Thrombosis Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

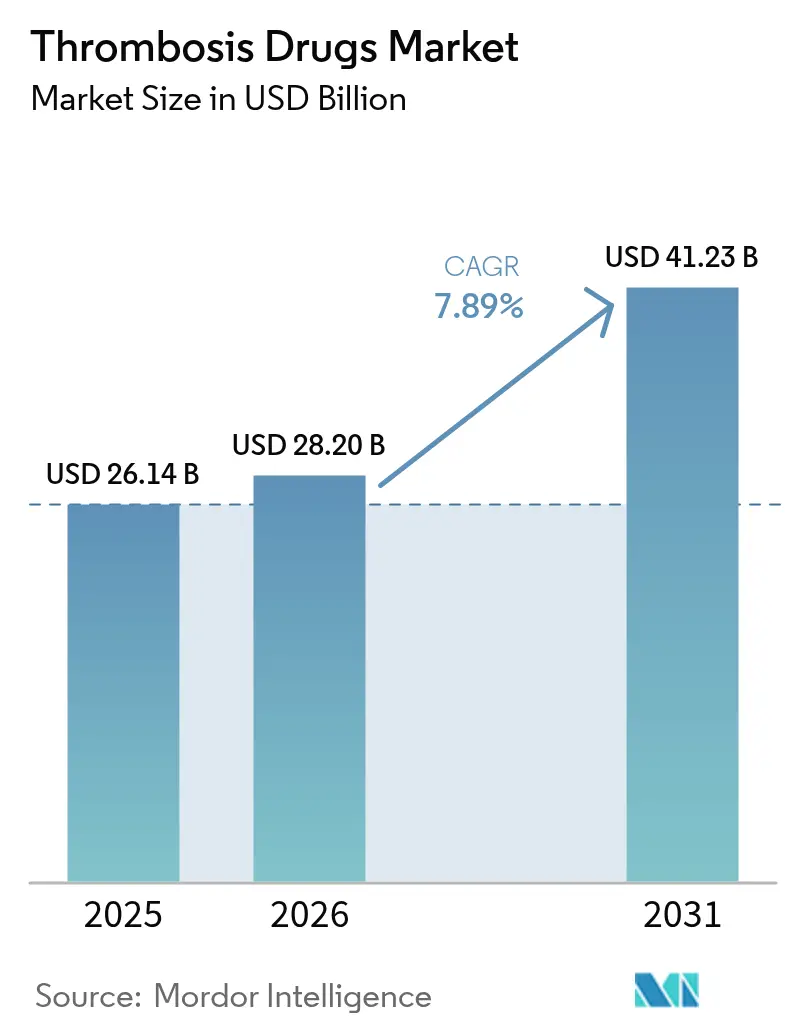

| Market Size (2026) | USD 28.2 Billion |

| Market Size (2031) | USD 41.23 Billion |

| Growth Rate (2026 - 2031) | 7.89% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thrombosis Drugs Market Analysis by Mordor Intelligence

The thrombosis drugs market size was valued at USD 26.14 billion in 2025 and estimated to grow from USD 28.2 billion in 2026 to reach USD 41.23 billion by 2031, at a CAGR of 7.89% during the forecast period (2026-2031). Expanded life expectancy, rising venous thrombo-embolism (VTE) incidence, and accelerated adoption of direct oral anticoagulants (DOACs) are underpinning steady demand. Regulatory green lights for first-in-class Factor XI inhibitors, together with artificial-intelligence risk stratification tools, are recasting therapy selection beyond warfarin and heparin. Hospitals continue to favor rapid-onset injectables for acute care even as outpatient use of once-daily oral DOACs becomes the routine standard. Competitive responses to approaching patent cliffs include consolidation around safer mechanisms of action and discount programs aimed at sustaining loyalty during the shift from brands to generics.

Key Report Takeaways

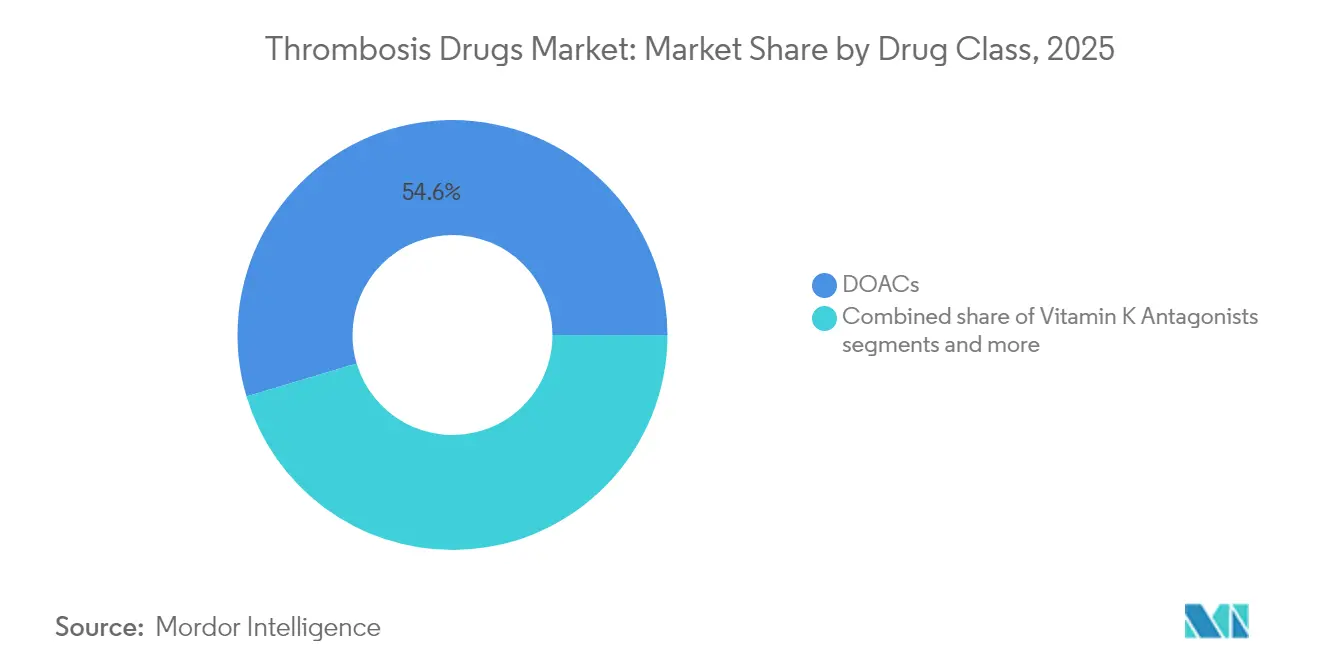

- By drug class, DOACs captured 54.62% of thrombosis drugs market share in 2025, while Factor XI inhibitors are projected to expand at an 8.24% CAGR through 2031.

- By disease type, deep-vein thrombosis led with 31.22% share of the thrombosis drugs market size in 2025; pulmonary embolism is set to grow at an 8.12% CAGR by 2031.

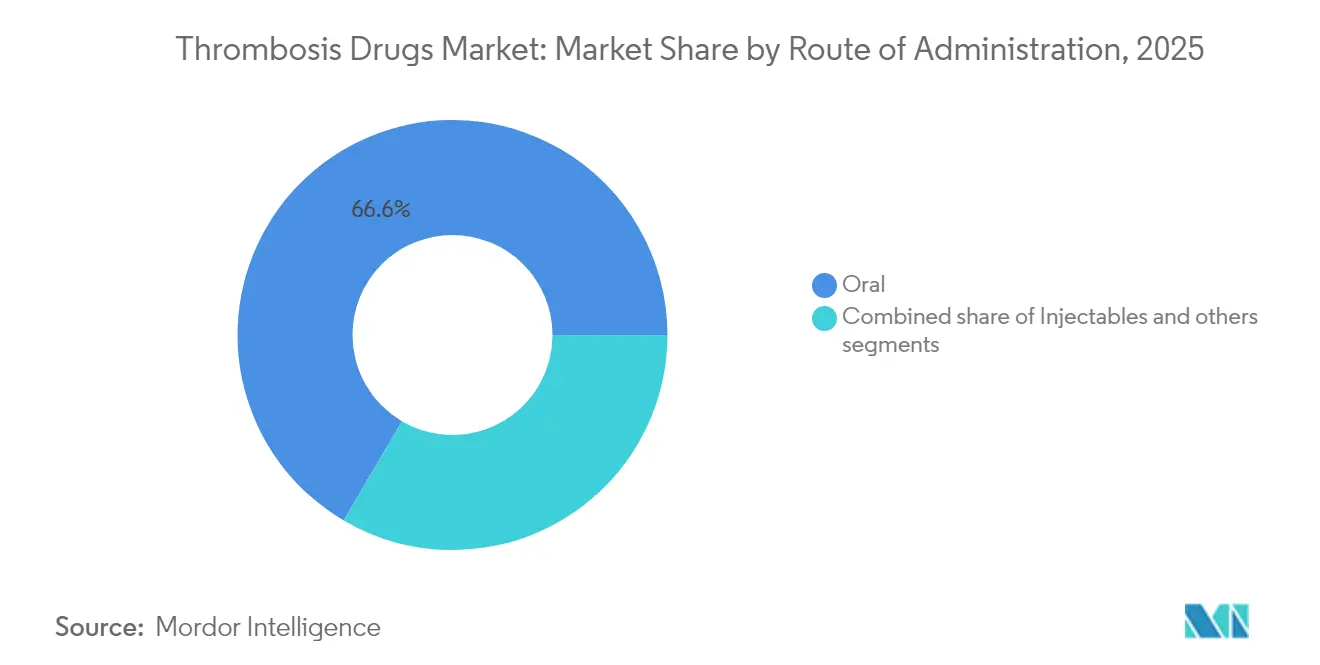

- By route of administration, oral products commanded 66.55% of the thrombosis drugs market size in 2025, whereas injectables are forecast to grow at 7.98% CAGR through 2031.

- By geography, North America held 37.86% of thrombosis drugs market share in 2025; Asia-Pacific is the fastest-growing region at 7.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thrombosis Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising venous thrombo-embolism (VTE) prevalence | +2.1% | Global, with concentration in aging populations of North America & Europe | Long term (≥ 4 years) |

| Rapid adoption of direct oral anticoagulants (DOACs) | +1.8% | North America & Europe leading, Asia-Pacific following | Medium term (2-4 years) |

| Growing surgical volumes & peri-operative prophylaxis need | +1.4% | Global, driven by Asia-Pacific healthcare expansion | Medium term (2-4 years) |

| Pipeline of Factor XI inhibitors promising lower bleed risk | +1.2% | North America & Europe early adoption, global expansion | Long term (≥ 4 years) |

| COVID-triggered protocols for inpatient thromboprophylaxis | +0.8% | Global, with persistent impact in hospital systems | Short term (≤ 2 years) |

| Expansion of AI-based risk stratification enabling targeted therapy | +0.6% | North America & Europe leading, selective Asia-Pacific adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising VTE prevalence

Higher life expectancy and a surge in cancer survival elevate VTE incidence, making long-term anticoagulation an essential component of chronic disease care. Lung-cancer patients face pulmonary-embolism rates roughly six times the population baseline, creating durable demand for safer oral agents[1]Source: Zhang Yi-Wen et al., “Research progress on the association between lung cancer and pulmonary embolism,” Journal of Cardiothoracic Surgery, journal.cardiothoracsurg.com . Hospitals respond by embedding thrombosis protocols within oncology pathways, shifting anticoagulation from episodic to continuous management.

Rapid adoption of DOACs

Evidence from ROCKET-AF and ARISTOTLE continues to drive prescriber confidence in rivaroxaban and apixaban. Bristol Myers Squibb and Pfizer recorded USD 3.2 billion in Eliquis sales in Q4 2024. Upcoming Medicare-negotiated prices effective January 2026 lower patient out-of-pocket costs, broadening eligibility without compromising margins.

Growing surgical volumes & peri-operative prophylaxis

Elective and trauma surgeries are rising fastest in Asia-Pacific, where low-molecular-weight heparins (LMWHs) cut hospital stays from 3.3 to 2.4 days in atrial-fibrillation cases. Outpatient same-day procedures heighten the need for predictable injectables that bridge surgery with outpatient prophylaxis.

Expanding pipeline of Factor XI inhibitors

Abelacimab reduced major or clinically relevant bleeding by 67% versus rivaroxaban in Phase II studies[2]Source: Anthos Therapeutics, “Abelacimab 150 mg Demonstrated 67% Bleeding Reduction,” Anthostherapeutics.com . Novartis secured the candidate through a USD 925 million acquisition that underscores industry intent to leapfrog DOAC safety limits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of novel anticoagulants | -1.5% | Global, with acute impact in price-sensitive emerging markets | Medium term (2-4 years) |

| Patent expiries & generic erosion | -1.2% | North America & Europe primarily, spreading to global markets | Short term (≤ 2 years) |

| Safety concerns – major bleeding & limited reversal agents | -0.9% | Global, with regulatory focus in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of novel anticoagulants

List prices often dwarf those of warfarin, curbing uptake in price-sensitive regions. Bristol Myers Squibb and Pfizer now sell Eliquis direct to patients at 40% discount, dropping monthly costs to USD 346. Policy shifts such as Medicare negotiations suggest broader price pressure is imminent.

Patent expiries & generic erosion

FDA approval of generic rivaroxaban in March 2025 precipitated a 31% drop in Bayer’s Xarelto sales during Q1 2025. Similar erosion looms for Eliquis in 2028, forcing innovators to migrate portfolios toward next-generation assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: DOAC dominance alongside Factor XI momentum

DOACs yielded 54.62% thrombosis drugs market share in 2025 and represent a USD 14.28 billion slice of the thrombosis drugs market size, expanding on the back of simplified dosing and fewer monitoring demands. Factor XI inhibitors are forecast to climb at an 8.24% CAGR, converting bleeding-averse clinicians and patients.

Heparin and LMWHs sustain relevance for in-patient bridging and oncology protocols. Vitamin K antagonists retreat to resource-limited settings, while thrombolytics retain niche roles in stroke and massive pulmonary-embolism emergencies. The arrival of once-monthly subcutaneous Factor XI agents could blur traditional oral-versus-injectable boundaries, recasting competitive alignment within the thrombosis drugs market.

By Disease Type: DVT leadership against rapid PE growth

Deep-vein thrombosis accounted for 31.22% of thrombosis drugs market size in 2025, driven by guideline-mandated anticoagulation post-orthopedic surgery. Pulmonary embolism is set to expand fastest at 8.12% CAGR, fueled by improved CT angiography diagnostics.

Adoption of Pulmonary Embolism Response Teams (PERTs) standardizes rapid treatment, while cancer-associated thrombosis gains visibility as survival rates rise. Stroke prevention in atrial-fibrillation patients remains a high-value application, especially with Factor XI safety data promising broader eligibility.

By Route of Administration: Oral prevalence with injectable resurgence

Oral therapies represented 66.55% of thrombosis drugs market size in 2025. Long-acting once-daily formulations reinforce adherence, particularly in outpatient atrial-fibrillation management.

Hospitals rely on LMWHs and unfractionated heparin for immediate onset and quick reversal. Pipeline assets such as weekly subcutaneous Factor XI inhibitors may offer an oral-free alternative that merges convenience with rapid titration, giving injectables renewed prominence within the thrombosis drugs market.

By Distribution Channel: Hospital lead amid digital expansion

Hospital pharmacies generated 46.15% of value in 2025, tied to acute care initiation. Retail outlets support chronic management, yet online pharmacies are advancing at 7.84% CAGR as telehealth normalizes digital prescriptions.

Direct-to-consumer discount programs bypass traditional benefit managers, and specialty pharmacies integrate adherence apps that transmit dosing data to clinicians. Such hybrid models are reshaping last-mile delivery economics in the thrombosis drugs market.

Geography Analysis

North America’s reimbursement systems and early DOAC adoption anchored 37.86% thrombosis drugs market share in 2025. Federal price negotiations aim to balance affordability with innovation, potentially widening drug access without hampering R&D investments.

Europe maintains harmonized clinical guidelines that speed incorporation of breakthrough agents; the region shows consistent mid-single-digit growth supported by aging demographics.

Asia-Pacific, projected at 7.97% CAGR, benefits from infrastructure upgrades and higher elective-surgery volumes. China’s tiered hospital reform and India’s Ayushman Bharat scheme expand insured cohorts, while Japan’s super-aged society sustains high per-capita anticoagulant use. Latin America and the Middle East & Africa trail but show rising awareness campaigns and imported generics that lower entry barriers, gradually enlarging their footprint in the thrombosis drugs market.

Competitive Landscape

Intellectual-property expiries are tilting power toward pipelines rather than current brands. Bristol Myers Squibb–Pfizer’s Eliquis alliance exemplifies a scale-economies approach, yet its 2028 exclusivity sunset drives the partners to explore next-wave targets. Bayer pivots toward cardiometabolic diversification after seeing Xarelto revenues slide on generic pressure.

Novartis’ acquisition of Anthos Therapeutics positions abelacimab as a flagship entrant into the Factor XI space, while Johnson & Johnson advances milvexian to Phase III in multiple indications. The field witnesses a rising prevalence of strategic collaborations pairing molecule innovation with digital risk-stratification platforms to deepen clinical stickiness.

Generic manufacturers Lupin and Taro capitalize on newly granted approvals, enabling payers to swap to lower-cost options rapidly. Market contenders therefore race to offer differentiated bleeding profiles or bundled care ecosystems, reaffirming that future competitiveness hinges on holistic thrombosis-management solutions rather than drug efficacy alone.

Thrombosis Drugs Industry Leaders

Boehringer Ingelheim GmbH

Johnson & Johnson

Sanofi SA

Pfizer Inc.

Laurus Lab (Aspen Pharmacare Holdings Limited)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Bristol Myers Squibb and Pfizer began direct-to-consumer Eliquis sales at 40% discount

- March 2025: FDA cleared first rivaroxaban generics from Lupin and Taro, triggering immediate price competition

Global Thrombosis Drugs Market Report Scope

As per the scope of the report, a thrombus is a blood clot that develops on the inside of the heart or on the walls of blood vessels as a result of the adhesion of blood platelets, proteins, and cells. Thrombosis is considered to be the major source of morbidity and mortality among elderly patients. It has been established that thrombosis is caused due to certain cardiovascular disorders as a result of old age or obesity.

The thrombosis drugs market is segmented by drug class, disease type, distribution channel, and geography. By drug class, the market is segmented as factor Xa Inhibitor, Heparin, P2Y12 Platelet Inhibitor, and other drug classes. By disease type, the market is segmented as pulmonary embolism, atrial fibrillation, deep vein thrombosis, and other disease types. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Direct Oral Anticoagulants (DOACs) |

| Heparin & Low-Molecular-Weight Heparin |

| Vitamin K Antagonists |

| Thrombolytics / Fibrinolytics |

| P2Y12 Platelet Inhibitors |

| Factor XI / XII Inhibitors (emerging) |

| Others |

| Deep Vein Thrombosis |

| Pulmonary Embolism |

| Atrial Fibrillation |

| Peripheral Arterial Disease |

| Stroke & Transient Ischemic Attack |

| Others |

| Oral |

| Injectable |

| Topical |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Mail-Order Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Drug Class (Value) | Direct Oral Anticoagulants (DOACs) | |

| Heparin & Low-Molecular-Weight Heparin | ||

| Vitamin K Antagonists | ||

| Thrombolytics / Fibrinolytics | ||

| P2Y12 Platelet Inhibitors | ||

| Factor XI / XII Inhibitors (emerging) | ||

| Others | ||

| By Disease Type (Value) | Deep Vein Thrombosis | |

| Pulmonary Embolism | ||

| Atrial Fibrillation | ||

| Peripheral Arterial Disease | ||

| Stroke & Transient Ischemic Attack | ||

| Others | ||

| By Route of Administration (Value) | Oral | |

| Injectable | ||

| Topical | ||

| By Distribution Channel (Value) | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Mail-Order Pharmacies | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the thrombosis drugs market?

The thrombosis drugs market size is USD 28.2 billion in 2026.

Which drug class leads the thrombosis drugs market?

Direct oral anticoagulants hold 54.62% market share, making them the leading class.

How fast will Factor XI inhibitors grow?

Factor XI inhibitors are forecast to post an 8.24% CAGR between 2026 and 2031.

Why is pulmonary embolism the fastest-growing disease segment?

Improved CT angiography diagnostics and widespread thromboprophylaxis protocols are accelerating treatment volumes.

Page last updated on: