Myelodysplastic Syndrome (MDS) Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

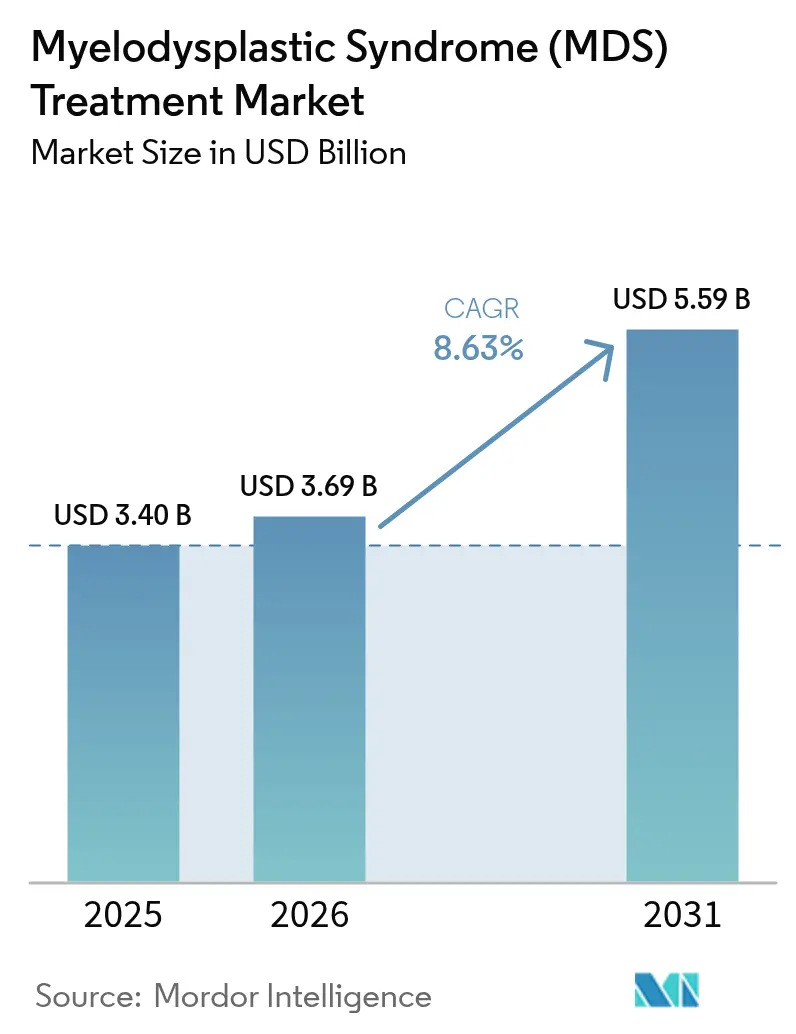

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 5.59 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Myelodysplastic Syndrome (MDS) Treatment Market Analysis by Mordor Intelligence

The Myelodysplastic syndrome treatment market size is expected to grow from USD 3.4 billion in 2025 to USD 3.69 billion in 2026 and is forecast to reach USD 5.59 billion by 2031 at 8.63% CAGR over 2026-2031. Rapid regulatory approvals of breakthrough drugs such as imetelstat and treosulfan-fludarabine are shortening development timelines and widening patient access. Precision oncology, expanding geriatric populations, and hospital-led molecular triage programs are converging to lift treatment volumes, while strong venture funding is accelerating gene-edited transplant platforms. Asia Pacific, supported by sustained healthcare capital expenditure and rising diagnostic rates, is the fastest-growing region. Headwinds include cytopenia-linked toxicity that curtails adherence and escalating cost-effectiveness scrutiny in public payor systems, yet AI-driven prognostic tools are improving dose individualization and preserving drug margins.

Key Report Takeaways

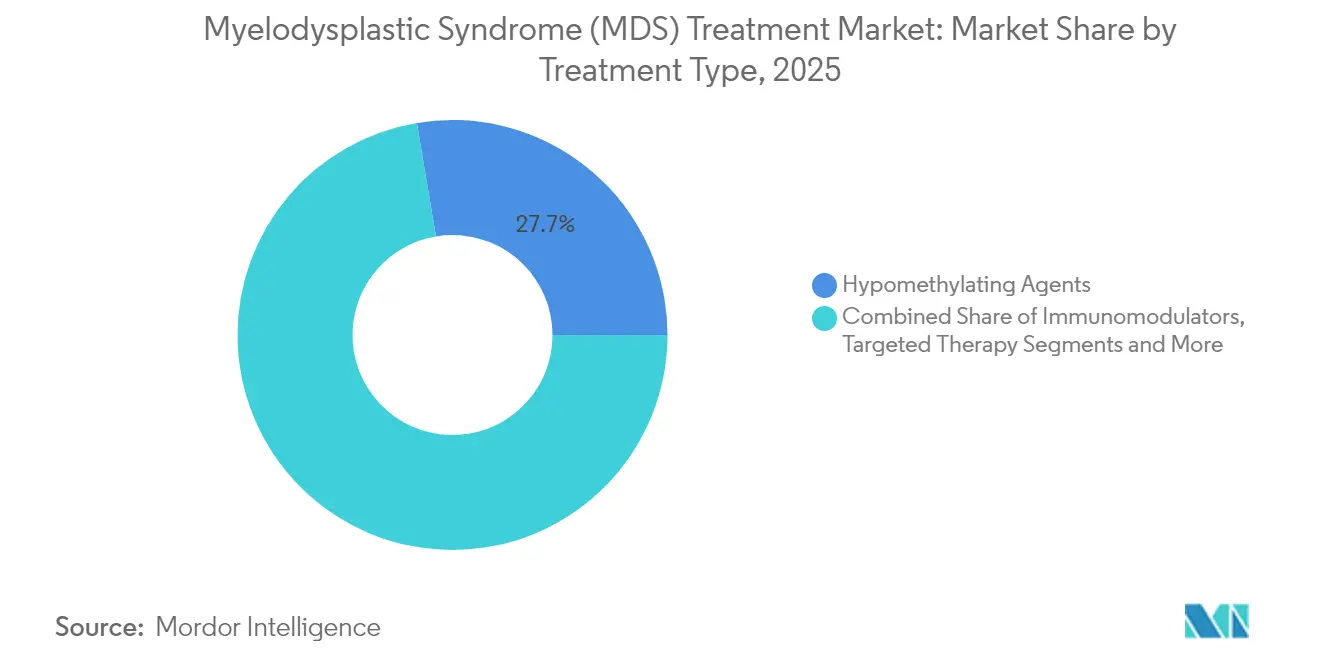

- By treatment type, hypomethylating agents led with 27.65% of the Myelodysplastic syndrome treatment market share in 2025, while targeted therapy is expanding at a 11.72% CAGR through 2031.

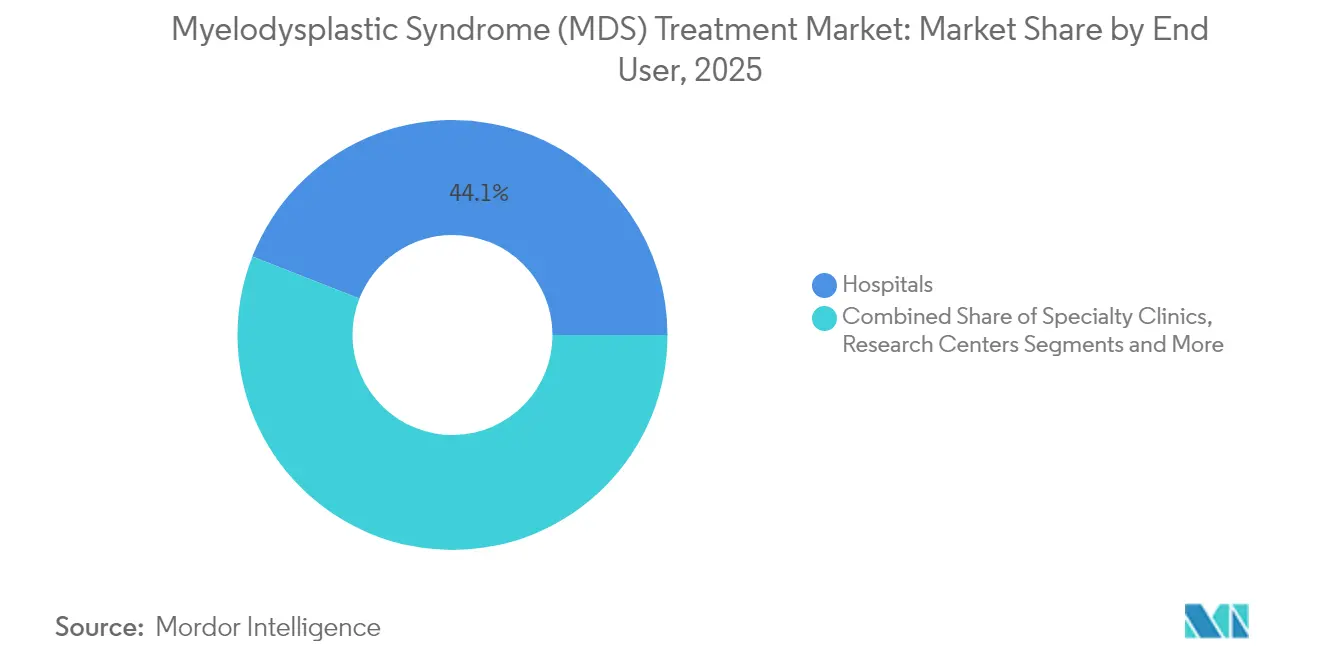

- By end user, hospitals held a 44.05% share of the Myelodysplastic syndrome treatment market in 2025, and online pharmacies are advancing at an 11.05% CAGR to 2031.

- By geography, North America commanded 38.95% share of the Myelodysplastic syndrome treatment market in 2025; Asia Pacific is projected to rise at a 10.21% CAGR during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Myelodysplastic Syndrome (MDS) Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D spending on next-generation hypomethylating and combination regimens | +2.10% | North America, Europe | Medium term (2-4 years) |

| Accelerated FDA/EMA breakthrough & orphan designations | +1.80% | North America, European Union | Short term (≤ 2 years) |

| Ageing population-linked incidence surge | +1.40% | China, Western Europe, Japan | Long term (≥ 4 years) |

| Hospital-initiated molecular triage programs | +1.20% | North America, selective APAC markets | Medium term (2-4 years) |

| Venture-capital funding for ex-vivo gene-edited HSCT | +0.90% | Global, led by North America | Long term (≥ 4 years) |

| AI-driven prognostic scoring tools | +0.70% | North America, European Union | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High R&D Spending on Next-Generation Hypomethylating and Combination Regimens

Capital allocation into multi-agent regimens is accelerating after luspatercept delivered 58.5% transfusion independence versus 31.2% for epoetin alfa in the COMMANDS trial.[1]Bristol Myers Squibb, “COMMANDS Phase III Results,” bms.com Novartis is running a Phase III evaluation of MBG453 plus azacitidine, and Takeda licensed elritercept (TAK-226) to broaden its anemia pipeline. These programs target distinct mutational profiles, boosting response durability and underpinning the medium-term uplift in the Myelodysplastic syndrome treatment market.

Accelerated FDA/EMA Breakthrough & Orphan Designations

Fast-track pathways are compressing time-to-market. The FDA granted orphan designation to bexmarilimab in March 2025, while the EMA issued a positive CHMP opinion for imetelstat in December 2024 ahead of a March 2025 clearance.[2]European Medicines Agency, “CHMP Positive Opinion for Imetelstat,” ema.europa.eu Such regulatory alignment is drawing biotechnology capital and accelerating global launches.

Ageing Population-Linked Incidence Surge

Median diagnosis ages of 67 years in Western countries and 52 years in Chinese cohorts highlight pressing demand for expansion.[3]Li Zhang, “Clinical Features of Myelodysplastic Syndromes in Chinese Patients,” Chinese Medical Journal, cmj.org.cn Japanese incidence reached 1.6 per 100,000 men, increasing steadily with population aging. Demographic pressure is steering developers to design low-toxicity regimens appropriate for frail patients.

Hospital-initiated molecular triage programs

Routine next-generation sequencing now precedes overt cytopenia in many U.S. and EU centers, allowing earlier, lower-dose intervention. TP53 mutation status predicts superior decitabine response and guides regimen intensity. Hospitals are pairing sequencing with AI blood-test algorithms that raise diagnostic accuracy, reinforcing demand for precision drugs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Cytopenia-Related Adverse Events Limiting Drug Adherence | -1.60% | Global, particularly acute in elderly populations | Short term (≤ 2 years) |

| High Total-Care Cost Versus QALY Thresholds In Public Payor Systems | -1.30% | Europe, Canada, emerging markets with public healthcare | Medium term (2-4 years) |

| Donor-Matching Bottlenecks For Allogeneic HSCT In Emerging Markets | -1.00% | Asia Pacific, Middle East & Africa, South America | Long term (≥ 4 years) |

| Limited Predictive Biomarkers For HMA-Refractory Patients | -0.80% | Global, with research concentration in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Cytopenia-Related Adverse Events Limiting Drug Adherence

Thrombocytopenia and neutropenia required dose modifications in 40% of imetelstat recipients in pivotal trials. Similar issues arise with hypomethylating agents, leading to premature discontinuation that blunts therapeutic benefit. Developers are engineering antibody-drug conjugates and selective inhibitors with narrower marrow impact to offset this short-term drag on the Myelodysplastic syndrome treatment market.

High Total-Care Cost Versus QALY Thresholds In Public Payor Systems

Oral precision drugs often exceed established cost-effectiveness thresholds, driving strict reimbursement filters, particularly in Western Europe. Health technology bodies are requesting real-world outcomes evidence before broad coverage, slowing uptake in price-sensitive markets and dampening the medium-term contribution of premium therapies to the Myelodysplastic syndrome treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Targeted Therapy Accelerates Growth

Targeted therapy posted the fastest 11.72% CAGR to 2031, reshaping the competitive field even though hypomethylating agents still accounted for 27.65% of the Myelodysplastic syndrome treatment market share in 2025. The approval of imetelstat, the first telomerase inhibitor, validates mechanism-specific development. Venetoclax-based combinations reached 96% overall response, underscoring the clinical upside of biomarker-matched regimens.

Expanding molecular diagnostics that stratify patients by TP53, SF3B1, and IDH mutations are reinforcing demand for targeted agents and guiding drug choice. Although chemotherapeutic conditioning remains vital for HSCT candidates, oral high-selectivity compounds are gaining frontline positioning in lower-risk cohorts. Premium pricing is counterbalanced by improved transfusion independence, lowering supportive-care costs, and lifting the segment’s contribution to the Myelodysplastic syndrome treatment market size over the forecast horizon.

By End User: Homecare Reshapes Delivery Models

Hospitals retained a 44.05% revenue share in 2025, reflecting their central role in transfusion services and HSCT. Yet homecare and online pharmacies are registering an 11.05% CAGR due to oral hypomethylating therapies such as INQOVI, which eliminate infusion center visits.

Medicare’s 2025 home health payment update and broad telehealth reimbursement have catalyzed remote monitoring adoption. Tablets with adherence-tracking sensors and AI-driven toxicity alerts ensure safety outside acute settings, improving patient quality of life while reducing total care expenditure. Thus, they deepen the penetration of ambulatory channels within the Myelodysplastic syndrome treatment market.

Geography Analysis

North America led with a 38.95% share of the Myelodysplastic syndrome treatment market in 2025, owing to robust clinical-trial infrastructure, swift FDA pathways, and favorable reimbursement. Early uptake of imetelstat, luspatercept, and treosulfan-fludarabine illustrates the region’s appetite for innovation. Europe follows, supported by universal healthcare and EMA alignment. Germany, France, and the United Kingdom quickly incorporated telomerase inhibition after the March 2025 approval, while cost-containment forces are steering payors toward oral agents with lower administration overheads.

Asia Pacific is the fastest-growing sub-region at 10.21% CAGR through 2031. China’s younger median diagnosis age and distinct cytogenetics are driving domestic research and localized guidelines. Japan’s aging population and sophisticated insurance coverage foster high drug adoption, whereas India’s widening middle class and medical-tourism hubs are improving therapy access. Regulatory harmonization projects, such as ASEAN CTPP, are set to streamline approvals, providing further upside for the Myelodysplastic syndrome treatment market.

Emerging regions face infrastructure gaps. However, the United Arab Emirates opened a comprehensive HSCT center at Burjeel Medical City in 2024, and Egypt’s transplant program surpassed 4,000 cumulative procedures, signaling capacity upgrades that will gradually expand the addressable patient pool.

Competitive Landscape

The Myelodysplastic syndrome treatment market remains moderately concentrated. Bristol Myers Squibb leveraged the Celgene acquisition to dominate anemia management with luspatercept, while also advancing venetoclax combinations under investigational protocols. Geron commercialized imetelstat across the United States and Europe in under nine months, underscoring execution speed.

Rigel, Takeda, and Novartis are competing on novel targets including IRAK1/4 and TIM-3, often via co-development agreements that distribute risk. Takeda’s license of elritercept from Keros exemplifies pipeline expansion through external innovation. Gene-editing entrants, backed by venture funds, are pursuing curative ex vivo transplantation solutions, though manufacturing complexity poses entry barriers.

Market incumbents rely on scale efficiencies in manufacturing, pharmacovigilance, and global supply to defend share. Yet, the rise of AI-enabled patient stratification platforms lowers the threshold for niche biotech challengers that can identify underserved molecular subsets. The competitive narrative is therefore characterized by strategic alliances, lifecycle management of first-in-class assets, and a measured expansion into outpatient-friendly formulations to capture demand in the rapidly evolving Myelodysplastic syndrome treatment market.

Myelodysplastic Syndrome (MDS) Treatment Industry Leaders

Takeda Pharmaceutical Company Limited

Bristol-Myers Squibb

LUPIN

Accord Healthcare

Otsuka America Pharmaceutical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: European Commission granted marketing authorization for imetelstat (Rytelo) for transfusion-dependent lower-risk MDS.

- January 2025: FDA approved treosulfan-fludarabine conditioning for allogeneic HSCT in AML/MDS.

- January 2025: Rigel received orphan designation for R289 in relapsed/refractory MDS

- December 2024: Takeda licensed elritercept (TAK-226) for MDS-associated anemia from Keros Therapeutics.

- November 2024: FDA cleared Revumenib for KMT2A-rearranged acute leukemia, broadening the targeted therapy precedent.

Global Myelodysplastic Syndrome (MDS) Treatment Market Report Scope

As per the scope of the report, myelodysplastic syndrome (MDS) is a group of diverse bone marrow disorders in which the bone marrow does not produce enough healthy blood cells. MDS is often referred to as a "bone marrow failure disorder." These disorders are characterized by ineffective hematopoiesis, including abnormalities in proliferation, differentiation, and apoptosis. The Myelodysplastic Syndrome (MDS) Treatment Market is segmented by Treatment Type (Chemotherapy, Immune Treatments, Stem Cell Transplant, Other Treatment Types), End-User (Hospitals, Specialty Clinics, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (USD million) for the above segments.

| Chemotherapy |

| Hypomethylating Agents |

| Immunomodulators |

| Targeted Therapy |

| Other Treatment Types |

| Hospitals |

| Specialty Clinics |

| Academic & Research Centers |

| Homecare & Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Chemotherapy | |

| Hypomethylating Agents | ||

| Immunomodulators | ||

| Targeted Therapy | ||

| Other Treatment Types | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Academic & Research Centers | ||

| Homecare & Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Myelodysplastic syndrome treatment market?

The market stood at USD 3.69 billion in 2026 and is projected to reach USD 5.59 billion by 2031.

Which treatment class is growing fastest?

Targeted therapy is expanding at a 11.72% CAGR, driven by telomerase inhibition and novel combination regimens.

Which region is expected to post the highest growth?

Asia Pacific is forecast to rise at a 10.21% CAGR thanks to healthcare modernization and broadened access to advanced drugs.

Why are homecare channels gaining traction?

Oral hypomethylating agents such as INQOVI allow outpatient administration, and updated Medicare reimbursement supports home-based care.

What are the main barriers to market growth?

Cytopenia-related toxicities that limit adherence and high therapy costs that challenge public payor cost-effectiveness thresholds.

How concentrated is the competitive landscape?

The top five companies control roughly 60% of revenues, reflecting moderate concentration with room for biotech disruptors.

Page last updated on: