions and orthopedic surgeries, highlighting reimbursement challenges in emerging economies. Long-term center experience shows persistent under-diagnosis across all types, prompting calls for registry expansion and payer support for genetic testing. Growing awareness of drug-induced VWD in aging populations further enlarges the Von Willebrand disease treatment market.

By Treatment Type: Recombinant Innovation Challenges Traditional Concentrates

Combination VWF/FVIII concentrates retained 46.02% of revenue in 2025, reflecting broad clinical familiarity and dual factor coverage. Yet recombinant VWF-only lines are rising fast at 13.05% CAGR, signaling a decisive procurement shift. Hospitals seek pathogen-free products amid heightened pharmacovigilance, and value-based contracts incentivize bleed reduction, accelerating recombinant adoption in the Von Willebrand disease treatment market. Desmopressin remains key for Type 1 management, though nasal-spray adherence issues motivate investment in subcutaneous nano-formulations.

Antifibrinolytics such as tranexamic acid, alongside topical agents, provide adjunct control for mucosal bleeds. Curative gene therapies are emerging, following BEQVEZ proof-of-concept, and they could reset demand profiles by reducing recurrent concentrate use. Octapharma’s wilate prophylaxis label broadening forces competitors to demonstrate comparative efficacy, intensifying innovation within the Von Willebrand disease treatment market.

By Route of Administration: Subcutaneous Innovation Transforms Patient Experience

Intravenous infusion remained dominant with 69.98% share in 2025 because clinical protocols and infusion-center infrastructure are well established. However, subcutaneous delivery grows at 12.78% CAGR, reflecting demand for self-administration. Alhemo’s 2024 approval confirms daily subcutaneous prophylaxis can match IV efficacy, freeing patients from port-access hurdles. Intranasal DDAVP supports pediatric and mild cases, but variable absorption limits adult use. Oral antifibrinolytics remain supplemental, with research underway into oral desmopressin bio-enhancers that could further diversify options.

Patient-reported-outcome studies show higher satisfaction scores and lower missed-dose rates with subcutaneous regimens, implying a structural shift in the Von Willebrand disease treatment market. Controlled-release injections designed for weekly or monthly dosing aim to displace traditional IV prophylaxis in high-income geographies.

Geography Analysis

North America contributed 38.36% of 2025 revenue, underpinned by 340B discounts and comprehensive treatment-center networks that guarantee product access. Gene therapy reimbursement frameworks emerge first in the United States, enabling earlier adoption and supporting premium pricing. Canada trails slightly due to provincial formulary reviews but benefits from centralized plasma procurement.

Europe exhibits high recombinant uptake as national payers demand virus-safe concentrates, yet stringent health-technology assessments delay some novel therapies. Western European markets negotiate risk-sharing deals for gene therapy, tying payment to sustained factor independence, which shapes purchasing dynamics in the Von Willebrand disease treatment market. Eastern Europe faces tighter budgets and slower diagnostic rollout, creating a two-tier landscape within the region.

Asia-Pacific leads growth with a 10.12% CAGR through 2031 because regulators are streamlining review pathways and governments are investing in local manufacturing. China, India, and South-Korea expand newborn-screening panels and subsidize concentrate imports, driving double-digit volume gains. South America, notably Brazil, leverages centralized purchasing and clinical-protocol standardization to broaden access despite economic constraints. In contrast, Middle East and Africa progress is hampered by diagnostic and cold-chain deficits, although recombinant price declines could unlock latent demand later in the forecast.

Competitive Landscape

The Von Willebrand disease treatment market remains moderately consolidated, with CSL Behring, Takeda, and Octapharma controlling the bulk of plasma-derived concentrate supply. Their vertical integration from plasma collection to finished biologics ensures scale economies and supply security. Market entrants focus on recombinant innovation, subcutaneous delivery, and curative modalities to differentiate. CSL Behring expands beyond plasma through HEMGENIX gene therapy, while Sanofi uses RNA-interference candidate Qfitlia to address inhibitor populations.

Strategic alliances proliferate. Plasma leaders license AI-driven dosing software to embed value-based outcomes in sales pitches. Gene-therapy developers forge risk-sharing accords with U.S. Medicaid programs to expedite patient onboarding. Device makers collaborate with concentrate suppliers to co-package subcutaneous autoinjectors, simplifying home use. Competitive intensity therefore shifts from pure volume toward clinical-outcome differentiation, reshaping commercial models across the Von Willebrand disease treatment market.

White-space opportunities include diagnostic platforms for low-income regions, extended-half-life recombinant constructs, and cold-chain-free formulations. Barriers to entry encompass plasma-fractionation capital cost, complex biologic approvals, and payer hesitancy around high upfront gene-therapy prices. Nonetheless, innovation and partnership depth suggest gradual dilution of incumbent share, bringing heightened rivalry through 2030.

Von Willebrand Disease Treatment Industry Leaders

CSL Behring

Grifols, S.A.

Octapharma AG

Bio Products Laboratory Ltd.

Takeda (Shire)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Hemab Therapeutics dosed the first participant in Velora Pioneer, its Phase 1/2 study of HMB-002, a subcutaneous therapy for VWD.

- January 2025: Star Therapeutics received FDA Fast-Track designation for VGA039 in VWD.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the von Willebrand disease (VWD) treatment market as all prescription medicinal products, plasma-derived, recombinant, synthetic or adjunctive, that are administered to prevent or control bleeding episodes in patients diagnosed with Type 1, Type 2 (2A, 2B, 2M, 2N), Type 3, or acquired VWD.

The review leaves out diagnostic assays, general hemostatic agents used for surgery-related bleeding unrelated to VWD, and pipeline gene therapies that are still in clinical trials.

Segmentation Overview

- By Disease Type

- Type 1

- Type 2 (2A, 2B, 2M, 2N)

- Type 3

- Acquired VWD

- By Treatment Type

- Desmopressin (DDAVP)

- VWF/FVIII Combination Concentrates

- Recombinant VWF-only Concentrates

- Antifibrinolytics (e.g., Tranexamic Acid)

- Topical & Adjunctive Agents

- By Route of Administration

- Intravenous

- Intranasal

- Oral

- Sub-cutaneous

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with hematologists, hospital pharmacists, and payer advisers across North America, Europe, and Asia helped validate treated-patient ratios, average annual IU usage, and the speed at which prophylactic regimens are replacing on-demand care. Follow-up surveys with advocacy groups clarified self-infusion uptake and out-of-pocket hurdles.

Desk Research

Analysts began with curated medical-science databases, combing peer-reviewed journals such as Blood and Haemophilia for prevalence ratios and dose-response data. We added regulatory statistics from the FDA's Biologics License Application archive, EMA's Community Register, and reimbursement tariffs published by CMS and Germany's G-DRG catalog. Trade groups, for example, the World Federation of Hemophilia, provided annual patient and treatment-days counts, while import-export trends were parsed through Volza shipment data to benchmark concentrate flows. Company 10-Ks, investor decks, and Factiva press archives enriched price-mix and launch timelines. These sources, though illustrative, are not exhaustive; numerous additional public records underpin the evidence base.

Market-Sizing & Forecasting

A prevalence-to-treated-cohort top-down model anchors our baseline. Diagnosed prevalence per geography is multiplied by treatment penetration and average annual dose to yield volume, which is then priced using cleansed ASP ranges. Supplier roll-ups and sampled tender data supply a selective bottom-up cross-check, letting us adjust outliers. Key variables include newborn screening coverage, prophylaxis share, shift from plasma to recombinant VWF, mean IU per infusion, and regional ASP dispersion. Multivariate regression, coupled with scenario analysis for gene-therapy arrival, projects figures to 2030; missing micro-data are bridged with clinically accepted dose bands and regional payer caps.

Data Validation & Update Cycle

Outputs pass anomaly screens against independent hospital utilization audits and customs trends before a two-step analyst review. The dataset refreshes annually, with interim updates whenever material events, such as a new biologic approval or reimbursement change, trigger a re-run.

Why Our Von Willebrand Disease Treatment Baseline Stands Up to Scrutiny

Published estimates vary because firms pick different product baskets, patient funnels, and refresh cadences.

Key gap drivers include inclusion of diagnostic revenues, absence of penetration adjustments for emerging economies, or single-source ASP assumptions. Mordor's disciplined scope definition, dual-sourced volume checks, and annual refresh mitigate these pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.40 B | Mordor Intelligence | - |

| USD 2.51 B | Global Consultancy A | Bundles diagnostic kit sales and counts prophylaxis uptake at 100 % in developed nations |

| USD 1.88 B | Industry Association B | Uses reported sales from five majors only; omits hospital-compounding and regional generics |

In sum, clients gain a balanced, transparent baseline from Mordor Intelligence, one that traces every dollar to clear epidemiologic and pricing variables and can be repeated or stressed without hidden assumptions.

Key Questions Answered in the Report

What is the current size of the Von Willebrand disease treatment market?

The market reached USD 2.55 billion in 2026 and is projected to grow to USD 3.44 billion by 2031 at a 6.15% CAGR.

Which disease segment generates the largest revenue?

Type 1 VWD accounts for 71.78% of global revenue, reflecting its high prevalence and reliance on cost-effective desmopressin therapy.

How fast is the recombinant VWF-only concentrate segment growing?

Recombinant VWF-only products are expanding at a 13.05% CAGR, outpacing plasma-derived options due to safety and efficacy advantages.

Why is Asia-Pacific the fastest-growing regional market?

Government investment in screening and regulatory convergence initiatives produce a 10.12% CAGR, making Asia-Pacific the most dynamic region.

What role do gene therapies play in future growth?

Recently approved one-time treatments like BEQVEZ and HEMGENIX can reduce lifelong factor use, creating new revenue streams while reshaping payer economics.

Page last updated on: