Lymphedema Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

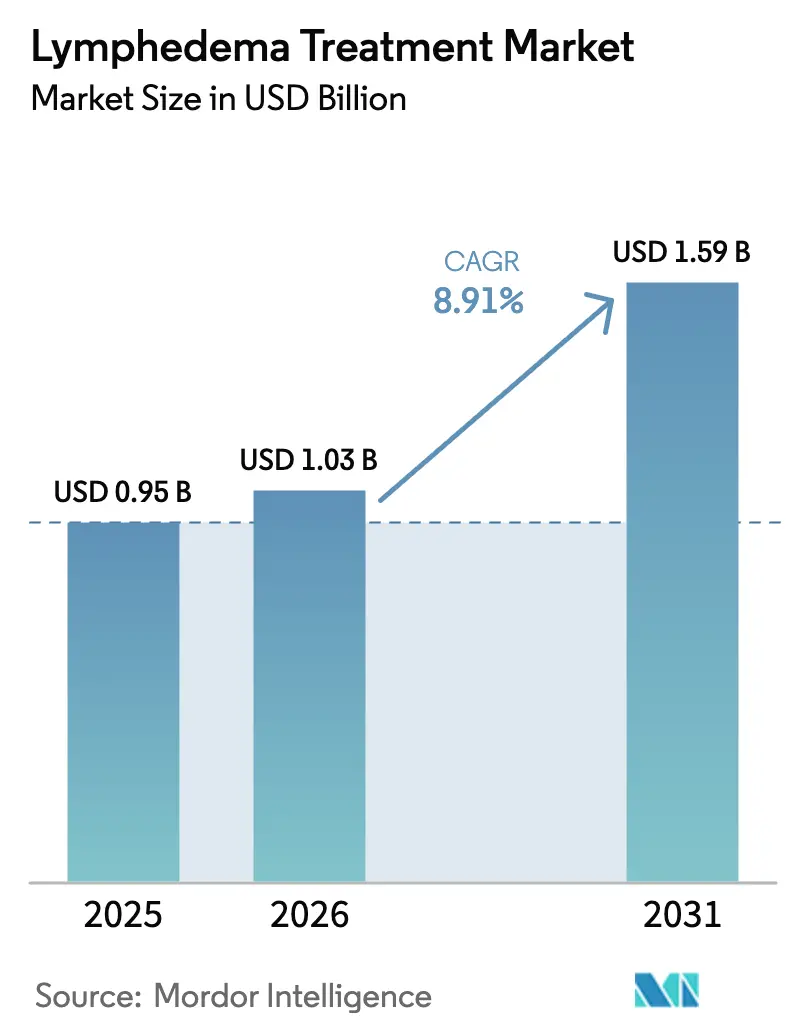

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 8.91% CAGR |

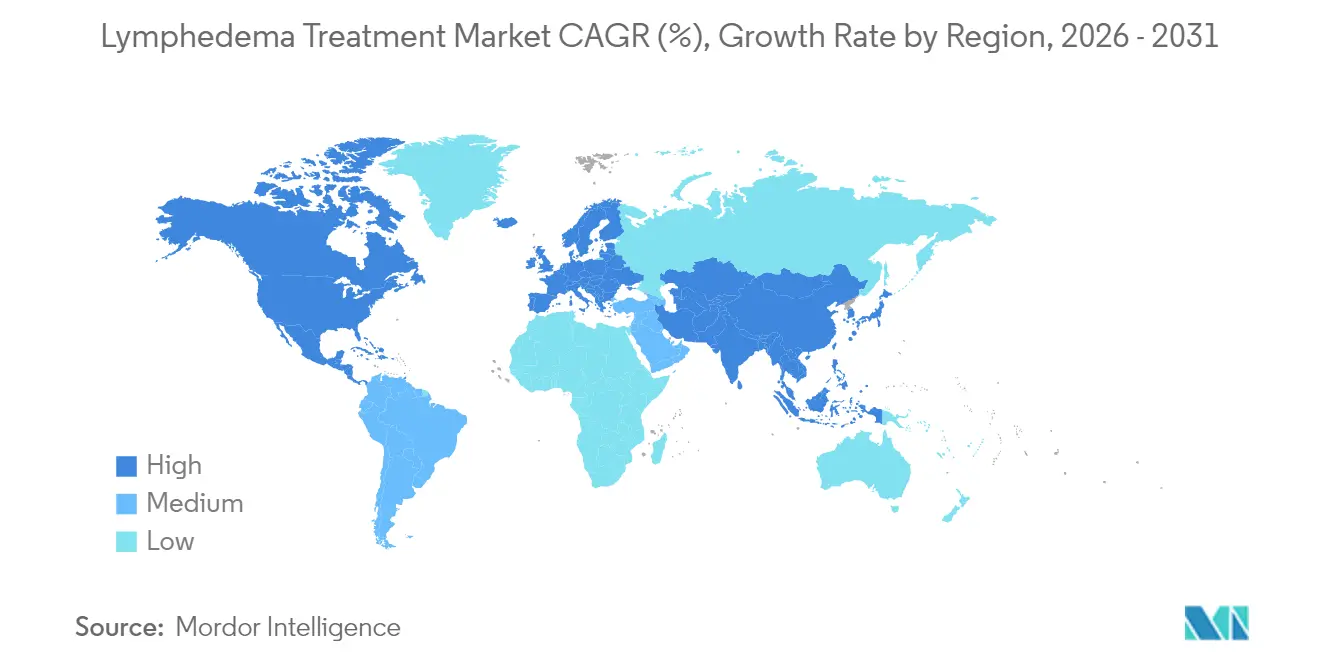

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lymphedema Treatment Market Analysis by Mordor Intelligence

The lymphedema treatment market size is expected to grow from USD 0.95 billion in 2025 to USD 1.03 billion in 2026 and is forecast to reach USD 1.59 billion by 2031 at 8.91% CAGR over 2026-2031. Strong growth springs from three reinforcing forces: expanding cancer survivorship, rapid device innovation rooted in digital health, and a reimbursement environment that now classifies compression garments as medically necessary. Medicare’s 2024 policy shift, in particular, has moved thousands of U.S. patients from self-pay to covered status, unlocking pent-up demand and encouraging providers to standardize therapy protocols. Meanwhile, early-detection technologies and minimally invasive microsurgery are edging treatment toward proactive disease modification rather than late-stage symptom control. Competitive pressure has intensified as start-ups integrate IoT sensors into lighter pneumatic pumps while pharmaceutical innovators test lymphangiogenic drug candidates. These converging trends point to a 54% cumulative value expansion through 2030 and underline the sizeable unmet need still characterizing chronic lymphedema care.

Key Report Takeaways

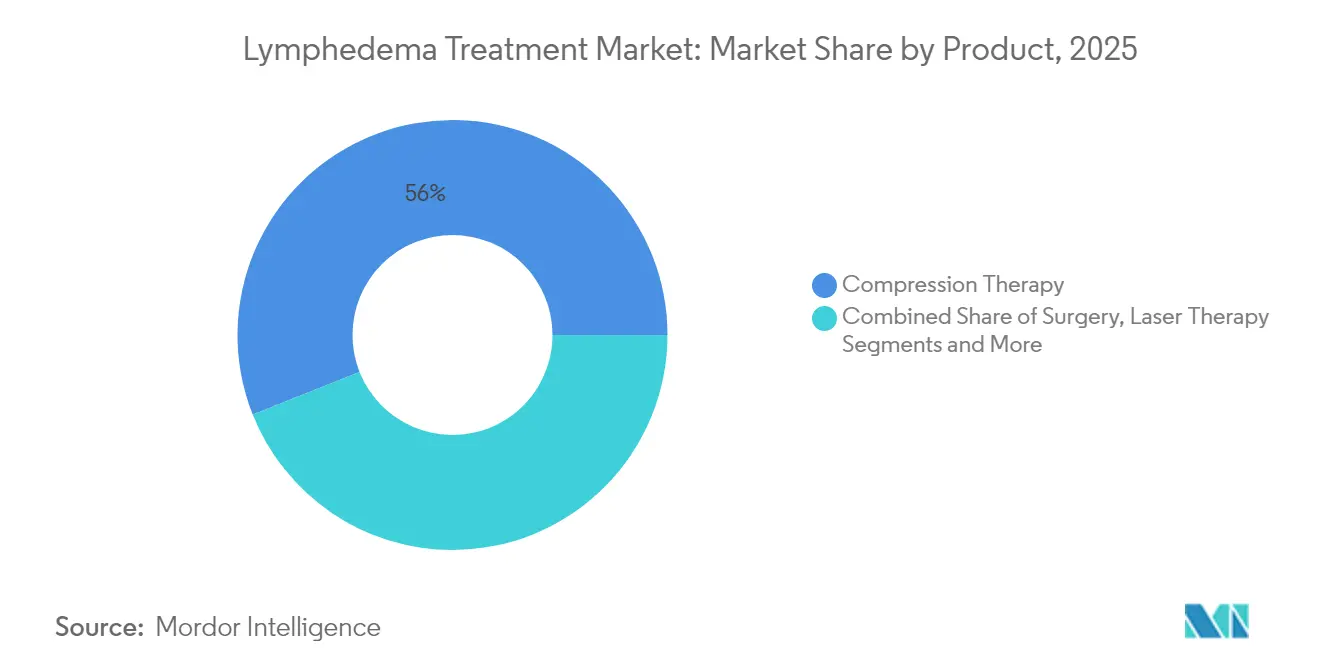

- By treatment type, compression therapy retained 56.02% of the lymphedema treatment market share in 2025, while pharmacologic therapy is projected to expand at a 9.25% CAGR through 2031.

- By type, secondary lymphedema accounted for 81.05% of cases in 2025; primary lymphedema is forecast to register a 8.95% CAGR to 2031.

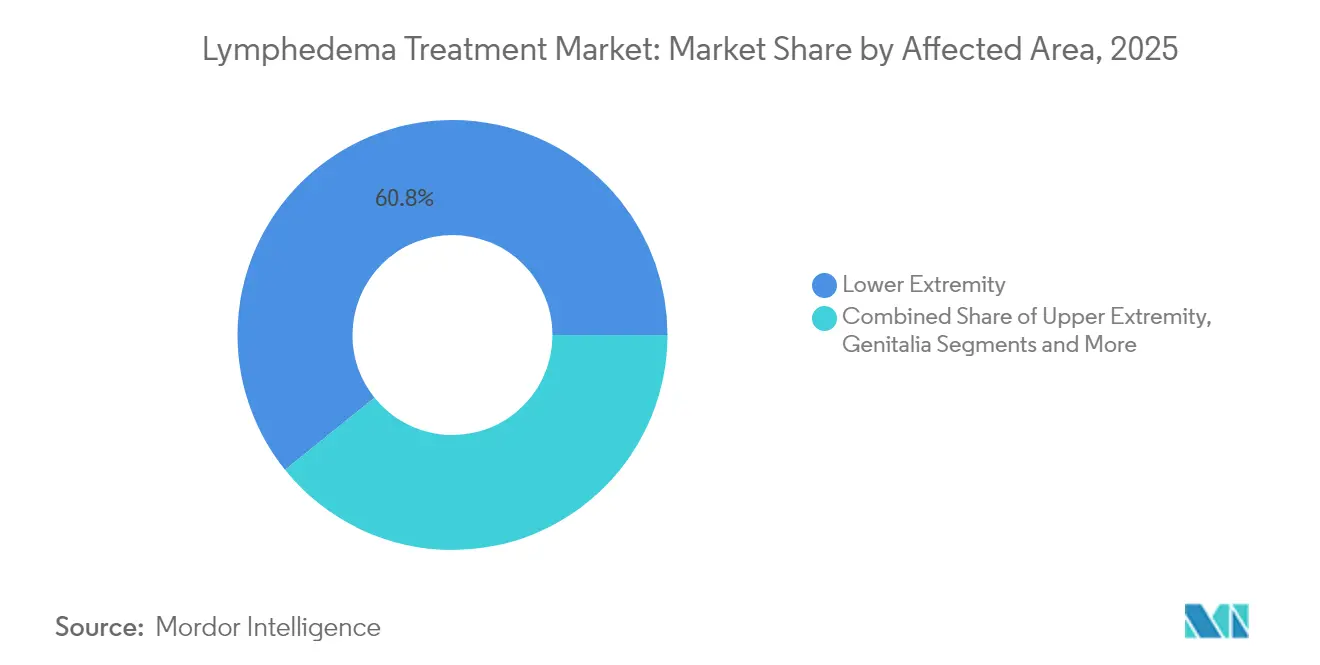

- By affected area, lower extremity conditions held 60.78% of the lymphedema treatment market size in 2025; genitalia lymphedema is poised for an 8.18% CAGR between 2026 and 2031.

- By end user, hospitals commanded 44.85% of 2025 revenues, whereas home-care settings are set to rise at a 6.85% CAGR to 2031.

- By geography, North America captured 41.95% of global value in 2025, but Asia Pacific leads growth with an 8.12% regional CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lymphedema Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Cancer-Related And Chronic-Disease Lymphedema | +2.10% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Growing Adoption Of Compression Therapy Devices | +1.80% | Global, led by North America, expanding to APAC | Medium term (2-4 years) |

| Increasing Patient-Education And Advocacy Programs | +1.20% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Favorable Reimbursement (E.G., 2024 U.S. Medicare Coverage For Garments) | +1.50% | North America, with spillover to other developed markets | Short term (≤ 2 years) |

| IoT-Enabled Smart Compression Systems Boost Adherence | +1.00% | North America & Europe, early adoption phase | Medium term (2-4 years) |

| Preventive Lymphatic Microsurgery (LYMPHA/LVB) Uptake | +0.80% | Global, concentrated in specialized centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cancer-Related and Chronic-Disease Lymphedema

Improved survival after breast, gynecologic, prostate, and melanoma surgeries has enlarged the global cohort at risk of secondary lymphedema. One in three breast cancer patients undergoing axillary dissection eventually develops arm swelling, sometimes years post-treatment.[1]Inspira Health, “Breast Cancer-Related Lymphedema Statistics,” inspirahealthnetwork.org Bioimpedance devices now detect fluid shifts equivalent to 2.4 tablespoons, enabling clinicians to start therapy before irreversible tissue remodeling occurs. Epidemiologic links to obesity and diabetes further widen the patient pool, prompting hospitals to embed lymphatic surveillance inside survivorship programs. Governments are responding: several European cancer plans now mandate routine limb-volume monitoring as a quality metric. Collectively, these dynamics elevate baseline demand across every care setting and position the lymphedema treatment market for sustained long-run expansion.

Growing Adoption of Compression Therapy Devices

Next-generation pneumatic pumps are 40% smaller and 68% lighter than prior models, allowing patients to complete home sessions without mobility restrictions. Tactile Medical’s Nimbl platform exemplifies the shift by pairing Bluetooth-enabled sleeves with a therapy-tracking app that uploads adherence data to clinicians. Veterans Affairs studies show such systems cut limb circumference and boost quality-of-life scores versus legacy pumps. Portable, non-pneumatic wearables such as Koya Medical’s Dayspring further disrupt the segment by letting patients walk during treatment, a step change for working-age users. As Medicare, private U.S. payers, and several EU funds now bundle advanced pumps into benefits packages, compression therapy’s addressable base is widening fast.

Increasing Patient-Education and Advocacy Programs

Passage of the U.S. Lymphedema Treatment Act followed a decade-long grassroots push led by patient groups that demonstrated how untreated swelling fuels cellulitis admissions and multiplies oncology costs. Advocacy has also financed registries that catalog ongoing clinical trials of GLP-1 agonists, ketogenic diets, and topical tacrolimus for lymphatic repair.[2]Lymphatic Education & Research Network, “Clinical Trials Database,” lymphaticnetwork.org Educational modules for primary-care physicians are narrowing diagnostic delays, while webinars and peer coaches help patients master daily self-bandaging. These efforts improve adherence, accelerate referrals to certified therapists, and lift demand for devices and garments worldwide.

Favorable Reimbursement Coverage

On 1 January 2024, Medicare activated 81 HCPCS codes covering day- and night-time garments, bandage kits, and accessories, with allowances for three-day sleeves every six months and two-night garments every two years.[3]Centers for Medicare & Medicaid Services, “Lymphedema Compression Treatment Items Coverage,” cms.gov Private insurers commonly mirror CMS policy, rapidly expanding coverage across commercial lives. The rule obliges physicians to document ICD-10 codes and lymphedema staging, spurring standardized assessment protocols. Although surgical procedures remain under-reimbursed, the garments policy has already eased average annual patient out-of-pocket spending by more than USD 1,000 and stabilized ordering cycles for suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Advanced Devices And Surgeries | -1.20% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Limited Long-Term Clinical Evidence For Novel Therapies | -0.80% | Global, affecting regulatory approvals | Long term (≥ 4 years) |

| Shortage Of Certified Lymphedema Therapists And Fragmented Referral Pathways | -1.50% | Global, most acute in rural and underserved areas | Long term (≥ 4 years) |

| Regulatory Uncertainties For Drug-Based Lymphangiogenic Therapies | -0.60% | Global, concentrated in major pharmaceutical markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Devices and Surgeries

Physiologic surgeries such as lymphovenous anastomosis can cost USD 15,000–30,000, substantially above median household income in many economies. Insurance coverage remains thin: fewer than 12% of U.S. policies reimburse lymphatic bypass or node transfer, and uptake is even lower in Asia’s middle-income countries. Advanced pneumatic pumps retail for USD 4,000–6,000, a figure still prohibitive for many newly diagnosed patients, despite long-term cost-effectiveness. In low-resource settings, surgeons have adapted super-microsurgical techniques using generic instruments to cut costs, but scaling remains limited. Until broader reimbursement or lower-price hardware arrives, cost barriers will temper adoption outside high-income urban centers.

Shortage of Certified Lymphedema Therapists

International standards call for 135 hours of postgraduate training in complete decongestive therapy, yet supply is inadequate: one U.S. county study showed only 1 therapist per 100,000 residents. Fragmented referral pathways mean oncologists, vascular surgeons, and primary-care doctors often fail to identify swelling early, pushing patients to social media for advice. Tele-rehabilitation platforms and wearable sensors promise remote supervision, but licensure rules and payer parity laws lag behind technology. Unless training capacity scales and reimbursement recognizes virtual care, provider scarcity will continue to cap treatment volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Compression Therapy Dominance, Faces Technology Disruption

Compression therapy captured 56.02% of the lymphedema treatment market in 2025, thanks to decades of clinical proof and now solid Medicare backing. IoT-connected pumps and lighter textile designs are rejuvenating the segment and drawing in younger, more active patients. Pharmacologic options, while still nascent, exhibit the fastest 9.25% CAGR on the strength of GLP-1 receptor agonist trials that reduce inflammation and adipose deposition. Surgical interventions remain a specialty niche reserved for refractory cases or prophylactic use during oncologic procedures, constrained by reimbursement gaps and variable surgeon expertise.

Smart compression generates daily adherence data that clinicians fold into electronic records, creating feedback loops to optimize pressure profiles. Non-pneumatic mobility-friendly devices are adding new use cases, such as workplace therapy. Surgery’s role is evolving: several U.S. centers now perform prophylactic lymphatic microsurgery at the time of mastectomy, aiming to cut downstream treatment spend. Topical tacrolimus creams and localized drug delivery systems are in Phase II pipelines, signaling that pharmacology could challenge device hegemony beyond 2030.

By Type: Secondary Lymphedema Drives Market Growth

Secondary lymphedema controlled 81.05% of 2025 revenue as cancer therapies, trauma, infection, and obesity synergistically damage lymphatic pathways. The segment’s scale has anchored payer policy and clinical guidelines, thereby sustaining demand for garments, pumps, and physiologic surgery across all care settings. Primary lymphedema, although rarer, is growing at 8.95% annually as next-generation gene sequencing uncovers mutations in VEGFR3, FOXC2, and PIEZO1, prompting earlier interventions.

Secondary cases benefit from standardized oncology follow-up pathways that route survivors into screening clinics where baseline limb volumes are captured. Conversely, primary patients often endure diagnostic odysseys before referral, delaying therapy initiation and worsening fibrosis. Early-stage detection tools, including near-infrared fluorescence lymphography, are shrinking this gap. Continued emphasis on survivorship quality metrics will keep the lymphedema treatment market size anchored in the secondary segment for the foreseeable future.

By Affected Area: Lower Extremity Complexity Drives Innovation

Lower-limb conditions commanded 60.78% of global spending in 2025, reflecting the biomechanical challenge of pumping fluid upward against gravity. Chronic venous insufficiency and obesity compound leg swelling, increasing reliance on class-III compression stockings and high-pressure pneumatic protocols. The genitalia sub-segment, though only a fraction of cases, is accelerating at 8.18% CAGR as urological oncology programs screen patients more diligently and surgeons adopt lymph-sparing techniques.

Evidence shows modern pumps reduce lower-limb volume by 370 mL versus 83 mL for legacy systems, emphasizing technology’s role in difficult-to-treat legs. Custom garment manufacturers now offer anatomically contoured thigh pieces that improve pressure gradients and comfort. In genitalia lymphedema, interdisciplinary teams combine debulking surgery, compression shorts, and on-demand pneumatic sleeves, a multi-modal approach fueling product innovation within this smaller but high-growth niche.

By End User: Hospital-to-Home Transition Accelerates

Hospitals still held 44.85% of global turnover in 2025 because they diagnose, stage, and launch intensive decongestive therapy. Yet the shift toward value-based care and home infusion analogues is redirecting revenue: the home-care channel is advancing 6.85% per year, making it the fastest-growing outlet for compression pumps and garments. Specialty lymphedema clinics capture complex surgical and rehabilitation cases, filling a middle-ground niche between tertiary hospitals and primary care.

The 2024 CMS rule effectively moved initial compression costs from patients to payers, generating predictable resupply cycles that favor mail-order distributors and tele-rehab models. Portable pumps with cellular modems transmit adherence data, allowing therapists to titrate protocols remotely. Ambulatory surgery centers are expanding as microsurgeons increasingly perform lymphovenous bypass under regional anesthesia, reducing inpatient stays. Collectively, these trends tilt the lymphedema treatment market toward decentralized, patient-centric delivery models.

Geography Analysis

North America contributed 41.95% of global spending in 2025, buoyed by expansive insurance penetration, a dense network of certified therapists, and swift translation of advocacy into policy. The United States anchors the region through Medicare coverage that funds three replacement day sleeves every six months, creating regular purchase cycles for garment vendors. Canada’s single-payer model reimburses intensive decongestive therapy nationwide, although provincial variability still prompts inter-provincial travel. Mexico’s medical-tourism corridors increasingly advertise lymphatic surgeries at one-third U.S. prices, drawing inbound flow from uninsured Americans and Latin American neighbors. Continued FDA approvals of digital pumps, plus Phase II trials of GLP-1 agonists at major cancer centers, keep innovation pipelines vibrant.

Asia Pacific registers the fastest 8.12% CAGR to 2031, spurred by rising cancer incidence, lifestyle diseases, and government investment in surgical microskills. Japan’s microsurgeons now perform more than 400 lymphatic bypasses annually, setting best-practice benchmarks regionwide. China’s reimbursement pilots for advanced compression in Guangdong and Jiangsu provinces hint at future nationwide rollouts. India, already a major garment exporter, is scaling domestic pump production to cut import dependence and pricing. Yet rural therapy access lags; patients in Indonesia or Vietnam often travel 200 km for specialist consultation, a bottleneck that mobile clinics and telemedicine aim to relieve.

Europe maintains steady single-digit growth underpinned by robust public insurance. Germany and the United Kingdom lead engineering refinements in flat-knit garments and pressure-mapping textiles, while Nordic countries pioneer e-referral paths that pair oncology discharge summaries with automatic lymphedema screening invites. Regulatory harmonization under the EU Medical Device Regulation tightens evidence requirements, modestly delaying novel pump launches but boosting clinician confidence. Persistent therapist shortages, especially in Eastern Europe, continue to limit adoption despite universal reimbursement for garments, underscoring workforce as the region’s principal constraint.

Competitive Landscape

The lymphedema treatment market features an oligopoly in compression garments but fragmented competition across pharmacologic and surgical modalities. Legacy European houses such as SIGVARIS GROUP, medi GmbH, and PAUL HARTMANN AG leverage multi-country distribution and hospital tenders to safeguard volume. In the United States, Tactile Medical controls a leading pneumatic share and is migrating customers to its Nimbl platform, which weighs only 2.7 kg and pairs with the Kylee smartphone app for adherence coaching. Disruptors like Koya Medical deploy non-pneumatic wearable sleeves that permit ambulation, targeting active patients frustrated by tethered pumps.

Digital capability is the new battleground. Manufacturers embed LTE chips into sleeves, generating device-as-a-service revenue through cloud dashboards sold to home-health agencies. Analytics engines then flag non-adherence, enabling just-in-time coaching calls that improve outcomes and justify premium monthly fees. Pharmaceutical entrants are watching closely: positive Phase II data on GLP-1 analogues could lure metabolic-disease franchises into lymphatic disorders, bringing larger R&D budgets and direct-to-consumer marketing clout.

Regionally, barriers to entry vary. In Europe, notified-body capacity constraints under MDR slow small-scale innovators, favoring incumbents that can fund extended clinical dossiers. In Asia Pacific, local pump assemblers exploit lower labor costs and government procurement preferences but must still navigate disparate reimbursement codes. Partnerships are proliferating: 2025 has already seen a Japanese-Indian joint venture to co-manufacture flat-knit compression stockings for ASEAN markets. Over the forecast horizon, solution-centric bundles—garment plus pump plus tele-coach—are expected to redefine how value is captured across the care continuum.

Lymphedema Treatment Industry Leaders

Tactile Medical

medi GmbH & Co. KG

3M Company

SIGVARIS GROUP

Huntleigh Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Institute for Advanced Reconstruction opened a 110-adult trial of GLP-1 agonists for lymphedema, with read-out expected in 2026.

- January 2024: Cardinal Health introduced a new chronic-care compression platform aimed at hospital and home health channels.

- September 2024: Koya Medical secured up to USD 30 million in financing from OrbiMed to scale the distribution of its Dayspring wearable compression system. 51.

- October 2024: FDA cleared the full U.S. commercial launch of Tactile Medical’s Nimbl pump under HCPCS E06

Global Lymphedema Treatment Market Report Scope

Lymphedema is a chronic medical condition characterized by the abnormal accumulation of lymphatic fluid, typically in the arms or legs, causing swelling and discomfort. Management typically involves comprehensive care to reduce swelling, which includes compression therapy, manual lymphatic drainage, and other treatments. The lymphedema treatment market is segmented by treatment type, type, affected area, end-user, and geography. By treatment type, the market is segmented into compression therapy, surgery, laser therapy, and other treatment types. Other treatment types include drugs, exercise, and manual lymph. By type, the market is segmented into secondary lymphedema and primary lymphedema. By affected area, the market is segmented into lower extremity, upper extremity, and genitalia. By end user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and other end users. Other end-users include homecare settings and rehabilitation centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across regions. For each segment, the market sizing and forecasts were made on the basis of revenue (USD).

| Compression Therapy |

| Surgery |

| Laser Therapy |

| Pharmacologic Therapy |

| Multi-modal Home Therapy Devices |

| Other Treatment Types |

| Secondary Lymphedema |

| Primary Lymphedema |

| Lower Extremity |

| Upper Extremity |

| Genitalia |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Homecare Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Compression Therapy | |

| Surgery | ||

| Laser Therapy | ||

| Pharmacologic Therapy | ||

| Multi-modal Home Therapy Devices | ||

| Other Treatment Types | ||

| By Type | Secondary Lymphedema | |

| Primary Lymphedema | ||

| By Affected Area | Lower Extremity | |

| Upper Extremity | ||

| Genitalia | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Homecare Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the lymphedema treatment market?

It is valued at USD 1.03 billion in 2026 and is projected to reach USD 1.59 billion by 2031.

Which treatment segment is growing the fastest?

Pharmacologic therapy is expanding at a 9.25% CAGR as GLP-1 agonists and anti-inflammatory agents advance through trials.

How did the 2024 Medicare rule change the market?

CMS coverage for compression garments introduced 81 HCPCS codes, shifting significant out-of-pocket costs onto insurers and stimulating re-order demand cycles.

Why is secondary lymphedema dominant?

Cancer survivorship improvements have increased post-surgical lymphatic injury cases, giving secondary lymphedema 81.05% of global revenue in 2025.

Which region will grow the fastest through 2031?

Asia Pacific is forecast to lead with an 8.12% CAGR due to rising cancer incidence, policy reforms, and expanding microsurgical capacity.

Page last updated on: