Rum Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

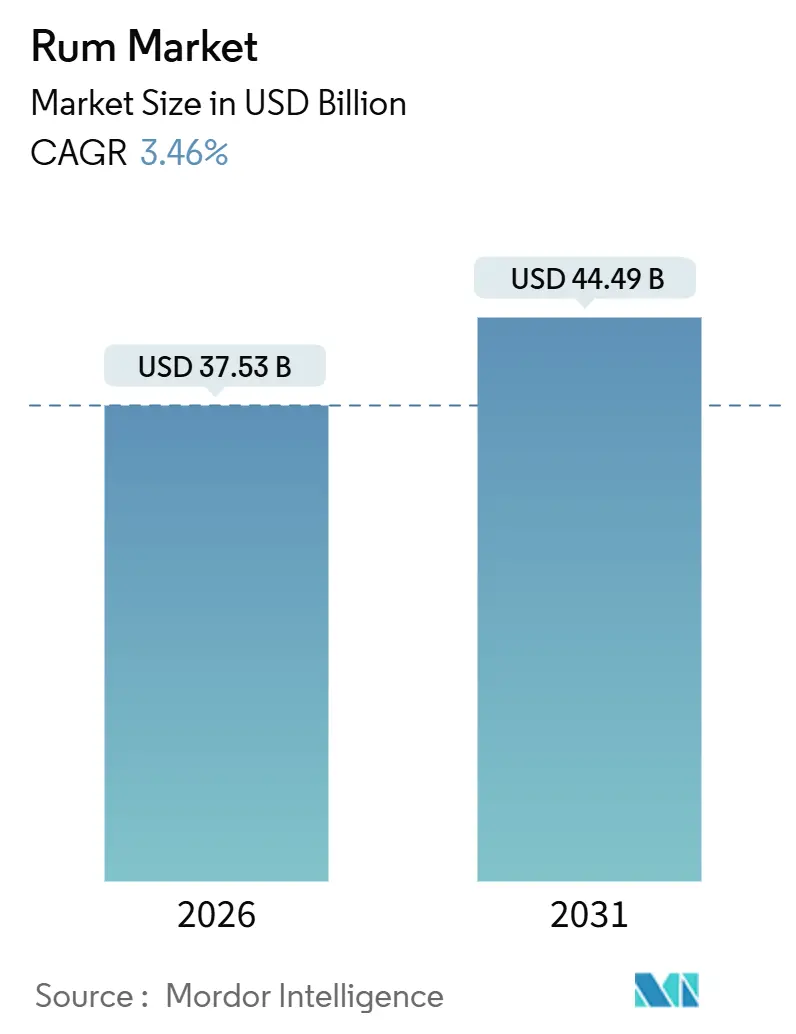

| Market Size (2026) | USD 37.53 Billion |

| Market Size (2031) | USD 44.49 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rum Market Analysis by Mordor Intelligence

The global rum market size was valued at USD 37.53 billion in 2026 and is projected to grow to USD 44.49 billion by 2031, registering a Compound Annual Growth Rate (CAGR) of 3.46%. The market is witnessing a noticeable shift toward premium and aged rum varieties, driven by distillers adopting advanced maturation techniques traditionally used in whiskey and bourbon production. At the same time, flavor innovations are playing a crucial role in keeping entry-level price tiers appealing to younger consumers. Despite facing regulatory challenges in key consumer markets that are slowing growth, the market benefits from several positive factors. These include the rapid recovery of the on-trade segment, the growing popularity of cocktail culture, and an increasing female consumer base, all of which are helping to offset these challenges. Craft producers are gaining traction by focusing on provenance and providing transparent aging statements, which resonate with consumers seeking authenticity in their purchases. Additionally, multinational brand owners are optimizing their portfolios by reducing low-margin Stock Keeping Units (SKUs) and redirecting investments toward higher-margin acquisitions, signaling a strategic emphasis on super-premium price categories.

Key Report Takeaways

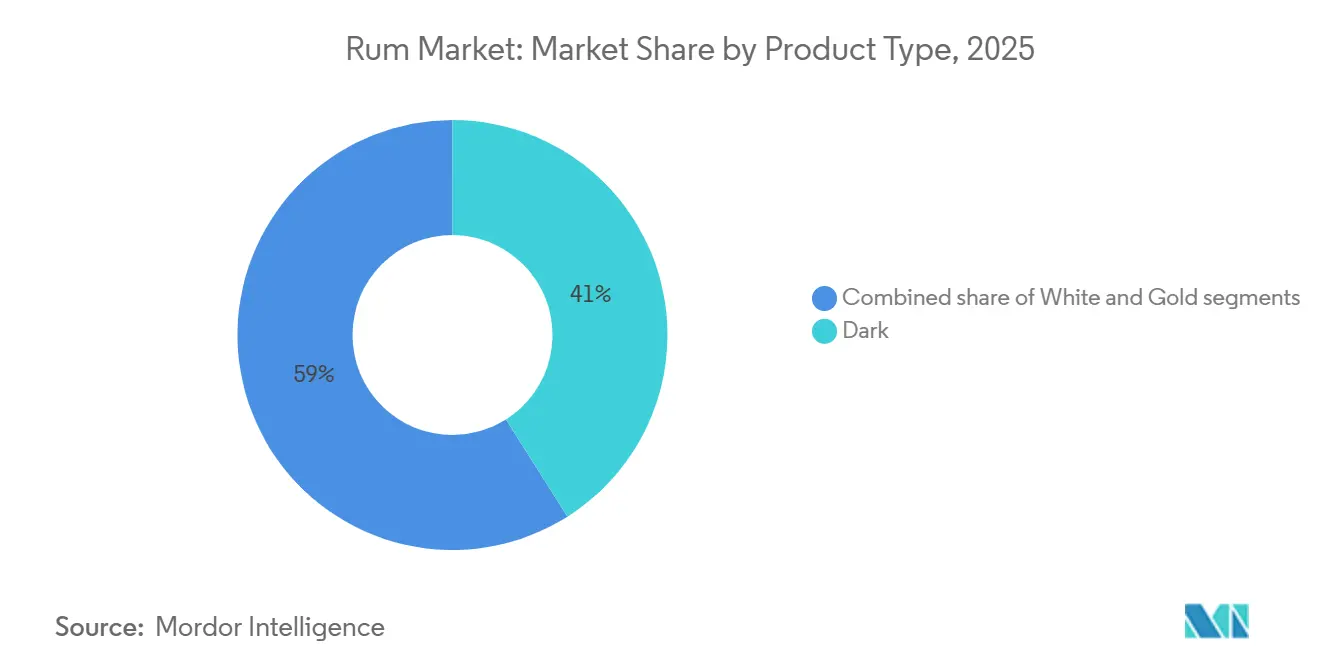

- By product type, dark rum led with 41.02% of global rum market share in 2025; gold rum is forecast to post a 3.81% CAGR to 2031.

- By end user, male consumers represented 61.83% of 2025 demand; the female segment is growing at a 4.13% CAGR to 2031.

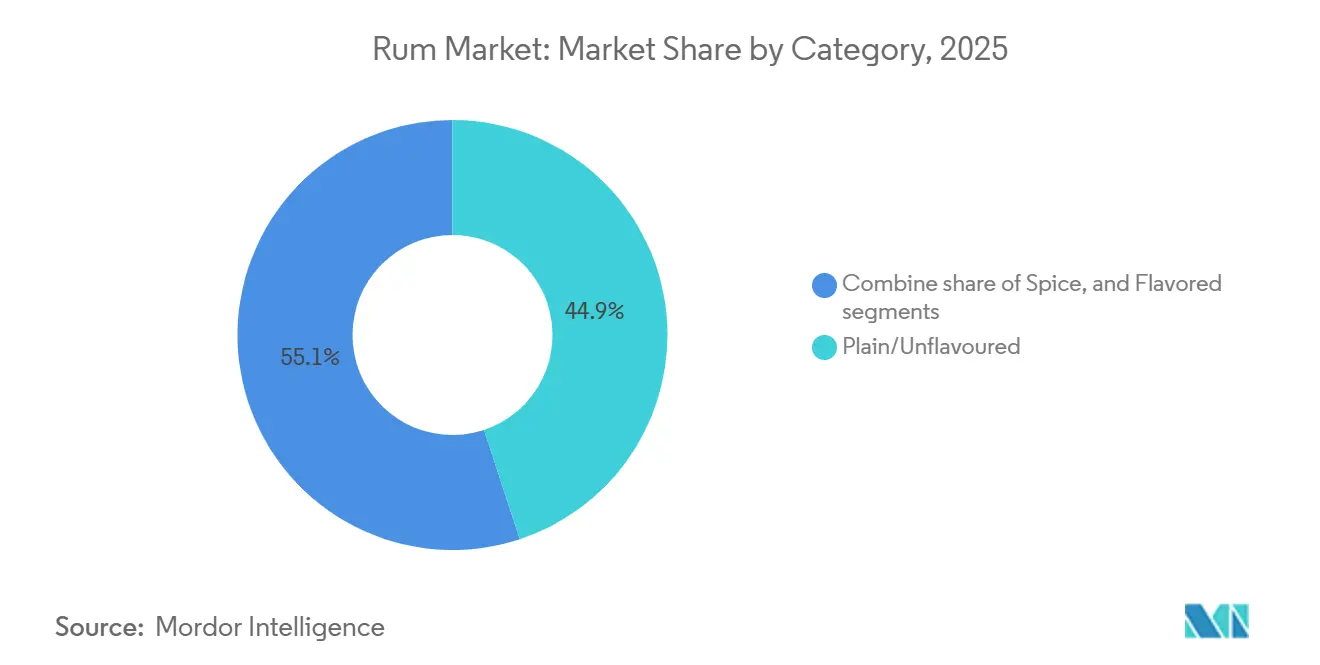

- By category, plain or unflavoured variants held 44.92% of 2025 volume, whereas spiced rum is expanding at a 4.02% CAGR to 2031.

- By distribution channel, the off-trade segment accounted for 77.53% of the global rum market size in 2025, while the on-trade channel is advancing at a 4.92% CAGR through 2031.

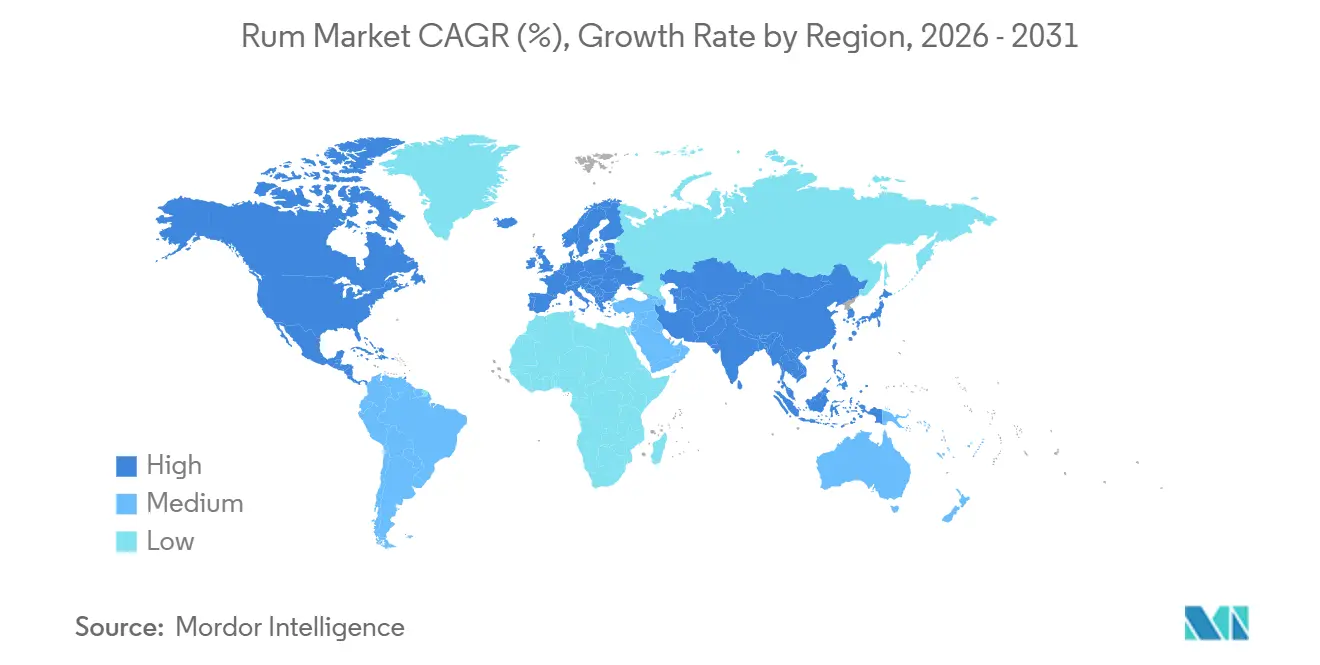

- By geography, Asia-Pacific captured 39.11% of 2025 volume; South America is projected to expand at a 4.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rum Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising premium and aged rum consumption in developed markets | +0.8% | North America and Europe | Long term (≥ 4 years) |

| Growing flavored and spiced rum innovations across major brands | +0.6% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expanding global cocktail and mixology culture in bars and restaurants | +0.7% | Global, led by urban centers in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Increasing craft and artisanal rum distilleries worldwide | +0.5% | North America, Europe, South America | Long term (≥ 4 years) |

| Strong brand storytelling around heritage, origin, and authenticity | +0.4% | Global | Long term (≥ 4 years) |

| Product portfolio expansion by large spirits manufacturers | +0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising premium and aged rum consumption in developed markets

Consumers in the United States, United Kingdom, and Germany are increasingly moving away from traditional white mixing rums in favor of aged rum expressions priced above USD 40 per 750-milliliter bottle. This shift aligns with a broader premiumization trend, similar to the one observed in the whiskey market approximately a decade ago. A significant example is Diageo Public Limited Company’s acquisition of Don Papa in 2024, a Filipino single-island rum priced about 50 percent higher than standard gold variants, appealing to collectors who value its unique origin and craftsmanship. Retail data shows that aged rums with eight-year or twelve-year age statements now account for approximately 18 percent of spirits-aisle facings in premium liquor stores. This reflects strong consumer interest in barrel-finishing techniques influenced by Scotch whisky and bourbon production methods. Craft distilleries, such as Koloa Rum in Hawaii and Devon Rum Company in the United Kingdom, are also capitalizing on this trend by using locally sourced sugarcane or molasses to justify higher price points and drive additional revenue through on-site tasting rooms. While the premiumization trend is expected to persist as younger, affluent consumers increasingly prioritize quality over quantity, potential economic challenges in 2026 may slow the growth of these high-value purchases.

Growing flavored and spiced rum innovations across major brands

Flavor innovation has become a significant factor in driving volume growth, with brands introducing new variants that combine culinary spices, tropical fruits, and savory notes to differentiate themselves in competitive retail markets. In 2024, Captain Morgan launched Sweet Chili Lime, aiming to attract consumers seeking a combination of heat and citrus complexity in ready-to-drink formats. Similarly, Bacardi expanded its Tropical range in 2025 by adding passionfruit and guava options. Cruzan Rum's flavored portfolio, which includes mango, pineapple, and coconut variants, accounted for 34 percent of the brand's total volume in 2025, demonstrating how flavor extensions can revitalize established trademarks. Spiced rums featuring flavors such as vanilla, cinnamon, and ginger have become particularly popular among mixologists creating seasonal cocktails, as these profiles reduce the need for additional modifiers at the bar. However, maintaining authenticity remains a challenge for brands, as those relying on artificial flavorings risk facing criticism from consumers who increasingly demand natural extracts and transparency in ingredient labeling.

Expanding global cocktail and mixology culture in bars and restaurants

The recovery of on-trade venues, including bars, restaurants, and other alcohol-serving establishments, following the pandemic has strengthened rum's position in the craft cocktail segment. Bartenders are revisiting classic cocktails such as the mojito, daiquiri, and piña colada, while also introducing modern variations that emphasize aged and spiced rum varieties. According to Bacardi’s 2025 Cocktail Trends Report, the mojito ranked as the most-ordered rum cocktail globally, followed by the piña colada and daiquiri. The report further highlighted that 42 percent of bartenders are using innovative culinary ingredients, such as miso, smoked paprika, and fermented honey, to craft unique rum-based beverages. This trend is driving higher per-serve pricing, with premium cocktails featuring aged rum typically priced between USD 16 and USD 22 in major metropolitan bars, compared to USD 8 to USD 12 for standard well-spirit options. Additionally, rum tourism is experiencing growth, with distilleries in Barbados, Jamaica, and Martinique offering guided tasting sessions and barrel-aging workshops that enhance brand engagement and create supplementary revenue streams. The compound annual growth rate (CAGR) of 4.92 percent for the on-trade channel reflects this upward trend, although challenges such as workforce shortages and rising ingredient costs continue to impact bar operations.

Increasing craft and artisanal rum distilleries worldwide

Craft rum production has grown beyond its traditional Caribbean origins, with new distilleries emerging in the United States, Europe, and South America. These producers are setting themselves apart through transparent sourcing practices, small-batch aging, and direct-to-consumer business models, which resonate with consumers looking for authenticity and local provenance. Companies such as Newport Craft Brewing in Rhode Island and Middle West Spirits in Ohio have made significant investments in pot-still facilities and barrel-aging warehouses. Their goal is to attract a premium segment of consumers who associate higher quality with locally crafted products. In Colombia, distilleries like Dictador, La Hechicera, and Ron Santísima Trinidad are reviving traditional recipes and enhancing their offerings by aging rum in former bourbon and sherry casks, directly challenging the dominance of Caribbean imports. Favorable regulatory frameworks in certain regions further support this growth. For instance, the Alcohol Wholesaler Registration Scheme in the United Kingdom requires supply chain traceability but does not restrict production scale, allowing micro-distilleries to compete effectively in retail and hospitality channels. However, the segment also faces challenges such as potential market fragmentation, as the increasing variety of products may lead retailers to streamline their offerings and prioritize brands with stronger distribution networks.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent alcohol advertising and promotion restrictions in many countries | -0.5% | Europe, Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| High excise duties and complex alcohol taxation structures | -0.6% | Global, with acute impact in Europe and Asia-Pacific | Medium term (2-4 years) |

| Negative health perceptions around high-strength spirits consumption | -0.4% | Global, led by developed markets in North America and Europe | Long term (≥ 4 years) |

| Supply chain disruptions affecting packaging and logistics reliability | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent alcohol advertising and promotion restrictions in many countries

Regulatory frameworks for alcohol marketing have become more stringent across various jurisdictions, limiting brands' ability to engage with consumers through digital, broadcast, and point-of-sale channels. In Ireland, the Public Health (Alcohol) Act 2018 requires health warnings on labels, restricts advertising near schools and public transport, and prohibits sponsorship of sporting events. These measures have led rum brands to redirect marketing budgets toward trade partnerships and experiential activations [1]Source: Irish Revenue Commissioner, “Excise Duty rates,” revenue.ie. Thailand enforces one of the strictest alcohol advertising regulations globally, banning all broadcast and print promotions and mandating that health warnings cover 30 percent of label space. This significantly hampers brand-building efforts in a market where rum competes with locally produced spirits [2]Source: World Health Organization, “Mental Health, Brain Health and Substance Use,” who.int. In India, direct alcohol advertising is prohibited, pushing brands to rely on surrogate campaigns promoting music festivals, glassware, or mineral water under the same trademark. This approach dilutes brand messaging and complicates attribution. These restrictions disproportionately affect new entrants and craft distilleries, which often lack the resources to invest in alternative marketing channels. As a result, established multinational brands with extensive trade relationships continue to maintain a competitive advantage.

High excise duties and complex alcohol taxation structures

Excise taxation continues to be the most significant cost burden for rum producers and distributors, as the rates vary considerably across different markets and are often subject to sudden increases. These abrupt changes can compress profit margins and discourage long-term investments in the industry. In recent years, countries such as the United Kingdom and Ireland have made adjustments to their duties on spirits, which has influenced pricing strategies and affected retail competitiveness. In India, the Goods and Services Tax (GST) framework, combined with substantial state-level excise duties, has resulted in locally produced rum becoming significantly more expensive for consumers. Similarly, in Australia, the periodic indexing of excise duties to inflation has further reduced affordability for mid-segment consumers [3]Source: Australian Taxation Office, “Excise duty rates for alcohol,” ato.gov.au. These evolving tax policies across various jurisdictions have increased the complexity of compliance for multinational rum producers. Companies are required to manage diverse rate structures, handle regulatory filings, and meet audit requirements across multiple international markets, adding to the operational challenges they face.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aged Expressions Drive Premiumization

Gold rum is projected to grow at a compound annual growth rate (CAGR) of 3.81% through 2031, marking the fastest growth rate among all product types. This growth is primarily driven by producers adopting barrel-finishing techniques and emphasizing age-statement marketing to appeal to consumers who are transitioning from white mixing rums to more premium options. Dark rum, which accounted for 41.02% of the 2025 volume, is strongly supported by Caribbean heritage brands such as Angostura, Mount Gay, and Appleton Estate. These brands focus on traditional pot-still distillation methods and extended aging processes in ex-bourbon casks, which enhance the flavor profile and premium positioning of their products.

White rum, which has traditionally been the foundation for high-volume cocktails like mojitos and daiquiris, is facing increasing margin pressures. This is due to bars and restaurants shifting their focus toward premium offerings that can justify higher per-drink pricing. In line with this trend, Diageo's decision in 2024 to divest Pampero and Cacique, two brands heavily focused on white rum, reflects a strategic move away from low-margin segments. Instead, the company is prioritizing aged rum portfolios that deliver higher gross profit per case, aligning with the growing consumer demand for premium and aged spirits.

By End User: Female Segment Reshapes Marketing and Product Development

The female consumer segment is projected to grow at a compound annual growth rate (CAGR) of 4.13% through 2031, representing the fastest growth rate among end-user categories. This expansion is being driven by brands actively reformulating their products, redesigning packaging, and utilizing social media campaigns to challenge the traditionally masculine image associated with rum. Historically, rum has been linked to naval heritage, Caribbean culture, and high-proof sipping traditions, which have contributed to its strong appeal among male consumers. In 2025, men accounted for 61.83% of the total volume, reflecting this longstanding association.

However, this dominance is gradually diminishing as brands increasingly recognize the revenue potential of female consumers. Women in this segment tend to prioritize attributes such as flavor variety, lower alcohol by volume (ABV), and aesthetically pleasing packaging. To cater to these preferences, brands have introduced products like Captain Morgan's Sweet Chili Lime and Bacardi's Tropical range, launched in 2024 and 2025 respectively. These offerings feature pastel-colored packaging, fruit-forward flavor profiles, and sub-30% ABV formulations, providing an approachable entry point for female drinkers into the rum category.

By Category: Spiced Variants Capture Mixology Momentum

Spiced rum is projected to grow at a compound annual growth rate (CAGR) of 4.02% through 2031, surpassing the growth of plain or unflavored variants, which accounted for 44.92% of the 2025 volume. This growth is primarily driven by the preferences of bartenders and home consumers who are looking for more complex flavor profiles without the higher cost and time commitment associated with aged rum expressions. Spiced rum formulations commonly include ingredients such as vanilla, cinnamon, nutmeg, and ginger. These botanicals are layered onto white or gold rum bases to create versatile spirits that are well-suited for mixing. These products not only enhance classic cocktails but also support seasonal menu rotations, making them a popular choice in both professional and home settings. Captain Morgan Spiced, the leading brand in this category, held an estimated 28% share of global spiced rum volume in 2025. The brand's success can be attributed to its widespread distribution network, consistent flavor profiles, and competitive promotional pricing strategies, which have helped it maintain a dominant position on retail shelves.

Flavored rum, which includes fruit-infused options such as coconut, pineapple, mango, and passionfruit, appeals to consumers who prioritize sweetness and tropical flavor associations over the traditional characteristics of rum. Cruzan's flavored rum portfolio, which features 12 distinct variants, represented a significant portion of the brand's 2025 volume. This diverse range of offerings enables retailers to provide variety to their customers without requiring excessive shelf space for individual stock-keeping units (SKUs). This approach allows retailers to cater to a broader range of consumer preferences while optimizing their inventory management.

By Distribution Channel: On-Trade Rebound Signals Experiential Shift

On-trade venues are expected to grow at a compound annual growth rate (CAGR) of 4.92% through 2031, marking the fastest growth among distribution channels. This growth is driven by bars, restaurants, and hotels reclaiming market share lost during pandemic-related closures. These establishments are focusing on creating experiential formats to enhance customer engagement and justify premium pricing. Off-trade channels accounted for 77.53% of the 2025 volume, reflecting consumers' established habit of purchasing spirits from retail stores for home consumption. However, this dominance is gradually declining as younger consumers increasingly prioritize social experiences and craft cocktails over traditional at-home mixing. Within the off-trade segment, specialty liquor stores stand out by offering knowledgeable staff, curated product selections, and tasting events that replicate the engagement typically found in on-trade venues. In contrast, other off-trade channels, such as supermarkets and convenience stores, primarily compete by focusing on price and promotional strategies.

The recovery of on-trade channels is particularly evident in urban areas, where cocktail bars, rum-focused speakeasies, and tiki lounges have expanded significantly since 2024. These venues provide consumers with multi-sensory experiences that combine craft cocktails, live music, and immersive décor, creating a unique and engaging atmosphere. Bacardi's 2025 Cocktail Trends Report highlights that experiential cocktails, which incorporate elements such as smoke, fire, or tableside preparation, are the fastest-growing serve format in premium on-trade establishments. Rum-based cocktails account for 38% of this category, underscoring their substantial role in driving this trend.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 39.11% of the market volume, making it the largest regional segment. This leadership is driven by the Philippines, where Tanduay Distillers produces over 20 million cases annually and dominates domestic consumption through competitive pricing and extensive retail distribution. India represents the second-largest market in the region, with McDowell's No.1 Rum holding an estimated 40% market share despite regulatory challenges that require separate state-level registrations and excise filings. In China, the rum market remains underdeveloped due to consumer preferences for baijiu and whiskey. However, premiumization trends and the growing adoption of cocktail culture in tier-1 cities such as Shanghai and Beijing are creating opportunities for Caribbean and craft rum brands. Indonesia and Thailand face regulatory challenges, including strict advertising restrictions and high excise duties, which limit market growth and favor locally produced spirits.

South America is projected to grow at a compound annual growth rate (CAGR) of 4.32% through 2031, making it the fastest-growing regional segment. This growth is fueled by Colombia's craft rum resurgence and Brazil's gradual shift from cachaça to premium aged imports. In Colombia, heritage distilleries such as Dictador, La Hechicera, and Ron Santísima Trinidad are revitalizing traditional recipes, aging rums in ex-bourbon and ex-sherry casks, and exporting to North America and Europe at competitive price points against Caribbean brands. In Brazil, the rum market is constrained by cachaça's cultural dominance and regulatory protections. However, urban consumers in cities like São Paulo and Rio de Janeiro are increasingly embracing imported rums as symbols of sophistication and global connectivity.

North America, Europe, and the Middle East and Africa collectively account for the remaining market share, with each region showcasing distinct growth drivers and competitive dynamics. The United States is the largest single-country market, where craft distilleries in states like Hawaii, Rhode Island, and Ohio are challenging Caribbean imports by emphasizing local provenance and transparent aging practices. In Canada, provincial liquor-control boards influence the market by limiting distribution and enforcing minimum pricing, though premiumization trends align with those observed in the United States. In Mexico, rum competes with tequila and mezcal for consumer spending, with coastal resort areas driving on-trade consumption through all-inclusive hotel packages and beach-bar offerings. In Europe, the largest markets include the United Kingdom, Germany, Spain, and France, which exhibit mature demand profiles with growth concentrated in premium aged rums and craft innovations. The United Kingdom's Alcohol Wholesaler Registration Scheme enforces traceability requirements that benefit established brands with strong compliance infrastructure, while craft distilleries such as Devon Rum Company have successfully navigated these regulations to access retail and on-trade channels. The Middle East and Africa face regulatory and cultural barriers, with alcohol sales restricted or prohibited in several countries. However, South Africa, the United Arab Emirates, and Turkey represent pockets of demand where expatriate communities and tourism drive consumption.

Competitive Landscape

The Global Rum Market is moderately concentrated, with major players such as Diageo plc, Pernod Ricard SA, Beam Suntory, Inc., and Davide Campari-Milano N.V. leading prominent brands. Meanwhile, regional producers and craft distilleries are capitalizing on opportunities to target niche segments. Strategic developments reveal a dual approach: multinational companies are divesting low-margin white rum brands while acquiring super-premium assets to diversify and strengthen their portfolios. Craft producers are focusing on local provenance, transparent aging methods, and direct-to-consumer strategies to expand their market presence in developed regions. For instance, Diageo plc's 2024 sale of Pampero and Cacique, followed by its acquisition of Don Papa, underscores its shift from commodity segments to premium brands with higher gross profit margins per case. Similarly, Davide Campari-Milano N.V.'s USD 1.32 billion acquisition of Courvoisier in 2024 demonstrates its strategy to integrate rum and cognac expertise, potentially incorporating barrel-finishing techniques and luxury positioning into its rum portfolio.

New opportunities are emerging in three key areas: low-alcohol-by-volume (ABV) ready-to-drink (RTD) products targeting health-conscious consumers, aged rums with transparent provenance claims competing with whiskey, and sustainability-focused brands utilizing recycled packaging and carbon-neutral production methods. Craft distilleries such as Foursquare in Barbados and Newport Craft Brewing in Rhode Island are taking advantage of these trends by launching single-barrel expressions, offering distillery tours, and engaging consumers through social media platforms.

Although technology adoption in the rum market is limited compared to other spirits categories, some brands are using blockchain for supply chain traceability, augmented reality for label storytelling, and e-commerce platforms for direct sales. Regulatory frameworks, such as the United Kingdom's Alcohol Wholesaler Registration Scheme, which requires digital record-keeping and audit trails, are encouraging smaller players to invest in compliance software and cloud-based inventory systems. Emerging disruptors include Colombian craft distilleries blending traditional recipes with modern marketing strategies, Filipino producers expanding exports beyond domestic markets, and European micro-distilleries targeting premium on-trade accounts with limited-edition releases.

Rum Industry Leaders

Diageo plc

Pernod Ricard SA

Beam Suntory Inc.

Campari Group

Tanduay Distillers Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Himmaleh Spirits, known for brands like Kumaon&I and Bandarful, has launched Neoli Himalayan Rum, positioned as the world’s first white pure single Himalayan Agricole-style rum. Distilled in Kumaon, it sets a new benchmark for terroir-led Indian spirits.

- March 2025: Wray & Nephew has unveiled Wray’s 43, a new white Jamaican rum exclusive to the UK, boasting an ABV of 43%. This launch aims to tap into the surging appetite for flavorful and mix-friendly spirits. This limited edition rum, a blend of unaged Jamaican white rums, tantalizes the palate with notes of rich fruits, charred pineapple, and molasses.

- March 2025: Brugal Rum unveiled the Andrés Brugal Edition 02, marking the second limited release in its ultra-premium rum lineup, with a mere 416 bottles distributed worldwide. Priced at USD 3,000 each, this edition boasts a blend from four single casks aged in American oak, highlighting notes of coconut, vanilla, and subtle spices.

- December 2024: Synergy Flavours has unveiled a new range of rum flavors, catering to both alcoholic beverages and low- or no-alcohol products. This rum lineup features three genuine profiles: white, dark, and spiced rum. Additionally, it offers three cocktail-inspired flavors: Strawberry Daiquiri, Mojito, and Piña Colada.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the rum market as the retail and on-trade sales of spirituous beverages distilled from fermented sugarcane molasses or juice, bottled at a minimum of 37.5% alcohol by volume and classified commercially as white, gold, dark, spiced, or flavored rum across all price tiers.

Scope exclusion: Industrial alcohol, ready-to-drink cocktails, and cane-based spirits not labeled "rum" are omitted.

Segmentation Overview

- By Product Type

- White

- Gold

- Dark

- By End User

- Men

- Women

- By Category

- Plain/Unflavoured

- Flavored

- Spiced

- By Distribution Channel

- On-Trade

- Off-Trade

- Specialty/Liquor Stores

- Others Off-Trade Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed master blenders, duty-free buyers, large distributors, and bartending guild heads in Asia-Pacific, Europe, the Americas, and Africa to verify volume splits, premiumization ratios, and channel margins. They then ran short online surveys among urban consumers to check flavor and occasion preferences that were unclear in secondary data.

Desk Research

We began with publicly available statistics such as UN Comtrade shipment data, World Health Organization per-capita alcohol consumption files, national excise registries, and tourism arrival dashboards because these series reveal underlying demand and trade balances. Company 10-Ks, investor decks, and customs filings supplied average selling prices and brand mix trends, while trade bodies such as the West Indies Rum & Spirits Producers' Association and spirits duty documents helped us pin down regional production. Subscription tools like D&B Hoovers and Dow Jones Factiva enriched our financial checks on leading distillers. This list is illustrative; many further open and paid references were reviewed during data gathering and validation.

Market-Sizing & Forecasting

We apply a top-down apparent-consumption model that starts with country production plus net imports, converts bulk liters to nine-liter cases, and then values the pool using weighted average shelf prices. Supplier roll-ups and sampled price-point × case checks act as bottom-up guardrails. Key variables feeding the model include sugarcane output, legal drinking-age population, real disposable income, tourism nights, and excise-tax shifts, each projected through 2030. A multivariate regression with GDP per capita and premium share as drivers establishes base CAGR, which is stress tested through scenario analysis before finalization.

Data Validation & Update Cycle

Model outputs pass variance screens against historic series, peer ratios, and channel audits; outliers trigger re-contact with experts. Two analyst reviews precede sign-off. Reports refresh every twelve months, and material regulatory or duty changes prompt interim updates so clients receive the latest view.

Credibility Anchor for Rum Market Numbers

Published rum values often diverge because firms select different product mixes, price bases, and update cadences, and they rarely reconcile trade flows with retail depletions.

Key gap drivers include narrower product scope, factory-gate valuation without on-trade mark-ups, lighter primary validation, and less frequent refreshes, which together compress totals reported by several publishers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 36.28 B (2025) | Mordor Intelligence | |

| USD 19.17 B (2025) | Global Consultancy A | Excludes premium craft SKUs and uses manufacturer revenue without channel margins |

| USD 14.63 B (2025) | Trade Journal B | Factory-gate approach, limited regional coverage, five-year refresh cycle |

In sum, by aligning production, trade, and retail pricing and by revisiting assumptions annually, Mordor delivers a transparent, reproducible baseline that decision-makers can trust for planning and investment.

Key Questions Answered in the Report

What is the current value of the global rum market?

The global rum market size stood at USD 37.53 billion in 2026.

How fast is the premium rum segment growing?

Gold and aged expressions are advancing at a 3.81% CAGR through 2031.

Which region is expanding most rapidly?

South America leads with a projected 4.32% CAGR to 2031.

How large is the female consumer base for rum?

Women accounted for roughly 38% of 2025 demand and are growing at a 4.13% CAGR through 2031.

What share does dark rum command?

Dark rum held 41.02% of global rum market share in 2025.

Page last updated on: