Global Hodgkin Lymphoma Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

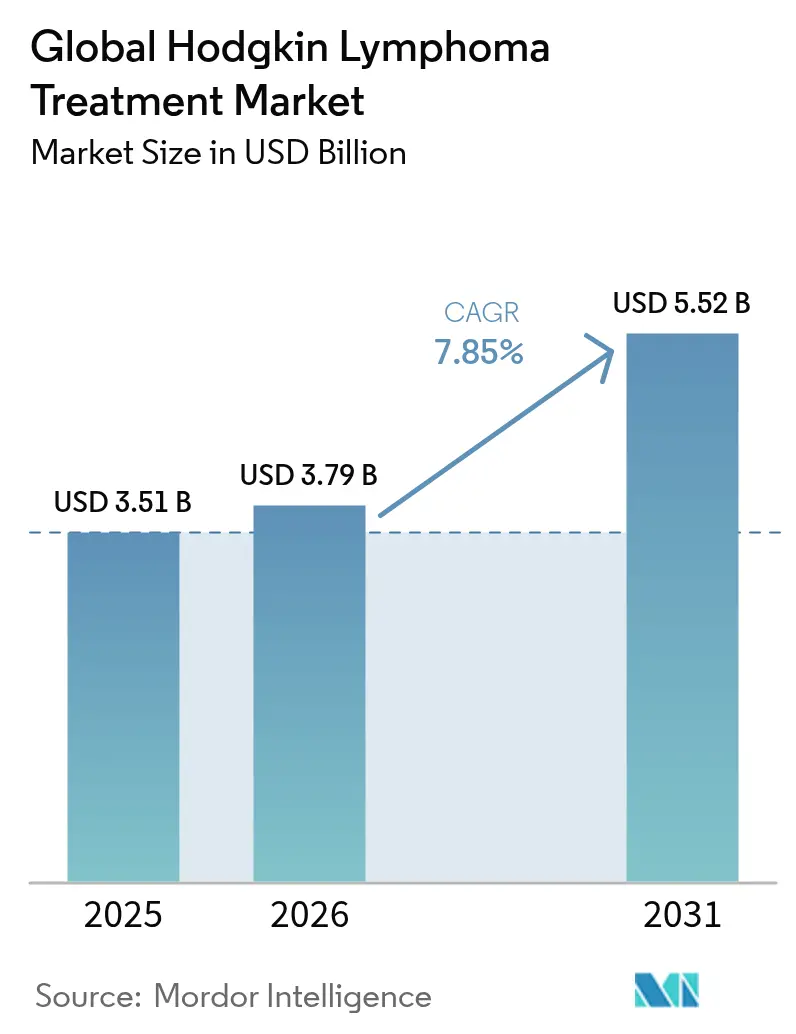

| Market Size (2026) | USD 3.79 Billion |

| Market Size (2031) | USD 5.52 Billion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Hodgkin Lymphoma Treatment Market Analysis by Mordor Intelligence

The Hodgkins lymphoma treatment market size was valued at USD 3.51 billion in 2025 and estimated to grow from USD 3.79 billion in 2026 to reach USD 5.52 billion by 2031, at a CAGR of 7.85% during the forecast period (2026-2031). This robust expansion mirrors the rapid uptake of checkpoint inhibitors, antibody–drug conjugates, and CAR-T therapies that together are redefining standard care across stages and geographies. The hodgkins lymphoma treatment market is also benefiting from precision diagnostics such as PET-adaptive protocols and liquid biopsy monitoring that improve disease stratification and support earlier intervention. Capacity additions worth USD 3.5 billion from global and Asian contract manufacturers are easing recent supply bottlenecks for ADC linker payloads, while 15 FDA approvals since early 2024 shorten launch cycles and broaden drug availability. Parallel regulatory incentives, notably breakthrough therapy and orphan-drug designations, are lowering evidence thresholds for conditional approvals and allowing companies to recoup R&D costs more swiftly, reinforcing the attractiveness of the Hodgkins lymphoma treatment market to both incumbents and new entrants.

Key Report Takeaways

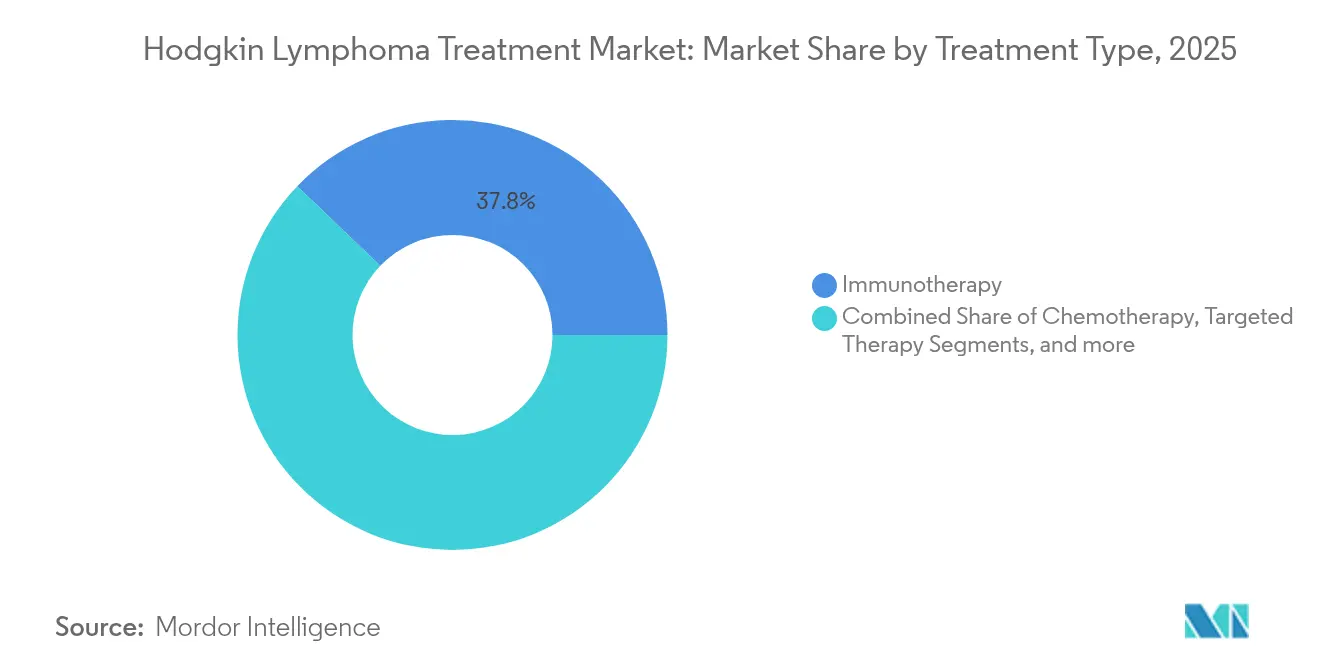

- By treatment type, immunotherapy held 37.84% of the Hodgkins lymphoma treatment market share in 2025; targeted therapy is poised to expand at an 8.47% CAGR to 2031.

- By stage of disease, advanced-stage (III–IV) disease accounted for 45.12% revenue share of the Hodgkins lymphoma treatment market size in 2025 and will post an 8.35% CAGR through 2031.

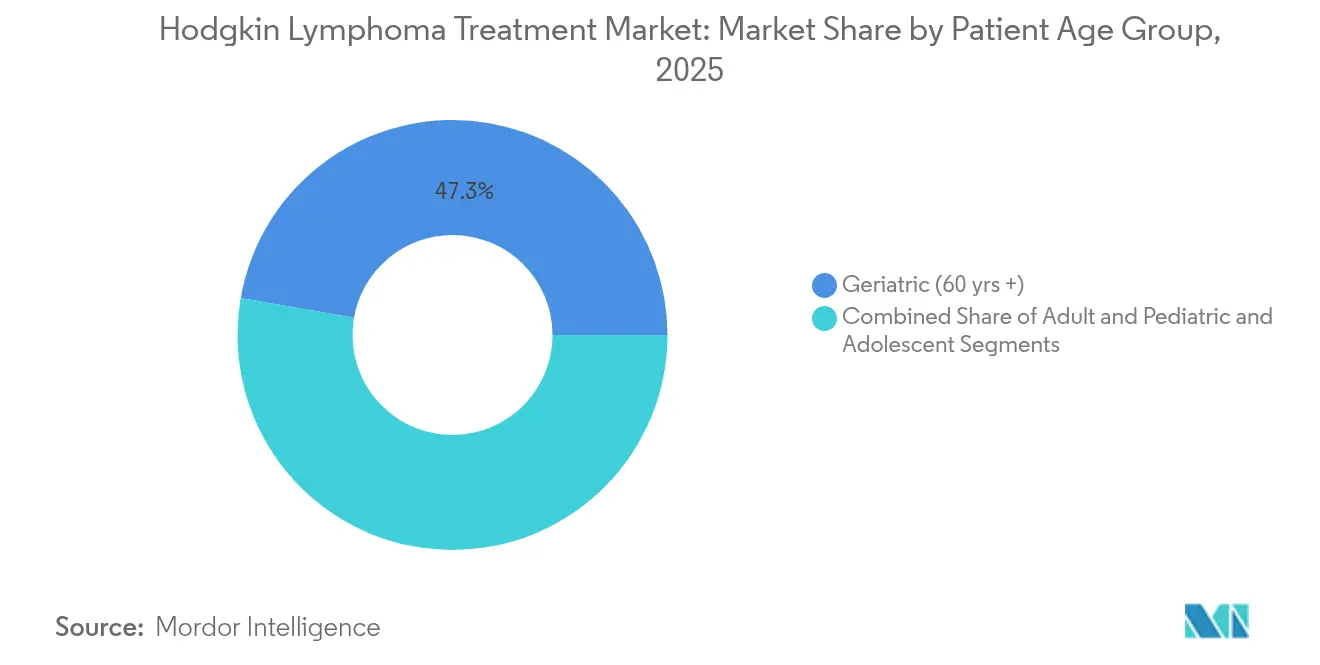

- By patient age group, the geriatric cohort (60+ years) captured 47.25% of the Hodgkins lymphoma treatment market share in 2025, while adults (20-59 years) register the fastest growth at 8.38% CAGR.

- By route of administration, intravenous delivery commanded 50.66% share of the Hodgkins lymphoma treatment market size in 2025 and continues to lead with an 8.22% CAGR.

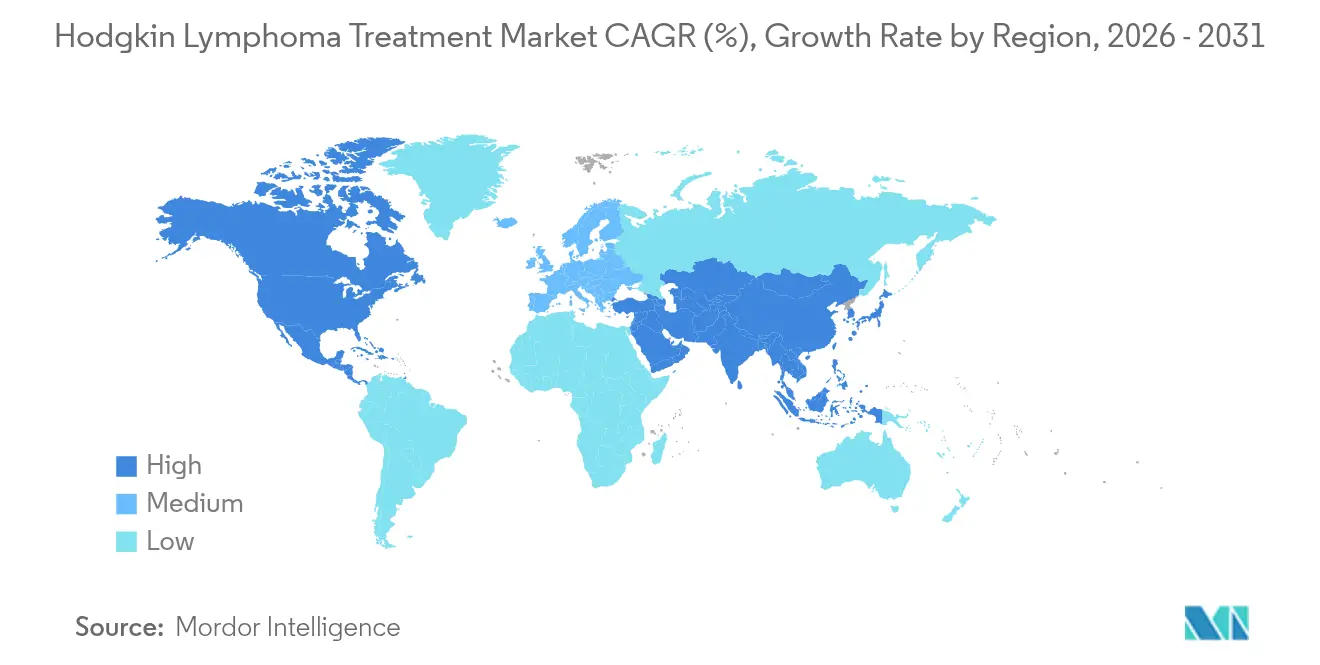

- By geography, North America contributed 39.88% revenue share in 2025; Asia-Pacific represents the fastest-growing region, accelerating at a 8.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hodgkin Lymphoma Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global disease burden & survivorship improvements | +1.8% | North America, Europe, expanding APAC urban centers | Long term (≥ 4 years) |

| Increasing public- and clinician-awareness initiatives | +1.2% | APAC core with spill-over to MEA and Latin America | Medium term (2-4 years) |

| PET-adaptive regimens accelerating adoption of novel drugs | +1.5% | North America and EU with penetration into urban APAC | Medium term (2-4 years) |

| Shift to fixed-dose subcutaneous checkpoint inhibitors | +1.4% | Early uptake in North America, Germany, UK | Short term (≤ 2 years) |

| Orphan-drug and accelerated-approval incentives | +1.1% | USA and EU regulatory frameworks | Short term (≤ 2 years) |

| AI-powered pathology and liquid biopsies | +0.9% | USA, EU, Japan and pilot programs in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Disease Burden & Survivorship Improvements

An expanding incidence curve, particularly in aging societies, is swelling the patient pool and generating recurring therapy demand as relapse rates hover between 30% and 40%. Five-year survival for early-stage disease now exceeds 90%, yet longer life spans mean many survivors require multiple lines of therapy over decades. Targeted agents and checkpoint inhibitors with favorable tolerability profiles are increasingly chosen for elderly patients unable to tolerate intensive chemotherapy. As a result, the Hodgkins lymphoma treatment market is gaining a demographic dividend that reinforces long-term revenue visibility.

PET-adaptive Regimens Accelerating Adoption of Novel Drugs

Interim PET scanning guides therapy intensification or de-escalation in real time, driving faster integration of novel agents. The Phase III S1826 study showed nivolumab-AVD achieving a 92% two-year progression-free survival versus 83% for brentuximab vedotin-AVD, reshaping frontline standards. PET-adaptive protocols support more precise drug selection, particularly favoring agents that elicit rapid metabolic responses. In parallel, AI-enhanced image analysis is lifting diagnostic accuracy and further accelerating uptake of precision regimens within the Hodgkins lymphoma treatment market.

Shift to Fixed-dose Subcutaneous Checkpoint Inhibitors Enabling Day-care Therapy

The December 2024 FDA approval of subcutaneous nivolumab (Opdivo Qvantig) validated non-inferior pharmacokinetics and fewer severe adverse events versus intravenous dosing. Day-care administration shortens chair time from hours to minutes and broadens access beyond tertiary centers, helping alleviate CAR-T capacity constraints. Subcutaneous formulations also eliminate weight-based calculations and substantially cut nursing time, adding a strong workflow efficiency incentive for oncology practices.

AI-powered Pathology & Liquid Biopsies Guiding Personalized Regimens

Machine-learning models now reach classification accuracies of up to 100% for Hodgkin lymphoma histology, while liquid biopsy sensitivity approaches 95% for circulating tumor DNA detection. Early molecular response signals enable dynamic treatment adjustments, which reduce unnecessary toxicity and direct high-cost drugs to patients most likely to benefit. Together, these tools advance the Hodgkins lymphoma treatment market toward fully personalized care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Treatment-related long-term toxicities | -1.8% | Global, highest concern in pediatric cohorts | Long term (≥ 4 years) |

| High total-care costs & reimbursement hurdles | -1.7% | Emerging markets, rural areas in high-income countries | Medium term (2-4 years) |

| ADC manufacturing bottlenecks & linker shortages | -1.3% | Global, pronounced in supply-dependent regions | Medium term (2-4 years) |

| Unequal PET or biomarker access | -1.1% | Low-income regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Treatment-related Long-term Toxicities

Secondary malignancies and cardiovascular events associated with legacy regimens constrain aggressive therapy use, especially in younger patients whose projected survival exceeds five decades. Checkpoint inhibitors introduce immune-related adverse events that often require prolonged immunosuppression, while CAR-T procedures carry neurotoxicity and cytokine-release risks. Such toxicities compel clinicians to weigh cure rates against quality-adjusted life years, tempering adoption in certain subgroups and moderating Hodgkins lymphoma treatment market growth.

High Total-care Costs & Reimbursement Hurdles

With CAR-T treatments exceeding USD 500,000 per patient, payers increasingly demand value-based contracts and real-world data, slowing broad reimbursement in cost-sensitive regions. Only 311 accredited CAR-T centers currently operate in the United States, illustrating the infrastructural and financial barriers that limit widespread uptake. Such economic frictions narrow access and dampen near-term revenue expansion until manufacturing scale efficiencies and financing models evolve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Immunotherapy Drives Frontline Adoption

Immunotherapy captured 37.84% of the Hodgkins lymphoma treatment market share in 2025 and remains the dominant modality thanks to checkpoint inhibitors that combine high response rates with favorable tolerability. Two-year progression-free survival of 92% for nivolumab-AVD positions immunotherapy as a backbone for future combination strategies. Chemotherapy still underpins many frontline regimens, but its growth rate trails targeted and cellular approaches. The hodgkins lymphoma treatment market size attributed to targeted therapy is set to expand at an 8.47% CAGR as ADCs such as brentuximab vedotin and next-generation CD30 conjugates penetrate earlier lines. Radiotherapy grows modestly as PET-adapted protocols trim field sizes, while autologous stem-cell rescue maintains a niche in highly refractory cases. Emerging CAR-T constructs (HSP-CAR30) attest to the expanding immunotherapy toolbox, delivering complete remission in 50% of heavily pre-treated patients.

A second wave of innovation is unfolding around subcutaneous and fixed-dose formulations that slash chair time and improve patient convenience. The hodgkins lymphoma treatment market is therefore likely to see increasing regimen diversity, with optimized combinations tailored to genetic markers, age cohorts, and toxicity tolerances. Real-world evidence will play a growing role in refining sequencing decisions as payers seek clear survival and quality-of-life gains before approving high list-price drugs.

By Stage of Disease: Advanced Cases Propel Revenue Growth

Advanced-stage disease held 45.12% of the hodgkins lymphoma treatment market size in 2025 and is forecast to grow at 8.35% CAGR, capturing a rising share as novel modalities address complex tumor biology. Advanced cases often require multi-agent regimens that command premium pricing, bolstering topline growth for manufacturers. Early-stage disease benefits from de-escalation initiatives that strive to minimize late toxicities without sacrificing cure rates, thereby marginally tempering revenue potential. Relapsed or refractory presentations continue to generate disproportionate value as patients cycle through successive lines of increasingly specialized therapy, each with higher per-treatment costs.

Stage-specific personalization gains momentum with PET-guided escalation and circulating tumor DNA surveillance. These technologies help clinicians pinpoint residual disease early, facilitating timely switches to next-line agents and improving overall outcomes. Consequently, the hodgkins lymphoma treatment market sees steady demand across disease stages, though advanced cases remain the primary engine of absolute dollar growth.

By Patient Age Group: Adults Drive Incremental Volume, Geriatrics Dominate Value

Geriatric patients (60+ years) represent 47.25% of the hodgkins lymphoma treatment market share in 2025, reflecting demographic aging and improved diagnostic reach. Yet adults aged 20-59 produce the fastest incremental growth at 8.38% CAGR, aided by earlier detection programs and survivorship gains that prolong treatment horizons. Pediatric and adolescent segments stay clinically significant but commercially modest due to smaller cohorts and dose adjustments that reduce drug volumes.

Age-tailored regimens are becoming standard practice. Elderly patients often receive checkpoint inhibitors or targeted agents with lower toxicity burdens, whereas younger adults may tolerate combination chemotherapy plus immunotherapy, leading to higher cure probabilities. The growing adult survivor base will continue to demand chronic monitoring and potential retreatment, reinforcing the hodgkins lymphoma treatment market’s long-run revenue visibility.

By Route of Administration: Intravenous Retains Core Position, Subcutaneous Ascends

Intravenous delivery accounted for 50.66% of the hodgkins lymphoma treatment market share in 2025 and still leads growth at 8.22% CAGR due to ingrained clinical workflows and the need for controlled infusion of combination regimens. The December 2024 launch of subcutaneous nivolumab introduces meaningful disruption by enabling outpatient efficiency gains and reducing infusion-center bottlenecks. Oral formulations are gaining role for maintenance therapy, whereas emerging on-body injector platforms promise additional convenience.

The competitive edge now tilts toward manufacturers that can migrate high-volume antibodies to fixed-dose subcutaneous formats without efficacy sacrifice. Such convenience-maximizing shifts improve adherence and broaden geographic reach, especially in rural regions lacking infusion infrastructure. The hodgkins lymphoma treatment market therefore balances entrenched intravenous protocols with an accelerating pivot toward patient-centric delivery systems.

Geography Analysis

North America generated 39.88% of total revenue in 2025, powered by 311 accredited CAR-T centers, rapid regulatory approvals, and premium reimbursement frameworks that absorb high list prices. Breakthrough designations such as the 2025 status for pembrolizumab streamline U.S. launch timelines and reinforce the region’s early-adopter profile. Nevertheless, capacity constraints at high-volume centers and payer scrutiny over budget impact are nudging stakeholders toward subcutaneous and community-based care models, gradually decentralizing the North American delivery landscape.

Asia-Pacific is the fastest-growing region, expanding at 8.62% CAGR through 2031 on the back of rising disease incidence, local manufacturing hubs, and government-sponsored oncology programs. China’s projected incidence of 5.57 per 100,000 by 2035 underscores the region’s long-term demand pool. Biosimilar uptake and cross-border clinical collaborations allow earlier access to innovation while containing costs. Manufacturing expansions by WuXi Biologics and Samsung Biologics shift global supply chains eastward, giving local markets preferential access to fresh ADC capacity.

Europe maintains steady growth, helped by EMA conditional approvals such as odronextamab in August 2024. Cross-border treatment protocols improve care continuity across member states, yet market uptake still hinges on country-level health technology assessments that weigh clinical value against fiscal restraint. Latin America and the Middle East/Africa show emerging momentum, supported by medical tourism and public-private partnerships, though lingering reimbursement and diagnostic-access hurdles keep adoption levels below global averages.

Competitive Landscape

The hodgkins lymphoma treatment market is moderately consolidated. Bristol Myers Squibb leverages its nivolumab franchise, posting 92% two-year PFS in the pivotal S1826 trial and setting a high efficacy benchmark[2]Davy James, “Opdivo Combination Shows Superior Survival, Fewer Adverse Effects in Advanced Hodgkin Lymphoma,” Applied Clinical Trials, appliedclinicaltrialsonline.com. Pfizer’s USD 43 billion purchase of Seagen secures leading ADC technology, notably Adcetris, and bolsters pipeline depth PharmaShots. AstraZeneca and Daiichi Sankyo are committing USD 1.5 billion and USD 1 billion respectively to new ADC facilities, signaling a race to overcome longstanding linker-payload shortages.

Smaller biotechs such as the Sant Pau Research Institute demonstrate disruptive potential with CD30-directed CAR-T constructs achieving complete remission in refractory cases[3]News-Medical, “First-in-Human CD30 CAR-T Data from Sant Pau Research Institute,” news-medical.net. Diagnostic innovators are equally active: AI pathology start-ups and liquid biopsy platform owners partner with pharmaceutical companies to embed companion diagnostics into trial designs. As a result, technology convergence—rather than molecule exclusivity—defines the next competitive frontier, rewarding firms that integrate therapeutics with data-enabled care pathways.

Global Hodgkin Lymphoma Treatment Industry Leaders

Bristol-Myers Squibb Company

Merck & Co. Inc.

Biogen Inc.

Amneal Pharmaceuticals, Inc.

Seagen Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BioInvent received FDA Orphan Drug Designation for BI-1808, an anti-TNFR2 antibody showing partial responses in refractory T-cell lymphoma patients.

- March 2025: Merck secured Breakthrough Therapy Designation for KEYTRUDA in classical Hodgkin lymphoma, accelerating review timelines.

- March 2025: Legend Biotech announced plans to double Carvykti manufacturing capacity, launching additional production in New Jersey to mitigate CAR-T shortages.

- December 2024: The FDA approved subcutaneous nivolumab (Opdivo Qvantig), the first PD-1 inhibitor delivered via fixed-dose injection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Hodgkin's lymphoma treatment market as all prescription therapeutics, including chemotherapy regimens, radiotherapy plans billed as packaged drugs, targeted antibodies, checkpoint inhibitors, ADCs, CAR-T products, and autologous or allogeneic stem-cell transplants, administered to manage classical or nodular lymphocyte-predominant Hodgkin's lymphoma across all patient ages and geographies. We, therefore, size only manufacturer ex-factory drug revenues and modeled therapy package costs that are traceable to product labels.

Scope exclusion: Diagnostic test kits, inpatient procedure charges, and all Non-Hodgkin's lymphoma therapies fall outside this assessment.

Segmentation Overview

- By Treatment Type

- Chemotherapy

- Radiotherapy

- Targeted Therapy

- Immunotherapy

- Stem-Cell Transplant

- By Stage of Disease

- Early Stage (I–II)

- Advanced Stage (III–IV)

- Relapsed / Refractory

- By Patient Age Group

- Pediatric & Adolescent (0-19 yrs)

- Adult (20-59 yrs)

- Geriatric (60 yrs +)

- By Route of Administration

- Intravenous

- Oral

- Subcutaneous

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with oncologists, hematology pharmacists, payor advisors, and life-science procurement leads across North America, Europe, and fast-growing Asia-Pacific helped us test treatment pathways, dose intensities, and real-world adherence. Surveys with patient-advocacy coordinators further fine-tuned regional reimbursement and access adjustments that our desk work could not fully catch.

Desk Research

Mordor analysts first compile incidence and prevalence curves from widely quoted public datasets such as WHO-IARC GLOBOCAN, CDC SEER, Eurostat cancer registry, and country-level health ministry dashboards, which anchor our epidemiology pool. Next, regulatory disclosures from the US FDA, EMA, and PMDA, alongside trial registries (ClinicalTrials.gov, EU-CTR), give clarity on approved lines and pipeline read-outs that influence uptake timings.

We supplement this base with company 10-Ks, investor decks, peer-reviewed journals like Blood and The Lancet Oncology, and industry association white papers. Paid repositories, such as D&B Hoovers for therapy revenue splits, Dow Jones Factiva for launch newsflow, and Questel for patent velocity, add commercial color. The list above is illustrative; many additional open and subscription sources were reviewed to verify numbers and wording assumptions.

Market-Sizing & Forecasting

A prevalence-to-treated-cohort top-down model converts incident cases into first-, second-, and third-line therapy volumes, multiplied by region-specific average selling prices. Supplier roll-ups on the five largest drug classes act as a bottom-up sense-check before final balances are locked. Key variables include stage-wise treatment rates, label-extension timelines, checkpoint-inhibitor price erosion curves, stem-cell transplant eligibility ratios, and emerging CAR-T penetration. Multivariate regression with scenario analysis projects each driver through 2030, while missing hospital-discount data are gap-filled using conservative midpoint estimates vetted with our expert panel.

Data Validation & Update Cycle

Outputs move through variance scans against historical spend, cross-regional ASP parity, and anomaly triggers. Senior reviewers sign off once swings stay within predefined bands. Our numbers refresh annually, yet interim updates are issued when a material market event, such as an early FDA approval, occurs. A final pass is performed just before release so clients receive our latest view.

Why Mordor's Hodgkin Lymphoma Treatment Baseline Commands Trust

Published figures rarely match because firms diverge on scope, data cadence, and model levers. We anchor on strictly HL-only drug revenues and refresh our epidemiology every twelve months, thereby avoiding inflation from unrelated services or non-HL regimens.

Key gap drivers include whether supportive-care spend is bundled, how off-invoice rebates are handled, the breadth of country coverage, and the speed at which new checkpoint inhibitors are layered in. Mordor's disciplined variable tracking and annual refresh cadence correct these skews before totals are shared.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.51 B (2025) | Mordor Intelligence | - |

| USD 8.98 B (2023) | Regional Consultancy A | Combines diagnostics and pediatric charity funding; two-year refresh lag |

| USD 1.60 B (2024) | Industry Journal B | Omits transplants and latest PD-1 drugs; covers only nine nations |

| USD 5.00 B (2025) | Data Aggregator C | Prevalence × average spend proxy, no primary validation, limited segment splits |

The comparison shows that once differing inclusions and outdated inputs are stripped away, Mordor provides a balanced, transparent baseline grounded in clear variables and repeatable steps, allowing decision-makers to move forward with confidence.

Key Questions Answered in the Report

What is the current value of the Hodgkins lymphoma treatment market?

The hodgkins lymphoma treatment market size stood at USD 3.79 billion in 2026 and is forecast to reach USD 5.52 billion by 2031.

Which therapy type holds the largest market share?

Immunotherapy leads with 37.84% of the hodgkins lymphoma treatment market share in 2025, driven by checkpoint inhibitors such as nivolumab-AVD.

Which region will grow the fastest through 2031?

Asia-Pacific shows the highest momentum, expanding at a 8.62% CAGR thanks to rising incidence, local manufacturing capacity, and biosimilar uptake.

Why are subcutaneous formulations important?

Fixed-dose subcutaneous checkpoint inhibitors shorten administration time to minutes, cut infusion center costs, and broaden rural patient access while maintaining efficacy.

How do PET-adaptive regimens influence treatment decisions?

Interim PET scans guide real-time therapy adjustment, allowing physicians to escalate or de-escalate treatment based on metabolic response, which improves outcomes and limits unnecessary toxicity.

What manufacturing trends are shaping supply security?

Over USD 3.5 billion in new ADC capacity from AstraZeneca, Daiichi Sankyo, and Asian CDMOs is easing payload-linker shortages, ensuring steadier drug availability as demand rises.

Page last updated on: